Sub-National Institutional Contingencies and Corporate Social Responsibility Performance: Evidence from China

,

,

Abstract

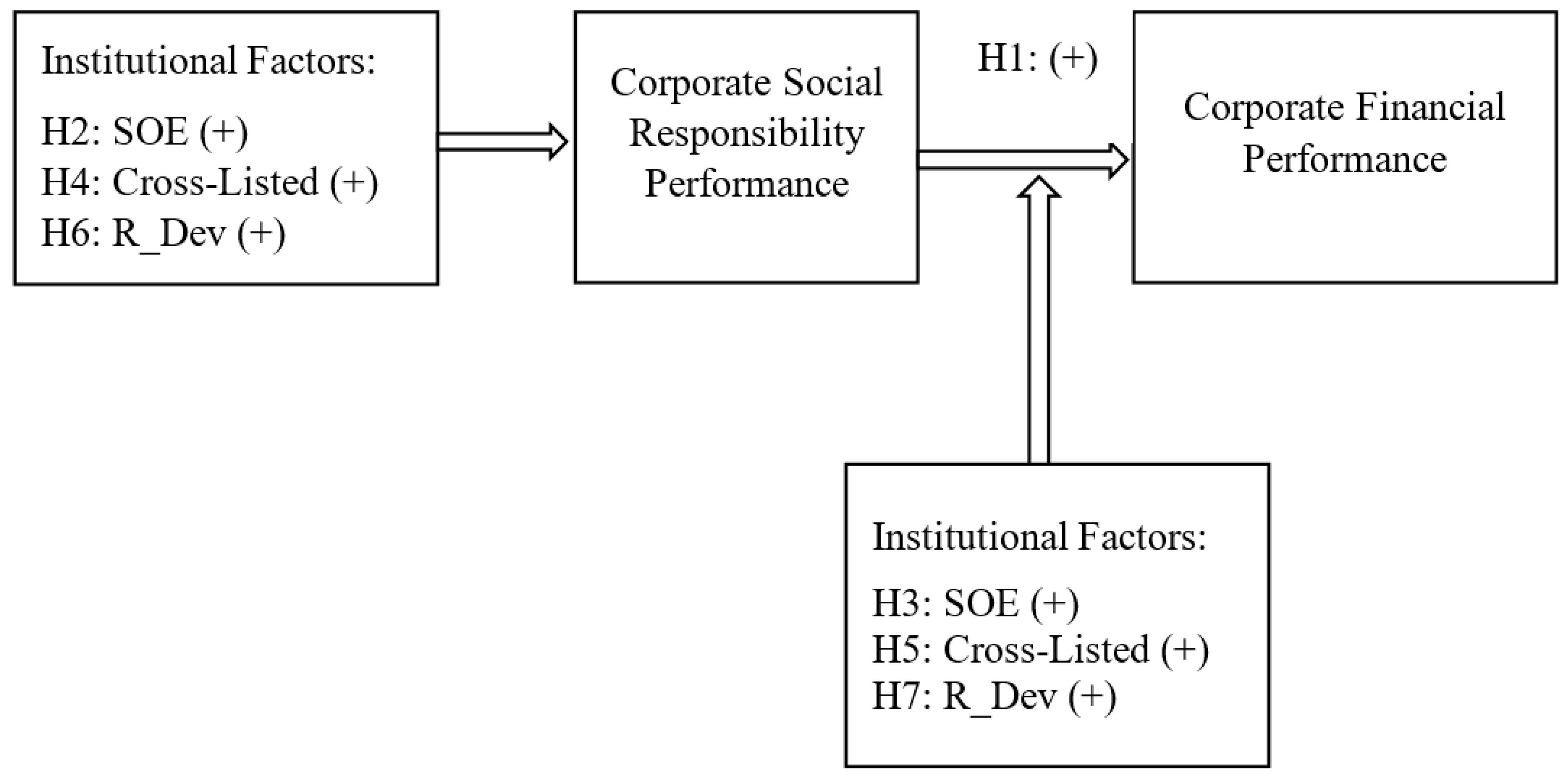

:1. Introduction

2. Institutional Background

3. Literature Review

4. Sample, Variables, Descriptive Statistics, and Methodology

4.1. Data Source and Sample

4.2. Variable Measurement

4.3. Descriptive Statistics and Correlation Matrix

4.4. Theoretical Model

4.5. Empirical Model

5. Results and Discussion

Endogeneity

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Garde-Sanchez, R.; López-Pérez, M.V.; López-Hernández, A.M. Current Trends in Research on Social Responsibility in State-Owned Enterprises: A Review of the Literature from 2000 to 2017. Sustainability 2018, 10, 2403. [Google Scholar] [CrossRef]

- Deegan, C.; Rankin, M.; Tobin, J. An examination of the corporate social and environmental disclosures of BHP from 1983–1997: A test of legitimacy theory. Account. Audit. Account. J. 2002, 15, 312–343. [Google Scholar] [CrossRef]

- Chen, C.F.; Tsai, D. How destination image and evaluative factors affect behavioral intentions? Tour. Manag. 2007, 28, 1115–1122. [Google Scholar] [CrossRef]

- Sial, M.S.; Zheng, C.; Khuong, N.V.; Khan, T.; Usman, M. Does Firm Performance Influence Corporate Social Responsibility Reporting of Chinese Listed Companies? Sustainability 2018, 10, 2217. [Google Scholar] [CrossRef]

- Goranova, M.; Ryan, L.V. Shareholder Activism. J. Manag. 2013, 40, 1230–1268. [Google Scholar] [CrossRef] [Green Version]

- Wu, C.L.; Fang, D.P.; Liao, P.C.; Xue, J.W.; Li, Y.; Wang, T. Perception of corporate social responsibility: The case of Chinese international contractors. J. Clean. Prod. 2015, 107, 185–194. [Google Scholar] [CrossRef]

- Font, X.; Guix, M.; Bonilla-Priego, M.J. Corporate social responsibility in cruising: Using materiality analysis to create shared value. Tour. Manag. 2016, 53, 175–186. [Google Scholar] [CrossRef]

- O’Rourke, A. A new politics of engagement: Shareholder activism for corporate social responsibility. Bus. Strat. Environ. 2003, 12, 227–239. [Google Scholar] [CrossRef]

- Montiel, I. Corporate social responsibility and corporate sustainability—Separate pasts, common futures. Organ. Environ. 2008, 21, 245–269. [Google Scholar] [CrossRef]

- Uhlaner, L.M.; Berent-Braun, M.M.; Jeurissen, R.J.M.; De Wit, G. Beyond Size: Predicting Engagement in Environmental Management Practices of Dutch SMEs. J. Bus. Ethics 2011, 109, 411–429. [Google Scholar] [CrossRef]

- Hasan, I.; Kobeissi, N.; Liu, L.; Wang, H. Corporate Social Responsibility and Firm Financial Performance: The Mediating Role of Productivity. J. Bus. Ethics 2016, 149, 671–688. [Google Scholar] [CrossRef] [Green Version]

- Fernández-Guadaño, J.; Sarria-Pedroza, J.H. Impact of Corporate Social Responsibility on Value Creation from a Stakeholder Perspective. Sustainability 2018, 10, 2062. [Google Scholar] [CrossRef]

- Fassin, Y.; Werner, A.; Van Rossem, A.; Signori, S.; Garriga, E.; von Weltzien Hoivik, H.; Schlierer, H.J. CSR and related terms in SME owner–managers’ mental models in six European countries: National context matters. J. Bus. Ethics 2015, 128, 433–456. [Google Scholar] [CrossRef]

- Doh, J.P.; Guay, T.R. Corporate Social Responsibility, Public Policy, and NGO Activism in Europe and the United States: An Institutional-Stakeholder Perspective. J. Manag. Stud. 2006, 43, 47–73. [Google Scholar] [CrossRef]

- Colombo, S.; Guerci, M.; Miandar, T. What Do Unions and Employers Negotiate Under the Umbrella of Corporate Social Responsibility? Comparative Evidence from the Italian Metal and Chemical Industries. J. Bus. Ethics 2017, 155, 445–462. [Google Scholar] [CrossRef]

- Kang, N.; Moon, J. Institutional complementarity between corporate governance and Corporate Social Responsibility: A comparative institutional analysis of three capitalisms. Socio Econ. Rev. 2011, 10, 85–108. [Google Scholar] [CrossRef]

- Marano, V.; Kostova, T. Unpacking the Institutional Complexity in Adoption of CSR Practices in Multinational Enterprises. J. Manag. Stud. 2016, 53, 28–54. [Google Scholar] [CrossRef]

- Arena, M.; Azzone, G.; Mapelli, F. What drives the evolution of Corporate Social Responsibility strategies? An institutional logics perspective. J. Clean. Prod. 2018, 171, 345–355. [Google Scholar] [CrossRef]

- Arena, M.; Azzone, G.; Mapelli, F. Corporate Social Responsibility strategies in the utilities sector:A comparative study. Sustain. Prod. Consum. 2019, 18, 83–95. [Google Scholar] [CrossRef]

- Mellahi, K.; Frynas, J.G.; Sun, P.; Siegel, D. A Review of the Nonmarket Strategy Literature. J. Manag. 2015, 42, 143–173. [Google Scholar] [CrossRef] [Green Version]

- Frynas, J.G.; Yamahaki, C. Corporate Social Responsibility: An Outline of Key Concepts, Trends, and Theories. In Practising CSR in the Middle East; Palgrave Macmillan: Cham, Switzerland, 2019; pp. 11–37. [Google Scholar]

- Jia, M.; Zhang, Z. The role of corporate donations in Chinese political markets. J. Bus. Ethics 2018, 153, 519–545. [Google Scholar] [CrossRef]

- Marquis, C.; Qian, C. Corporate Social Responsibility Reporting in China: Symbol or Substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef]

- Horak, S.; Restel, K. A Dynamic Typology of Informal Institutions: Learning from the Case of Guanxi. Manag. Organ. Rev. 2016, 12, 525–546. [Google Scholar] [CrossRef]

- Du, J.; Bai, T.; Chen, S. Integrating corporate social and corporate political strategies: Performance implications and institutional contingencies in China. J. Bus. Res. 2019, 98, 299–316. [Google Scholar] [CrossRef]

- Zhao, M. CSR-Based Political Legitimacy Strategy: Managing the State by Doing Good in China and Russia. J. Bus. Ethics 2012, 111, 439–460. [Google Scholar] [CrossRef]

- Tang, P.; Yang, S.; Boehe, D. Ownership and corporate social performance in China: Why geographic remoteness matters. J. Clean. Prod. 2018, 197, 1284–1295. [Google Scholar] [CrossRef]

- Ortas, E.; Álvarez, I.; Jaussaud, J.; Garayar, A.; Fredes, E.O. The impact of institutional and social context on corporate environmental, social and governance performance of companies committed to voluntary corporate social responsibility initiatives. J. Clean. Prod. 2015, 108, 673–684. [Google Scholar] [CrossRef]

- Huang, X.X.; Hu, Z.-P.; Liu, C.S.; Yu, D.J.; Yu, L.F. The relationships between regulatory and customer pressure, green organizational responses, and green innovation performance. J. Clean. Prod. 2016, 112, 3423–3433. [Google Scholar] [CrossRef]

- Giroud, X.; Mueller, H.M. Corporate Governance, Product Market Competition, and Equity Prices. J. Financ. 2011, 66, 563–600. [Google Scholar] [CrossRef] [Green Version]

- Li, Z. Mutual monitoring and corporate governance. J. Bank. Financ. 2014, 45, 255–269. [Google Scholar]

- Li, Z.F. Mutual Monitoring and Agency Problems. SSRN Electron. J. 2014. [Google Scholar] [CrossRef]

- Coles, J.L.; Li, Z.; Wang, A.Y. Industry tournament incentives. Rev. Financ. Stud. 2017, 31, 1418–1459. [Google Scholar] [CrossRef]

- Li, Z.F.; Lin, S.; Sun, S.; Tucker, A. Risk-adjusted inside debt. Glob. Financ. J. 2018, 35, 12–42. [Google Scholar] [CrossRef] [Green Version]

- Core, J.; Guay, W. The use of equity grants to manage optimal equity incentive levels. J. Account. Econ. 1999, 28, 151–184. [Google Scholar] [CrossRef] [Green Version]

- Sun, S.L.; Peng, M.W.; Shi, W.S.; Shi, W. Sub-National Institutional Contingencies, Network Positions, and IJV Partner Selection. J. Manag. Stud. 2012, 49, 1221–1245. [Google Scholar]

- Khan, F.U.; Zhang, J.; Usman, M.; Badulescu, A.; Sial, M.S. Ownership Reduction in State-Owned Enterprises and Corporate Social Responsibility: Perspective from Secondary Privatization in China. Sustainability 2019, 11, 1008. [Google Scholar] [CrossRef]

- Tse, E. The China Strategy: Harnessing the Power of the World’s Fastest-Growing Economy; Basic Books: New York, NY, USA, 2010. [Google Scholar]

- He, L.; Fang, J. Subnational institutional contingencies and executive pay dispersion. Asia Pac. J. Manag. 2015, 33, 371–410. [Google Scholar] [CrossRef]

- Davis, G.F. New Directions in Corporate Governance. Annu. Rev. Sociol. 2005, 31, 143–162. [Google Scholar] [CrossRef]

- North, D. Institutions, Institutional Change and Economic Performance; Cambridge University Press: Cambridge, MA, USA, 1990. [Google Scholar]

- Scott, W.R. Institutions and Organizations; Sage Publications: Thousand Oak, CA, USA, 1995. [Google Scholar]

- Mike, W.P.; Sunny, L.S.; Brian, P.; Hao, C.; Peng, M.W.; Sun, S.L.; Pinkham, B.; Chen, H. The Institution-Based View as a Third Leg for a Strategy Tripod. Acad. Manag. Perspect. 2009, 23, 63–81. [Google Scholar]

- Westphal, J.D.; Gulati, R.; Shortell, S.M. Customization or Conformity? An Institutional and Network Perspective on the Content and Consequences of TQM Adoption. Adm. Sci. Q. 1997, 42, 366–394. [Google Scholar] [CrossRef]

- Chen, D.; Li, S.; Xiao, J.Z.; Zou, H. The effect of government quality on corporate cash holdings. J. Corp. Financ. 2014, 27, 384–400. [Google Scholar] [CrossRef] [Green Version]

- Xu, E.; Yang, H.; Quan, J.M.; Lu, Y. Organizational slack and corporate social performance: Empirical evidence from China’s public firms. Asia Pac. J. Manag. 2015, 32, 181–198. [Google Scholar] [CrossRef]

- Filatotchev, I.; Nakajima, C. Corporate Governance, Responsible Managerial Behavior, and Corporate Social Responsibility: Organizational Efficiency Versus Organizational Legitimacy? Acad. Manag. Perspect. 2014, 28, 289–306. [Google Scholar] [CrossRef]

- Moratis, L. Consequences of Collaborative Governance in CSR: An Empirical Illustration of Strategic Responses to Institutional Pluralism and Some Theoretical Implications. Bus. Soc. Rev. 2016, 121, 415–446. [Google Scholar] [CrossRef]

- Bowen, H.R.; Johnson, F.E. Social Responsibilities of the Businessman, With a Commentary by Ernest Johnson, F.; University of Iowa Press: New York, NY, USA, 1953. [Google Scholar]

- Li, Z.; Minor, D.; Wang, J.; Yu, C. A Learning Curve of the Market: Chasing Alpha of Socially Responsible Firms. SSRN Electron. J. 2019, 38. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3224796 (accessed on 15 September 2019). [CrossRef]

- Lu, W.; Ye, M.; Chau, K.; Flanagan, R. The paradoxical nexus between corporate social responsibility and sustainable financial performance: Evidence from the international construction business. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 844–852. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate Social Responsibility: A Theory of the Firm Perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Lundgren, T. A microeconomic model of corporate social responsibility. Metroeconomica 2011, 62, 69–95. [Google Scholar] [CrossRef]

- Lee, J.; Graves, S.B.; Waddock, S. Doing good does not preclude doing well: Corporate responsibility and financial performance. Soc. Responsib. J. 2018, 14, 764–781. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Beyond dichotomy: The curvilinear relationship between social responsibility and financial performance. Strat. Manag. J. 2006, 27, 1101–1122. [Google Scholar] [CrossRef]

- Simpson, W.G.; Kohers, T. The Link Between Corporate Social and Financial Performance: Evidence from the Banking Industry. J. Bus. Ethics 2002, 35, 97–109. [Google Scholar] [CrossRef]

- Busch, T.; Friede, G. The Robustness of the Corporate Social and Financial Performance Relation: A Second-Order Meta-Analysis. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 583–608. [Google Scholar] [CrossRef] [Green Version]

- Aguilera, R.V.; Rupp, D.E.; Williams, C.A.; Ganapathi, J. Putting the S back in corporate social responsibility: A multilevel theory of social change in organizations. Acad. Manag. Rev. 2007, 32, 836–863. [Google Scholar] [CrossRef]

- Story, J.; Neves, P. When corporate social responsibility (CSR) increases performance: Exploring the role of intrinsic and extrinsic CSR attribution. Bus. Ethics A Eur. Rev. 2015, 24, 111–124. [Google Scholar] [CrossRef]

- Rettab, B.; Mellahi, K. Practising CSR in the Middle East; Springer: Berlin/Heidelberg, Germany, 2019. [Google Scholar]

- Welford, R. Corporate social responsibility in Europe and Asia: Critical elements and best practice. J. Corp. Citizsh. 2004, 13, 31–47. [Google Scholar]

- Khan, M.K.; He, Y.; Akram, U.; Sarwar, S. Financing and monitoring in an emerging economy: Can investment efficiency be increased? China Econ. Rev. 2017, 45, 62–77. [Google Scholar] [CrossRef]

- Lazzarini, S.G. Strategizing by the government: Can industrial policy create firm-level competitive advantage? Strateg. Manag. J. 2015, 36, 97–112. [Google Scholar] [CrossRef]

- Musacchio, A.; Lazzarini, S.G.; Aguilera, R.V. New Varieties of State Capitalism: Strategic and Governance Implications. Acad. Manag. Perspect. 2015, 29, 115–131. [Google Scholar] [CrossRef] [Green Version]

- Fan, J.P.; Wong, T.; Zhang, T. Politically connected CEOs, corporate governance, and Post-IPO performance of China’s newly partially privatized firms. J. Financ. Econ. 2007, 84, 330–357. [Google Scholar] [CrossRef]

- Hu, F.; Pan, X.; Tian, G. Does CEO pay dispersion matter in an emerging market? Evidence from China’s listed firms. Pac. Basin Financ. J. 2013, 24, 235–255. [Google Scholar] [CrossRef]

- Firth, M.; Fung, P.M.; Rui, O.M. How ownership and corporate governance influence chief executive pay in China’s listed firms. J. Bus. Res. 2007, 60, 776–785. [Google Scholar] [CrossRef]

- Shen, W.; Lin, C. Firm Profitability, State Ownership, and Top Management Turnover at the Listed Firms in China: A Behavioral Perspective. Corp. Gov. Int. Rev. 2009, 17, 443–456. [Google Scholar] [CrossRef] [Green Version]

- Campbell, J.L. Why would corporations behave in socially responsible ways? an institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Hung, M.Y.; Wong, T.; Zhang, T. Political considerations in the decision of Chinese SOEs to list in Hong Kong. J. Account. Econ. 2012, 53, 435–449. [Google Scholar] [CrossRef]

- Li, D.; Lin, H.; Yang, Y.-W. Does the stakeholders—Corporate social responsibility (CSR) relationship exist in emerging countries? Evidence from China. Soc. Responsib. J. 2016, 12, 147–166. [Google Scholar] [CrossRef]

- Zheng, H.; Zhang, Y. Do SOEs outperform private enterprises in CSR? Evidence from China. Chin. Manag. Stud. 2016, 10, 435–457. [Google Scholar] [CrossRef]

- Li, S.; Song, X.; Wu, H. Political Connection, Ownership Structure, and Corporate Philanthropy in China: A Strategic-Political Perspective. J. Bus. Ethics 2014, 129, 399–411. [Google Scholar] [CrossRef]

- Zhang, C. Political connections and corporate environmental responsibility: Adopting or escaping? Energy Econ. 2017, 68, 539–547. [Google Scholar] [CrossRef]

- Chen, J.; Ezzamel, M.; Cai, Z. Managerial power theory, tournament theory, and executive pay in China. J. Corp. Financ. 2011, 17, 1176–1199. [Google Scholar] [CrossRef]

- Liu, X.; Zhang, C. Corporate governance, social responsibility information disclosure, and enterprise value in China. J. Clean. Prod. 2017, 142, 1075–1084. [Google Scholar] [CrossRef]

- Smith, N.; Smith, V.; Verner, M. Do women in top management affect firm performance? A panel study of 2,500 Danish firms. Int. J. Prod. Perform. Manag. 2006, 55, 569–593. [Google Scholar] [CrossRef]

- Li, Q.; Luo, W.; Wang, Y.; Wu, L. Firm performance, corporate ownership, and corporate social responsibility disclosure in China. Bus. Ethics A Eur. Rev. 2013, 22, 159–173. [Google Scholar] [CrossRef]

- Shi, H.; Zhang, X.; Zhou, J. Cross-listing and CSR performance: Evidence from AH shares. Front. Bus. Res. China 2018, 12, 11. [Google Scholar] [CrossRef]

- Ferris, S.P.; Kim, K.A.; Noronha, G. The Effect of Crosslisting on Corporate Governance: A Review of the International Evidence. Corp. Gov. Int. Rev. 2009, 17, 338–352. [Google Scholar] [CrossRef]

- Boubakri, N.; El Ghoul, S.; Wang, H.; Guedhami, O.; Kwok, C.C. Cross-listing and corporate social responsibility. J. Corp. Financ. 2016, 41, 123–138. [Google Scholar] [CrossRef]

- Bell, R.G.; Filatotchev, I.; A Rasheed, A. The liability of foreignness in capital markets: Sources and remedies. J. Int. Bus. Stud. 2011, 43, 107–122. [Google Scholar] [CrossRef] [Green Version]

- Liu, G. Do Cross-Listed Firms Report Better Social Responsibility Performance? In Proceedings of the SHS Web of Conferences, Kuching Sarawak, Malaysia, 14 February 2017. 05003. [Google Scholar]

- Koh, P.S.; Qian, C.; Wang, H. Firm litigation risk and the insurance value of corporate social performance. Strateg. Manag. J. 2014, 35, 1464–1482. [Google Scholar] [CrossRef]

- Hong, H.; Liskovich, I. Crime, Punishment and the Halo Effect of Corporate Social Responsibility; National Bureau of Economic Research: Cambridge, MA, USA, 2015. [Google Scholar]

- Sun, Q.; Tong, W.H.; Wu, Y. Overseas listing as a policy tool: Evidence from China’s H-shares. J. Bank. Financ. 2013, 37, 1460–1474. [Google Scholar] [CrossRef]

- Del Mar Miras-Rodríguez, M.; Carrasco-Gallego, A.; Escobar-Pérez, B. Are socially responsible behaviors paid off equally? A cross-cultural analysis. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 237–256. [Google Scholar] [CrossRef]

- Chan, C.M.; Makino, S.; Isobe, T. Does subnational region matter? Foreign affiliate performance in the United states and China. Strat. Manag. J. 2010, 31, 1226–1243. [Google Scholar] [CrossRef]

- Fan, G.; Wang, X.; Zhu, H. NERI Index of Marketization of China’s Provinces 2011 Report; Economic Science Press: Beijing, China, 2011. [Google Scholar]

- Cordeiro, J.J.; He, L.; Conyon, M.; Shaw, T.S. Informativeness of performance measures and Chinese executive compensation. Asia Pac. J. Manag. 2013, 30, 1031–1058. [Google Scholar] [CrossRef]

- Marquis, C.; Glynn, M.A.; Davis, G.F. Community isomorphism and corporate social action. Acad. Manag. Rev. 2007, 32, 925–945. [Google Scholar] [CrossRef]

- Davis, J.C.; Henderson, J.V. The agglomeration of headquarters. Reg. Sci. Urban Econ. 2008, 38, 445–460. [Google Scholar] [CrossRef]

- Husted, B.W.; Jamali, D.; Saffar, W. Near and dear? The role of location in CSR engagement. Strateg. Manag. J. 2016, 37, 2050–2070. [Google Scholar] [CrossRef]

- Klier, T.; Testa, W. Location trends of large company headquarters during the 1990s. Econ. Perspect. -Fed. Reserve Bank Chic. 2002, 26, 12–26. [Google Scholar]

- Conyon, M.J.; He, L. CEO turnover in China: The role of market-based and accounting performance measures. Eur. J. Financ. 2014, 20, 657–680. [Google Scholar] [CrossRef]

- Bebchuk, L.A.; Cremers, K.M.; Peyer, U.C. The CEO pay slice. J. Financ. Econ. 2011, 102, 199–221. [Google Scholar] [CrossRef]

- Barnea, A.; Rubin, A. Corporate Social Responsibility as a Conflict Between Shareholders. J. Bus. Ethics 2010, 97, 71–86. [Google Scholar] [CrossRef]

- Wu, W.F.; Johan, S.A.; Rui, O.M. Institutional Investors, Political Connections, and the Incidence of Regulatory Enforcement Against Corporate Fraud. J. Bus. Ethics 2016, 134, 709–726. [Google Scholar] [CrossRef]

- Hung, M.; Shi, J.; Wang, Y. Mandatory CSR Disclosure and Information Asymmetry: Evidence from a Quasi-natural Experiment in China. In Proceedings of the Asian Finance Conference 2013. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2206877 (accessed on 15 September 2019). [CrossRef]

- McGuinness, P.B.; Vieito, J.P.; Wang, M. The role of board gender and foreign ownership in the CSR performance of Chinese listed firms. J. Corp. Financ. 2017, 42, 75–99. [Google Scholar] [CrossRef] [Green Version]

- Luo, X.; Wang, D.; Zhang, J. Whose Call to Answer: Institutional Complexity and Firms’ CSR Reporting. Acad. Manag. J. 2017, 60, 321–344. [Google Scholar] [CrossRef]

- Lau, C.M.; Lu, Y.; Liang, Q. Corporate Social Responsibility in China: A Corporate Governance Approach. J. Bus. Ethics 2016, 136, 73–87. [Google Scholar] [CrossRef]

- Harjoto, M.A.; Jo, H. Corporate Governance and CSR Nexus. J. Bus. Ethics 2011, 100, 45–67. [Google Scholar] [CrossRef]

- Borghesi, R.; Houston, J.F.; Naranjo, A. What Motivates Corporate Managers to Make Socially Responsible Investments? SSRN Electron. J. 2012, 26, 164–181. [Google Scholar] [CrossRef]

- Jiraporn, P.; Chintrakarn, P. How do powerful CEOs view corporate social responsibility (CSR)? An empirical note. Econ. Lett. 2013, 119, 344–347. [Google Scholar] [CrossRef]

- Li, F.; Li, T.; Minor, D. CEO power, corporate social responsibility, and firm value: A test of agency theory. Int. J. Manag. Financ. 2016, 12, 611–628. [Google Scholar] [CrossRef]

- McCarthy, S.; Oliver, B.; Song, S. Corporate social responsibility and CEO confidence. J. Bank. Financ. 2017, 75, 280–291. [Google Scholar] [CrossRef] [Green Version]

- Cai, Y.; Jo, H.; Pan, C. Vice or Virtue? The Impact of Corporate Social Responsibility on Executive Compensation. J. Bus. Ethics 2011, 104, 159–173. [Google Scholar] [CrossRef]

- Fernández-Gago, R.; Cabeza-García, L.; Nieto, M. Independent directors’ background and CSR disclosure. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 991–1001. [Google Scholar] [CrossRef]

- Yu, L.; Wang, D.; Wang, Q. The Effect of Independent Director Reputation Incentives on Corporate Social Responsibility: Evidence from China. Sustainability 2018, 10, 3302. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Cuadrado-Ballesteros, B.; Sepulveda, C. Does media pressure moderate CSR disclosures by external directors? Manag. Decis. 2014, 52, 1014–1045. [Google Scholar] [CrossRef]

- Rao, K.K.; Tilt, C.A.; Lester, L.H. Corporate governance and environmental reporting: An Australian study. Corp. Gov. Int. J. Bus. Soc. 2012, 12, 143–163. [Google Scholar]

- Esa, E.; Ghazali, N.A.M. Corporate social responsibility and corporate governance in Malaysian government-linked companies. Corp. Gov. Int. J. Bus. Soc. 2012, 12, 292–305. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Description |

|---|---|

| CSR_Rating | CSR rating score is weighted average ranging from 0 to 100 issued by Rankings (RKS). |

| SOE (state-owned enterprise) | A dummy variable that equals 1 if the state or central government is the controlling owner and 0 if it is a non-SOE. |

| Cross-listed | A dummy variable that equals 1 if the firm is cross-listed Hong Kong Stock Exchange and 0 if it is non-cross-listed. |

| R_Dev (regional development) | A dummy variable that equals 1 if the firm’s head office is located in more developed regions of China, and 0 otherwise. |

| B_Size | The number of directors on the board. |

| Ind_Dir | The proportion of independent/outside directors on the board. |

| CEO duality | A dummy variable that equals 1 if the CEO is working as a chairperson and otherwise 0. |

| B_Share | The percentage of shares held by a firm board of directors. |

| Size | The log of total sales. |

| Growth | Change in firms total assets. |

| F_Lev | The ratio of total debt to the total asset. |

| F_Age | The number of years the firm has been listed on the stock exchange. |

| TobinQ | The industry-adjusted Tobin’s Q ratio. |

| BTMA | The book-to-market ratio. A ratio of a publicly traded company’s book value to its market value. |

| Variable | Mean | Standard Deviation | Min | Max |

|---|---|---|---|---|

| CSR_Rating | 28.71 | 19.44 | 0 | 90.84 |

| SOE | 0.46 | 0.50 | 0 | 1 |

| Cross-listed | 0.03 | 0.18 | 0 | 1 |

| R_Dev | 0.25 | 0.43 | 0 | 1 |

| B_Size | 10.27 | 2.64 | 5 | 27 |

| Ind_Dir | 0.38 | 0.07 | 0.17 | 0.8 |

| CEO duality | 0.25 | 0.43 | 0 | 1 |

| B_Share | 0.1 | 0.18 | 0 | 0.89 |

| Size | 3.06 | 0.07 | 2.20 | 3.36 |

| Growth | 0.71 | 2.08 | −45.72 | 64.69 |

| F_Leverage | 0.55 | 2.37 | −0.19 | 142.72 |

| F_Age | 10.19 | 6.35 | 0 | 26 |

| TobinQ | 5.40 | 372.16 | 0.03 | 50,939.53 |

| BTMA | 0.92 | 1.07 | 0 | 36.72 |

| Sub Sample | N | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| STATE = 1 | 5051 | 31.73 | 21.75 | −13.05 | 90.83 |

| STATE = 0 | 5758 | 26.06 | 16.72 | −15.20 | 90.32 |

| Cross-Listed = 1 | 367 | 49.68 | 23.20 | −8.33 | 90.25 |

| Cross-Listed = 0 | 10,419 | 27.95 | 18.86 | −15.20 | 90.84 |

| R_Dev = 1 | 4815 | 30.02 | 19.37 | −15.20 | 89.12 |

| R_Dev = 0 | 5994 | 27.66 | 19.44 | −13.95 | 90.32 |

| Variables | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. CSR_ rating | 1.00 | ||||||||||||||

| 2. SOE | 0.15 * | 1.00 | |||||||||||||

| 3. Cross-listed | 0.20 * | 0.15 * | 1.00 | ||||||||||||

| 4. R_Dev | 0.06 * | −0.15 * | 0.04 * | 1.00 | |||||||||||

| 5. B_Size | 0.05 * | 0.22 * | 0.11 * | −0.04 * | 1.00 | ||||||||||

| 6. Ind_Dir | 0.01 | −0.10 * | 0.03 * | 0.02 * | −0.08 * | 1.00 | |||||||||

| 7. CEO duality | −0.08 * | −0.30 * | −0.05 * | 0.09 * | −0.10 * | 0.07 * | 1.00 | ||||||||

| 8. SOE | 0.15 * | 1.00 * | 0.15 * | −0.15 * | 0.22 * | −0.10 * | −0.29 * | 1.00 | |||||||

| 9. B_Share | −0.07 * | −0.49 * | −0.09 * | 0.14 * | −0.17 * | 0.11 * | 0.26 * | −0.49 * | 1.00 | ||||||

| 10. Size | 0.36 * | 0.35 * | 0.31 * | 0.01 | 0.21 * | 0.02 * | −0.16 * | 0.35 * | −0.26 * | 1.00 | |||||

| 11. Growth | 0.03 * | −0.05 * | −0.02 * | −0.00 | 0.05 * | −0.01 | 0.05 * | −0.05 * | 0.06 * | 0.02 | 1.00 | ||||

| 12. F_Leverage | −0.03 * | 0.00 | 0.00 | −0.03 * | 0.07 * | −0.01 | −0.04 * | 0.00 | −0.15 * | 0.11 * | −0.12 * | 1.00 | |||

| 13. F_Age | 0.03 * | 0.39 * | 0.02 * | −0.15 * | 0.14 * | −0.06 * | −0.22 * | 0.39 * | −0.55 * | 0.19 * | −0.05 * | 0.07 * | 1.00 | ||

| 14. TobinQ | −0.03 * | −0.01 | −0.00 | −0.01 | −0.03 * | 0.01 | 0.00 | −0.01 | 0.01 | −0.12 * | 0.02 * | 0.57 * | 0.00 | 1.00 | |

| 15. BTMA | 0.17 * | 0.26 * | 0.15 * | −0.02 * | 0.12 * | −0.01 | −0.11 * | 0.26 * | −0.24 * | 0.51 * | −0.02 * | 0.03 * | 0.21 * | −0.01 | 1.00 |

| Subnational Institutional Contingencies and CSR Performance | CSR and Performance | |||||

|---|---|---|---|---|---|---|

| Performance | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

| CSR_ Rating | -------- | -------- | -------- | -------- | 0.06 *** (4.85) | 0.06 *** (4.55) |

| SOE | 0.97 ** (2.24) | -------- | -------- | 0.871 ** (2.01) | -------- | 0.13** (2.21) |

| Cross-listed | -------- | 8.93 *** (9.22) | -------- | 8.80 *** (9.07) | -------- | 4.03 *** (2.99) |

| R_Dev | -------- | -------- | 0.91 ** (2.39) | 0.75 ** (1.96) | -------- | 0.25 *** (2.47) |

| B_Size | −0.12 * (−1.75) | −0.13 ** (−2.01) | −0.12 * (−1.73) | −0.13 ** (−1.99) | −0.20 ** (−2.24) | −0.21 ** (−2.32) |

| Ind_Dir | 5.80 ** (2.49) | 5.11 ** (2.20) | 5.89 ** (2.53) | 5.20 ** (2.24) | 3.50 ** (1.99) | 3.24 ** (1.89) |

| CEO duality | −0.35 (−0.87) | −0.45 (−1.10) | −0.40 (−0.99) | −0.49 (−1.20) | −1.27 ** (−2.28) | −1.32 ** (−2.35) |

| B_Share | 3.18 *** (2.72) | 3.22 *** (2.77) | 2.98 ** (2.54) | 3.05 *** (2.61) | −2.32 (−1.44) | 2.30 (−1.42) |

| Size | 124.77 *** (42.08) | 118.06 *** (38.90) | 123.82 *** (41.41) | 117.37 *** (38.42) | −59.71 *** (−13.67) | −62.44 *** (−13.96) |

| Growth | 0.05 (0.60) | 0.09 (1.03) | 0.06 (0.68) | 0.10 (1.09) | 1.51 *** (12.42) | 1.52 *** (12.53) |

| F_Leverage | −2.26 *** (−7.21) | −2.24 *** (−7.16) | −2.25 *** (−7.18) | −2.23 *** (−7.13) | 13.02 *** (31.43) | 13.01 *** (31.39) |

| F_Age | −0.11 *** (−3.10) | −0.09 *** (−2.63) | −0.11 *** (−2.98) | −0.09 ** (−2.55) | −0.06 (−1.23) | −0.05 (−1.03) |

| TobinQ | 0.03 *** (4.85) | 0.03 *** (4.56) | 0.03 *** (4.84) | 0.03 *** (4.55) | -------- | -------- |

| BTMA | −1.63 *** (−7.40) | −1.68 *** (−7.67) | −1.59 *** (−7.21) | −1.65 *** (−7.50) | −0.14 (−0.47) | −0.16 (−0.54) |

| Constants | −355.71 *** (−39.58) | −335.05 *** (−36.40) | 353.10 *** (−39.01) | −333.18 *** (−36.00) | 178.05 *** (13.56) | 186.45 *** (13.87) |

| Year dummies | Included | Included | Included | Included | Included | Included |

| Industry dummies | Included | Included | Included | Included | Included | Included |

| R2 | 0.243 | 0.249 | 0.243 | 0.249 | 0.118 | 0.119 |

| SOE | Non-SOE | Cross-Listed | Non-Cross-Listed | R_Dev | Less-R_Dev | |

|---|---|---|---|---|---|---|

| Performance | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

| CSR_Rating | 0.01 *** (7.30) | 0.08 *** (2.96) | 0.01* (1.64) | 0.06 *** (4.61) | 0.01 *** (6.88) | 0.17 *** (8.45) |

| SOE | -------- | -------- | 0.02 (0.14) | 0.14 (0.23) | 0.19 ** (2.37) | 0.88 (1.01) |

| Cross-listed | 0.60 *** (6.61) | 6.72 (1.34) | -------- | -------- | 0.61 *** (3.80) | 3.87* (1.77) |

| R_Dev | 0.11 ** (2.23) | −0.29 (−0.28) | 0.11 (0.92) | 0.20 (0.37) | -------- | -------- |

| B_Size | 0.00 (0.25) | −0.49 *** (−2.66) | 0.02 (1.37) | −0.23 ** (−2.38) | 0.02 (1.38) | −0.29 ** (−2.23) |

| Ind_Dir | 0.77 *** (2.60) | 2.11 (0.36) | 0.79 (1.33) | 3.20 (0.96) | 0.75 * (1.86) | 2.72 (0.56) |

| CEO duality | −0.15 ** (−2.28) | −2.07 ** (−2.29) | 0.12 (0.81) | −1.36 ** (−2.35) | 0.13 ** (1.97) | −2.34 (−2.67) |

| B_Share | 5.98 *** (5.21) | −4.18* (−1.76) | −0.18 (−0.19) | −2.29 (−1.39) | 0.23 (1.23) | 0.29 (0.11) |

| Size | −12.41*** (−29.52) | −97.60 *** (−11.71) | −5.61 *** (−6.92) | −64.63 *** (−13.85) | −11.74*** (−20.09) | −92.99 *** (−14.30) |

| Growth | −0.01 (−0.84) | 2.63 *** (12.03) | 0.17 ** (2.37) | 1.54 *** (12.39) | −0.10 *** (−5.55) | 1.72 *** (10.28) |

| F_Leverage | 0.60 *** (6.90) | 14.21 *** (24.08) | −0.82 ** (−2.31) | 13.04 *** (30.88) | 1.07 *** (27.46) | 60.97 *** (58.25) |

| F_Age | 0.00 (0.58) | −0.05 (−0.58) | 0.02 * (1.79) | −0.04 (−0.82) | 0.01* (1.76) | −0.44 *** (−6.13) |

| BTMA | −0.33 *** (−14.16) | 0.55 (0.66) | −0.10 ** (−2.26) | −0.16 (−0.47) | −0.57 *** (−14.03) | −3.31 *** (−7.38) |

| Constants | 39.59 *** (31.40) | 295.22 *** (11.76) | 19.48 *** (7.79) | 193.14 *** (13.76) | 37.44 *** (21.08) | 259.65 *** (13.29) |

| Year dummies | Included | Included | Included | Included | Included | Included |

| Industry dummies | Included | Included | Included | Included | Included | Included |

| R2 | 0.405 | 0.142 | 0.516 | 0.119 | 0.381 | 0.401 |

| PSM | |||

|---|---|---|---|

| SOE | Cross-Listed | R_Dev | |

| CSR_Rating | Model 1 | Model 2 | Model 3 |

| SOE | 0.38 *** (2.93) | -------- | -------- |

| Cross-listed | -------- | 7.96 *** (6.04) | -------- |

| R_Dev | -------- | -------- | 0.68 *** (2.62) |

| B_Size | −0.03 (−0.48) | −0.26* (−1.61) | −0.01 (−0.10) |

| Ind_Dir | 3.59 (1.31) | −1.03 (−0.18) | −0.14 (−0.06) |

| CEO duality | −0.50 (−0.82) | 0.63 (0.60) | −0.54 (−1.35) |

| B_Share | 21.61 ** (2.47) | 2.79 (0.95) | 1.66 (1.48) |

| Size | 152.25 *** (40.85) | 135.36 *** (15.01) | 129.52 *** (37.40) |

| Growth | 0.00 (0.03) | −0.07 (−0.25) | 0.04 (0.35) |

| F_Leverage | −2.18 *** (−7.47) | −7.58 *** (−5.49) | −2.71 *** (−8.18) |

| F_Age | 0.05 (1.35) | −0.08 (−0.86) | −0.17 *** (−4.71) |

| TobinQ | 0.91 *** (9.18) | 0.15 *** (2.62) | 0.96 *** (9.29) |

| BTMA | −1.96 *** (−8.94) | −1.55 *** (−3.19) | −1.22 *** (−4.89) |

| Constants | −441.18 *** (−38.75) | −380.20 *** (−13.38) | −367.64 *** (−34.52) |

| Year dummies | Included | Included | Included |

| Industry dummies | Included | Included | Included |

| R2 | 0.273 | 0.378 | 0.276 |

| PSM | ||||||

|---|---|---|---|---|---|---|

| SOE | Non-SOE | Cross-Listed | Non-Cross-Listed | R_Dev | Less-R_Dev | |

| Performance | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

| CSR_Rating | 0.03 ** (2.65) | 0.02* (1.90) | 0.01* (1.64) | 0.04 *** (3.19) | 0.01 *** (6.92) | 0.00 *** (2.83) |

| SOE | -------- | -------- | −0.02 (−0.14) | −1.20* (−1.94) | −0.20 ** (−2.52) | −0.12 *** (−2.67) |

| Cross-listed | 0.65 ** (2.61) | 0.25 ** (1.98) | -------- | -------- | 0.61 *** (3.79) | 0.29 ** (2.05) |

| R_Dev | 0.15* (1.65) | 0.27 (0.98) | 0.11 (0.92) | −0.29 (−0.58) | -------- | -------- |

| B_Size | 0.03 (1.54) | 0.01 ** (2.22) | 0.02 (1.37) | −0.23 *** (−2.61) | 0.02 (1.42) | 0.01 ** (2.02) |

| Ind_Dir | 0.89 (1.53) | −1.30 (−0.49) | 0.79 (1.33) | −1.39 (−0.46) | 0.69* (1.70) | 0.04 (0.18) |

| CEO duality | 0.14 (0.85) | −0.67 (−1.39) | 0.12 (0.81) | −0.66 (−1.29) | 0.13* (1.90) | 0.04 (0.89) |

| B_Share | 0.29 (1.42) | 0.59 *** (3.11) | −0.18 (−0.19) | −3.75 *** (−2.69) | 0.19 (1.02) | 0.59 *** (5.11) |

| Size | −10.62*** (−16.12) | −6.15 *** (−14.15) | −5.61 *** (−6.92) | −46.98 *** (−9.23) | −11.82 *** (−20.10) | −6.15 *** (−16.25) |

| Growth | 0.19 ** (2.27) | 0.12 (1.29) | 0.17 ** (2.37) | 0.140 (1.09) | −0.09 *** (−5.59) | 0.04 *** (3.55) |

| F_Leverage | 1.10 *** (25.27) | −1.17 *** (−8.23) | −0.82 ** (−2.31) | 1.85 *** (2.84) | 1.07 *** (27.37) | −1.17 *** (−10.63) |

| F_Age | 0.02* (1.69) | 0.15 *** (2.90) | 0.02* (1.79) | 0.14 *** (2.92) | 0.01* (1.77) | 0.01 *** (3.52) |

| BTMA | −0.65 *** (−12.46) | −0.44 *** (−14.13) | −0.10 ** (−2.26) | 0.12 (0.44) | −0.56 *** (−13.86) | −0.44 *** (−17.23) |

| Constants | 35.65 *** (20.10) | 20.99 *** (15.16) | 19.48 *** (7.79) | 152.11 *** (9.60) | 37.68 *** (21.09) | 21.97 *** (19.36) |

| Year Dummies | Included | Included | Included | Included | Included | Included |

| Industry Dummies | Included | Included | Included | Included | Included | Included |

| R2 | -------- | -------- | -------- | 0.107 | 0.381 | 0.503 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ali, S.; Zhang, J.; Usman, M.; Khan, F.U.; Ikram, A.; Anwar, B. Sub-National Institutional Contingencies and Corporate Social Responsibility Performance: Evidence from China. Sustainability 2019, 11, 5478. https://doi.org/10.3390/su11195478

Ali S, Zhang J, Usman M, Khan FU, Ikram A, Anwar B. Sub-National Institutional Contingencies and Corporate Social Responsibility Performance: Evidence from China. Sustainability. 2019; 11(19):5478. https://doi.org/10.3390/su11195478

Chicago/Turabian StyleAli, Shahid, Junrui Zhang, Muhammad Usman, Farman Ullah Khan, Amir Ikram, and Bilal Anwar. 2019. "Sub-National Institutional Contingencies and Corporate Social Responsibility Performance: Evidence from China" Sustainability 11, no. 19: 5478. https://doi.org/10.3390/su11195478