3.2. Carbon Emissions Calculation of the Case Building

(1) Carbon Emissions in Stage 1

In this stage, carbon emissions mainly consist of direct carbon emissions from materials production and indirect carbon emissions from energy consumption. For a specific building case, the carbon emissions calculation is based on the consumption of building materials and the corresponding carbon emission factors. The equation is as follows:

where

is the carbon emission factor of material

i, which is provided in the Chinese life cycle database (CLCD) developed by IKE Environmental Technology CO., Ltd (IKE, Chengdu, China) [

40];

is the quantity of material

i;

is the carbon emission of transportation, mainly related with the quantity of material, transportation distance, and fuel type, which can be expressed as:

where

is the carbon emissions factor of transportation with material

i (kg/t·km), which is provided by the Chinese life cycle database (CLCD) developed by IKE Co. Ltd [

40], and

is transportation distance of material

i.

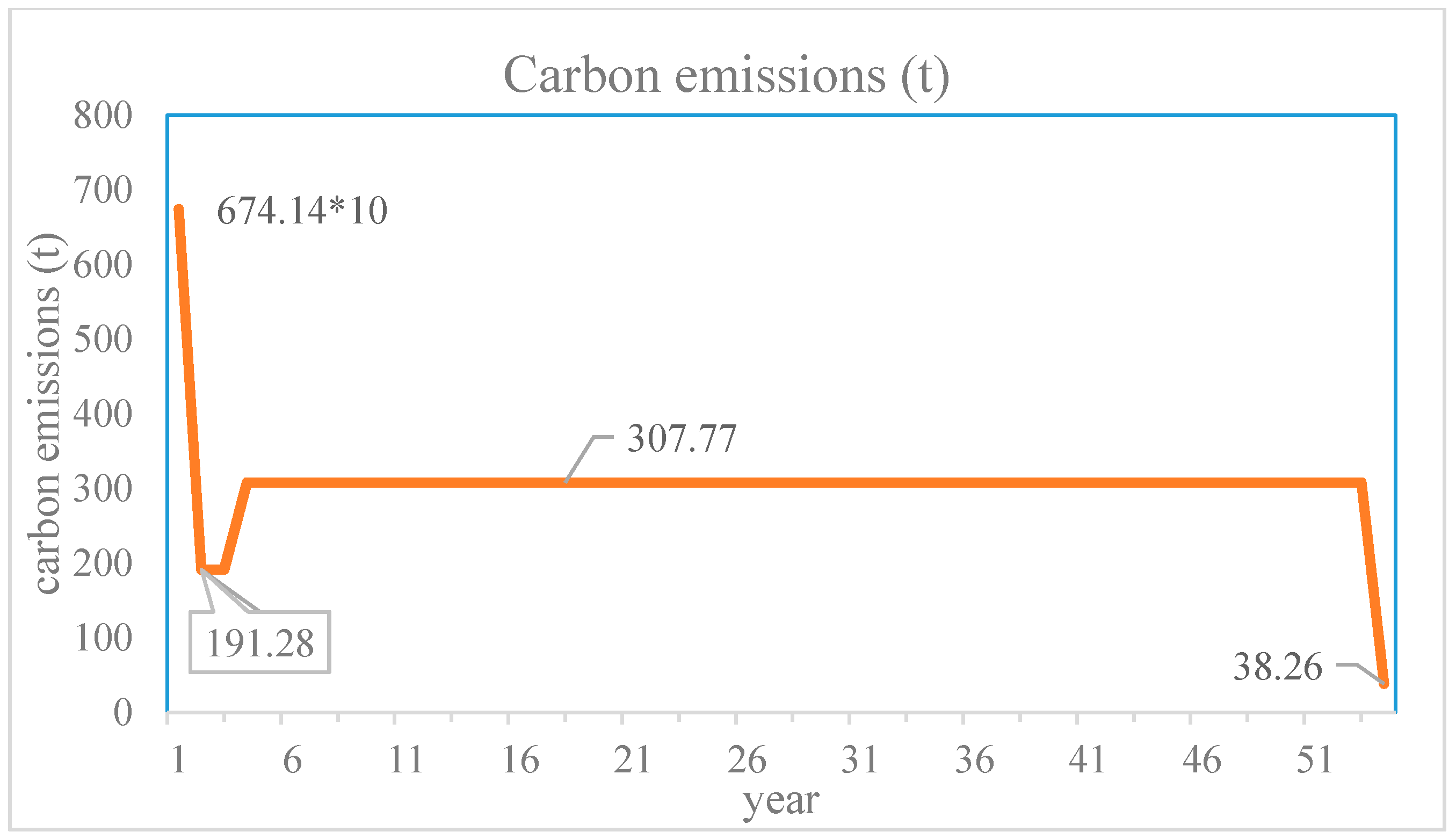

According to the bill of materials, transportation mode, and distance, the carbon emission in building material production and transportation stages can be acquired. Since hundreds of types of building materials are involved in the building, it is difficult to quantify them all. Therefore, by consulting the bill of quantities, the consumption data of three types of main building materials (concrete, reinforcement bars, and blocks) was collected. Their consumption is 5831.02 m

3, 881.64 t, and 2110.28 m

3, respectively. Investigating the results indicate that the materials are transported from the suburbs by diesel truck (the carbon emission factor of diesel trucks is 1983 kg CO

2-e/10

4·t·km). Due to the inability to specifically measure the transport distance, this paper assumes that the transportation distance is 15 km. The carbon emission in this stage can be calculated by Equation (4) and Equation (5). The calculation results of carbon emissions in Stage 1 are shown in

Table 2.

(2) Carbon Emissions in Stage 2

Building construction stage means the construction process after building materials transported to the construction site. Carbon emissions of the construction stage can be calculated according to construction technology, as shown in Equation (6):

where

is total construction of construction method

i, and

is carbon emission factor of the construction method

i. Construction technology normally includes earthwork excavation, earthwork leveling, crane handling, horizontal transportation, lighting, and concrete pouring.

Table 3 shows the carbon emission factors of different construction technologies.

According to the machine-team table, the carbon emission in the construction stage can be calculated by the construction technology, as shown in

Table 3.

(3) Carbon Emissions in Stage 3

Carbon emissions of the operational phase are mainly converted from energy and resource consumption used during the building’s life, such as lighting, heating, air conditioning, ventilation, and others:

where

is the carbon emission factor of energy

i,

is the quantity of energy

i consumption, and

a is the building design service life of 50 years.

The main resource consumed in the building operational stage is tap water; 1 m

3 tap water will create 0.213 kg of carbon emissions [

27]. It is worth noting that the carbon emissions of the operational phase are not only related to building energy consumption, but also related to the energy structure of the area where the building located. The Intergovernmental Panel on Climate Change (IPCC) [

41] pointed out that the carbon emissions from fossil fuel combustion can be estimated based on the total amount of used energy and their average carbon content. Carbon emission factors of different fossil energy types are shown in

Table 4.

Electricity, as a secondary energy, is closely related to the local energy structure. The higher the proportion of thermal power, the greater the unit power of carbon emissions. The

2010 China Regional Power Grid Baseline Emission Factor released by China’s National Development and Reform Commission climate division announced the carbon emission factors of the regional power grid [

42], as seen in

Table 5.

In the operational stage, carbon emissions are related to many factors, such as human behavior, methods of energy consumption, and so on. Since the case building is a newly-constructed building, there is no related data. Thus, in this study, the average value of Xiamen City by searching the statistical yearbook is adopted; the annual water consumption per capita is 54.3 t, and the electricity and natural gas consumption is 1163.93 kWh and 17.39 m

3, respectively. According to the design drawing of residential architecture, there are 78 households in total. Assuming that every household is a typical Chinese family of three—in this case, a residential building—the annual water consumption, electricity, and natural gas consumption are 12,706.2 t, 272,359.62 kWh, and 4069.26 m

3, respectively. In addition, the two elevators equipped in the building also consume some energy. The nominal power of each elevator is 18 kW. According to the calculation method of elevator energy consumption presented by Al-Sharif, the annual energy consumed by the two elevators is 32,850 kWh. The detailed calculation process can be found in the

supplementary material. According to the carbon emission conversion factors of different types of energy, the annual carbon emissions in the operational stage can be calculated. Since natural gas is measured by m

3, and the carbon emission factor for natural gas is 2.36 kgCO

2-e/kg, it is necessary to convert the volume of natural gas to calculate the carbon emission.

Table 6 shows the annual carbon emissions in the operational stage.

(4) Carbon Emissions in Stage 4

The demolition stage refers to the demolition process of the site, site preparation, and solid waste shipping and handling, etc. Carbon emissions in this stage are mainly indirect carbon emissions caused by energy consumption, such as construction machines and equipment operation, transportation energy, and disposal of solid wastes. The equation is as follows:

Since the building is still in operation, there is no relevant demolition data. According to Japanese AIJ-LCA research [

43], the carbon emission in the demolition stage is about 10% of the construction stage. Therefore, the carbon emission in the demolition stage is about 38.26 t CO

2-e.

(5) Total Carbon Emissions of the Case Building during its Life Cycle

The calculation model of the total life cycle carbon emissions of the case building can be determined as follows:

The carbon emissions in the four stages have been calculated, then the total carbon emissions can be obtained.

Table 7 summarized the carbon emissions in the case building’s different life cycle stages.

3.3. Determining Life Cycle Carbon Cost

Supposing that the carbon cost in the building materials production and transportation stage occurred in the initial year (2000), this carbon cost is the present value. In addition, the building’s project time limit is two years, assuming that the annual carbon emission in the construction stage is similar, so the related carbon cost in this stage can be calculated.

Figure 1 shows the quantity of carbon emissions and their occurrence time.

Due to the scarcity of research on unit pollution damage costs of carbon emission, in this study, EIB’s research results are adopted [

30,

31]. In addition, it is noted that the selection of a suitable discount rate is crucial in LCC analysis. Kishk et al. gave a review of various criteria proposed in the literature for the selection of the discount rate [

44]. For example, the discount rate may be established as the highest interest an organization expects to pay to borrow the money needed for a project; or defined as the rate of return that could be earned from the best alternative use of the funds devoted for the project under consideration. Nowadays, there is no consensus regarding the selection of the most suitable discount rate. In the UK, a discount rate of 8% is usually used, whilst in the USA the rate is 6%, in Germany, 3%, and in Switzerland, 2% [

45]. Rebitezer [

46] proposed to use a 5% discount rate and employ a sensitivity analysis, varying the rate from 0% to 10%, to test the robustness of the results. Research indicated that a high discount rate will tend to favor options with low capital cost and high recurring cost, whilst a low discount rate will have the opposite effect [

47]. That is to say, the higher the discount rate, the less important are the long term costs.

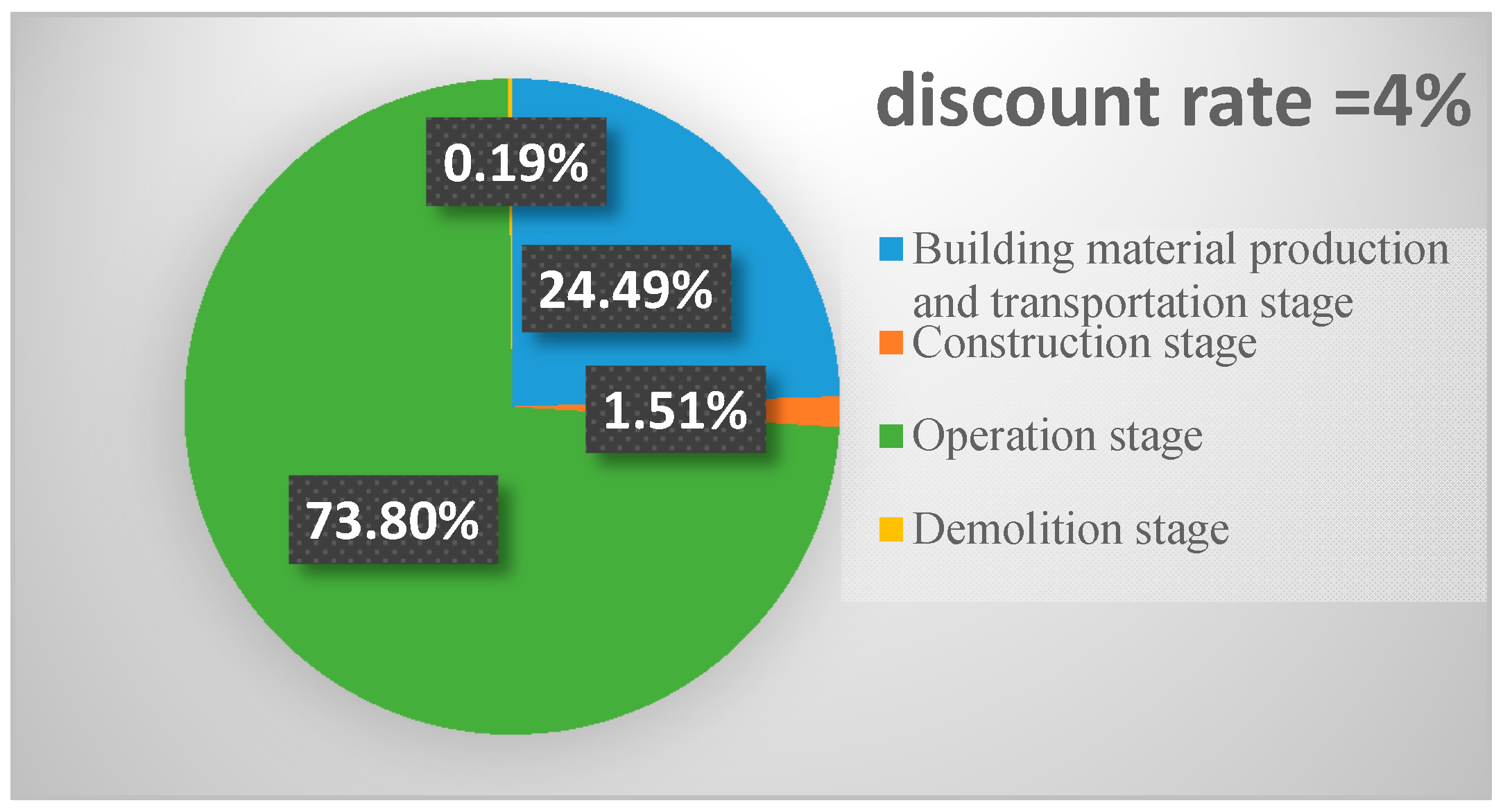

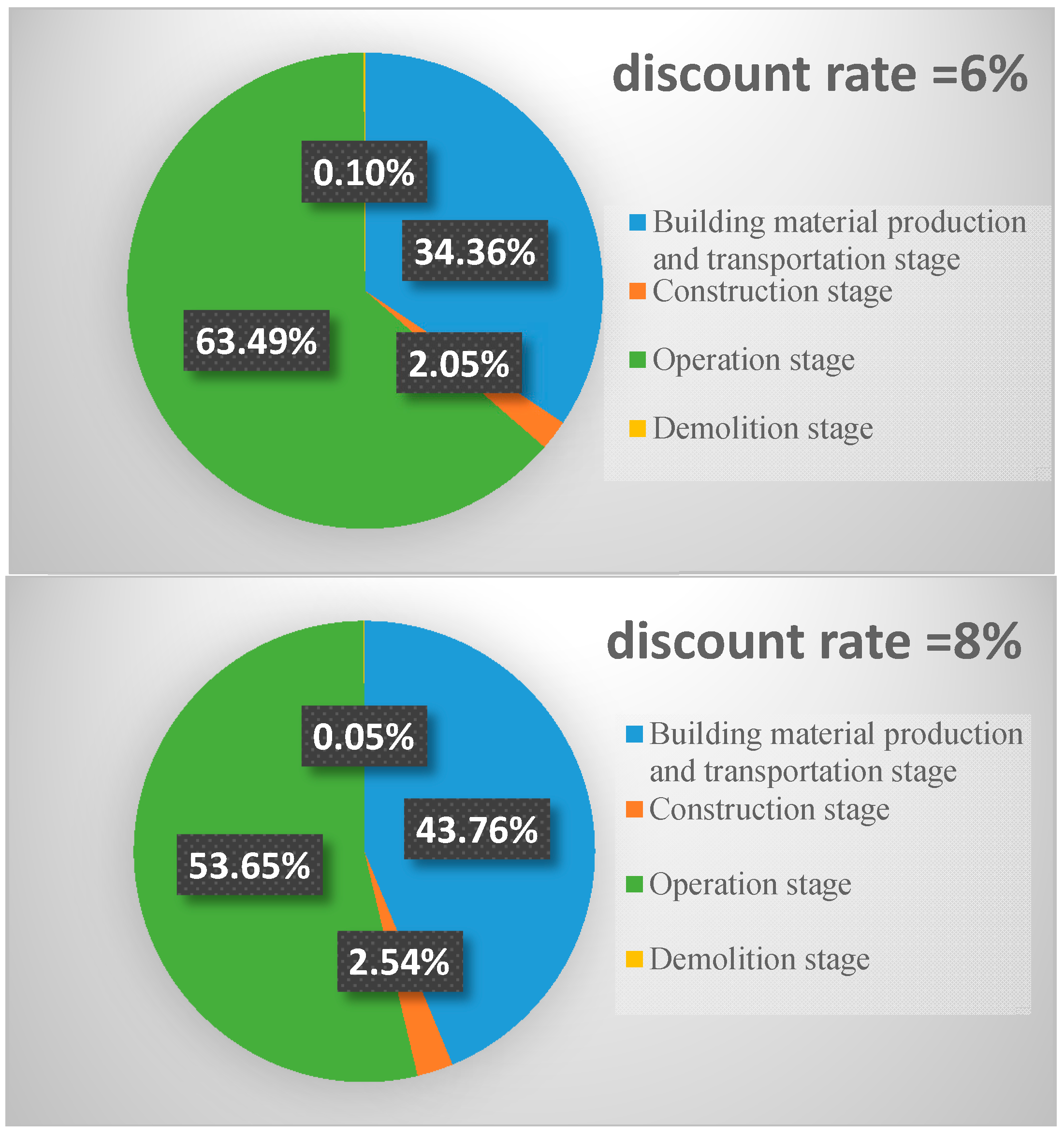

Therefore, a scenario analysis of the discount analysis is conducted. According to the previous studies on the discount rate mentioned above and at the end of

Section 2.2, the discount rate is chosen as 4%, 6%, and 8% for comparison. According to Equation (3) mentioned above, the present value of the life cycle carbon cost can be determined, with the known discount rate, quantity, and occurrence time of carbon emissions, and the relevant unit pollution damage cost of carbon emissions.

{kind=link}

{kind=link}

{kind=link}