The Empirical Analysis of the Impact of Bank Capital Regulations on Operating Efficiency

Abstract

:1. Introduction

2. Related Literature

2.1. Theoretical Underpinnings

2.2. Empirical Review

3. Data and Methodology

3.1. Data Collection

3.2. Model Specification

4. Empirical Results

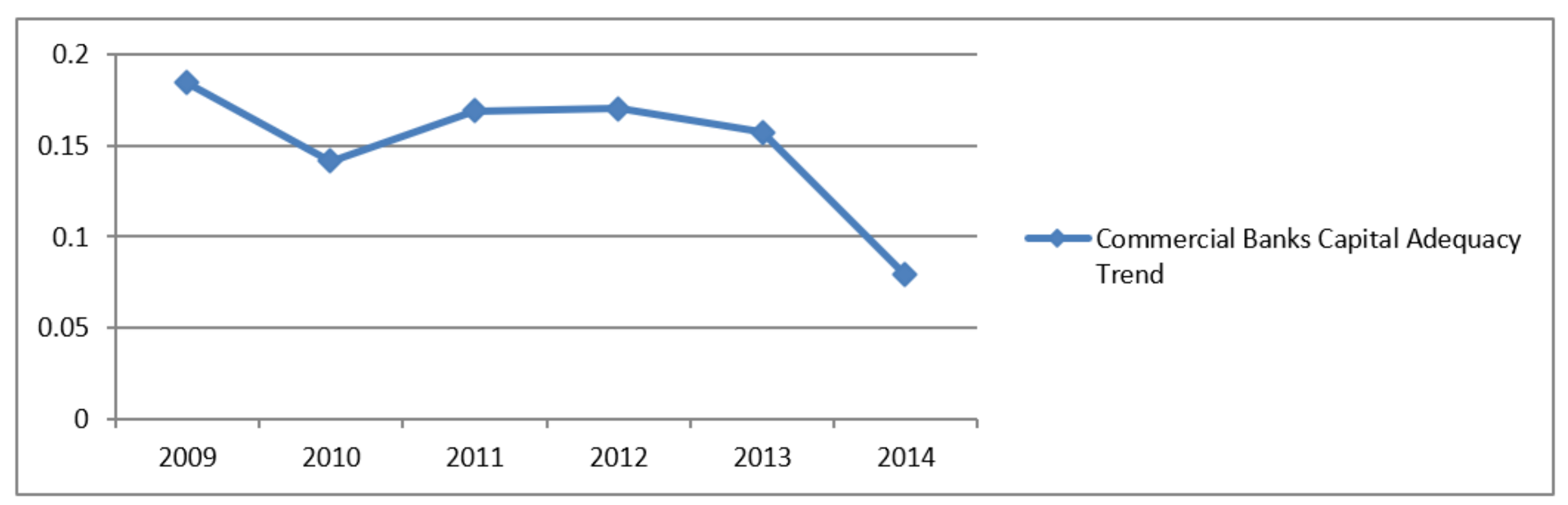

4.1. Descriptive Statistics

4.2. Regression Results

5. Concluding Remarks and Recommendations

Conflicts of Interest

References

- Aggarwal, Raj, and Kevin T. Jacques. 2001. The impact of FDICIA and prompt corrective action on bank capital and risk: Estimates using a simultaneous equations model. Journal of Banking and Finance 25: 1139–60. [Google Scholar] [CrossRef]

- Allen, Linda, and Anoop Rai. 1996. Operational Efficiency in Banking: An International Comparison. Journal of Banking & Finance 20: 655–72. [Google Scholar]

- Altunbas, Yener, Santiago Carbo, Edward P.M. Gardener, and Philip Molyneux. 2007. Examining the relationship between capital, risk and efficiency in European Banking. European Financial Management 13: 49–70. [Google Scholar] [CrossRef]

- Aly, Hassan Y., Richard Grabowski, Carl Pasurka, and Nanda Rangan. 1990. Technical, scale, and allocative efficiencies in US banking: An empirical investigation. The Review of Economics and Statistics 72: 211–18. [Google Scholar] [CrossRef]

- Athanasoglou, Panayiotis P., Sophocles N. Brissimis, and Matthaios D. Delis. 2008. Bank-specific, industry-specific and macroeconomic determinants of bank profitability. Journal of International Financial Markets, Institutions and Money 6: 1833–3850. [Google Scholar] [CrossRef] [Green Version]

- Barth, James R., Chen Lin, Yue Ma, Jesús Seade, and Frank M. Song. 2013. Do Bank Regulation, Supervision and Monitoring Enhance or Impede Bank Efficiency? Journal of Banking and Finance 37: 2879–92. [Google Scholar] [CrossRef]

- Guidance for National Authorities Operating the Countercyclical Capital Buffer. 2010. Basel: Bank for International Settlements Communications.

- Berger, Allen N., and Emilia Bo-naccorsi di Patti. 2006. Capital structure and performance in the US banking industry. European Financial Management 4: 49–70. [Google Scholar]

- Berger, Allen N., and Christa H.S. Bouwman. 2009. How does capital affect bank performance during financial crises? Journal of Financial Economics 109: 146–76. [Google Scholar] [CrossRef]

- Berger, Allen N., Richard J. Herring, and Giorgio P. Szegö. 1995. The role of capital in financial institutions. Wharton 19: 50–90. [Google Scholar] [CrossRef]

- Directorate of Banking Supervision. 2008, In The Banking and Financial Institutions (Licensing) Regulations. G.N. No. 150. Dar es Salaam: The Bank of Tanzania.

- Directorate of Banking Supervision. 2014, In The Banking and Financial Institutions (Licensing) Regulations. G.N. No. 297. Dar es Salaam: The Bank of Tanzania.

- Directorate of Banking Supervision. 2016, In Bank of Tanzania Annual Report. Dar es Salaam: The Bank of Tanzania.

- Calomiris, Charles W., and Charles M. Kahn. 1991. The role of demandable debt in structuring optimal banking arrangements. American Economic Review 81: 497–513. [Google Scholar]

- Chortareas Georgios E., Claudia Girardone, and Alexia Ventouri. 2012. Bank supervision, regulation, and efficiency: Evidence from the European Union. Journal of Financial Stability 8: 292–302. [Google Scholar] [CrossRef]

- Das, Abhimaan, and Saibal Ghosh. 2006. Financial deregulation and efficiency: An empirical analysis of Indian banks during the post reform period. Review of Financial Economics 15: 193–221. [Google Scholar] [CrossRef]

- Fama, Eugene F. 1980. Agency Problems and the Theory of the Firm. Journal of Political Economy 88: 288–307. [Google Scholar] [CrossRef]

- Färe, R., S. Grosskopf, and F. Hernandez-Sancho. 2004. Environmental Performance: An Index Number Approach. Resource and Energy Economics 26: 343–52. [Google Scholar] [CrossRef]

- Fiordelisi, Franco, and David Marques-Ibanez. 2013. Is bank default risk systematic? Journal of Banking and Finance 37: 2000–10. [Google Scholar] [CrossRef]

- Fungacova, Zuzana, Laura Solanko, and Laurent Weill. 2014. Does competition influence the bank lending channel in the Euro area? Journal of Banking and Finance 49: 356–66. [Google Scholar] [CrossRef]

- Greene, William H. 2008. Econometric Analysis, 6th ed. Upper Saddle River: Prentice Hall. [Google Scholar]

- Holmstrom, Bengt, and Jean Tirole. 1997. Financial intermediation, loan-able funds, and the real sector. Quantitative Journal of Economics 112: 663–91. [Google Scholar] [CrossRef]

- Isik, Ihsan, and M. Kabir Hassan. 2002. Technical, scale and allocative efficiencies of Turkish banking industry. Banking and Finance 26: 719–66. [Google Scholar] [CrossRef]

- Karimzadeh, Majid. 2012. Efficiency analysis by using Data Envelop Analysis Model: Evidence from Indian Banks. International Journal of Finance, Economics and Science 2: 228–37. [Google Scholar]

- Kopecky, Kenneth J., and David VanHoose. 2006. Capital regulation, heterogeneous monitoring costs and aggregate loan quality. Banking and Finance 6: 2235–55. [Google Scholar] [CrossRef]

- Llewellyn, David. 1999. The technical efficiency of large bank production. Journal of Banking and Finance 4: 495–509. [Google Scholar]

- Lotto, Josephat. 2016. Efficiency of Capital Adequacy Requirements in Reducing Risk-Taking Behavior of Tanzanian Commercial Banks. Research Journal of Finance and Accounting 7: 21. [Google Scholar]

- Lotto, Josephat, and Justus Mwemezi. 2016. Assessing the Determinants of Bank Liquidity with an Experience from Tanzanian Banks. The African Journal of Finance and Management 23: 76–88. [Google Scholar]

- Mehran, Hamid, and Anjan Thakor. 2011. Bank capital and value in the cross-section. Review of Financial Studies 24: 1019–67. [Google Scholar] [CrossRef]

- Milne, Alistair, and A. Elizabeth Wiley. 2001. Bank Capital Regulation and Incentives for Risk—Taking (December 2001). Cass Business School Research Paper. Available at SSRN: https://ssrn.com/abstract=299319 or http://dx.doi.org/10.2139/ssrn.299319.

- Niu, Xiaoyan. 2008. Theoretical and practical review of capital structure and its determinants. International Journal of Business and Management 13: 801–60. [Google Scholar] [CrossRef]

- Odunga, Robert M. 2016. Specific performance indicators, market share and operating efficiency for commercial banks in Kenya. International Journal of Finance and Accounting 8: 135–45. [Google Scholar]

- Pasiouras, Fotios, Sailesh Tanna, and Constantin Zopounidis. 2009. The impact of banking regulation on banks cost and profit efficiency: Cross-country evidence. International Review of Financial Analysis 6: 294–302. [Google Scholar] [CrossRef]

- Sealey, Calvin W., and James T. Lindley. 1977. Inputs, Outputs, and Theory of Production Cost at Depository Financial Institutions. Journal of Finance 32: 1251–66. [Google Scholar] [CrossRef]

- Operational Efficiency a Brand Point Management Perspective. 2008. Available online: http://www.schawk.com (accessed on 23 May 2017).

- Thakor, Anjan V. 1996. Capital requirements monetary policy and aggregate bank lending: Theory and empirical evidence. The journal of American Finance Association 51: 279–324. [Google Scholar] [CrossRef]

{kind=link}

| Hausman Fixed Random | |||

|---|---|---|---|

| Coefficients | (b) | (B) | (b-B) |

| fixed | random | Difference | |

| CAR | 0.788294 | 0.3952661 | 0.3935633 |

| ROA | −1.669282 | −1.999588 | 0.3303062 |

| SIZE | 0.006313 | 0.0167513 | −0.0104384 |

| LOAN - DEPOSIT | −0.0428018 | −0.0461751 | 0.0033733 |

| NPL | −0.1267676 | −0.1371741 | 0.0104065 |

| −0.1267676 | |||

| B = consistent under Ho and Ha; obtained from a regression command(xtreg) | |||

| B = inconsistent under alternative hypothesis (Ha), efficient under null hypothesis (Ho); obtained from regression command(xtreg) | |||

| difference in coefficients not systematic | |||

| = 164.54 | |||

| Prob > chi2 | = 0.0001 | ||

| (V_b-V_B is not positive definite) | |||

| Observations | Mean | Standard Deviation | Min. | Max. | |

|---|---|---|---|---|---|

| OEFF | 48 | 0.1222766 | 0.0386319 | 0.041 | 0.204 |

| CAR | 48 | 0.1264725 | 0.0301037 | 0.0895609 | 0.2371712 |

| ROA | 48 | 0.0201331 | 0.0152364 | −0.0207176 | 0.532177 |

| LN-DEP | 48 | 0.4845155 | 0.1421845 | 0.178 | 0.7067356 |

| NPL | 48 | 0.06897 | 0.024364 | 0 | 0.25 |

| SIZE | 48 | 13.90863 | 0.6163424 | 13.1305 | 15.23251 |

| Fixed-Effects (within) Regression | Number of Observation | = | 48 | |||||

|---|---|---|---|---|---|---|---|---|

| Group variable: Bank | Number of groups | = | 8 | |||||

| R-sq: | within | = | 0.5027 | Obs/group: | Min. | = | 6 | |

| between | = | 0.0652 | 6.0 | Avg. | = | 6.0 | ||

| overall | = | 0.0304 | 6 | Max. | = | 6 | ||

| F(5, 35) | = | 7.08 | ||||||

| Corr. ( | = | −0.3895 | Prob. ˃ F | = | 0.0001 | |||

| OEFF | Coeff. | Std. Err. | t | P ˃ |t| | [95% Conf. | Interval] | ||

| CAR | 0.788294 | 0.169275 | 4.66 | 0.000 | 0.4451829 | 1.132476 | ||

| ROA | −1.669282 | 0.375437 | −4.45 | 0.000 | −2.431459 | −0.907104 | ||

| SIZE | 0.006313 | 0.007105 | 0.89 | 0.380 | −0.008111 | 0.0207369 | ||

| LN-DEP | −0.0428018 | 0.0236661 | −1.81 | 0.079 | −0.0908466 | 0.0052429 | ||

| NPL | −0.1267676 | 0.0720683 | −1.76 | 0.087 | −0.273074 | 0.0195388 | ||

| _cons | 0.005097 | 0.107601 | 0.05 | 0.962 | −0.2133446 | 0.2235386 | ||

| sigma_u | 0.04036947 | |||||||

| sigma_e | 0.01878804 | |||||||

| rho | 0.82196346 | (fraction of variance due to ) | ||||||

| F test that all = 0 | F(7, 35) = | 9.87 | Prob. ˃ F | = 0.0000 | ||||

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lotto, J. The Empirical Analysis of the Impact of Bank Capital Regulations on Operating Efficiency. Int. J. Financial Stud. 2018, 6, 34. https://doi.org/10.3390/ijfs6020034

Lotto J. The Empirical Analysis of the Impact of Bank Capital Regulations on Operating Efficiency. International Journal of Financial Studies. 2018; 6(2):34. https://doi.org/10.3390/ijfs6020034

Chicago/Turabian StyleLotto, Josephat. 2018. "The Empirical Analysis of the Impact of Bank Capital Regulations on Operating Efficiency" International Journal of Financial Studies 6, no. 2: 34. https://doi.org/10.3390/ijfs6020034

APA StyleLotto, J. (2018). The Empirical Analysis of the Impact of Bank Capital Regulations on Operating Efficiency. International Journal of Financial Studies, 6(2), 34. https://doi.org/10.3390/ijfs6020034