A Study to Identify Long-Term Care Insurance Using Advanced Intelligent RST Hybrid Models with Two-Stage Performance Evaluation

1

College of Management, National Chin-Yi University of Technology, Taichung 411030, Taiwan

2

Department of Finance, Chaoyang University of Technology, Taichung 413310, Taiwan

3

Executive Doctoral Business Administration, Danphine University of Business, CEDEX 16, 75775 Paris, France

*

Author to whom correspondence should be addressed.

Mathematics 2023, 11(13), 3010; https://doi.org/10.3390/math11133010

Submission received: 23 May 2023

/

Revised: 24 June 2023

/

Accepted: 3 July 2023

/

Published: 6 July 2023

(This article belongs to the Special Issue Industrial Mathematics in Management and Engineering)

Abstract

:With the motivation of long-term care 2.0 plans, forecasting models to identify potential customers of long-term care insurance (LTCI) are an important and interesting issue. From the limited literature, most past researchers emphasize traditional statistics techniques to address this issue; however, these are lacking in some areas. For example, intelligent hybrid models for LTCI are lacking, performance measurement of components for hybrid models is lacking, and research results for interpretative capacities are lacking, resulting in a black box scenario and difficulty in making decisions, and the gap between identifying potential customers and constructing hybrid models is unbridged. To solve the shortcomings mentioned above, this study proposes some advanced intelligent single and hybrid models; the study object is LTCI customers. The proposed hybrid models were used on the experimental dataset collected from real insurance data and possess the following advantages: (1) The feature selection technique was used to simplify variables for the purpose of improving model performance. (2) The performance of hybrid models was evaluated against some machine learning methods, including rough set theory, decision trees, multilayer perceptron, support vector machine, genetic algorithm, random forest, logistic regression, and naive Bayes, and sensitivity analysis was performed in terms of accuracy, coverage, rules number, and standard deviation. (3) We used the C4.5 algorithm of decision trees and the LEM2 algorithm of rough sets to extract and provide valuably comprehensible decisional rules as decision-making references for the interested parties for their varied benefits. (4) We used post hoc testing to verify the significant difference in groups. Conclusively, this study effectively identifies potential customers for their key attributes and creates a decision rule set of knowledge for use as a reference when solving practical problems by forming a structured solution. This study is a new trial in the LTCI application field and realizes novel creative application values. Such a hybrid model is rarely seen in identifying LTCI potential customers; thus, the study has sufficient application contribution and managerial benefits to attract much concern from the interested parties.

Keywords:

long-term care insurance; potential customer; feature selection technique; data discretization method; decision tree; rough set theoryMSC:

68Q15; 68Q171. Introduction

This section introduces the related issues of research background, research problems, and main research motivation, and accordingly explores research originality as well as research importance and research purposes.

1.1. Research Background, Research Problems, and Research Motivation

In recent years, Taiwan has been affected by the social problems of decreasing birth rate and aging population, and this issue and importance of these problems have led to the demand for new models and emerging techniques with regard to long-term care insurance (abbreviated as LTCI in this study). Therefore, this study was developed with the intention of researching the effect of the four powerful motivating words “new”, “heart”, “salary”, and “warmth” on LTCI.

First of all, we started with the first brand “new” models of emerging technology for addressing mathematical application issues to solve the real-life problem faced. After the emergence of new information technology (IT) techniques, the hottest technical issues recently are related to data mining for machine learning (ML) [1] methods, such as decision trees (DTs), random forests (RFs), and multilayer perceptrons (MLPs), with other related topics that have also been introduced into the financial and insurance industry, resulting in the rise of finance and insurance 4.0 and arousing widespread attention from academia and industry. Next, with the generation and collection of a large amount of transaction data, technologies for addressing how to deal with the large amount of data have emerged one after another. We know that the hierarchical structure of knowledge is divided into four stages in order: data ➔ information ➔ knowledge ➔ wisdom [2], the concerns of which involve how to transform the bottom-level data into a more useful information system, then upgrade it to a higher level of professional knowledge and even the highest level of wisdom. In turn, this framework has greatly contributed to the evolution of data mining techniques in mainstream research fields in the past 20–30 years, leading the industrial transformation brought about by the digital economy and itself benefiting in terms of learning how to transform data into knowledge/wisdom. In particular, in contrast to the urgently needed long-term care issues for the elderly under the current financial and insurance 4.0 framework, the core importance of “LTCI” data accumulated rapidly and closely related to the future of the people becomes even more important for quality of life in old age. Thus, this study investigates an important and interesting issue: developing data models of machine learning techniques as its first core research interest from the perspective of industry data applications.

Accordingly, in order to match and conform to the government’s future policy priorities, it is necessary to explore the recent issue of disability and LTCI. In particular, LTCI was primarily chosen as the research topic to address the fact that Taiwan has entered the state of an aging society; thus, to properly improve the second half of life for the elderly in the near future, this study’s second core research interest is identifying LTCI data. According to a newspaper report, a report released by the Ministry of Health, Welfare and Welfare of Japan in 2013 shows that only 4.3% of the people who paid LTCI were between the ages of 40 and 64, and most of the rest of the payers were 65 and older. Moreover, they had heart disease, dementia, arthritis, stroke, fractures, and slips, and elderly debilitating diseases accounted for 75.4% of the serious diseases. It can be seen that the social problems of the elderly are still serious in Taiwan, and thus we need increased attention on these problems even more in advance. By the above reason, we should follow the guidance of the second motivation, “loving heart”, in facing this practical problem in the insurance industry. It is true that life is always full of crises and changeable characteristics in ever-changing circumstances, and the damage this may cause can be very scary and unpredictable. Thus, it is necessary to prepare for emergencies, and this implies that the mechanism of insurance is requisite, particularly for the elderly. It was found that many elderly people may be limited by finances and illnesses in their later years, without dignity; they suffer from the abandonment of their relatives. Thus, this case deeply shows the key importance of the protection of LTCI for the elderly in the face of the imminent future. As Taiwan has been negatively impacted by the declining birth rate in recent years, the elderly have more difficult lives in their later years and may be even more unhappy; they may suffer from illness and even worse. These important and interesting focus topics are worthy of a great degree of our attention. Therefore, exploring the issue of long-term care [3] for the elderly is something that we as a country and society need to face seriously, which drives this study.

Therefore, if we have the customer’s “LTCI” data information, we can use a “new” technical model to identify the characteristics of future potential customers of LTCI and may generate their decision-making rule set, so the “new” technical model + “LTCI” data combination becomes extremely important. However, there are three gaps for general insurance salesmen (referred to as insurers) when looking at real-world insurance data in practice: (1) a lack of professional technical knowledge regarding the huge amount of insurance data in industry databases, and the fact that it is impossible to effectively identify information in the field of new techniques; (2) a lack of effective technical models to interpret information, as well as a lack of analysis capabilities; and (3) insufficient transparency of insurance financial data, which may cause information asymmetry and lead to adverse consequences, causing insurers and managers to be full of selfish behaviors and eventually lead to mutual suspicion. The short-term problem is discord among employees, and the longer-term problem is direct possible tangible damage to the operating performance of the insurance company and indiscernible reputation damage. In addition, early scholars focused on the analysis of traditional statistical theory in LTCI research, and an effective LTCI prediction system for practical development is absent, resulting in the inability to effectively correlate and verify the research theory and practice results. Based on the above reasons, it is urgent to build a practical and effective “new” advanced intelligent LTCI forecasting system. When we have insurance customers’ data, this can help insurers quickly develop potential customer targets, increase personal business performance, and create wealth through the mining of various possible hidden factors using effective hybrid models of noted machine learning techniques. Based on different classification functions of machine learning models, this study proposes an evolutionary method for the framework of advanced and intelligent data application analysis and builds an improved LTCI forecasting system. According to the literature review, these appliable methods are rarely used in the related LTCI mining research.

1.2. Continuous Research Motivation and Research Originality

Regarding the key issue of LTCI, we started from the following two aspects, the insurance industry and insurers. The first is the insurance industry. With the recent rapid development of IT techniques and continuous research and development, the industry market of insurance management information systems (IMISs) has become vigorously developed [4]. In particular, they can now solve the problem of the storage of a large amount of customer insurance data, complete with preserving resource deposits. The financial concept of “Insurance” is a kind of mutual assistance that originated in the United Kingdom. It also is the cornerstone of stabilizing the national economy and an important indicator to guide a country’s economic development. Furthermore, from the perspective of Taiwan’s insurance development history, there are six important stages of development, starting from 1962 to the present. In particular, the final sixth stage, from 1994 to the present, is important. This stage concerns the development of diversified insurance products for Taiwan. During this policy period, there are some special products, such as major diseases, end-of-life, and second- and third-level disability exemptions, including LTCI. In addition, due to the gradual aging of the population in Taiwan, the average life expectancy has increased, and the social problems of the elderly population and the need for long-term care have gradually surfaced. The support of disability insurance can allow people to be protected by insurance at every stage of life [5], so insurance products are more complete and diversified, and LTCI was therefore produced in response to this timing. The next step is to explore and understand the professional issues of insurers. Recently, sales of diversified insurance policies in Taiwan have truly professionalized insurance business operations. In particular, since Taiwan’s insurance financial market has reached maturity and saturation, the business expansion of insurers has been greatly restricted and hindered. At present, insurers have to face the following three business operating problems: (1) Excessive competition: There are currently over 320,000 insurers registered in the insurance association. In contrast, product performance is naturally highly competitive. Therefore, in order to develop operating performance, all insurers must muster their strength. (2) Call center marketing: In the insurance industry, it is important to develop potential new customers to purchase new policies. However, traditional insurers often make cold calls to strangers through a call center in order to develop customers. The effect is often not as good as expected. The success ratio is often less than 1%, and this process often requires some frustration. (3) DM marketing: Insurance is an intangible commodity that cannot be touched or seen, and insurers only have cold numbers on their report papers. Therefore, marketing through DM is just like looking for a needle in a haystack. It is problematic that DMs are often sent but the response rate is still less than 1%, and thus this may be described as a miserable operation. The above three questions prompted this study’s investigation of motivation power, and we constructed an effective method to help insurers develop potential customers. Therefore, the idea of helping insurance companies and insurers and helping them enhancing salaries became the third triggering force, “salary”, to drive this study.

Moreover, based on a survey report from the Ministry of Health and Welfare, the government’s LTCI was launched in 2017, and there are currently about 670,000 people who need long-term care; however, the current LTCI coverage rate in Taiwan is only 2.04% (about 470,000 people), which means that nearly 98% of these people have not purchased LTCI. From the above report, this implies that there is an emerging need for the requirement of LTCI. In addition, insurance experts suggest that individuals should prepare LTCI in advance when they have the possibility of bearing a burden so that their family members can experience a reduced high degree of insecurity and uncertainty in the future, and this can prepare a better-secured “warmth” for family life. Importantly, issues related to LTCI were the fourth, heartwarming driving force, “warm”, of this study.

It is true that we can review and learn the relevant historical data to actively face present and future problems, meet challenges, and solve problems. Therefore, we must always consider whether there are some rules or some attribute correlations among the insurance-related information. Relatively speaking, it is important to find the key attributes of LTCI and to apply effective data or new intelligent hybrid modeling methods [6] as effective auxiliary tools to address the industry data analysis. By developing an effective forecasting model, we can help insurers engage in the business of developing future potential customers. From different perspectives, all the above signs show the key importance of data mining technology, and we can use and trace the application of “new” models for data mining technology to dig out any hidden information from the given data; in particular, treasure can be excavated from past insurance data. Therefore, this study serves to establish future effective decision-making rules and criteria from an amount of LTCI data [7] to help the insurance industry and insurers expand their operating performance. However, insurers face a mature insurance market full of highly uncertain and highly competitive risks now. This situation highlights the strong demand of insurers for valuable information, such as future personal business performance and potential customer feature development. In practice, insurers can be divided into two types: one utilizes subjective judgement, relying on their own subjective consciousness and intuition to “blindly” advocate customers to buy LTCI; conversely, the other utilizes objective analysis, using effective tools to “clearly” screen data collected for identifying potential customer characteristics. The first type has its disadvantages because the subjective person has a slightly random method of choosing targets, which may tend to give the feeling of compulsory insurance sales and lead to poor performance and low morale. On the contrary, the second type has the help of new technology models, and for them it is more feasible to effectively find out potential customers for targeted marketing. Therefore, we need an objective and effective advanced intelligent hybrid LTCI model [8,9] (named AIHLCIM in this study) to help insurers correctly and effectively identify potential LTCI customers and actively develop operating performance. The establishment of this hybrid model can ensure the successful development of potential customers for addressing the key factors of characteristics. Developing the AIHLCIM and its performance evaluation is an urgent need for interested parties under different interest considerations. The important functions of the AIHLCIM include recording practical examples of LTCI, providing forecasting capabilities, providing decision-making knowledge base rules of LTCI potential customers, and supplying interested parties with use. The AIHLCIM can not only identify a group of important determinants that affect LTCI, but also has a valuable property. After the above analysis results, we understand that it is easier to fully mine the characteristics of potential LTCI customers by using some useful and objective tools or methods. The AIHLCIM can not only increase the information transparency or information disclosure of potential customers [10,11], but also can reduce the operating risk of insurers and the insurance industry. More importantly, the calculation and acquisition of data for the AIHLCIM model does not require a highly specialized role, and all insurers easily have this ability in a friendly manner. For insurers, after standardizing the operation and acquisition of this advanced hybrid model [12], it is helpful to easily establish a LTCI prediction model [8]; thus, it becomes a topic of friendly operation and of academic research value.

In the past decades, data mining rule techniques in machine learning technology have developed to a fairly mature and stable stage and can be applied to various fields, such as medical diagnosis analysis, financial management, retail market analysis, manufacturing industry process, and other related fields. However, in our limited review of the literature, it has not been applied to the study of mining potential customer characteristics of LTCI, especially for the advanced intelligent hybrid model built in this study, for which data are even more lacking. Therefore, this study uses the LTCI data collected from existing customers to construct an advanced hybrid model, conduct mining, excavate unknown mineral deposits hidden in a given dataset, extract and summarize decision-making knowledge classification rules, apply them to the actual issues of LTCI, help insurance companies and insurers operate well, and achieve a win–win situation among insurance companies, insurers, and customers. The application of machine learning technology to excavate the laws hidden in the database and provide an advanced model is a practical topic that has considerable reference value for insurers because it can accelerate the improvement of service quality and added value in the insurance industry, continuously improve management performance, and establish sustainable competitive advantages.

From reviewing the limited literature, it was found that the research of LTCI in the early days used traditional statistics-based research frameworks to deal with related LTCI issues and obtained satisfactory results to varying degrees; however, traditional statistical methods have two major problems. First, the results are affected by many factors (or problems) or application constraints. Second, one encounters the limitations of assumptions and conditions during data distribution processing. However, most of the data models used to deal with qualitative or quantitative data often violate the above-mentioned data distribution restrictions in the real world of LTCI, and it is even more difficult to correctly reflect the real insurance market data status. In addition, traditional statistical methods combined with LTCI issues [13] have the following five main shortcomings: (1) past research has not seen the construction of such advanced intelligent hybrid models; (2) no scholars have discussed and developed the application of this practical AIHLCIM; (3) a lack of individual performance measurement to explore the constituent technologies (elements) of this advanced intelligent hybrid model; (4) traditional research results lack effective rule interpretation capabilities, and are put at risk by their black box operations so as to encounter difficulties in decision making; and (5) the above knowledge gap has not been effectively filled. Most of the popular prediction models in recent years are composed of different modes or steps (hybrid or fusion), and their past performance has been obtained in the literature [14,15,16], where it is demonstrated that such an intelligent hybrid model is superior to a stand-alone model, since each classification technique has its strengths and weaknesses. In the past decades, scholars have devoted themselves to the application of intelligent hybrid models, which shows that advanced machine learning technology will still occupy a significant leading position in the future [15]. Based on the above comprehensive discussion, it is urgent to apply objective and effective machine learning techniques to the mining of potential customer characteristics of LTCI and its model performance evaluation [17], and it is also of great development value. Therefore, this study proposes a superior set of advanced intelligent hybrid models, with an eye towards maximizing the advantages of individual models while minimizing their disadvantages.

This study develops the AIHLCIM to eradicate the above two major deficiencies and five major problems. The reasons for the selection of the five main components for the hybrid AIHLCIM models are introduced below. (1) Data discretization technique: First, in order to improve the classification performance of the intelligent models, two application methods of data discretization techniques are proposed, including expert discretization and automatic discretization. According to the research of Ouyang and Chou [18] and Zhao and Wu [19], it is known that expert discretization performance is better than automatic discretization performance, but sometimes it is difficult to obtain the results of expert discretization performance, and automatic discretization is the only good choice. Therefore, based on the above reasons, this study adopts expert discretization for decision-making attributes for better performance and automatic discretization for conditional attributes (because it is difficult for experts to agree on this part). (2) Feature selection method: This is used in the field of data mining technology in the data pre-processing stage, and it plays a very important role, mostly in terms of selecting important key attributes to speed up the experimental operation of the intelligent models [20]. It has the following three key advantages: improving classification prediction efficiency, eliminating experimental overfitting problems, and developing more rapid and effective cost-effectiveness models. Due to its satisfactory research results in the classifier prediction model community, it is often applied to different fields, such as statistical data analysis, financial accounting, medical services, and industrial services [21]. Therefore, it was chosen for the advanced intelligent hybrid model proposed in this study. (3) Machine learning techniques: Many studies have switched to machine learning techniques [22,23,24] to overcome the limitations of statistical assumptions [25] and successfully solve various prediction (or classification) problems in the real world. More common classification techniques used, such as rough set theory (RST) [26], DT [27], RF [28], and MLP [29,30], have become an important research trend at present. Moreover, Bayes network (BN) learning [31], logistic regression (LR) [32], naïve Bayesian (NB) [33], and support vector machine (SVM) [34] classifiers are always emerging techniques helpful for industry application fields; thus, they were also selected and emphasized in this study for the sake of comparison. (4) The rule extraction method: The extracted decision rule set has attracted the attention of many researchers and established an effective decision rule knowledge base to mine hidden information, such as the famous C4.5 of the decision tree and the LEM2 algorithms of the rough set theory, and it has been applied in different fields [35] with outstanding performance. Therefore, this study selects it as the main rule generation technical basis for the advanced intelligent hybrid models. (5) Post hoc test analysis: The well-known ANOVA test and Scheffe’s test [36] were used to effectively review and measure the differences afterwards.

1.3. Research Importance and the Purposes of Research

To sum up the above arguments, these four triggering forces rigorously shape this study and motivate the implementation of this research work. Then, we have the following three positive practices to rationalize the methods proposed in this study. (1) The proposed AIHLCIM in this study has the following advantages: it simplifies the set of decision-making rules, facilitates rule interpretation and understanding, provides robust and reliable empirical results, and simultaneously processes nominal and categorical data. (2) With valuable experience in financial and insurance-related industries, we are confident to establish a knowledge base for mining potential customer characteristics of LTCI. (3) The construction of such a trustworthy LTCI potential customer prediction model is extremely desired by insurance decision makers and insurers for taking advantage of the superior background of industry knowledge and removing the shortcomings of the aforementioned problems. Importantly, this study takes LTCI customers as the research object to organize attribute selection methods, data discretization techniques, rough set theory, decision trees, and different classifiers based on the individual advantages of decision-making rule extraction algorithms and other techniques. Relatively, this study is focused on “insurance field application analysis”, a relatively new field. Based on the limited information, no other researchers have found such a mixed model and applied it to the prediction of potential LTCI customers. Therefore, if the research topic of this study is important, the proposed method is a little innovative and has specific application value and contribution in academics and industries on the research and development of related LTCI studies in this professional field.

Based on the above descriptions, this study has the following research purposes, as follows: (1) Construct a suitable advanced intelligent hybrid model for the mining of potential customer characteristics of LTCI and explore its classification knowledge. (2) Measure the performance difference during verification of the feature selection method. (3) Measure the performance difference during verification of the different classification algorithms. (4) Perform data analysis on the classification accuracy rate. (5) Identify the determinants that affect the LTCI. (6) Generate comprehensible decision-making rules of LTCI purchase as the basis for establishing a knowledge base system.

The remainder of this paper is structured in the following order established. Section 2 describes the related literature review for some topics of LTCI with its application and some emerging classification techniques. Section 3 describes the structures of the proposed hybrid models. Section 4 introduces a real case of long-term insurance data and the empirical results with its discussion. Section 5 describes the research findings and limitations of the research results, and Section 6 reports the analysis of the results and the conclusions for subsequent research.

2. Literature Review

The relevant literature of this study includes LTCI and its related potential customer application issues, feature selection and its related applications, data discretization and its related applications, decision tree learning classifier and its related applications, rough set theory and its related applications, rule filtering methods, and the introduction of other famous classifiers and their related application research, described in detail as follows.

2.1. LTCI and Its Related Application Issues for Developing Potential Customers

It is a true that unpredictable things and good and bad times happen randomly; thus, it is really appropriate to extend the meaning of this sentence to insurance. The so-called “insurance” means that once a risk occurs, it will inevitably cause large or small personal financial losses, but it can be compensated through gathering the resource power (such as money) of everyone from insuring insurance [37]. If you have bought insurance, you can avoid risks and benefit from an agreement of insurance. The real concept of insurance should mean and imply that paying a relatively small amount of money can be exchanged for greater compensation and protection, especially for the need of long-term care in the elderly, when unfortunate things happen. Long-term care refers to the need to provide life care and medical care for a specific group of people whose physical and mental disability lasts for more than 6 months. In response to Taiwan’s aging population with the rapid growth of the population that needs to be specifically taken care of and in order to reduce the burden on the family, the government first proposed the long-term care 1.0 plan, which is the 10-year long-term care plan. Continually, long-term care 2.0 is an upgraded version of 1.0; the original 1.0 service items have been increased from 8 to 17 items in the 2.0 version, the applicable objects have also increased from the original 4 items to 8 items, and the number of services has increased from the original estimate of more than 510,000 people to more than 730,000. Furthermore, driven by the implementation of the long-term service 2.0 project from 2017, the insurance for long-term care has begun and is ready to be offered to the people.

However, in the actual operations of the insurance business, two problems are faced. One is the professionalism of insurance, and the other is that the valuable customer information stored in the database is ineffectively use, which results in a serious problem: potential customers cannot be discovered using existing insurance data for performance enhancement. It is necessary that enterprises should think of the problematic dilemma between the development of new customers and the maintenance of old customers to expand business. For sustainable operation, enterprises must allow old customers to continue to buy new and old products and maintain long-term strong relationships to ensure steady growth in operation performance. In particular, it is interesting that the cost of developing a new customer is several times more than maintaining old customers. Under this concept, it is easier to retain old customers with a low cost; thus, to retain old customers is more important than to constantly develop new customers. With the progress of IT, combined with corporate processes and emerging technology, it is important to collect and quickly analyze insurance customer data to establish an effective prediction model. Liu et al. [38] explained that the customer information system can grasp complete and correct data. By analyzing customer needs through the collected data to reduce transaction costs, switching costs can be increased, and customers’ dependence on enterprises will increase. Alseadoon et al. [39] pointed out that the use of the technical support of software can improve tailor-made services and maintain the maximum profit of enterprises. Woratschek et al. [40] combined enterprise processes and emerging techniques to enable enterprises to better understand all aspects of customer data on continuous innovation, service improvement, and maintenance of customer relationships, thereby improving customer satisfaction and customer loyalty. Sheth and Kellstadt [41] pointed out that database marketing uses computer technology to manage a database system of information about existing customers and potential customers and to establish a good long-term relationship with customers. Shah and Murthi [42] indicated that the purpose of database marketing is to use customer data to improve the application of marketing resources by enterprises, deliver more useful information to specific objects, and maintain a good long-term close relationship with customers.

As stated above, it is an important concept that a good instrument holds good benefits; thus, this study proposes that from the data of some existing customer databases in accordance with the attributes of the databases, we can find out the special features, characteristics, or hidden information of potential customers. Given the above reason, currently only 2.04% of those for whom LTCI is relevant are insured, so there is still a lot of room for growth of selling new products for long-term insurance; thus, we can find a niche that can develop new value from existing customers. Based on this principle, this study establishes a set of advanced and intelligent hybrid models to identify the key attributes that affect the purchase of LTCI and generate the decision-making decision rules for interested parties.

2.2. Feature Selection and Its Related Application

Practice data often have high-dimensional attribute characteristics; however, many past studies have shown that when dealing with high-dimensional data, if the training samples are limited, the Hughes phenomenon will be encountered because high-dimensional data require more training samples. Under a fixed training sample, the classification accuracy gradually decreases as the high-dimensional data continue to increase [43]. At this time, to overcome the above defects, feature selection (or attribute selection) technology is needed as an effective method to lower the dimensions [44,45]. Since the 1970s, attribute selection has been widely studied and used in many research fields, such as statistical technical model analysis [46], machine learning [47], data mining [48,49], etc. Attribute selection has many advantages [50], including: (1) Data collection: It can reduce the cost of data collection, which can reduce the waste of unnecessary collection costs and resources since the amount of data is reduced. The data are also clearer and easier to see. (2) Data processing: By deleting redundant attributes, data storage space can be reduced. Because the amount of data is reduced, the calculation of the classification model can be made more efficient, and the model can be more simplified. (3) Data interpretation: After attribute selection, the shortcomings of irrelevant attributes that interfere with the prediction results can be improved. This also makes the research results more explanatory, accelerates the classification model derivation and explores structured knowledge, and leads to a better ability to explain the results of target variables. Therefore, attribute selection is usually used mainly for the following four reasons: to simplify the model, to be more convenient and easier to interpret, to speed up the model derivation, and to simplify the establishment of structured knowledge. According to the literature [51], evolutionary attribute selection technology can be simply divided into linear and nonlinear models, which are used to screen important conditional attributes and have significantly better performance. In terms of practical statistical applications, it can be widely applied to services in different fields, such as data mining [49] and other industrial services [52], all of which have excellent performance reflections and objective evaluations for reducing model complexity.

In summary, it is known that attribute selection techniques have performed well according to the research results of past scholars. Thus, this study implements and absorbs the advantages of this attribute selection technique to simplify the derivation of this advanced intelligent hybrid model and increase the accuracy of the classification model and accelerates the definition of main determinants that affect the purchase of LTCI.

2.3. Data Discretization and Its Related Application

In the field of data mining, data discretization [53] is an important data preprocessing function. In the literature [19,54], it is pointed out that data discretization includes two methods: expert discretization and automatic discretization. The former represents experts in different fields cutting data according to personal professional experience, judgment, knowledge, or intuition, while the latter uses different mathematical equations to carry out automatic data cutting. Unfortunately, in the real world, due to certain possible problems, such as the amount of data being too large, resources are limited, data experts cannot easily obtain them, subjective factors may be involved, or unreasonable factors may lead to possible wrong decisions, etc. Expert opinion cutting cannot be obtained when there are no expert discretization data for reference, and the automatic discrete method is the only and best choice. There are three core functions of data discretization: (1) it helps reduce the number of subsequent rule generations; (2) it helps improve the performance of classifiers; and (3) it cuts off continuous value attributes, which is helpful for human natural semantics representation of value.

Based on the excellent function of data discretization, this study uses the data discretization method on decision attribute and condition attributes. With the advantages of these two data discretization methods, it helps the proposed hybrid models improve classification quality and generate human nature semantic value for ease of reading and understanding.

2.4. Research on Decision Tree Learning Classifier and Its Related Application

In the field of applied research, the DT learning classifier has been a very popular classification algorithm and prediction tool [55,56] used to analyze data or assist decision making. A DT is a special tree structure that utilizes a tree-like graph and possible outcomes to model a target decision [57]. DTs [27] are commonly used algorithms, including CARTs (classification and regression trees), ID3 (Iterative Dichomizer 3), and C4.5 rule induction algorithms. (1) The CART algorithm was proposed by Breiman et al. [58]; it is a binary DT, which is composed of nodes formed at different stages and branches between nodes under various conditions. (2) The ID3 algorithm is widely used to deal with discrete data and can take into account the advantages of improving the classification accuracy and reducing the complexity of the tree [59]. (3) The C4.5 was proposed by Quinlan [60], mainly to improve the shortcomings of ID3; it uses information theory and selects the attribute with the largest increase in information as the segmentation attribute to construct a complete DT structure by the inductive learning method.

A DT mainly uses the concept of entropy to measure the information value of the attribute; assuming that a set includes a possible result , the entropy for its mathematical algorithm can be defined as the following Equation (1), in which represents the category (class) belonging to the ratio of set [59]:

In addition, represents the information gain of an attribute in the set , and its Equation (2) for mathematical formation is defined as follows:

where the value of attribute is , and is a sub-set of set , then is the number of elements in the sub-set , and is the number of elements in the set .

In summary, a DT [61] has the following advantages: (1) it has the property of fast construction, (2) it can generate decision rule sets, (3) it is easy to understand and implement for rule sets, (4) it can handle data with category attributes concurrently, (5) it has excellent classification performance, and (6) it can make feasible and effective classification results for large data sources in a relatively short period of time. Due to DTs having the above-mentioned advantages, and the resulting decision rules having the advantage of being clear at a glance, a variety of evolutionary DT-related models have been constructed to be applied to various industrial fields, such as finance and banking, industrial fraud detection banking, credit crisis early warning model, and bioinformatics and other integrated application research, and all have performed well.

Therefore, due to the excellent performance and advantages of the DT C4.5 algorithm [61] in the past, it was favored in this study and was selected as one of the best candidates for classifier verification of classification performance.

2.5. Research on Rough Set Theory and Its Related Applications

RST [62,63] has the ability to deal with classification problems of fuzzy and uncertain information, and it thus has been widely used in medical, financial, manufacturing, imaging processing, and other fields of different industries. In RST [26,64], the training sample and the corresponding attributes are regarded as an information system, a decision table is composed of all data, and the decision rule is based on “If conditional attribute then decision attribute” for if–then decision rules to represent. The data composition has lower and upper approximations [65,66,67] as the basis for data classification. The following five major definitions of RST are explained as follows:

Definition 1.

Let

and

, be in a finite set

with non-empty attributes ( is the conditional attributes, and is the decisional attributes), is a reduction set of attributes, and represents a sub-set of the universe of discourse that is a finite (non-empty) set of objects; then let

, be a conditional attribute

for a collection of values, and for observations (objects)

and

, let

and

, and

refers to a decisional attribute.

Definition 2.

For

, it represents that the indiscernibility or equivalence relation is recorded as

, which is called the indiscernibility relation of

, and

represents the equivalence classification of the indiscernibility or equivalence relation of

, which are formatted as the following Equations (3) and (4) for the mathematical algorithm. Importantly, the universe

of discourse is also a finite (non-empty) set of objects.

Definition 3.

In the set

, the lower bound

and the upper bound

of

are represented by approximation sets, which are expressed in Equations (5) and (6) for their mathematical formation below:

is an observation value (object) in the value range , and is the approximately the lower bound of the set , which means that it is included in , and it must belong to the set ; is approximately the upper bound of the set , and this is expressed as the same, as the set has a non-empty intersection that may belong to the set . If the set is a non-empty intersection, then the set is rough or roughly definable as . However, is expressed as the boundary of ; if the lower bound is approximately the same as the upper bound, then the set cannot be classified exactly. The boundary, the positive boundary , and the negative boundary are mathematically formatted as Equations (7)–(9), respectively, as follows:

Next, the classification accuracy and classification quality are defined by the following Equations (10) and (11) for their mathematical formation, respectively. (Note: if , it means that the decision table is consistent; otherwise, it is not consistent.)

Definition 4.

Another important function of RST is defined as

, which is defined as

, and the reduced set is marked as

; it needs to satisfy;

concurrently; that is, it can retain the original attribute set information, and the reduction is expressed in Equation (12) for its mathematical formation, as follows:

Definition 5.

The core is also another important function of RST that can provide the most relevant attribute information. First, let

be the set of all reduced attributes, and the

refers to a non-empty attribute of a finite set with all the conditional attributes and the decisional attributes. The core can be formatted and expressed as Equation (13) for its mathematical definition, as follows:

RST contains two main important functions for attributes: core and reduction. (1) If the set of data attributes is the most relevant and indispensable set of attributes in the data set, it is called the core, (2) but if the set of data attributes is interdependent, all possible minimum sets of attributes can be found, it has the same number of unit sets and provides the same quality as the original data set, and then it is called a reduction. Specifically, if some attributes or attribute values are redundant or repeated in the entire dataset, reduction can filter out or delete these unnecessary attributes or attribute values to form several smaller attribute sets. Thus, the reduction is the smallest set of attributes that can be preserved and represents all original attributes; the core, however, is the set of all reduced common elements. The redundant attributes in the decision table are deleted first, and then the core attributes are found. The purpose of this is to use fewer attributes to classify the data and reduce the difficulty of analyzing the huge dataset without losing the complete information that the original data can provide, bringing more efficient and fast classification results to the construction of models.

To sum up, RST has been widely used in academia and practice recently such as for feature selection [68], and it has achieved excellent performance. In addition, regarding the numerical attribute data, this study has special interests and concerns; that is, it is necessary to discretize the data before performing rule derivation, and then to simplify the model, simplify the number of decision rules, and increase the accuracy rate of the mixed models. Therefore, in this study, we first discretized the data and then implemented the rule derivation. The LEM2 (Learning from Examples Module, version 2) [69] rule derivation algorithm is just more commonly used in the rule derivation method of the LERS (Learning from Examples based on Rough Set) system [70] in such a type. Therefore, this study uses LEM2 as one of the important components of the hybrid models and as the rule derivation algorithm of the main classification technology, after which we conducted a performance evaluation so as to construct a better LTCI hybrid model.

2.6. Rule Filtering Method

A model established using RST as the medium (or basis) has a big disadvantage: The set of decision rules it derives often contains a large number of rules [67], resulting in a complicated number of decision rules that are very difficult to understand. When some extraction rules are redundant or of “poor quality”, these extracted rules limit classification ability and also limit the decision-making simplification principle, causing decision-making troubles. Thus, we must perform some appropriate disposal measures and tasks. In particular, some rule filter algorithms are necessary [71], and they are often used to filter and reduce unnecessary or superfluous decision rules and lower the number of rule sets [72]. For example, the determination of the upper limit on the minimum number of rules can be used to remove some weak rules from the input rule set, and these rules may be redundant or “poor quality”.

Since this study uses two kinds of DT and RST as the rule extraction methods [73] for the main classification techniques, we know that the rule filter method has some specific advantages in the mixed model of this study; its necessity demonstrates its key importance. In addition to increasing the accuracy rate of the proposed models and reducing the number of generated rules, they also increase the model’s interpretation ability and simplify the decision-making process for creating the decision-making rule set.

2.7. Other Well-Known Classifier Techniques and Related Application Areas

To enhance the comparable performance of the hybrid model, this study applies some well-known classification techniques into the proposed models as performance evaluations and comparison functions. The techniques used include BN learning, LR, MLP, NB, RF, and SVM classifiers described as follows: (1) BN learning is a well-known classification algorithm in machine learning areas for the application of industry data analysis. We have also learned from the past that it has advantageous performance in different fields, such as vault settlement in urban tunnels [74]. (2) LR [32,75] is mainly used to discuss the relationship between the dependent and the independent variables, which is suitable for the situation of the binary category data of the dependent variable. For example, the two results (with and without insurance) that are suitable for predicting LTCI are addressed in a method of reaction variable statistical model analysis on learning from the literature, and its past classification performance is also very outstanding. (3) The MLP neural network is one of the more popular neural networks at present [29,76] and has three layers, the input layer, hidden layer, and output layer, uses supervised learning, and can handle nonlinear problems with good classification performance. This neural network has the following advantages: high model accuracy, nonlinear model construction, different types of input variables, wide range of application fields, and ambiguity of input and output variables allowed. (4) The NB [33,63] is a statistical classification method, and it can be expressed in the “icon model” to explain the relationship between each attribute. NB can be used to calculate the possible values, hoping to achieve a complete and reasonable speculation; therefore, it can be used to explore and predict the classification models. For example, the literature has designed a set of intrusion detection systems to further reduce the classification of characteristic selection. Simple NB classification can produce the best performance because this classifier has the advantages of simple use, fast operation speed, and good classification accuracy rate, and it is currently widely used in classification prediction for data exploration and analysis. (5) In the field of ML, RF [28] has a result of wide application scope and satisfactory performance, and it has gradually attracted the attention of academic circles. In addition to regression and classification work, it can be applied to the attribute reduction task and also has good results in handling omissions and abnormal values. It has the following advantages, especially applicable to classification problems: generating high classification accuracy, training and test speed, strong fault-tolerant capability, and handling high-dimensional characteristics data. (6) The SVM [34,77,78] is based on the core function of statistical learning theory for training and learning; following input of the training data, it can be used to find a maximum boundary that can separate the data for classification. It is a supervised learning method based on statistical theory. In addition to being widely used in the data analysis of statistical classification models for patterns, it can also be used as a tool for LR analysis. SVM has the following three advantages: (a) better generalized application ability; (b) better classification results; and (c) faster data training.

Based on the above instructions, the above six famous classifiers were selected as evaluation criteria for comparative studies of the advanced hybrid models in this study because of their outstanding performance in past research.

3. The Proposed AIHLCIM

This section mainly describes the proposed AIHLCIM, including the reasons for using it and its algorithm in detail, as follows:

3.1. Reasons for Using the Proposed Models

According to a report by the Economic Daily on 26 April 2018 (https://www.businessweekly.com.tw/business/blog/22593 accessed on 24 October 2021), although Taiwan’s insurance penetration ranks first in the world, the coverage rate of LTCI in Taiwan is only 2.04%; from this viewpoint, there is still a lot of room for improvement in LTCI coverage. In other words, the need of insurers for help defining the related characteristics of potential customers for LTCI indicates that data mining technology has important practical application value. After preliminary investigation on perspectives of exploration from the limited literature, we learned that most scholars in past research have focused on discussing property insurance issues (such as fire insurance, automobile insurance, etc.), but relatively few have focused on life insurance, especially in LTCI. Effectively mining the characteristics of potential customers is not only important, but also can bring substantial long-term benefits to the promotion of performance of insurance companies and insurers. However, there is currently a lack of applied research on this practical application analysis of insurance data. In addition to relying on salespersons to develop their annual performance marketing plans (such as introduction to old acquaintances or blind sales to strangers), insurance companies only rely on customer source guidance for business promotion, but technology–customer development education and training is not the only effective development strategy or tactical SOP method. Obviously, from the limited literature review, there is a serious lack of effective relevant technologies or predictive models for “LTCI” customer development. Therefore, if there is an effective potential customer development model, this is a good thing that will definitely attract great attention from academic circles and industry. This study thus came into being in such a meaningful context, engaged in a valuable and interesting research topic. Based on the motivation of helping insurance companies and insurers, this study builds a set of practical advanced intelligent hybrid models, and the characteristics of potential customers of LTCI are excavated from the insurance policy data of existing customers. Some applications of our research results are effectively providing insurers with help in developing potential customers, making the most efficient visits, speeding up and implementing new LTCI policies for the company, increasing training confidence and the application of auxiliary resources, reducing frustration, and creating the maximum benefits for insurers and insurance companies.

It becomes very important to engage in knowledge mining with excellent data mining techniques for transforming data into formalized knowledge capabilities by extracting hidden or undiscovered rule information from a large number of heterogeneous databases [79]. Therefore, how to combine a set of useful professional learning techniques to find out the characteristics of potential customers, avoid waste of resources, and verify the technology performance of the individual model and the advanced intelligent hybrid model are the focus and benefit of this research. The following subsections continue to describe the research methods adopted, and the details are introduced as follows.

3.2. The Proposed Models Used

This study proposes an advanced intelligent hybrid long-term care insurance model (called AIHLCIM) including four processing stages: data collection, data preprocessing, rule learning, and two-order in-depth performance evaluation. The constituent elements include attribute selection technology, data discretization methods, the decision tree C4.5, the rough set classifier LEM2, rule extraction and rule filters, relative comparison (or comparative studies; BN, LR, MLP, NB, RF, and SVM), ANOVA and Scheffe’s post hoc tests, etc. In order to verify performance with/without the use of the attribute selection method, with/without the use of data discretization technology, with/without the use of rule filtering technology, the difference between different rule derivation algorithms (C4.5 and LEM2), the combination differences of single models and advanced intelligent hybrid models were compared, and two-order depth grade verification was performed. A total of 16 (Models A-P) intelligent hybrid models are shown in Table 1 below, mainly to evaluate the performance of different component technologies applied to the LTCI experimental data set.

The processing flow of the 16 models includes 4 phases, 5 relative techniques, and 11 respective steps; due to limited space, it is shown in Figure 1 below. Practically, from our review of the literature, these advanced intelligent hybrid models have application innovation and importance in the field of long-term care 2.0 projects. Long-term care issues may seriously affect us in real-life practice; these proposed models thus help research investigations solve the professional problems of insurers and insurance company in a systematic way.

In this research, we briefly describe the institution of the four main processing phases of the AIHLCIM and its component combinations as follows:

- (1)

- Data collection phase: This consists of three sub-steps: (a) selection of insurance-source databases, (b) selection of basic attributes, and (c) collection of data. The key point is to first select the possible initial basic condition attributes through the relevant insurance and financially experienced knowledge of experts, then select the used condition attributes based on the relevant LTCI literature. Accordingly, supplemented by insurance experts’ knowledge of the unique characteristics of Taiwan’s insurance industry and LTCI experience, some conditional attributes are also selected; the sum of the above attributes is for all conditional attributes. Finally, the relevant attribute data are collected.

- (2)

- The data preprocessing phase: This includes three sub-steps: (a) format conversion, (b) selection of important attributes, and (c) data discretization. The key direction of this phase is to apply the necessary preprocessing procedures to the collected data, including (a) first removing multiple incorrect or noisy observations that may have arisen, (b) removing possible outlier examples, (c) converting the collected data set into the necessary format for the experiment, such as an EXCEL .csv file, to facilitate subsequent experimental operations, and (d) making a simple data normalization technique used for modeling all the ML-based methods for the benefits of a uniform format, good for follow-up experiments; then, attribute selection technology are used to remove irrelevant or redundant condition attributes. In order to further obtain the effective combination of important attributes, it is beneficial to reduce the complexity of the model (that is, reduce the data dimensions) and improve the predictive ability. Finally, the data discretization technique is applied to the numerical (digital) data of the key influencing condition attributes on the LTCI after the attributes are selected; the automatic discretization method is used to cut the individual attribute data into different interval values to leverage human natural language expressions (e.g., small, medium, and large) and enhance classifier performance.

- (3)

- The rule learning phase: This also consists of three sub-steps: (a) rule generation, (b) rule testing, and (c) rule filtering. Key tasks at this stage include first executing the extraction decision rule algorithm (such as C4.5 or LEM2), executing rule testing, and then performing the filtering decision rule work (only LEM2 requires it, because C4.5 has the rule prune function). The main detailed tasks are to discretize the numerical data of the selected important condition attributes, add whether the decision attribute is LTCI (coded Y: yes and N: no), and then put all the attribute data into DT and RST classifiers according to three types of data partitioning: 66% for training and 34% for testing (i.e., about 2:1), 75%/25% (3:1), and 80%/20% (4:1) sub-sets. The combined data are randomly disassembled, and the C4.5 and LEM2 algorithms are accordingly executed to generate rules. A meaningful decision rule set is thus extracted; concurrently, the number of rules of a set generated by the testing is obtained with the initial classification accuracy. Finally, the support threshold for LEM2 is separately set, the decision rules with too-low support are filtered out, and the disadvantage of too many rules in the rough set is overcome, thereby reducing the complexity of the decision rules and improving the classification quality.

- (4)

- The performance evaluation phase: This majorly includes two sub-steps: (a) the first stage involves a performance evaluation and (b) the second stage involves post-event statistical verification. The focus of the first stage is to randomly divide the experimental data set into the same proportion again, 66% as the training data sub-set and the remaining 34% as the testing data sub-set, so as to test the performance of the AIHLCIM and compare it with other different ML techniques. The comparison benchmarks are as follows: (a) internal comparison (for Models A-P, 16 models), (b) single model and intelligent hybrid model comparison (comparison of Models A-L vs. M-P), and (c) external comparison (comparison of optimal Models A-L vs. M-P accuracy rate). Following this, model performance is analyzed according to internal comparison, single model and intelligent hybrid model comparison, and external comparison according to self-defined evaluation criteria: (d) performance comparisons of the rough set and decision tree for properties such as accuracy rate, and (e) performance comparison of C4.5 and LEM2 for rule induction. The second stage involves (a) a one-way ANOVA analysis of variance and (b) a post hoc test of Schaeffer’s method to understand the empirical results of significant differences in the accuracy of the methods and the degree of difference between their groups. Afterwards, the results of differences are analyzed and the reasons are discussed, conclusions are made from the results, and the possible implications and possible major findings of the experimental results in terms practical management for the insurance industry are explained.

The following introductions detail the actual implementations and steps of the AIHLCIM algorithm with a real case study and research institute in detail, as follows:

3.2.1. Phase 1: Data Collection

- Step 1. Select the insurance database

First, we collected relevant insurance data (including LTCI) from potential databases, such as those from life insurance companies, as the experimental data set to verify and review the performance of the AIHLCIM proposed in this study.

- Step 2. Select basic attributes

We then selected attribute data from three aspects: (1) we first found out the relevant basic attributes from the data of a certain life insurance company, (2) then used variables used in the relevant literature as conditions; (3) in accordance with the professional experience of cooperative insurance experts in the relevant insurance industry, the selection of conditional attributes was added; the attributes selected by organizing these three directions were regarded as the basic condition attributes of this research. The preliminary acquisition of 31 original attributes includes gender, education, marriage, nature of work, whether the spouse is working, family salary structure, payment method, occupation, position, payer, location of the policyholder, main source of income, whether the three generations live together, the date when insurance policy was purchased for the first time, whether to repurchase investment insurance policy, whether to repurchase savings policy, whether to repurchase accident insurance policy, whether to pay renewal premiums, whether to refer customers, age, number of family members, approximate annual salary, the total number of insurance policies purchased in the past, the number of valid policies, the time in months since the first purchase, the insured amount of critical illness insurance, the total premiums of effective insurance policies for this year, the total insurance amount of property insurance, the total insurance amount of life insurance, the total sum of insured insurance, and total insurance premiums. After an interview and discussion with experts, 19 features of the above 31 original attributes remained. For the convenience of expression in the text for the reserved features, C1–C19 are used to represent the above 19 condition attributes, and D1 (class category code) represents a decision attribute (Y means LTCI and N means no LTCI); at the same time, this data set is named LTCI (long-term care insurance), and its detailed information is shown in Table 2.

- Step 3. Collect data

After the basic attributes were selected and established, we started to collect data from different sources. This part of the work was handled carefully so as not to cause any omissions or to affect the final empirical results due to data errors. Accordingly, we ran the analysis of descriptive statistics to calculate the relevant information of attributes, such as maximum value (max), minimum value (min), mean value (mean), and standard deviation, after collecting. It is helpful to understand the important information of each attribute’s observation value.

3.2.2. Phase 2: Data Preprocessing

- Step 4. Format conversion

Data preprocessing plays a very important role in data mining work [49], as real-world data may have outliers (attributes have exceptional values), noise (such as garbled characters or data errors), or inconsistent cases (such as inconsistent codes or names, or abnormal values), resulting in errors that the data cannot match with; all these serious problems show the necessity and importance of data preprocessing work. Therefore, we needed to remove or correct outliers, noises, and inconsistencies. Then, we converted the processed data mentioned above and used simple normalization jobs, such as making a uniform data length for each attribute and coding attributes, for parsing the proposed methods into the same format (such as an EXCEL.csv). Afterwards, we performed attribute coding for the benefits of a unified and identified formatting, which also facilitated subsequent experimental operations and procedures to be carried out more simply and efficiently through the use of coded data. Specifically, all these numeric data used were in the same unit of new Taiwan dollars (abbreviated as NT$), applicable for the following experiments. Importantly, the decision attribute was coded according to expert opinions, and the encoded attributes C1–C19 and D1 were identified and determined.

- Step 5. Select important attributes

We learned from the literature [79] that attribute selection can effectively reduce the data dimensions. This sub-step focuses on the application of the attribute selection method and completely deletes irrelevant (meaningless) or redundant condition attributes to achieve the purpose of selecting important attributes, prevent unnecessary attributes from interfering with experimental results, and increase the performance advantages of advanced intelligent hybrid models. Therefore, this sub-step was only executed in Models A-H (please refer to Table 1 above) and was not executed in the other models.

- Step 6. Perform data discretization

According to the literature [80], the data discretization method is not only helpful for the extraction of the decision rules set and can be explained in human natural language, but also helps to improve the accuracy of the classifier. Data discretization is divided into two types: expert discretization and automatic discretization. Therefore, this step focuses on using different discretization techniques to discretize the important conditional attributes obtained in the previous steps (only for numerical attributes). For example, if the discrete results are represented by L1, L2, and L3, indicating the upper, middle, and lower semantic values, respectively, the natural language of these data can be fully expressed, and then the model can be interpreted more naturally. This step was executed for Models A-D and Models I-L (please see Table 1) using expert and automatic discretization, respectively.

- Step 6-1. Execute expert discretization

Using the opinions of experts in the insurance field, the decision-making attribute was divided into two categories: Y and N, which represent “with LTCI” and “without LTCI”, respectively, to facilitate the understanding of interpretable results produced by sets of decision rules.

- Step 6-2. Execute automatic discretization

In this sub-step, we adopted the automatic discretization technique to apply data discretization to the selected important numerical condition attributes mentioned above to automatically cut the attributes into different interval values to represent different natural semantic values.

3.2.3. Phase 3: Rule Learning

- Step 7. Rule generation

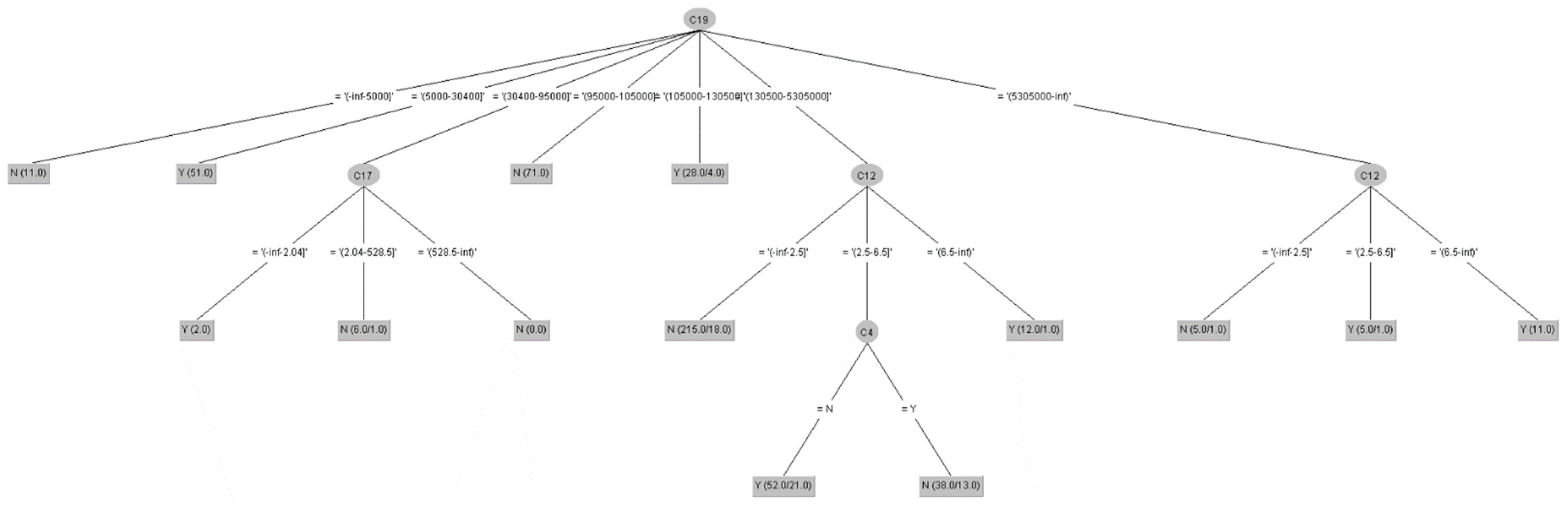

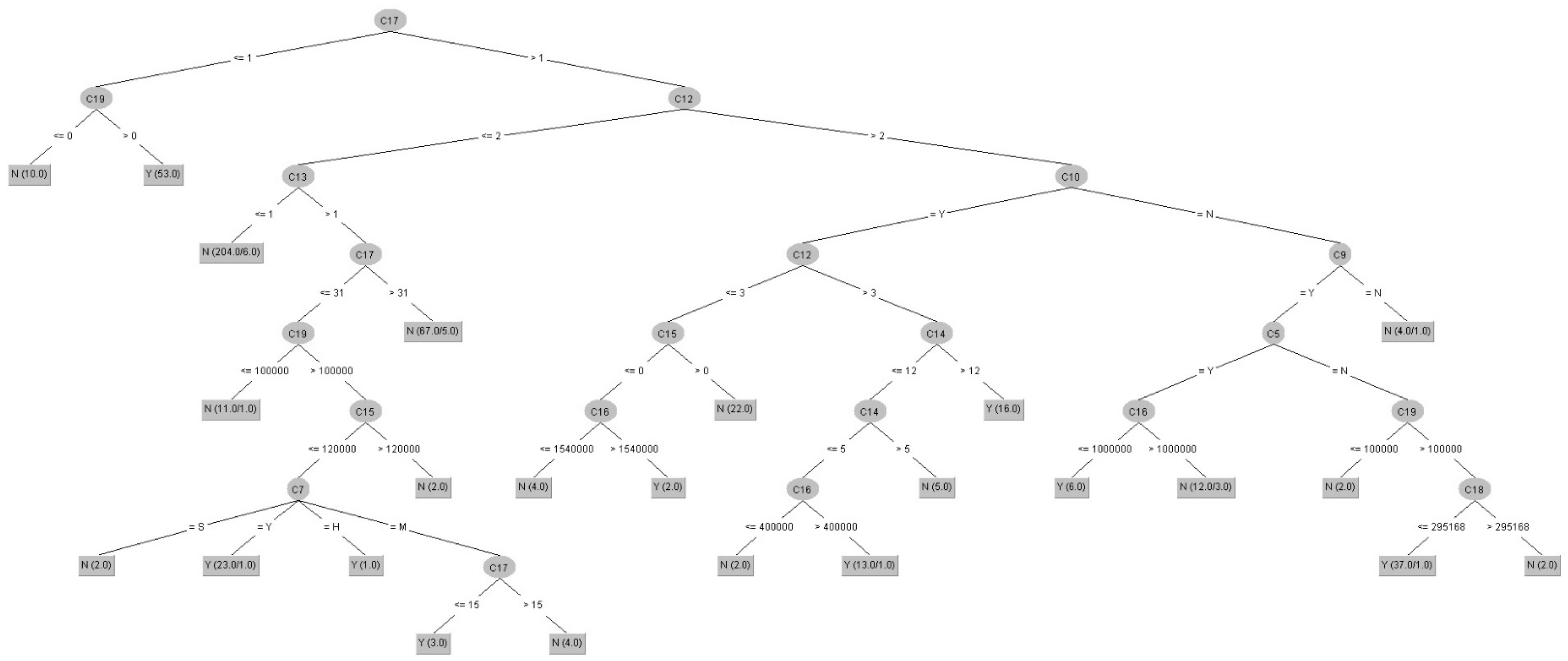

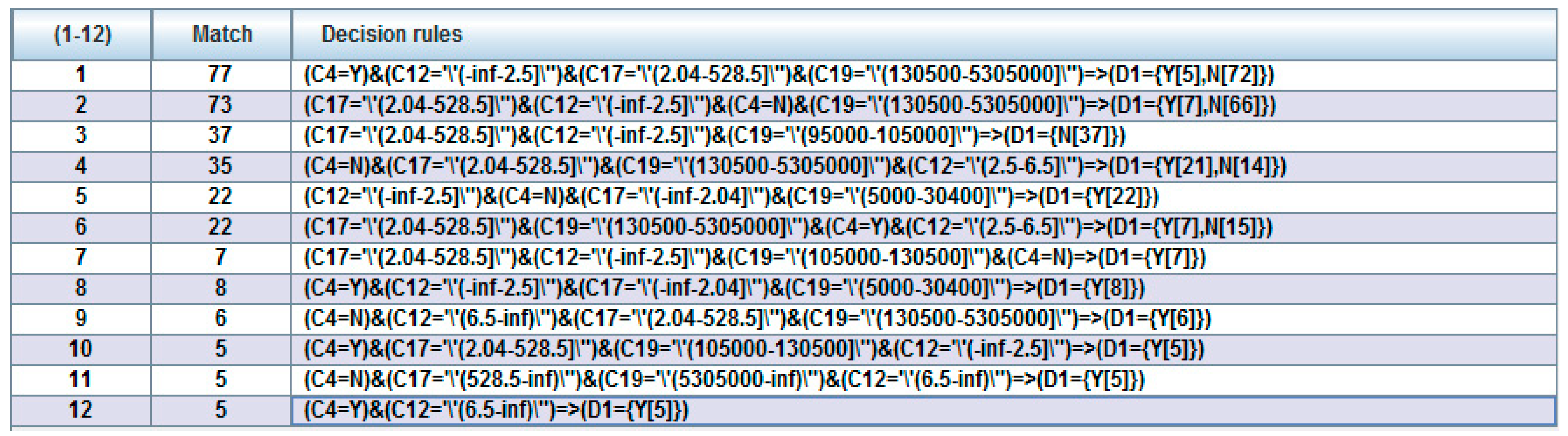

In this sub-step, we executed the rule derivation algorithms of DT-C4.5 (Models B, F, J, N) and RST-LEM2 (Models C, D, G, H, K, L, O, P), since they have the advantage of being able to derive a minimal set of rules to represent the original data set without changing the structure of the original data and without being affected by the absence of certain observations; the resulting of “If…Then” general decision rule set can be used to discover the unknown information hidden in the data, and these have become two of the most commonly used decision rule derivation algorithms. In addition, the algorithms mentioned above [69] have the advantage of being able to directly derive a decision rule set from a symbolic or numerical attribute of the data set. Therefore, in this study, we used them to randomly cut the new experimental data set generated in the previous step (including the important condition attributes and decision attributes after the discretization of the data) into 66% training data set and 34% testing data set, the minimum set of decision-making rules was extracted, and these rules of each category (two categories in total) were deduced as the basis for predicting the insurance status of LTCI in the future. The generation of a decision rule set is jointly established by important condition attributes and decision attributes, similar to the general rules of “If conditions then decisions.” Moreover, the ratios 75%/25% (3:1) and 80%/20% (4:1) of training/testing data were run again for this step.

An example is expressed as follows:

Rule 1: “If (C4 is high) & (C14 is high) Then Class = Y”, interpreted in natural language as: “If C4 is a high value (−0.2252–∞) and C14 is a high value (0.545–∞)…, then the customer (subject) is a person with LTCI.” Such a structured knowledge base system enables stakeholders to easily interpret the true meaning of the decision-making rules, and then we can calculate the strength of the rules based on the number of supports each rule received.

- Step 8. Rule testing

Using the above initially structured decision-making rule set, and then using the remaining 33% of the testing data set to test the performance of the above listed classifiers, the original classification accuracy rate of each classifier was achieved.

- Step 9. Rule filtering

This sub-step includes two possible situations; one is to execute the rule filter (Models C, G, K, O), and the other is to skip it and not execute it. The RST algorithm has the disadvantage of generating too many rules, and it increases the complexity of the rule set [81]. Therefore, in order to solve this defect, rule filtering techniques are important for effectively improving the quality of the rules [72]. In this sub-step, we first set a threshold based on the support number of the rule (for example, set the number of supports to be less than or equal to 1 (i.e., ≤1), because these decision rules represent that at most only one instance conforms to this rule), and then set the threshold value of the following rules for deletion. This proactive approach is based on the following reasons: (1) When more rules are generated, it means that more conditions must be considered, which increases the complexity of the advanced intelligent hybrid model. (2) When there are too many rules with low support, it means that the explanatory power of the predicted results from these rules is not high. (3) The quality of prediction can be improved through the regular filtering method, and the classification accuracy rate can be further increased. The above focus is on reducing the number of rules and providing the smallest subset with the same function or even better, giving decision makers a simple, easy, and meaningful knowledge-based decision rule set as a reference for future decision making for interested parties.

3.2.4. Phase 4: Two-Order in-Depth Performance Evaluation

- Step 10. The first-order performance evaluation

The performance of the AIHLCIM was addressed for the first-order verification. The evaluation criteria used include the accuracy rate (the higher the better), the number of important attributes (the less the better), the number of decision-making rules (the less the better), and the standard deviation of accuracy rate (the smaller the better). This sub-step is divided into the following three items to execute: (1) Perform internal comparison: Compare the Models A-P (16 models) of the proposed AIHLCIM and evaluate the effects of their individual constituent elements, including (a) Models A-H vs. I-P for first-order verification with or without feature selection differences in methods; (b) Models A-D vs. E-H and Models I-L vs. M-P for first-order verification with or without differences in data discretization method, respectively; and (c) Models C vs. D, G vs. H, K vs. L, and N vs. O to verify whether there is a difference in the use of the rule filter method for RST classifiers. (2) Perform model comparison between single models and hybrid models: Use Models A-L vs. M-P to verify the model difference between the single model and hybrid model (that is, to review the conclusion of the literature: the hybrid model is better than the single model in terms of classification accuracy). (3) Execute external comparison: This refers to comparing the internal comparison of the previous item on the highest accuracy rate with the ML techniques commonly used in the literature for forecasting LTCI (a total of six types: BN, LR, MLP, NB, RF, and SVM, which can be regarded as external classifiers in this study) compared with DT and RST for result comparison and difference analysis. Therefore, in order to verify the performance of the AIHLCIM in the first-order verification, the data need to be randomly divided into two sub-experimental data sets of 66%/34% (training/testing) again; the 66% training data set was also used to generate the classification decision rule set, and then the classification accuracy was evaluated using the 34% testing data set. After performing this random repetition 10 times, the average accuracy rate, the average number of decision rules, and the standard deviation for equivalent performance index between the average accuracy rate and the number of decision rules were calculated. Afterwards, we compared the performance with the above eight classifiers; finally, we found the best classifier among the above three different comparison results and analyzed and summarized the experimental results. Furthermore, based on the limited literature, although general evaluation indicators, such as the classification accuracy, area under ROC (AUC), precision rate, recall rate, and F1-score [82] are commonly used to measure the performance of classification models constructed for further verification, they have different evaluation directions with different performance objectives. Thus, if there are no special requirements for a particular class, we can directly use the indicator of the classification accuracy as a representative to evaluate the built model, as accurateness is the evaluation of performance from the perspective of the overall model, and it has great value for measuring the overall evaluation results of models. Importantly, it is emphasized in this research that only classification accuracy was used for an indicator of performance evaluation to assess the performance of models from the view of the overall model.

- Step 11. The second-order statistical test