Risks, Volume 5, Issue 2 (June 2017) – 12 articles

Cover Story (view full-size image):

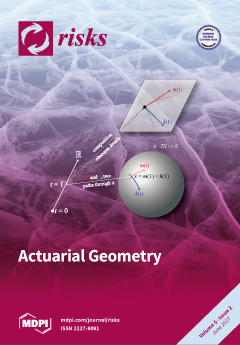

Actuarial Geometry studies how the shape of an aggregate loss distribution changes as expected loss volume changes. The theory of Markov processes implies Levy processes are straight lines even though their distribution changes shape as expected losses increase. In contrast, an asset-return model retains a constant shape but represents a curved path. The difference is significant in the theory of risk measures and capital allocation, which are based on marginal changes in loss volume. In the figure the Levy process (red) is a great circle straight line whereas the asset model (blue) is a curved path. Growth along the two paths results in different measures of marginal risk (top right). View this paper

- Issues are regarded as officially published after their release is announced to the table of contents alert mailing list.

- You may sign up for e-mail alerts to receive table of contents of newly released issues.

- PDF is the official format for papers published in both, html and pdf forms. To view the papers in pdf format, click on the "PDF Full-text" link, and use the free Adobe Reader to open them.

Previous Issue

Next Issue