- Article

External Macroeconomic Variables and Stock Returns: Evidence from Conventional and Islamic Indices

- Muhammad Hanif

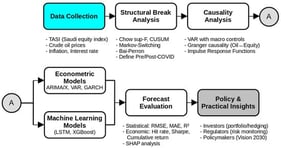

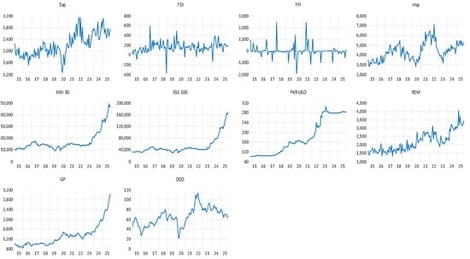

The study documents the impact of the external sector on movements of the Pakistan Stock Exchange (PSX), covering conventional and Islamic indices. Selected variables include international trade, foreign investment, remittances, oil, gold, and currency markets, as well as the KSE-100 and KMI-30 indices. The sample period covers the latest 130 months, from 2015/01 to 2025/10. Results are documented through descriptive statistics, pairwise correlations, and OLS regression. Stability of coefficients during the review period is checked by calculating BTC-Var and switching Var. Outstanding momentum is evident in market indices (in the final phase), accompanied by growth in remittances, while the national currency has experienced an alarming depreciation. The combined impact of the external sector is not in the higher range for either index (adjusted R-square values are low). A group of four variables (remittances, oil, gold, and currency markets) was significant for the conventional index, while a group of three variables (oil, gold, and currency markets) was significant for the Islamic index. All significant variables contribute positively to stock index movements, except the exchange rate. BTC-Var and switching var suggest instability of relationships and regime-dependent var dynamics. The findings are beneficial for managers and investors in predicting index movements and portfolio diversification, as well as for relevant authorities in making policy decisions that promote prudent exchange-rate management and facilitate remittances. To the best of the author’s knowledge, this study is among the few that jointly examine the impact of external-sector variables on stock market movements.

2 March 2026

![Structure of the LSTM Architecture. Arrows indicate the direction of information flow between the input layer, gates, cell state, and output. Source: [14].](https://mdpi-res.com/cdn-cgi/image/w=281,h=192/https://mdpi-res.com/forecasting/forecasting-08-00021/article_deploy/html/images/forecasting-08-00021-g001-550.jpg)