In this paper, the filtered input and output indicators were analyzed by the data envelope analysis software DEAP2.1. DEA and Malmquist methods were used to calculate and analyze the efficiency values of 65 listed retail enterprises in 2016 and 2020. At the same time, 45 sample listed enterprises that did not use the new retail model and 20 sample listed enterprises that used the new retail model were separately calculated and analyzed. In this way, the differences and impact of operating efficiency before and after the transformation were analyzed from both horizontal and vertical perspectives.

4.1. Efficiency Positive Results Based on DEA Method

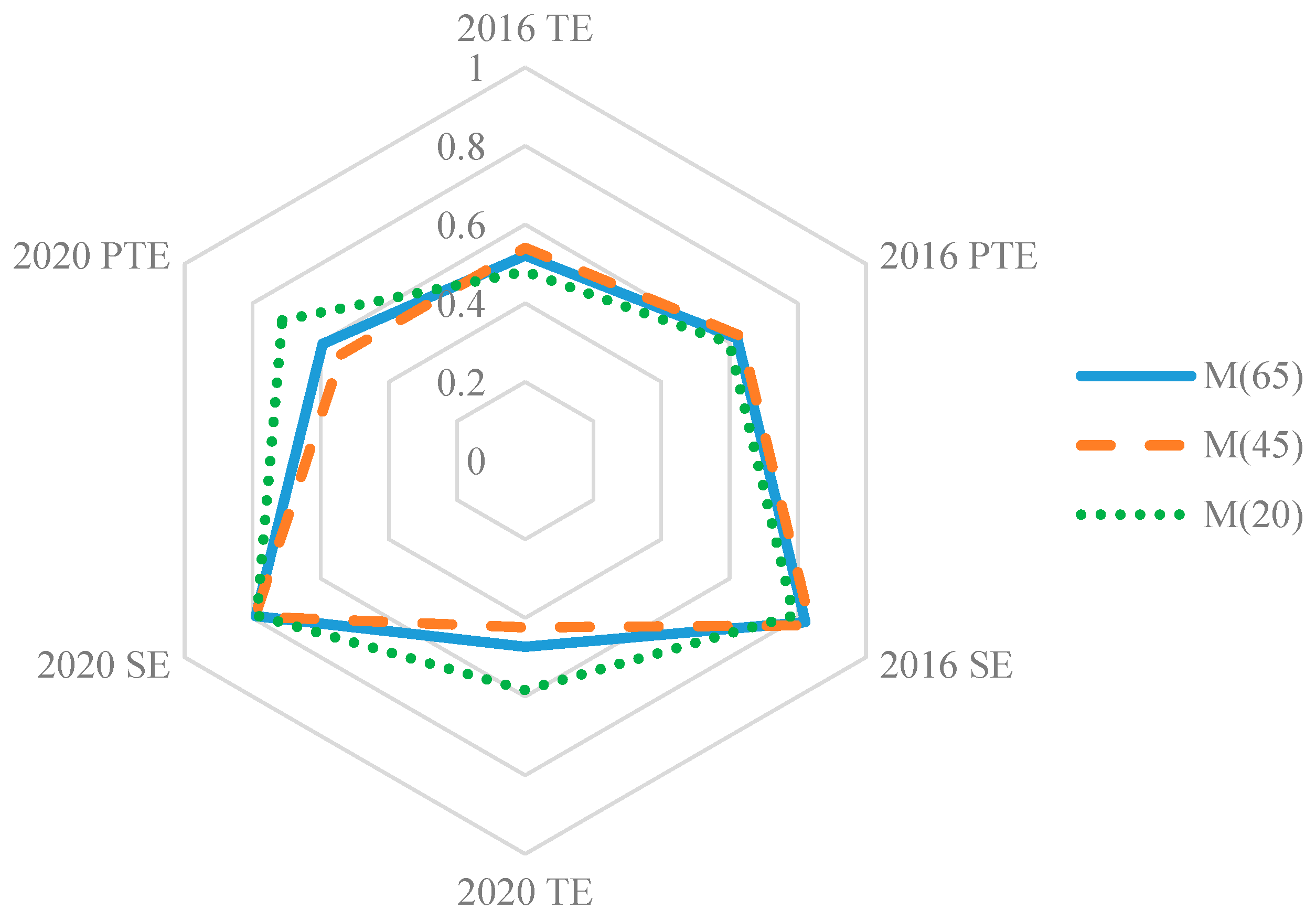

In the DEA method, the input–output data of technical efficiency (TE), pure TE (PTE), and scale efficiency (SE) were calculated using the C

2R model and BC

2 model (see

Figure 1).

Table 3 shows that the overall operating efficiency of the listed retail enterprises in China in 2016 and 2020 is not high, among which the average technical efficiency in 2016 and 2020 was 0.522 and 0.473, respectively, which is a large gap in terms of the effectiveness of DEA. This is also consistent with the operating situation of the entire retail industry in recent years, which reflects increases in cost and expenditure, a decline in operating profit, and an increasing burden on enterprises. In addition, the average efficiency in 2020 showed a large decrease compared with 2016 (down by nearly 5%), indicating that it has become urgent to address the declining efficiency and sustainable operation of retail enterprises. The suspension of some Chinese retail enterprises during the COVID-19 pandemic is another important reason.

In 2020, the average efficiency of 45 traditional retail enterprises that did not use the new retail model was 0.424, down 0.117 from the average efficiency of 0.541 in 2016. The average efficiency of 45 enterprises in 2020 was 0.424, which was lower than the overall efficiency of 65. This indicates that the business performance of traditional retail enterprises was worse. The average efficiency of the 20 new retail enterprises using the new retail model was 0.583, significantly higher than the average efficiency of 65 enterprises (0.473) and of 45 enterprises (0.424). Compared with 2016 and 2020, the enterprise efficiency improved from 0.481 to 0.583. This indicates that enterprises adopting the transformation and exploration of the new retail model performed well, and their operating efficiency improved.

At the same time, in order to compare the advantages of the new retail enterprises, the average efficiency of 45 enterprises not using the new retail model and 20 enterprises using the new retail model was calculated.

Efficiency measurement results of 45 companies that did not use the new retail model as shown in

Appendix A Table A5.

As seen from the individual company efficiency changes of 45 sample enterprises, the top three enterprises in the efficiency value in 2020 were Doctor Glass, Zhejiang Winter, and Liqun Shares. The last three were the supply and marketing market, agricultural products, and Zhongbai Group. From 2016 to 2020, 31 companies saw their technology efficiency decline, and about 69% of traditional retail companies had poor operating efficiency. Of the 31 declining enterprises, in 24 the reduction in technical efficiency was attributed to a decrease in pure technical efficiency, accounting for 77.4%. The decline in technical efficiency of the other seven listed enterprises was attributed to a reduction in scale efficiency, accounting for 22.6%. This indicates that pure technical efficiency is the main reason for the decline in operating efficiency of traditional retail enterprises. From 2016 to 2020, there were only 12 enterprises with an upward trend of technical efficiency, accounting for 27%. The increase in pure technical efficiency caused a 66.7% efficiency increase for these 12 listed enterprises, and the remaining 33.3% was caused by scale efficiency, which further demonstrates the importance of pure technical efficiency.

Combined with the overall and individual efficiency changes, this shows that, at present, the traditional business model relying on manpower, business area, and “commodity delivery and real estate expansion” is increasingly unable to meet the needs of the business environment. Homogeneous goods will only lead to market saturation, making the scale efficiency of enterprises decrease. Therefore, on the one hand, enterprises must change their management concept, and further optimize the internal and external management level by, for example, flat operation, reducing the operation cycle, and improving the quality of management. On the other hand, companies need to respect the technological content, and practical value of their products: big data, cloud computing, and other technologies help stores to realize intelligent production and diversified operations improve the input and output efficiency of enterprises through a series of measures to improve management and technology.

The efficiency measurement results of 20 enterprises using the new retail model are shown in

Appendix A Table A6.

As can be seen from the empirical results of 20 enterprises, the average technical efficiency of enterprises using the new retail model was 0.583. The mean value of pure technical efficiency and scale efficiency was 0.713 and 0.788, respectively, which are greater than the average efficiency of the sample enterprises in 2016. In addition, the average efficiency of 20 enterprises using the new retail model was 0.583, much higher than the average efficiency of 45 traditional retail models (0.424), and the average efficiency of 65 retail enterprises was 0.473, so the operating efficiency was significantly improved.

As can be seen from the 20 sampled companies with efficiency changes, the technical efficiency of 14 out of the 20 listed companies improved after using the new retail model, accounting for 70% of the sample listed enterprises, such as Yonghui Supermarket, Nanjing Xinbai, Sanjiang Shopping, etc. The list includes Maoye Commercial, Ewushang A, and Zhejiang China Commodities City Group, with the pure technical efficiency enhanced in 2020. The pure technical efficiency was 1, indicating that the enterprise improved management and technology applications within a year, which significantly contributed to the technical efficiency. After the introduction of the new retail model, the technical efficiency of Sanjiang Shopping, Nanjing Xinbai, Fujian Dongbai Group, and Shanghai New World improved significantly compared with 2016, with an efficiency increase of more than 14%, indicating that they performed well in the exploration of the new retail model. Their business status is developing along a good trend. Suning Commerce, Xujiahui, Rainbow Holdings, and Bailian Holdings enterprises reduced their efficiency after using the new retail model, but the overall decrease was not significant.

The operating efficiency of enterprises is affected by pure technical efficiency to varying degrees, indicating that there may be some restrictions and obstacles in management and technology preventing the new retail model’s implementation. In the early stage of the new business model, a change in traditional business projects requires significant human resources, material resources, and financial resources in the early stages, and it is not easy to obtain the expected high returns in a short period. At the same time, due to the lack of a mature reform mode and precise strategic planning in the internal management of the enterprise, the efficiency value of the new retail model may be reduced.

4.2. Efficiency Changes Based on the Malmquist Index Method

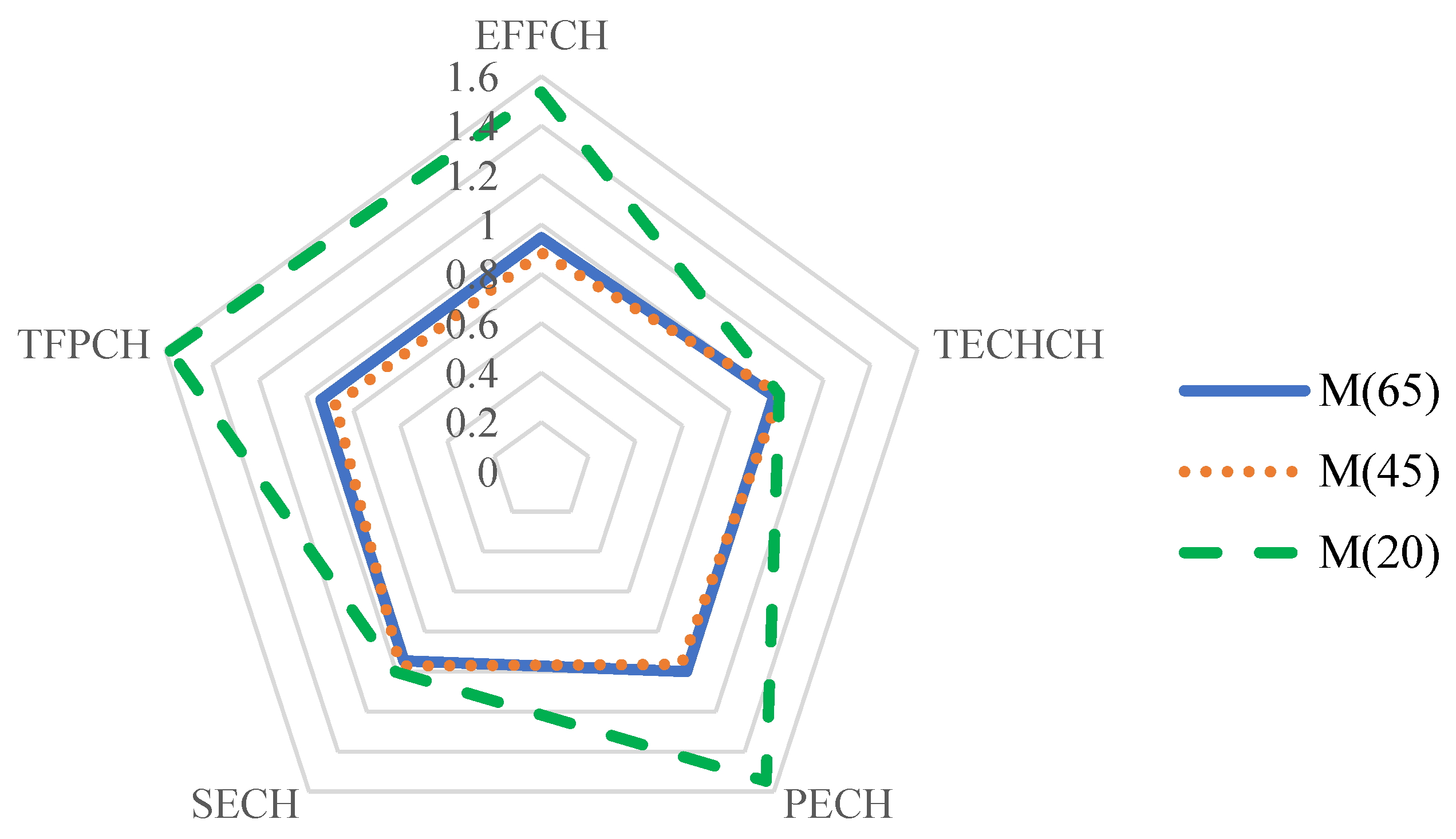

The DEA method above measures and analyzes the efficiency of each listed sample enterprise from the static efficiency level, but cannot dynamically analyze the specific progress and regression of enterprise efficiency. Therefore, the Malmquist index continues to be used to measure and analyze the change in enterprise efficiency. It enables us to quantify changes in enterprise technical efficiency (EFFCH), technological progress (TECHCH), pure technical efficiency (PECH), scale efficiency (SECH), and total factor productivity (TFPCH). The Malmquist method was used to obtain the change value of total factor productivity and its decomposition index of 65 enterprises. Meanwhile, the mean change values of 45 sample enterprises that did not apply the new retail model, and the mean change values of 20 sample enterprises that applied the new retail mode, are shown in

Figure 2.

As can be seen from the calculation results in

Table 4, the mean change in total factor productivity of 65 Chinese enterprises from 2016 to 2020 was 0.938, an overall decrease of 0.62%. From the perspective of decomposition indicators, both technological efficiency and technological progress change indicators show a declining trend, among which the decrease in scale efficiency mainly causes a decrease in technological efficiency. This suggests that in the Chinese retail market, after struggling to realize the importance of the transformation, many enterprises began to close poor-performing stores. Paying less attention to the supply chain system and third-party payment technology, but not overall investment, management, and technology, it is still necessary to strengthen innovation, especially in terms of big data management, intelligent operations, and other aspects, to further appreciate “people, goods, and field”.

The mean change in total factor productivity of 45 traditional retail enterprises that did not use the new retail model was only 0.876, a decrease of 12.4%, showing an apparent downward trend. According to the Malmquist decomposition index, although the change index of technological progress was greater than 1, the total factor productivity did not improve. The main reason for the decrease is a decrease in technical efficiency of 11.4%. Further decomposition of technical efficiency shows that the inefficiency was mainly reflected in the substantial reduction of pure technical efficiency, indicating that traditional retail enterprises that have not explored new retail models have a small investment range in technology and management. Therefore, their operating efficiency has not been effectively improved.

From 2016 to 2020, the mean change in total factor productivity of the 20 listed retail enterprises using the new retail model was 1.578, an increase of 57.8%. The overall operation status of the sample listed retail enterprises improved and developed rapidly after the new retail model was applied. It can be observed from the Malmquist decomposition index that the change indexes of technological progress and technological efficiency were both greater than 1, and the mean change of technological efficiency was 1.536, an increase of more than 50%. Further decomposition of technical efficiency indicates that, when the scale efficiency remains basically unchanged, the growth of pure technical efficiency index directly determines the significant improvement of the technical efficiency index. Twenty listed enterprises using the new retail model actively utilized technologies such as facial recognition, intelligent terminals, mobile payment, etc. This allowed them to improve the store layout, commodity supply, and overall shopping experience, which made an outstanding contribution to total factor productivity.

Efficiency changes results of 45 companies that did not use the new retail model are shown in

Appendix A Table A7.

According to the empirical results of 45 sample enterprises, there were 9 enterprises with a total factor productivity greater than 1 from 2016 to 2020, accounting for 20% of the sample enterprises. There were 35 enterprises with a total factor productivity of less than 1, accounting for 77.8% of the sample enterprises. Among the 35 enterprises with a total factor productivity less than 1, the decrease in total factor productivity of 28 enterprises was caused by a decrease in the technical efficiency index. Further subdividing technical efficiency, it can be seen that the reduction in efficiency index of 20 enterprises was attributed to a reduction in pure technical efficiency, and the reduction in efficiency index of the other five enterprises was attributed to a reduction in scale efficiency index. At the same time, the reduction of total factor productivity of 10 enterprises was caused by a reduction in the technological progress index.

To sum up: The total factor productivity of the 45 enterprises that did not use the new retail mode declined from 2016 to 2020. Although traditional retail enterprises achieved better technological progress results in the same period, productivity did not improve the total factor. It is still necessary to further improve the technology and management level. Enterprises should pay particular attention to the role of big data in future operations and management, and try out the new retail model. Enterprises should also strengthen internal and external management, coordinate the relationship between upstream and downstream suppliers and customers, and realize the improvement of operational efficiency.

The efficiency change results of 20 enterprises using the new retail model are shown in

Appendix A Table A8.

According to the empirical results of 20 sample enterprises, there were 14 enterprises with a total factor productivity greater than 1 from 2016 to 2020 (accounting for 70% of the sample enterprises), and only six enterprises with a total factor productivity less than 1. This indicates that sample enterprises transforming from the traditional retail mode to the new retail mode performed well on the whole, and total factor productivity improved. Among the 14 enterprises with an improvement in total factor productivity, the improvement in total factor productivity of Baida Group, Shanghai Join Buy, and Zhejiang China Commodities City Group could be attributed to technological progress. After the application of the new retail model, these three enterprises showed outstanding performance in terms of the improvement in technical efficiency, and made remarkable achievements in the application of new retail technology.

The total factor productivity change value in the top three enterprises were Fujian Dongbai Group, Kunming Sinobright Group (5I5J Holding Group) and Shanghai New World. Compared with the previous year’s total factor productivity, five enterprises (Shanghai Join Buy, Maoye Business, Sanjiang Supermarket Shopping, Yong Hui and Zhejiang China Commodities City Group) increased rapidly in technical efficiency, with an increase of more than 40%, especially for e-commerce companies and online business development. The level of management technology saw great progress, with timely adjustment of production scale and good prospects for development. At the same time, although the change value of the total factor productivity of traditional department stores Xujiahui and Nanjing Xinbai was less than 1, they were both greater than 0.9, indicating that the operation of physical stores has declined in recent years. Still, they made positive adjustments after the new retail layout, and the overall performance was developing in a good direction. Enterprises must invest a lot of money early on in switching to a new retail model. After the transformation, it takes time to find the management method most suitable for the enterprise. In the early stage of applying the new retail model, these enterprises will face problems such as inappropriate input–output distribution, improper management means to adapt to the new model, and immature application of new technology. Enterprises should improve the above aspects to improve efficiency.

{kind=link}

{kind=link}