Hybrid CUSUM Change Point Test for Time Series with Time-Varying Volatilities Based on Support Vector Regression

Abstract

:1. Introduction

2. Support Vector Regression for the GARCH Model

- Step 1. Prescribe the points to be evaluated within this space, then divide the given time series into training and validation time series of size n and , respectively. This preliminary procedure is required for the subsequent task of validating the fitted SVR-GARCH model, which determines the best tuning parameter sets.

- Step 2. Note that the conditional variance of (9) is unknown. As a remedy, replace with the initial estimates , which plays the role of a proxy of . The estimate is based on the training time series using a moving average method (Niemira [43]):where m is a positive integer. When t is smaller than m, is computed as an average of the first to the tth squares of observations, i.e., when .

- Step 3. Given a set of tuning parameters, we estimate g in (1) with using the SVR with replaced by . Then, the estimate of is obtained as:

- Step 4. Applying the estimated SVR-GARCH model and using the same proxy formula as in Step 2 for the validation time series, the mean absolute error (MAE) is computed as follows:The MAE escalates the robustness of the model against outliers and therefore provides more flexibility in a model fitting than the root mean squared error.

- Step 5. Repeat Steps 2 to 4 for all the tuning parameter sets selected in Step 1 and choose the combination that minimizes the MAE. Then, perform Steps 2 and 3 using the training and validation time series together to determine the final model, which is used in obtaining the residuals.

3. Hybrid CUSUM Test via the SVR-GARCH Model

4. Simulation Results

- Step 1. Generate a time series of length from a prescribed GARCH model.

- Step 2. Follow the estimation scheme described in Section 3 with . In this procedure, the first 0.7n number of time series constitute the training set, and the following number of time series constitute the validation set.

- Step 3. Conduct the CUSUM of squares test described in Section 3. We utilize the remaining n number of time series as a testing set.

- Step 4. Repeat Steps 1 to 3 1000 times iteratively, and then, compute the empirical sizes and powers.

- GARCH(1,1) model:

- AGARCH(1,1) model:

- GJR-GARCH(1,1) model:

- TGARCH(1,1) model:

- Log-linear GARCH(1,1) model (a specific variation of the EGARCH() model):

- GARCH model: ;

- AGARCH model: ;

- GJR-GARCH model: ;

- TGARCH model: ;

- log-linear GARCH model: .

- GARCH(1,1) changes to log-linear GARCH(1,1);

- log-linear GARCH(1,1) changes to GARCH(1,1);

- TGARCH(1,1) changes to AGARCH(1,1);

- AGARCH(1,1) changes to GJR-GARCH(1,1).

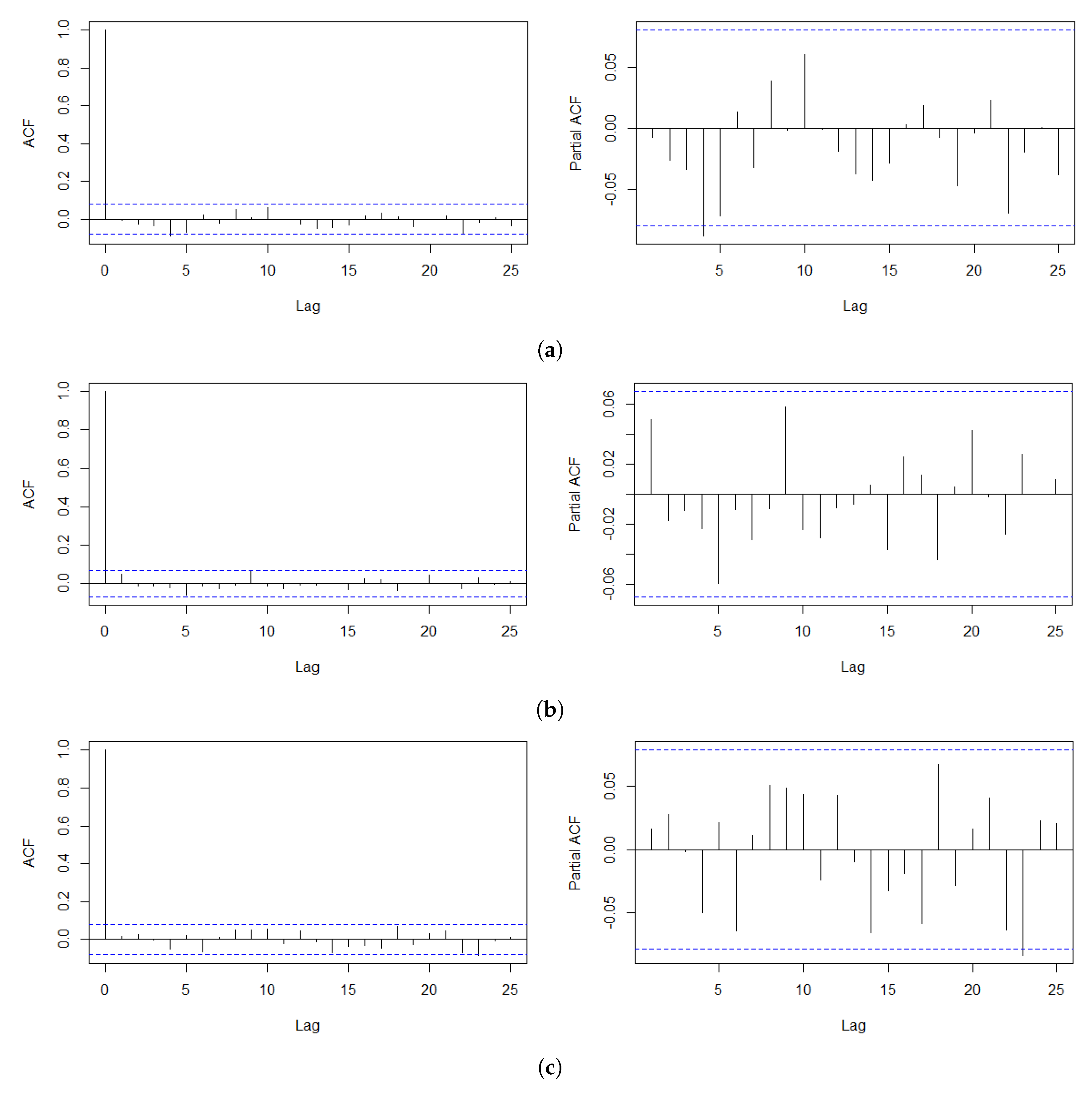

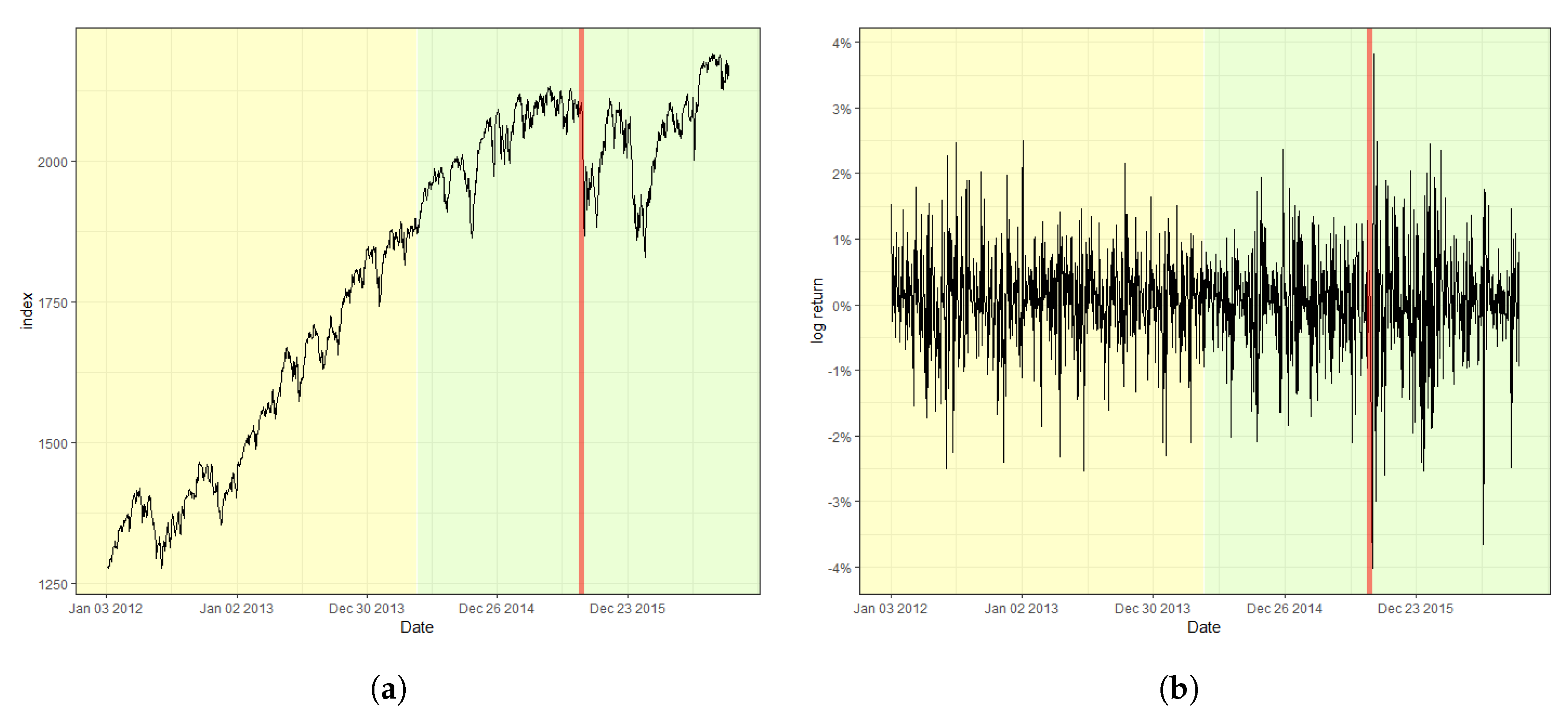

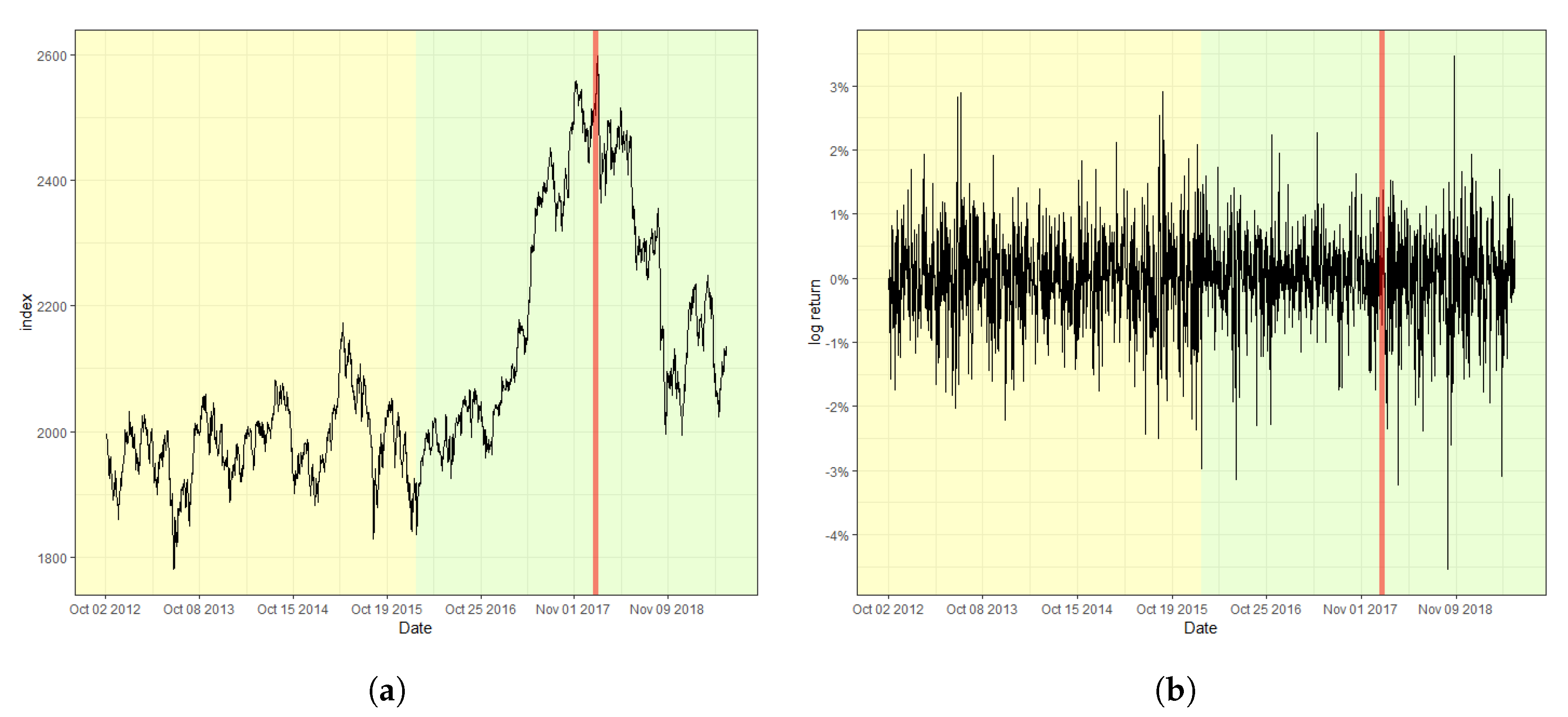

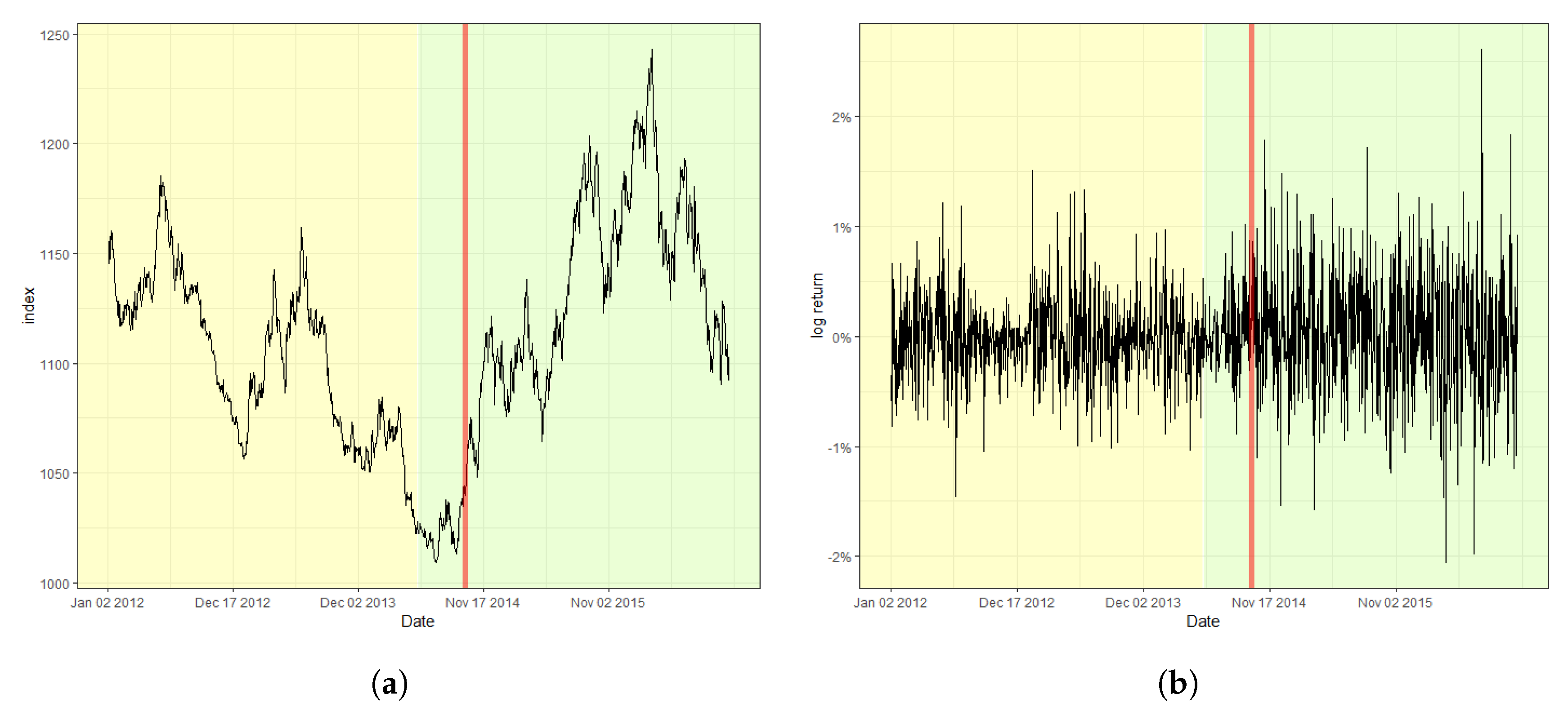

5. Real Data Analysis

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Abbreviations

| CUSUM | cumulative sum |

| SVR | support vector regression |

| SVM | support vector machine |

| GARCH | generalized autoregressive conditionally heteroscedastic |

| EGARCH | exponential GARCH |

| GJR-GARCH | Glosten, Jagannathan, and Runkle-GARCH |

| TGARCH | threshold GARCH |

| APARCH | asymmetric power ARCH |

| NN | neural network |

| ARMA | autoregressive and moving average |

| QMLE | quasi-maximum likelihood estimator |

| KOSPI | Korea Composite Stock Price Index |

| KRW | Korean Won |

| VaR | value at risk |

| ES | expected shortfall |

References

- Engle, R.F. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 1982, 50, 987–1007. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef] [Green Version]

- Engle, R.F. Stock volatility and the crash of ’87: Discussion. Rev. Financ. Stud. 1990, 3, 103–106. [Google Scholar] [CrossRef]

- Nelson, D.B. Stationarity and persistence in the GARCH (1, 1) model. Econom. Theory 1990, 6, 318–334. [Google Scholar] [CrossRef]

- Zakoïan, J.M. Threshold heteroskedastic models. J. Econ. Dynamic. Control 1994, 18, 931–955. [Google Scholar] [CrossRef]

- Glosten, L.R.; Jagannathan, R.; Runkle, D.E. On the relation between the expected value and the volatility of the nominal excess return on stocks. J. Financ. 1993, 48, 1779–1801. [Google Scholar] [CrossRef]

- Ding, Z.; Granger, C.W.; Engle, R.F. A long memory property of stock market returns and a new model. J. Emp. Financ. 1993, 1, 83–106. [Google Scholar] [CrossRef]

- Carrasco, M.; Chen, X. Mixing and moment properties of various GARCH and stochastic volatility models. Econ. Theory 2002, 18, 17–39. [Google Scholar] [CrossRef]

- Fernandez-Rodriguez, F.; Gonzalez-Martel, C.; Sosvilla-Rivero, S. On the profitability of technical trading rules based on artificial neural networks: Evidence from the Madrid stock market. Econ. Lett. 2000, 69, 89–94. [Google Scholar] [CrossRef]

- Cao, L.; Tay, F. Financial forecasting using support vector machines. Neural Comp. Appl. 2001, 10, 184–192. [Google Scholar] [CrossRef]

- Pérez-Cruz, F.; Afonso-Rodriguez, J.; Giner, J. Estimating GARCH models using SVM. Quant. Financ. 2003, 3, 163–172. [Google Scholar] [CrossRef]

- Cherkassky, V.; Ma, Y. Practical selection of SVM parameters and noise estimation for SVM regression. Neural Net. 2004, 17, 113–126. [Google Scholar] [CrossRef] [Green Version]

- Chen, S.; Härdle, W.K.; Jeong, K. Forecasting volatility with support vector machine-based GARCH model. J. Forecast. 2010, 433, 406–433. [Google Scholar] [CrossRef]

- Shim, J.; Kim, Y.; Lee, J.; Hwang, C. Estimating value at risk with semiparametric support vector quantile regression. Comp. Stat. 2012, 27, 685–700. [Google Scholar] [CrossRef]

- Shim, J.; Hwang, C.; Seok, K. Support vector quantile regression with varying coefficients. Comp. Stat. 2016, 31, 1015–1030. [Google Scholar] [CrossRef]

- Bezerra, P.C.S.; Albuquerque, P.H.M. Volatility forecasting via SVR–GARCH with mixture of Gaussian kernels. Comp. Manag. Sci. 2017, 14, 179–196. [Google Scholar] [CrossRef]

- Vapnik, V. The Nature of Statistical Learning Theory; Springer: New York, NY, USA, 2000. [Google Scholar]

- Smola, A.J.; Schölkopf, B. A tutorial on support vector regression. Stat. Comp. 2004, 14, 199–222. [Google Scholar] [CrossRef] [Green Version]

- Tay, F.; Cao, L. Application of support vector machines in financial time series forecasting. Omega 2001, 29, 309–317. [Google Scholar] [CrossRef]

- Page, E.S. A test for a change in a parameter occurring at an unknown point. Biometrika 1955, 42, 523–527. [Google Scholar] [CrossRef]

- Csörgő, M.; Horváth, L. Limit Theorems in Change-Point Analysis; John Wiley & Sons Inc.: New York, NY, USA, 1997. [Google Scholar]

- Chen, J.; Gupta, A.K. Parametric Statistical Change Point Analysis with Applications to Genetics, Medicine, and Finance; Wiley: New York, NY, USA, 2012. [Google Scholar]

- Kim, M.; Lee, S. Nonlinear expectile regression with application to value-at-risk and expected shortfall estimation. Comp. Stat. Data Anal. 2016, 94, 1–19. [Google Scholar] [CrossRef]

- Inclán, C.; Tiao, G.C. Use of cumulative sums of squares for retrospective detection of changes of variance. J. Am. Stat. Assoc. 1994, 89, 913–923. [Google Scholar]

- Kim, S.; Cho, S.; Lee, S. On the cusum test for parameter changes in GARCH (1, 1) models. Comm. Stat. Theory Meth. 2000, 29, 445–462. [Google Scholar] [CrossRef]

- Lee, S.; Ha, J.; Na, O.; Na, S. The CUSUM test for parameter change in time series models. Scand. J. Stat. 2003, 30, 781–796. [Google Scholar] [CrossRef]

- Berkes, I.; Horváth, L.; Kokoszka, P. Testing for parameter constancy in GARCH(p,q) models. Stat. Prob. Lett. 2004, 70, 263–273. [Google Scholar] [CrossRef]

- Hillebrand, E. Neglecting parameter changes in GARCH models. J. Econometrics 2005, 129, 121–138. [Google Scholar] [CrossRef]

- Gombay, E. Change detection in autoregressive time series. J. Multi. Anal. 2008, 99, 451–464. [Google Scholar] [CrossRef] [Green Version]

- Tahmasbi, R.; Rezaei, S. Change point detection in garch models for voice activity detection. IEEE Trans. Audio Speech Lang. Proc. 2008, 16, 1038–1046. [Google Scholar] [CrossRef]

- Ross, G.J. Modelling financial volatility in the presence of abrupt changes. Phys. A Stat. Mech. Appl. 2013, 392, 350–369. [Google Scholar] [CrossRef] [Green Version]

- Oh, H.; Lee, S. Modified residual CUSUM test for location-scale time series models with heteroscedasticity. Ann. Inst. Stat. Math. 2019, 71, 1059–1091. [Google Scholar] [CrossRef]

- Kang, J.; Lee, S. Parameter change test for Poisson autoregressive models. Scand. J. Stat. 2014, 41, 1136–1152. [Google Scholar] [CrossRef]

- Oh, H.; Lee, S. On score vector- and residual-based CUSUM tests in ARMA-GARCH models. Stat. Methods Appl. 2018, 27, 385–406. [Google Scholar] [CrossRef]

- Lee, S.; Tokutsu, Y.; Maekawa, K. The cusum test for parameter change in regression models with ARCH errors. J. Japan Stat. Soc. 2004, 34, 173–188. [Google Scholar] [CrossRef] [Green Version]

- De Pooter, M.; Van Dijk, D. Testing for Changes in Volatility in Heteroskedastic Time Series—A Further Examination; Econometric Institute Research Papers EI 2004-38; Erasmus University Rotterdam, Erasmus School of Economics (ESE), Econometric Institute: Rotrerdam, The Netherlands, 2004. [Google Scholar]

- Lee, S.; Lee, J. Parameter change test for nonlinear time series models with GARCH type errors. J. Korean Math. Soc. 2015, 52, 503–553. [Google Scholar] [CrossRef] [Green Version]

- Lee, S.; Lee, S.; Moon, M. Hybrid change point detection for time series via support vector regression and CUSUM method. Appl. Soft Comput. 2020, 89, 106101. [Google Scholar] [CrossRef]

- Francq, C.; Zakoïan, J.M. Maximum likelihood estimation of pure GARCH and ARMA-GARCH processes. Bernoulli 2004, 10, 605–637. [Google Scholar] [CrossRef]

- Francq, C.; Zakoïan, J. GARCH Models: Structure, statistical Inference, and Financial Applications; Wiley: New York, NY, USA, 2010. [Google Scholar]

- Cortes, C.; Vapnik, V. Support-vector networks. Mach. Learn. 1995, 20, 273–297. [Google Scholar] [CrossRef]

- Abe, S. Support Vector Machines for Pattern Classification; Springer: London, UK, 2005. [Google Scholar]

- Niemira, M.P. Forecasting Financial and Economic Cycles; John Wiley & Sons Inc.: New York, NY, USA, 1994; Volume 49. [Google Scholar]

- Bergstra, J.; Bengio, Y. Random search for hyper-parameter optimization. J. Mach. Learn. Res. 2012, 13, 281–305. [Google Scholar]

- Billingsley, P. Convergence of Probability Measure; Wiley: New York, NY, USA, 1968. [Google Scholar]

- Hansen, P.R.; Lunde, A. A forecast comparison of volatility models: Does anything beat a GARCH(1,1)? J. Appl. Econ. 2005, 20, 873–889. [Google Scholar] [CrossRef] [Green Version]

- Huh, J.; Oh, H.; Lee, S. Monitoring parameter change for time series models with conditional heteroscedasticity. Econ. Lett. 2017, 152, 66–70. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| size | 0.023 | 0.038 | 0.055 | |

| change of | 0.761 | 0.826 | 0.956 | |

| 0.612 | 0.792 | 0.97 | ||

| change of | 0.355 | 0.651 | 0.949 | |

| 0.649 | 0.802 | 0.952 | ||

| change of mixed parameters | 0.871 | 0.969 | 0.981 | |

| 0.848 | 0.952 | 0.964 | ||

| size | 0.031 | 0.04 | 0.03 | |

| change of | 0.881 | 0.951 | 0.975 | |

| 0.26 | 0.613 | 0.904 | ||

| change of | 0.783 | 0.939 | 0.975 | |

| 0.762 | 0.863 | 0.941 | ||

| change of b | 0.591 | 0.897 | 0.976 | |

| 0.898 | 0.936 | 0.957 | ||

| change of mixed parameters | 0.565 | 0.726 | 0.846 | |

| 0.879 | 0.926 | 0.966 | ||

| size | 0.021 | 0.029 | 0.028 | |

| change of | 0.851 | 0.912 | 0.947 | |

| 0.644 | 0.787 | 0.866 | ||

| change of | 0.418 | 0.695 | 0.879 | |

| 0.421 | 0.751 | 0.888 | ||

| change of mixed parameters | 0.657 | 0.863 | 0.928 | |

| 0.717 | 0.857 | 0.925 | ||

| size | 0.037 | 0.049 | 0.059 | |

| change of | 0.718 | 0.795 | 0.879 | |

| 0.647 | 0.84 | 0.902 | ||

| change of | 0.805 | 0.886 | 0.913 | |

| 0.735 | 0.838 | 0.897 | ||

| change of mixed parameters | 0.907 | 0.97 | 0.994 | |

| 0.499 | 0.674 | 0.772 | ||

| size | 0.047 | 0.039 | 0.037 | |

| change of | 0.906 | 0.984 | 0.997 | |

| 0.228 | 0.382 | 0.507 | ||

| change of | 0.868 | 0.946 | 0.976 | |

| 0.917 | 0.985 | 1 | ||

| change of mixed parameters | 0.82 | 0.973 | 0.998 | |

| 0.862 | 0.944 | 0.971 | ||

| GARCH → log-GARCH | 0.879 | 0.946 | 0.956 | |

| 0.668 | 0.918 | 0.969 | ||

| log-GARCH → GARCH | 0.907 | 0.97 | 0.994 | |

| 0.499 | 0.674 | 0.772 | ||

| TGARCH → AGARCH | 0.728 | 0.795 | 0.879 | |

| 0.851 | 0.891 | 0.919 | ||

| AGARCH → GJR-GARCH | 0.549 | 0.861 | 0.958 | |

| 0.802 | 0.931 | 0.976 | ||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, S.; Kim, C.K.; Lee, S. Hybrid CUSUM Change Point Test for Time Series with Time-Varying Volatilities Based on Support Vector Regression. Entropy 2020, 22, 578. https://doi.org/10.3390/e22050578

Lee S, Kim CK, Lee S. Hybrid CUSUM Change Point Test for Time Series with Time-Varying Volatilities Based on Support Vector Regression. Entropy. 2020; 22(5):578. https://doi.org/10.3390/e22050578

Chicago/Turabian StyleLee, Sangyeol, Chang Kyeom Kim, and Sangjo Lee. 2020. "Hybrid CUSUM Change Point Test for Time Series with Time-Varying Volatilities Based on Support Vector Regression" Entropy 22, no. 5: 578. https://doi.org/10.3390/e22050578

APA StyleLee, S., Kim, C. K., & Lee, S. (2020). Hybrid CUSUM Change Point Test for Time Series with Time-Varying Volatilities Based on Support Vector Regression. Entropy, 22(5), 578. https://doi.org/10.3390/e22050578