Inferring Dealer Networks in the Foreign Exchange Market Using Conditional Transfer Entropy: Analysis of a Central Bank Announcement

Abstract

1. Introduction

2. Materials and Methods

2.1. Data

2.2. Data Processing

2.3. Information-Theoretic Metrics

2.4. Algorithm

2.5. Weighted Reciprocity

2.6. Validation and Code Availability

3. Results

3.1. Baseline—27 February to 11 March

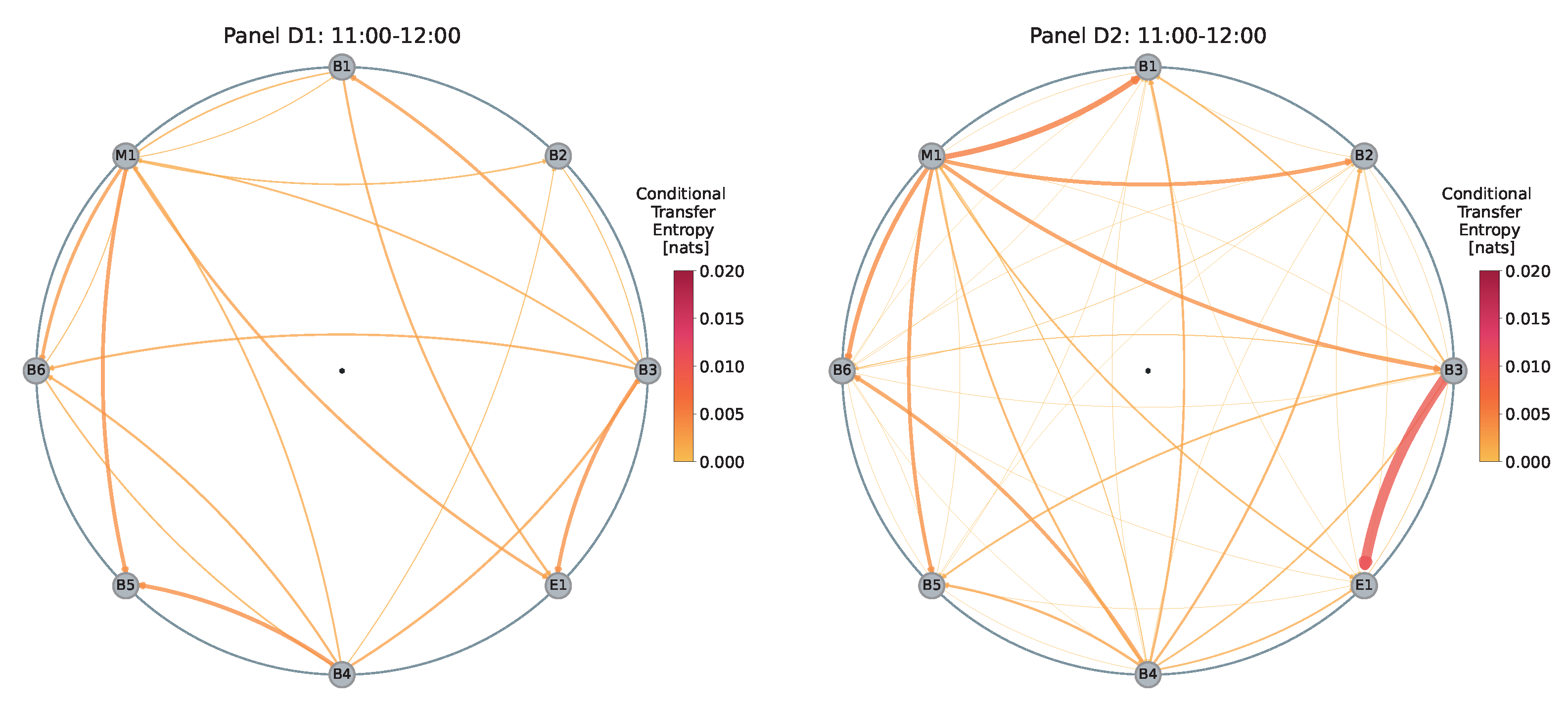

3.2. Qualitative Assessment of Changes in the Network’s Topology on 12 March 2020

3.3. Quantitative Assessment of Changes in the Network’s Topology on 12 March 2020

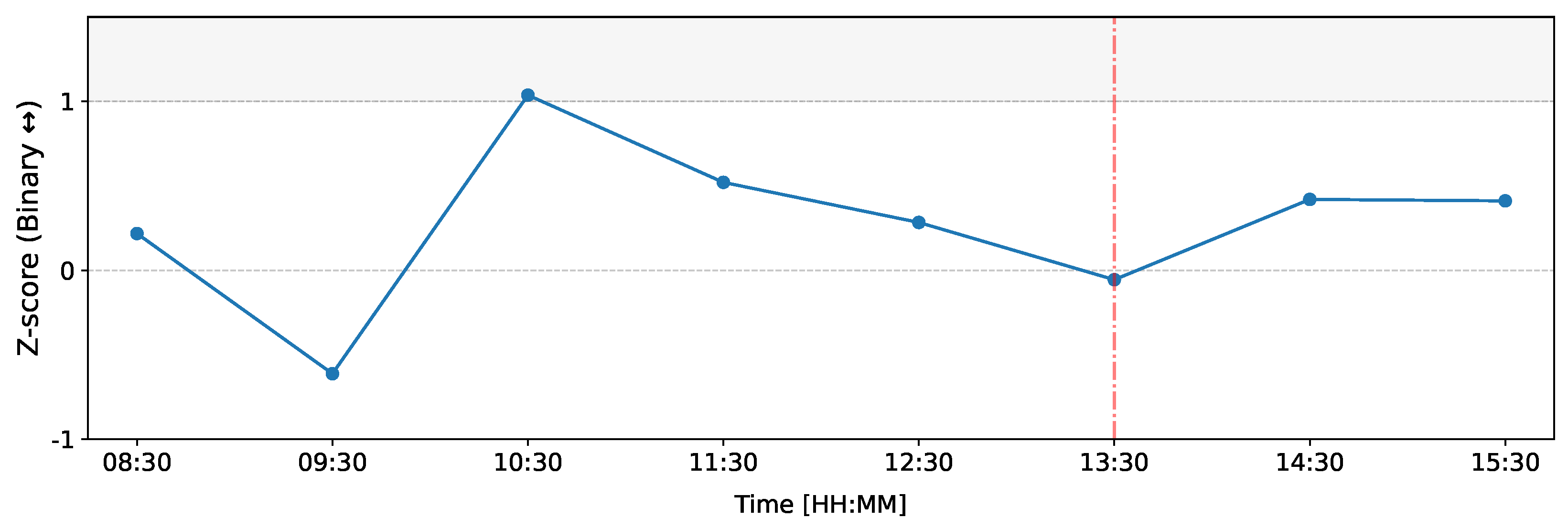

3.4. Quantitative Assessment of Changes in the Binary Network’s Topology on 12 March 2020

4. Discussion

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| TE | Transfer Entropy |

| CTE | Conditional Transfer Entropy |

| KSG | Kraskov, Stögbauer, and Grassberger |

| FX | Foreign Exchange Market |

| ECB | European Central Bank |

| GMT | Greenwich Mean Time |

Appendix A. Baseline and Hourly Information Maps for the Period of 13 March 2020–7 March 2020

References

- Bonanno, G.; Lillo, F.; Mantegna, R.N. Levels of complexity in financial markets. Phys. A Stat. Mech. Its Appl. 2001, 299, 16–27. [Google Scholar] [CrossRef]

- Bouchaud, J.P.; Cont, R. A Langevin Approach to Stock Market Fluctuations and Crashes. Eur. Phys. J. B-Condens. Matter Complex Syst. 1998, 6, 543–550. [Google Scholar] [CrossRef]

- Bouchaud, J.P. The (unfortunate) complexity of the economy. Phys. World 2009, 22, 28. [Google Scholar] [CrossRef]

- Battiston, S.; Farmer, J.D.; Flache, A.; Garlaschelli, D.; Haldane, A.G.; Heesterbeek, H.; Hommes, C.; Jaeger, C.; May, R.; Scheffer, M. Complexity theory and financial regulation. Science 2016, 351, 818–819. [Google Scholar] [CrossRef]

- Bardoscia, M.; Barucca, P.; Battiston, S.; Caccioli, F.; Cimini, G.; Garlaschelli, D.; Saracco, F.; Squartini, T.; Caldarelli, G. The Physics of Financial Networks. Nat. Rev. Phys. 2021, 3, 490–507. [Google Scholar] [CrossRef]

- Squartini, T.; Van Lelyveld, I.; Garlaschelli, D. Early-warning signals of topological collapse in interbank networks. Sci. Rep. 2013, 3, 3357. [Google Scholar] [CrossRef]

- Cimini, G.; Squartini, T.; Garlaschelli, D.; Gabrielli, A. Systemic Risk Analysis on Reconstructed Economic and Financial Networks. Sci. Rep. 2015, 5, 15758. [Google Scholar] [CrossRef]

- Bardoscia, M.; Battiston, S.; Caccioli, F.; Caldarelli, G. Pathways towards instability in financial networks. Nat. Commun. 2017, 8, 14416. [Google Scholar] [CrossRef] [PubMed]

- Novelli, L.; Wollstadt, P.; Mediano, P.; Wibral, M.; Lizier, J.T. Large-scale directed network inference with multivariate transfer entropy and hierarchical statistical testing. Netw. Neurosci. 2019, 3, 827–847. [Google Scholar] [CrossRef]

- Quax, R.; Kandhai, D.; Sloot, P. Information dissipation as an early-warning signal for the Lehman Brothers collapse in financial time series. Sci. Rep. 2013, 3, 1898. [Google Scholar] [CrossRef]

- Rodriguez-Rodriguez, N.; Miramontes, O. Shannon Entropy: An econophysical approach to cryptocurrency portfolios. Entropy 2022, 24, 1583. [Google Scholar] [CrossRef] [PubMed]

- Drzazga-Szczesniak, E.A.; Szczepanik, P.; Kaczmarek, A.Z.; Szczesniak, D. Entropy of financial time series due to the shock of war. Entropy 2023, 25, 823. [Google Scholar] [CrossRef]

- Olbryś, J.; Ostrowski, K. An entropy-based approach to measurement of stock market depth. Entropy 2021, 23, 568. [Google Scholar] [CrossRef] [PubMed]

- Wolinsky, A. Information revelation in a market with pairwise meetings. Econom. J. Econom. Soc. 1990, 58, 1–23. [Google Scholar] [CrossRef]

- Duffie, D.; Manso, G. Information Percolation in Large Markets. Am. Econ. Rev. 2007, 97, 203–209. [Google Scholar] [CrossRef]

- Duffie, D.; Malamud, S.; Manso, G. Information Percolation with Equilibrium Search Dynamics. Econometrica 2009, 77, 1513–1574. [Google Scholar]

- Duffie, D.; Malamud, S.; Manso, G. Information Percolation in Segmented Markets. J. Econ. Theory 2014, 153, 1–32. [Google Scholar] [CrossRef]

- Almog, A.; Shmueli, E. Structural entropy: Monitoring correlation-based networks over time with application to financial markets. Sci. Rep. 2019, 9, 10832. [Google Scholar] [CrossRef] [PubMed]

- Schreiber, T. Measuring Information Transfer. Phys. Rev. Lett. 2000, 85, 461. [Google Scholar] [CrossRef]

- Shannon, C.E. A Mathematical Theory of Communication. Bell Syst. Tech. J. 1948, 27, 379–423. [Google Scholar] [CrossRef]

- Lizier, J.; Rubinov, M. Multivariate Construction of Effective Computational Networks from Observational Data; Max-Planck Institut: Leipzing, Germany, 2012; Available online: http://www.mis.mpg.de/preprints/2012/preprint2012_25.pdf (accessed on 1 February 2022).

- Lizier, J.T.; Prokopenko, M. Differentiating information transfer and causal effect. Eur. Phys. J. B 2010, 73, 605–615. [Google Scholar] [CrossRef]

- Bossomaier, T.; Barnett, L.; Harré, M.; Lizier, J. An Introduction to Transfer Entropy: Information Flow in Complex Systems; Springer International Publishing: Cham, Switzerland, 2016. [Google Scholar]

- Albers, D.J.; Hripcsak, G. Using time-delayed mutual information to discover and interpret temporal correlation structure in complex populations. Chaos Interdiscip. J. Nonlinear Sci. 2012, 22, 013111. [Google Scholar] [CrossRef] [PubMed]

- Wibral, M.; Wollstadt, P.; Meyer, U.; Pampu, N.; Priesemann, V.; Vicente, R. Revisiting Wiener’s principle of causality—interaction-delay reconstruction using transfer entropy and multivariate analysis on delay-weighted graphs. In Proceedings of the 2012 Annual International Conference of the IEEE Engineering in Medicine and Biology Society, San Diego, CA, USA, 28 August 2012–1 September 2012; pp. 3676–3679. [Google Scholar]

- Janczewski, A.; Anagnostou, I.; Kandhai, D. Supplementary material for “Inferring Dealer Networks in the FX Market Using Conditional Transfer Entropy: Analysis of a Central Bank Announcement” 2024.

- Kraskov, A.; Stögbauer, H.; Grassberger, P. Estimating Mutual Information. Phys. Rev. E 2004, 69, 066138. [Google Scholar] [CrossRef] [PubMed]

- Lizier, J.T. JIDT: An information-theoretic toolkit for studying the dynamics of complex systems. Front. Robot. AI 2014, 1, 11. [Google Scholar] [CrossRef]

- Vejmelka, M.; Paluš, M. Inferring the directionality of coupling with conditional mutual information. Phys. Rev. E 2008, 77, 026214. [Google Scholar] [CrossRef]

- Lizier, J. Is KSG Estimator Deterministic?—[Java Information Dynamics Toolkit (JIDT) Discussion], 2015. Available online: https://groups.google.com/g/jidt-discuss/c/EmLEXo9BGcA (accessed on 2 November 2023).

- Michalowicz, J.V.; Nichols, J.M.; Bucholtz, F. Handbook of Differential Entropy; CRC Press: Boca Raton, FL, USA, 2013. [Google Scholar]

- Frenzel, S.; Pompe, B. Partial Mutual Information for Coupling Analysis of Multivariate Time Series. Phys. Rev. Lett. 2007, 99, 204101. [Google Scholar] [CrossRef] [PubMed]

- Wibral, M.; Vicente, R.; Lizier, J.T. Directed Information Measures in Neuroscience; Springer: Berlin/Heidelberg, Germany, 2014. [Google Scholar]

- Runge, J. Detecting and Quantifying Causality from Time Series of Complex Systems. Ph.D. Thesis, Mathematisch-Naturwissenschaftliche Fakultät, Humboldt-Universität zu Berlin, Berlin, Germany, 2014. [Google Scholar] [CrossRef]

- Meyer, P.E.; Kontos, K.; Lafitte, F.; Bontempi, G. Information-Theoretic Inference of Large Transcriptional Regulatory Networks. EURASIP J. Bioinform. Syst. Biol. 2007, 2007, 79879. [Google Scholar] [CrossRef]

- Ragwitz, M.; Kantz, H. Markov models from data by simple nonlinear time series predictors in delay embedding spaces. Phys. Rev. E 2002, 65, 056201. [Google Scholar] [CrossRef] [PubMed]

- Lindner, M.; Vicente, R.; Priesemann, V.; Wibral, M. TRENTOOL: A Matlab open source toolbox to analyse information flow in time series data with transfer entropy. BMC Neurosci. 2011, 12, 119. [Google Scholar] [CrossRef]

- Wibral, M.; Pampu, N.; Priesemann, V.; Siebenhühner, F.; Seiwert, H.; Lindner, M.; Lizier, J.T.; Vicente, R. Measuring Information-Transfer Delays. PLoS ONE 2013, 8, e55809. [Google Scholar] [CrossRef]

- Virtanen, P.; Gommers, R.; Oliphant, T.E.; Haberland, M.; Reddy, T.; Cournapeau, D.; Burovski, E.; Peterson, P.; Weckesser, W.; Bright, J.; et al. SciPy 1.0: Fundamental Algorithms for Scientific Computing in Python. Nat. Methods 2020, 17, 261–272. [Google Scholar] [CrossRef] [PubMed]

- Lizier, J.T.; Heinzle, J.; Horstmann, A.; Haynes, J.D.; Prokopenko, M. Multivariate information-theoretic measures reveal directed information structure and task relevant changes in fMRI connectivity. J. Comput. Neurosci. 2011, 30, 85–107. [Google Scholar] [CrossRef] [PubMed]

- Squartini, T.; Picciolo, F.; Ruzzenenti, F.; Garlaschelli, D. Reciprocity of weighted networks. Sci. Rep. 2013, 3, 2729. [Google Scholar] [CrossRef]

- Kaiser, A.; Schreiber, T. Information transfer in continuous processes. Phys. D Nonlinear Phenom. 2002, 166, 43–62. [Google Scholar] [CrossRef]

- Bank, E.C. Asset Purchase Programmes. 2023. Available online: https://www.ecb.europa.eu/mopo/implement/app/html/index.en.html (accessed on 13 June 2024).

- Ricketts, L.R. Quantitative Easing Explained. Liber8 Economic Information Newsletter. 2011. Available online: https://fraser.stlouisfed.org/title/page-one-economics-6840/quantitative-easing-explained-627615 (accessed on 6 June 2024).

- Bank of England. Quantitative Easing. Available online: https://www.bankofengland.co.uk/monetary-policy/quantitative-easing (accessed on 17 May 2024).

- Fischer, A.M.; Ranaldo, A. Does FOMC News Increase Global FX Trading? J. Bank. Financ. 2011, 35, 2965–2973. [Google Scholar] [CrossRef]

- Mueller, P.; Tahbaz-Salehi, A.; Vedolin, A. Exchange Rates and Monetary Policy Uncertainty. J. Financ. 2017, 72, 1213–1252. [Google Scholar] [CrossRef]

- Bundesbank, D. The Eurosystem’s Bond Purchases and the Exchange Rate of the Euro. Monthly Report, January 2017. Available online: https://www.bundesbank.de/resource/blob/707604/ad5d6a4c1a430a1bfee21a378572f87a/mL/2017-01-anleihekaeufe-eurosystem-data.pdf (accessed on 12 June 2024).

- European Central Bank. Monetary Policy Decisions. 2020. Available online: https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.mp200312~8d3aec3ff2.en.html (accessed on 10 May 2024).

- European Central Bank. Monetary Policy in a Pandemic: Ensuring Favourable Financing Conditions. 2020. Available online: https://www.ecb.europa.eu/press/key/date/2020/html/ecb.sp201126~c5c1036327.en.html (accessed on 13 June 2024).

- Hagströmer, B.; Menkveld, A.J. Information Revelation in Decentralized Markets. J. Financ. 2019, 74, 2751–2787. [Google Scholar] [CrossRef]

- Addison, A.; Andrews, C.; Azad, N.; Bardsley, D.; Bauman, J.; Diaz, J.; Didik, T.; Fazliddin, K.; Gromoa, M.; Krish, A.; et al. Low-latency trading in the cloud environment. In Proceedings of the 2019 IEEE International Conference on Computational Science and Engineering (CSE) and IEEE International Conference on Embedded and Ubiquitous Computing (EUC), New York, NY, USA, 1–3 August 2019; pp. 272–282. [Google Scholar]

- Berrett, T.B.; Samworth, R.J.; Yuan, M. Efficient multivariate entropy estimation via k-nearest neighbour distances. Ann. Stat. 2019, 47, 288–318. [Google Scholar]

- Cao, L. Practical method for determining the minimum embedding dimension of a scalar time series. Phys. Nonlinear Phenom. 1997, 110, 43–50. [Google Scholar] [CrossRef]

- Chen, S.-H.; Kaboudan, M.; Du, Y.-R. The Oxford Handbook of Computational Economics and Finance; Oxford University Press: Oxford, UK, 2018. [Google Scholar]

- Devroye, L.; Gyöfi, L. On the consistency of the Kozachenko-Leonenko entropy estimate. IEEE Trans. Inf. Theory 2021, 68, 1178–1185. [Google Scholar] [CrossRef]

- Dobrushin, R.L. A simplified method of experimentally evaluating the entropy of a stationary sequence. Theory Probab. Its Appl. 1958, 3, 428–430. [Google Scholar] [CrossRef]

- Gómez-Herrero, G.; Wu, W.; Rutanen, K.; Soriano, M.C.; Pipa, G.; Vicente, R. Assessing coupling dynamics from an ensemble of time series. Entropy 2015, 17, 1958–1970. [Google Scholar] [CrossRef]

- Guo, Z.; McClelland, V.M.; Simeone, O.; Mills, K.R.; Cvetkovic, Z. Multiscale Wavelet Transfer Entropy with Application to Corticomuscular Coupling Analysis. IEEE Trans. Biomed. Eng. 2021, 69, 771–782. [Google Scholar] [CrossRef]

- Hagströmer, B.; Menkveld, A.J. A Network Map of Information Percolation; Working Paper; SSRN: Atlanta, GA, USA, 2016. [Google Scholar]

- Hasbrouck, J.; Saar, G. Low-latency trading. J. Financ. Mark. 2013, 16, 646–679. [Google Scholar] [CrossRef]

- Hegger, R.; Kantz, H.; Schreiber, T. Practical implementation of nonlinear time series methods: The TISEAN package. Chaos Interdiscip. J. Nonlinear Sci. 1999, 9, 413–435. [Google Scholar] [CrossRef]

- Hlaváčková-Schindler, K.; Paluš, M.; Vejmelka, M.; Bhattacharya, J. Causality detection based on information-theoretic approaches in time series analysis. Phys. Rep. 2007, 441, 1–46. [Google Scholar] [CrossRef]

- King, M.R.; Osler, C.L.; Rime, D. Foreign exchange market structure, players and evolution. In Handbook of Exchange Rates; Norges Bank Working Paper; Wiley: Hoboken, NJ, USA, 2011. [Google Scholar]

- Kozachenko, L.F.; Leonenko, N.N. Sample estimate of the entropy of a random vector. Probl. Peredachi Informatsii 1987, 23, 9–16. [Google Scholar]

- Lizier, J. Ragwitz Auto-Embedding in Conditional Transfer Entropy—[Java Information Dynamics Toolkit (JIDT) Discussion]. 2022. Available online: https://groups.google.com/g/jidt-discuss/c/TEcGwPQ__7U (accessed on 1 February 2022).

- Lord, W.M.; Sun, J.; Bollt, E.M. Geometric k-nearest neighbor estimation of entropy and mutual information. Chaos Interdiscip. J. Nonlinear Sci. 2018, 28, 033114. [Google Scholar] [CrossRef] [PubMed]

- Menkveld, A.J. High frequency trading and the new market makers. J. Financ. Mark. 2013, 16, 712–740. [Google Scholar] [CrossRef]

- Montalto, A.; Faes, L.; Marinazzo, D. MuTE: A MATLAB toolbox to compare established and novel estimators of the multivariate transfer entropy. PLoS ONE 2014, 9, e109462. [Google Scholar]

- Pan, S.; Duraisamy, K. On the structure of time-delay embedding in linear models of non-linear dynamical systems. Chaos Interdiscip. J. Nonlinear Sci. 2020, 30, 073135. [Google Scholar] [CrossRef] [PubMed]

- Pedregosa, F.; Varoquaux, G.; Gramfort, A.; Michel, V.; Thirion, B.; Grisel, O.; Blondel, M.; Prettenhofer, P.; Weiss, R.; Dubourg, V.; et al. Scikit-learn: Machine Learning in Python. J. Mach. Learn. Res. 2011, 12, 2825–2830. [Google Scholar]

- Shahsavari Baboukani, P.; Graversen, C.; Alickovic, E.; Østergaard, J. Estimating Conditional Transfer Entropy in Time Series Using Mutual Information and Nonlinear Prediction. Entropy 2020, 22, 1124. [Google Scholar] [CrossRef] [PubMed]

- Takens, F. Detecting strange attractors in turbulence. In Dynamical Systems and Turbulence, Warwick 1980; Springer: Berlin/Heidelberg, Germany, 1981; pp. 366–381. [Google Scholar]

- Vasicek, O. A test for normality based on sample entropy. J. R. Stat. Soc. Ser. B (Methodol.) 1976, 38, 54–59. [Google Scholar] [CrossRef]

- Vitale, P. A Market Microstructure Analysis of Foreign Exchange Intervention; ECB Working Paper; Bank of Canada: Ottawa, ON, Canada, 2006. [Google Scholar]

- Wollstadt, P.; Lizier, J.T.; Vicente, R.; Finn, C.; Martinez-Zarzuela, M.; Mediano, P.; Novelli, L.; Wibral, M. IDTxl: The Information Dynamics Toolkit xl: A Python package for the efficient analysis of multivariate information dynamics in networks. arXiv 2018, arXiv:1807.10459. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Inflows [ Nats] | ||||||||||

| Outflows [ Nats] | B6 | B5 | B4 | E1 | B3 | B2 | B1 | M1 | Sum | |

| B6 | - | 3.1 | 2.9 | 2.0 | 4.6 | 4.9 | 2.3 | 3.5 | 23.3 | |

| B5 | 1.5 | - | 2.2 | 2.1 | 2.9 | 0.9 | 1.5 | 2.4 | 13.5 | |

| B4 | 24.4 | 18.1 | - | 13.0 | 14.3 | 17.5 | 21.4 | 6.0 | 114.6 | |

| E1 | 0.4 | 0.6 | 2.3 | - | 2.3 | 0.9 | 1.0 | 1.0 | 8.4 | |

| B3 | 5.8 | 5.8 | 3.5 | 93.9 | - | 6.2 | 5.7 | 2.3 | 123.3 | |

| B2 | 2.9 | 2.2 | 2.6 | 0.9 | 3.3 | - | 1.9 | 2.4 | 16.2 | |

| B1 | 1.4 | 0.6 | 3.2 | 0.5 | 3.2 | 1.7 | - | 1.9 | 12.5 | |

| M1 | 59.3 | 52.9 | 21.2 | 15.0 | 50.4 | 49.2 | 59.4 | - | 307.4 | |

| Sum | 95.5 | 83.3 | 37.9 | 127.4 | 81.0 | 81.4 | 93.3 | 19.5 | - | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Janczewski, A.; Anagnostou, I.; Kandhai, D. Inferring Dealer Networks in the Foreign Exchange Market Using Conditional Transfer Entropy: Analysis of a Central Bank Announcement. Entropy 2024, 26, 738. https://doi.org/10.3390/e26090738

Janczewski A, Anagnostou I, Kandhai D. Inferring Dealer Networks in the Foreign Exchange Market Using Conditional Transfer Entropy: Analysis of a Central Bank Announcement. Entropy. 2024; 26(9):738. https://doi.org/10.3390/e26090738

Chicago/Turabian StyleJanczewski, Aleksander, Ioannis Anagnostou, and Drona Kandhai. 2024. "Inferring Dealer Networks in the Foreign Exchange Market Using Conditional Transfer Entropy: Analysis of a Central Bank Announcement" Entropy 26, no. 9: 738. https://doi.org/10.3390/e26090738

APA StyleJanczewski, A., Anagnostou, I., & Kandhai, D. (2024). Inferring Dealer Networks in the Foreign Exchange Market Using Conditional Transfer Entropy: Analysis of a Central Bank Announcement. Entropy, 26(9), 738. https://doi.org/10.3390/e26090738