Regional Economic and Financial Interconnectedness and the Impact of Sanctions: The Case of the Commonwealth of Independent States

Abstract

:1. Introduction

2. The Economies of CIS Countries

2.1. Major Economic and Social Indicators

2.2. Interconnectedness with the Russian Economy

2.3. Economic and Political Environment

3. Data and Methodology

3.1. Data Description

3.2. Methodology

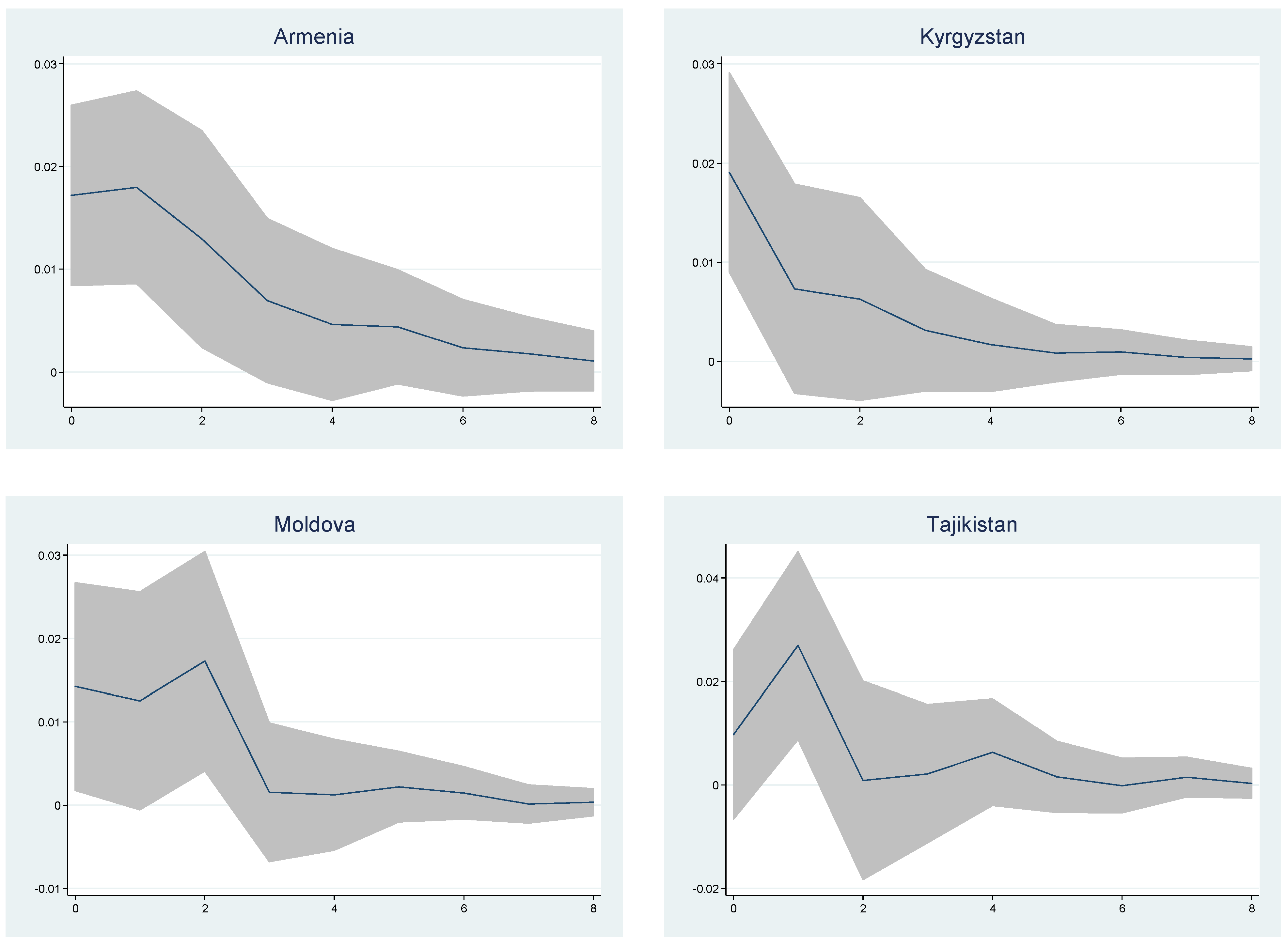

4. Empirical Findings

5. Discussion

6. Concluding Remarks and Policy Implications

Funding

Data Availability Statement

Conflicts of Interest

References

- Akaike, Hirotugu. 1974. A new look at the statistical model identification. IEEE Transactions on Automatic Control 19: 716–23. [Google Scholar] [CrossRef]

- Bayramov, Vugar, Nabi Rustamli, and Gulnara Abbas. 2020. Collateral damage: The Western sanctions on Russia and the evaluation of implications for Russia’s post-communist neighbourhood. International Economics 162: 92–109. [Google Scholar] [CrossRef]

- Campbell, M. Kurt, and Rush Doshi. 2020. The Coronavirus Could Reshape Global Order: China Is Maneuvering for International Leadership as the United States Falters. Foreign Affairs. March 18. Available online: https://www.foreignaffairs.com/articles/china/2020-03-18/coronavirus-could-reshape-global-order (accessed on 20 August 2022).

- Central Bank of Russia. 2022. External Sector Statistics. The Central Bank of the Russian Federation. Available online: https://www.cbr.ru/eng/statistics/macro_itm/svs/ (accessed on 8 June 2022).

- CIS STAT. 2022. CIS in Figures. Interstate Statistical Committee of the Commonwealth of Independent States. Available online: http://www.cisstat.com/eng (accessed on 6 June 2022).

- Devonshire-Ellis, Chris. 2022. China, Russia Stand Firm in ‘New, Fair, Multipolar World Order’. China Briefing. March 30. Available online: https://www.china-briefing.com/news/china-russia-stand-firm-in-new-fair-multipolar-world-order/ (accessed on 4 June 2022).

- Dreger, Christian, Jarko Fidrmuc, Konstantin Kholodilin, and Dirk Ulbricht. 2015. The Ruble between the Hammer and the Anvil: Oil Prices and Economic Sanctions. Discussion Papers 1488. Berlin: DIW Berlin, German Institute for Economic Research. [Google Scholar]

- Engle, R. Robert, and John C. W. Granger. 1987. Co-integration and error correction: Representation, estimation, and testing. Econometrica 55: 251–76. [Google Scholar] [CrossRef]

- Freedom House. 2022. Countries and Territories: Global Freedom Scores, Internet Freedom Scores, Democracy Scores. Freedom House. Available online: https://freedomhouse.org/countries/freedom-world/scores (accessed on 2 June 2022).

- Granger, C. W. John. 1969. Investigating causal relations by econometric models and cross-spectral methods. Econometrica 37: 424–38. [Google Scholar] [CrossRef]

- Haas, Richard. 2020. The World: A Brief Introduction. New York: Penguin Press. [Google Scholar]

- Heritage Foundation. 2022. 2022 Index of ECONOMIC Freedom. The Heritage Foundation. Available online: https://www.heritage.org/index/heatmap (accessed on 4 June 2022).

- IMF. 2015. Russian Federation, 2015 Article IV Consultation. IMF Country Report, No. 15/211. Washington, DC: International Monetary Fund. [Google Scholar]

- Johansen, Soren. 1988. Statistical analysis of cointegration vectors. Journal of Economic Dynamics and Control 12: 231–54. [Google Scholar] [CrossRef]

- Johansen, Soren. 1995. Likelihood-Based Inference in Cointegrated Vector Autoregressive Models. Oxford: Oxford University Press. [Google Scholar]

- Kholodilin, Konstantin, and Aleksei Netsunajev. 2016. Crimea and Punishment: The Impact of Sanctions on Russian and European Economies. Discussion Papers of DIW Berlin 1569. Berlin: DIW Berlin, German Institute for Economic Research. [Google Scholar]

- Kholodilin, Konstantin, and Aleksei Netšunajev. 2019. Crimea and punishment: The impact of sanctions on Russian economy and economies of the Euro Area. Baltic Journal of Economics 19: 39–51. [Google Scholar] [CrossRef]

- NBT. 2022. Analytical Table of Export and Import of Goods by Country. National Bank of Tajikistan. Available online: https://nbt.tj/en/statistics/tavozuni-pardokhti-jt/savdoi-molu-khikhmatrasonihoi-berunai-jumhurii-tojikiston/jadvali_tahlili_sodirot.php (accessed on 16 June 2022).

- Pestova, Anna, and Mikhail Mamonov. 2019. Should We Care? The Economic Effects of Financial Sanctions on the Russian Economy. BOFIT Discussion Paper No. 13/2019. Available online: https://www.econstor.eu/handle/10419/212921 (accessed on 14 August 2022). [CrossRef]

- Radio Free Europe/Radio Liberty. 2018. A timeline of all Russia-related sanctions: A detailed look at all the sanctions levied against Russia, and its countersanctions, since 2014. Paper presented at Ivan Gutterman, Wojtek Grojec, and RFE/RL’s Current Time, Prague, Czechia, September 19. [Google Scholar]

- Shirov, Alexanderovich Alexander, Alexey Anatolievich Yantovskii, and Vadim Viktorovich Potapenko. 2015. Evaluation of the potential effect of sanctions on the economic development of Russia and the European Union. Studies on Russian Economic Development 26: 317–26. [Google Scholar] [CrossRef]

- Sultonov, Mirzosaid. 2020. The impact of international sanctions on Russian financial markets. Economies 8: 107. [Google Scholar] [CrossRef]

- Transparency International. 2021. Corruption Perceptions Index. Transparency International. Available online: https://www.transparency.org/en/cpi/2021 (accessed on 16 August 2022).

- Tyll, Ladislav, Karel Pernica, and Markéta Arltová. 2018. The impact of economic sanctions on Russian economy and the RUB/USD exchange rate. Journal of International Studies 11: 21–33. [Google Scholar] [CrossRef]

- UNDP. 2020. Human Development Report 2020: The Next Frontier, Human Development and the Anthropocene. New York: The United Nations Development Programme. [Google Scholar]

- White House. 2021. Renewing America’s Advantages: Interim National Security Strategic Guidance. President Joseph R. Biden, Jr, The White House, Washington, March 2021. Available online: https://www.whitehouse.gov/wp-content/uploads/2021/03/NSC-1v2.pdf (accessed on 15 August 2022).

- WITS. 2022. Detailed Country Analysis. World Integrated Trade Solutions, UNSD COMTRADE. Available online: http://wits.worldbank.org/visualization/detailed-country-analysis-visualization.html (accessed on 5 August 2022).

- World Bank. 2022a. Population, Total. World Development Indicators, The World Bank Group. Available online: https://data.worldbank.org/indicator/SP.POP.TOTL (accessed on 10 August 2022).

- World Bank. 2022b. GDP (Current US$). World Development Indicators, The World Bank Group. Available online: https://data.worldbank.org/indicator/NY.GDP.MKTP.CD (accessed on 10 August 2022).

- World Bank. 2022c. GDP per Capita (current US$). World Development Indicators, The World Bank Group. Available online: https://data.worldbank.org/indicator/NY.GDP.PCAP.CD (accessed on 10 August 2022).

- World Bank. 2022d. GDP Growth (Annual %). World Development Indicators, The World Bank Group. Available online: https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG (accessed on 12 August 2022).

- World Bank. 2022e. Exports of Goods and Services (% of GDP). World Development Indicators, The World Bank Group. Available online: https://data.worldbank.org/indicator/NE.EXP.GNFS.ZS (accessed on 12 August 2022).

- World Bank. 2022f. Imports of Goods and Services (% of GDP). World Development Indicators, The World Bank Group. Available online: https://data.worldbank.org/indicator/NE.IMP.GNFS.ZS (accessed on 11 August 2022).

- World Bank. 2022g. Personal Remittances, Received (% of GDP). World Development Indicators, The World Bank Group. Available online: https://data.worldbank.org/indicator/BX.TRF.PWKR.DT.GD.ZS (accessed on 13 August 2022).

- World Bank. 2022h. Foreign Direct Investment, Net Inflows (% of GDP). World Development Indicators, The World Bank Group. Available online: https://data.worldbank.org/indicator/BX.KLT.DINV.WD.GD.ZS (accessed on 14 August 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Population, Million People, 2020 | GDP, Billion USD, 2020 | GDP per Capita, USD, 2020 | Human Development Index, 2019 |

|---|---|---|---|---|

| Armenia | 3.0 | 12.6 | 4266.02 | 0.776, High |

| Azerbaijan | 10.1 | 42.7 | 4229.91 | 0.756, High |

| Belarus | 9.4 | 61.5 | 6555.43 | 0.823, Very high |

| Kazakhstan | 18.8 | 171.1 | 9121.64 | 0.825, Very high |

| Kyrgyzstan | 6.6 | 7.8 | 1182.52 | 0.697, Medium |

| Moldova | 2.6 | 11.9 | 4525.76 | 0.750, High |

| Russia | 144.1 | 1488.3 | 10,161.98 | 0.824, Very high |

| Tajikistan | 9.5 | 8.1 | 852.83 | 0.668, Medium |

| Ukraine | 44.1 | 156.6 | 3751.74 | 0.779, High |

| CIS total | 248.1 | 1960.6 | ||

| CIS as world share | 3.2 | 2.3 | ||

| CIS average | 4960.87 | 0.766, High | ||

| High-income countries average | 43,282.42 | |||

| Middle-income countries average | 5237.02 | |||

| Upper-middle-income countries average | 9166.46 | |||

| Lower-middle-income countries average | 2285.71 | |||

| Low-income countries average | 703.73 | |||

| World average | 10,936.06 | |||

| Country | Exports to Russia, % of Total Exports, Average for 2011–2019 | Imports from Russia, % of Total Imports, Average for 2011–2019 | Remittance Inflow as % of GDP (Remittance from Russia % of Total Remittances), Average of 2011–2020 | FDI Net Inflow % GDP (FDI Net Inflow from Russia, Percent of Total) Average of 2011–2020 |

|---|---|---|---|---|

| Armenia | 21.7 | 27.2 | 14.8 (70.6) | 2.8 (25.8) |

| Azerbaijan | 3.7 | 16.2 | 2.6 (76.0) | 5.8 (0.5) |

| Belarus | 40.6 | 55.4 | 1.8 (26.1) | 2.9 (46.7) |

| Kazakhstan | 8.7 | 37.5 | 0.2 (>90.0) | 4.7 (6.3) |

| Kyrgyzstan | 12.5 | 29.9 | 29.7 (86.7) | 5.4 (17.0) |

| Moldova | 17.1 | 13.7 | 19.2 (40.2) | 2.7 (-2.7) |

| Tajikistan | 5.7 | 28.8 | 33.2 (>90.0) | 3.0 (3.8) |

| Ukraine | 17.0 | 22.9 | 8.1 (18.1) | 2.7 (8.1) |

| Country | Overall Score | Property Rights | Tax Burden | Business Freedom | Monetary Freedom | Trade Freedom | Investment Freedom | Financial Freedom |

|---|---|---|---|---|---|---|---|---|

| Armenia | 65.3 | 50.4 | 86.9 | 64.9 | 77.5 | 73.6 | 75.0 | 70.0 |

| Azerbaijan | 61.6 | 53.6 | 87.7 | 64.6 | 74.5 | 66.6 | 70.0 | 60.0 |

| Belarus | 53.0 | 34.5 | 93.3 | 54.5 | 70.2 | 75.6 | 30.0 | 20.0 |

| Kazakhstan | 64.4 | 55.3 | 92.7 | 64.7 | 69.1 | 75.4 | 50.0 | 50.0 |

| Kyrgyzstan | 55.8 | 25.1 | 94.8 | 56.1 | 71.4 | 73.2 | 60.0 | 50.0 |

| Moldova | 61.3 | 55.9 | 94.1 | 64.2 | 72.4 | 76.6 | 55.0 | 50.0 |

| Russia | 56.1 | 36.8 | 93.1 | 62.5 | 68.0 | 69.0 | 30.0 | 30.0 |

| Tajikistan | 49.7 | 29.5 | 95.3 | 56.9 | 67.1 | 69.6 | 25.0 | 30.0 |

| Ukraine | 54.1 | 39.7 | 89.1 | 61.1 | 71.2 | 78.6 | 35.0 | 30.0 |

| CIS average | 57.9 | 42.3 | 91.9 | 61.1 | 71.3 | 73.1 | 47.8 | 43.3 |

| Free (80–100), Mostly free (70.0–79.9), Moderately free (60.0–69.9), Mostly unfree (50.0–59.9), Repressed (0–49.9) | ||||||||

| Country | Freedom Score | Internet Freedom Score | Democracy Score | Corruption Perception Index |

|---|---|---|---|---|

| Armenia | 55, Partly free | 71, Free | 34, Transitional or hybrid regime | 49 |

| Azerbaijan | 9, Not free | 35, Not free | 1, Consolidated authoritarian regime | 30 |

| Belarus | 8, Not free | 31, Not free | 3, Consolidated authoritarian regime | 41 |

| Kazakhstan | 23, Not free | 33, Not free | 6, Consolidated authoritarian regime | 37 |

| Kyrgyzstan | 27, Not free | 53, Partly free | 13, Consolidated authoritarian regime | 27 |

| Moldova | 62, Partly free | NA | 35, Transitional or hybrid regime | 36 |

| Russia | 19, Not free | 30, Not free | 5, Consolidated authoritarian regime | 29 |

| Tajikistan | 8, Not free | NA | 2, Consolidated authoritarian regime | 25 |

| Ukraine | 61, Partly free | 62, Partly free | 39, Transitional or hybrid regime | 32 |

| Variables | Observations | Mean | Standard Deviation | Minimum | Maximum | Phillips-Perron Test for Unit Root |

|---|---|---|---|---|---|---|

| Armenia, GDP | 79 | 0.0168 | 0.0531 | −0.2336 | 0.1118 | −6.793 *** |

| Azerbaijan, GDP | 79 | 0.0154 | 0.1191 | −0.3315 | 0.5595 | −9.133 *** |

| Belarus, GDP | 79 | −0.0228 | 0.1240 | −0.5153 | 0.2956 | −7.466 *** |

| Kazakhstan, GDP | 79 | 0.0112 | 0.0856 | −0.4730 | 0.1418 | −6.872 *** |

| Kyrgyzstan, GDP | 79 | 0.0115 | 0.0494 | −0.1547 | 0.1842 | −8.043 *** |

| Moldova, GDP | 79 | 0.0100 | 0.0644 | −0.2282 | 0.3377 | −10.016 *** |

| Russia, GDP | 79 | 0.0014 | 0.0920 | −0.4075 | 0.1696 | −6.880 *** |

| Tajikistan, GDP | 79 | 0.0035 | 0.0961 | −0.3277 | 0.4625 | −13.183 *** |

| Ukraine, GDP | 79 | −0.0056 | 0.0976 | −0.4399 | 0.1925 | −5.369 *** |

| Russian trade with CIS | 79 | −0.0094 | 0.1083 | −0.4725 | 0.1680 | −6.681 *** |

| Variables | Observations | Mean | Standard Deviation | Minimum | Maximum | Phillips-Perron Test for Unit Root |

|---|---|---|---|---|---|---|

| Armenia | 250 | −0.0006 | 0.0205 | −0.0961 | 0.1801 | −14.225 *** |

| Azerbaijan | 250 | 0.0025 | 0.0265 | −0.1072 | 0.2083 | −12.047 *** |

| Belarus | 250 | 0.0121 | 0.0511 | −0.2095 | 0.4243 | −12.538 *** |

| Kazakhstan | 250 | 0.0043 | 0.0573 | −0.3330 | 0.3524 | −16.394 *** |

| Kyrgyzstan | 250 | 0.0022 | 0.0410 | −0.2670 | 0.4815 | −27.364 *** |

| Moldova | 250 | 0.0013 | 0.0204 | −0.1279 | 0.1201 | −13.752 *** |

| Russia | 250 | 0.0038 | 0.0341 | −0.1400 | 0.1680 | −8.744 *** |

| Tajikistan | 250 | 0.0065 | 0.1118 | −1.3263 | 1.0986 | −38.226 *** |

| Ukraine | 250 | 0.0063 | 0.0562 | −0.2480 | 0.3886 | −18.801 *** |

| Independent Variables | Dependent Variables | |||||||

|---|---|---|---|---|---|---|---|---|

| GDP | Trade with CIS | GDP | Trade with CIS | |||||

| Coef. | Std. Err. | Coef. | Std. Err. | Coef. | Std. Err. | Coef. | Std. Err. | |

| GDP, L1 | ||||||||

| −0.1682 | 0.1515 | −0.0322 | 0.1840 | −0.2832 ** | 0.1331 | −0.0021 | 0.1514 | |

| GDP, L2 | −0.2686 ** | 0.1240 | 0.0528 | 0.1410 | ||||

| Trade with CIS, L1 | 0.4545 *** | 0.1287 | 0.3018 * | 0.1563 | 0.3190 *** | 0.1162 | −0.0200 | 0.1322 |

| Trade with CIS, L2 | 0.2530 ** | 0.1111 | 0.0151 | 0.1264 | ||||

| Sanctions | −0.0846 *** | 0.0199 | −0.0887 *** | 0.0227 | ||||

| Financial crisis | −0.2823 *** | 0.0527 | −0.4413 *** | 0.0600 | ||||

| Constant | 0.0060 | 0.0095 | −0.0038 | 0.0116 | 0.0304 *** | 0.0088 | 0.0218 ** | 0.0100 |

| Lagrange-multiplier test | ||||||||

| Lags | Test statistics | p | Test statistics | p | ||||

| L1 | 6.2965 | 0.1781 | 5.0124 | 0.2860 | ||||

| L2 | 8.0097 | 0.0912 | 6.8575 | 0.1436 | ||||

| L3 | 3.3155 | 0.5065 | 4.0759 | 0.3958 | ||||

| L4 | 7.0072 | 0.1355 | 7.8579 | 0.0969 | ||||

| Sample period: 2000Q3–2019Q4 Selection-order criteria: AIC | Johansen tests for cointegration | |||||||

| Maximum rank | Trace statistic | 5% critical value | ||||||

| 0 | 9.1508 * | 15.41 | ||||||

| 1 | 1.3976 | 3.76 | ||||||

| Independent Variables | Dependent Variables | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Russia | Armenia | Kyrgyzstan | Moldova | Tajikistan | ||||||

| Coef. | Std. Err. | Coef. | Std. Err. | Coef. | Std. Err. | Coef. | Std. Err. | Coef. | Std. Err. | |

| Russia | ||||||||||

| L1 | 0.0782 | 0.1255 | 0.2086 *** | 0.0610 | 0.0758 | 0.0697 | 0.2021 ** | 0.0842 | 0.4181 *** | 0.1092 |

| L2 | −0.1970 | 0.1425 | 0.0289 | 0.0693 | 0.0386 | 0.0791 | 0.1845 * | 0.0956 | 0.0258 | 0.1240 |

| Armenia | ||||||||||

| L1 | 0.3915 * | 0.2192 | 0.0596 | 0.1066 | 0.2177 * | 0.1217 | 0.1397 | 0.1470 | −0.3635 * | 0.1907 |

| L2 | −0.2817 | 0.2189 | 0.4120 *** | 0.1064 | −0.0463 | 0.1215 | −0.0147 | 0.1468 | 0.4426 ** | 0.1905 |

| Kyrgyzstan | ||||||||||

| L1 | 0.2588 | 0.2559 | −0.0272 | 0.1244 | −0.1609 | 0.1420 | −0.1349 | 0.1716 | 0.1257 | 0.2226 |

| L2 | 0.3158 | 0.2561 | 0.0187 | 0.1245 | −0.0273 | 0.1422 | 0.0454 | 0.1718 | −0.0330 | 0.2228 |

| Moldova | ||||||||||

| L1 | 0.2615 | 0.1725 | −0.0033 | 0.0838 | 0.0567 | 0.0957 | −0.2597 ** | 0.1157 | −0.0236 | 0.1500 |

| L2 | 0.2162 | 0.1693 | −0.1367 * | 0.0823 | 0.0619 | 0.0940 | 0.0011 | 0.1135 | 0.0832 | 0.1473 |

| Tajikistan | ||||||||||

| L1 | −0.0724 | 0.1290 | −0.0120 | 0.0627 | −0.0575 | 0.0716 | −0.0742 | 0.0865 | −0.4342 *** | 0.1123 |

| L2 | −0.0276 | 0.1196 | 0.0045 | 0.0582 | −0.0030 | 0.0664 | 0.0468 | 0.0802 | −0.0805 | 0.1041 |

| Constant | −0.0106 | 0.0110 | 0.0105 ** | 0.0053 | 0.0086 | 0.0061 | 0.0109 | 0.0074 | 0.0020 | 0.0095 |

| Lagrange-multiplier test | Johansen tests for cointegration | |||||||||

| Lags | Test statistics | p | Maximum rank | Trace statistic | 5% critical value | |||||

| L1 | 33.7134 | 0.1142 | 0 | 61.2470 * | 68.52 | |||||

| L2 | 35.4492 | 0.0804 | 1 | 32.8337 | 47.21 | |||||

| L3 | 21.8152 | 0.6464 | 2 | 10.8622 | 29.68 | |||||

| L4 | 29.5718 | 0.2407 | 3 | 3.6337 | 15.41 | |||||

| Selection-order criteria: AIC | 4 | 0.8933 | 3.76 | |||||||

| Sample period: 2000Q4–2019Q4 | ||||||||||

| Independent Variables | Dependent Variables | |||||

|---|---|---|---|---|---|---|

| Russia | Belarus | Ukraine | ||||

| Coef. | Std. Err. | Coef. | Std. Err. | Coef. | Std. Err. | |

| Russia, L1 | 0.1288 | 0.1521 | −0.0410 | 0.2080 | 0.3699 *** | 0.1435 |

| Belarus, L1 | −0.0507 | 0.0881 | 0.1116 | 0.1204 | −0.0937 | 0.0831 |

| Ukraine, L1 | 0.1754 | 0.1379 | 0.2072 | 0.1886 | 0.2524 * | 0.1301 |

| Constant | 0.0010 | 0.0103 | −0.0178 | 0.0141 | −0.0069 | 0.0097 |

| Lagrange-multiplier test | Johansen tests for cointegration | |||||

| Lags | Test statistics | p | Maximum rank | Trace statistic | 5% critical value | |

| L1 | 10.5274 | 0.3095 | 0 | 21.7939 * | 29.68 | |

| L2 | 12.7311 | 0.1752 | 1 | 7.5718 | 15.41 | |

| L3 | 3.7303 | 0.9283 | 2 | 0.7204 | 3.76 | |

| L4 | 9.5130 | 0.3913 | ||||

| Sample period: 2000Q3–2019Q4 | ||||||

| Selection-order criteria: AIC | ||||||

| Independent Variables | Dependent Variables | ||||

|---|---|---|---|---|---|

| Russia | Azerbaijan | ||||

| Coef. | Std. Err. | Coef. | Std. Err. | ||

| Russia, L1 | 0.1890 | 0.1204 | 0.3672 ** | 0.1547 | |

| Azerbaijan, L1 | 0.0699 | 0.0930 | −0.1623 | 0.1196 | |

| Constant | 0.0000 | 0.0102 | 0.0164 | 0.0131 | |

| Lagrange-multiplier test | Johansen tests for cointegration | ||||

| Lags | Test statistics | p | Maximum rank | Trace statistic | 5% critical value |

| L1 | 4.3609 | 0.3594 | 0 | 15.1713 * | 15.41 |

| L2 | 5.0483 | 0.2824 | 1 | 2.4839 | 3.76 |

| L3 | 1.7647 | 0.7789 | |||

| L4 | 15.2270 | 0.0043 | |||

| Sample period: 2000Q3–2019Q4 | |||||

| Selection-order criteria: AIC | |||||

| Independent Variables | Dependent Variables | |||||

|---|---|---|---|---|---|---|

| Kazakhstan | Russia | ECT L1 | ||||

| Coef. | Std. Err. | Coef. | Std. Err. | Coef. | Std. Err. | |

| ECT, L1 | −0.1051 ** | 0.0429 | 0.0268 | 0.0465 | ||

| Kazakhstan, L1 | 0.2167 * | 0.1124 | 0.5816 *** | 0.1217 | 1 | |

| Kazakhstan, L2 | −0.1815 | 0.1286 | −0.3844 *** | 0.1393 | ||

| Kazakhstan, L3 | −0.1225 | 0.1320 | 0.1342 | 0.1429 | ||

| Russia, L1 | 0.1794 | 0.1241 | 0.2185 | 0.1344 | −1.1666 *** | 0.2006 |

| Russia, L2 | −0.2005 * | 0.1173 | −0.0772 | 0.1271 | ||

| Russia, L3 | 0.3996 *** | 0.1081 | 0.1044 | 0.1171 | ||

| Constant | 0.0002 ** | 0.0095 | 0.0006 * | 0.0103 | 4.4207 | |

| Lagrange-multiplier test | Johansen tests for cointegration | |||||

| Lags | Test statistics | p | Maximum rank | Trace statistic | 5% critical value | |

| L1 | 7.4092 | 0.1158 | 0 | 17.162 | 15.41 | |

| L2 | 7.0568 | 0.1329 | 1 | 2.6537 * | 3.76 | |

| L3 | 7.3177 | 0.1200 | ||||

| L4 | 6.0329 | 0.1967 | ||||

| Sample period: 2001Q2–2019Q4 | ||||||

| Armenia | Belarus | Kazakhstan | Kyrgyzstan | Moldova | Russia | Tajikistan | Ukraine | |

|---|---|---|---|---|---|---|---|---|

| Armenia | 3.2482 | 6.9952 | 9.6471 ** | 13.3300 *** | 3.2780 | 101.6500 *** | 3.0803 | |

| Belarus | 1.7136 | 3.7323 | 0.4962 | 2.2602 | 2.9887 | 1.1559 | 5.9091 | |

| Kazakhstan | 4.9543 | 0.2997 | 6.0789 | 1.4152 | 3.1492 | 7.6718 | 1.5528 | |

| Kyrgyzstan | 1.1362 | 3.7207 | 3.5109 | 4.0569 | 1.5982 | 5.5590 | 0.9200 | |

| Moldova | 3.3712 | 1.6867 | 1.3316 | 2.1955 | 5.0490 | 3.3052 | 3.4693 | |

| Russia | 19.0850 *** | 17.4480 *** | 13.8910 *** | 23.5410 *** | 35.0900 *** | 3.9888 | 24.8070 *** | |

| Tajikistan | 1.6939 | 4.9404 | 0.7280 | 0.5820 | 10.8840 ** | 3.3138 | 1.3074 | |

| Ukraine | 7.9161 * | 2.4080 | 0.8983 | 1.2734 | 3.2595 | 1.8719 | 13.2210 *** | |

| All | 51.8000 *** | 29.1010 | 35.943 | 65.2340 *** | 82.3160 *** | 25.0710 | 163.3800 *** | 74.4190 *** |

| Lagrange-multiplier test | Johansen tests for cointegration | |||||||

| Lags | Test statistics | p | Maximum ranks | Trace statistic | 5% critical value | |||

| Sample period: 2001M6-2021M11 Selection-order criteria: AIC Number of lags for VAR: 4 | 1 | 64.8755 | 0.4459 | 0 | 143.1525 * | 156.00 | ||

| 2 | 65.1731 | 0.4357 | 1 | 101.6010 | 124.24 | |||

| 3 | 59.5087 | 0.6358 | 2 | 67.2589 | 94.15 | |||

| 4 | 64.2233 | 0.4687 | 3 | 42.1854 | 68.52 | |||

| Armenia | Belarus | Kazakhstan | Kyrgyzstan | Moldova | Tajikistan | Ukraine | |

|---|---|---|---|---|---|---|---|

| Russia, L1 | 0.187 *** (0.049) | 0.394 *** (0.126) | 0.513 *** (0.140) | 0.334 *** (0.085) | 0.226 *** (0.046) | −0.055 (0.177) | 0.529 *** (0.129) |

| Russia, L2 | 0.018 (0.059) | −0.184 (0.150) | −0.237 (0.166) | 0.070 (0.102) | 0.085 (0.055) | 0.042 (0.211) | 0.088 (0.154) |

| Russia, L3 | −0.051 (0.057) | 0.029 (0.145) | 0.090 (0.160) | −0.129 (0.098) | −0.021 (0.053) | −0.108 (0.203) | 0.335 ** (0.149) |

| Russia, L4 | 0.068 (0.054) | −0.311 ** (0.138) | −0.011 (0.153) | 0.193 ** (0.093) | 0.030 (0.051) | 0.372 * (0.194) | 0.082 (0.142) |

| Sanctions | Exchange Rate of Ruble |

|---|---|

| All | 0.004 (0.007) |

| Economic sanctions | 0. 031 *** (0.010) |

| Financial sanctions | 0.028 ** (0.012) |

| Corporate sanctions | −0.021 *** (0.007) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sultonov, M. Regional Economic and Financial Interconnectedness and the Impact of Sanctions: The Case of the Commonwealth of Independent States. J. Risk Financial Manag. 2022, 15, 565. https://doi.org/10.3390/jrfm15120565

Sultonov M. Regional Economic and Financial Interconnectedness and the Impact of Sanctions: The Case of the Commonwealth of Independent States. Journal of Risk and Financial Management. 2022; 15(12):565. https://doi.org/10.3390/jrfm15120565

Chicago/Turabian StyleSultonov, Mirzosaid. 2022. "Regional Economic and Financial Interconnectedness and the Impact of Sanctions: The Case of the Commonwealth of Independent States" Journal of Risk and Financial Management 15, no. 12: 565. https://doi.org/10.3390/jrfm15120565