Abstract

This study aims to synthesize the literature on the top management team (TMT) characteristics influence on environmental disclosures of public organizations and identify recent trends, key themes, influential journals, and authors. Our study recruited 88 research articles on the relationship of TMT characteristics and environmental disclosures from 54 academic journals published from 2010 to 2021 for bibliometric analysis. Our study has identified three influential streams: (1) Role of Politically connections of TMT, good governance in environmental disclosures; (2) Significance of environmental disclosures and performance; and (3) institutional investors and environmental disclosures. Thematic map classifies the TMT characteristics and environmental disclosures relationship themes into four categories: Niche theme (e.g., financial expertise, CFO characteristics, CEO tenure, and board backgrounds); motor themes (e.g., environmental sustainability and climate change); emerging/declining themes (e.g., Environmental disclosure, managerial ownership, and CEO tenure); and basic/transversal themes (e.g., CEO characteristics, upper echelon theory, corporate governance). This study assists academicians, policymakers, managers, and consultants in the corporate sector to understand the role of different dimensions of TMT characteristics regarding environmental disclosures. Our study concludes with important practical implications and future research directions.

1. Introduction

Environmental disclosures by public organizations have gained immense attention as an important area of research in recent years due to adverse climate change (Bilal et al. 2021; Ramos-Meza et al. 2021). Different stakeholders of corporations, such as customers, investors, managers, regulators, employees, etc., respond positively to high environmental disclosures (Fromont et al. 2022; López-Concepción et al. 2021; Radhouane et al. 2020; Sutantoputra 2021). Firms legitimize the whole process of a firm’s operations by paying back to society through reliable and transparent environmental disclosures. Institutional theory (Luo et al. 2017; Marquis and Qian 2014) and stakeholder theory (Donaldson 1999; Thijssens et al. 2015) view environmental disclosures as a response to the pressure mount by different stakeholders such as governments, activists, and other important stakeholders (Reid and Toffel 2009; Sutantoputra 2021; Van Aaken et al. 2013). These environmental disclosures matter a lot for sustainability literature, specifically when nuclear and alternative energy generation is discussed (Bilal et al. 2022; Khan et al. 2022; Lyu et al. 2022) and in the era of COVID-19 (Adebayo et al. 2022; Fareed et al. 2021; Shuai et al. 2021).

The reporting of environmental disclosures is voluntary in most countries; that is why top management discretion in the decision of environmental disclosures and spending becomes very important (Hambrick 2007). Top management is answerable to shareholders and the board of directors for environmental disclosure reporting activities (Hambrick and Mason 1984). Managerial preferences play a vital role in environmental disclosure spending because of the voluntary nature and management discretion (Hemingway and Maclagan 2004). Another important element is the competitive factors. Most companies want to become “environmental friendly” to create a good social impact on their stakeholders, urging top management to take appropriate environmental disclosures initiatives (Kuo and Chen 2013; Rashed et al. 2022). The third important factor recognized by academicians is top manager’s characteristics are important facets in determining how businesses respond to institutional pressures and CSR reporting. Specifically, given the CEO’s pivotal position in corporate decision-making, researchers examined how several demographic and personality characteristics (e.g., gender, age, educational background, experience, personality, political orientation, religious views, experience, leadership style, strength, and media exposure) influence their companies’ environmental reporting decisions.

As a result, some studies show that TMT/CEO characteristics significantly affect their companies’ environmental strategies (Lewis et al. 2014; Shah et al. 2021; Shahab et al. 2018; Zhou et al. 2021), and the associated environmental disclosure (Clarkson et al. 2006; Elmagrhi et al. 2019; Khan et al. 2021; Kim and Ferguson 2019; Li et al. 2018; Meng et al. 2013; Meng et al. 2015). However, the prior literature has examined this issue over the years, and a shared view is still lacking. Although recently, several studies have reviewed the environmental disclosures literature (Borghei 2021; Hahn et al. 2015; He et al. 2021; Velte et al. 2020; Zhang and Liu 2020). However, none of these studies has focused on TMT characteristics and environmental disclosures.

Therefore, this study set out to synthesize the literature on the top management team (TMT) characteristics’ influence on CSR disclosures of firms and identify recent trends, key themes, influential journals, and authors in recent years. Adopting to borderer perspective and addressing recent calls for more research on this topic, our study addresses the following three research questions:

RQ1. What are the most influential aspects of TMT characteristics and environmental disclosure literature?

RQ2. What are the major patterns and core themes in this topic?

RQ3. What lessons can we draw from the past literature to plan for the future, and what future agendas can be set?

Our study contributes to this contemporary research in the sustainable finance and business literature in several ways. First, our study provides a complete summary of this fragmented literature using big data technology, a bibliometric analysis. Second, our study identifies the historical milestones, such as the most influential papers, authors, journals, and institutions in this field. Our study also highlights the top research trends and themes in this research domain. Third, our study provides implications for the companies’ policymakers, regulators, and managers regarding the importance of CEO characteristics in CSR management activities. Finally, our study offers suggestions for the researchers to extend this research domain.

2. Materials and Methods

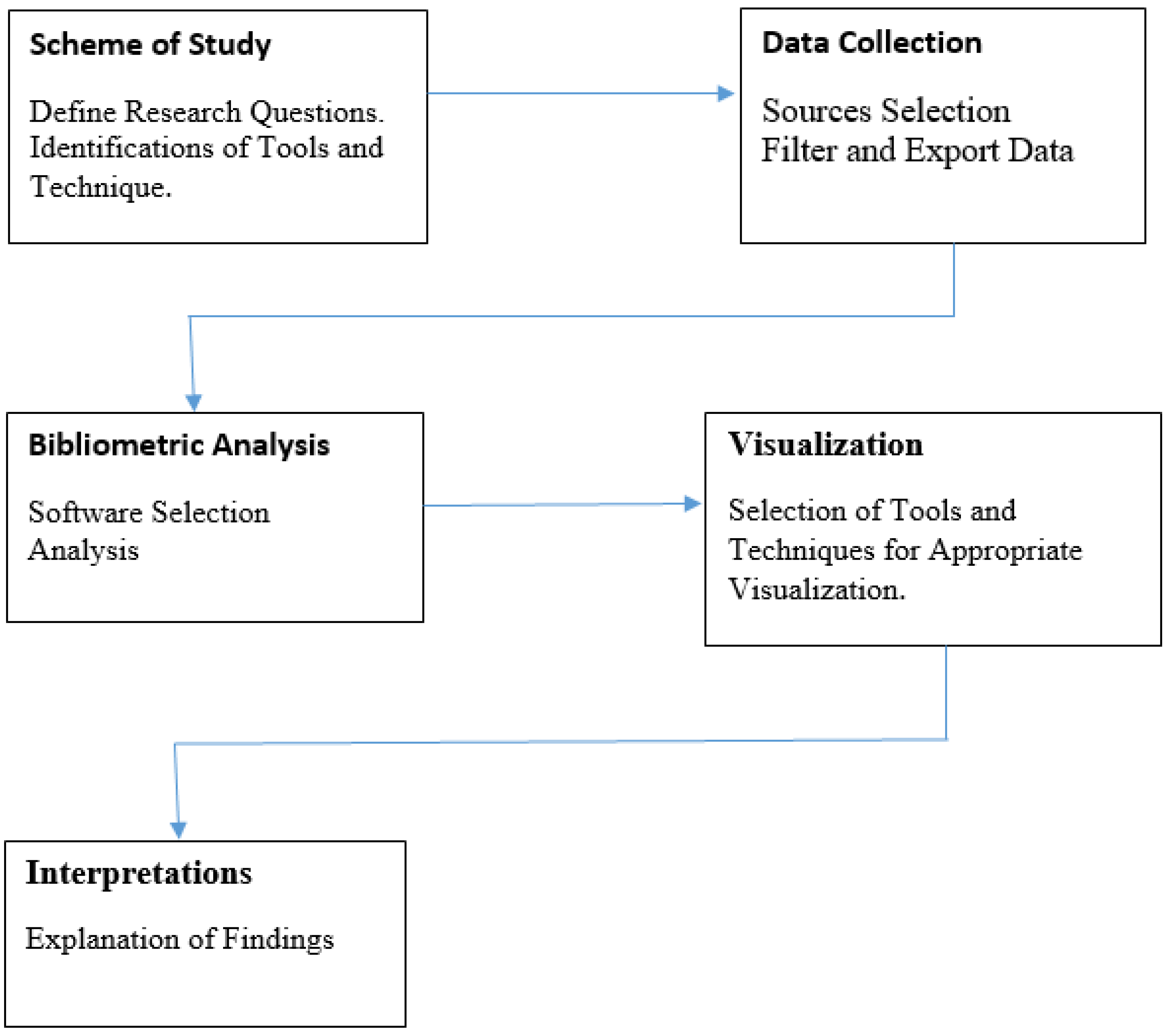

2.1. Five-Step Process of Bibliometric Analysis

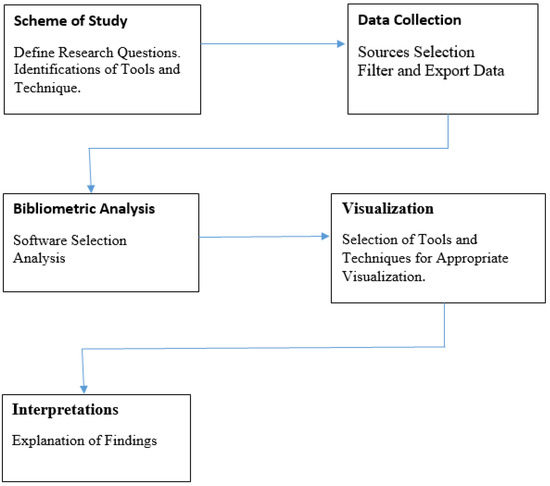

This article follows a five-step process suggested by Silvente et al. (2018), known as a bibliometric workflow. The five steps in the bibliometric study of TMT characteristics and CSR disclosure are depicted in Figure 1.

Figure 1.

Process of Bibliometric Analysis.

2.2. Scheme of Study

The current global environment poses many concerns that must be addressed. This study answered RQ1 (e.g., What are the most influential aspects of TMT characteristics and environmental disclosure literature?) with descriptive analysis and identified core sources, authors, countries, publications, and affiliation in the TMT characteristics and environmental disclosure publications. We used source influence, total citations, and net publications (NP) per year for core sources and authors. We also use Bradford’s Law to classify the primary sources. Sources are divided into three zones according to Bradford’s Law. Area 1 is the most active zone and is also known as the nuclear zone. Zone 2 is moderately active, while zone 3 is barely productive in comparison to Zone 1 and Zone 2 (Viju and Ganesh 2013). Based on the frequency of publications and total citations, we recommend the top countries and affiliations.

To address the RQ2, we have identified key trends and themes from the literature on TMT characteristics and environmental disclosures through co-occurrence maps, thematic maps, and thematic evolution. Research streams and themes are identified from authors keywords and keywords plus (e.g., system-generated keywords) of the selected studies, operated in ‘biblioshiny’, a bibliometric tool provided by the R-program. For RQ3, the future research agenda of the study is derived from our findings.

2.3. Objectives, Tools, and Techniques

The current study objective is to conduct a bibliometric overview of TMT characteristics and environmental disclosure literature. We use ‘biblioshiny,’ a web-specific R package (‘bibliometrix 3.0’). The first objective is analyzing the most influential aspects through descriptive analysis, Bradford’s Law, global citation, h, g, and m-index are some of the research tools available via the biblioshiny GUI. The second goal is to identify the major research sources and themes. We are going to use science mapping techniques of conceptual structure as well as authors keywords and keywords plus as input data to achieve this goal. We will provide a concise interpretation and identify future research agendas once we have addressed objectives 1 and 2.

2.4. Composing of Bibliomatric Data

Our bibliometric data is divided into two parts. Following the prior bibliometric studies (Chaudhuri et al. 2020; Faruk et al. 2021; Khudzari et al. 2018; Yas et al. 2020), we have used the Scopus database to select related literature. The final search query is (TITLE-ABS-KEY (carbon OR “Carbon emission*” OR “climate change” OR ghg OR “greenhouse gas*” OR environment*) AND TITLE (“Top management team” OR “TMT” OR “CEO” OR “CFO” OR “director*” OR “executive*” or “manager*”) AND TITLE-ABS-KEY (disclosure*)) AND (LIMIT-TO (LANGUAGE, “English”)). The query was run on the Scopus database on 10 January 2022. Initially, 148 articles were retrieved related to our search query. Most related articles on our topic, which we have selected, are 88 from 54 journals from 2010 to 2022 based on studies that have examined the relationship between TMT characteristics and environmental disclosures.

2.5. Bibliometric Analysis and Visualization

Biblioshiny is a R package designed for non-coders to provide full scientometric and bibliometric analysis with various options grouped into sources, records, writers, conceptual structure, social structure, and intellectual structure (Moral-Muñoz et al. 2020). Table A1 in Appendix A describes 88 selected studies from 54 journals with 214 keywords plus and 277 author’s keywords from 2010–2022. These documents were written by 236 authors, with only eight papers having a single author. The collaboration index 2.85 indicates a high level of collaboration in TMT characteristics and environmental disclosure publications. Collaboration by the single-authored documents is 8, the ratio of documents per author is 0.373, and the authors per documents ratio is 2.68. Collaboration with Co-authors per document is 2.85.

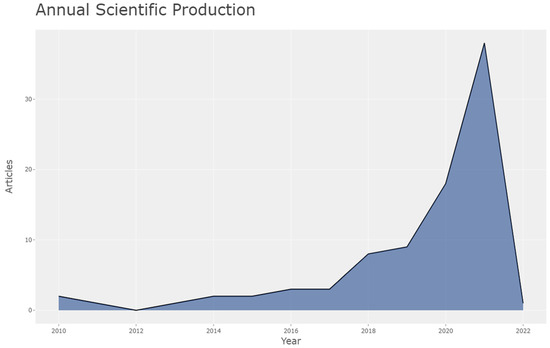

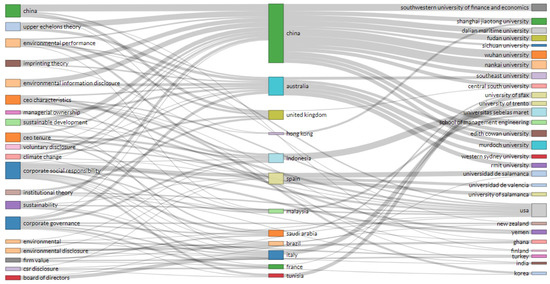

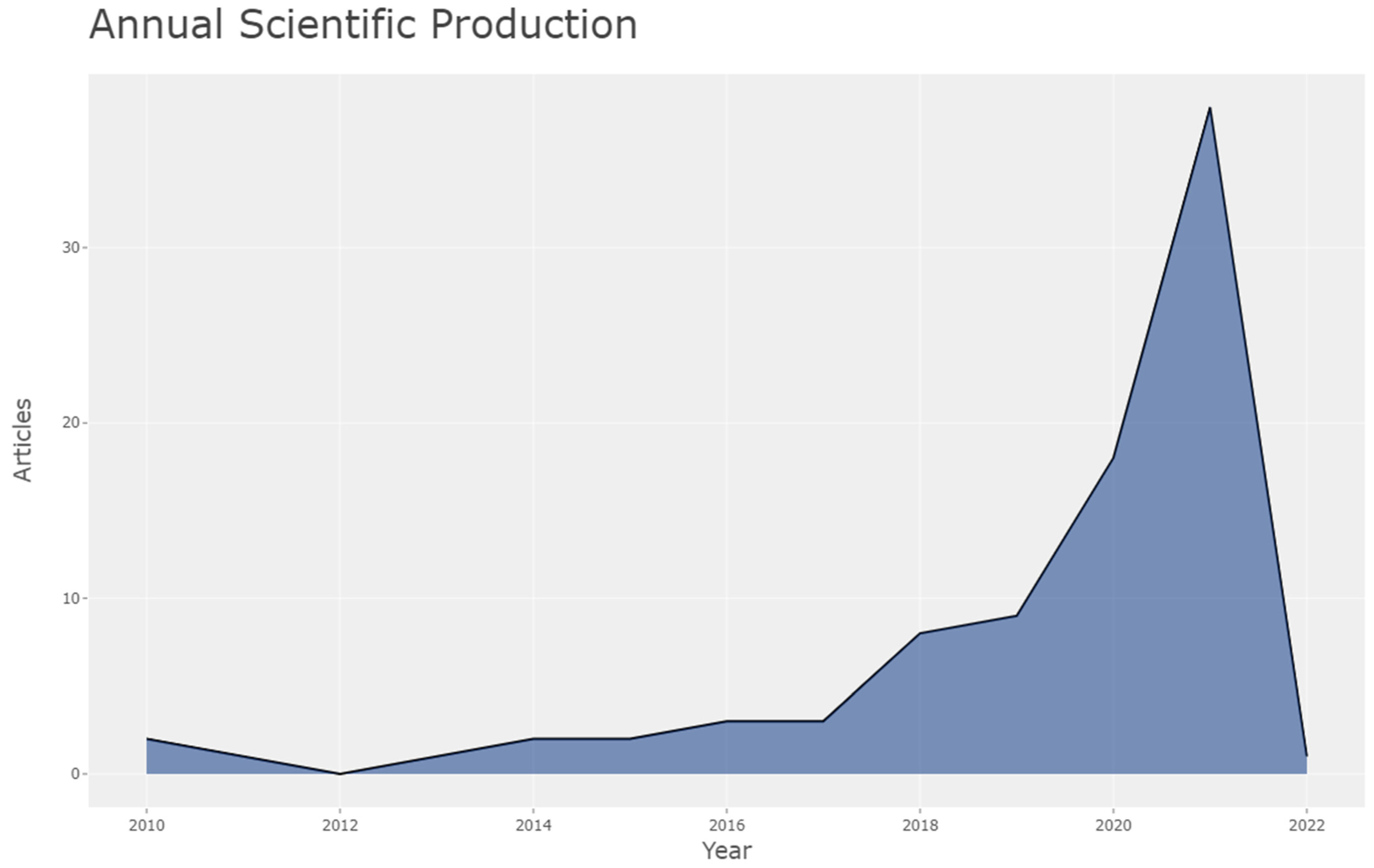

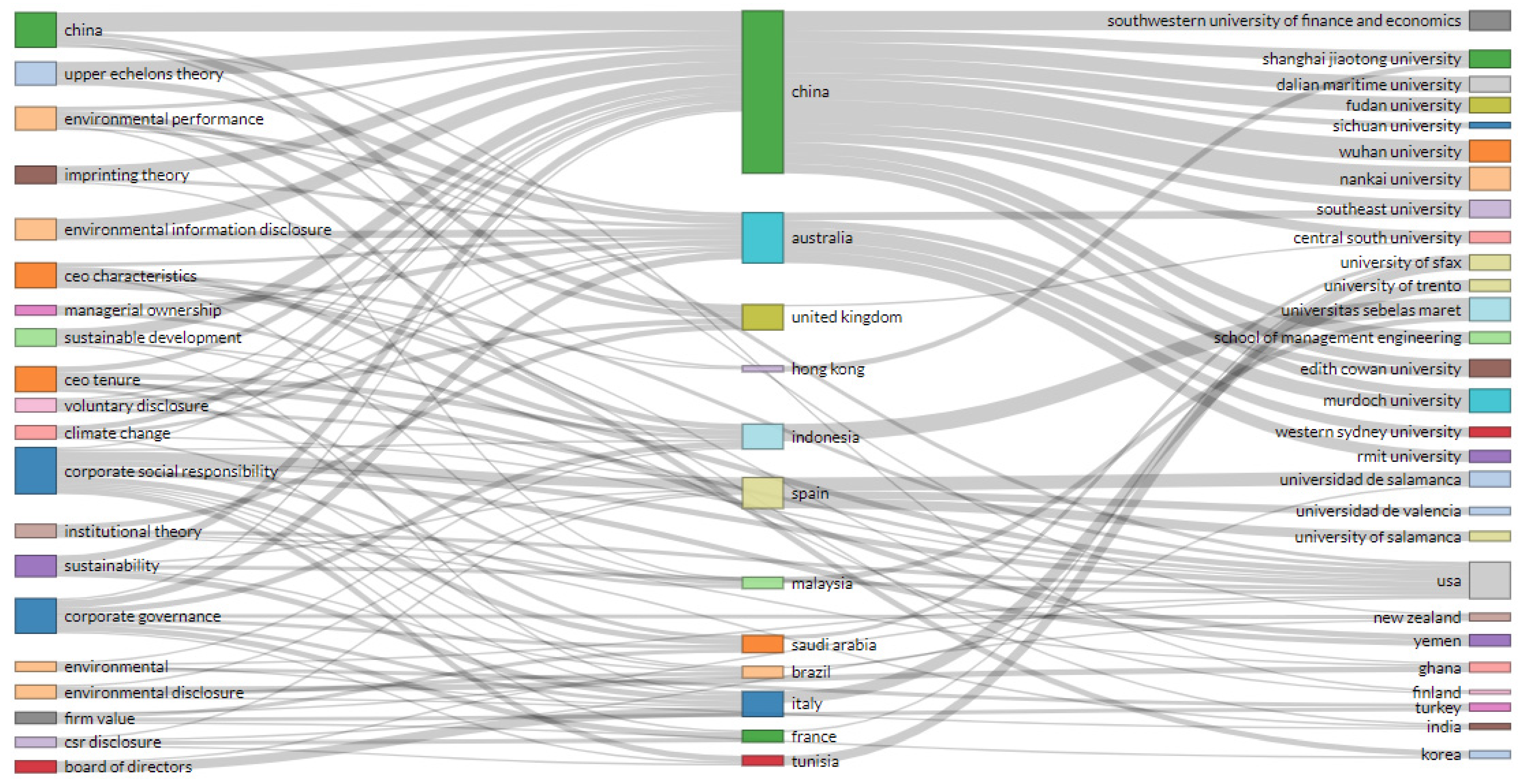

The annual production of TMT characteristics and environmental publications is depicted in Figure 2. From 2010 to 2017 publication of articles was very low among our selected studies. However, we have observed an upward trend in the publication on the topic in 2018. Figure 3 presents the three-field (e.g., keywords, countries, and their affiliation from left to right, respectively) analysis of the studies on the relationship between TMT characteristics and environmental disclosures. The most prominent affiliations in this literature are China, Australia, Spain, UK, and Italy. The most dominating keywords are environmental disclosures (e.g., environmental disclosure, environmental performance, and climate change), corporate social responsibility, CEO characteristics, and upper echelon theory. As China is the dominant country in publishing articles, Chinese universities are the most contributing affiliations, such as Nankai University, Wuhan University, and South Western University of Finance and economics.

Figure 2.

Annual Scientific Production.

Figure 3.

Three-field analysis of TMT characteristics and environmental disclosure literature.

3. Influential Aspects of TMT Characteristics and Environmental Disclosure

3.1. Core Journals

We use source impact and Bradford Law to find the key journals that publish TMT characteristics and environmental disclosure literature. According to the Bradford rule, as seen in Table 1, divides the journal into three zones. Zone 1 is immensely valuable and considered a nuclear zone. Zone 2 is slightly productive compared to Zone 1, and Zone 3 is barely productive compared to Zone 1 and 2. We discovered that six journals out of 54 fall into core zone 1, and the remaining ones fall into zones 2 and 3. Sustainability (Switzerland) is the top-ranked journal according to Bradford rule in Zone 1, and it has published 10articles on TMT characteristics and environmental disclosures. Table A2 in Appendix A shows the rankings of publications based on the h-, m-, and g-indexes, total citations, and net output (NP), as well as the publication year (PY start). Furthermore, top affiliations are suggested based on publication frequency and their citations.

Table 1.

Journal rankings.

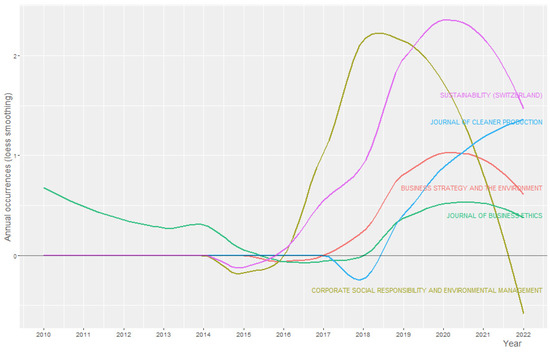

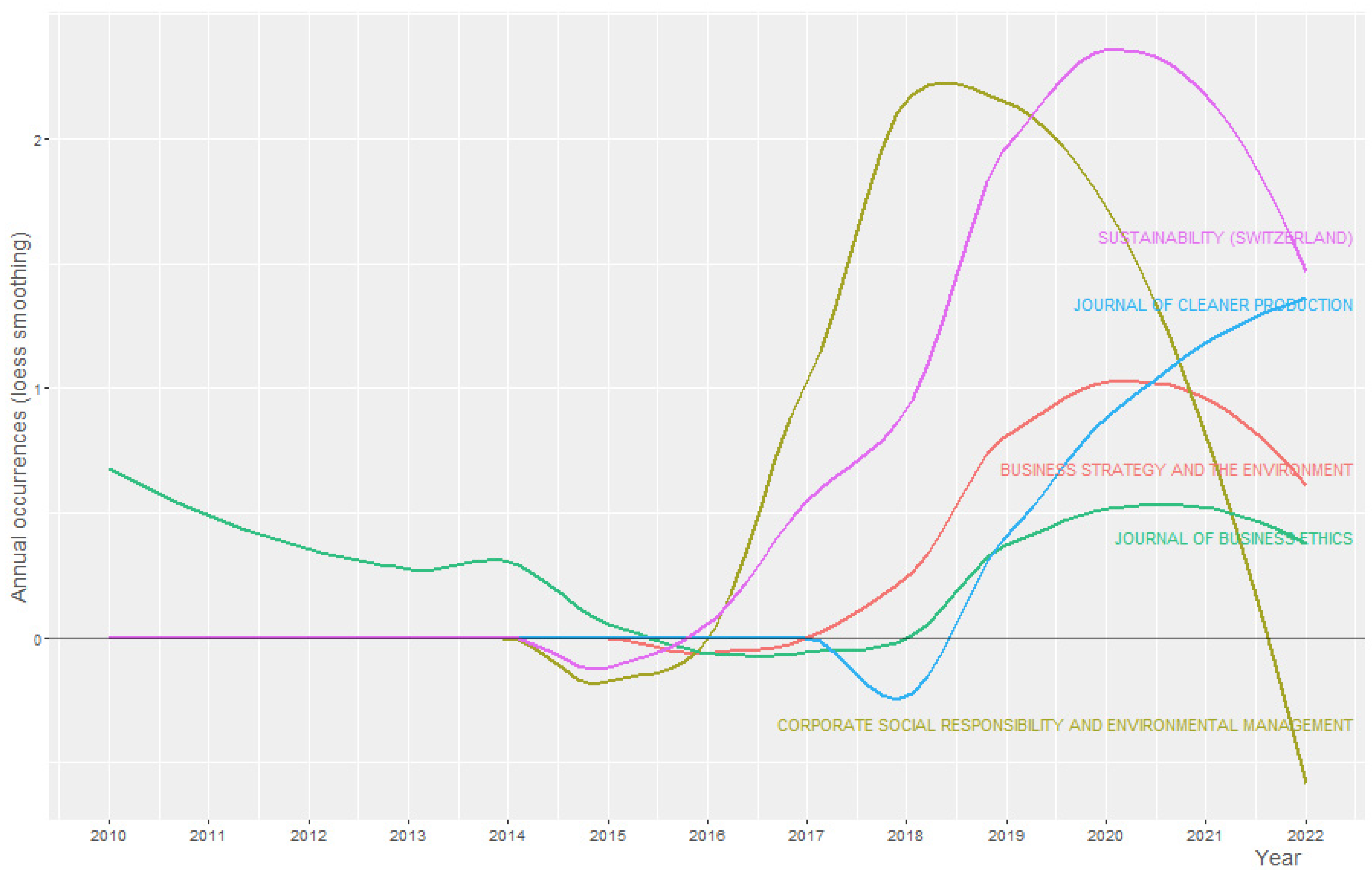

The growth in a publication by top journals is depicted in Figure 4. We use regression analysis to explain the smooth line with a time plot or scatter plot using the loess smoothing method, locally weighted smoothing. Loess smoothing aids in comprehending treads over time in a research field (Sauerbrei et al. 2006). From 2010–2015, there has been a decreasing trend. Since 2016, there has been a substantial increase in publications related to environmental disclosures and the top management team’s characteristics. There is an upward trend in Sustainability, Journal of Cleaner Production, and Business Strategy and Environment journals publications after 2016.

Figure 4.

Source Growth.

3.2. Core Journal Articles

The top papers in TMT characteristics and environmental disclosure publications are highlighted in this section. Table A3 in Appendix A shows the top 10 most-cited publications worldwide on the topic. In the first study, Prado-Lorenzo and Garcia-Sanchez (2010) published the most cited article with 283 citations and discussed the role of the board of directors in disseminating the greenhouse gasses information. They found that gender-diverse and independent boards of directors disseminate greenhouse gas information to stakeholders to avoid litigation risk and improve the image in front of stakeholders. The second, most influential article in the list with 200 citations is regarding the educational background of CEOs on environmental disclosure (Lewis et al. 2014). They concluded that newly appointed and MBA CEOs are more likely to report environmental information disclosure than older appointed and layer qualification CEOs. Likewise, other influential studies are presented in Table A3 of Appendix A.

3.3. Core Words

The most commonly used terms in TMT characteristics and environmental disclosure literature are mentioned in Table 2. In keyword plus, the keywords generated in the system, the frequent words include China, environmental management, industry, and managers. ‘The author’s most frequent keywords include corporate governance and corporate social responsibility, having the highest occurrence of 6 times. These keywords are related to TMT characteristics and environmental disclosure and show the relationship between these two variables.

Table 2.

Most frequent words.

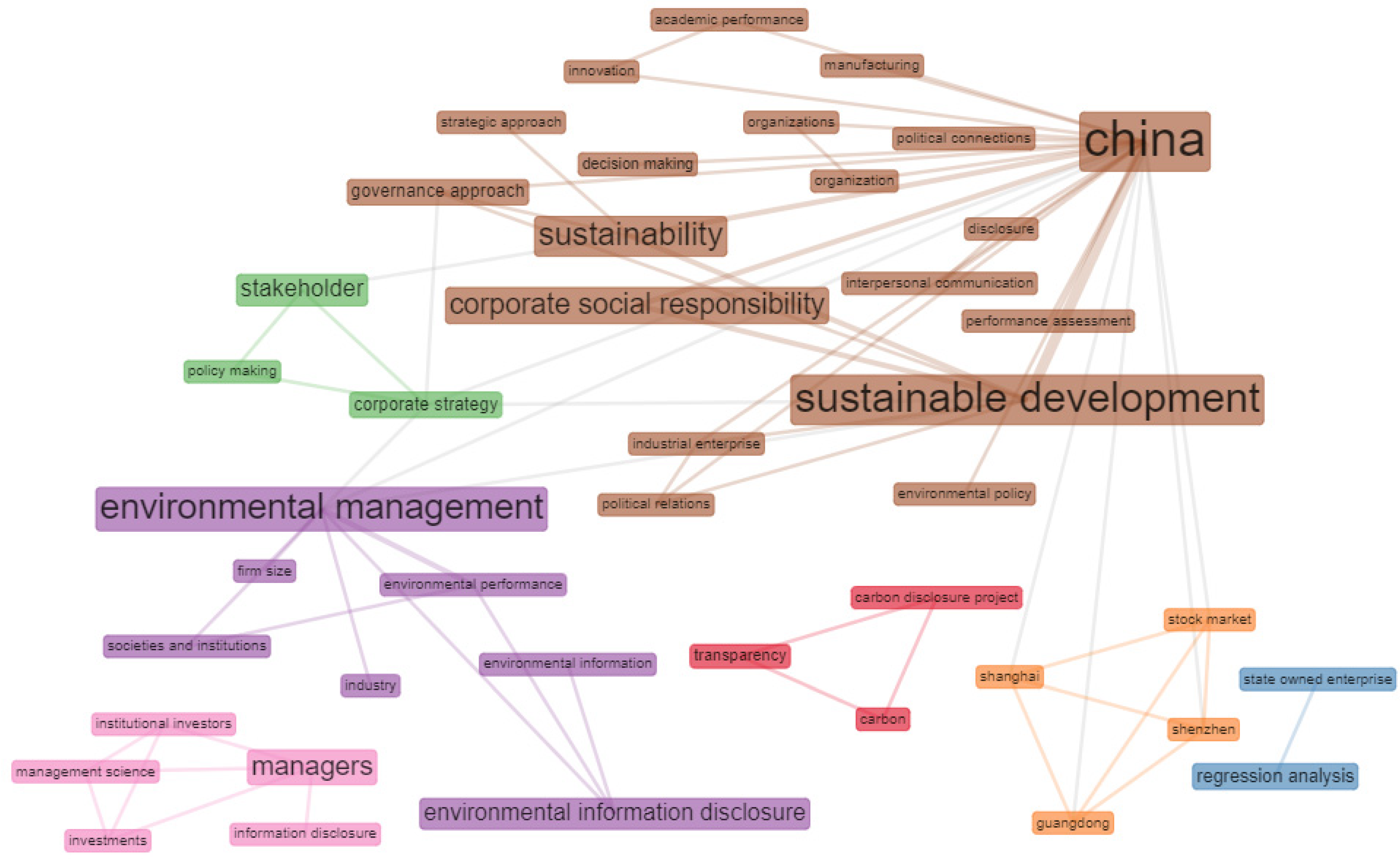

The word cloud generated from keyword plus is shown in Figure 5. Words that often appear in the literature have a larger font size. In the literature on TMT characteristics and environmental disclosure, the terms: Environmental management, CSR, and China appear most frequently. As a result, these are the most important terms used. Then there are stakeholders, corporate strategy, governance approach performance assessment, directors, boards, and corporate strategy in the literature.

Figure 5.

Word Cloud.

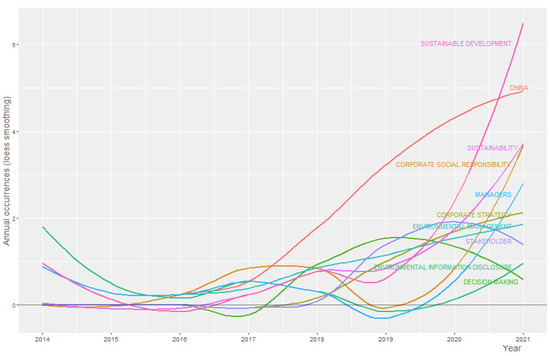

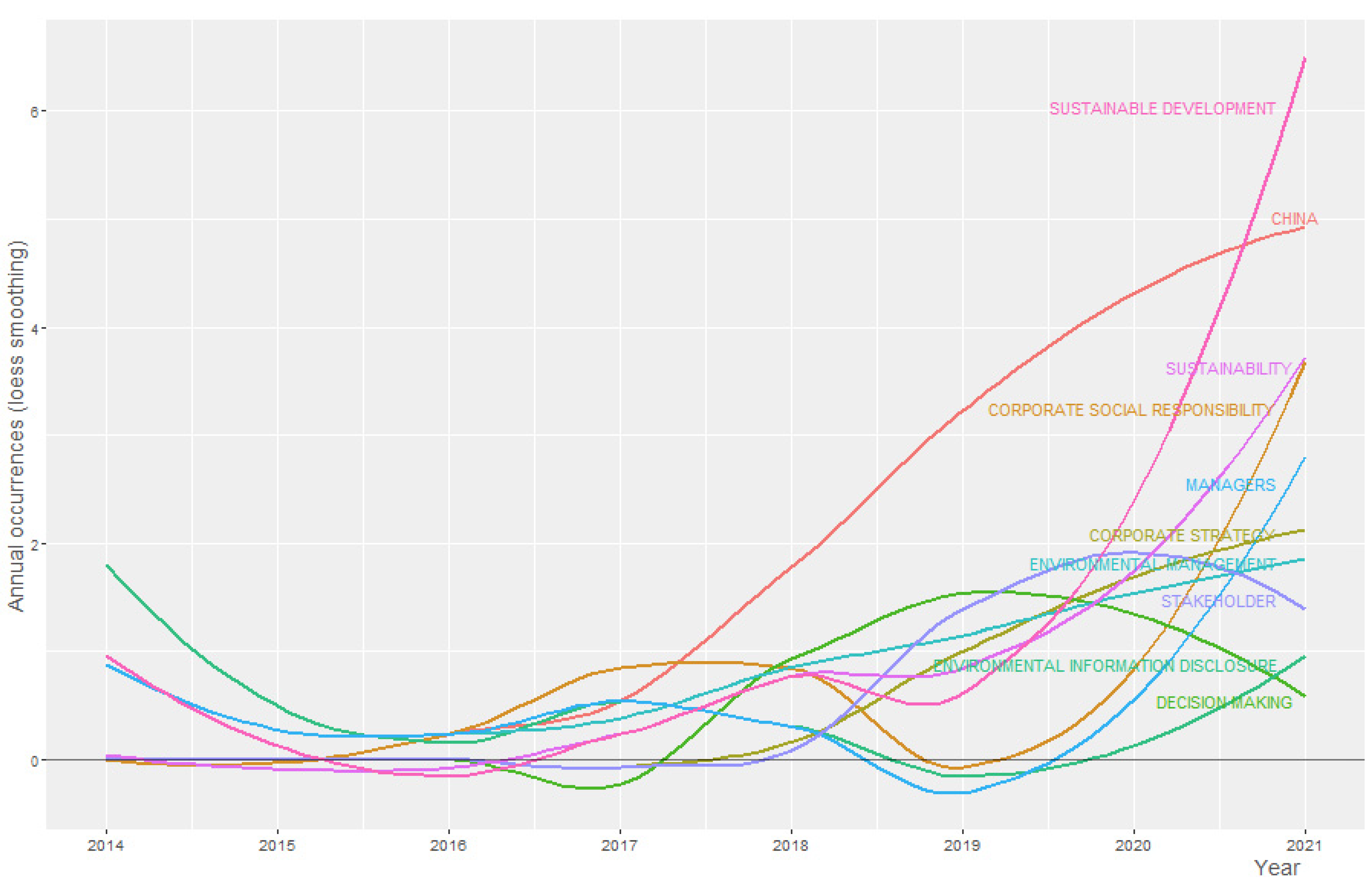

Figure 6 depicts the development of words in literature over time in addition to the word cloud. The keyword china began to expand in 2017, as seen in the graph. The keyword sustainability development also shows an increasing trend from 2017. Figure 6 examines the development of keywords over time using a loess smoothing technique. Since 2015, with a sharp rise in industry-related topics in 2017.

Figure 6.

Word Growth Overtime.

Table 3 displays two sets of data: on the left, the countries and regions with the most scientific outputs over time; on the right, the countries and regions with the least scientific productions. Countries with several citations can be found on the right side. Since Spain is the first most contributing country with 385 citations, the United Kingdom is second with 248 citations, and the USA is the third country with 243 citations.

Table 3.

Top countries in terms of publications and citations.

Table 4 shows the data for the top 10 corresponding author nations, with China ranking first. China’s corresponding authors contributed in 24 articles, 16of which are single country publications [SCP] and eight multiple country publications [MCP]. At least one co-author from a foreign country is needed for multiple country publications. The USA is in second place, with eight articles of correspondence. Four single-country publications and four multiple-country publications. Spain is in the third slot with five single-country publications and two multiple-country publications. The United Kingdom is fourth, with one single country publication and four multiple country publications.

Table 4.

Corresponding author’s country.

Table 5 depicts the international cooperation network between countries. Chinese and Australian authors have published three articles in collaboration. In contrast, Chinese authors published one article from Finland, three with Hong Kong, one with the United Kingdom and two with American authors.

Table 5.

Collaboration network.

4. Conceptual Framework

4.1. Co-Occurrence Network

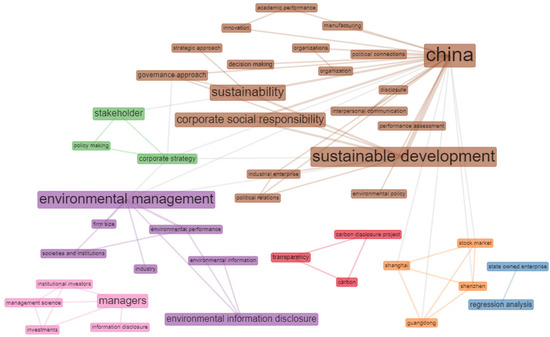

The co-occurrence network of the authors’ keywords is depicted in Figure 7. The figure is taken from the R-package’ biblioshiny’ (‘bibliometrix’). The co-occurrence network of keywords reveals four distinct streams of TMT characteristics literature with environmental and divided this literature into three clusters, brown, purple and pink.

Figure 7.

Co-occurrence network.

The brown cluster directs a research stream named: Politically connections; governance; decision-making strategy; and performance assessment role in organizational sustainable development. Thus, these search streams indicate the characteristics of the Chinese economy where corporate political connections of TMT and corporate governance-related issues are studied with environmental disclosures. Several studies in this cluster have examined the role of political connections of the TMT and environmental management in the USA (Jeong et al. 2021), in China (Zhang 2017; Zong et al. 2020; Arslan et al. 2021), and Vietnam (Tran and Pham 2020). These studies documented that TMT political connections negatively influence environmental performance.

The purple cluster focuses on the following research areas: the importance of environmental information disclosure in large firms’, environmental management, and environmental performance. Therefore, this cluster depicts the significance of environmental disclosures and performance considering the role of TMT characteristics. First, several studies documented that female CFOs, directors, and CEOs significantly enhance environmental performance (Elmagrhi et al. 2019; Tran and Pham 2020; Wang et al. 2021). Second, studies in the cluster found mixed evidence regarding the relationship between TMT education and environmental performance. Thus, few studies found TMT education enhance environmental performance documented that female CFOs, directors, and CEOs significantly enhance environmental performance (Lewis et al. 2014; Ma et al. 2019; Sarfraz et al. 2020; Tran and Pham 2020). However, Elmagrhi et al. (2019) found a no association between education of directors and environmental performance. Third stream of studies in this cluster focused on the influence of practical exposure of TMT on environmental performance. Mardini and Lahyani (2021) found that foreign directors with overseas experience in firm boards improve carbon performance and carbon disclosures.

The pink cluster covers the studies on environmental investment as the main research areas are Information disclosure by managers and institution investment strategy. The remaining small clusters collectively explain the presence of state-owned firms in Chinese listed firms and the importance of the carbon disclosure project (CDP) in information transparency. Following are the important studies in this cluster. For example, Pucheta-Martínez and López-Zamora (2018) discussed the role of two types of representatives of institutional investors in environmental reporting and concluded that banks and insurance companies’ representatives (e.g., pressure-sensitive institutional directors) have an insignificant relationship with firms’ environmental information disclosures because of short-term perspective of pressure-sensitive institutional directors. In contrast, a significant positive relationship has been identified between pressure-resistant institutional directors (e.g., mutual funds, investment funds, and pensions funds representatives) and environmental information disclosure because reassuring resistant directors have a long-term perspective for the firm that is why they focus on decisions that improve firms reputation and their personal reputation in front of stakeholders. Xu and Zhang (2017) have discussed the triangular relationship between managerial power, institutional investors, and environmental performance information disclosure in Chinese state-owned and private listed firms. They found that firms with more managerial powers discourage environmental performance information disclosure whereas stable institutional investors manage the powers of executives positively, which results in high environmental performance information disclosure.

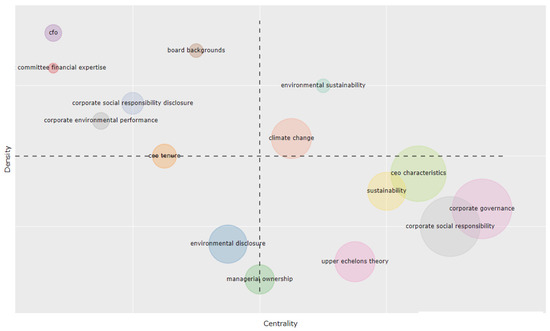

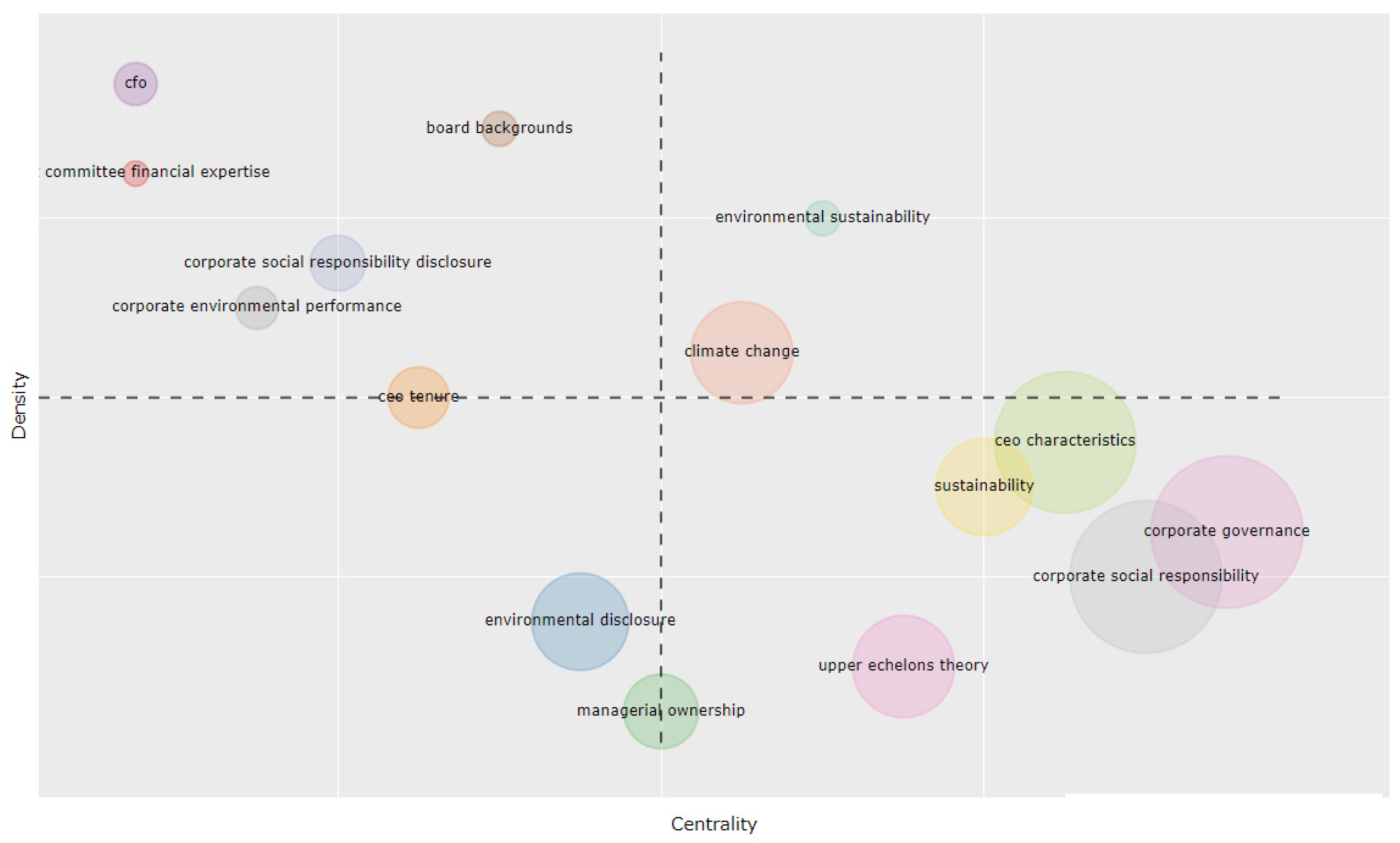

4.2. Thematic Map

To better understand the findings, we have identified some study themes. To evaluate the significance and creation of the research theme, we can group the established themes into a strategic diagram. The thematic map based on density (y-axis) and centrality (x-axis) is shown in Figure 8 (Cobo et al. 2011). The value of the chosen theme is measured by centrality. In contrast, the growth of the chosen theme is measured by its density. The graph is split into four parts. Emerging or decreasing themes are those that appear in the lower-left corner. These new themes may appear and improve the research field or fade away. The basic or transversal themes are found in the lower right corner of the thematic map. These themes have a low density but are very crucial. On these topics, a lot of research has been carried out.

Figure 8.

Thematic Map.

Environmental sustainability and climate change are the concepts present in the upper right corner of the thematic map called the motor theme. These themes represent the advancement of these concepts in TMT characteristics and environmental disclosure literature. CSR and corporate environmental performance are representative of sustainability disclosures. TMT characteristics relevant keywords are financial expertise, CFO characteristics, CEO tenure, and board backgrounds in the upper left corner of the thematic map called the niche theme, representing the well-developed concepts in the literature of TMT characteristics and environmental disclosures. These concepts are present in the niche theme of this topic. Environmental disclosure, managerial ownership, and CEO tenure are present in the lower-left corner named emerging/declining theme. Much research has been conducted in environmental disclosure literature in the context of managerial ownership and CEO tenure. CEO characteristics under the light of upper echelon theory with strong corporate governance in sustainability literature are the less developed and basic concepts present in the lower right corner named basic/transversal theme. These concepts in the specific setting identified by the basic theme need further research for value addition on this topic.

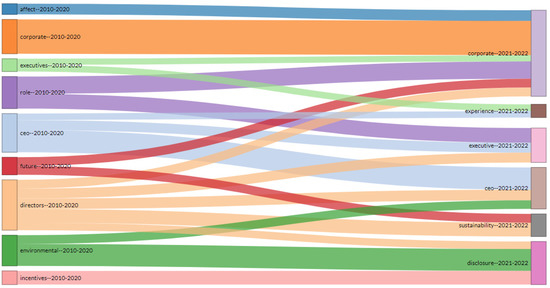

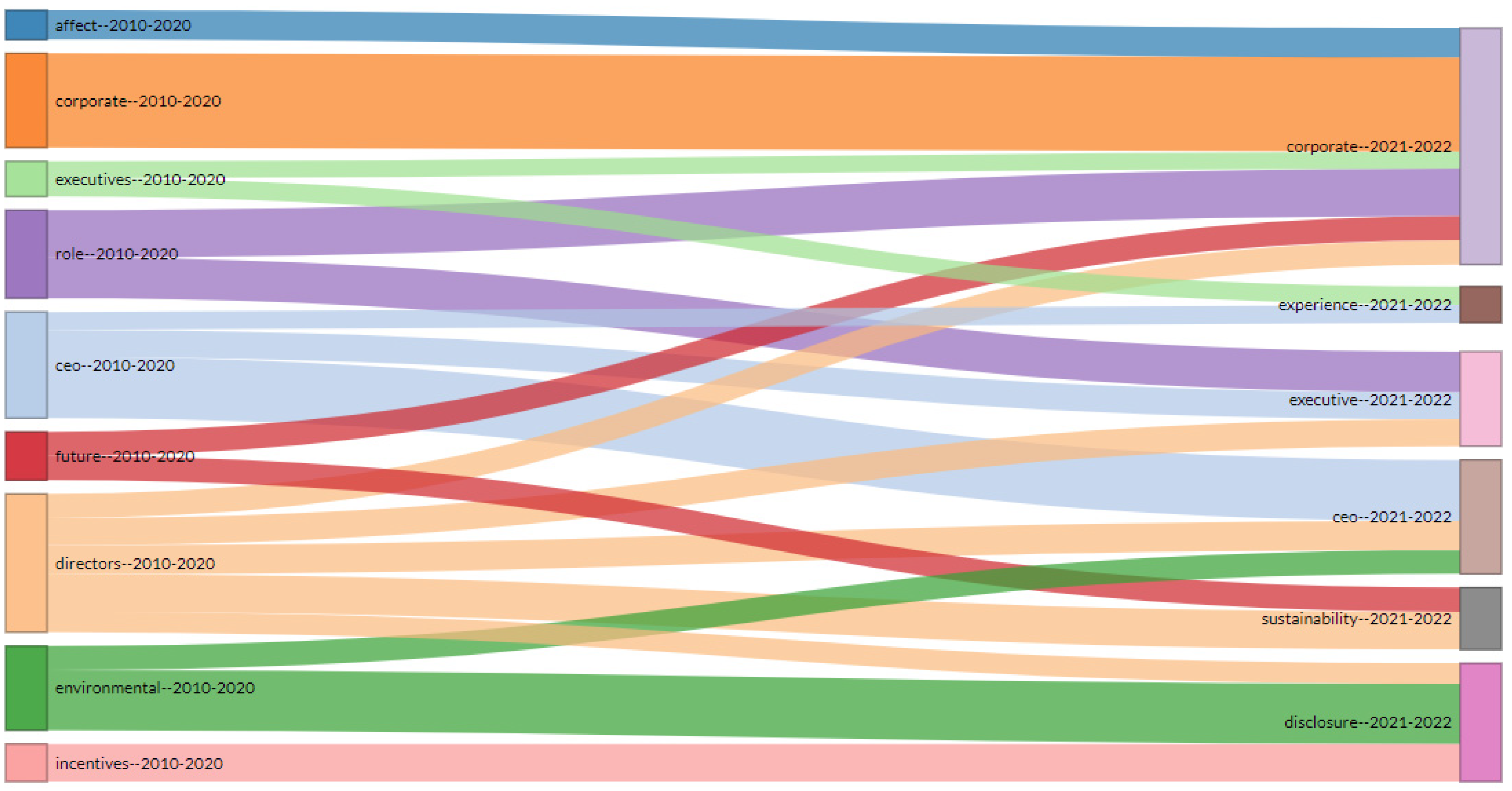

4.3. Thematic Evaluation

In addition to the thematic diagram, there is also thematic evolution (Figure 9), which depicts the evolution of literature over time. The history of themes and their evolution is depicted using keywords and thematic evolution. Thematic progression is achieved by the use of ‘biblioshiny’ and dividing thematic evolution into two segments. The first section covers the years 2010 to 2020. In the first phase, the selected studies have discussed the role of incentives for top executives, CEO, and directors in determining environmental performance in the corporate sector. In the last time segment spanning 2021 to 2022, the experience of executives and CEOs has given immense weightage in sustainability disclosure literature.

Figure 9.

Thematic Evolution.

5. Discussion and Future Research Directions

Our study provides several insights on TMT characteristics and environment disclosures literature. First, regarding the first research question, we have identified the following influential aspects:

- (1)

- The recent year 2021–2022 have the highest number of publications. This finding indicates that TMT characteristics and environmental disclosures literature is still a potential issue for researchers in sustainable finance for more research contributions.

- (2)

- The top avenues for publishing more research on this topic are Sustainability (Switzerland), Corporate Social Responsibility and Environmental Management, and ‘Business Strategy and the Environment.

- (3)

- Prado-Lorenzo and Garcia-Sanchez (2010) work were identified as the most influential article in this field. The recent citations of this study might assist the researchers to contributes more advanced research on this topic.

- (4)

- China is the most contributing country in this research field. We encourage the upcoming studies to focus on more cross-country research using a panel of companies from high and low carbon-emitting countries.

Second, our findings from the second research question regarding the most common trends in this domain open avenues for the upcoming research. The first trend in our sample focused on political connections of TMT and good governance in environmental disclosures literature. The second trend is about the role of TMT characteristics in improving environmental performance. The third trend focused on institutional investors’ role in TMT characteristics and environmental disclosures. However, these prior studies are limited to the specific context: for example, in the USA (Jeong et al. 2021), in China (Zhang 2017; Zong et al. 2020), and in Vietnam (Tran and Pham 2020). Therefore, we urge the upcoming studies to extend this research in cross-country settings with different cultural backgrounds (Jeong et al. 2021), institutional barriers (Chen et al. 2016), and environmental mitigation strategies (Laposa and Villupuram 2010).

Third, our findings highlight that emerging themes are environmental disclosure, managerial ownership, and CEO tenure. The upcoming studies contribute to these emerging cross-country themes and innovative research design. The detailed discussion of these themes as follows. First element of emerging themes, environmental disclosures by firms is an emerging theme identified by thematic map, mainly influenced by institutional pressure (George et al. 2006). As the top management teams have to make firms strategic decisions that is why their values and specifically CEOs cognitive style matter a lot in this matter (George et al. 2006; Grimm and Smith 1991; Hambrick and Mason 1984; Keeney and Keeney 2009; Norburn 1989; Wally and Baum 1994). Environmental disclosures are voluntary in most of the which provide discretion to the company’s managers in reporting (Clarkson et al. 2008). Prior research indicates that environmental disclosures provide numerous benefits to companies such as improved reputation (Aerts and Cormier 2009), better financial performance (Cho et al. 2019; Fauzi and Idris 2009), new corporate client attachment (Dewi 2013; Wang 2014), and strong voice in the public policy process (Cho and Patten 2007). In contrast, some issues may arise such as litigation risk (Boyer and Kordonsky 2020; Choi and Jung 2021), future regulatory constraints (Delbard 2008; Krichewsky 2017), and firms can be labelled as greenwashers (Lyon and Maxwell 2011). The top management has to avoid possible threats by making effective policymaking regarding environmental disclosure and making quality spending in environmental matters. Meanwhile, shareholders expect better environmental performance because this performance positively influences current and prospective investors, customers, regulators and non-governmental organizations (Clarkson et al. 2008). Second element, TMTs having equity stakes in a firm create an interesting situation for sustainability disclosure as it shifts the mindset of managers towards sustainability spending and disclosure with profit maximization ideology (Godos-Díez et al. 2011; Lyu et al. 2022). Sustainability disclosures support the long-term perspective of a firm intending to enhance the firm reputation (Block and Wagner 2014; Foss and Klein 2018; Landry et al. 2013). Thus, managerial ownership can be an indicator for improving sustainability spending and disclosure.

Third emerging sub-theme, CEO tenure has strategic importance concerning sustainability spending and disclosures in two perspectives. The first one is related to carrier concern and the second one is related to horizon concern. Early tenured CEOs have to establish their ability in front of internal and external stakeholders via some financial and non-financial performance indicators. CEOs signal their ability to external stakeholders via sustainability performance (Gibbons and Murphy 1992; Holmstrom 1982; Shih-Chi and Sharfman 2018). Meanwhile, CEOs have this incentive to establish high performance at the start of their tenure compared to mid tenure CEOs to build personal and firm reputation via sustainability (Ali and Zhang 2015; Bénabou and Tirole 2010; Borghesi et al. 2014). Most of the literature has discussed the decision of more sustainability spending in the early period of CEOs appointment (Chen and Tsang 2017; Chen et al. 2019; Hillman et al. 2000; Huang 2013; Oh et al. 2018; Thomas and Simerly 1994). Early tenured CEOs have a longer time horizon as compared to the mid-tenured CEOs that is why they have more incentive to invest firm’s resources in sustainable business operations because sustainability investment reaps fruit in the form of improved personal and firm reputation in long-run (Lys et al. 2015; Stiglitz 2000).

Fourth, the upcoming studies contribute to the environmental disclosure and TMT characteristics by considering the role of sustainability assurance following the recent studies in this area (Al-Shaer and Zaman 2019; Hoang and Trotman 2021; Román et al. 2021). Finally, most of the studies on TMT characteristics and environmental disclosures are archival using secondary data. Fifth, we urge the researchers to move forward with this contemporary literature using qualitative research designs such as interviews of the chief sustainability officers about the TMT role in environmental disclosures and challenges faced in preparing CSR reports. Finally, the selected studies in our study are not enough on the relationship of TMT characteristics and environmental disclosure for more advanced bibliometric analysis. Hence, the upcoming studies might extend our work on the nexus between environmental disclosure and TMT characteristics with a larger sample in future.

6. Conclusions

Our study’s main objective is to highlight the contributions of academicians on the role of TMT characteristics regarding corporate environmental disclosures. Specifically, using bibliometric analysis of 88 studies from 2010 to 2021, our study has identified the influential aspects, recent trends, and key themes. Among the influential aspects, our study identified the top journals, authors, countries, keywords, and most important studies in this field. Our study has identified three influential streams: role of Politically connections of TMT, good governance in environmental disclosures; the significance of environmental disclosures and performance; and institutional investors and environmental disclosures. Thematic map classifies the TMT characteristics and environmental disclosures relationship themes into four categories: Niche theme (e.g., financial expertise, CFO characteristics, CEO tenure, and board backgrounds); motor themes (e.g., environmental sustainability and climate change); emerging/declining themes (e.g., Environmental disclosure, managerial ownership, and CEO tenure); and basic/transversal themes (e.g., CEO characteristics, upper echelon theory, corporate governance). Our study has provided implications and future research directions based on our research findings. Our systematic and bibliometric review presents the topic trends in the relationship between TMT characteristics and environmental disclosures. However, our study has highlighted some contractionary findings in the selected studies that might be addressed effectively via meta-analysis in this field.

Author Contributions

Conceptualization, H.M.A., B. and Y.Y.; methodology, H.M.A., B.; software, H.M.A., M.S.; validation H.M.A. and B.; formal analysis, H.M.A. and M.S.; investigation, Y.C.; resources, Y.C.; data curation, H.M.A., B. and Y.C.; writing—original draft preparation, H.M.A., B.; writing—review and editing, Y.C., B., M.S. and Y.Y. All authors have read and agreed to the published version of the manuscript.

Funding

We acknowledge the financial support of Hubei University of Economics to support the open access of this article through its excellent Ph.D. program-wide grant number XJ18BS06.

Data Availability Statement

Our study employed the published studies’ publicly available meta-data.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Descriptive characteristics of TMT characteristics and environmental disclosure.

Table A1.

Descriptive characteristics of TMT characteristics and environmental disclosure.

| Description | Results |

|---|---|

| MAIN INFORMATION ABOUT DATA | |

| Timespan | 2010:2022 |

| Sources (Journals, Books, etc.) | 54 |

| Documents | 88 |

| Average years from publication | 2.73 |

| Average citations per documents | 17.51 |

| Average citations per year per doc | 3.178 |

| References | 6447 |

| DOCUMENT TYPES | |

| article | 82 |

| conference paper | 5 |

| review | 1 |

| DOCUMENT CONTENTS | |

| Keywords Plus (ID) | 214 |

| Author’s Keywords (DE) | 277 |

| AUTHORS | |

| Authors | 236 |

| Author Appearances | 271 |

| Authors of single-authored documents | 8 |

| Authors of multi-authored documents | 228 |

| AUTHORS COLLABORATION | |

| Single-authored documents | 8 |

| Documents per Author | 0.373 |

| Authors per Document | 2.68 |

| Co-Authors per Documents | 3.08 |

| Collaboration Index | 2.85 |

Source: Own elaboration.

Table A2.

Top journals according to source impact.

Table A2.

Top journals according to source impact.

| Source | h-index | g_index | m_index | TC | NP | PY_start |

|---|---|---|---|---|---|---|

| Corporate Social Responsibility And Environmental Management | 6 | 7 | 1.5 | 173 | 7 | 2018 |

| Business Strategy And The Environment | 1 | 2 | 0.333333333 | 68 | 2 | 2019 |

| British Accounting Review | 1 | 1 | 0.25 | 82 | 1 | 2018 |

| Corporate Governance: An International Review | 1 | 1 | 0.0625 | 20 | 1 | 2006 |

| Information And Management | 1 | 1 | 0.090909091 | 9 | 1 | 2011 |

| International Journal Of Environmental Research And Public Health | 1 | 1 | 0.333333333 | 10 | 1 | 2019 |

| Journal Of Business Ethics | 1 | 1 | 0.076923077 | 5 | 1 | 2009 |

| Journal Of Cleaner Production | 1 | 1 | 0.111111111 | 8 | 1 | 2013 |

| Management Decision | 1 | 1 | 0.142857143 | 24 | 1 | 2015 |

| Nankai Business Review International | 1 | 1 | 0.090909091 | 10 | 1 | 2011 |

Source: Own elaboration.

Table A3.

Most globally cited article.

Table A3.

Most globally cited article.

| Paper | Total Citation | Total Citations per Year |

|---|---|---|

| The role of the board of directors in disseminating relevant information on greenhouse gases | 283 | 21.769 |

| Difference in degrees: ceo characteristics and firm environmental disclosure | 200 | 22.222 |

| Diversity of board of directors and environmental social governance: evidence from italian listed companies | 126 | 25.2 |

| The impact of environmental, social, and governance disclosure on firm value: the role of ceo power | 125 | 25 |

| A study of environmental policies and regulations, governance structures, and environmental performance: the role of female directors | 111 | 27.75 |

| The future of the planet in the hands of mbas: an examination of ceomba education and corporate environmental performance | 66 | 5.077 |

| Big egos can be green: a study of ceo hubris and environmental innovation | 61 | 12.2 |

| Whether top executives’ turnover influences environmental responsibility: from the perspective of environmental information disclosure | 55 | 5.5 |

| Political connections and corporate environmental responsibility: adopting or escaping? | 52 | 8.667 |

| Investigating the relationship between director’s profile, board interlocks and corporate social responsibility | 32 | 4 |

Source: Own elaboration.

References

- Adebayo, Tomiwa Sunday, Hauwah K. K. AbdulKareem, Bilal, Dervis Kirikkaleli, Muhammad Ibrahim Shah, and Shujaat Abbas. 2022. CO2 behavior amidst the COVID-19 pandemic in the United Kingdom: The role of renewable and non-renewable energy development. Renewable Energy. [Google Scholar] [CrossRef]

- Aerts, Walter, and Denis Cormier. 2009. Media legitimacy and corporate environmental communication. Accounting, Organizations and Society 34: 1–27. [Google Scholar] [CrossRef]

- Al-Shaer, Habiba, and Mahbub Zaman. 2019. CEO compensation and sustainability reporting assurance: Evidence from the UK. Journal of Business Ethics 158: 233–52. [Google Scholar] [CrossRef] [Green Version]

- Ali, Ashiq, and Weining Zhang. 2015. CEO tenure and earnings management. Journal of Accounting and Economics 59: 60–79. [Google Scholar] [CrossRef]

- Arslan, Hafiz, Bilal, and Muhammad Bashir. 2021. Contemporary research on spillover effects of COVID-19 in stock markets. A systematic and bibliometric review. Paper presented at the 3rd International Electronic Conference on Environmental Research and Public Health—Public Health Issues in the Context of the COVID-19 Pandemic, Online, January 11–25. [Google Scholar]

- Bilal, Ali Meftah Gerged, Hafiz Muhammad Arslan, Ali Abbas, Songsheng Chen, and Shahid Manzoor. 2021. Review of Corporate Environmental Disclosure Research: A Bibliometric Approach. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3982298 (accessed on 13 February 2022).

- Bilal, Irfan Khan, Duojiao Tan, Waseem Azam, and Syed Tauseef Hassan. 2022. Alternate energy sources and environmental quality: The impact of inflation dynamics. Gondwana Research 106: 51–63. [Google Scholar] [CrossRef]

- Bénabou, Roland, and Jean Tirole. 2010. Individual and corporate social responsibility. Economica 77: 1–19. [Google Scholar] [CrossRef] [Green Version]

- Block, Joern, and Marcus Wagner. 2014. Ownership versus management effects on corporate social responsibility concerns in large family and founder firms. Journal of Family Business Strategy 5: 339–46. [Google Scholar] [CrossRef]

- Borghei, Zahra. 2021. Carbon disclosure: A systematic literature review. Accounting & Finance 61: 5255–80. [Google Scholar] [CrossRef]

- Borghesi, Richard, Joel F. Houston, and Andy Naranjo. 2014. Corporate socially responsible investments: CEO altruism, reputation, and shareholder interests. Journal of Corporate Finance 26: 164–81. [Google Scholar] [CrossRef]

- Boyer, M Martin, and Ksenia Kordonsky. 2020. Corporate Social Responsibility and Litigation Risk. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3704572 (accessed on 13 February 2022).

- Chaudhuri, Ranjan, Demetris Vrontis, Gitesh Chavan, and S. M. Riad Shams. 2020. Social business enterprises as a research domain: A bibliometric analysis and research direction. Journal of Social Entrepreneurship, 1–15. [Google Scholar] [CrossRef]

- Chen, Long, and Albert Tsang. 2017. CEO Tenure and Corporate Social Responsibility (CSR) reporting. Fairfax: George Mason Univerisity, pp. 1–51. [Google Scholar]

- Chen, Po-Han, Chuan-Fang Ong, and Shu-Chien Hsu. 2016. Understanding the relationships between environmental management practices and financial performances of multinational construction firms. Journal of Cleaner Production 139: 750–60. [Google Scholar] [CrossRef]

- Chen, Wanyu Tina, Gaoguang Stephen Zhou, and Xindong Kevin Zhu. 2019. CEO tenure and corporate social responsibility performance. Journal of Business Research 95: 292–302. [Google Scholar] [CrossRef]

- Cho, Charles H., and Dennis M. Patten. 2007. The role of environmental disclosures as tools of legitimacy: A research note. Accounting, Organizations and Society 32: 639–47. [Google Scholar] [CrossRef]

- Cho, Sang Jun, Chune Young Chung, and Jason Young. 2019. Study on the Relationship between CSR and Financial Performance. Sustainability 11: 343. [Google Scholar] [CrossRef] [Green Version]

- Choi, Sanghak, and Hail Jung. 2021. Effects of the litigation risk coverage on corporate social responsibility. Applied Economics Letters 28: 1836–41. [Google Scholar] [CrossRef]

- Clarkson, Peter, Ami Lammerts Van Bueren, and Julie Walker. 2006. Chief executive officer remuneration disclosure quality: Corporate responses to an evolving disclosure environment. Accounting and Finance 46: 771–96. [Google Scholar] [CrossRef]

- Clarkson, Peter M., Yue Li, Gordon D. Richardson, and Florin P. Vasvari. 2008. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organizations and Society 33: 303–27. [Google Scholar] [CrossRef]

- Cobo, Manuel J., Antonio Gabriel López-Herrera, Enrique Herrera-Viedma, and Francisco Herrera. 2011. Science mapping software tools: Review, analysis, and cooperative study among tools. Journal of the American Society for Information Science and Technology 62: 1382–402. [Google Scholar] [CrossRef]

- Delbard, Olivier. 2008. CSR legislation in France and the European regulatory paradox: An analysis of EU CSR policy and sustainability reporting practice. Corporate Governance: The International Journal of Business in Society 8: 397–405. [Google Scholar] [CrossRef]

- Dewi, Dian Masita. 2013. CSR effect on market and financial performance. El Dinar 1: 1–19. [Google Scholar] [CrossRef] [Green Version]

- Donaldson, Thomas. 1999. Making stakeholder theory whole. Academy of Management Review 24: 237–41. [Google Scholar] [CrossRef]

- Elmagrhi, Mohamed H., Collins G. Ntim, Ahmed A. Elamer, and Qingjing Zhang. 2019. A study of environmental policies and regulations, governance structures, and environmental performance: The role of female directors. Business Strategy and the Environment 28: 206–20. [Google Scholar] [CrossRef]

- Fareed, Zeeshan, Muhammad Farhan Bashir, Bilal, and Sultan Salem. 2021. Investigating the Co-movement Nexus Between Air Quality, Temperature, and COVID-19 in California: Implications for Public Health. Frontiers in Public Health 9. [Google Scholar] [CrossRef]

- Faruk, Mohammad, Mahfuzur Rahman, and Shahedul Hasan. 2021. How digital marketing evolved over time: A bibliometric analysis on scopus database. Heliyon 7: e08603. [Google Scholar] [CrossRef] [PubMed]

- Fauzi, Hasan, and Kamil Idris. 2009. The relationship of CSR and financial performance: New evidence from Indonesian companies. Issues in Social and Environmental Accounting 3: 45–65. [Google Scholar] [CrossRef]

- Foss, Nicolai J., and Peter G. Klein. 2018. Stakeholders and corporate social responsibility: An ownership perspective. In Sustainability, Stakeholder Governance, and Corporate Social Responsibility. Bentley: Emerald Publishing Limited. [Google Scholar]

- Fromont, Emmanuelle, Thi Le Hoa Vo, and Gulliver Lux. 2022. Impact of GHG Reporting Quality on Investors’ Valuations in a Regulatory Context: The Case of SBF 120 Companies. Accounting Auditing Control 28: 133–60. [Google Scholar]

- George, Elizabeth, Prithviraj Chattopadhyay, Sim B Sitkin, and Jeff Barden. 2006. Cognitive underpinnings of institutional persistence and change: A framing perspective. Academy of Management Review 31: 347–65. [Google Scholar] [CrossRef] [Green Version]

- Gibbons, Robert, and Kevin J. Murphy. 1992. Optimal incentive contracts in the presence of career concerns: Theory and evidence. Journal of Political Economy 100: 468–505. [Google Scholar] [CrossRef] [Green Version]

- Godos-Díez, José-Luis, Roberto Fernández-Gago, and Almudena Martínez-Campillo. 2011. How important are CEOs to CSR practices? An analysis of the mediating effect of the perceived role of ethics and social responsibility. Journal of Business Ethics 98: 531–48. [Google Scholar] [CrossRef]

- Grimm, Curtis M., and Ken G. Smith. 1991. Research notes and communications management and organizational change: A note on the railroad industry. Strategic Management Journal 12: 557–62. [Google Scholar] [CrossRef]

- Hahn, Rüdiger, Daniel Reimsbach, and Frank Schiemann. 2015. Organizations, Climate Change, and Transparency: Reviewing the Literature on Carbon Disclosure. Organization & Environment 28: 80–102. [Google Scholar] [CrossRef]

- Hambrick, Donald C. 2007. Upper Echelons Theory: An Update. Briarcliff Manor: Academy of Management Briarcliff Manor, p. 10510. [Google Scholar]

- Hambrick, Donald C., and Phyllis A. Mason. 1984. Upper echelons: The organization as a reflection of its top managers. Academy of Management Review 9: 193–206. [Google Scholar] [CrossRef]

- He, Rong, Le Luo, Abul Shamsuddin, and Qingliang Tang. 2021. Corporate carbon accounting: A literature review of carbon accounting research from the Kyoto Protocol to the Paris Agreement. Accounting & Finance 62: 261–98. [Google Scholar] [CrossRef]

- Hemingway, Christine A., and Patrick W. Maclagan. 2004. Managers’ personal values as drivers of corporate social responsibility. Journal of Business Ethics 50: 33–44. [Google Scholar] [CrossRef]

- Hillman, Amy J., Albert A. Cannella, and Ramona L. Paetzold. 2000. The resource dependence role of corporate directors: Strategic adaptation of board composition in response to environmental change. Journal of Management Studies 37: 235–56. [Google Scholar] [CrossRef]

- Hoang, Hien, and Ken T. Trotman. 2021. The effect of CSR assurance and explicit assessment on investor valuation judgments. Auditing: A Journal of Practice & Theory 40: 19–33. [Google Scholar]

- Holmstrom, Bengt. 1982. Moral hazard in teams. The Bell Journal of Economics 13: 324–40. [Google Scholar] [CrossRef]

- Huang, Shihping Kevin. 2013. The impact of CEO characteristics on corporate sustainable development. Corporate Social Responsibility and Environmental Management 20: 234–44. [Google Scholar] [CrossRef]

- Jeong, Nara, Nari Kim, and Jonathan D. Arthurs. 2021. The CEO’s tenure life cycle, corporate social responsibility and the moderating role of the CEO’s political orientation. Journal of Business Research 137: 464–74. [Google Scholar] [CrossRef]

- Keeney, Ralph L., and Ralph L. Keeney. 2009. Value-Focused Thinking: A Path to Creative Decisionmaking. Cambridge: Harvard University Press. [Google Scholar]

- Khan, Talat Mehmood, Bai Gang, Zeeshan Fareed, and Anwar Khan. 2021. How does CEO tenure affect corporate social and environmental disclosures in China? Moderating role of information intermediaries and independent board. Environmental Science and Pollution Research 28: 9204–20. [Google Scholar] [CrossRef]

- Khan, Irfan, Duojiao Tan, Syed Tauseef Hassan, and Bilal. 2022. Role of alternative and nuclear energy in stimulating environmental sustainability: Impact of government expenditures. Environmental Science and Pollution Research. [Google Scholar] [CrossRef]

- Khudzari, Jauharah Md, Jiby Kurian, Boris Tartakovsky, and G. S. Vijaya Raghavan. 2018. Bibliometric analysis of global research trends on microbial fuel cells using Scopus database. Biochemical Engineering Journal 136: 51–60. [Google Scholar] [CrossRef]

- Kim, Yeonsoo, and Mary Ann Ferguson. 2019. Are high-fit CSR programs always better? The effects of corporate reputation and CSR fit on stakeholder responses. Corporate Communications: An International Journal 24: 471–98. [Google Scholar] [CrossRef]

- Krichewsky, Damien. 2017. CSR public policies in India’s democracy: Ambiguities in the political regulation of corporate conduct. Business and Politics 19: 510–47. [Google Scholar] [CrossRef]

- Kuo, Lopin, and Vivian Yi-Ju Chen. 2013. Is environmental disclosure an effective strategy on establishment of environmental legitimacy for organization? Management Decision 51: 1462–487. [Google Scholar] [CrossRef]

- Landry, Suzanne, Manon Deslandes, and Anne Fortin. 2013. Tax aggressiveness, corporate social responsibility, and ownership structure. Journal of Accounting, Ethics & Public Policy 14: 611–45. [Google Scholar]

- Laposa, Steven, and Sriram Villupuram. 2010. Corporate real estate and corporate sustainability reporting: An examination and critique of current standards. Journal of Sustainable Real Estate 2: 23–49. [Google Scholar] [CrossRef]

- Lewis, Ben W., Judith L. Walls, and Glen W. S. Dowell. 2014. Difference in degrees: CEO characteristics and firm environmental disclosure. Strategic Management Journal 35: 712–22. [Google Scholar] [CrossRef] [Green Version]

- Li, Yiwei, Mengfeng Gong, Xiuye Zhang, and Lenny Koh. 2018. The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. British Accounting Review 50: 60–75. [Google Scholar] [CrossRef] [Green Version]

- López-Concepción, Arelys, Ana I. Gil-Lacruz, and Isabel Saz-Gil. 2021. Stakeholder engagement, Csr development and Sdgs compliance: A systematic review from 2015 to 2021. Corporate Social Responsibility and Environmental Management 29: 19–31. [Google Scholar] [CrossRef]

- Luo, Xiaowei Rose, Danqing Wang, and Jianjun Zhang. 2017. Whose call to answer: Institutional complexity and firms’ CSR reporting. Academy of Management Journal 60: 321–44. [Google Scholar] [CrossRef] [Green Version]

- Lyon, Thomas P., and John W. Maxwell. 2011. Greenwash: Corporate environmental disclosure under threat of audit. Journal of Economics & Management Strategy 20: 3–41. [Google Scholar]

- Lys, Thomas, James P Naughton, and Clare Wang. 2015. Signaling through corporate accountability reporting. Journal of Accounting and Economics 60: 56–72. [Google Scholar] [CrossRef] [Green Version]

- Lyu, Lu, Irfan Khan, Abdulrasheed Zakari, and Bilal. 2022. A study of energy investment and environmental sustainability nexus in China: A bootstrap replications analysis. Environmental Science and Pollution Research 29: 8464–72. [Google Scholar] [CrossRef] [PubMed]

- Ma, Yuan, Qiang Zhang, Qiyue Yin, and Bingcheng Wang. 2019. The influence of top managers on environmental information disclosure: The moderating effect of company’s environmental performance. International Journal of Environmental Research and Public Health 16: 1167. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Mardini, Ghassan H., and Fathia Elleuch Lahyani. 2021. Impact of foreign directors on carbon emissions performance and disclosure: Empirical evidence from France. Sustainability Accounting, Management and Policy Journal 13: 221–46. [Google Scholar] [CrossRef]

- Marquis, Christopher, and Cuili Qian. 2014. Corporate social responsibility reporting in China: Symbol or substance? Organization Science 25: 127–48. [Google Scholar] [CrossRef] [Green Version]

- Meng, X. H., S. X. Zeng, Arthur W. T. Leung, and C. M. Tam. 2015. Relationship Between Top Executives’ Characteristics and Corporate Environmental Responsibility: Evidence from China. Human and Ecological Risk Assessment 21: 466–91. [Google Scholar] [CrossRef]

- Meng, X. H., S. X. Zeng, C. M. Tam, and X. D. Xu. 2013. Whether Top Executives’ Turnover Influences Environmental Responsibility: From the Perspective of Environmental Information Disclosure. Journal of Business Ethics 114: 341–53. [Google Scholar] [CrossRef]

- Moral-Muñoz, José A., Enrique Herrera-Viedma, Antonio Santisteban-Espejo, and Manuel J. Cobo. 2020. Software tools for conducting bibliometric analysis in science: An up-to-date review. Profesional de la Información 29: 1–20. [Google Scholar] [CrossRef] [Green Version]

- Norburn, David. 1989. The chief executive: A breed apart. Strategic Management Journal 10: 1–15. [Google Scholar] [CrossRef]

- Oh, Won-Yong, Young Kyun Chang, and Rami Jung. 2018. Experience-based human capital or fixed paradigm problem? CEO tenure, contextual influences, and corporate social (ir) responsibility. Journal of Business Research 90: 325–33. [Google Scholar] [CrossRef]

- Prado-Lorenzo, Jose-Manuel, and Isabel-Maria Garcia-Sanchez. 2010. The role of the board of directors in disseminating relevant information on greenhouse gases. Journal of Business Ethics 97: 391–424. [Google Scholar] [CrossRef]

- Pucheta-Martínez, María Consuelo, and Blanca López-Zamora. 2018. Engagement of directors representing institutional investors on environmental disclosure. Corporate Social Responsibility and Environmental Management 25: 1108–20. [Google Scholar] [CrossRef]

- Radhouane, Ikram, Mehdi Nekhili, Haithem Nagati, and Gilles Paché. 2020. Is voluntary external assurance relevant for the valuation of environmental reporting by firms in environmentally sensitive industries? Sustainability Accounting, Management and Policy Journal 11: 65–98. [Google Scholar] [CrossRef]

- Ramos-Meza, Carlos Samuel, Rinat Zhanbayev, Hazrat Bilal, Mubbashra Sultan, Zehra Betül Pekergin, and Hafiz Muhammad Arslan. 2021. Does digitalization matter in green preferences in nexus of output volatility and environmental quality? Environmental Science and Pollution Research 28: 66957–67. [Google Scholar] [CrossRef] [PubMed]

- Rashed, Abdulkarim Hasan, Suad Ahmed Rashdan, and Ahmed Y Ali-Mohamed. 2022. Towards Effective Environmental Sustainability Reporting in the Large Industrial Sector of Bahrain. Sustainability 14: 219. [Google Scholar] [CrossRef]

- Reid, Erin M., and Michael W. Toffel. 2009. Responding to public and private politics: Corporate disclosure of climate change strategies. Strategic Management Journal 30: 1157–78. [Google Scholar] [CrossRef] [Green Version]

- Román, Carmen Córdova, Ana Zorio-Grima, and Paloma Merello. 2021. Economic development and CSR assurance: Important drivers for carbon reporting… yet inefficient drivers for carbon management? Technological Forecasting and Social Change 163: 120424. [Google Scholar] [CrossRef]

- Sarfraz, Muddassar, Bin He, and Syed Ghulam Meran Shah. 2020. Elucidating the effectiveness of cognitive CEO on corporate environmental performance: The mediating role of corporate innovation. Environmental Science and Pollution Research 27: 45938–48. [Google Scholar] [CrossRef]

- Sauerbrei, Willi, Carolina Meier-Hirmer, A. Benner, and Patrick Royston. 2006. Multivariable regression model building by using fractional polynomials: Description of SAS, STATA and R programs. Computational Statistics & Data Analysis 50: 3464–85. [Google Scholar]

- Shah, Syed Ghulam Meran, Muddassar Sarfraz, and Larisa Ivascu. 2021. Assessing the interrelationship corporate environmental responsibility, innovative strategies, cognitive and hierarchical CEO: A stakeholder theory perspective. Corporate Social Responsibility and Environmental Management 28: 457–73. [Google Scholar] [CrossRef]

- Shahab, Yasir, Collins G. Ntim, Ye Chengang, Farid Ullah, and Samuel Fosu. 2018. Environmental policy, environmental performance, and financial distress in China: Do top management team characteristics matter? Business Strategy and the Environment 27: 1635–52. [Google Scholar] [CrossRef]

- Shih-Chi, Chiu, and Mark Sharfman. 2018. Corporate Social Irresponsibility and Executive Succession: An Empirical Examination. Journal of Business Ethics 149: 707–23. [Google Scholar]

- Shuai, Zhai, Najaf Iqbal, Rai Imtiaz Hussain, Farrukh Shahzad, Yong Yan, Zeeshan Fareed, and Bilal. 2021. Climate indicators and COVID-19 recovery: A case of Wuhan during the lockdown. Environment, Development and Sustainability. [Google Scholar] [CrossRef]

- Silvente, Giseli Alves, Clébia Ciupak, and Julio Araujo Carneiro-da-Cunha. 2018. Top management teams: A bibliometric research from 2005 to 2015. International Journal of Management and Decision Making 17: 95–124. [Google Scholar] [CrossRef]

- Stiglitz, Joseph E. 2000. The contributions of the economics of information to twentieth century economics. The Quarterly Journal of Economics 115: 1441–78. [Google Scholar] [CrossRef]

- Sutantoputra, Aries. 2021. Do stakeholders’ demands matter in environmental disclosure practices? Evidence from Australia. Journal of Management and Governance, 1–30. [Google Scholar] [CrossRef]

- Thijssens, Thomas, Laury Bollen, and Harold Hassink. 2015. Secondary stakeholder influence on CSR disclosure: An application of stakeholder salience theory. Journal of Business Ethics 132: 873–91. [Google Scholar] [CrossRef] [Green Version]

- Thomas, Anisya S., and Roy L. Simerly. 1994. The chief executive officer and corporate social performance: An interdisciplinary examination. Journal of Business Ethics 13: 959–68. [Google Scholar] [CrossRef]

- Tran, Nhat Minh, and Bich-Ngoc Thi Pham. 2020. The influence of CEO characteristics on corporate environmental performance of SMEs: Evidence from Vietnamese SMEs. Management Science Letters 10: 1671–82. [Google Scholar] [CrossRef]

- Van Aaken, Dominik, Violetta Splitter, and David Seidl. 2013. Why do corporate actors engage in pro-social behaviour? A Bourdieusian perspective on corporate social responsibility. Organization 20: 349–71. [Google Scholar] [CrossRef] [Green Version]

- Velte, Patrick, Martin Stawinoga, and Rainer Lueg. 2020. Carbon performance and disclosure: A systematic review of governance-related determinants and financial consequences. Journal of Cleaner Production 254: 120063. [Google Scholar] [CrossRef]

- Viju, Vijay Ganesh Wardikar, and Vijay Ganesh. 2013. Application of Bradford’s Law of Scattering to the Literature of Library & Information Science: A Study of Doctoral Theses Citations Submitted to the Universities of Maharashtra, India. In Library Philosophy and Practice. Lincoln: University of Nebraska–Lincoln, pp. 1–45. [Google Scholar]

- Wally, Stefan, and J. Robert Baum. 1994. Personal and structural determinants of the pace of strategic decision making. Academy of Management Journal 37: 932–56. [Google Scholar]

- Wang, Shuqin. 2014. On the Relationship between CSR and Profit. Journal of International Business Ethics 7: 51–57. [Google Scholar]

- Wang, Bo, Zehui Wang, Jun Wen, and Xiaotian Tina Zhang. 2021. Executive Gender and Firm Environmental Management: Evidence from CFO Transitions. Sustainability 13: 3653. [Google Scholar] [CrossRef]

- Xu, Jing, and Liming Zhang. 2017. Institutional Investors, Managers’ Power and Environmental Performance Information Disclosure: Evidence from Listed Firms of Heavy Polluting Industries in Shanghai Stock Exchange of China. In Paper Presented at the Proceedings of the Tenth International Conference on Management Science and Engineering Management. Singapore: Springer. [Google Scholar]

- Yas, Harith, Ahmad Jusoh, Alhamzah F. Abbas, Abbas Mardani, and Khalil Md Nor. 2020. A review and bibliometric analysis of service quality and customer satisfaction by using Scopus database. International Journal of Management (IJM) 11: 459–70. [Google Scholar]

- Zhang, Cui. 2017. Political connections and corporate environmental responsibility: Adopting or escaping? Energy Economics 68: 539–47. [Google Scholar] [CrossRef]

- Zhang, Yue-Jun, and Jing-Yue Liu. 2020. Overview of research on carbon information disclosure. Frontiers of Engineering Management 7: 47–62. [Google Scholar] [CrossRef]

- Zhou, Mengling, Fanglin Chen, and Zhongfei Chen. 2021. Can CEO education promote environmental innovation: Evidence from Chinese enterprises. Journal of Cleaner Production 297: 126725. [Google Scholar] [CrossRef]

- Zong, Jiafeng, Man Guo, Zongjian Lin, and Qi Yang. 2020. Senior Executives’ Political Connections and Corporate Environmental Behavior—Empirical Research From the Chinese A-Share Market. Review of Policy Research 37: 556–71. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).