Saddlepoint Method for Pricing European Options under Markov-Switching Heston’s Stochastic Volatility Model

Abstract

:1. Introduction

2. Markov-Switching Heston’s Stochastic Volatility Model

3. Saddlepoint Methods

4. Pricing European Options in Markov-Switching Heston’s Model

5. Numerical Examples

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Bollen, Nicolas P.B. 1998. Valuing options in regime-switching models. Journal of Derivatives 6: 38–49. [Google Scholar] [CrossRef]

- Boyle, Phelim, and Thangaraj Draviam. 2007. Pricing exotic options under regime switching. Insurance: Mathematics and Economics 40: 267–82. [Google Scholar] [CrossRef]

- Buffington, John, and Robert J. Elliott. 2002. American options with regime switching. International Journal of Theoretical and Applied Finance (IJTAF) 5: 497–514. [Google Scholar] [CrossRef]

- Chan, Leunglung, and Song-Ping Zhu. 2015. An explicit analytic formula for pricing barrier options with regime switching. Mathematics and Financial Economics 9: 29–37. [Google Scholar] [CrossRef]

- Chan, Leunglung, and Song-Ping Zhu. 2021a. An Analytic Approach for Pricing American Options with Regime Switching. Journal of Risk and Financial Management 14: 188. [Google Scholar] [CrossRef]

- Chan, Leunglung, and Song-Ping Zhu. 2021b. An Exact and Explicit Formula for Pricing Lookback Options with Regime Switching. Journal of Industrial and Management Optimization. [Google Scholar] [CrossRef]

- Daniels, Henry E. 1954. Saddleppoint Approximations in Statistics. Annals of Mathematical Statistics 25: 1943–78. [Google Scholar] [CrossRef]

- Daniels, Henry. E. 1987. Tail probability approximations. International Statistical Review 55: 37–48. [Google Scholar] [CrossRef]

- Duan, Jin-Chuan, Peter Ritchken, and Ivilina Popova. 2002. Option pricing under regime switching. Quantitative Finance 2: 116–32. [Google Scholar] [CrossRef]

- Elliott, Robert J., and Guang-Hua Lian. 2013. Pricing variance and volatility swaps in a stochastic volatility model with regime switching: Discrete observations case. Quantitative Finance 13: 687–98. [Google Scholar] [CrossRef]

- Elliott, Robert J., Lakhdar Aggoun, and John B. Moore. 1994. Hidden Markov Models: Estimation and Control. Berlin, Heidelberg and New York: Springer. [Google Scholar]

- Elliott, Robert J., Leunglung Chan, and Tak K. Siu. 2005. Option pricing and Esscher transform under regime switching. Annals of Finance 1: 423–32. [Google Scholar] [CrossRef]

- Elliott, Robert J., Leunglung Chan, and Tak K. Siu. 2013. Option valuation under a regime-switching constant elasticity of variance process. Applied Mathematics and Computation 219: 4434–43. [Google Scholar] [CrossRef]

- Elliott, Robert J., Tak K. Siu, and Leunglung Chan. 2014. On pricing barrier options with regime switching. Journal of Computational and Applied Mathematics 9: 196–210. [Google Scholar] [CrossRef]

- Egami, Masahiko, and Rusudan Kevkhishvili. 2020. A direct solution method for pricing options in regime-switching models. Mathematical Finance 30: 547–76. [Google Scholar] [CrossRef]

- Glasserman, Paul, and Kyoung-Kuk Kim. 2009. Saddlepoint Approximations for Affine Jump-Diffusion Models. Journal of Economic Dynamics and Control 33: 15–36. [Google Scholar] [CrossRef]

- Guo, Xin. 2001. Information and option pricings. Quantitative Finance 1: 38–44. [Google Scholar] [CrossRef]

- Hardy, Mary. 2001. A regime switching model of long-term stock returns. North American Actuarial Journal 5: 41–53. [Google Scholar] [CrossRef]

- Heston, Steven L. 1993. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies 6: 327–43. [Google Scholar] [CrossRef]

- Li, Jonathan Y., Michael J. Kim, and Roy H. Kwon. 2012. A moment approach to bounding exotic options under regime switching. Optimization 61: 1253–69. [Google Scholar] [CrossRef]

- Lu, Xiaoping, and Endah R. M. Putri. 2020. A semi-analytical valuation of American options under a two-state regime-switching economy. Physica A 538: 122968. [Google Scholar] [CrossRef]

- Vo, Minh T. 2009. Regime-switching stochastic volatility: Evidence from the crude oil market. Energy Economics 31: 779–88. [Google Scholar] [CrossRef]

- Zhang, Mengzhe, and Leunglung Chan. 2016. Saddlepoint Approximations to Option Price in a Regime-Switching Model. Annals of Finance 12: 55–69. [Google Scholar] [CrossRef]

- Zhu, Song-Ping, Alexander Badran, and Xiaoping Lu. 2012. A new exact solution for pricing European options in a two-state regime-switching economy. Computers and Mathematics with Applications 64: 2744–55. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| First | Order | Sec | Order | |||

|---|---|---|---|---|---|---|

| (year) | ||||||

| 0.1 | 8.5315 | 8.2114 | 8.4556 | 8.0806 | 8.5043 | 8.1738 |

| 0.2 | 8.4257 | 7.8141 | 8.0043 | 7.3541 | 8.3253 | 7.7503 |

| 0.5 | 8.0846 | 7.1332 | 7.2920 | 6.2731 | 7.9300 | 7.0056 |

| 1 | 7.7494 | 6.7888 | 6.8765 | 5.8592 | 7.5898 | 6.6773 |

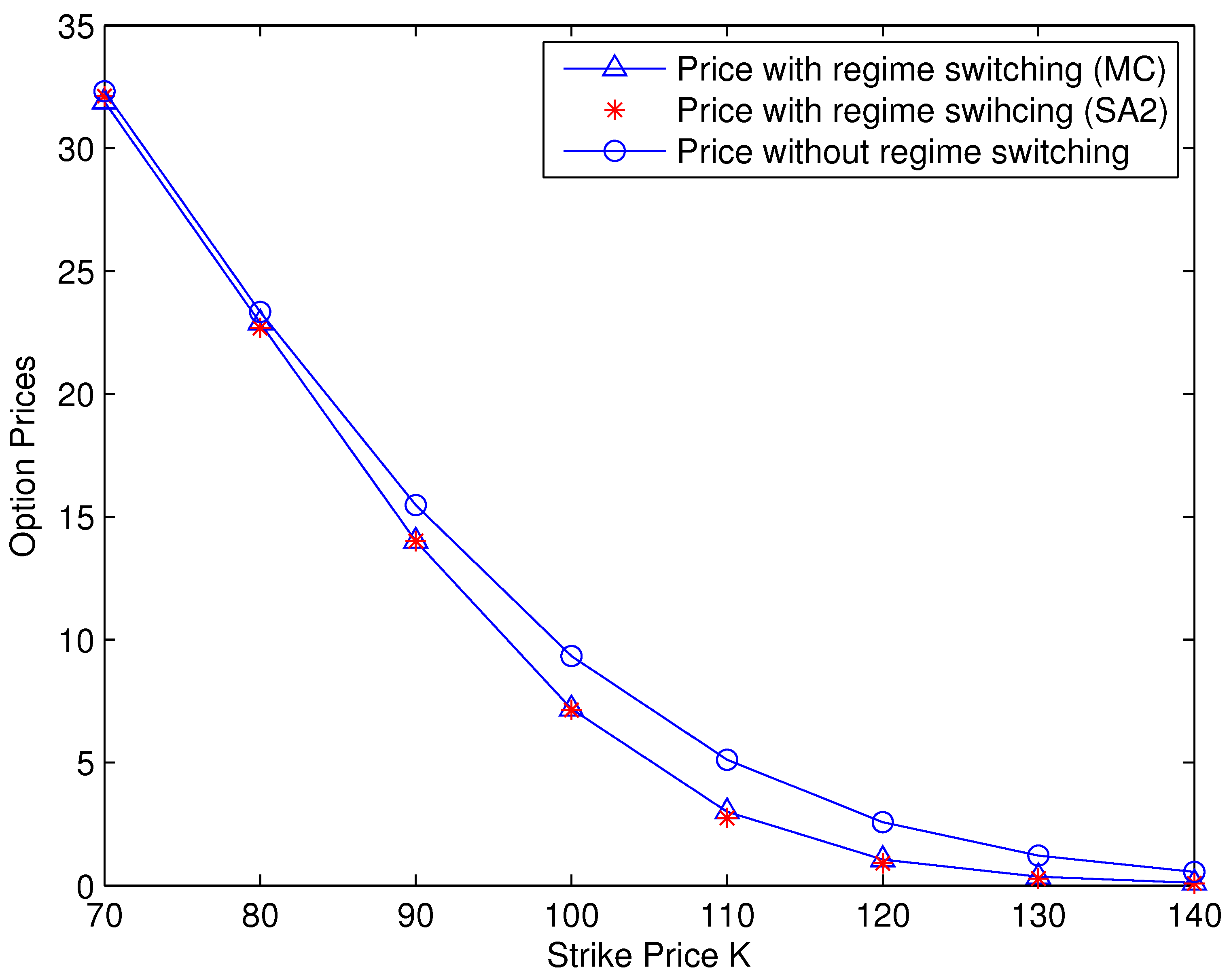

| with Regime-Switching | with Regime-Switching | without Regime-Switching | |

|---|---|---|---|

| K | First State | ||

| 70 | 32.0532 | 32.1250 | 32.3157 |

| 80 | 22.8978 | 22.6910 | 23.3394 |

| 90 | 14.0194 | 14.0200 | 15.4829 |

| 100 | 7.1860 | 7.1398 | 9.3352 |

| 110 | 3.0066 | 2.7466 | 5.1183 |

| 120 | 1.0630 | 0.9057 | 2.5812 |

| 130 | 0.3573 | 0.2758 | 1.2193 |

| 140 | 0.1071 | 0.0829 | 0.1175 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, M.; Chan, L. Saddlepoint Method for Pricing European Options under Markov-Switching Heston’s Stochastic Volatility Model. J. Risk Financial Manag. 2022, 15, 396. https://doi.org/10.3390/jrfm15090396

Zhang M, Chan L. Saddlepoint Method for Pricing European Options under Markov-Switching Heston’s Stochastic Volatility Model. Journal of Risk and Financial Management. 2022; 15(9):396. https://doi.org/10.3390/jrfm15090396

Chicago/Turabian StyleZhang, Mengzhe, and Leunglung Chan. 2022. "Saddlepoint Method for Pricing European Options under Markov-Switching Heston’s Stochastic Volatility Model" Journal of Risk and Financial Management 15, no. 9: 396. https://doi.org/10.3390/jrfm15090396

APA StyleZhang, M., & Chan, L. (2022). Saddlepoint Method for Pricing European Options under Markov-Switching Heston’s Stochastic Volatility Model. Journal of Risk and Financial Management, 15(9), 396. https://doi.org/10.3390/jrfm15090396