1. Introduction

Remittance is the money migrants send to their native origin countries, and it significantly contributes as a developmental component in recipient countries. From only around USD 2 billion in 1970, total international remittances grew to USD 131 billion in 2000 and, despite a drawn-out global financial crisis, USD 430 billion in 2010; remittances were USD 711 billion in 2020. Despite the pandemic, remittance flows increased again to USD 781 billion and are expected to increase in the following financial years. One potential reason is that most recipient countries offer more incentives for remittance inflows.

1 Developing countries have received more than 70% of global remittances in recent years. Despite the effect of the COVID-19 pandemic, low and medium-income countries heavily rely on remittance, which is more than the amount of foreign direct investment (FDI) and foreign development assistance (FDA). In recent years, remittances have become a more stable foreign income than private debt, portfolio equity flows, and international development aid.

An increasing number of studies have examined the effect of remittance on development in recipient countries. For example,

Adams (

2006),

Mora and Taylor (

2005),

Acosta et al. (

2006), and

Anyanwu and Erhijakpor (

2010) examined the effect of remittance on poverty, while

Caceres and Saca (

2006),

Mundaca (

2009),

Giuliano and Ruiz-Arranz (

2009),

Cox-Edwards and Ureta (

2003),

López-Córdova (

2006),

Yang (

2008),

Acosta et al. (

2006),

Calero et al. (

2009),

Adams and Cuecuecha (

2010), and

Amuedo-Dorantes et al. (

2011) examined its effect on economic growth, the exchange rate, and exports.

Bredl (

2011) and

Forhad and Alam (

2021) investigated the impact of remittances on education, while

Kanaiaupuni and Donato (

1999),

Hildebrandt and McKenzie (

2005),

López-Córdova (

2006), and

Amuedo-Dorantes et al. (

2011) examined their effect on health or mortality, and

Antén (

2010),

Massey and Parrado (

1998), and

Woodruff and Zenteno (

2007) investigated their effect on microenterprises. However, very few studies have examined how remittances affect financial development in remittance-recipient countries.

Ramirez and Sharma (

2008) found that financial development and remittances are substitutes for economic growth because an efficient remittance transaction can promote growth through its alleviating effect on the credit constraint.

Aggarwal et al. (

2011),

Bhattacharya et al. (

2018),

Chowdhury (

2011),

Cooray (

2012),

Fromentin (

2018), and

Gupta et al. (

2009) showed that remittance positively impacts the financial development in the recipient country. However, while remittances lead to an expansion in the financial sector, the causation may also go in the opposite direction (

Demirgüç-Kunt et al. 2011). For example, a development in the financial industry might lower the transmission costs, increasing remittance inflows to the recipient countries (

Aggarwal et al. 2011). To address the reverse causality, using the weighted gross national income (GNI) of remittance-sending counties as an instrument of remittance,

Azizi (

2020) found that remittance positively affects financial development. Recently, especially during the COVID-19 pandemic, technological developments and their uses have significantly increased, easing financial transactions and ultimately influencing the inclusion of the financial market. On the other hand,

Masunda and Maharaj (

2023) found that COVID-19 adversely affected remittances and familial relations. Some other studies, such as

Zhang et al. (

2022) and

Chattoraj and Ullah (

2023), argue that the pandemic restricts labor force movement and remittances and affects household consumption behavior and saving tendencies.

In most previous studies, remittances from all sending countries were assumed to be homogeneous, which might not be realized. For example, some migrants from one country could send a larger portion of their foreign income, while other migrants could not. Remittance senders from capital-abundant host countries could also have a different perspective than labor-abundant host countries. Moreover, remittance recipients might respond differently to their financial activities. Therefore, financial development could be affected. Thus, the null hypothesis is whether remittance affects financial development in recipient countries. This study also examines whether such responses to financial-development indicators respond differently based on remittance-sending countries.

Our study is different from the other studies in a number of ways. First, instead of considering remittance as the total amount received from the world, we first consider remittance from low- and high-skilled migrant-abundant source countries. The reason for such a consideration is to examine whether remittance from high-skilled or educated individuals has a different effect than their low-skilled counterparts. As highly educated individuals are usually better informed about the financial system and investment opportunities than their low-educated counterparts, educational levels may lead them to respond differently. For example,

Ghosh (

2006) argued that highly educated and well-paid migrants save more of their income and invest in their host countries, while lower-educated migrants send a larger share of their income to their native countries.

Ghosh (

2006) showed that Indian migrants in North America, on average, earn more money than in Gulf countries but send a relatively low share of their income than their counterparts. In this study, we assume that a higher portion of the remittance from the Gulf Cooperation Council (GCC) countries mainly comes from low-skilled migrants as these countries do not require highly educated or skilled workers. We also assume that the Group of Seven (G7) usually absorbs more educated and skilled migrants, and thereby, remittance coming from these countries is mainly sent by higher-educated migrants. Second, we use an instrumental variable method using weighted average GNI per capita of remittance-sending countries as instruments where weights are extracted from estimated bilateral remittances to address the endogeneity.

The outline of this paper is as follows:

Section 2 reviews the literature related to remittance and financial development.

Section 3 and

Section 4 describe data and methodological issues concerning the specification and estimation, respectively. Our empirical results are reported and discussed in

Section 5, and finally,

Section 6 provides our conclusions.

2. Literature Review

The link between remittance and the financial sector is essential in many ways. For example, a financial institution acts as an intermediary between remittance senders and recipients. A well-functioning financial system would offer a relatively cheap and more accessible approach to remittance transmission. These financial inflows help overcome liquidity constraints and act as an alternative source for investment. Considering 99 developing countries,

Aggarwal et al. (

2011) showed a significant and positive relationship between remittances and bank deposit to GDP ratio and credit to GDP.

Gupta et al. (

2009) also show that remittance inflows significantly facilitate sub-Saharan Africa’s financial sector’s development.

Mundaca (

2009) theoretically showed that remittances affect growth by themselves and with financial intermediaries. Using data for selected Central American countries, Mexico, and the Dominican Republic,

Mundaca (

2005) also empirically demonstrated the effect of financial intermediaries on growth, which is also stimulated when it interacts with remittances.

Similarly, using a System GMM panel data analysis,

Rao and Hassan (

2011) found that remittances indirectly facilitate economic growth by increasing the money supply to GDP ratio. The remittance, as inflows of foreign exchange, can also be used an alternative source of investment. Given the difficulties associated with borrowing and obtaining insurance in developing countries, particularly in rural areas,

Giuliano and Ruiz-Arranz (

2009) indicated that the growth effect of remittances is greater in countries with a relatively weak financial sector. They argued that remittances can compensate for the lack of credit in countries with less developed financial sectors. This compensation helps relax financial constraints and has a dampening effect on credit market development.

On the other hand, an improved financial system enables more remittance inflows, especially for those transacted through informal channels.

Ramirez and Sharma (

2008) also found that financial development and remittances are substitutes, and an efficient remittance transaction system can promote growth by alleviating credit constraints. Therefore, a reverse causality problem may exist while examining the effect of remittance on financial development. In addition, omitted variables in measuring remittance and financial development might lead to a biased result.

To address these concerns,

Aggarwal et al. (

2011) used four instruments: per capita income, unemployment, views on immigration, and policies on immigration in remittance-sending countries. Considering the top five remittance-sending countries, they found a positive and significant link between financial development and remittances.

Freund and Spatafora (

2008) also argued that remittance inflows are highly associated with the transaction cost. A well-developed financial system offers incentives for migrants to send remittances through formal channels. Other studies—

Bhattacharya et al. (

2018),

Chowdhury (

2011),

Cooray (

2012), and

Fromentin (

2018)—found that remittance has a positive impact on financial development in recipient countries. However, the central challenge of examining the effect of remittance on financial development is endogeneity, mainly raised from the measurement error (

Aggarwal et al. 2011).

Most studies use remittance from the official records; they might ignore money sent through non-bank institutions and informal channels.

Freund and Spatafora (

2008) argued that estimates of unrecorded remittances range from 50 to 250 percent of official statistics on remittances. Therefore, choosing valid and strong instruments to address the endogeneity of remittances has remained one of the biggest challenges. Research studies have used lagged values of remittances as instruments. Although using lagged values as an instrument is convenient, they would still have endogeneity because of the measurement error. For example,

Aggarwal et al. (

2011) argued that the lagged values of the remittances are likely to suffer from measurement error. To address the issue, using a panel cointegration method,

Basnet et al. (

2020) found a positive and significant impact of remittances on financial development in selected South Asian countries.

Although studies show a sincere effort to mitigate the endogeneity problem by choosing a set of conditioning variables or choosing the appropriate estimation technique, the primary approach is to use instrumental variables. To address the endogeneity of remittances,

Azizi (

2020) uses an instrumental variable (IV) approach by incorporating per capita gross national income (GNI) of the remittance-sending countries as an instrument. As countries receive remittance from many source countries, recipient countries are relevant to sending countries. On the other hand, remittance-recipient countries do not directly affect the GNI of the remittance-sending countries, indicating that the exclusion restriction is satisfied. Considering remittance altogether from sending countries,

Azizi (

2020) found that remittances positively and significantly impact financial development in recipient countries. In recent years, particularly during the COVID-19 pandemic, technical advancements and applications have expanded dramatically, facilitating financial transactions and increasing financial market participation. Some studies, such as

Zhang et al. (

2022) and

Chattoraj and Ullah (

2023), found that the pandemic deters labor force migration and remittances, and impacts household spending behavior and, hence, saving tendencies. According to

Masunda and Maharaj (

2023), COVID-19 has had a negative impact on remittances and familial relationships.

Shastri (

2022) also argued that the pandemic has reduced remittance flows in recipient countries despite altruism being a relatively dominant factor.

Most research assumed that remittances from all sending nations were homogeneous, which may not be the case. Some migrants from one country, for example, might send a larger share of their foreign income, while others could not. Remittance senders from capital-rich host nations may have a different perspective than those from labor-rich host countries. Moreover, remittance receivers may respond differently to their financial activity. As a result, financial development may differ between these two category recipients. This study also investigates whether such reactions to financial-development indices alter depending on remittance-sending countries.

3. Data

We mainly consider selected Asian countries as remittance-recipient countries since these countries send migrants to both low- and high-skilled labor-intensive destination countries. For example, Bangladesh and India have a significant share of the total migrants in both Saudi Arabia and the United States. While a relatively high percentage of migrants in Saudi Arabia is low or semi-skilled, the United States has a somewhat higher rate of skilled migrants from these two countries. This statistic implies that remittance inflows in these countries are dependent on both types of skilled and unskilled migrant-abundant source countries. On the other hand, Mexico, one of the top remittance-receiving countries, highly depends on the United States, regardless of its migrants’ skill status. We use macro-level data on some selected countries to examine whether the remittance from low-skilled migrants has different impacts on the financial development in their recipient countries. As there is a larger heterogeneity in remittance-recipient countries worldwide, we focus on some selected countries: Afghanistan, Bangladesh, China, India, Indonesia, Pakistan, Philippines, Sri Lanka, Thailand, and Vietnam.

According to the Global Knowledge Partnership on Migration and Development (KNOMAD), countries with a higher proportion of unskilled emigrants usually have a larger ratio of unskilled or low-educated labor. For example, Middle Eastern countries mostly absorb inexperienced and low-educated labor force and are also the top remittance-sending countries.

Ghosh (

2006) found that Indian migrants in North America, on average, earn more money than in the Gulf but send a lower share of their income than their counterparts.

Faini (

2005) also argued that remittances decrease with an increase in the migrant share with tertiary education. Using a survey on Latino households in the United States,

DeSipio (

2002) showed that each additional year of education of a migrant reduces the likelihood of remitting funds home by 7%.

In this study, we assume that a larger portion of the remittance from the Gulf Cooperation Council (GCC) countries comes from low-skilled migrants as these countries do not require highly educated or skilled workers. The selected countries are Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates. Similarly, the Group of Seven (G7) countries—Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States—are the source of high-skilled or highly educated remittance-sending countries.

Following

Aggarwal et al. (

2011),

Basnet et al. (

2020),

Beck et al. (

2000),

Gupta et al. (

2009), and

King and Levine (

1993), we mainly use the ratio between domestic private credit and GDP, liquid liabilities and GDP, and stock market capitalization and GDP to measure the financial development. Domestic credit to the private sector refers to financial resources provided to the private sector by financial corporations, such as loans, purchases of nonequity securities, trade credits, and other accounts receivable that establish a claim for repayment. Liquid liabilities refer to broad money or M3.

Fromentin (

2018) and

Donou-Adonsou and Sylwester (

2017) argued that the depth of the financial system of a country depends on its domestic private credit to GDP and liquidities to GDP ratios, while the market capitalization indicates the relative size of the stock market. We also use depositors per 1000 adults with bank accounts as another measure of financial development. As the selected countries are mainly developing, this indicator examines how remittances affect financial inclusion through the banking channels. We also consider the gross savings to GDP ratio and gross domestic savings to GDP ratio as other measures of financial development. Gross savings are defined as gross national income less total consumption and net transfers, while gross domestic savings is GDP less final consumption expenditure (total consumption).

We collected annual data from World Development Indicators (WDI) of the World Bank for the period 1990–2015. As we considered ten remittance recipient countries for 26 years, the total number of observations is 260. Linear interpolation was used to replace the missing values. Data on remittances were also collected from the World Bank, where remittances are defined as the sum of two components: personal transfers (workers’ remittances) and employee compensation. We also used other variables, namely, income per capita GDP, trade openness, and inflation rate. Trade openness is the ratio of exports plus imports to GDP, while the inflation rate is the annual percentage change in the Consumer Prices Index (CPI). The stock market capitalization is the percentage ratio between the total values of listed domestic companies and GDP. The credit to GDP ratio represents the percentage ratio between the total amount of credits to the private sector and GDP. The domestic savings to GDP ratio represents the percentage ratio between total amount of deposits and GDP. The per capita income is used in the logarithmic form, while all other variables are measured in percentage. These selected control variables are consistent with the literature on the relationship between remittances and financial development.

Table A1 provides a summary description of the variables used in the study.

Table 1 shows the descriptive statistics of the variables. The average ratio of domestic credit to GDP is 37.64%, with a standard deviation of 31.82, and the average ratio of gross savings to GDP is 23.65, with a standard deviation of 17.06, indicating significant heterogeneity across countries. The average percentage of stock market capitalization to GDP is 24.60. On average, 481 individuals per 1000 have an account in the commercial bank. On average, 12.94% of the total remittance was received from the GCC countries and 40.15% was received from the G7 countries. A higher standard deviation in both cases indicates that recipient countries are heterogeneous. Similarly, the average weighted remittance for G7 countries is higher. The standard deviation for G7 countries is also higher than for GCC countries.

4. Empirical Model

To examine the effect of remittance on financial development, we employ the following empirical model:

2

where

is the financial development indicator for country

i at time

t;

is the remittance inflow of country i in period

;

is a vector of other variables that might affect financial development indicators;

is the time-fixed effect;

is the country-specific fixed effect. Following the standard literature, we consider savings, depositors or bank account holders, liquid liability, credits, and stock market capitalization as proxy representations for financial development. Countries could have different country-specific policies or effects that could affect financial development indicators in their homeland. To capture this country-specific effect, we control for it. The coefficient of interest is

which is expected to be positive and statistically significant. This implies that remittance inflows positively affect financial development in recipient countries.

We first estimate Equation (1) using the pooled ordinary least squares (POLS) model. However, the main challenge is endogeneity, resulting from reverse causality between remittances and financial development in its recipient countries. For example, sending remittances requires transfer fees that might discourage individuals from sending through financial channels. Second, migrants might use informal channels. For example, migrants from developing countries are more likely to remit through informal channels, such as family and friends. Therefore, the official measure of remittance might have a measurement error, causing an endogeneity problem. There might also have been omitted variable bias. Thus, estimates from the OLS model may lead to a biased result.

To address the issue, the conventional approach is to use the instrument variable (IV) for remittance. For example, some studies suggest using variables related to remittance-receiving countries. However, these IVs can easily be correlated with the financial development of the same country. Others suggest using an instrument that is directly related to the cost of remittance. However, the main problem is that remittance-sending cost-related data are unavailable for most recipient countries. Other studies suggest using an IV related to remittance-sending countries. As these variables are not directly related to remittance-receiving countries, they are more likely to be valid. For example,

Aggarwal et al. (

2011) argued that remittance-source countries’ economic conditions likely affect migrant outflows from the remittance-recipient countries. Following

Azizi (

2018), we consider an instrument variable related to remittance inflows and uncorrelated dependent variables in the recipient countries. As remittance is the total amount of money sent by the migrants from their host countries to their native countries, it might be related to remittance-sending and -receiving countries. As this study focuses on the financial development in remittance recipient countries, remittance inflows might be correlated with sending countries’ economic conditions but uncorrelated with other factors in recipient countries that might affect the financial development. Moreover, the percentage share of the total remittances from each source country would differently impact the recipient countries. Therefore, we use a weighted average for the GCC and G7 countries as an instrument of the remittances. In such a case, the weight of remittance-receiving country i in year t for each remittance-sending country j is as follows:

If the weight of country

i with country

j is 0.07 in 2010, it indicates that country i received 7% of its total remittances in 2010 from country

j. We then calculate the weighted average of per capita GNI (

) using the following formula:

where

is the per capita GNI of remittance-sending country

j in year

t. Instead of considering a variable in the recipient countries, we consider the weighted average of the per capita GNI of remittance-sending countries as an instrumental variable for remittance inflows to the recipient countries. We assume that the per capita GNI of remittance-sending countries does not directly impact capital ratio, lending ratio, and other financial development indicators in recipient countries. This instrument has relevance to the remittance, but it also satisfies exclusion conditions for other explanatory variables. The question is whether the instrument variable is strong. To investigate the strength of the instruments, we report the estimated effects from first-stage regressions in

Table 2. Column 1 shows the estimated result for remittance-sending GCC countries, while Column 2 shows the same for G7 countries. In each case, F-test statistics are greater than 10, indicating that the instruments for remittance are not weak.

5. Analysis of Results

Table 3 shows the effect of remittance on the gross saving to GDP ratio. Using a simple OLS model, in Column 1, the estimated impact for GCC remittance-sending countries is 0.1907, which is statistically significant. Similarly, Columns 2 and 3 show the estimated effects using fixed effects and instrumental variable models, respectively. The season of using fixed effects models is that remittance-recipient countries could have their domestic policies. These policies could be different in other countries. Therefore, country-fixed effects could capture these country-specific impacts. One could also argue that this analysis could have some other random effects. Using the chi-square value from the Hausman test, we found that the panel dataset is more appropriate for fixed effects estimation. In

Table 3, the estimated effect is positive and statistically significant in each case. For example, the estimated impact from the instrument variable is 0.1511. This estimate implies that a 10% increase in remittance from the GCC countries increases deposits by 15.11%.

On the other hand, it is 19.05% for the G7 remittance-sending countries. Comparing GCC remittance-sending countries, it is reported that remittance from G7 countries has a larger effect on savings in recipient countries. The effects of the inflation rate on the saving ratio are statistically significant for the instrument variable model in both cases. The results of the per capita income of recipient countries and trade openness also positively impact financial development.

Table 4 shows the estimated effect of remittance on the credit ratio in the selected recipient countries. The estimated coefficient of the remittance on savings implies that the null hypothesis is rejected. In both cases, remittance positively and statistically significantly impacts the credit ratio. For example, using the IV model, in Column 3, the estimated effect is 0.2011, indicating that a 10% increase in remittance from the GCC countries increases the credit ratio by 20.11%. On the other hand, it is 24.10% for the G7 remittance-sending countries. Similar to

Table 3, per capita income and trade openness positively affect the credit ratio.

The estimated effect of remittance on the liquid liability is reported in

Table 5. A positive and significant effect indicates that remittance increases the liquid liabilities in recipient countries. Comparing the estimated impacts of remittance from GCC, liquid liabilities are highly affected by remittance from the G7 countries.

Table 6 reports the estimated effects of remittance on stock market capitalization. Columns 1 to 3 show that none of the estimates for the GCC countries is statistically significant, indicating that remittance from the GCC countries does not significantly impact the stock market capitalization. On the other hand, the estimated effects for the G7 countries reported in Columns 4 to 6 show that remittance from the G7 countries positively affects stock market capitalization in recipient countries. This result indicates that remittance from highly skilled and educated migrants significantly improves the stock market.

In

Table 7, we report the impact of remittance on gross domestic savings to GDP ratio. The results show that, on average, a 10% increase in remittance from the GCC countries increases the savings ratio by around 10% in each estimated model. The G7 remittance-sending countries have the same positive effect with a relatively large magnitude. This means that remittance recipients from the GCC countries have lower significant saving tendencies than their counterpart G7 countries.

Similar to

Table 3, per capita income and trade openness positively affect the commercial bank account opening tendencies. One of the potential reasons is that migrants to the GCC countries are less educated. Therefore, they are less likely to be attached to the formal banking sectors than their counterpart G7 counties. On the other hand, whenever families in these low-educated or skilled migrants have financial inflows, they are more likely to be attached to banking sectors than their G7 countries.

Table 8 shows the estimated effect of remittance on the selected recipient countries’ commercial bank account opening rate. In both cases, remittance has a positive and statistically significant impact on commercial bank account opening tendencies. For example, using the IV model, in Column 3, the estimated effect is 0.4733, indicating that a 10% increase in remittance from the GCC countries increases the credit ratio by 47.33%. On the other hand, it is only 12.47% for the G7 remittance-sending countries.

To summarize the empirical results, we found a significant positive impact of remittances on financial development in both the highly skilled and the low-skilled labor-abundant remittance-sending countries. We also found that remittance from low-skilled abundant countries has a greater impact on savings and commercial bank account opening. In other words, remittance from low-skilled immigrants significantly improves financial inclusion in the recipient countries. On the other hand, remittance from high-skilled immigrants has a greater impact on improving the stock market and credit ratio than their low-skilled counterparts.

Despite different estimated effects of remittances on financial development in recipient countries, in terms of the nature of the effect, our findings are consistent with the literature. For example,

Coulibaly (

2015) identified a positive relationship between financial development and remittance in sub-Saharan African countries. Using data from 1971 to 2008,

Chowdhury (

2011) also argued that remittances impact financial development. Chowdhury also argued that remittances causally impact financial development, but the opposite is not true.

Nabi and Alam (

2011) argued that remittances improve economic development, including employment generation, poverty alleviation, import financing, and a healthy foreign exchange market. Similarly, for countries in sub-Saharan Africa,

Gupta et al. (

2009) found that remittances reduce poverty and improve sub-Saharan financial development.

Demirgüç-Kunt et al. (

2011) argued that remittances are strongly associated with greater banking breadth and depth, increasing the number of branches and accounts per capita and the amount of deposits compared to GDP.

Fromentin (

2018) found a positive and significant association between remittances and financial development in Latin American and Caribbean countries.

Using Bangladesh as a case study, this study attempts to answer why different results are found for different types of remittance-sending countries. One potential reason is that emigrants have higher living costs in developed countries. However, compared to the emigrants living in GCC countries, their living costs and living standards are low. Therefore, migrants mainly send a higher proportion of their total earnings as remittances. On the other hand, compared to their counterparts, emigrants living in developed countries are less likely to send more significant remittance earnings, measured in terms of the percentage of the total income, as a remittance. In addition, those living in developed countries are more likely to settle for themselves or their family members in developed countries. In such cases, emigrants’ earnings are spent on the immigration process of their respective host countries instead of sending them to their home countries.

Niimi et al. (

2010) also argue that remittances decrease for migrants with tertiary education. As most migrants living in GCC countries are likely to return to their native country, they or their families are more likely to have savings in their home countries. On the other hand, host countries with welcoming immigration policies are more likely to focus on settling their families abroad and, therefore, less likely to plan more in their home countries. Moreover, in recent times, like other sectors, the COVID-19 pandemic has caused an imbalance in the mechanism of migration and its remittance flow. Hence, we examine the particular effect of the COVID-19 pandemic using Bangladesh as a case study due to the unavailability of global data.

Does the same pattern follow during the pandemic?

The COVID-19 pandemic has adversely affected the financial markets and economy, causing high volatility in the stock market (

Fallahgoul 2021;

Farzanegan et al. 2021;

Procacci et al. 2020). For example, increasing the infection numbers decreased the market indices and increased negative financial values (

Albulescu 2020;

Grima et al. 2021;

Tomal 2021). Furthermore,

Brown and Rocha (

2020) argued that businesses were affected during the COVID-19 pandemic, distressing the debt market and leading to another global financial crisis.

Salinas et al. (

2021) argued that people face multidimensional dynamics with many recursively interacting indicators. This complex interaction ultimately produces emerging behaviors of great uncertainty.

Vasin (

2022) argued that the pandemic indirectly affected the economy through the uncertainty and rigidity of preventive measures.

As the worldwide economy has been adversely affected by the COVID-19 pandemic, it is highly likely to affect remittance and migrants adversely. However, data are not available to examine whether remittance from labor-intensive emigrants’ countries has the same effect reported in the earlier section. Therefore, we consider Bangladesh as a case study.

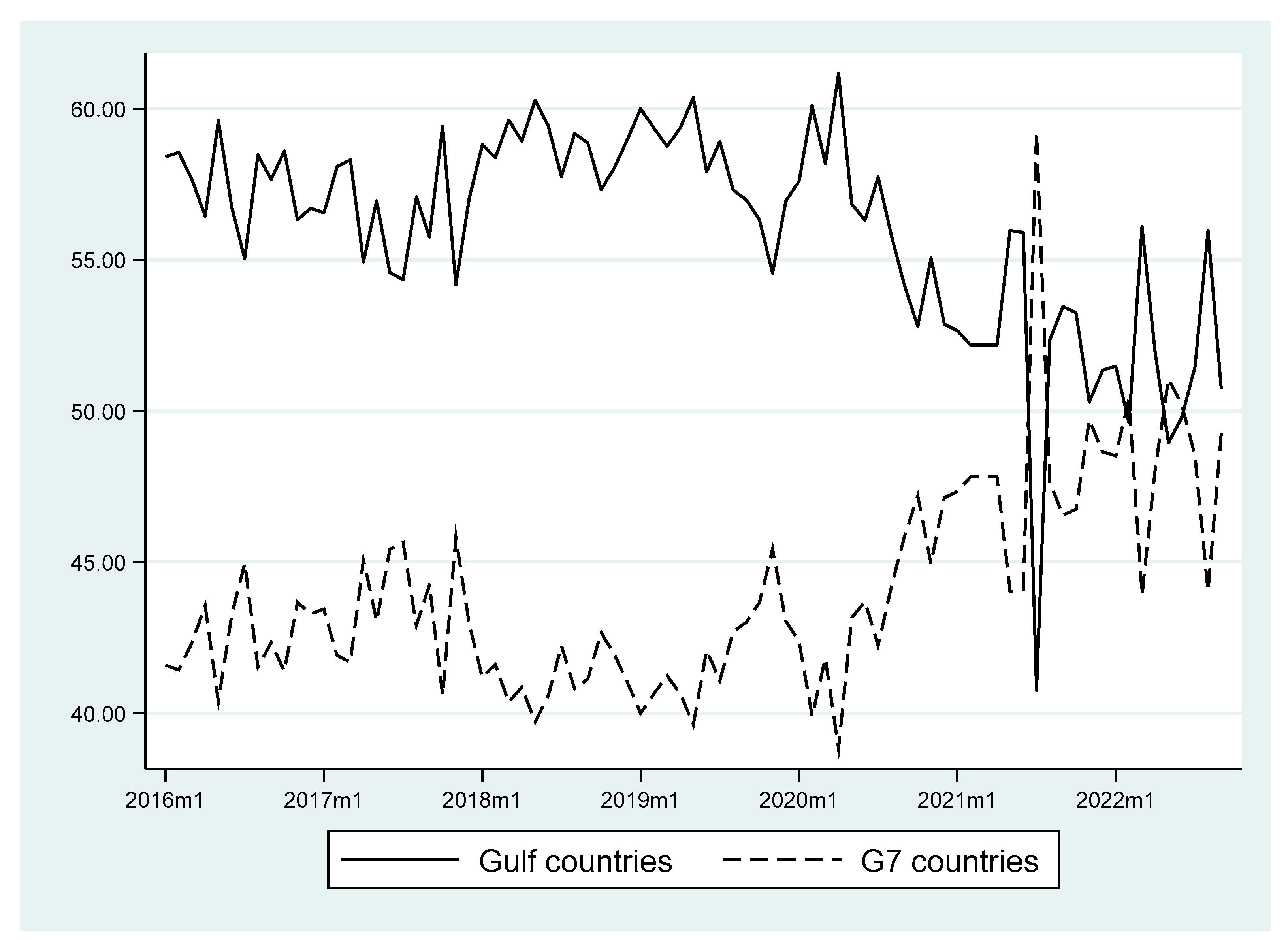

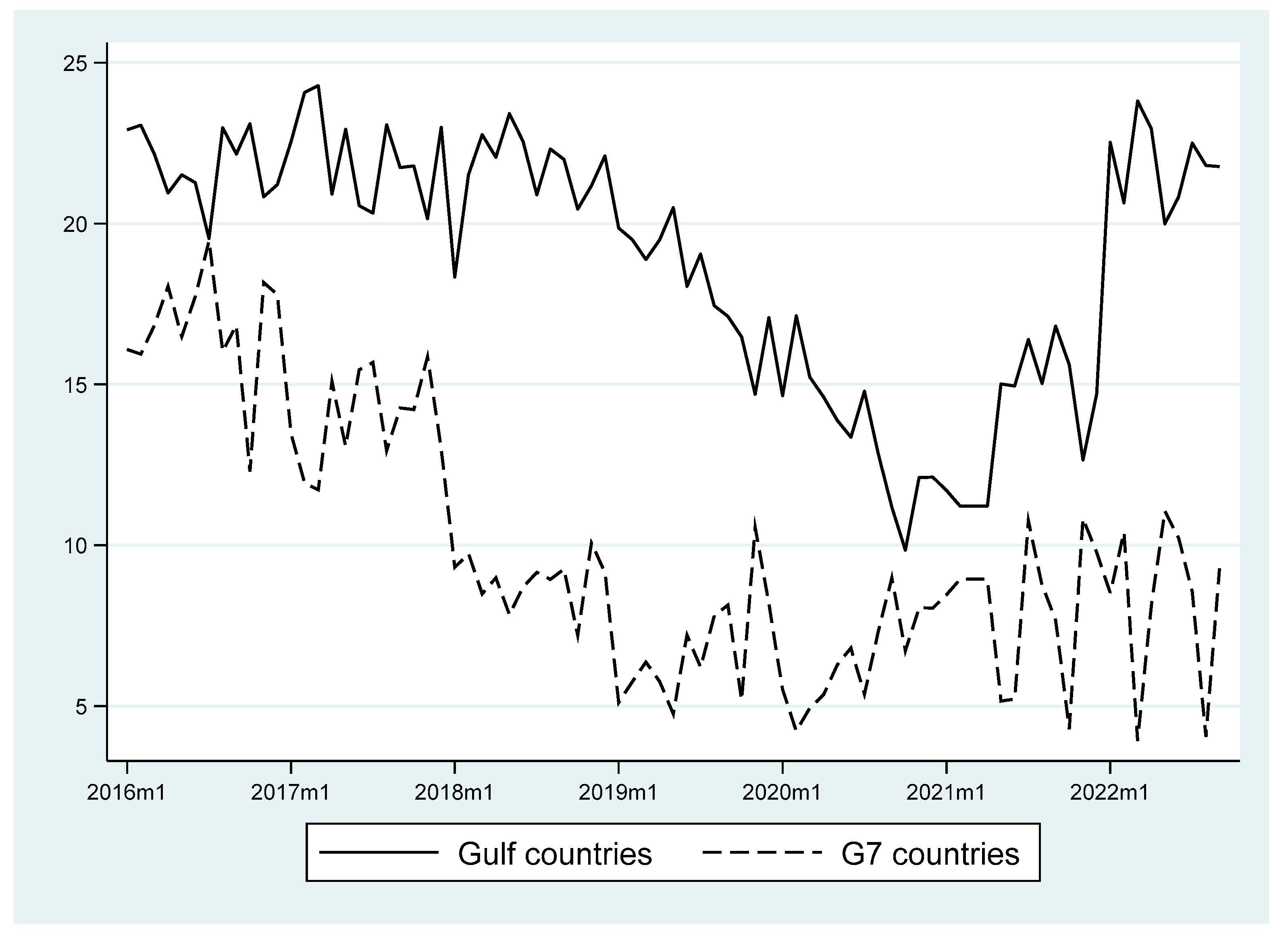

Figure 1 shows that the percentage share of remittance from GCC countries has been higher since 2006, except in mid-2021. Due to lack of data, considering Bangladesh as a case study, we also consider three commercial bank branches to examine the same effect on the savings ratio.

We consider three banks and depositors with remittances. There are 1540 bank account holders, 221 accounts receiving remittances from GCC countries, and 200 receiving them from G7 countries. We found the same patterns in

Figure 2. During the COVID-19 pandemic, remittance from GCC and G7 countries decreased, but the remittance share from GCC countries was higher than the G7 countries. In addition, bank authorities confirmed that recipients from the GCC countries had less cash withdrawal tendencies than their counterpart G7 countries. In other words, remittance recipients from the GCC countries have more savings. These findings ultimately confirm that the GCC countries’ remittance has more impact on the financial development than their counterpart countries.

6. Conclusions

Although remittance has a greater impact on recipient countries’ economic development, few studies have examined whether the types of remittance-sending countries have different effects on financial development in recipient countries. Considering the GCC countries as a source of remittance from low-skilled labor countries and G7 countries as high-skilled source countries, using an IV approach, we found that remittance positively impacts the financial development in recipient countries. We also found that remittance from relatively low-skilled emigrants has a greater impact on financial inclusion in the recipient countries than their high-skilled counterparts. The findings also suggest similar effects of remittance on financial development during the pandemic. The results suggest that policymakers should plan for policies that provide better foreign employment opportunities and investment policies in the home financial markets. Such approaches allow remittance-recipient countries to effectively manage the disruption of economic activity caused by the pandemic.

Although this study found a positive impact of remittance on financial inclusion, it has the following limitations: underreporting macro-level remittance amount and sporadic or missing data. First, the GCC and G7 countries were assumed to be a source of remittance from the low and high-skilled migrants as official micro-level data with educational or skilled-based information were not available. Second, G7 member countries could have more unskilled migrants from neighboring countries. Third, remittance inflows and migrant numbers might be uncorrelated. Fourth, some countries might inconsistently report remittances. For example, some countries report only workers’ remittances or compensation of employees, while others report these variables and migrant transfers. Fifth, the COVID-19 pandemic adversely affected the global economy from both micro and macro perspectives. For example, many small businesses have closed during the pandemic, leading to a reduced number of employees. This ultimately reduces the earnings of some of the emigrants, which could reduce their remittances. Examining the effect of closing shops and restaurants on remittances and financial development in recipient countries would be an interesting future study. Moreover, an analysis after the pandemic era for many countries would offer a more comprehensive scenario to policymakers. Finally, a significant amount of remittance is transferred through informal channels, such as migrants bringing cash with them when visiting their native country.

{kind=link}

{kind=link}