Equity Market Pricing and Central Bank Interventions: A Panel Data Approach

Abstract

1. Introduction

2. Literature Review

3. Methodology and Data

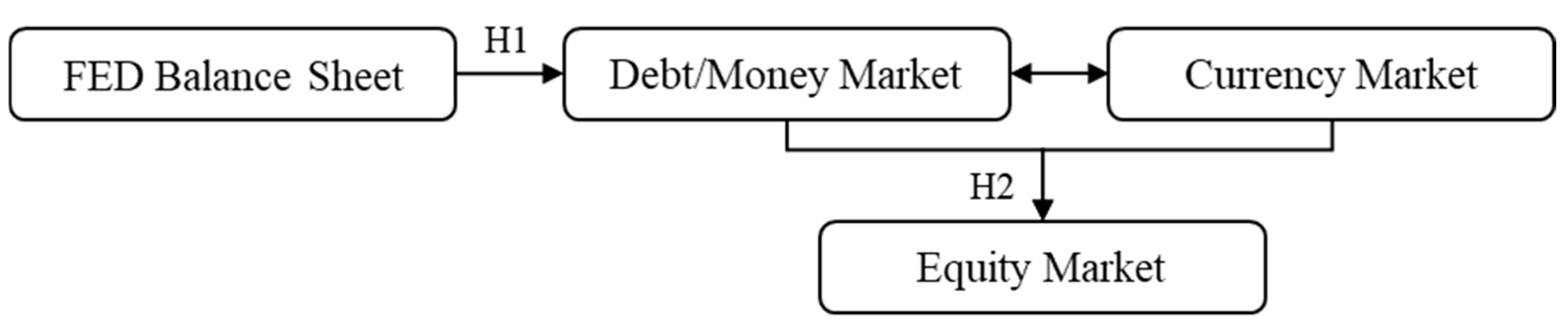

3.1. Empirical Model

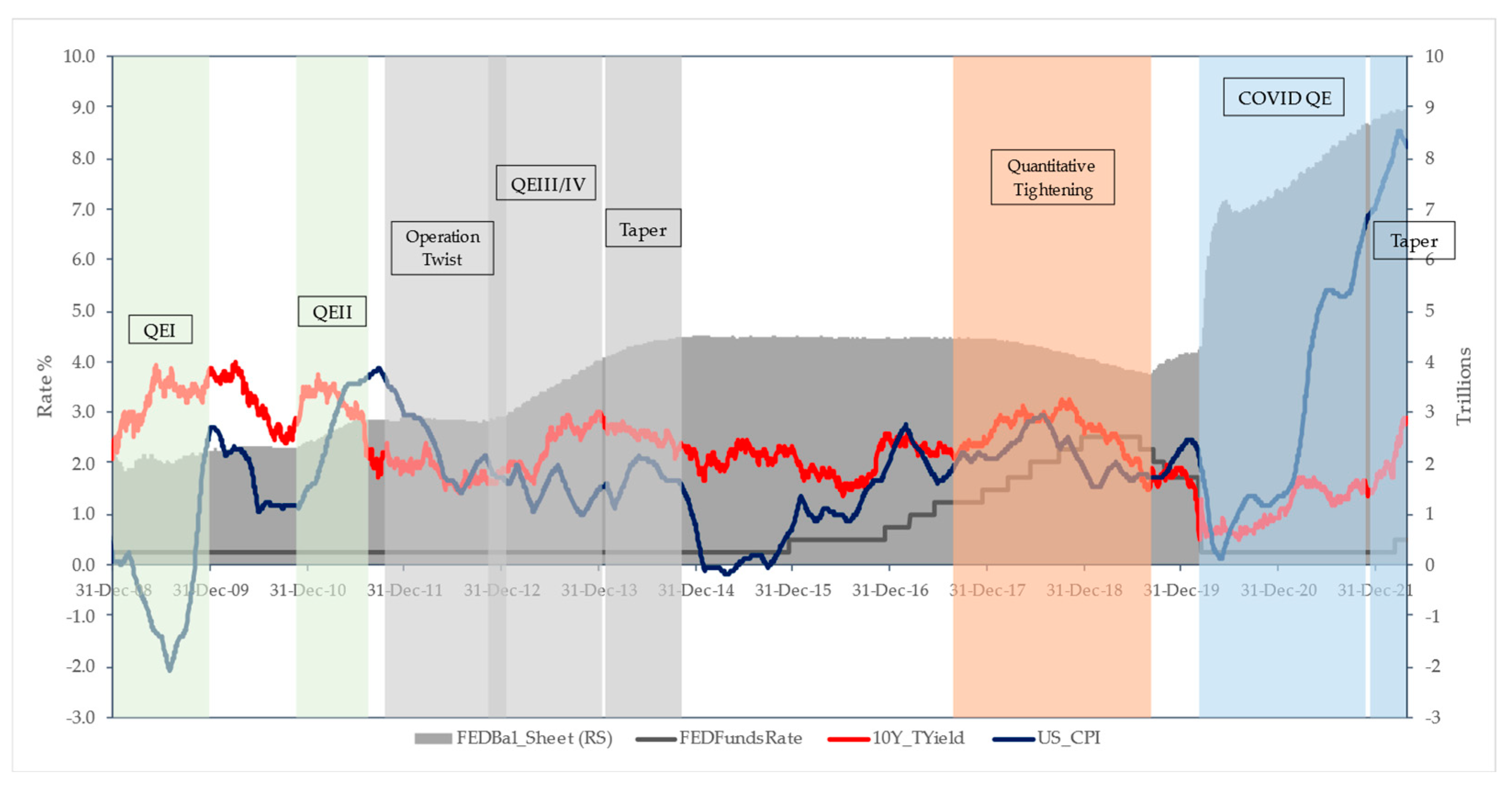

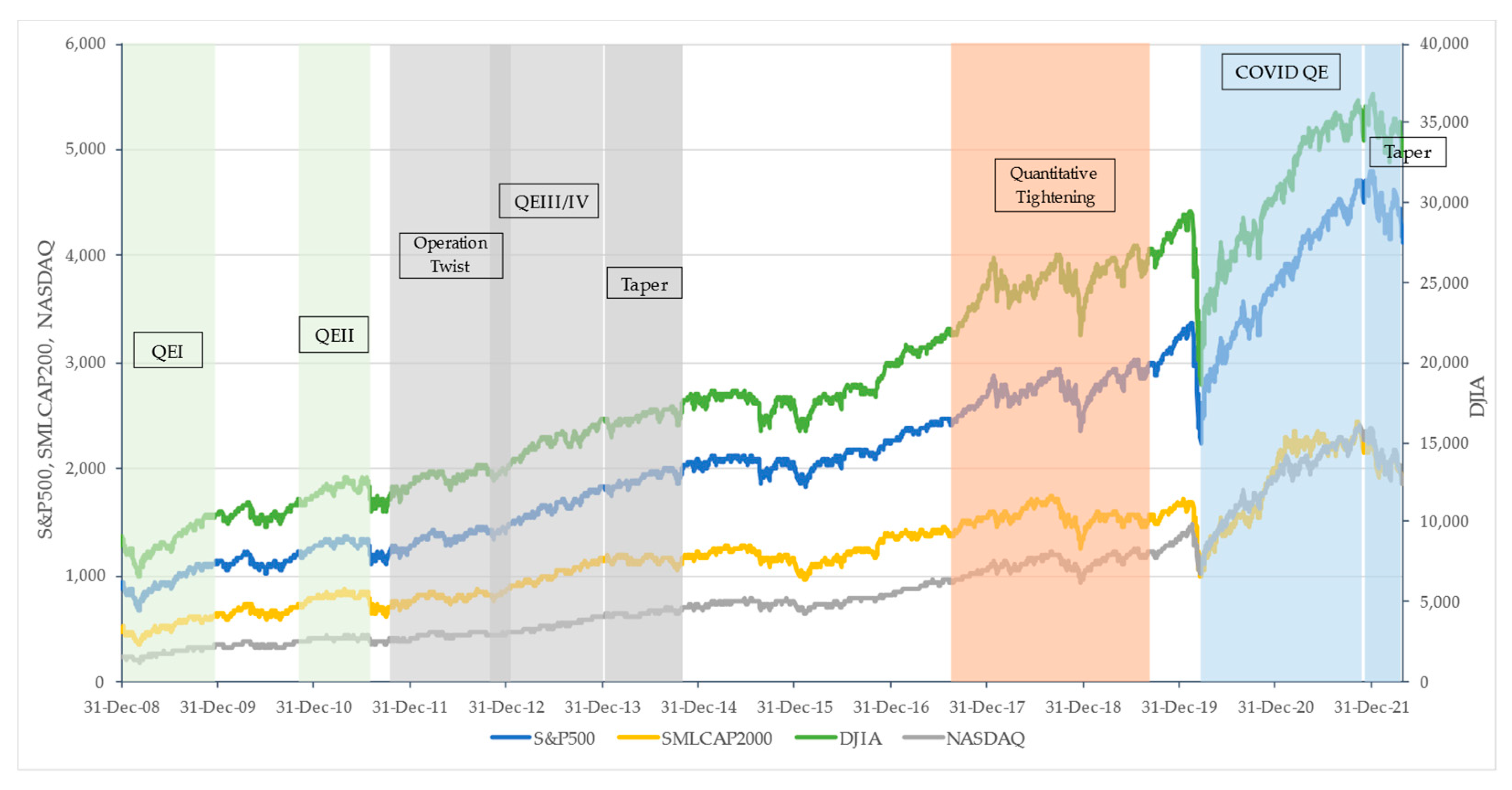

3.2. Data

4. Results and Discussion

4.1. Correlations Analysis

4.2. Regressions Results

4.3. Intervention Regressions Results

4.4. The Portfolio Approach

Panel Data Regression Results

4.5. Identification of Instrumental Variables Tests

4.6. Relevance of Instrumental Variables Tests

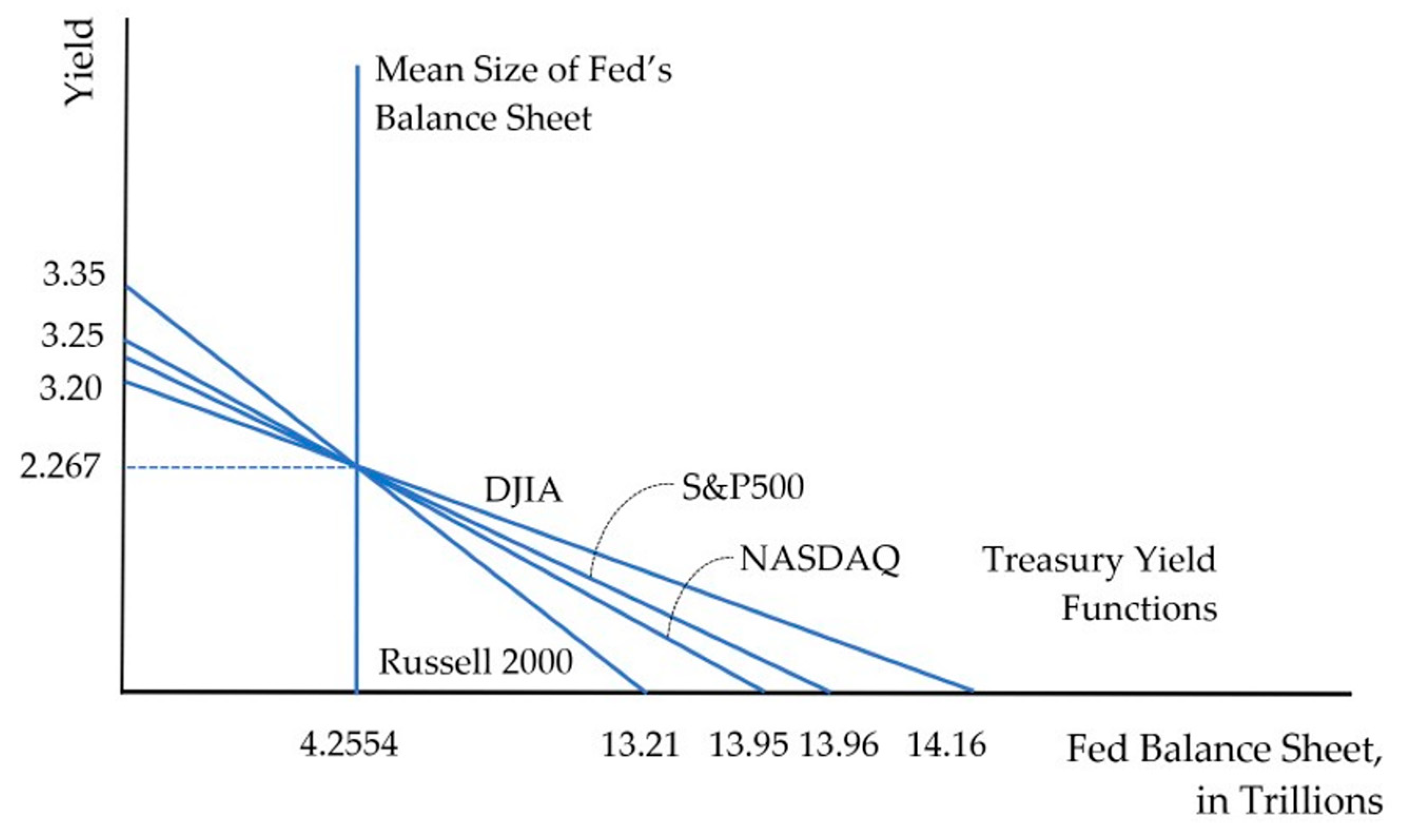

4.7. Results Discussion

5. Implications

6. Conclusions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| SP500 | DJIA | Nasdaq | Russell | Fed_BS | L1_BS | L5_BS | Fed_FRte | t_yield | usd_eur | wti_spt | us_cpi | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SP500 | 1 | |||||||||||

| DJIA Nasdaq | 0.9956 * 0.0000 0.9950 * 0.0000 | 1 0.9900 * 0.0000 | 1 | |||||||||

| Russell | 0.9914 * | 0.9844 * | 0.9896 * | 1 | ||||||||

Fed_BS | 0.0000 0.9391 * | 0.0000 0.9391 * | 0.0000 0.9427 * | 0.9322 * | 1 | |||||||

L1_BS | 0.0000 0.9386 * | 0.0000 0.9388 * | 0.0000 0.9425 * | 0.0000 0.9316 * | 0.9996 * | 1 | ||||||

L5_BS | 0.0000 0.9368 * 0.0000 | 0.0000 0.9374 * 0.0000 | 0.0000 0.9418 * 0.0000 | 0.0000 0.9293 * 0.0000 | 0.0000 0.9982 * 0.0000 | 0.9986 * 0.0000 | 1 | |||||

| Fed_FRte | - | - | - | - | - | - | - | 1 | ||||

| - | - | - | - | - | - | - | ||||||

| t_yield | −0.4187 * | −0.4707 * | −0.4211 * | −0.3546 * | −0.4962 * | −0.4979 * | −0.5067 * | - | 1 | |||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | - | |||||

| usd_eur | 0.1716 * | 0.1940 * | 0.1821 * | 0.1411 * | 0.1938 * | 0.1946 * | 0.1976 * | - | −0.5324 * | 1 | ||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | - | 0.0000 | ||||

| wti_spt | 0.8186 * | 0.8385 * | 0.8342 * | 0.8335 * | 0.7295 * | 0.7291 * | 0.7290 * | - | −0.2902 * | 0.0066 | 1 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | - | 0.0000 | 0.8146 | |||

| us_cpi | 0.3866 * | 0.4392 * | 0.4068 * | 0.4032 * | 0.4016 * | 0.4016 * | 0.4017 * | - | −0.3064 * | 0.0608 | 0.6168 * | 1 |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | - | 0.0000 | 0.0304 | 0.0000 |

| SP500 | DJIA | Nasdaq | Russell | Fed_BS | L1_BS | L5_BS | Fed_FRte | t_yield | usd_eur | wti_spt | us_cpi | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SP500 | 1 | |||||||||||

| DJIA Nasdaq | 0.9909 * 0.0000 0.9783 * 0.0000 | 1 0.9762 * 0.0000 | 1 | |||||||||

| Russell | 0.9176 * | 0.9454 * | 0.9530 * | 1 | ||||||||

Fed_BS | 0.0000 0.9395 * | 0.0000 0.9169 * | 0.0000 0.8818 * | 0.7923 * | 1 | |||||||

L1_BS | 0.0000 0.9387 * | 0.0000 0.9156 * | 0.0000 0.8808 * | 0.0000 0.7897 * | 0.9985 * | 1 | ||||||

L5_BS | 0.0000 0.9329 * 0.0000 | 0.0000 0.9074 * 0.0000 | 0.0000 0.8758 *0.0000 | 0.0000 0.7799 * 0.0000 | 0.0000 0.9942 * 0.0000 | 0.9952 * 0.0000 | 1 | |||||

| Fed_FRte | 0.137 | 0.1129 | 0.0779 | 0.0518 | 0.1998 * | 0.2005 * | 0.2003 * | 1 | ||||

| 0.0019 | 0.0105 | 0.0778 | 0.2416 | 0.0000 | 0.0000 | 0.0000 | ||||||

| t_yield | 0.8249 * | 0.8272 * | 0.7448 * | 0.7776 * | 0.8121 * | 0.8190 * | 0.8280 * | 0.3310 * | 1 | |||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |||||

| usd_eur | −0.2720 * | −0.3581 * | −0.4108 * | −0.5149 * | −0.0833 | −0.0792 | −0.0457 | 0.2030 * | −0.048 | 1 | ||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0594 | 0.0736 | 0.3043 | 0.0000 | 0.2774 | ||||

| wti_spt | 0.9011 * | 0.8884 * | 0.8441 * | 0.8231 * | 0.8783 * | 0.8786 * | 0.8812 * | 0.2782 * | 0.9232 * | −0.1361 | 1 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0020 | |||

| us_cpi | 0.8725 * | 0.8317 * | 0.7680 * | 0.6746 * | 0.8822 * | 0.8838 * | 0.8902 * | 0.2509 * | 0.8595 * | 0.1269 | 0.9073 * | 1 |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0040 | 0.0000 |

Appendix B

| Model | 3SLS | 3SLS_L5 | SUR | SUR_L5 | Robust | Robust_L5 |

|---|---|---|---|---|---|---|

| Index | S&P500 | |||||

| Fed_FRte | 384.93074 | 382.39472 | 341.87481 | 343.29474 | 404.62291 | 397.81695 |

| us_cpi | 333.8543 | 332.7608 | 320.0322 | 319.9994 | 337.4309 | 335.8427 |

| _cons | 1327.1010 | 1331.8388 | 1380.8500 | 1381.1001 | 1307.7838 | 1316.1561 |

| t_yield | ||||||

| Fed_BS | −0.2337 | −1.4081 | −0.2225 | −1.7064 | −0.2202 | −1.7530 |

| L5_BS | 1.1790 | 1.4893 | 1.5363 | |||

| _cons | 3.2618 | 3.2549 | 3.2141 | 3.2070 | 3.2042 | 3.2056 |

| usd_eur | ||||||

| t_yield | −0.0450 | −0.0422 | −0.0391 | −0.0375 | −0.0472 | −0.0435 |

| wti_spt | −0.0018 | −0.0018 | −0.0017 | −0.0017 | −0.0018 | −0.0018 |

| _cons | 1.0480 | 1.0427 | 1.0234 | 1.0217 | 1.0519 | 1.0449 |

| Index | Nasdaq | |||||

| Fed_FRte | 1183.6028 | 1174.2210 | 1026.3398 | 1031.1730 | 1164.4119 | 1145.8599 |

| us_cpi | 1292.0513 | 1289.9159 | 1243.1496 | 1244.3260 | 1275.7923 | 1272.5377 |

| _cons | 2642.4893 | 2655.5136 | 2835.7710 | 2833.6290 | 2685.8162 | 2706.8413 |

| t_yield | ||||||

| Fed_BS | −0.2340 | −1.3605 | −0.2260 | −1.6988 | −0.2122 | −2.0778 |

| L5_BS | 1.1304 | 1.4781 | 1.8716 | |||

| _cons | 3.2629 | 3.2586 | 3.2289 | 3.2219 | 3.1702 | 3.1642 |

| usd_eur | ||||||

| t_yield | −0.0520 | −0.0490 | −0.0411 | −0.0395 | −0.0555 | −0.0513 |

| wti_spt | −0.0018 | −0.0018 | −0.0017 | −0.0018 | −0.0018 | −0.0018 |

| _cons | 1.0638 | 1.0583 | 1.0324 | 1.0308 | 1.0699 | 1.0623 |

| Index | DJIA | |||||

| Fed_FRte | 4137.8341 | 4119.3297 | 3813.1064 | 3823.4318 | 4350.7396 | 4308.5433 |

| us_cpi | 2469.4851 | 2462.0312 | 2362.0200 | 2362.6059 | 2502.5455 | 2494.4704 |

| _cons | 11,913.1050 | 11,947.2620 | 12,324.6550 | 12,325.5320 | 11,715.0120 | 11,765.1700 |

| t_yield | ||||||

| Fed_BS | −0.2289 | −1.3725 | −0.2182 | −1.6731 | −0.2067 | −2.1008 |

| L5_BS | 1.1476 | 1.4598 | 1.9005 | |||

| _cons | 3.2415 | 3.2364 | 3.1956 | 3.1901 | 3.1468 | 3.1391 |

| usd_eur | ||||||

| t_yield | −0.0465 | −0.0437 | −0.0393 | −0.0377 | −0.0502 | −0.0461 |

| wti_spt | −0.0018 | −0.0018 | −0.0017 | −0.0017 | −0.0018 | −0.0018 |

| _cons | 1.0512 | 1.0458 | 1.0248 | 1.0231 | 1.0576 | 1.0500 |

| Index | Russell | |||||

| Fed_FRte | 208.4120 | 206.6854 | 186.2845 | 186.9564 | 212.6758 | 209.6973 |

| us_cpi | 146.9944 | 146.2313 | 140.5160 | 140.3782 | 148.0706 | 147.0385 |

| _cons | 807.1451 | 810.3717 | 833.5691 | 834.1026 | 802.3836 | 806.9149 |

| t_yield | ||||||

| Fed_BS | −0.2532 | −1.5440 | −0.2403 | −1.8271 | −0.2490 | −1.6239 |

| L5_BS | 1.2980 | 1.5945 | 1.3810 | |||

| _cons | 3.3449 | 3.3278 | 3.2897 | 3.2735 | 3.3270 | 3.3154 |

| usd_eur | ||||||

| t_yield | −0.0390 | −0.0366 | −0.0374 | −0.0359 | −0.0397 | −0.0369 |

| wti_spt | −0.0019 | −0.0019 | −0.0017 | −0.0017 | −0.0019 | −0.0019 |

| _cons | 1.0372 | 1.0322 | 1.0200 | 1.0182 | 1.0384 | 1.0328 |

| Endogenous variables: | 1896 1923 1971 1984 t_yield usd_eur | |||||

| Exogenous variables: | Fed_FRte us_cpi L5_BS Fed_BS wti_spt | |||||

Appendix C

| Panel A: Correlation Matrix of Residuals (without Balance Sheet Weekly Lag): | Panel B: Correlation Matrix of Residuals (with Balance Sheet Weekly Lag): | ||||||

| SP500 | t_yield | usd_eur | SP500 | t_yield | usd_eur | ||

| SP500 | 1 | SP500 | 1 | ||||

| t_yield | −0.1666 | 1 | t_yield | −0.1631 | 1 | ||

| usd_eur | 0.1094 | 0.2443 | 1 | usd_eur | 0.1042 | 0.2207 | 1 |

| Breusch–Pagan test of independence: | Breusch–Pagan test of independence: | ||||||

| chi2(3) = 334.467, | Pr = 0.0000 | chi2(3) = 289.651, | Pr = 0.0000 | ||||

| Correlation matrix of residuals: | Correlation matrix of residuals: | ||||||

| DJIA | t_yield | usd_eur | DJIA | t_yield | usd_eur | ||

| DJIA | 1 | DJIA | 1 | ||||

| t_yield | −0.1859 | 1 | t_yield | −0.1813 | 1 | ||

| usd_eur | 0.0984 | 0.2443 | 1 | usd_eur | 0.0931 | 0.2207 | 1 |

| Breusch–Pagan test of independence: | Breusch–Pagan test of independence: | ||||||

| chi2(3) = 349.718, | Pr = 0.0000 | chi2(3) = 303.367, | Pr = 0.0000 | ||||

| Correlation matrix of residuals: | Correlation matrix of residuals: | ||||||

| Nasdaq | t_yield | usd_eur | Nasdaq | t_yield | usd_eur | ||

| Nasdaq | 1 | Nasdaq | 1 | ||||

| t_yield | −0.1702 | 1 | t_yield | −0.1649 | 1 | ||

| usd_eur | 0.029 | 0.2443 | 1 | usd_eur | 0.0238 | 0.2207 | 1 |

| Breusch–Pagan test of independence: | Breusch–Pagan test of independence: | ||||||

| chi2(3) = 301.150, | Pr = 0.0000 | chi2(3) = 257.073, | Pr = 0.0000 | ||||

| Correlation matrix of residuals: | Correlation matrix of residuals: | ||||||

| Russell 2000 | t_yield | usd_eur | Russell 2000 | t_yield | usd_eur | ||

| Russell 2000 | 1 | Russell 2000 | 1 | ||||

| t_yield | −0.0943 | 1 | t_yield | −0.0981 | 1 | ||

| usd_eur | 0.162 | 0.2443 | 1 | usd_eur | 0.1568 | 0.2207 | 1 |

| Breusch–Pagan test of independence: | Breusch–Pagan test of independence: | ||||||

| chi2(3) = 319.167, | Pr = 0.0000 | chi2(3) = 278.725, | Pr = 0.0000 | ||||

References

- Albu, Lucian Liviu, Radu Lupu, and Adrian Cantemir Călin. 2016. Quantitative easing, tapering and stock market indices. Economic Computation and Economic Cybernetics Studies and Research 50: 5–23. [Google Scholar]

- Amano, Robert, and Simon van Norden. 1995. Exchange Rates and Oil Prices. Munich: University Library of Munich, Germany. Available online: https://EconPapers.repec.org/RePEc:wpa:wuwpif:9509001 (accessed on 27 August 2022).

- Beckmann, Joscha, Robert L. Czudaj, and Vipin Arora. 2020. The relationship between oil prices and exchange rates: Revisiting theory and evidence. Energy Economics 88: 104772. [Google Scholar] [CrossRef]

- Bernanke, Ben S., and Kenneth N. Kuttner. 2005. What Explains the Stock Market’s Reaction to Federal Reserve Policy? The Journal of Finance 60: 1221–57. [Google Scholar] [CrossRef]

- Boeckx, Jef, Maarten Dossche, and Gert Peersman. 2014. Effectiveness and Transmission of the ECB’s Balance Sheet Policies. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Breusch, Trevor S., and Adrian R. Pagan. 1980. The Lagrange Multiplier Test and its Applications to Model Specification in Econometrics. The Review of Economic Studies 47: 239–53. [Google Scholar] [CrossRef]

- Chari, Anusha, Karlye Dilts Stedman, and Christian Lundblad. 2017. Taper Tantrums: QE, Its Aftermath and Emerging Market Capital Flows. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Cochrane, John H. 2005. Asset Pricing, Rev. ed. Princeton: Princeton University Press. [Google Scholar]

- Cox, Jeff. 2021. Fed to Start Tapering Bond Purchases Later This Month as it Begins Pulling back on Pandemic Aid. Englewood Cliffs: CNBC. Available online: https://www.cnbc.com/2021/11/03/fed-decision-taper-timetable-as-it-starts-pulling-back-on-pandemic-era-economic-aid-.html (accessed on 27 August 2022).

- Cragg, John G., and Stephen Donald. 1993. Testing Identifiability and Specification in Instrumental Variable Models. Econometric Theory 9: 222–40. [Google Scholar] [CrossRef]

- D’Amico, Stefania, and Thomas King. 2010. Flow and Stock Effects of Large-Scale Treasury Purchases. Washington, DC: Board of Governors of the Federal Reserve System (U.S.). Available online: https://EconPapers.repec.org/RePEc:fip:fedgfe:2010-52 (accessed on 27 August 2022).

- D’Amico, Stefania, William English, David Lopez-Salido, and Edward Nelson. 2012. The Federal Reserve’s Large-Scale Asset Purchase Programs: Rationale and Effects (Issue 9145). C.E.P.R. Discussion Papers. Available online: https://EconPapers.repec.org/RePEc:cpr:ceprdp:9145 (accessed on 27 August 2022).

- Doh, Taeyoung. 2010. The efficacy of large-scale asset purchases at the zero lower bound. Economic Review 95: 5–34. [Google Scholar]

- EIKON Refinitive. 2022. Eikon Financial Analysis & Trading SoftwareRefinitiv. Available online: https://solutions.refinitiv.com/eikon-trading-software?utm_content=Refinitiv%20Brand%20Product-CEE-EMEA-G-EN-BMM&utm_medium%20=cpc&utm_source=google&utm_campaign=68832_RefinitivBAUPaidSearch&elqCampaignId=5917&utm_term=%20%20refinitiv%20%20eikon&gclid=EAIaIQobChMI5eiJ_OjO6gIVgbHtCh3ODAUqEAAYASAAEgKcvPD_BwE (accessed on 16 May 2022).

- Fama, Eugene F. 1965. Random Walks in Stock Market Prices. Financial Analysts Journal 21: 55–59. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 2002. The Equity Premium. The Journal of Finance 57: 637–59. [Google Scholar] [CrossRef]

- Federal Reserve. 2021a. Federal Reserve Issues FOMC Statement; Washington, DC: Board of Governors of the Federal Reserve System. Available online: https://www.federalreserve.gov/newsevents/pressreleases/monetary20211103a.htm (accessed on 27 August 2022).

- Federal Reserve. 2021b. Federal Reserve Issues FOMC Statement; Washington, DC: Board of Governors of the Federal Reserve System. Available online: https://www.federalreserve.gov/newsevents/pressreleases/monetary20211215a.htm (accessed on 27 August 2022).

- Fisher, Franklin M. 1970. Simultaneous Equations Estimation: The State of the Art. p. 55. Available online: https://ideas.repec.org/p/mit/worpap/55.html (accessed on 27 August 2022).

- Fratzscher, Marcel, Daniel Schneider, and Ine Van Robays. 2013. Oil Prices, Exchange Rates and Asset Prices. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Gagnon, Joseph, Matthew Raskin, Julie Remache, and Brian Sack. 2011. The Financial Market Effects of the Federal Reserve’s Large-Scale Asset Purchases. International Journal of Central Banking 7: 3–43. [Google Scholar]

- Hamilton, James, and Jing Cynthia Wu. 2012. The Effectiveness of Alternative Monetary Policy Tools in a Zero Lower Bound Environment. Journal of Money, Credit and Banking 44: 3–46. [Google Scholar] [CrossRef]

- Hausman, Jerry. 1983. Specification and estimation of simultaneous equation models. In Handbook of Econometrics. Edited by Zvi Griliches and Michael. D. Intriligator. Amsterdam: Elsevier, vol. 1, pp. 391–448. Available online: https://EconPapers.repec.org/RePEc:eee:ecochp:1-07 (accessed on 27 August 2022).

- Hausman, Jerry, Whitney Newey, and William Taylor. 1987. Efficient Estimation and Identification of Simultaneous Equation Models with Covariance Restrictions. Econometrica 55: 849–74. [Google Scholar] [CrossRef]

- Khemraj, Tarron, and Sherry Yu. 2015. The Effectiveness of Quantitative Easing: New Evidence on Private Investment. Applied Economics 48: 2625–35. [Google Scholar] [CrossRef]

- Kim, Duhyeong. 2023. International effects of quantitative easing and foreign exchange intervention. Journal of International Economics 145: 103815. [Google Scholar] [CrossRef]

- Krugman, Paul. 1980. Oil and the Dollar. Issue 0554. Cambridge: National Bureau of Economic Research, Inc. Available online: https://EconPapers.repec.org/RePEc:nbr:nberwo:0554 (accessed on 27 August 2022).

- Krugman, Paul, and Maurice Obstfeld. 2006. International Economics: Theory and Policy. Boston: Addison-Wesley. Available online: https://books.google.vu/books?id=7ep-ngEACAAJ (accessed on 27 August 2022).

- Moench, Emanuel, and Soroosh Soofi-Siavash. 2022. What moves treasury yields? Journal of Financial Economics 146: 1016–43. [Google Scholar] [CrossRef]

- Moessner, Richhild. 2015. Effects of ECB balance sheet policy announcements on inflation expectations. Applied Economics Letters 22: 483–87. [Google Scholar] [CrossRef]

- Mokni, Khaled. 2020. Time-varying effect of oil price shocks on the stock market returns: Evidence from oil-importing and oil-exporting countries. Energy Reports 6: 605–19. [Google Scholar] [CrossRef]

- Narayanan, R. 1969. Computation of Zellner-Theil’s Three Stage Least Squares Estimates. Econometrica 37: 298–306. [Google Scholar] [CrossRef]

- O’Donnell, Niall, Barry Sheehan, and Darren Shannon. 2024. The impact of monetary policy interventions on banking sector stocks: An empirical investigation of the COVID-19 crisis. Financial Innovation 10: 44. [Google Scholar] [CrossRef]

- Olea, José Luis Montiel, and Carolin Pflueger. 2013. A Robust Test for Weak Instruments. Journal of Business & Economic Statistics 31: 358–69. [Google Scholar]

- Pflueger, Carolin E., and Su Wang. 2015. A Robust Test for Weak Instruments in Stata. The Stata Journal 15: 216–25. [Google Scholar] [CrossRef]

- Rao, D. Tripati, and Rahul Kumar. 2023. An Assessment of Unconventional Monetary Policy During COVID-19 Pandemic in India. Journal of Emerging Market Finance 22: 297–325. [Google Scholar] [CrossRef]

- Rigobon, Roberto, and Brian Sack. 2004. The impact of monetary policy on asset prices. Journal of Monetary Economics 51: 1553–75. [Google Scholar] [CrossRef]

- Sargan, John D. 1964. Three-Stage Least-Squares and Full Maximum Likelihood Estimates. Econometrica 32: 77–81. [Google Scholar] [CrossRef]

- Sharpe, William F. 1964. Capital Asset Prices: A Theory of Market Equilibrium Under Conditions of Risk*. The Journal of Finance 19: 425–42. [Google Scholar] [CrossRef]

- Stock, James, and Mark Yogo. 2005. Testing for Weak Instruments in Linear IV Regression. In Identification and Inference for Econometric Models. Edited by Donald W. K. Andrews. Cambridge: Cambridge University Press, pp. 80–108. Available online: http://www.economics.harvard.edu/faculty/stock/files/TestingWeakInstr_Stock\%2BYogo.pdf (accessed on 27 August 2022).

- Vasicek, Oldrich. 1977. An equilibrium characterization of the term structure. Journal of Financial Economics 5: 177–88. [Google Scholar] [CrossRef]

- Vukovic, Darko, Kseniya A. Lapshina, and Moinak Maiti. 2019. European Monetary Union bond market dynamics: Pre & post crisis. Research in International Business and Finance 50: 369–80. [Google Scholar] [CrossRef]

- Wei, Xiaoyun, and Liyan Han. 2021. The impact of COVID-19 pandemic on transmission of monetary policy to financial markets. International Review of Financial Analysis 74: 101705. [Google Scholar] [CrossRef]

- Wooldridge, Jeffrey M. 2002. Econometric Analysis of Cross Section and Panel Data. Cambridge: MIT Press. [Google Scholar]

- Zellner, Arnold, and Henry Theil. 1962. Three-Stage Least Squares: Simultaneous Estimation of Simultaneous Equations. Econometrica 30: 54. [Google Scholar] [CrossRef]

| Variable | Obs. | Mean | Std. Dev. | Min | Max | Variance | Skewness | Kurtosis |

|---|---|---|---|---|---|---|---|---|

| SP500 | 3366 | 2210.98 | 981.02 | 676.53 | 4796.56 | 96,2396.9 | 0.776312 | 2.919836 |

| DJIA | 3366 | 19,267.45 | 7585.67 | 6547.05 | 36,799.65 | 57,500,000 | 0.535292 | 2.316637 |

| Nasdaq | 3366 | 5869.56 | 3670.72 | 1268.64 | 16,057.44 | 13,500,000 | 1.118963 | 3.39836 |

| Russell | 3366 | 1220.94 | 472.38 | 343.26 | 2442.74 | 223,147.1 | 0.512697 | 2.711547 |

| Fed_BS | 3366 | 4.2554 | 1.7627 | 1.8434 | 8.9650 | 3.106988 | 1.120021 | 3.684149 |

| L1_BS | 3365 | 4.2540 | 1.7611 | 1.8434 | 8.9650 | 3.101389 | 1.120168 | 3.687226 |

| L5_BS | 3361 | 4.2484 | 1.7547 | 1.8434 | 8.9650 | 3.078825 | 1.120617 | 3.699171 |

| Fed_FRte | 3366 | 0.6326 | 0.6877 | 0.250 | 2.500 | 0.472965 | 1.64255 | 4.223993 |

| t_yield | 3366 | 2.2673 | 0.7317 | 0.499 | 3.994 | 0.535385 | −0.06953 | 2.715562 |

| usd_eur | 3366 | 0.81961 | 0.07531 | 0.6605 | 0.9627 | 0.005672 | −0.15913 | 1.747966 |

| wti_spt | 3366 | 68.8356 | 23.1513 | 7.79 | 126.47 | 535.981 | −0.08693 | 2.232741 |

| us_cpi | 3366 | 1.9182 | 1.6700 | −2.10 | 8.56 | 2.788834 | 1.361179 | 6.635508 |

| SP500 | DJIA | Nasdaq | Russell | Fed_BS | L1_BS | L5_BS | Fed_FRte | t_yield | usd_eur | wti_spt | us_cpi | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SP500 | 1 | |||||||||||

| DJIA | 0.9925 * | 1 | ||||||||||

| 0.0000 | ||||||||||||

| Nasdaq | 0.9893 * | 0.9731 * | 1 | |||||||||

| 0.0000 | 0.0000 | |||||||||||

| Russell | 0.9771 * | 0.9803 * | 0.9546 * | 1 | ||||||||

| 0.0000 | 0.0000 | 0.0000 | ||||||||||

| Fed_BS | 0.9255 * | 0.8830 * | 0.9342 * | 0.8857 * | 1 | |||||||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | |||||||||

| L1_BS | 0.9257 * | 0.8832 * | 0.9343 * | 0.8860 * | 0.9999 * | 1 | ||||||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | ||||||||

| L5_BS | 0.9262 * | 0.8838 * | 0.9345 | 0.8875 | 0.9996 * | 0.9997 * | 1 | |||||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |||||||

| Fed_FRte | 0.3128 * | 0.4120 * | 0.2373 * | 0.3602 * | −0.0184 | −0.0178 | −0.0156 | 1 | ||||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.2866 | 0.3014 | 0.3672 | ||||||

| t_yield | −0.5405 * | −0.5189 * | −0.5578 * | −0.4742 * | −0.6140 * | −0.6134 * | −0.6111 * | 0.0951 * | 1 | |||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |||||

| usd_eur | 0.6167 * | 0.6318 * | 0.5551 * | 0.6078 * | 0.5391 * | 0.5390 * | 0.5388 * | 0.4339 * | −0.4978 * | 1 | ||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | ||||

| wti_spt | −0.2946 * | −0.3043 * | −0.2948 * | −0.2483 * | −0.2748 * | −0.2750 * | −0.2760 * | −0.2653 * | 0.4104 * | −0.6676 * | 1 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |||

| us_cpi | 0.5742 * | 0.5522 * | 0.5703 * | 0.5450 * | 0.5439 * | 0.5440 * | 0.5446 * | 0.0587 * | −0.1449 * | 0.1221 * | 0.3675 * | 1 |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0007 | 0.0000 | 0.0000 | 0.0000 |

| (1) | (2) | (3) | (4) | |||||

|---|---|---|---|---|---|---|---|---|

| Variable | SP500 | SP500_L5 | DJIA | DJIA_L5 | Nasdaq | Nasdaq_L5 | Russell | Russell_L5 |

| Fed_FRte | 384.9307 *** | 382.3947 *** | 4137.8340 *** | 4119.3300 *** | 1183.6030 *** | 1174.2210 *** | 208.4120 *** | 206.6854 *** |

| us_cpi | 333.8543 *** | 332.7607 *** | 2469.4850 *** | 2462.0310 *** | 1292.0510 *** | 1289.9160 *** | 146.9944 *** | 146.2313 *** |

| _cons | 1327.1010 *** | 1331.8390 *** | 11,913.1100 *** | 11,947.2600 *** | 2642.4890 *** | 2655.5140 *** | 807.1451 *** | 810.3717 *** |

| R-squared | 0.4077 | 0.4068 | 0.4494 | 0.4486 | 0.3657 | 0.3649 | 0.4044 | 0.4034 |

| χ | 2411.66 | 2385.72 | 2903.65 | 2873.31 | 2230.06 | 2210.86 | 2187.3 | 2161.54 |

| p-Value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| t_yield | ||||||||

| Fed_BS | −0.233722 *** | −1.408131 *** | −0.228948 *** | −1.372496 *** | −0.233966 *** | −1.360477 *** | −0.253249 *** | −1.543998 *** |

| L5_BS | - | 1.178981 *** | - | 1.147626 *** | - | 1.130360 *** | - | 1.298019 |

| _cons | 3.261833 *** | 3.25493 *** | 3.241519 *** | 3.236392 *** | 3.262874 *** | 3.258566 *** | 3.344931 *** | 3.327776 *** |

| R-squared | 0.3744 | 0.3897 | 0.3731 | 0.3883 | 0.3745 | 0.3895 | 0.377 | 0.3929 |

| χ | 1778.33 | 1862.02 | 1714.78 | 1800.21 | 1783.27 | 1871.68 | 2060.26 | 2123.75 |

| p-Value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| usd_eur | ||||||||

| t_yield | −0.044983 *** | −0.042221 *** | −0.046512 *** | −0.043667 *** | −0.051962 *** | −0.049034 *** | −0.038969 *** | −0.036551 *** |

| wti_spt | −0.001836 *** | −0.001847 *** | −0.001832 *** | −0.001844 *** | −0.001836 *** | −0.001849 *** | −0.001878 *** | −0.001882 *** |

| _cons | 1.047974 *** | 1.042690 *** | 1.051195 *** | 1.045825 *** | 1.063766 *** | 1.058340 *** | 1.037202 *** | 1.032244 *** |

| R-squared | 0.4767 | 0.4907 | 0.4716 | 0.4865 | 0.4490 | 0.4669 | 0.4918 | 0.5026 |

| χ | 4490.07 | 4345.55 | 4565.02 | 4419.63 | 4910.79 | 4763.24 | 4309.16 | 4164.75 |

| p-Value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Endogenous variables: | SP500 DJIA Nasdaq Russell t_yield usd_eur | |||||||

| Exogenous variables: | Fed_FRte us_cpi L5_BS Fed_BS wti_spt | |||||||

| Panel A: Regressions Results First Intervention (2008–2013) | ||||||||

| Index | SP500 | SP500_L5 | DJIA | DJIA_L5 | Nasdaq | Nasdaq_L5 | Russell | Russell_L5 |

| Variable | (1) | (2) | (3) | (4) | ||||

| Fed_FRte | (omitted) | (omitted) | (omitted) | (omitted) | (omitted) | (omitted) | (omitted) | (omitted) |

| us_cpi | 71.7047 *** | 70.8900 *** | 707.6381 *** | 700.8915 *** | 185.9111 *** | 183.6030 *** | 52.0364 *** | 51.4864 *** |

| _cons | 1159.469 *** | 1161.948 *** | 10,754.628 *** | 10,774.796 *** | 2373.388 *** | 2380.588 *** | 671.684 *** | 673.402 *** |

| p-Value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| t_yield | (5) | (6) | (7) | (8) | ||||

| Fed_BS | −0.7962 *** | 2.2288 *** | −0.7390 *** | 2.3320 *** | −0.7995 *** | 2.2430 *** | −0.8747 *** | 2.0488 *** |

| L5_BS | - | −3.0620 *** | - | −3.1103 *** | - | −3.0796 *** | - | −2.9574 *** |

| _cons | 4.8069 *** | 4.8887 *** | 4.6529 *** | 4.7403 *** | 4.8159 *** | 4.8980 *** | 5.0185 *** | 5.0925 *** |

| p-Value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| usd_eur | (9) | (10) | (11) | (12) | ||||

| t_yield | −0.0308 *** | −0.0339 *** | −0.0311 *** | −0.0342 *** | −0.0304 *** | −0.0334 *** | −0.0303 *** | −0.0332 *** |

| wti_spt | −0.0005 *** | −0.0006 *** | −0.0005 *** | −0.0006 *** | −0.0005 *** | −0.0006 *** | −0.0005 *** | −0.0006 *** |

| _cons | 0.8665 *** | 0.8826 *** | 0.8673 *** | 0.8833 *** | 0.8665 *** | 0.8825 *** | 0.8663 *** | 0.8823 *** |

| p-Value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Panel B: Regressions Results 2nd Intervention (2020–2022) | ||||||||

| Index | SP500 | SP500_L5 | DJIA | DJIA_L5 | Nasdaq | Nasdaq_L5 | Russell | Russell_L5 |

| Variable | (13) | (14) | (15) | (16) | ||||

| Fed_FRte | −899.4386 * | −934.4934 * | −8372.9004 * | −9421.7857 * | −5603.9925 ** | −5440.0177 *** | −1481.5871 *** | −1570.1119 *** |

| us_cpi | 209.6201 *** | 198.2083 *** | 1343.0482 *** | 1263.4306 *** | 682.0166 *** | 631.6812 *** | 94.3413 *** | 89.6114 *** |

| _cons | 3379.689 *** | 3440.396 *** | 28,658.166 *** | 29,297.266 *** | 11,841.987 *** | 12,023.146 *** | 1979.489 *** | 2026.039 *** |

| p-Value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| t_yield | (17) | (18) | (19) | (20) | ||||

| Fed_BS | 0.4025 *** | 1.4701 *** | 0.3935 *** | 1.5285 *** | 0.3993 *** | 1.5056 *** | 0.3774 *** | 1.6158 *** |

| L5_BS | - | −0.9766 *** | - | −1.0390 *** | - | −1.0100 *** | - | −1.1297 *** |

| _cons | −1.8795 *** | −2.6344 *** | −1.8098 *** | −2.6064 *** | −1.8549 *** | −2.6521 *** | −1.6859 *** | −2.5842 *** |

| p-Value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| usd_eur | (21) | (22) | (23) | (24) | ||||

| t_yield | 0.2952 *** | 0.1108 * | 0.2637 *** | 0.0964 * | 0.3541 *** | 0.1165 ** | 0.3205 *** | 0.1128 *** |

| wti_spt | −0.0038 *** | −0.0011 | −0.0032 *** | −0.0008 | −0.0048 *** | −0.0012 | −0.0041 *** | −0.0011 |

| _cons | 0.7107 *** | 0.7838 *** | 0.7175 *** | 0.7862 *** | 0.6925 *** | 0.7836 *** | 0.6966 *** | 0.7802 *** |

| p-Value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Endogenous variables: | SP500 DJIA Nasdaq Russell t_yield usd_eur | |||||||

| Exogenous variables: | Fed_FRte us_cpi L5_BS Fed_BS wti_spt | |||||||

| Intervention | (2008–2022) | (2008–2013) | (2020–2022) | |||

|---|---|---|---|---|---|---|

| Variable | PD3SLS | PD3SLS_L5 | PD3SLS | PD3SLS_L5 | PD3SLS | PD3SLS_L5 |

| Index | ||||||

| Fed_FRte | 1475.3616 *** | 1472.4005 *** | 2469.4850 | 2462.0310 | 1292.0510 | 1289.9160 |

| us_cpi | 1079.7697 *** | 1078.8033 *** | 11,913.1100 | 11,947.2600 | 2642.4890 | 2655.5140 |

| _cons | 4137.7912 *** | 4147.3559 *** | 0.4494 | 0.4486 | 0.3657 | 0.3649 |

| t_yield | ||||||

| Fed_BS | −0.27328 *** | −1.29542 *** | −0.68698 *** | 2.34144 *** | 0.38780 *** | 1.11081 *** |

| 5L_BS | - | 1.02347 *** | - | −3.05222 *** | - | −0.68834 *** |

| idcode | ||||||

| 1923 | −0.06365 *** | −0.06212 *** | 0.01690 | 0.01667 | −0.00552 | −0.00249 |

| 1971 | −0.05000 *** | −0.04878 ** | 0.01468 | 0.01448 | −0.00372 | −0.00168 |

| 1984 | −0.06735 *** | −0.06573 *** | 0.01773 | 0.01749 | −0.00592 | −0.00267 |

| _cons | 3.47543 *** | 3.47138 *** | 4.50041 *** | 4.55814 *** | −1.76234 *** | −2.04237 *** |

| usd_eur | ||||||

| t_yield | −0.04424 *** | −0.04365 *** | −0.03336 *** | −0.03548 *** | 0.54657 *** | 0.30718 *** |

| wti_spt | −0.00188 *** | −0.00188 *** | −0.00041 *** | −0.00049 *** | −0.00797 *** | −0.00436 *** |

| idcode | ||||||

| 1923 | −0.00130 | −0.00124 | 0.00085 | 0.00081 | −0.00379 | −0.00415 |

| 1971 | −0.00102 | −0.00097 | 0.00074 | 0.00070 | −0.00255 | −0.00279 |

| 1984 | −0.00137 | −0.00131 | 0.00089 | 0.00085 | −0.00406 | −0.00444 |

| _cons | 1.05060 *** | 1.04929 *** | 0.86797 *** | 0.88047 *** | 0.63617 *** | 0.72941 *** |

| note: Fed_FRte omitted because of collinearity | legend: * p < 0.05; ** p < 0.01; *** p < 0.001 | |||||

| idcodes: 1896 = DJIA, 1923 = SP500, 1971 = Nasdaq, 1984 = Russell | ||||||

| Endogenous variables: | 1896 1923 1971 1984 t_yield usd_eur | |||||

| Exogenous variables: | Fed_FRte us_cpi L5_BS Fed_BS wti_spt | |||||

| Underidentification test | Sargan statistic | |||||||

| (Anderson canon. corr. LM statistic): | (overidentification test of all instruments): | |||||||

| Ho: underidentification of instrumental variables | Ho: underidentification of instrumental variables | |||||||

| Intervention Period: (2008–2013) | ||||||||

| Panel2SLS | 2100.473 | Chi-sq(6) p-value | = | 0.0000 | 4852.170 | Chi-sq(5) p-value | = | 0.0000 |

| Panel2SLS_L5 | 1236.610 | Chi-sq(7) p-value | = | 0.0000 | 2825.749 | Chi-sq(6) p-value | = | 0.0000 |

| Intervention Period: (2020–2022) | ||||||||

| Panel2SLS | 908.122 | Chi-sq(6) p-value | = | 0.0000 | 2010.235 | Chi-sq(5) p-value | = | 0.0000 |

| Panel2SLS_L5 | 521.401 | Chi-sq(7) p-value | = | 0.0000 | 1176.060 | Chi-sq(6) p-value | = | 0.0000 |

| Intervention Period: (2008–2022) | ||||||||

| Panel2SLS | 6347.892 | Chi-sq(6) p-value | = | 0.0000 | 11,000.000 | Chi-sq(5) p-value | = | 0.0000 |

| Panel2SLS_L5 | 3727.789 | Chi-sq(7) p-value | = | 0.0000 | 6307.683 | Chi-sq(6) p-value | = | 0.0000 |

| Weak Identification Test (Cragg–Donald Wald F Statistic): | ||||||

|---|---|---|---|---|---|---|

| Panel2SLS | Panel2SLS_L5 | |||||

| 2008–2013 | 596.264 | 302.789 | ||||

| 2020–2022 | 270.322 | 130.619 | ||||

| 2008–2022 | 2000.412 | 1013.536 | ||||

| Stock–Yogo weak ID test critical values: | ||||||

| 5% maximal IV relative | 19.28 | 5% maximal IV relative | 19.86 | |||

| 10% maximal IV relative | 11.12 | 10% maximal IV relative | 11.29 | |||

| 20% maximal IV relative | 6.76 | 20% maximal IV relative | 6.73 | |||

| 30% maximal IV relative | 5.15 | 30% maximal IV relative | 5.07 | |||

| 10% maximal IV size | 29.18 | 10% maximal IV size | 31.5 | |||

| 15% maximal IV size | 16.23 | 15% maximal IV size | 17.38 | |||

| 20% maximal IV size | 11.72 | 20% maximal IV size | 12.48 | |||

| 25% maximal IV size | 9.38 | 25% maximal IV size | 9.93 | |||

| Montiel–Pflueger robust weak instrument test | ||||||

| Critical Values: | TSLS | LIML | Critical Values: | TSLS | LIML | |

| % of Worst Case Bias | % of Worst Case Bias | |||||

| tau = 5% | 19.595 | 7.209 | tau = 5% | 20.297 | 6.346 | |

| tau = 10% | 11.520 | 4.874 | tau = 10% | 11.804 | 4.352 | |

| tau = 20% | 7.209 | 3.595 | tau = 20% | 7.294 | 3.264 | |

| tau = 30% | 5.673 | 3.134 | tau = 30% | 5.695 | 2.874 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rincon, C.J. Equity Market Pricing and Central Bank Interventions: A Panel Data Approach. J. Risk Financial Manag. 2024, 17, 440. https://doi.org/10.3390/jrfm17100440

Rincon CJ. Equity Market Pricing and Central Bank Interventions: A Panel Data Approach. Journal of Risk and Financial Management. 2024; 17(10):440. https://doi.org/10.3390/jrfm17100440

Chicago/Turabian StyleRincon, Carlos J. 2024. "Equity Market Pricing and Central Bank Interventions: A Panel Data Approach" Journal of Risk and Financial Management 17, no. 10: 440. https://doi.org/10.3390/jrfm17100440

APA StyleRincon, C. J. (2024). Equity Market Pricing and Central Bank Interventions: A Panel Data Approach. Journal of Risk and Financial Management, 17(10), 440. https://doi.org/10.3390/jrfm17100440