Macroeconomic Dynamics in the Greek Economy during the Pre- and Post-Euro Adoption Periods

Abstract

1. Introduction

2. Literature Review

3. Methodology

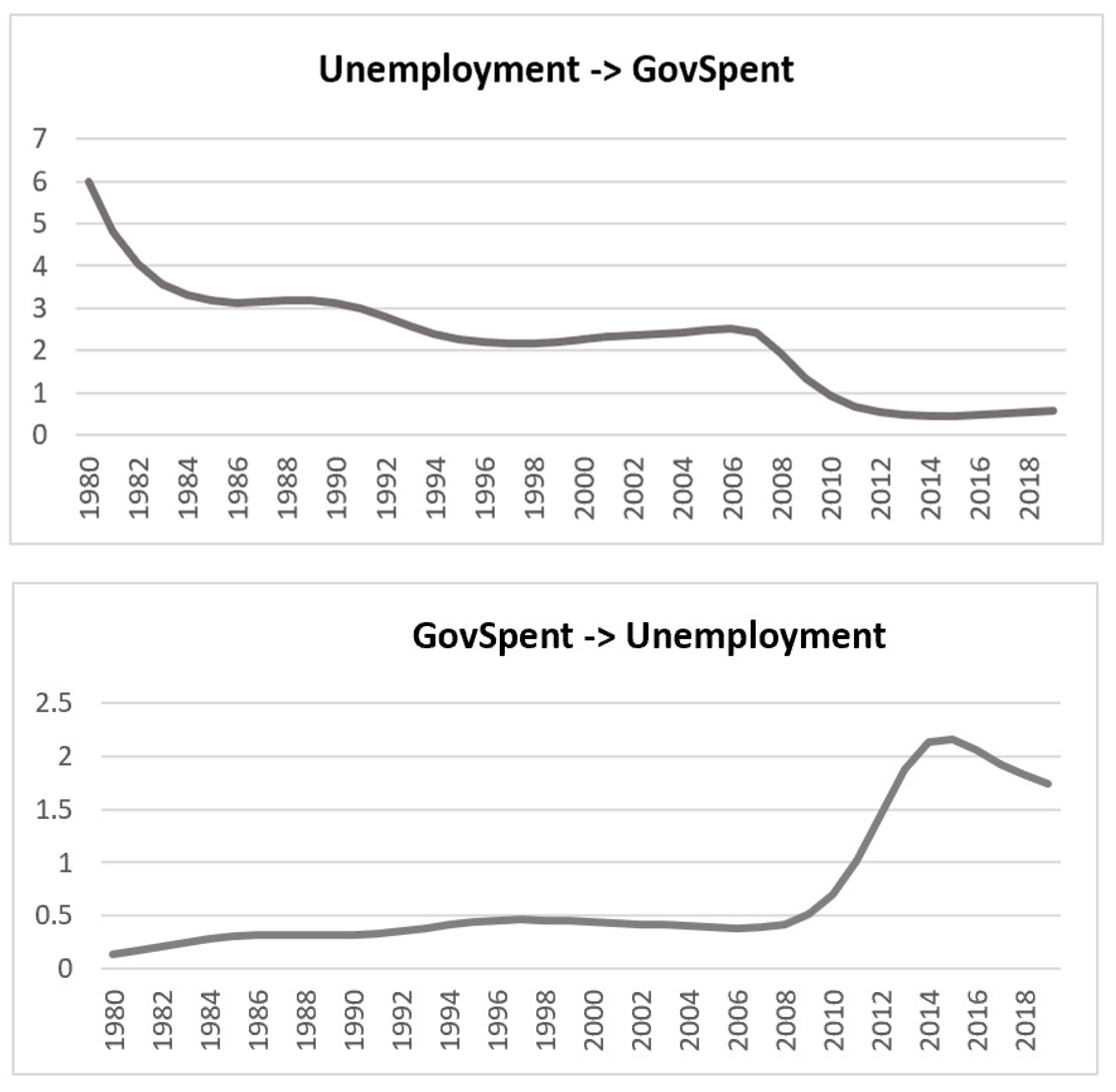

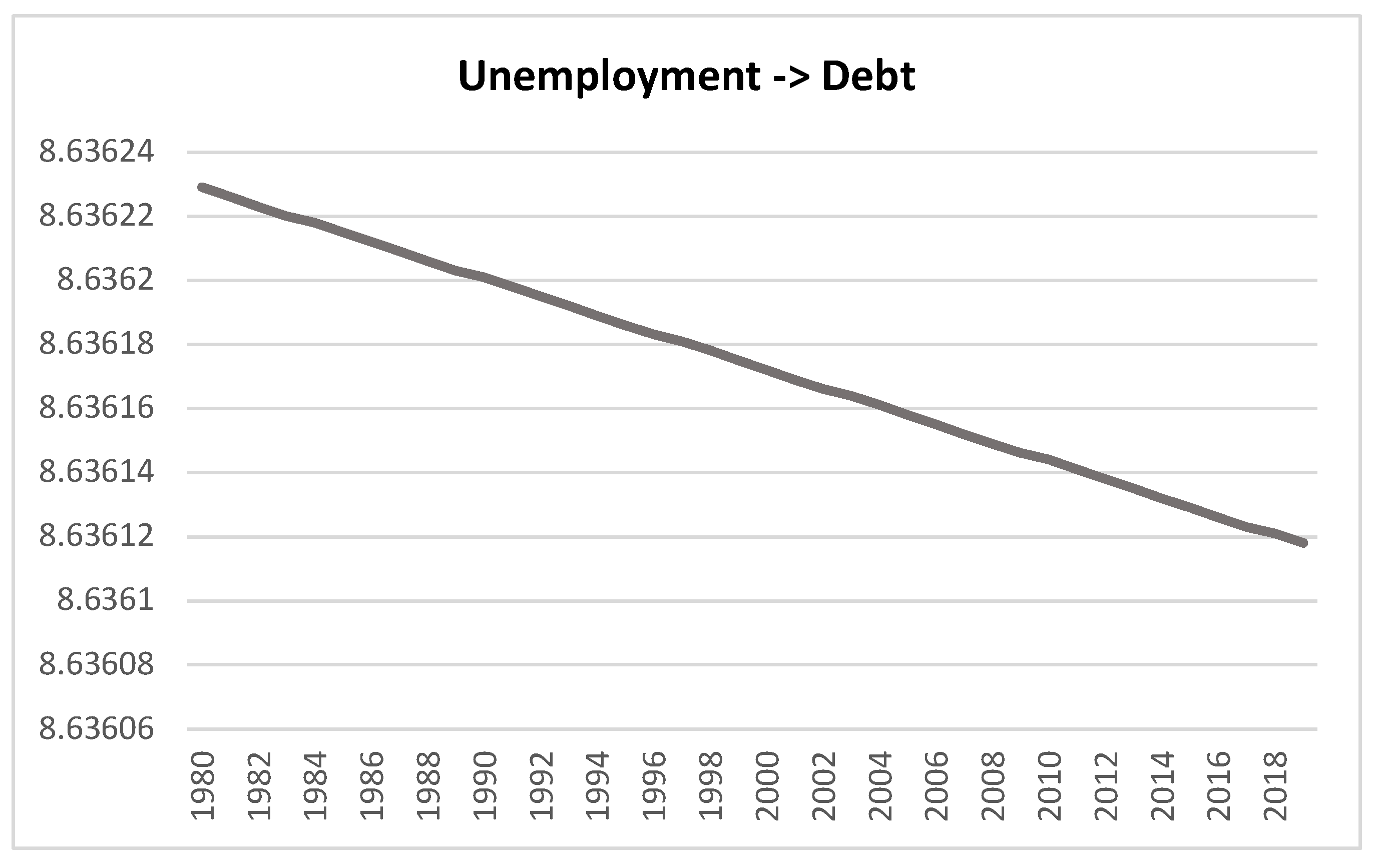

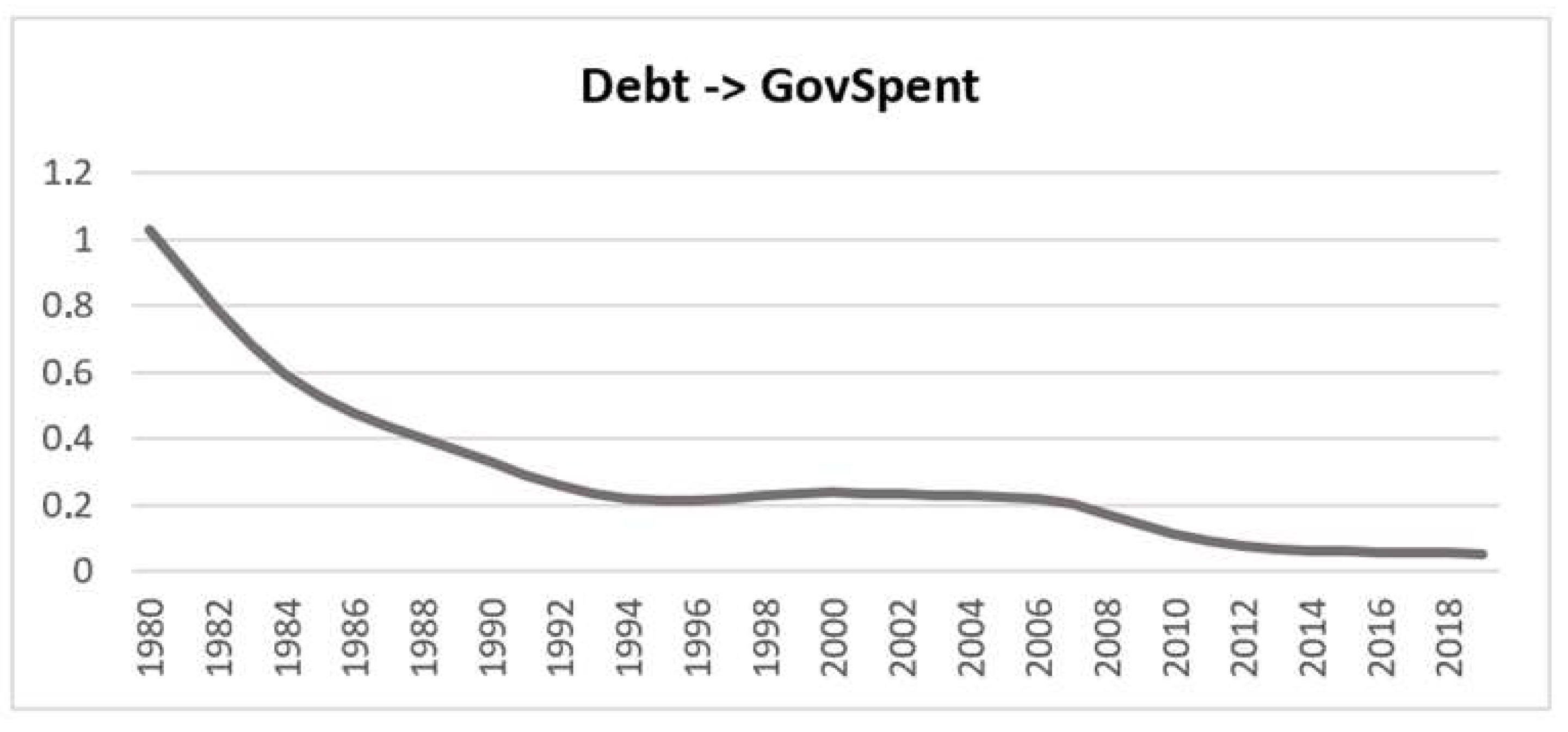

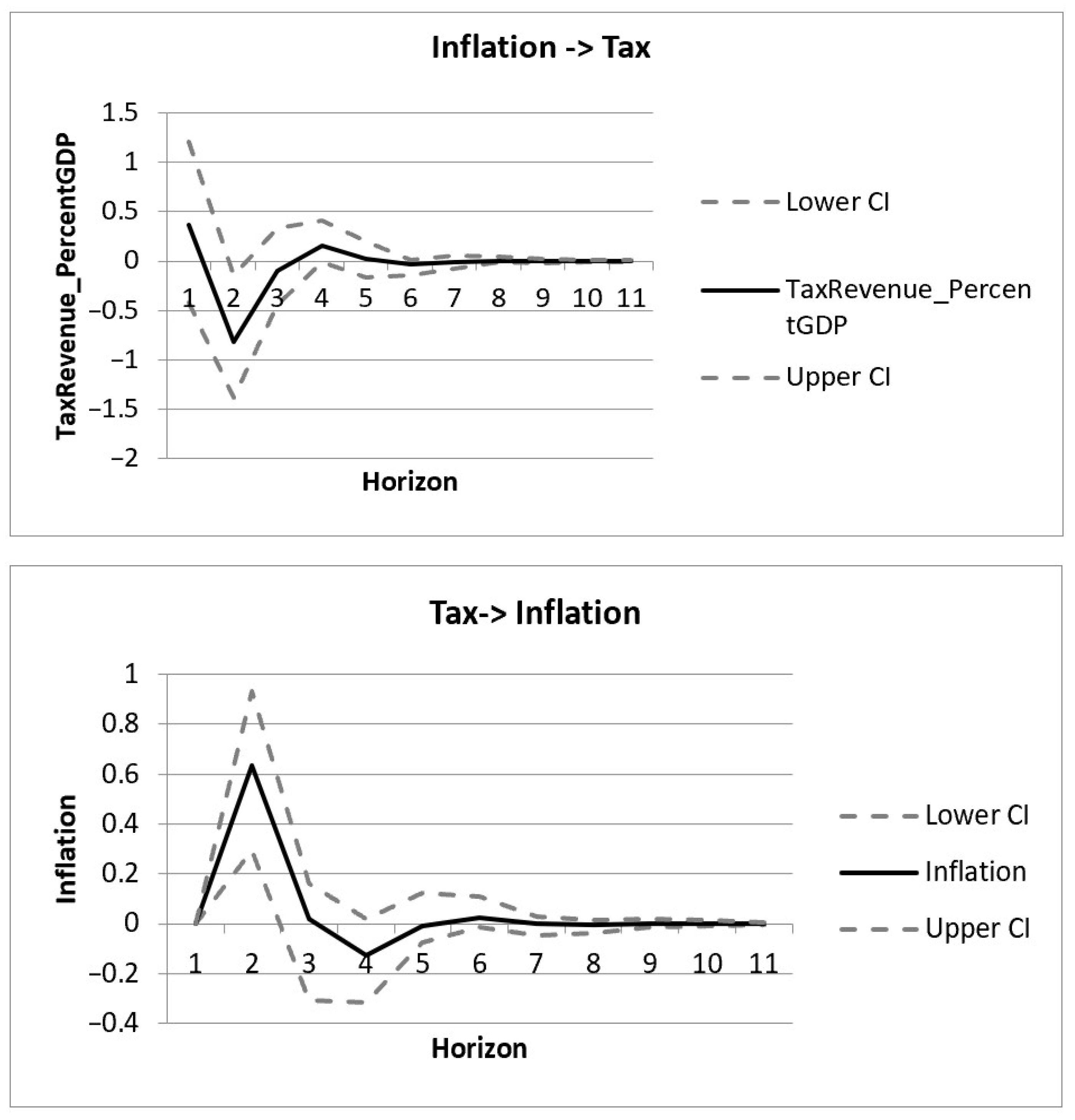

4. Empirical Analysis

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

Appendix B

| Date | GDP | GovSpent_PercentGDP | Unemployment | TaxRevenue_PercentGDP | Inflation | Debt_PercentGDP |

| 1980 | 56.83 | 31 | 2.7 | 13.8 | 24.68 | 22.53 |

| 1981 | 52.35 | 28 | 3.4 | 12.3 | 24.51 | 26.68 |

| 1982 | 54.62 | 25 | 4.9 | 14.9 | 20.99 | 29.31 |

| 1983 | 49.43 | 27 | 7.8 | 15.6 | 20.18 | 33.59 |

| 1984 | 48.02 | 22 | 8.1 | 14 | 18.46 | 40.06 |

| 1985 | 47.82 | 24 | 7.8 | 13.8 | 19.31 | 46.62 |

| 1986 | 56.38 | 25 | 7.4 | 15.6 | 23.02 | 47.14 |

| 1987 | 65.65 | 23 | 7.3 | 16.4 | 16.4 | 52.41 |

| 1988 | 76.26 | 23 | 7.7 | 15.1 | 13.53 | 57.07 |

| 1989 | 79.17 | 24 | 7.5 | 13 | 13.66 | 59.82 |

| 1990 | 97.89 | 25 | 7 | 15.1 | 20.43 | 73.15 |

| 1991 | 105.14 | 24 | 7.7 | 20.1 | 19.46 | 74.68 |

| 1992 | 116.22 | 23 | 7.8 | 20.1 | 15.88 | 79.97 |

| 1993 | 108.81 | 22 | 8.6 | 20.1 | 14.41 | 100.29 |

| 1994 | 116.60 | 20 | 8.9 | 20.1 | 10.87 | 98.3 |

| 1995 | 136.88 | 20 | 9.1 | 18.6 | 8.93 | 98.99 |

| 1996 | 145.86 | 21 | 9.6 | 18.6 | 8.19 | 101.34 |

| 1997 | 143.16 | 20 | 9.6 | 19.5 | 5.54 | 99.45 |

| 1998 | 144.43 | 24 | 10.8 | 20.5 | 4.77 | 97.42 |

| 1999 | 142.59 | 25 | 11.9 | 21.4 | 2.64 | 98.91 |

| 2000 | 130.46 | 25 | 11.2 | 22.5 | 3.15 | 104.93 |

| 2001 | 136.31 | 25 | 10.5 | 20.9 | 3.37 | 107.08 |

| 2002 | 154.56 | 24 | 10 | 21.3 | 3.63 | 104.86 |

| 2003 | 202.37 | 25 | 9.4 | 19.7 | 3.53 | 101.46 |

| 2004 | 240.96 | 24 | 10.3 | 19.1 | 2.9 | 102.87 |

| 2005 | 247.88 | 21 | 10 | 20.3 | 3.55 | 107.39 |

| 2006 | 273.55 | 24 | 9 | 20 | 3.2 | 103.57 |

| 2007 | 318.90 | 26 | 8.4 | 20.2 | 2.9 | 103.1 |

| 2008 | 355.91 | 24 | 7.8 | 20.2 | 4.15 | 109.42 |

| 2009 | 331.31 | 21 | 9.6 | 19.8 | 1.21 | 126.74 |

| 2010 | 297.12 | 17 | 12.7 | 20.4 | 4.71 | 146.25 |

| 2011 | 283.00 | 14 | 17.9 | 22.5 | 3.33 | 172.1 |

| 2012 | 242.03 | 12 | 24.4 | 24.3 | 1.5 | 159.56 |

| 2013 | 238.91 | 11 | 27.5 | 24.1 | −0.92 | 177.68 |

| 2014 | 235.46 | 11 | 26.5 | 24.9 | −1.31 | 180.06 |

| 2015 | 195.68 | 11 | 24.9 | 24.9 | −1.74 | 176.94 |

| 2016 | 193.15 | 11 | 23.5 | 26.7 | −0.83 | 194.62 |

| 2017 | 199.84 | 12 | 21.5 | 26.5 | 1.12 | 198.97 |

| 2018 | 212.05 | 11 | 19.3 | 26.9 | 0.63 | 208.84 |

| 2019 | 205.14 | 11 | 17.3 | 26.2 | 0.25 | 212.38 |

| 1 | Unemployment: 1980: https://www.imf.org/en/Countries/GRC (accessed on 10 October 2023), 1981–2019: https://data.worldbank.org/indicator/SL.UEM.TOTL.NE.ZS?locations=GR (accessed on 10 October 2023), Gross Fixed Capital Formation: https://data.worldbank.org/indicator/NE.GDI.FTOT.ZS?locations=GR (accessed on 10 October 2023), Tax: https://data.worldbank.org/indicator/GC.TAX.TOTL.GD.ZS?locations=GR (accessed on 11 October 2023), Inflation: https://www.macrotrends.net/countries/GRC/greece/inflation-rate-cpi (accessed on 11 October 2023), Debt: 2016–2019: https://www.macrotrends.net/countries/GRC/greece/debt-to-gdp-ratio (accessed on 11 October 2023), 1960–2015: https://www.imf.org/external/datamapper/DEBT1@DEBT/GRC?zoom=GRC&highlight=GRC (accessed on 12–14 October 2023). |

References

- Albani, Maria, and Yannis Stournaras. 2009. A Model to Deal with Aggregate Supply and Demand Imbalances: The Case of Greece. The Journal of Economic Asymmetries 6: 15–28. [Google Scholar] [CrossRef]

- Alikaj, Mirsida, and Yiorgos Alexopoulos. 2014. Analysis of the Economy of Region of Western Greece. An Application of the Social Accounting Matrix (SAM). Procedia Economics and Finance 14: 3–12. [Google Scholar] [CrossRef][Green Version]

- Alogoskoufis, George S. 1985. Macroeconomic policy and aggregate fluctuations in a semi-industrialized open economy. European Economic Review 29: 35–61. [Google Scholar] [CrossRef]

- Angelopoulos, Angelos, George Economides, George Liontos, Apostolis Philippopoulos, and Stelios Sakkas. 2022. Public redistributive policies in general equilibrium: An application to Greece. The Journal of Economic Asymmetries 26: e00271. [Google Scholar] [CrossRef]

- Antoniadis, Ioannis, A. Alexandridis, and Nikolaos Sariannidis. 2014. Mergers and Acquisitions in the Greek Banking Sector: An Event Study of a Proposal. Procedia Economics and Finance 14: 13–22. [Google Scholar] [CrossRef]

- Baltas, Nicholas C. 2013. The Greek financial crisis and the outlook of the Greek economy. The Journal of Economic Asymmetries 10: 32–37. [Google Scholar] [CrossRef]

- Beshenov, Sergey, and Ivan Rozmainsky. 2015. Hyman Minsky’s financial instability hypothesis and the Greek debt crisis. Russian Journal of Economics 1: 419–38. [Google Scholar] [CrossRef][Green Version]

- Bitros, George C., Bala Batavia, and Parameswar Nandakumar. 2016. Economic crisis in the European periphery: An assessment of EMU membership and home policy effects based on the Greek experience. The North American Journal of Economics and Finance 36: 312–27. [Google Scholar] [CrossRef][Green Version]

- Bitzenis, Aristidis, and Ioannis Makedos. 2014. The Absorption of a Shadow Economy in the Greek GDP. Procedia Economics and Finance 9: 32–41. [Google Scholar] [CrossRef][Green Version]

- Caloghirou, Yannis D., Alexi G. Mourelatos, and Tompson Henry. 1997. Industrial energy substitution during the 1980s in the Greek economy. Energy Economics 19: 476–91. [Google Scholar] [CrossRef]

- Christodoulakis, Nicos M., and Sarantis Kalyvitis. 2000. The Effects of the Second Community Support Framework 1994–99 on the Greek Economy. Journal of Policy Modeling 22: 611–24. [Google Scholar] [CrossRef]

- Christopoulos, Dimitris K. 2003. Does underground economy respond symmetrically to tax changes? Evidence from Greece. Economic Modelling 20: 563–70. [Google Scholar] [CrossRef]

- Daglis, Theodoros. 2022. The excessive gaming and gambling during COVID-19. Journal of Economic Studies 49: 888–901. [Google Scholar] [CrossRef]

- Daglis, Theodoros. 2023a. An investigation of the impact of COVID-19 on health-related cryptocurrencies using time-varying parameters and impulse responses. Healthcare Analytics 4: 100226. [Google Scholar] [CrossRef]

- Daglis, Theodoros. 2023b. The dynamic relationship of cryptocurrencies with supply chain and logistics stocks—The impact of COVID-19. Journal of Economic Studies 50: 840–57. [Google Scholar] [CrossRef]

- Daglis, Theodoros. 2023c. The Tourism Industry’s Performance During the Years of the COVID-19 Pandemic. Computational Economics. [Google Scholar] [CrossRef]

- Daglis, Theodoros, and Maria-Anna Katsikogianni. 2022. The Repercussions of Covid-19 on the Stock Market of the Tourism Industry. Tourism Analysis 27: 77–91. [Google Scholar] [CrossRef]

- Daniel, Betty C., and Jinwook Nam. 2022. The Greek debt crisis: Excusable vs. strategic default. Journal of International Economics 138: 103632. [Google Scholar] [CrossRef]

- Dimakopoulou, Vasiliki, George Economides, and Apostolis Philippopoulos. 2022. The ECB’s policy, the Recovery Fund and the importance of trust and fiscal corrections: The case of Greece. Economic Modelling 112: 105846. [Google Scholar] [CrossRef]

- Fasianos, Apostolos, and Panos Tsoukalis. 2023. Decomposing wealth inequalities in the wake of the Greek debt crisis. The Journal of Economic Asymmetries 28: e00307. [Google Scholar] [CrossRef]

- Germaschewski, Yin, and Shu-Ling Wang. 2022. Fiscal stabilization in high-debt economies without monetary independence. Journal of Macroeconomics 72: 103398. [Google Scholar] [CrossRef]

- Gogos, Stylianos G., Nikolaos Mylonidis, Dimitris Papageorgiou, and Vanghelis Vassilatos. 2014. 1979–2001: A Greek great depression through the lens of neoclassical growth theory. Economic Modelling 36: 316–31. [Google Scholar] [CrossRef]

- Goodhart, Charles, Udara Peiris, and Dimitrios Tsomocos. 2018. Debt, recovery rates and the Greek dilemma. Journal of Financial Stability 36: 265–78. [Google Scholar] [CrossRef]

- Hatgioannides, John, Marika Karanassou, Hector Sala, Menelaos G. Karanasos, and Panagiotis D. Koutroumpis. 2018. The legacy of a fractured Eurozone: The Greek Dra(ch)ma. Geoforum 93: 11–21. [Google Scholar] [CrossRef]

- Kammas, Pantelis, and Vassilis Sarantides. 2020. Democratisation and tax structure in the presence of home production: Evidence from the Kingdom of Greece. Journal of Economic Behavior & Organization 177: 219–36. [Google Scholar] [CrossRef]

- Kapitsinis, Nikos. 2018. Interpreting business mobility through socio-economic differentiation. Greek firm relocation to Bulgaria before and after the 2007 global economic crisis. Geoforum 96: 119–28. [Google Scholar] [CrossRef]

- Karafolas, Simeon, and G. Mantakas. 1996. A note on cost structure and economies of scale in Greek banking. Journal of Banking & Finance 20: 377–87. [Google Scholar] [CrossRef]

- Karfakis, Costas. 2013. Credit and business cycles in Greece: Is there any relationship? Economic Modelling 32: 23–29. [Google Scholar] [CrossRef][Green Version]

- Kasimati, Evangelia, and Peter Dawson. 2009. Assessing the impact of the 2004 Olympic Games on the Greek economy: A small macroeconometric model. Economic Modelling 26: 139–46. [Google Scholar] [CrossRef]

- Katsimi, Margarita, and Thomas Moutos. 2010. EMU and the Greek crisis: The political-economy perspective. European Journal of Political Economy 26: 568–76. [Google Scholar] [CrossRef]

- Konstantakis, Konstantinos N., Panayotis G. Michaelides, and Angelos T. Vouldis. 2016. Non performing loans (NPLs) in a crisis economy: Long-run equilibrium analysis with a real time VEC model for Greece (2001–2015). Physica A: Statistical Mechanics and Its Applications 451: 149–61. [Google Scholar] [CrossRef]

- Kottis, Athena Petraki. 1990. Shifts over time and regional variation in women’s labor force participation rates in a developing economy: The case of Greece. Journal of Development Economics 33: 117–32. [Google Scholar] [CrossRef]

- Kyrkilis, Dimitrios, and Semasis Simeon. 2015. Greek Agriculture’s Failure. The Other Face of a Failed Industrialization. From Accession to EU to the Debt Crisis. Procedia Economics and Finance 33: 64–77. [Google Scholar] [CrossRef]

- Laopodis, Nikiforos T., Anna A. Merika, and Merika Annie Triantafillou. 2016. Unraveling the political budget cycle nexus in Greece. Research in International Business and Finance 36: 13–27. [Google Scholar] [CrossRef]

- Mavridakis, Theofanis, Dimitrios Dovas, and Spiridoula Bravou. 2015a. The Effectiveness of the Adjustment Policies Applied to the Greek Economy. Procedia Economics and Finance 19: 101–9. [Google Scholar] [CrossRef][Green Version]

- Mavridakis, Theofanis, Dimitrios Dovas, and Spiridoula Bravou. 2015b. The Results of the Adjustment Program for the Greek Economy. Procedia Economics and Finance 33: 154–67. [Google Scholar] [CrossRef][Green Version]

- Mensi, Walid, Ur Rehman Mobeen, Shawkat Hammoudeh, Xuan Vingh Vo, and Won Joong Kim. 2023. How macroeconomic factors drive the linkages between inflation and oil markets in global economies? A multiscale analysis. International Economics 173: 212–32. [Google Scholar] [CrossRef]

- Michaelides, Panayotis G., Theofanis Papageorgiou, and Angelos T. Vouldis. 2013. Business cycles and economic crisis in Greece (1960–2011): A long run equilibrium analysis in the Eurozone. Economic Modelling 31: 804–16. [Google Scholar] [CrossRef]

- Missos, Vlassis, Charalampos Domenikos, and Nikos Pontis. 2024. Hardening the EU core-periphery lines, 2009–2019: Dependency, neoliberalism, welfare reformation and poverty in Greece. Structural Change and Economic Dynamics 69: 171–82. [Google Scholar] [CrossRef]

- Önder, Yasin Kürsat, and Enet Sunel. 2021. Inflation-default trade-off without a nominal anchor: The case of Greece. Review of Economic Dynamics 39: 55–78. [Google Scholar] [CrossRef]

- Ozturk, Serdar, and Ali Sozdemir. 2015. Effects of Global Financial Crisis on Greece Economy. Procedia Economics and Finance 23: 568–75. [Google Scholar] [CrossRef]

- Papadimitriou, Dimitri. 1990. The political economy of Greece. European Journal of Political Economy 6: 181–99. [Google Scholar] [CrossRef]

- Papageorgiou, Dimitris. 2012. Fiscal policy reforms in general equilibrium: The case of Greece. Journal of Macroeconomics 34: 504–22. [Google Scholar] [CrossRef]

- Papatheodorou, Yorgos E. 1990. Energy in the Greek economy. Energy Economics 12: 269–78. [Google Scholar] [CrossRef]

- Papatheodorou, Yorgos E. 1991. Production structure and cyclical behaviour. European Economic Review 35: 1449–71. [Google Scholar] [CrossRef]

- Pappas, Anastasios P. 2010. Capital Mobility and Macroeconomic Volatility: Evidence from Greece. The Journal of Economic Asymmetries 7: 101–21. [Google Scholar] [CrossRef]

- Passas, Costas. 2023. Standardized capital stock estimates for the Greek economy 1948–2020. Structural Change and Economic Dynamics 64: 236–44. [Google Scholar] [CrossRef]

- Provopoulos, George A. 2014. The Greek Economy and Banking System: Recent Developments and the Way Forward. Journal of Macroeconomics 39: 240–49. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, and Ioannis Tsakalos. 2013. How can a small country affect the European economy? The Greek contagion phenomenon. Journal of International Financial Markets, Institutions and Money 25: 18–32. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, and Stathis Polyzos. 2016. Freeing Greece from capital controls: Were the restrictions enforced in time? Research in International Business and Finance 37: 196–213. [Google Scholar] [CrossRef]

- Stamopoulos, Dimitrios, Petros Dimas, and Aggelos Tsakanikas. 2022. Exploring the structural effects of the ICT sector in the Greek economy: A quantitative approach based on input-output and network analysis. Telecommunications Policy 46: 102332. [Google Scholar] [CrossRef]

- Trigkas, Mariw, Glykeria Karagouni, K. Mpyrou, and Ioannis Papadopoulos. 2020. Circular economy. The Greek industry leaders’ way towards a transformational shift. Resources, Conservation and Recycling 163: 105092. [Google Scholar] [CrossRef]

- Tserkezos, Dikaios E. 1991. A distributed lag model for quarterly dlsaggregatmn of the annual personal disposable income of the Greek economy. Economic Modelling 8: 528–36. [Google Scholar] [CrossRef]

- Vinci, Sabato, Fransesca Bartolacci, Rosanna Salvia, and Luca Salvati. 2022. Housing markets, the great crisis, and metropolitan gradients: Insights from Greece, 2000–2014. Socio-Economic Planning Sciences 80: 101171. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Descriptive Statistics | GovSpent | Unemployment | Tax | Inflation | Debt |

|---|---|---|---|---|---|

| Average | 20.90 | 11.68 | 19.14 | 8.60 | 105.91 |

| Standard Error | 0.89 | 1.02 | 0.69 | 1.32 | 8.38 |

| Median | 23.00 | 9.50 | 19.75 | 4.43 | 101.40 |

| Kurtosis | −0.56 | 0.56 | −1.08 | −1.11 | −0.58 |

| Skewness | −0.77 | 1.26 | 0.18 | 0.62 | 0.43 |

| Min | 11.00 | 2.70 | 12.30 | −1.74 | 22.53 |

| Max | 31.00 | 27.50 | 26.90 | 24.68 | 212.38 |

| Variable | DF | p-Value |

|---|---|---|

| GovSpent_PercentGDP | −2.012 | 0.569 |

| Unemployment | −2.149 | 0.515 |

| TaxRevenue_PercentGDP | −2.770 | 0.271 |

| Inflation | −2.087 | 0.539 |

| Debt_PercentGDP | −1.464 | 0.784 |

| Dependent Variable | Independent Variables_Names | F-Stat | p-Value | Lag |

|---|---|---|---|---|

| GovSpent | Unemployment | 4.405 | 0.043 | 1 |

| Unemployment | GovSpent | 3.871 | 0.057 | 1 |

| Tax | Unemployment | 0.055 | 0.815 | 1 |

| Unemployment | Tax | 0.292 | 0.592 | 1 |

| Inflation | Unemployment | 0.700 | 0.408 | 1 |

| Unemployment | Inflation | 1.624 | 0.211 | 1 |

| Debt | Unemployment | 2.267 | 0.141 | 1 |

| Unemployment | Debt | 0.617 | 0.437 | 1 |

| Debt | Unemployment | 2.601 | 0.090 | 2 |

| Debt | GovSpent | 3.105 | 0.087 | 1 |

| GovSpent | Debt | 1.837 | 0.184 | 1 |

| Inflation | GovSpent | 1.800 | 0.188 | 1 |

| GovSpent | Inflation | 0.612 | 0.439 | 1 |

| Tax | GovSpent | 0.011 | 0.918 | 1 |

| GovSpent | Tax | 0.069 | 0.795 | 1 |

| Tax | Debt | 0.240 | 0.627 | 1 |

| Debt | Tax | 2.294 | 0.139 | 1 |

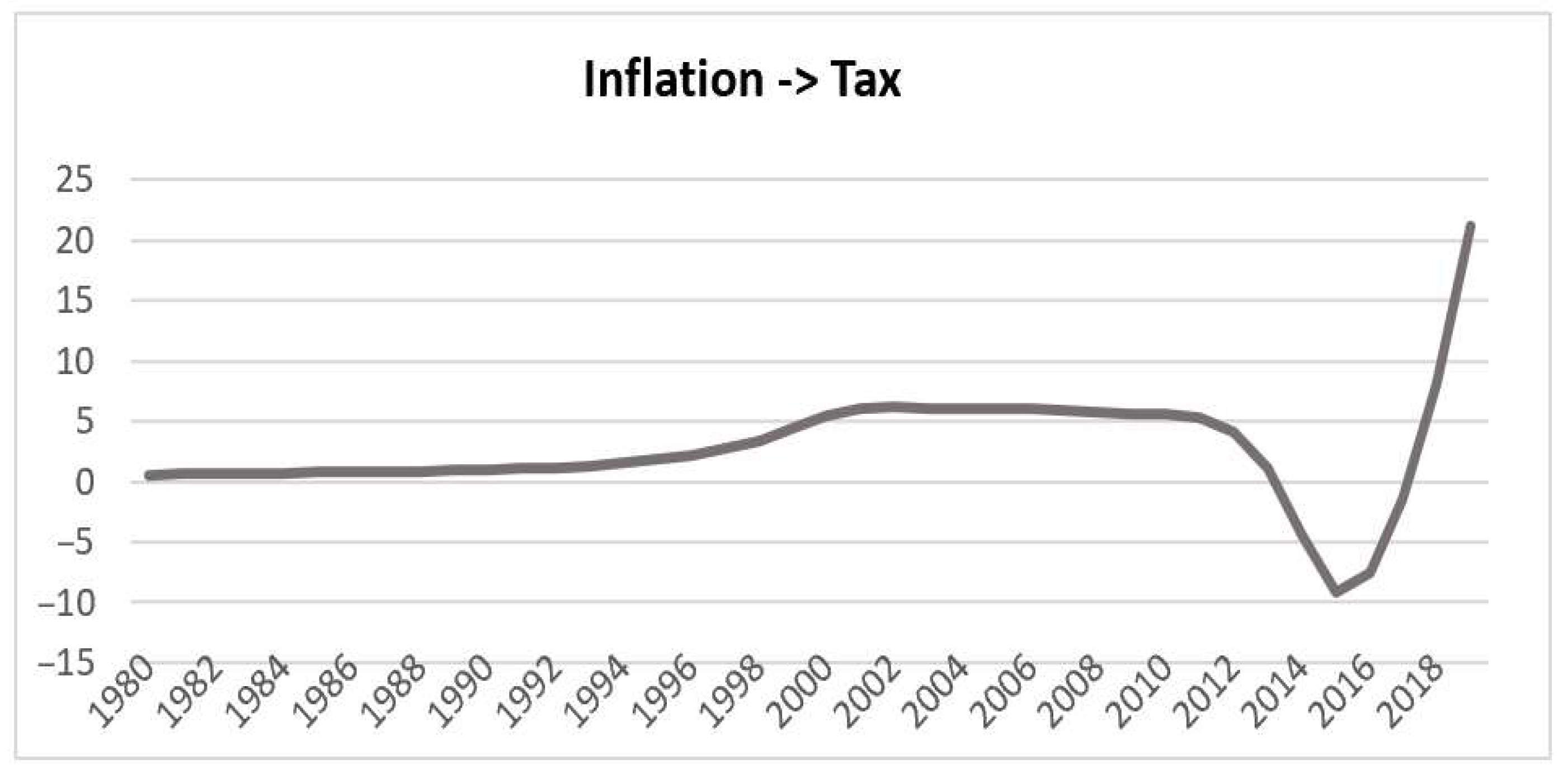

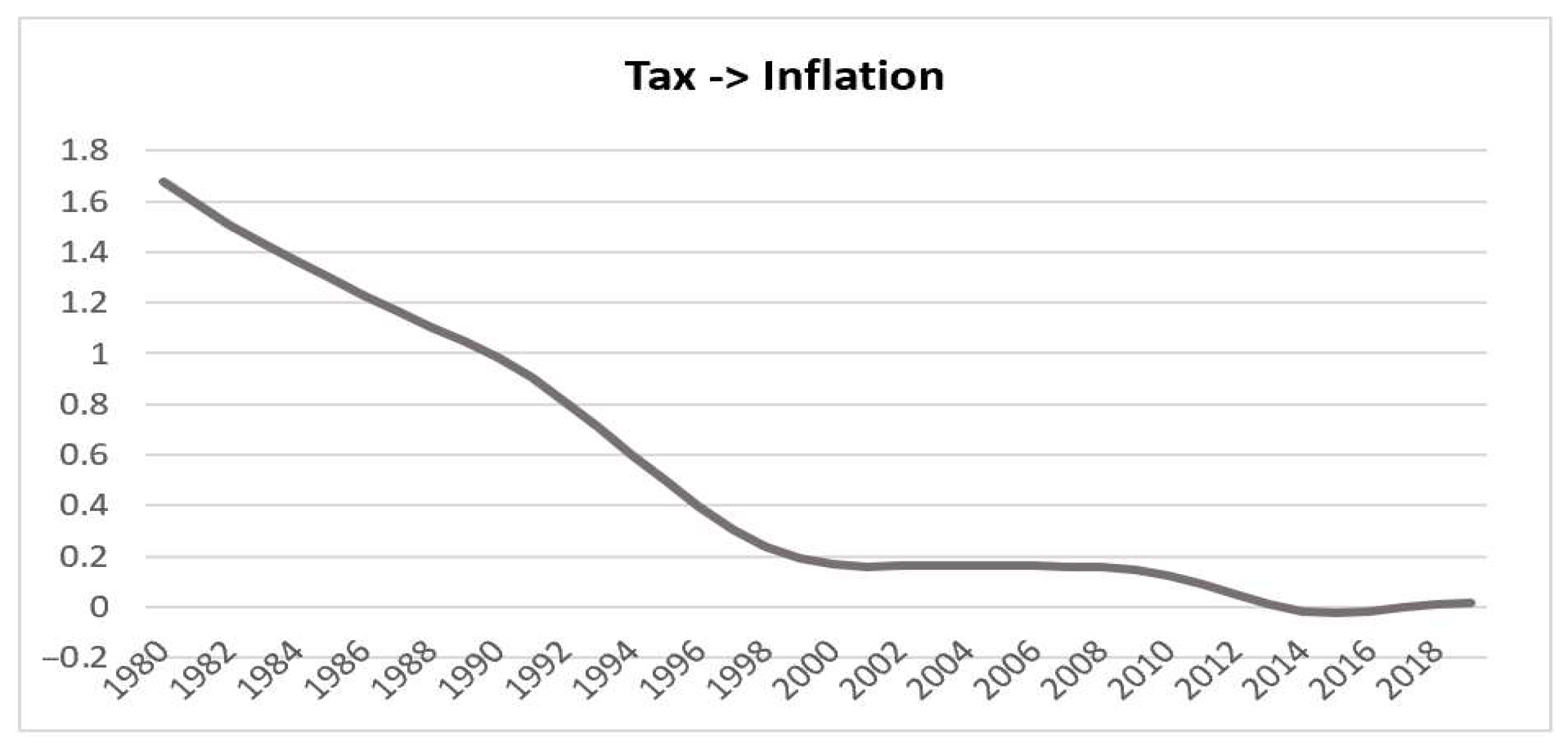

| Tax | Inflation | 6.842 | 0.013 | 1 |

| Inflation | Tax | 11.409 | 0.002 | 1 |

| Couples | Parameter | Corr | p-Value |

|---|---|---|---|

| GovSpent, Unemployment | Whole | −0.690 | 0.000 |

| Pre-Euro | −0.390 | 0.070 | |

| Euro | −0.880 | 0.000 |

| Couples | Parameter | Corr | p-Value |

|---|---|---|---|

| Debt, Unemployment | Whole | 0.872 | 0.000 |

| Pre-Euro | 0.810 | 0.000 | |

| Euro | 0.723 | 0.001 |

| Variable | Estimate | Std. Error | t-Value | Pr(>|t|) |

|---|---|---|---|---|

| (Intercept) | 4.469 | 2.129 | 2.100 | 0.046 |

| Debt(−1) | −0.090 | 0.210 | −0.427 | 0.673 |

| Debt(−1) | 0.057 | 0.203 | 0.279 | 0.782 |

| Unemployment | 1.368 | 1.541 | 0.887 | 0.383 |

| Unemployment(−1) | −0.415 | 2.148 | −0.193 | 0.848 |

| Unemployment(−2) | 1.568 | 2.144 | 0.732 | 0.471 |

| Unemployment(−3) | −3.506 | 2.007 | −1.746 | 0.093 |

| Unemployment(−4) | 2.367 | 1.994 | 1.187 | 0.246 |

| Unemployment(−5) | 0.169 | 1.520 | 0.111 | 0.912 |

| Couples | Parameter | Rho | S | p-Value |

|---|---|---|---|---|

| Debt, GovSpent | Whole | −0.702 | 18,146.000 | 0.000 |

| Pre-Euro | −0.471 | 2604.800 | 0.027 | |

| Euro | −0.923 | 1862.900 | 0.000 |

| Variable | Estimate | Std. Error | t-Value | Pr(>|t|) |

|---|---|---|---|---|

| (Intercept) | 0.440 | 0.477 | 0.924 | 0.364 |

| GovSpent(−1) | −0.012 | 0.199 | −0.061 | 0.952 |

| Debt | −0.096 | 0.034 | −2.801 | 0.010 |

| Debt(−1) | −0.070 | 0.039 | −1.807 | 0.083 |

| Debt(−2) | −0.036 | 0.036 | −1.008 | 0.323 |

| Debt(−3) | 0.019 | 0.033 | 0.557 | 0.582 |

| Debt(−4) | −0.024 | 0.035 | −0.693 | 0.495 |

| Debt(−5) | 0.032 | 0.036 | 0.901 | 0.376 |

| Couples | Parameter | Corr | p-Value |

|---|---|---|---|

| TaxRevenue_PercentGDP, Inflation | Whole | −0.842 | 0.000 |

| Pre-Euro | −0.736 | 0.000 | |

| Euro | −0.610 | 0.007 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Barkoulas, D.R.; Chionis, D. Macroeconomic Dynamics in the Greek Economy during the Pre- and Post-Euro Adoption Periods. J. Risk Financial Manag. 2024, 17, 156. https://doi.org/10.3390/jrfm17040156

Barkoulas DR, Chionis D. Macroeconomic Dynamics in the Greek Economy during the Pre- and Post-Euro Adoption Periods. Journal of Risk and Financial Management. 2024; 17(4):156. https://doi.org/10.3390/jrfm17040156

Chicago/Turabian StyleBarkoulas, Dimitrios R., and Dionysios Chionis. 2024. "Macroeconomic Dynamics in the Greek Economy during the Pre- and Post-Euro Adoption Periods" Journal of Risk and Financial Management 17, no. 4: 156. https://doi.org/10.3390/jrfm17040156

APA StyleBarkoulas, D. R., & Chionis, D. (2024). Macroeconomic Dynamics in the Greek Economy during the Pre- and Post-Euro Adoption Periods. Journal of Risk and Financial Management, 17(4), 156. https://doi.org/10.3390/jrfm17040156