Abstract

Governments worldwide cannot collect the required tax revenue for their planned activities. This study aims to assess how inefficient VAT audit function and related factors affect tax revenue performance in Amhara Region, Ethiopia. The study used primary data sources from 377 VAT registered taxpayers in Amhara Region. It also used the Ability to Pay theory of taxation, structural equation model, path diagram, and multiple regression with SPSS/AMOS software for data analysis to identify the relationship between VAT audit and tax revenue performance. Even though the Amhara Region has revenue potential to cover its expenditures, because of inefficient VAT audit functions, poor system of tax education, lack of tax resources, and long time served tax rate, the tax revenue performance is inefficient. The study assured that VAT audit and tax education significantly affect tax revenue performance. The scarcity of resources for the VAT audit function is a critical problem. Even if the existed technology networked up to woreda levels, tax auditors did not use this system appropriately. Long-time-served tax rates also greatly influence tax revenue performance. The study recommended that there should be a chain mentor relationship between experienced auditors to new and ineffective auditors. The government should supply appropriate technology that is simple to use and quickly detect tax evasion. The existed tax rate and the system of tax education should be revised. The above findings are essential for taxpayers, policymakers, and tax authorities to understand, analyze, and use the main causes of VAT audit problems on tax revenue performance.

1. Introduction

Taxation has always been a fundamental topic in political economy because it is one of all states’ main operations and a prerequisite for everything governments undertake [1,2]. Governments provide essential security services to their nations by collecting taxes from society and providing rich and poor resources. Tax revenues are the principal source of funding for government budgets to invest in public infrastructure [3]. In order to offer security, a tax is an obligatory levy levied on a subject or government property and can be used to direct the economy towards such social or economic objectives [4,5]. Every tax revenue source, especially the volatile ones, should be followed up regularly; value-added tax requires an organized and advanced degree of tax auditing. A tax audit determines an accurate and reasonable view of the business records for tax purposes. Under tax rules and regulations, the tax auditor is responsible for confirming that the reported amount is accurate and that the tax paid is correct. Another use of a tax audit is to ensure voluntary compliance with tax rules and proclamations, as well as a higher tax compliance rate in the Self-Assessment System [6,7]. Taxation is the lifeblood of every nation, and the level of growth of any country is often determined by the amount of cash generated by taxes [8]. Although the concept of tax and VAT has been defined in theory and practice in different ways, there is still no universal agreement on what it means instead of explained in contextual understandings.

However, different literature has explored the interaction between VAT audit and tax revenue performance. Regarding the impacts of VAT audit on tax revenue performance, some researches indicate positive or negative outcomes. According to Jalata [9], VAT is critical to Ethiopia’s national development and allows the country to achieve its present growth and transformation plan (GTP). VAT audit has a positive and significant impact on tax revenue performance in order to address public development needs, infrastructural development, and economic growth [10,11]. VAT audits, on the other hand, have a negative impact unless the combined effect of the probability of audit discovery and the number of audited files outweighs the individual effect in terms of taxpayer compliance [12]. Other studies indicated that tax education, tax resources, and tax rate are closely related to tax revenue performance [13,14]. In addition, an electronic tax system mediates the predictor variables and tax revenue performance [15].

Even if the above scholars expressed in such a way, Abshari et al. [16] opposed that although tax revenue plays an important role in developing countries, VAT cannot play its role as a major source of revenue, especially as VAT audit is fraught with challenges. As a result, it will not be able to meet the development needs of the society every year, and the result will lead to violence and riots. VAT has long been the primary tax tool used by governments in many nations to raise income [16]. VAT is China’s most important tax, earning significantly more revenues than any other [17]. In Ethiopia, VAT collection performance assured that the annual plan and the achievements are not matched; instead, the planned budget was covered by other sources. Because of tax evasion and avoidance, many taxpayers are non-compliant. Total tax collection is extremely affected by VAT Audit’s inefficient management, especially in Amhara Region, Ethiopia, which is a critical issue.

According to Gashaw and Ayalsew’s [18] finding, in tax evasion and avoidance practice in Bahir Dar city, Ethiopia, taxpayers evade taxes by non-declaration and under-reporting income. To hide the actual tax liability, they overstated business expenses and deductions, understated and overstated trading stock, and deducted personal expenses as business expenses. The study of Wuyah et al. [7] indicated that tax audits and investigations have a favorable association with VAT and can boost revenue collection through VAT audits. According to the study, tax audits and investigations could help curb tax evasion. Administrative support, audit quality, taxpayer awareness, and a standardized integrated government tax administration system all have a statistically significant positive influence on audit efficacy [6]. In contrast, tax law complexity, as well as tax accounting and reporting, have statistically significant negative effects.

Tax collection trends are decreasing day by day in audit functions and other ways, indicating that more needs to be performed to maximize tax revenue collection performance. Other tax collection issues include VAT knowledge (tax education), improper use of electronic tax register devices or a lack of tax technology, tax evasion, tax audit, and enforcement. The reluctant VAT audit function primarily influences the integrated development of total tax collection performance. The study’s main objective is to examine the effect of VAT audits on tax revenue performance in the Amhara Region, Ethiopia. Tax education, tax rate, resource allocation to audit sections, and the probability of being audited files are critical obstacles to tax revenue problems. Hence, this study intends to analyze the significant impacts of value-added tax audits on tax revenue collection in the Amhara region revenue Bureau. Tax revenue performance plays an essential role in Amhara Region, Ethiopia. In the area of taxation, there is limited research incorporated in the Amhara Region. The existing studies focused on value-added tax’s main problems for revenue collection. Folayan and Adeniyi [19], Gerard and Naritomi [20] and Olaoye and Ogundipe [21] explained and showed their findings on how tax evasion affects value-added tax collection. Adebisi and Gbegi [22], Mengistu et al. [23], and Shen et al. [24] focused on invoicing and related problems and the effect of tax avoidance and tax evasion.

The above findings show that the relationships between the influence of VAT audit and various dimensions of tax activities are unpredictable under different theoretical perspectives and empirical results, with contextual, methodological, and variable discrepancies. Although different researches have been conducted in this research area, there is a lack of research and a limited understanding of how VAT audit influences tax revenue performance in the Amhara Region. Value-added tax audit is an important activity to raise total tax revenue in Amhara Region, Ethiopia. Still, there is a shortage of research in the areas of the impacts of VAT audits on tax revenue performance. This knowledge gap is critical to a developing region such as Amhara Region, Ethiopia, where VAT audit is still not run by advanced technology and is in an infancy stage. Therefore, all the above researchers are not focused on VAT audit problems, tax education, tax resource, and tax rate. These variables are the critical problems of tax revenue performance in integrated ways. This research encompasses four independent variables to solve tax revenue performance problems, which are not reported yet. In addition, the research proposed a conceptual research model. It used mediating variable, electronic tax system, structural equation model, and path diagram model to address the impact of VAT audit on tax revenue performance. As a result, this study aims to fill in the gaps identified by past research, and the purpose of this research is to see how the four variables that influence tax revenue performance interact. The study primarily proposed a conceptual research model substantiated by a structural equation model and growth path tools.

This research tried to solve the subsequent three basic research questions: (1) What are the main factors influencing tax revenue performance in Amhara Region, Ethiopia? (2) How do these factors influence tax revenue performance? (3) How does the electronic tax system mediate the correlation between VAT audit, tax education, tax resource, and tax rate with tax revenue performance? (4) Is there a relationship between VAT audit, tax education, tax resource tax rate, electronic tax system, and CSR adoption?

2. Literature Review

2.1. The Evolution and Development of Taxation

Many aspects must be considered and questioned in order to study the historical origins of taxes in a society where taxation and mortality are unavoidable. As a result, when it comes to backstories, the first record of structured taxes dates from around 3000 B.C. in Egypt and is recorded in various historical documents, including the Bible. The Pharaoh would send commissioners to confiscate one-fifth of all grain crops as a levy, according to the Book of Genesis, Chapter 47, verse 33. Over time, it has evolved and adapted to new economic and social realities [25]. Tax audits and investigations have been known since the Biblical era.

Therefore, most researchers argue that the history of taxation is not known because of the early history of countries’ human development and government system. Thus, taxation is linked with the formation of the ruling group of society at the early stage of human beings. The ruling class collects taxes in kind forcefully from the existing people. The theoretical origins of the VAT are a little hazy; according to African Tax Institute [26] and Ufier [27], credit for the concept is widely provided to two theoreticians: an American economist, TS Adams, who first wrote on the subject in 1915 and cited for a 1921 piece, and a German economist, Wilhelm von Siemens, who wrote in 1920. Denmark, which was not a member of the Community at its implementation in 1967, was the first European country to implement a complete VAT system. France, as a founding member of the European Economic Community, had enacted the full VAT a year before, but the tax did not go into effect until 1968, when Germany enacted a similar VAT.

A country’s growth is defined by the amount of revenue earned by the government and spent on public infrastructure for the benefit of its population. Without enough resources for infrastructure development and the provision of power, public utilities, and services, no economy can grow [12,28]. VAT became a crucial component of an ever-increasing number of African countries’ revenue regimes in the second part of the twentieth century. External, internal, and hybrid factors all influenced the adoption of VAT regimes. Internal pressures included a lack of money from income taxes, excise taxes, and other levy collections [29,30].

On the contrary, VAT was introduced in Ethiopia in 2003 with the issuance of VAT Proclamation No. 285/2002 and VAT Regulation No. 79/2002 and was intended to replace the outdated sales tax, which had been collected at the manufacturing level for more than four decades [31]. In addition, auditing dates back to the Christian period. Anthropologists have discovered auditing records dating back to the early Babylonian period (around 3000 BC). Auditing was also practiced in ancient China, Greece, and Rome [32].

At the same time, tax audit has a long history compared to other fields of study and is directly chained with human the history and civilization of human development. Value-added tax audit started with the new commencement of VAT and was used to crosscheck the effectiveness and efficiency of tax collection performance [33]. Tax reform has received a lot of coverage in the international literature and in South Africa, as shown by the various studies cited [34]. Therefore, taxation has been in progress and developed according to the developed world, and VAT is one of the reform results.

2.2. Concepts and Definition of Tax

Tax is the income paid to the government to fulfill the public’s needs [35]. According to Kowal and Przekota [36], a tax is a mandatory levy imposed by government authority for which nothing is reimbursed and received and utilized for public investment. In addition, Krzikallová and Tošenovskỳ [37] explained that the main role of taxes in the economy is to secure income for public budgets. Onuoha and Dada [38] and Gomb, Vagask and Štefan [39] reiterated that a government levies tax on a product, income, or any activity for the development of the state.

The above literature indicates that tax has different concepts and contextual definitions; therefore, the amount levied by the government on taxpayers or a company’s profit or on commodities to fund government spending. In addition, VAT is collected at every step of the manufacturing process, but all taxes paid on purchased materials are promptly returned [36,40,41]. On top of these explanations, VAT is a consumption tax levied on practically all products and services supplied or consumed in the European Union (EU) [16,42]. Although VAT is one of the most fundamental and vital parts of taxes, it becomes a significant revenue source only when correctly executed a tax audit.

Furthermore, a VAT audit is a procedure in which the tax authorities verify whether the taxpayer declared the correct amount of tax due [43]. Consequently, one of the tools that can be used to improve tax revenue performance is a VAT audit. Developing the digital economy is the only way to accomplish effective growth in developing economies and secure a commanding position for future development [44]. All the concepts and definitions of tax, VAT, and audit expressed the critical values of taxation in any government.

2.3. The Relationship between the Independent, the Mediating, and Dependent Variable

Tax Education and Tax Revenue Performance

Several studies have examined the impacts and correlations between tax education and tax revenue performance. Tax education highly affects tax revenue performance positively and significantly [45]. The lack of well-organized taxpayer education and assistance programs about VAT, inadequate refund management, and low voluntary compliance of taxpayers are all challenges facing the Ethiopian tax administration [46]. Furthermore, higher levels of education are associated with a higher likelihood of compliance. Educated taxpayers may be aware of noncompliance chances; taxpayers with a greater comprehension of the tax system and a higher moral standard, on the other hand, are more compliant and accept this viewpoint [47,48].

On the other hand, 35% of all registered VAT payers submit their tax returns monthly and request a refund, while 38% of taxpayers have submitted reports with no tax liability. Tax bureau officials and merchants’ relations have deteriorated due to inefficient door-to-door support and continuous follow-up, and such official aids are viewed adversely by taxpayers as an enemy [49]. Other implications of tax education, such as perceptions, attitudes, and citizen participation, are also essential, as we will address next [50]. Thus, most studies agreed that tax education positively and significantly affects tax revenue performance.

Hypothesis 1 (H1).

Tax Education has a positive and significant impact on Tax Revenue Performance.

Tax Resource and Tax Revenue Performance

According to numerous studies, tax resource is one of the important variables that can affect the intended revenue. At a 1% significance level, the variable tax audit resource has a negative impact on revenue collection and is statistically significant [43,51]. According to Badra [52], in Bauchi State, Nigeria, the tax auditors are limited in number and not equipped with the required stationaries that affect the tax audit function. Administrative limitations in resource allocation, awareness creation, training and feedback, controlling and following up to combat VAT evaders, and employee corruption are key internal factors hindering tax collection. Employees’ rent-seeking (corruption) arises due to their close connection with business people [53].

Furthermore, the availability of tax resources through the tax audit function enhances the tax system and boosts tax revenue collection. Because of the attention paid to tax resources, countries with lower baseline compliance costs gain more from tax changes and expanding tax bases [54]. Therefore, almost all researchers agreed that tax resources played a substantial influence on tax revenue performance and are positively and significantly interrelated to tax revenue performance.

Hypothesis 2 (H2).

Tax Resource has a positive and significant impact on Tax Revenue Performance.

Tax Rate and Tax Revenue Performance

Lin and Jia [13] and Kopeć [55] found that a high tax rate will stifle people’s spending. Regardless of the direct tax rate level, the share of direct tax to total tax will increase. The intricacy of the tax structure influences the tax rate significantly. According to Helcmanovsk and Andrejovsk [56], in either scenario, the variables statutory and average effective tax rates have no significant impact on corporation tax collections. Taxpayers are burdened more by a higher tax rate. It may improve revenues slightly in the short term, but it has a long-term impact. It lowers taxpayers’ disposable income, lowering their spending power [57]. The above research indicates that the tax rate impacts tax revenue.

In addition, the Minister of Finance of South Africa announced a 1% increase in VAT to 15% in the 2018 budget. The increase in the VAT rate is part of a larger package of tax reform proposals targeted at increasing revenue [58]. On the other hand, lower income tax rates have a more significant impact on economic development in developing countries such as Botswana, where higher tax revenue collection, revenue creation, and GDP growth are positive outcomes [59]. Saudi Arabia previously established a 5% VAT on all goods and services; however, following the recent global epidemic of COVID-19, the kingdom has tripled this amount and will impose a 15% VAT starting in July 2020. Because economic activities have decreased and health costs have increased, the main rationale for raising this rate is to boost revenue [60]. The introduction of the VAT Flat Rate Scheme has bettered tax revenue mobilization in a developing country such as Ghana as it has increased the number of VAT-registered retailers [61].

In the Czech Republic, the regular VAT rate is below the revenue-maximizing rate, and lowering it would benefit both taxpayers and the state budget [62]. The higher the rates, the greater the motive to avoid or evade taxes or close the business. Consequently, the tax rate increases tax revenue performance if it increases based on the paying capacity and a certain society limit.

Hypothesis 3 (H3).

The tax rate has a positive and significant impact on Tax Revenue Performance.

VAT Audit and Tax Revenue Performance

VAT Audit and Investigation has a positive relationship with VAT and helps to generate more revenue. The study also found that efficient tax auditing and investigation might significantly reduce VAT evasion in Nigeria’s Kaduna State, resulting in significant increases in government revenue [7,43]. The Bauchi State Tax Authority used tax audits to meet revenue targets. Tax audits minimize tax evasion and other tax irregularities, according to the findings of [52]. The audit work of Hawassa City, Ethiopia, is very insignificant compared to the total number of VAT registrants in the city [53]. The VAT audit in Ethiopia is challenged by a lack of technically competent and proficient human resources, low data quality, poor intelligence inputs, low performance in terms of quality, tax yield, and revenue yield [63]. In general, all research finding assessed and agreed that tax audit and tax revenue performance has a positive and significant relationship.

Hypothesis 4 (H4).

VAT Audit has a positive and significant impact on Tax Revenue Performance.

The Mediating Effects of Electronics Tax System on Tax Revenue Performance

Adopting an electronic tax system is a partial mediator in the relationship between tax education and tax revenue; moreover, implementing an electronic tax system and having a positive attitude are linked to tax compliance or tax revenue performance [15]. Nigeria has seen a huge reduction in tax evasion thanks to an excellent electronic tax system [64]. Electronic tax collection has recently been a hot topic in developing countries in policy discussions [65,66].

Furthermore, small and micro Businesses feel that taxpayer awareness of electronic taxation positively impacts tax compliance in Lagos [67]. According to Allahverdi et al. [68], the rate of tax receipts to GDP in Turkey increased by 43.84 percent after implementing the electronic taxation system. On the other view, the extent to which taxpayers are aware of the electronic tax filing system influences their compliance rate; if the compliance cost is high, taxpayers may be hesitant to use it. Even though the effect of ease of use is not statistically significant, positive implies that it can affect tax performance. Gwaro et al. [69] and Manaye [70] revealed that VAT collection using cash register machines positively affects VAT revenue, and other independent variables significantly affect VAT. According to Eilu [71], domestic revenue collection via taxation in many Sub-Saharan African countries is still below its capacity. Several regional states have implemented electronic fiscal devices to advance VAT collection and maximize tax revenue. However, there have been difficulties implementing electronic fiscal devices in Kenya and Tanzania. Therefore, all the existing research agrees that electronic tax has a significant influence and a critical role in increasing tax revenue performance and is used to mediate different factors and tax revenue performance.

Hypothesis 5 (H5).

The electronic tax system mediates tax revenue performance.

To conclude, taxation is a critical agenda for people worldwide, particularly in developing countries, because foreign aid and grants cover the majority of their expenses. In all directions, the trend in tax revenue collection indicates complicated problems in collecting the required amount of revenue. Various studies encourage tax authorities to broaden the tax base and collect depending on regional revenue potentials. On the contrary, most researchers ignored the effects of VAT audit operations, particularly the combined impact of a VAT audit, tax education, tax resources, and tax rate. As a result, using a structural equation and a growth path model to examine the effect of the above variables on tax revenue performance, this study seeks to fill in the gaps left by prior studies by analyzing the mediating impacts of the electronic tax system.

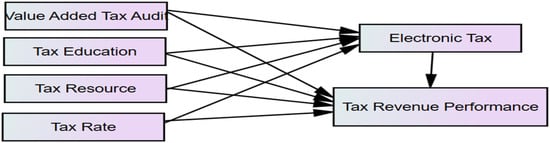

2.4. The Conceptual Model of the Study

This research anticipated the following conceptual research model to determine the empirical relationships between the independent and the mediating variables on tax revenue performance. The explanatory variables are VAT audit, tax education, tax resource, and tax rate. The mediating variable is the electronic tax system, and the observed variable is tax revenue performance. Following that, using the indirect and direct effects of the mediation variable electronic tax system, the conceptual framework of the subsequent model attempted to validate, estimate the fitness, and support the stated hypothesis. As a result, as shown in Figure 1, the proposed conceptual framework focuses on enhancing the assumptions of structural equation modeling, path diagram modeling, and growth path modeling analysis to reinforce the research results.

Figure 1.

Conceptual Research Model, Authors’ Design.

3. Research Methodology

3.1. Research Design and Data Collection

The framework of the research road map is research design, which addresses the research process, allowing researchers to identify where they are in the process. It compares study designs, techniques, analysis, and interpretation alternatives [72]. The study used both quantitative and qualitative research methods using a survey approach. The variables; VAT audit, tax education, tax resource, and tax rate were taken as the predictor variables in this study. It also considered the tax revenue performance as a dependent variable and the electronic tax system as a mediator variable. The research was conducted using primary data from a VAT registered taxpayers, tax experts, and regulatory bodies with structured and self-administered questionnaires; the secondary data were collected from various literature, reports, policy guidelines, and tax proclamations. A five-point Likert-scale questionnaire was constructed and administered for all variables. The questionnaires used in this study are adapted from [12,73,74,75].

3.2. Sampling Method and Sample Size Determination

The study used simple random sampling techniques to select a representative sample size to determine sample size. The researcher used the formula by Krejcie and Morgan [76] to choose a sample. Based on the data obtained from Amhara Revenue Bureau, the total active VAT registered taxpayers who report to the tax audit department for audit purposes is 20,336. Tax officials, auditors, and other tax experts are taken directly and purposively. Therefore, the required sample size is 377. The questionnaire was prepared and distributed to 377 respondents, and the researcher endeavored interviews with 25 respondents to take supporting evidence. This study interviewed taxpayers and officials to strengthen the qualitative research information. The study chose the three metropolitan cities (Bahirdar, Gondar, and Dessie) and the five medium city administrations (Debre Birhan, Debre Markos, Kombolcha, Woldia, and Debre Tabor) with purposive sampling techniques. All the selected cities are most likely to have a large proportion of VAT-registered taxpayers who represent rural area taxpayers.

3.3. Methods of Data Analysis

The research tested the stated hypotheses and evaluated the obtained data. It also used Social Sciences Statistical Package (SPSS)/AMOS 24 statistical software version for data analysis; the obtained and validated data were coded, processed, and analyzed. The structural equation model and path diagram model were used in this study. Multiple regression models were also used to study the relationship between the dependent and explanatory variables. An exploratory factor analysis (EFA), Pearson correlations, and regression analysis were the key statistics used in the study.

3.4. Measuring Instruments

3.4.1. The Dependent Variable

The research used the measurement instruments of the dependent variable, tax revenue performance, in five measuring questions and adopted from the previously validated research sources [77]. The dependent variable tax revenue performance was measured using conceptualized measuring instruments using five-point Likert-scale questions ranging from strongly disagree to strongly agree. The conceptualized measuring instruments (questionnaires) are attached in Appendix A.

3.4.2. Measurements of Independent Variables

VAT audit is the decisive factor that critically impacts tax revenue performance. Consequently, to execute the investigation on the impact of VAT audits on tax revenue performance, the researcher targets VAT registered taxpayers. Although the impact of VAT audit on tax revenue performance has been measured in different measurement methods, this research tried to measure and adapt the research results from previous research [4]. The adopted measuring instruments contained five measuring tools based on the research objectives. The second independent variable, tax education, was quantified and measured by the adopted measurement tools from Akintoye and Onuoha [78] and Onuoha et al. [79], and six measuring instruments were used to manage the impact of tax education on tax revenue performance in line with the research objectives. The third independent variable, tax resource influences on tax revenue performance, was measured by five measuring tools; the number of audit staff, resource materials, qualification and experience of the auditors, the capability of auditors, and the commitment of individual auditors in performing audit activities [43]. The four measuring tools were used to measure the tax rate variables. The past measured the influence of the independent variable tax rate validated and confirmed research results which were evaluated in four questions and adopted from [75,80].

3.4.3. Measurements of Mediator Variable

A tax electronics system is used as a mediating variable by strengthening tax compliance and ultimately increasing tax revenue performance. To assess the impact of the mediator variable, the tax electronics system, the researcher used the past literature validated and confirmed measuring tools [15,77,81]. If taxpayers are compliant with their attitude toward the electronic tax system, tax revenue performance will achieve in accordance with the planned objectives. Tax compliance and tax revenue performance are interdependent. Therefore, the mediating role of the electronic tax system was measured and validated in five research questions.

Generally, this research takes VAT audit, tax education, tax resource, and tax rate as the independent variable to predict the dependent variable, tax revenue performance using the mediation variable, the electronic tax system. Different measuring tools measured all the dependents, independent, and mediating variables.

4. Analysis and Interpretation

After the data were collected, coded, and reviewed for errors and completeness, it was analyzed using descriptive research methods and multiple regression analysis using SPSS/AMOS. The descriptive analysis provides demographic respondents’ data (gender, age, education, and work experience). The structured questions were provided to respondents to obtain reliable information. The study’s main aim is to assess the impacts of VAT audits on tax revenue performance in the Amhara Region, Ethiopia. As a result, the research analyzes all of the respondents’ demographic data in the following ways.

4.1. Demographic Profile of Respondents

All the study variable items, including the respondents’ demographic profile, were addressed based on 23 items and 377 respondents. The demographic details of the final respondents are presented in Appendix A, Table A1. As indicated in the result, the number of male taxpayers, 76.9%, is higher than females, 23.1%. From an economic perspective and logic, females are more active in business, but females are less than males. Concerning to age group, most respondents were in their mature age group, and they could respond without biased and assured their response independently. Only 22.3% are 25 years and below. Similarly, most respondents have different certificates; 47.7% have a certificate, 43.2% are in high school or below, and only 7.4% and 1.6% have a degree and masters in educational background. The data reliability is more accurate; it is more reliable if the degree holder is more than this. Finally, 47% of respondents were from 16 to 20 years old, and 19.6% were from 11 to 15 years old. Most respondents had good medium work experience from the work experience to provide relevant information for a reasonable decision, and well-experienced taxpayers can tackle tax avoidance and evasions.

4.2. Validity and Reliability Test

The study used SPSS/AMOS statistical software to validate and confirm the relevant questionnaire items for validity and reliability test of the assumptions. The study checked the reliability and validity using Cronbach alpha, factor loading, composite reliability (CR), and average variance extracted (AVE). According to Tavakol and Dennick [82], Cronbach alpha measures the internal consistency of a test or scale; it is expressed as a number between zero and one. Internal consistency defines the degree to which all the items in a test measure the same definition or construct. The researcher used the reliability test study to measure the impact of value-added tax audits on the tax revenue performance using Cronbach alpha (α) to satisfy determinant variables. The Cronbach alpha arbitrary value of 0.70 and above is a sufficient measure of reliability or an instrument’s internal consistency [83]. Therefore, the Cronbach alpha’s computed value in Table 1 results ranges from 0.757 to 0.957, which shows that all variables are reliable and the data are typically distributed.

Table 1.

Factor Loading Analysis, the result of validity and reliability.

Moreover, the most common main uses of factor analysis are discovering the relationship between all of the variables in a dataset and finding the inexplicable factors that affect the co-variation of numerous observations. A variable describes the variance on a specific element represented by factor loading values. A factor loading result of 0.70 or greater in an SEM shows that the factor absorbs sufficient variance from the variable [84]. As a result, the predictable factor loading values for the total variable items results, which are under the required standard, are most likely significant, confirming the measurement constructs strong convergent validity. The shared variance among the observed variables of a latent construct is referred to as composite reliability. Likewise, the composite reliability (CR) result of the shared variance of the observed variable of the latent constructs varied from 0.837 to 0.946, indicating that the result is accepted in terms of reliability, with an alpha threshold of >0.70 [85]. Therefore, the calculated variance value was greater than the estimated variance value, indicates the estimated values justify the internal consistency of reliability and validity.

The average variance extracted (AVE) is a commonly used metric for validating constructs; it measures the amount of variance captured by a construct versus the variance due to measurement error. It was calculated using factor loadings from estimated least squares or maximum likelihood regressions. Furthermore, the results were more efficient (0.50 AVE 1.00) [86]. Therefore, the average variance extracted (AVE) values for all derived construct components are appropriate, ranging from 0.519 to 0.816, which is between the above range and acceptable. The result indicates that the measuring tools used in the study reflect the structures of each research variable. The Table 1. presents factor loading analysis, the result of validity and reliability.

4.3. Correlation Matrix

The Pearson correlation coefficient was used to estimate correlations in this analysis. The parametric Pearson correlation was chosen over the non-parametric variant since the data were normally distributed. The presence (given by a p-value) and strength (supplied by the coefficient r between −1 and +1) of a linear relationship between two variables are measured using Pearson correlation [87]. Because p-values measure the degree of data compliance with the null hypothesis, researchers should always mention the actual number, not just words such as p < 0.05 or p > 0.05 [88]. The (AVE) from the observed variables specifies a positive and significant relationship between all predictor and response variables at p < 0.05. Consequently, the covariance values show that entirely the constructs are interconnected. Furthermore, this creates the VAT audit (VAA), tax education (TAE), tax resource (TAR), and tax rate (TART) towards the predicted variable, the tax revenue performance relationship. The mediation variable, the electronic tax system, also supports the relationship between variables, as presented in Table 2.

Table 2.

Correlations Result.

4.4. Multiple Regression Analysis

Multiple regression analysis is a statistical procedure that assesses the relationship between a dependent variable and several predictor variables [89]. This research regarded VAT audit, tax education, tax resource, and tax rate are predictor variables, tax revenue performance as the predicted variable, and the mediation variable, the electronic tax system. The predictor values of all parameter estimates (β) tax rate (TART) 0.637, tax education (TAE) 0.627, VAT audit (VAA) 0.552, tax resource (TAR) 0.751, to tax revenue performance (TRP) 0.497. The multiple regression analysis results show more possibility of having positive and significant relationships with a direct impact based on the results of Table 3. On the other hand, the parameter estimate (β) values were VAT audit (VAA) 0.559, tax rate (TART) 0.740, tax education (TAE) 0.677, tax resource (TAR) 0.817, tax revenue performance (TRP) 0.517, and the electronic tax system (ELT) 0.697, which have indirectly more possibly positive and significant relations, and which is supported by the mediation variable electronic tax system. As shown in Table 3, when the parameter estimates (β) were compared to their corresponding standard error (S.E), the critical ratio (C.R) score was greater than 1.96, confirming a positive and significant relationship, with a 0.05 p-value.

Table 3.

Regression Weight for the Level of Significant and Critical Ratio.

4.5. Mediation Effects of Electronic Tax System

The mechanism in which intervention provides its consequence is described by a mediating variable utilized as an intermediary variable [90]. This study used SPSS/AMOS statistical software to analyze the mediating effects of the electronic tax system using the structural equation model and the growth path model. Therefore, the models estimated the direct and indirect effects of mediating variables using growth path modeling and weighted multiple regression analysis.

In statistics, the Sobel test is a method of testing the significance of a mediation effect. The test statistics value of the Z-score for the Sobel test is more than 1.96, indicating that mediation effects occur [91]. In the interaction between the independent variables and the dependent variable, the mediating impact of the electronic tax system was active and mediated their relationships. The Sobel test fulfilled more than 1.96 requirements since its Z-score was greater than 1.999 and up to 8.0155; it was significant at a p-value of 0.05, as shown in Table 4. Moreover, the mediation effects and Sobel test findings are highly significant, verifying that the dual impact (direct and indirect) is vital. It means that the electronic tax system reliably mediates the relationship between the independent variable and tax revenue results. In other words, the Amhara Region is more likely to benefit from the electronic tax system.

Table 4.

Results of the mediation effects.

4.6. The Structural Equation Model and Growth Path Modeling Result Analysis

4.6.1. Structural Equation Model Goodness-of-Fit Indices

This research used SEM to analyze and crosscheck the Chi-square (χ2), Root Mean Square Error of Approximation (RMSEA < 0.06), Hoelter’s N, and Goodness of Fit Index. SEM (Structural Equation Modeling) is a technique for analyzing the correlation of factors from an exploratory survey with a key and then extracting a model of the relationship of various factors, which is the study’s basic theory or hypothesis. (1) Chi-square (χ2) should have a non-significance (p > 0.05) according to the statistics. (2) GFI (Goodness of Fit Index) >0.90 (3) and Root Mean Square Error of Approximation (RMSEA < 0.06) are used in SEM to determine the sufficiency and suitability of sample size (case) [92]. According to Civelek [93], Fit Indices, and Goodness of Fit Values are 2 < CMIN/DF < 3; 0.95 < CFI < 0.97; 0.85 < AGFI < 0.90; 0.90 < GFI < 0.95; 0.90 < NFI < 0.95 and 0.05 < RMSEA < 0.08. Therefore, the result of Table 5 indicates that the value of the Goodness of Fit Indices is 0.925, the Chi-square to Degree of Freedom (χ2/df) for the model is 2.144, and the Root Mean Square Error of Approximation (RMSEA) is 0.077, which satisfies under the acceptable range, <0.08.

Table 5.

Summary of Goodness of Fit Indices.

4.6.2. The Result of Model Fit Indices Analysis

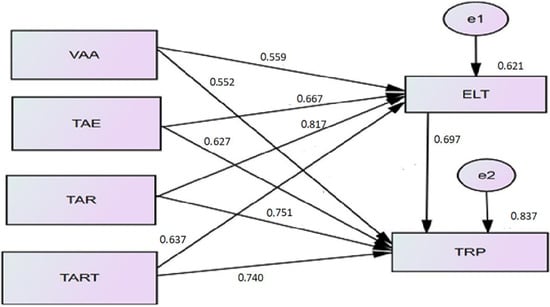

The level of model fitness and the effects of all the constraints on the outcome variable are revealed by estimated values of the variables’ standardized coefficients. The R-square (R2) estimated value for the proposed conceptual research model is 0.914 (19.4%) with a p-value of 0.000. With a p-value of 0.000, the indirect effects of the model fitness R-square (R2) based on the mediation variable are 0.952 (95.2%).

According to the result of the direct path diagram modeling in Figure 2, VAT audit (β = 0.552 ***), tax education (β = 0.627 ***), tax resource (β = 0.751 ***), and tax rate (β = 0.637 ***) positively affect the dependent variable tax revenue performance. In addition, the indirect path diagram modeling result indicates, VAT audit (β = 0.559 ***), tax education (β = 0.677 ***), tax resource (β = 0.817 ***), and tax rate (β = 0.740 ***) positively affect the dependent variable tax revenue performance, at the same instant, the mediating variable electronic tax system mediate at the estimated value of (β = 0.697 ***).

Figure 2.

Standardized path coefficients and significance of the structural equation model.

In the path diagram, the indirect and direct relationship between the predictor variable and the outcome variable shows that if the predictor variable increased by one unit, the outcome variable increased by the same amount, providing all other variables remained constant. The independent variables, VAT audit, tax education, tax resource, and tax rate, change; the dependent variable, tax revenue performance, also shifts by one unit. Furthermore, when the mediation variable, the electronic tax system, changed by one unit, indirectly, the dependent variable, tax revenue performance, was affected, positively and significantly, by the mediation effects of the electronic tax system. Therefore, VAT audit, tax education, tax resource, tax resource, and tax rate are significant factors influencing tax revenue performance.

In general, the mediation of the electronic tax system has a substantial multiplier effect; simultaneously, the findings and interview analyses revealed that VAT audit activity in Amhara Region is significantly higher in tax rate and tax resource, next to tax education.

4.7. Test of Hypothesis and Decisions

Researchers first forecast whether hypotheses are accepted or rejected; the researcher also approves when study results prove them based on the assumptions. Hence, this study developed five potential assumptions based on past research and can be accepted or rejected in line with research results. In this regard, the goal of this research was to fill in some gaps by presenting hypothetical conclusions on how VAT audit affects tax revenue application in Ethiopia’s Amhara Region.

Therefore, this research aims to propose research ideas based on this research finding and to fill gaps on the issues of how VAT audit affects tax revenue performance in the Amhara Region, Ethiopia. Consequently, Table 6 result indicates that all of the determined and tested hypotheses were shown to significantly and positively support the success or failure of tax revenue performance.

Table 6.

Result of Hypotheses Testing.

5. Discussion

The above result assured that VAT audit, tax education, tax resource, and tax rate positively and significantly influence the dependent variable tax revenue performance. This shows that the increase in the independent variable or the reluctant decision in these independent variables in tax administration will significantly influence the performance of the institution’s tax revenue.

In practice, the annual VAT audit functions are not appropriately audited based on the value of the available taxpayers’ files; the system of tax education is not out of the usual situation; it was not applied according to the situation. Especially in Amhara Region, Ethiopia, there has been a security problem in some parts of the region in the past three years. Thus, to reduce the impact of tax education on tax revenue performance Amhara Region Tax Revenue Bureau and the Regional State should apply a new system of tax education based on the situation. In addition, the allocated tax resources are not sufficiently and timely supplied to tax experts and totally to the tax offices. The existed tax rate was served for more than 15 years. Taxpayers have opposed the current tax rate. Taxpayers indicate some selected tax types that should be revised in the tax rate amount. These can increase the region’s tax revenue performance. The existing electronic tax systems are not appropriate and relevant to combat tax evasion and avoidance at the time of VAT audit. Tax electronic systems can reinforce VAT audit activities.

Moreover, to invest in public infrastructure sustainably in Amhara Region, the Region Revenue Bureau should install a new advanced electronic tax system; this can facilitate the VAT audit function, solve the shortage of tax resources, and support the old system of tax education. As a result, this research rejects the null hypothesis and accepts the alternative hypothesis that implementing and using the electronic tax system in the Amhara Region, Ethiopia, has improved tax revenue performance; this study supports Allahverdi [68] and Monica et al. [94], who found that the electronic tax system increased tax revenues and lowered the cost per tax in the long run.

Therefore, VAT audit, tax education, tax resource, and tax rate significantly impact tax revenue performance in Amhara Region, Ethiopia, for sustainable development and supplying public infrastructure. Thus, it is consistent with former research results [95]. In addition, this research also rejects the null hypothesis and accepts the alternative hypothesis that exhaustively using tax education in the Amhara Region has improved tax revenue performance. This study also supports the findings of [48]. Moreover, the research accepts the alternative hypothesis that allocating tax resources and revising a long time served tax rate in Amhara Region can reinforce the region’s tax revenue performance [80,96].

In addition, because of the current situation of the developing countries, tax revenue sources are the best weapons for the countries that can apply their strategic plan without influencing others. Therefore, based on the findings of the research result, the Amhara Region, Ethiopia, could not recognize the benefits of tax revenues and support the tax offices by supplying tax resources and revising a long time served tax rate. The government officials do not provide special attention to tax education activities and leave the tax education role to tax offices. VAT audit functions are not supported by technology but instead focused on tax auditors; because of this, more taxpayers’ files with arrears and fictitious reports are not critically assessed. The existing electronic tax systems are not renewed or updated and have served for more than 15 years. The electronic tax system significantly impacts tax compliance and tax revenue performance [97]. Consequently, the result assured that tax education has a significant and positive impact on tax revenue performance; tax education greatly influences tax revenue performance [14,50].

Generally, the inefficient use of VAT audit, tax education, tax resource, and tax rate, directly and indirectly, affect tax revenue performance. In addition, the electronic tax system mediates the impact of the independent variables on tax revenue performance.

6. Conclusions

6.1. Conclusions

The study examined the effect of VAT audits on tax revenue performance in the Amhara Region, Ethiopia. The findings of this study suggest the following conclusions about the impacts of VAT audits and the factors that influence tax revenue performance aligned with the research questions. The outcome variable, tax revenue performance, is highly affected by VAT audit, tax education, tax resource, and tax rate positively and significantly. All the indicators of variables have a positive and substantial relationship with the predictor and the outcome variable. Furthermore, the derived model fits at a value of R-square (R2) = 0.837 or 83.7%; this implies all the four identified response variables more influence the outcome variable. The study’s finding shows that the mediation of the electronic tax system has a strong multiplier effect. On the contrary, the other independent variables (VAT audit, tax education, tax resource, and tax rate) have a much higher significant impact on tax revenue performance.

Therefore, the study’s findings in the correlation matrix reveal that VAT audit, and tax education have a significant positive effect on tax revenue performance (β = 0.587 ***, p < 0.05), and (β = 0.801 ***, p < 0.05). In the meantime, tax resource, and tax rate have found to have a significant positive effect on Amhara Region tax revenue performance (β = 0.573 ***, p < 0.05) and (β = 0.816 ***, p < 0.05). Thus, VAT audit, tax education, tax resource and tax rate are crucial factors for tax revenue performance [4,12,14].

The electronic tax system also mediated the association between VAT audit, tax education, tax resource and tax rate, and tax revenue performance. The relationship between VAT audit, tax education, tax resource, tax rate, and tax revenue performance; implies that the electronic tax system had a significant multiplier effect. VAT audit, tax education, tax resource, and the tax rate can also enhance the Amhara Region’s tax collection performance. Consequently, all the proposed hypotheses were accepted [15,64]. Therefore, the results show that VAT audit, tax education, tax resource, and the tax rate could increase the collection performance of the region and its capacity to improve its audit and collection procedures with advanced technologies.

Moreover, tax revenue performance is influenced due to the support of lack of an electronic tax system in VAT audit functions. However, the Amhara Region Revenue Bureau tried to install SIGTAS (Standard Integrated Government Tax Administrative System) and network up to woreda levels fifteen years ago. The existing tax auditors were not well equipped, trained, and used efficiently. Excessive taxpayers’ files that are not audited on time and the imbalance of the number of auditors were critical problems of the audit function. In addition, the VAT auditors are not efficient in exploring tax fraud and evasion better than the taxpayer advisors’ and accountants’ misappropriations. Thus, it should be supported by advanced technology.

Furthermore, tax experts and officials’ lack of experience, awareness creation, and tax education problems for taxpayers and the public on tax proclamations and procedures are complicated obstacles to tax revenue performance. Another important concern confronting tax authorities is a lack of resources, which is limiting the region’s expected tax revenue performance. The working condition is not also convenient, including the availability of enough budget and equipment. The highest amount and long time served tax rate becomes a pushing factor for taxpayers to engage in tax evasion and avoidance. In addition, the tax rate is not determined based on the ability-to-pay principle. If tax auditors reject the taxpayer files at the auditing time, the rate will be too high when the tax assessment expert converts them to taxable income. According to the respondents’ interviews, VAT audit and tax education have a significant role if all are supported by an electronic tax system which can drastically increase tax revenue performance. Furthermore, the findings of this study have essential insinuations for academics, practitioners, and policymakers. It also highlights the theoretical and practical contributions.

6.2. Theoretical Implications

The current study makes three major theoretical contributions. First, it was apparent from the review of the literature that the impact of VAT audit on tax revenue performance. Therefore, this study significantly contributes to the literature because it is a pioneering study that examines the impact of each dimension of VAT audit on Tax revenue performance. In addition, this study filled the gap in the knowledge that was identified in previous studies [4,11,43,48,78,80,98].

Second, this study is compatible with the Ability to Pay theory of taxation as a theoretical framework and the equal sacrifices theory of taxation. The current study contributed in terms of combining the Ability to Pay theory of taxation and the equal sacrifices theory of taxation through the application of taxation. Hence, this study supports the Ability to Pay theory of taxation and equal sacrifices theory of taxation in the context of the field of taxation.

Finally, this study examined the mediating role of the electronic tax system on the relationship between VAT audit, tax education, tax resource, and tax rate with tax revenue performance. This study also confirmed the mediating role of the electronic tax system in the relationship between VAT audit, tax education, tax resource, and tax rate with tax revenue performance, which was not apparent before. Furthermore, this research is important because it widened the theoretical understanding of VAT audit and tax revenue performance.

6.3. Practical Implications

This research finding provides awareness about the impact of VAT audit on tax revenue performance in the Amhara Region to tax officials and policymakers from the viewpoint of the VAT audit, tax education, tax resource tax rate, and tax revenue performance. By using the research result of this study, tax officials and tax experts may be able to enhance their managing, tax collection, and audit performance. In order to provide VAT audit and tax education functions properly, tax officials and line department heads should provide more attention to tax auditors, tax education and communication experts, customer service delivery, and employee training, reward, and motivation system. Brazil’s practice of using a lottery system can be used in the Amhara region. In Brazil, consumers serve as tax auditors. They can choose to have their taxpayer identification number recorded on receipts, and merchants are obligated to transmit all receipts’ information to the tax authority, including consumers’ ID numbers. The total amount of the receipts are then used to obtain lottery tickets and tax rebates. This practice is conducive to improving public participation, compliance, and monitoring. The Amhara region can properly take similar measures to optimize the VAT management quality in terms of receipt management and motivation system.

In addition, tax resources should be sufficiently accessible. Apart from this, it was also confirmed that tax collection performance could not be exhaustively collected without employees’ commitment, modern technology, and the best-defined processes. This study indicated that VAT audits using an electronic tax system and auditing activities could examine, investigate, and manage taxpayers’ transactions and enhance tax revenue performance. Amhara region in Ethiopia can learn from the successful practices of international organizations or foreign areas to improve the use of the electronic tax system. For example, in the use of information systems, Russia sets the AIS VAT 3 (АСК НДС 3) module in the AIS Tax 3 system (АИС Налoг 3). Amhara region can refer to the Russian experience and set a special module about VAT in the electronic tax system to receive and process various information and issues about VAT, and thus facilitate the handling of VAT-related things. Meanwhile, provided the practices of OECD countries, especially the Netherlands, the Amhara region should improve its information and communication technology (ICT) and make the best use of advanced technologies to optimize its VAT management quality. Those measures are conducive to minimizing human labor and time and supplying reliable information for taxpayers’ audit findings in the long run. As a result, the required amount of revenue will be collected and enhance the institution’s performance as a whole. Therefore, this research provides practical implications for increasing tax revenue performance and the research areas of VAT audit and tax revenue performance.

6.4. Limitations and Directions for Further Research

This research has some limitations. On the one hand, it is limited to the Amhara Region, Ethiopia, in the area of tax collection performance, especially in the issue of a VAT audit, tax education, tax resource, tax rate, and tax automation only. Although the test results are expected, further research is still needed to track whether the results will be different in the future. On the other hand, other variables that influence tax revenue performance were not considered, such as tax evasion and avoidance, inflation, and GDP. Thus, further research is required in this area. This study also suggests some future research directions in order to increase tax revenue performance in the Amhara Region, Ethiopia, particularly in the area of VAT on selected overseas manufacturing businesses and industrial park investment. VAT audit does not massively address all woredas in the Amhara Region, which is instead covered by zone administrative office auditors. However, tax education has access at the woreda level.

Therefore, tax auditors should have engaged at all woreda levels and promoted all related issues to practice to different stakeholders to lay the foundation and create awareness about the pillars of the macroeconomic portion of the tax. Amhara Regional State government should implement strict rules and regulations to ensure that all taxpayers and tax authorities appropriately use the electronic tax systems at all levels of administration. Thus, more research in this area is required in the future.

Author Contributions

Conceptualization, R.M., L.Z. and N.M.F.; methodology, R.M., L.Z. and N.M.F.; validation, N.M.F.; formal analysis, R.M., L.Z. and N.M.F.; investigation, writing original draft preparation, N.M.F.; writing review and editing, N.M.F. and L.Z.; supervision, R.M. and N.M.F. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The corresponding author will provide all of the necessary data to support the research result.

Acknowledgments

The authors expressed our gratitude to everyone who took part in the survey and provided valuable inputs. We also thank all of the assistance from the Wuhan University of Technology, School of Management.

Conflicts of Interest

The authors declared no conflict of interest.

Appendix A

Table A1.

Questionnaire and Sources.

Table A1.

Questionnaire and Sources.

| Variables | Items | Sources |

|---|---|---|

| VAT Audit |

| [4] |

| ||

| ||

| ||

| ||

| Tax Education |

| [78,79] |

| ||

| ||

| ||

| ||

| ||

| Tax Resource |

| [43] |

| ||

| ||

| ||

| ||

| Tax Rate |

| [75,80] |

| ||

| ||

| ||

| Electronic Tax System |

| [15,77,81] |

| ||

| ||

| ||

| ||

| Tax Revenue Performance |

| [99] |

| ||

| ||

| ||

|

References

- Kiser, E.; Karceski, S.M. Political Economy of Taxation. Annu. Rev. Polit. Sci. 2017, 20, 75–92. [Google Scholar] [CrossRef]

- Siimon, R.; Lukason, O. A decision support system for corporate tax arrears prediction. Sustainability 2021, 13, 8363. [Google Scholar] [CrossRef]

- Barbu, L.; Mihaiu, D.M.; Șerban, R.-A.; Opreana, A. Knowledge Mapping of Optimal Taxation Studies: A Bibliometric Analysis and Network Visualization. Sustainability 2022, 14, 1043. [Google Scholar] [CrossRef]

- Olaoye, C.O.; Ekundayo, A.T. Effects of Tax Audit on Tax Compliance and Remittance of Tax Revenue in Ekiti State. Open J. Account. 2019, 8, 1–17. [Google Scholar] [CrossRef]

- Goossenaerts, J.B.; Zegers, A.T.; Smits, J.M. A multi-level model-driven regime for value-added tax compliance in ERP systems. Comput. Ind. 2009, 60, 709–727. [Google Scholar] [CrossRef]

- Nurebo, B.Y.; Deresse, M.L.; Mathewos, W. Effectiveness of Tax Audit: A Study in Kembata Tembaro Zone, Southern Ethiopia. Int. J. Commer. Financ. 2019, 5, 34–50. [Google Scholar]

- Wuyah, Y.T.; Aku, Y.Y.; Ahmad, M.D. Impact of tax audit and investigation on Value Added Tax Generation in Kaduna State. Am. J. Bus. Soc. 2018, 2, 52–56. [Google Scholar]

- Omesi, I.; Nzor, N.P. Tax Reforms in Nigeria: Case for Value Added Tax (VAT). Afr. Res. Rev. 2015, 9, 277. [Google Scholar] [CrossRef]

- Jalata, D.M. The Value Added Tax and Sales Tax in Ethiopia: A Comparative Overview. Eur. J. Bus. Manag. 2014, 6, 246–250. [Google Scholar]

- Adediran, S.A.; Alade, S.O.; Oshode, A.A. The Impact of Tax Audit and Investigation on Revenue Generation in Nigeria. Eur. J. Bus. Manag. 2013, 5, 171–177. [Google Scholar]

- Uvaneswaran, S.M.; Ayele, H.F. Determinants of value added tax on revenue administration using logit regression: An evidence from Ethiopia. Int. J. Intellect. Adv. Res. Eng. Comput. 2019, 7, 308–319. [Google Scholar]

- Mebratu, A.A. Impact of Tax Audit on Improving Taxpayers Compliance: Emperical Evidence from Ethiopian Revenue Authority at Federal Level. Int. J. Account. Res. 2016, 2, 1–19. [Google Scholar] [CrossRef]

- Lin, B.; Jia, Z. Tax rate, government revenue and economic performance: A perspective of Laffer curve. China Econ. Rev. 2019, 56, 101307. [Google Scholar] [CrossRef]

- Ndubula, E.; Matiku, E. The Effects of Tax Education on Government Revenue Collection: The Case of Small and Medium Enterprises in Morogoro Municipality, Tanzania. J. Econ. Manag. Trade 2021, 27, 28–41. [Google Scholar] [CrossRef]

- Night, S.; Bananuka, J. The mediating role of adoption of an electronic tax system in the relationship between attitude towards electronic tax system and tax compliance. J. Econ. Financ. Adm. Sci. 2019, 25, 73–88. [Google Scholar] [CrossRef]

- Abshari, Z.; Jenkins, G.P.; Kuo, C.-Y.; Shahee, M. Progressive Taxation versus Progressive Targeted Transfers in the Design of a Sustainable Value Added Tax System. Sustainability 2021, 13, 11165. [Google Scholar] [CrossRef]

- Lin, S. China’s value-added tax reform, capital accumulation, and welfare implications. China Econ. Rev. 2008, 19, 197–214. [Google Scholar] [CrossRef]

- Gashaw, A.; Ayalsew, M. A Study on Tax Evasion and Avoidance in Ethiopia: The Case of Ethiopian Revenue and Customs Authority Bahir Dar Branch. Res. J. Financ. Account. 2019, 10, 52–63. [Google Scholar]

- Folayan, D.O.; Adeniyi, A. Effects of Tax Evasion on Government Revenue Generation in OYO State, Nigeria. Eur. J. Account. Audit. Financ. Res. 2018, 1, 76–89. [Google Scholar]

- Gerard, F.; Naritomi, J. Value Added Tax in Developing Countries: Lessons from Recent Research; IGC Growth Brief Series 015; International Growth Centre: London, UK, 2018. [Google Scholar]

- Olaoye, C.O.; Ogundipe, A.A. Application of Tax Audit and Investigation on Tax Evasion Control in Nigeria. J. Account. Financ. Audit. Stud. 2018, 4, 79–92. [Google Scholar]

- Adebisi, J.F.; Gbegi, D.O. Effect of Tax Avoidance and Tax Evasion on Personal Income Tax Administration in Nigeria. Am. J. Humanit. Soc. Sci. 2013, 1, 125–134. [Google Scholar] [CrossRef]

- Mengistu, A.T.; Molla, K.G.; Mascagni, G. Trade Tax Evasion and the Tax Rate: Evidence from Transaction-level Trade Data. J. Afr. Econ. 2022, 31, 94–122. [Google Scholar] [CrossRef]

- Shen, X.; Chen, B.; Leibrecht, M.; Du, H. The Moderating Effect of Perceived Policy Effectiveness in Residents’ Waste Classification Intentions: A Study of Bengbu, China. Sustainability 2022, 14, 801. [Google Scholar] [CrossRef]

- Lucas-Mas, C.Ó.; Junquera-Varela, R.F. Tax Theory Applied to the Digital Economy: A Proposal for a Digital Data Tax and a Global Internet Tax Agency; International Bank for Reconstruction and Development, The World Bank: Washington, DC, USA, 2021. [Google Scholar]

- African Tax Institute. VAT in Africa 2008; Pretoria University Law Press (PULP): South Africa, Pritoria, 2008. [Google Scholar]

- Ufier, A. Quasi-experimental analysis on the effects of adoption of a value added tax. Econ. Inq. 2014, 52, 1364–1379. [Google Scholar] [CrossRef]

- Madina, S.; Lyazzat, S.; Kuralay, B.; Gulzhan, A.; Aliya, S.; Anar, K. Tax Revenues Estimation and Forecast for State Tax Audit. Entrep. Sustain. Issues 2020, 7, 2419–2435. [Google Scholar]

- Bikas, E.; Bagotyrius, G.; Jakubauskaitė, A. The impact of value-added tax on the fiscal sustainability. J. Secur. Sustain. Issues 2017, 7, 19. [Google Scholar] [CrossRef]

- Wang, J.; Shen, G.; Tang, D. Does tax deduction relax financing constraints? Evidence from China’s value-added tax reform. China Econ. Rev. 2021, 67, 101619. [Google Scholar] [CrossRef]

- Yesegat, W. Value added tax in Ethiopia: A study of operating costs and compliance. Int. J. Bus. Manag. 2009, 4, 419. [Google Scholar]

- Hayes, R.; Dassen, R.; Schilder, A.; Wallage, P. An Introduction to International Standards on Auditing, 2nd ed.; Prentice Hall, Financial Times: Amsterdam, The Netherlands, 1999. [Google Scholar]

- Sattar, U.; Javeed, S.A.; Latief, R. How Audit Quality Affects the Firm Performance with the Moderating Role of the Product Market Competition: Empirical Evidence from Pakistani Manufacturing Firms. Sustainability 2020, 12, 4153. [Google Scholar] [CrossRef]

- Jordaan, Y.; Schoeman, N.J. The benefit of aligning South Africa’s personal income tax thresholds and brackets with that of its peers using a micro-simulation tax model. S. Afr. J. Econ. Manag. Sci. 2018, 21, 9. [Google Scholar] [CrossRef]

- Kassa, E.T. Factors influencing taxpayers to engage in tax evasion: Evidence from Woldia City administration micro, small, and large enterprise taxpayers. J. Innov. Entrep. 2021, 10, 8. [Google Scholar] [CrossRef]

- Kowal, A.; Przekota, G. VAT Efficiency—A Discussion on the VAT System in the European Union. Sustainability 2021, 13, 4768. [Google Scholar] [CrossRef]

- Krzikallová, K.; Tošenovský, F. Is the Value Added Tax System Sustainable? The Case of the Czech and Slovak Republics. Sustainability 2020, 12, 4925. [Google Scholar] [CrossRef]

- Onuoha, L.N.; Dada, S.O. Tax audit and investigation as imperatives for efficient Tax Administration in Nigeria. J. Bus. Adm. Manag. Sci. Res. 2016, 5, 66–76. [Google Scholar]

- Gomb, M.; Vagask, A.; Štefan, T. Analytical View on the Sustainable Development of Tax and Customs Administration in the Context of Selected Groups of the Population of the Slovak Republic. Sustainability 2022, 14, 1891. [Google Scholar] [CrossRef]

- Claus, I. Is the value added tax a useful macroeconomic stabilization instrument? Econ. Model. 2013, 30, 366–374. [Google Scholar] [CrossRef]

- Giesecke, J.A.; Nhi, T.H. Modelling value-added tax in the presence of multi-production and differentiated exemptions. J. Asian Econ. 2010, 21, 156–173. [Google Scholar] [CrossRef][Green Version]

- Kleanthous, C.; Chatzis, S. Gated Mixture Variational Autoencoders for Value Added Tax audit case selection. Knowl.-Based Syst. 2019, 188, 105048. [Google Scholar] [CrossRef]

- Desalegn, G. Effects of Tax Audit on Revenue Collection Performance in Ethiopia:Evidence from ERCA Large Taxpayers’ Branch Office. Res. J. Financ. Account. 2020, 11, 1–10. [Google Scholar] [CrossRef]

- Li, T.; Yang, L. The Effects of Tax Reduction and Fee Reduction Policies on the Digital Economy. Sustainability 2021, 13, 7611. [Google Scholar] [CrossRef]

- Tamrie, W.; Gebregziabhere, G.; Gezae, A. Perceptions of Value Added Tax Filing and Invoicing Compliance in Ethiopia: The Case of Three Federal Branch Offices in Addis Ababa; African Tax Administration: Brighton, UK, 2019. [Google Scholar]

- Mohammed, M.; Tinsae, F. Implementation of VAT in Ethiopia: Critical Assessment of the Practice in Jigjiga Town. J. Law Policy Glob. 2017, 59, 125–133. [Google Scholar]

- Chan, C.W.; Troutman, C.S.; O’Bryan, D. An expanded model of taxpayer compliance: Empirical evidence from the United States and Hong Kong. J. Int. Account. Audit. Tax. 2000, 9, 83–103. [Google Scholar] [CrossRef]

- Mbilla, A.S.E.; Abiire, M.A.; Atindaana, P.A.; Ayimpoya, R.N. Tax Education and Tax Compliance In Ghana. Res. J. Account 2020, 8, 1–22. [Google Scholar]

- Tebebu, W.S.; Yitbarek, M.C. Implementation of Value Added Tax and Its Challenges: Evidence from Bench Sheko Zone, SNNPR, Ethiopia. J. Account. Financ. Audit. Stud. 2020, 6, 49–65. [Google Scholar]

- Mascagni, G.; Santoro, F. African Tax Administration Paper 1 What is the Role of Taxpayer Education in Africa? The Institute of Development Studies: Brighton, UK, 2018. [Google Scholar]

- Podik, I.I.; Shtuler, I.Y.; Gerasymchuk, N.A. The Comparative Analysis of Tax Audit Files. In Financial and Credit Activity Problems of Theory and Practice; University of Banking of the National Bank of Ukraine: Kyiv, Ukraine, 2019; pp. 147–156. [Google Scholar]

- Badra, M.S. The Effect of Tax Audit on Tax Compliance in Nigeria (A Study of Bauchi State Board of Internal Revenue). Res. J. Financ. Account. 2012, 3, 74–81. [Google Scholar]

- Jerene, W. Challenges of Value Added Tax (VAT) Collection Performance: A Case Study of Hawassa City Revenue Authority (South Ethiopia). Int. J. Bus. Manag. 2016, 4, 13–19. [Google Scholar]

- Barrios, S.; D’Andria, D.; Gesualdo, M. Reducing tax compliance costs through corporate tax base harmonization in the European Union. J. Int. Account. Audit. Tax. 2020, 41, 100355. [Google Scholar] [CrossRef]

- Kopeć, K. Reduced Value Added Tax (VAT) Rate on Books as a Tool of Indirect Public Funding in the Cultural Sector. Sustainability 2020, 12, 5590. [Google Scholar] [CrossRef]

- Helcmanovsk, M.; Andrejovsk, A. Tax Rates and Tax Revenues in the Context of Tax Competitiveness. J. Risk Financ. Manag. 2021, 14, 284. [Google Scholar] [CrossRef]

- Ferreira-Lopes, A.; Martins, L.F.; Espanhol, R. The relationship between tax rates and tax revenues in eurozone member countries-exploring the Laffer curve. Bull. Econ. Res. 2019, 72, 121–145. [Google Scholar] [CrossRef]

- Roos, E.L.; Horridge, J.M.; Van Heerden, J.H.; Adams, P.D.; Bohlmann, H.R.; Kobe, K.K.; Vumbukani-Lepolesa, B. National and Regional Impacts of an Increase in Value-Added Tax: A CGE Analysis for South Africa. S. Afr. J. Econ. 2019, 88, 90–120. [Google Scholar] [CrossRef]

- Bonu, N.S.; Motau, P. The impact of income tax rates (ITR) on the economic development of Botswana. J. Account. Tax. 2009, 1, 8–22. [Google Scholar]

- Sarwar, S.; Streimikiene, D.; Waheed, R.; Dignah, A.; Mikalauskiene, A. Does the Vision 2030 and Value Added Tax Leads to Sustainable Economic Growth: The Case of Saudi Arabia? Sustainability 2021, 13, 11090. [Google Scholar] [CrossRef]

- Asiedu, J.; Akanyonge, J.; Dickson, D.; Asapeo, A. The Influence of VAT Flat Rate Scheme on Tax Revenue in the Weija VAT Sub Office in Accra, Ghana. Acad. Lett. 2022, 4759, 1–6. [Google Scholar] [CrossRef]

- Mach, P. VAT Rates and their Impact on Business and Tax Revenue. Eur. Res. Stud. J. 2018, 21, 144–152. [Google Scholar] [CrossRef][Green Version]

- Tesema, G.; Teklu, K. Risk Based Tax Audit Practices in Ethiopia, Evidence from Western Addis Ababa Small Taxpayers Branch Office. Eur. J. Bus. Manag. 2020, 12, 40–47. [Google Scholar]

- Otekunrin, A.O.; Nwanji, T.I.; Eluyela, D.F.; Inegbedion, H.; Eleda, T. E-tax system effectiveness in reducing tax evasion in Nigeria. Probl. Perspect. Manag. 2021, 19, 175–185. [Google Scholar] [CrossRef]

- Argilés-Bosch, J.M.; Somoza, A.; Ravenda, D.; García-Blandón, J. An empirical examination of the influence of e-commerce on tax avoidance in Europe. J. Int. Account. Audit. Tax. 2020, 41, 100339. [Google Scholar] [CrossRef]

- Daniel, A.M.; Esther, I.O. Electronic Taxation and Tax Compliance Among Some Selected Fast Food Restaurants in Lagos State, Nigeria (Tax Payers Perspective). Eur. J. Account. Audit. Financ. Res. 2019, 7, 52–80. [Google Scholar]

- Azmi, A.; Sapiei, N.S.; Mustapha, M.Z.; Abdullah, M. SMEs’ tax compliance costs and IT adoption: The case of a value-added tax. Int. J. Account. Inf. Syst. 2016, 23, 1–13. [Google Scholar] [CrossRef]

- Allahverdi, M.; Alagöz, A.; Ortakarpuz, M. The Effect of E-taxation System on Tax Revenues and Costs: Turkey Case The Effect Of E-Taxation System On Tax Revenues And Costs: Turkey Case. In Proceedings of the International Conference on Accounting Studies (ICAS) 2017, Putrajaya, Malaysia, 18–20 September 2017; Volume 8, pp. 123–142. [Google Scholar]

- Gwaro, O.T.; Maina, K.; Kwasira, J. Influence of Online Tax Filing on Tax Compliance among Small and Medium Enterprises in Nakuru Town, Kenya. IOSR J. Bus. Manag. 2016, 18, 82–92. [Google Scholar] [CrossRef]

- Manaye, M.K. Collection of Vat Using Cash Register Machines in Wolaita Sodo Town: Reflection Of Challenging Factors. Int. J. Econ. Manag. Stud. 2019, 6, 230–240. [Google Scholar] [CrossRef]

- Eilu, E. Adoption of Electronic Fiscal Devices (EFDs) for Value-Added Tax (VAT) Collection in Kenya and Tanzania: A Systematic Review. Afr. J. Inf. Commun. 2018, 22, 111–134. [Google Scholar] [CrossRef]

- Burian, P.E.; Rogerson, L.; Iii, F.S.M. The Research Roadmap: A Primer to the Approach and Process. Contemp. Issues Educ. Res. (CIER) 2010, 3, 43–58. [Google Scholar] [CrossRef]

- Annuar, H.A.; Isa, K.; Ibrahim, S.A.; Solarin, S.A. Malaysian corporate tax rate and revenue: The application of Ibn Khaldun tax theory. ISRA Int. J. Islam. Financ. 2018, 10, 251–262. [Google Scholar] [CrossRef]

- Miki, B. The Effect of the VAT Rate Change on Aggregate Consumption and Economic Growth; Columbia University: New York, NY, USA, 2011. [Google Scholar]

- Mukhlis, I.; Utomo, S.H.; Soesetio, Y. The Role of Taxation Education on Taxation Knowledge and Its Effect on Tax Fairness as well as Tax Compliance on Handicraft SMEs Sectors in Indonesia. Int. J. Financ. Res. 2015, 6, 161–169. [Google Scholar] [CrossRef]

- Krejcie, R.V.; Morgan, D.W. Determining Sample Size for Research Activities. Educ. Psychol. Meas. 1970, 30, 607–610. [Google Scholar] [CrossRef]

- Harelimana, J.B. Effect of Tax Audit on Revenue Collection in Rwanda. Glob. J. Manag. Bus. Res. D Account. Audit. 2018, 18, 12. [Google Scholar]

- Akintoye, R.I.; Onuoha, L.N. Tax Revenue Sustainability: The Role of Tax Education and Enlightenment. Res. J. Financ. Account. 2019, 10, 40–52. [Google Scholar] [CrossRef]

- Onuoha, L.N.; Akintoye, I.R.; Oyedokun, G.E. Role of Tax Education and Enlightenment on Tax Revenue Growth in Nigeria. J. Tax. Econ. Dev. 2019, 18, 104–127. [Google Scholar]

- Mas’ud, A.; Aliyu, A.A.; Gambo, E.-M.J. Tax Rate and Tax Compliance in Africa. Eur. J. Account. Audit. Financ. Res. 2014, 2, 22–30. [Google Scholar]

- Le, H.T.D.; Bui, M.T.; Nguyen, G.T.C. Factors Affecting Electronic Tax Compliance of Small and Medium Enterprises in Vietnam. J. Asian Financ. Econ. Bus. 2021, 8, 823–832. [Google Scholar]

- Tavakol, M.; Dennick, R. Making sense of Cronbach’s alpha. Int. J. Med. Educ. 2011, 2, 53–55. [Google Scholar] [CrossRef]

- Taber, K.S. The Use of Cronbach’s Alpha When Developing and Reporting Research Instruments in Science Education. Res. Sci. Educ. 2018, 48, 1273–1296. [Google Scholar] [CrossRef]

- Kano, Y. Selection of Manifest Variables; Elsevier: Amsterdam, The Netherlands, 2007; Volume 1, p. 6. [Google Scholar]

- Aguirre-Urreta, M.I.; Marakas, G.M.; Ellis, M.E. Measurement of composite reliability in research using partial least squares: Some issues and an alternative approach. Data Base Adv. Inf. Syst. 2013, 44, 11–43. [Google Scholar] [CrossRef]

- dos Santos, P.M.; Cirillo, M. Construction of the average variance extracted index for construct validation in structural equation models with adaptive regressions. Commun. Stat.-Simul. Comput. 2021, 1–13. [Google Scholar] [CrossRef]

- Samuels, P. Pearson Correlation. Statstutor Community Project. 2015. Available online: https://www.researchgate.net/publication/274635640 (accessed on 12 July 2019).

- di Leo, G.; Sardanelli, F. Statistical significance: P value, 0.05 threshold, and applications to radiomics—reasons for a conservative approach. Eur. Radiol. Exp. 2020, 4, 1. [Google Scholar] [CrossRef]

- Takemura, K. Decision strategies and bad group decision-making: A group meeting experiment. ScienceDirect 2021, 1140, 1–21. [Google Scholar]

- Gunzler, D.; Chen, T.; Wu, P.; Zhang, H. Introduction to mediation analysis with structural equation modeling. Shanghai Arch. Psychiatry 2013, 25, 390–394. [Google Scholar] [CrossRef]

- Yay, M. The Mediation Analysis with The Sobel Test and the Percentile Bootstrap. Int. J. Manag. Appl. Sci. 2017, 3, 2. [Google Scholar]