Market-Specific Barriers and Enablers for Organizational Investments in Solar PV—Lessons from Flanders

Abstract

:1. Introduction

- Non-owner residential markets: including social and private rental housing, and collective housing (where residents only partially own the building they live in). These market segments have in common that third parties, such as social housing associations, landlords, or associations of co-owners, are involved in the decision-making process.

- Public and social infrastructure: including municipalities, schools, and health and social care facilities. These market segments have the production of (quasi-) public goods, public procurement procedures, and not-for-profit objectives in common.

- Companies and commercial real estate. These market segments share the commercial function of the infrastructure they invest in.

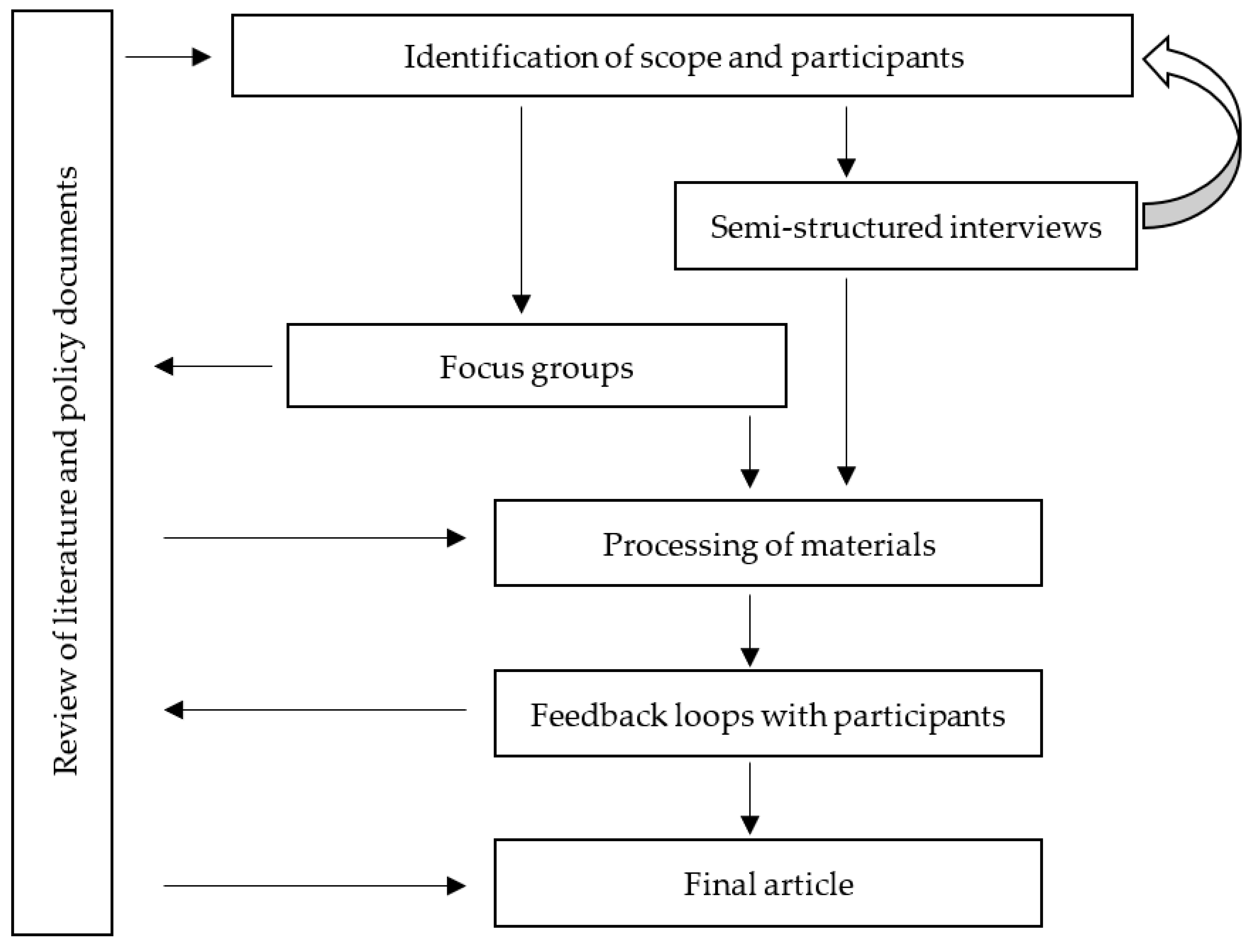

2. Materials and Methods

3. Results

3.1. PV Policy in Flanders

3.2. Non-Homeowner Residential Markets

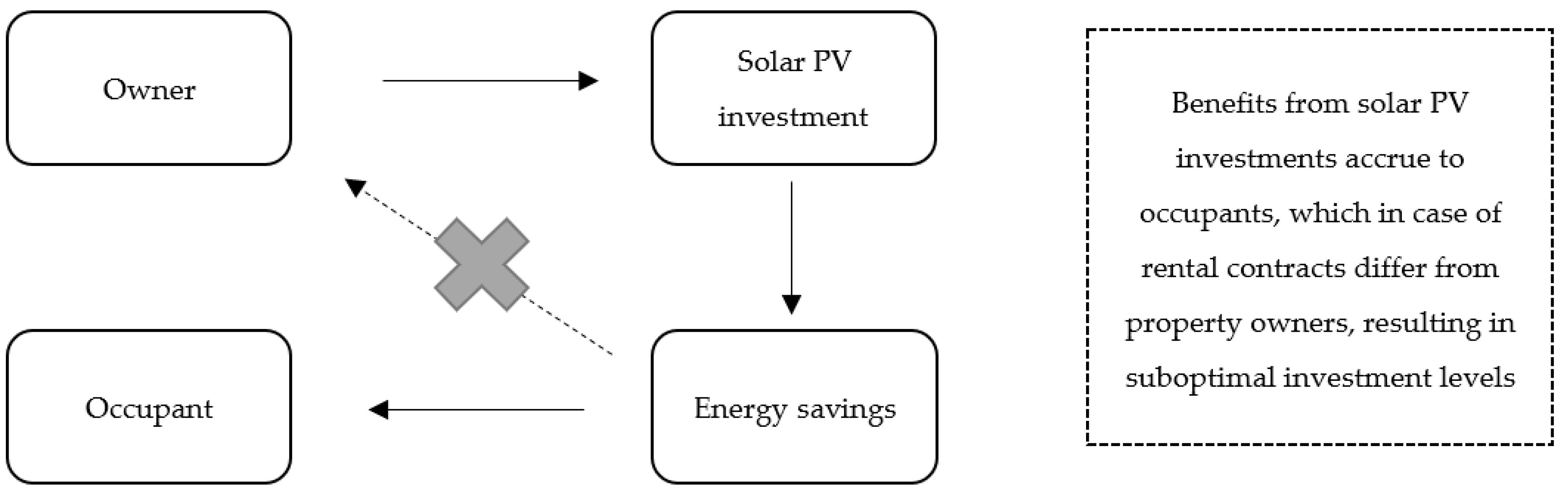

- Landlords buy and supply potentially energy efficient homes, but their incentive is to supply these at the lowest possible cost, because they do not pay the energy or utility bills. Tenants pay the energy bills, and have high incentives to increase efficiency, but no control over the means to do so.

- Except for fixed-term rental contracts, landlords have no idea about how long tenants will reside in their houses. Due to the probability of a tenant moving soon, an investment in efficiency having a high upfront capital cost is risky. This is called the temporal split incentive.

3.2.1. Social Rental Housing

3.2.2. Private Rental Housing

3.2.3. Collective Housing

3.3. Public, Educational, and Social Infrastructure

3.3.1. Public Authorities

3.3.2. Schools

3.3.3. Health and Social Care

3.4. Companies and Commercial Real Estate

3.4.1. Companies

3.4.2. Commercial Real Estate

4. Discussion

4.1. Barriers and Enablers

4.2. Limitations and Avenues for Further Research

5. Conclusions and Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| AGION | Flemish Agency for School Infrastructure |

| CAPEX | Capital Expenditures |

| DSO | Distribution System Operator |

| EEF | Energy Efficiency Fund |

| ESCO | Energy Service Company |

| ESG | Environmental, Social and Governance |

| EV | Electrical Vehicle |

| HVAC | Heating, Ventilation, and Air Conditioning |

| MaaS | Monitoring-as-a-Service |

| MIG | Market Implementation Guide |

| OECD | Organization for Economic Cooperation and Development |

| PPA | Power Purchasing Agreement |

| PSS | Product-Service-System |

| PV | Photovoltaic |

| SDG | Sustainable Development Goals |

| TGC | Tradeable Green Current |

| TPO | Third-Party Ownership |

| VEB | Flemish Energy Services Company |

| VIPA | Flemish Infrastructure Fund for Person-related Matters |

Appendix A

Appendix A.1. Respondents

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| ID | Date | Stakeholder Type |

|---|---|---|

| Respondent 1 | 19/11/2021 | Service provider 1 |

| Respondent 2 | 2/12/2021 | Service provider 2 |

| Respondent 3 | 2/12/2021 | Researcher 1 |

| Respondents 4 & 5 | 2/12/2021 | Federation of service providers |

| Respondent 6 | 6/12/2021 | Service provider 2 |

| Respondent 7 | 7/12/2021 | Service provider 3 |

Appendix A.2. Interview Structure

- Given the list of participants we identified already, which participants should we not forget to invite or include?

- What key questions would you like to ask to these focus group participants, if you had the chance to do so?

- Which relevant cases should we know to prepare this focus group?

Appendix B

| ID | Professional Position | Stakeholder Type |

|---|---|---|

| Participant 1.1 | Energy expert | Federation of municipalities |

| Participant 1.2 | PV expert | Public procurement agency on renewable energy |

| Participant 1.3 | Sustainable infrastructure expert | Supporting association for health & social care facilities and schools |

| Participant 1.4 | Energy expert | Governmental agency for school infrastructure |

| Participant 1.5 | Energy expert | Regional federation of schools |

| Participant 1.6 | Investment manager | Governmental investment company |

| Participant 1.7 | Public finance expert | Bank |

| ID | Professional Position | Stakeholder Type |

|---|---|---|

| Participant 2.1 | Policy expert | Association of social rental housing |

| Participant 2.2 | Operational manager | Energy co-operative of social housing associations |

| Participant 2.3 | CEO | Association of tenants |

| Participant 2.4 | CEO | Association of landlords |

| Participant 2.5 | Social Worker | Civil Society project organization |

| Participant 2.6 | President of the Board of Directors | Association for housing for vulnerable households |

| Participant 2.7 | Energy Expert | Environmental civil society organization |

| ID | Professional Position | Stakeholder Type |

|---|---|---|

| Participant 3.1 | Circular Economy expert | Employer federation |

| Participant 3.2 | Circular Economy expert | Employer federation |

| Participant 3.3 | Energy expert | Federation of farmers |

| Participant 3.4 | Innovation expert | Construction federation |

| Participant 3.5 | Innovation expert | Real estate study center |

Appendix C

References

- IEA. World Energy Outlook 2021; IEA: Paris, France, 2021. [Google Scholar]

- Global Solar Council Solar Power Lights the Way towards the SDGs with Broad Benefits for Green Recovery Plans. Available online: https://www.pv-magazine.com/press-releases/solar-power-lights-the-way-towards-the-sdgs-with-broad-benefits-for-green-recovery-plans/ (accessed on 31 August 2022).

- European Commission Energy and the Green Deal. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal/energy-and-green-deal_en#actions (accessed on 31 August 2022).

- European Commission REPowerEU: Affordable, Secure and Sustainable Energy for Europe. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal/repowereu-affordable-secure-and-sustainable-energy-europe_en#clean-energy (accessed on 31 August 2022).

- de Frutos Cachorro, J.; Willeghems, G.; Buysse, J. Strategic Investment Decisions under the Nuclear Power Debate in Belgium. Resour. Energy Econ. 2019, 57, 156–184. [Google Scholar] [CrossRef] [Green Version]

- De Groote, O.; Gautier, A.; Verboven, F. The Political Economy of Financing Climate Policy—Evidence from the Solar Pv Subsidy Programs. Soc. Sci. Res. Netw. 2022. Available online: https://ssrn.com/abstract=4119431 (accessed on 30 August 2022). [CrossRef]

- Palm, A. Early Adopters and Their Motives: Differences between Earlier and Later Adopters of Residential Solar Photovoltaics. Renew. Sustain. Energy Rev. 2020, 133, 110142. [Google Scholar] [CrossRef]

- Schulte, E.; Scheller, F.; Sloot, D.; Bruckner, T. A Meta-Analysis of Residential PV Adoption: The Important Role of Perceived Benefits, Intentions and Antecedents in Solar Energy Acceptance. Energy Res. Soc. Sci. 2022, 84, 102339. [Google Scholar] [CrossRef]

- Bird, S.; Hernández, D. Policy Options for the Split Incentive: Increasing Energy Efficiency for Low-Income Renters. Energy Policy 2012, 48, 506–514. [Google Scholar] [CrossRef] [Green Version]

- Boccard, N.; Gautier, A. Solar Rebound: The Unintended Consequences of Subsidies. Energy Econ. 2021, 100, 105334. [Google Scholar] [CrossRef]

- Verbruggen, A.; Laes, E. Early European Experience with Tradable Green Certificates Neglected by EU ETS Architects. Environ. Sci. Policy 2021, 119, 66–71. [Google Scholar] [CrossRef]

- Tukker, A.; Tischner, U. Product-Services as a Research Field: Past, Present and Future. Reflections from a Decade of Research. J. Clean. Prod. 2006, 14, 1552–1556. [Google Scholar] [CrossRef]

- Kokchang, K.; Tongsopit, S.; Junlakarn, S.; Wibulpolprasert, W.; Tossabanyad, M. Stakeholders’ Perspectives of Design Options for a Rooftop Solar PV Self-Consumption Scheme in Thailand. Appl. Environ. Res. 2018, 40, 42–54. [Google Scholar] [CrossRef]

- Lee, J.; Shepley, M.M. Benefits of Solar Photovoltaic Systems for Low-Income Families in Social Housing of Korea: Renewable Energy Applications as Solutions to Energy Poverty. J. Build. Eng. 2020, 28, 101016. [Google Scholar] [CrossRef]

- Hyder, F.; Sudhakar, K.; Mamat, R. Solar PV Tree Design: A Review. Renew. Sustain. Energy Rev. 2018, 82, 1079–1096. [Google Scholar] [CrossRef]

- Chen, C.; Li, J.; Shuai, J.; Nelson, H.; Walzem, A.; Cheng, J. Linking Social-Psychological Factors with Policy Expectation: Using Local Voices to Understand Solar PV Poverty Alleviation in Wuhan, China. Energy Policy 2021, 151, 112160. [Google Scholar] [CrossRef]

- Powell, J.W.; Welsh, J.M.; Pannell, D.; Kingwell, R. Factors Influencing Australian Sugarcane Irrigators’ Adoption of Solar Photovoltaic Systems for Water Pumping. Clean. Eng. Technol. 2021, 4, 100248. [Google Scholar] [CrossRef]

- Urmee, T.; Harries, D. A Survey of Solar PV Program Implementers in Asia and the Pacific Regions. Energy Sustain. Dev. 2009, 13, 24–32. [Google Scholar] [CrossRef]

- Flemish Government Solar PV in Flanders. Available online: https://www.lexology.com/library/detail.aspx?g=5c9e553e-5017-4f62-912f-38a707fe8574 (accessed on 31 August 2022).

- Eurostat Renewable Energy Statistics. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Renewable_energy_statistics (accessed on 31 August 2022).

- Stam, V. Solar Energy Policy Transitions in Flanders, Belgium. Master’s Thesis, Cardiff University, Wales, UK, Radboud University, Nijmegen, The Netherlands, 2018. [Google Scholar]

- Verbruggen, A. Tradable Green Certificates in Flanders (Belgium). Energy Policy 2004, 32, 165–176. [Google Scholar] [CrossRef]

- Bauwens, T. Analyzing the Determinants of the Size of Investments by Community Renewable Energy Members: Findings and Policy Implications from Flanders. Energy Policy 2019, 129, 841–852. [Google Scholar] [CrossRef]

- De Groote, O.; Pepermans, G.; Verboven, F. Heterogeneity in the Adoption of Photovoltaic Systems in Flanders. Energy Econ. 2016, 59, 45–57. [Google Scholar] [CrossRef] [Green Version]

- De Groote, O.; Verboven, F. Subsidies and Time Discounting in New Technology Adoption: Evidence from Solar Photovoltaic Systems. Am. Econ. Rev. 2019, 109, 2137–2172. [Google Scholar] [CrossRef]

- Engelken, M.; Römer, B.; Drescher, M.; Welpe, I.M.; Picot, A. Comparing Drivers, Barriers, and Opportunities of Business Models for Renewable Energies: A Review. Renew. Sustain. Energy Rev. 2016, 60, 795–809. [Google Scholar] [CrossRef]

- Jacksohn, A.; Grösche, P.; Rehdanz, K.; Schröder, C. Drivers of Renewable Technology Adoption in the Household Sector. Energy Econ. 2019, 81, 216–226. [Google Scholar] [CrossRef]

- Rai, V.; Reeves, D.C.; Margolis, R. Overcoming Barriers and Uncertainties in the Adoption of Residential Solar PV. Renew. Energy 2016, 89, 498–505. [Google Scholar] [CrossRef]

- Wolske, K. More Alike than Different: Profiles of High-Income and Low-Income Rooftop Solar Adopters in the United States. Energy Res. Soc. Sci. 2020, 63, 101399. [Google Scholar] [CrossRef]

- Wolske, K.S.; Stern, P.C.; Dietz, T. Explaining Interest in Adopting Residential Solar Photovoltaic Systems in the United States: Toward an Integration of Behavioral Theories. Energy Res. Soc. Sci. 2017, 25, 134–151. [Google Scholar] [CrossRef]

- Drury, E.; Miller, M.; Macal, C.; Graziano, D.; Heimiller, D.; Ozik, J.; Perry, T. The Transformation of Southern California’s Residential Photovoltaics Market through Third-Party Ownership. Energy Policy 2012, 42, 681–690. [Google Scholar] [CrossRef]

- Överholm, H. Alliance Formation by Intermediary Ventures in the Solar Service Industry: Implications for Product–Service Systems Research. J. Clean. Prod. 2017, 140, 288–298. [Google Scholar] [CrossRef]

- Överholm, H. Spreading the Rooftop Revolution: What Policies Enable Solar-as-a-Service? Energy Policy 2015, 84, 69–79. [Google Scholar] [CrossRef]

- Rai, V.; Sigrin, B. Diffusion of Environmentally-Friendly Energy Technologies: Buy versus Lease Differences in Residential PV Markets. Environ. Res. Lett. 2013, 8, 14022. [Google Scholar] [CrossRef]

- Hoppe, T. Adoption of Innovative Energy Systems in Social Housing: Lessons from Eight Large-Scale Renovation Projects in The Netherlands. Energy Policy 2012, 51, 791–801. [Google Scholar] [CrossRef]

- Heylen, K.; Vanderstraeten, L. Wonen in Vlaanderen Anno 2018; Gompel & Svacina: Antwerp, Belgium, 2019; ISBN 978-94-6371-140-1. [Google Scholar]

- Winters, S.; Van den Broeck, K. Social Housing in Flanders: Best Value for Society from Social Housing Associations or Social Rental Agencies? Hous. Stud. 2022, 37, 605–623. [Google Scholar] [CrossRef]

- McCabe, A.; Pojani, D.; van Groenou, A.B. Social Housing and Renewable Energy: Community Energy in a Supporting Role. Energy Res. Soc. Sci. 2018, 38, 110–113. [Google Scholar] [CrossRef]

- McCabe, A.; Pojani, D.; van Groenou, A.B. The Application of Renewable Energy to Social Housing: A Systematic Review. Energy Policy 2018, 114, 549–557. [Google Scholar] [CrossRef]

- Pinto, J.T.M.; Amaral, K.J.; Janissek, P.R. Deployment of Photovoltaics in Brazil: Scenarios, Perspectives and Policies for Low-Income Housing. Sol. Energy 2016, 133, 73–84. [Google Scholar] [CrossRef]

- Sdei, A.; Gloriant, F.; Tittelein, P.; Lassue, S.; Hanna, P.; Beslay, C.; Gournet, R.; McEvoy, M. Social Housing Retrofit Strategies in England and France: A Parametric and Behavioural Analysis. Energy Res. Soc. Sci. 2015, 10, 62–71. [Google Scholar] [CrossRef]

- Sunikka-Blank, M.; Chen, J.; Britnell, J.; Dantsiou, D. Improving Energy Efficiency of Social Housing Areas: A Case Study of a Retrofit Achieving an “A” Energy Performance Rating in the UK. Eur. Plan. Stud. 2012, 20, 131–145. [Google Scholar] [CrossRef]

- Teso, L.; Carnieletto, L.; Sun, K.; Zhang, W.; Gasparella, A.; Romagnoni, P.; Zarrella, A.; Hong, T. Large Scale Energy Analysis and Renovation Strategies for Social Housing in the Historic City of Venice. Sustain. Energy Technol. Assess. 2022, 52, 102041. [Google Scholar] [CrossRef]

- Agbonaye, O.; Keatley, P.; Huang, Y.; Bani-Mustafa, M.; Ademulegun, O.O.; Hewitt, N. Value of Demand Flexibility for Providing Ancillary Services: A Case for Social Housing in the Irish DS3 Market. Util. Policy 2020, 67, 101130. [Google Scholar] [CrossRef]

- Bahaj, A.S.; James, P.A.B. Urban Energy Generation: The Added Value of Photovoltaics in Social Housing. Renew. Sustain. Energy Rev. 2007, 11, 2121–2136. [Google Scholar] [CrossRef]

- Guazzi, G.; Bellazzi, A.; Meroni, I.; Magrini, A. Refurbishment Design through Cost-Optimal Methodology: The Case Study of a Social Housing in the Northern Italy. Int. J. Heat Technol. 2017, 35, S336–S344. [Google Scholar] [CrossRef]

- Pintanel, M.T.; Martínez-Gracia, A.; Uche, J.; del Amo, A.; Bayod-Rújula, Á.A.; Usón, S.; Arauzo, I. Energy and Environmental Benefits of an Integrated Solar Photovoltaic and Thermal Hybrid, Seasonal Storage and Heat Pump System for Social Housing. Appl. Therm. Eng. 2022, 213, 118662. [Google Scholar] [CrossRef]

- Coates, A.; Van Opstal, W. The Joys and Burdens of Multiple Legal Frameworks for Social Entrepreneurship—Lessons from the Belgian Case; Social Science Research Network: Rochester, NY, USA, 2009. [Google Scholar]

- Huybrechts, B.; Mertens, S. The Relevance of the Cooperative Model in the Field of Renewable Energy. Ann. Public Coop. Econ. 2014, 85, 193–212. [Google Scholar] [CrossRef]

- Best, R.; Burke, P.J.; Nepal, R.; Reynolds, Z. Effects of Rooftop Solar on Housing Prices in Australia. Aust. J. Agric. Resour. Econ. 2021, 65, 493–511. [Google Scholar] [CrossRef]

- Best, R.; Esplin, R.; Hammerle, M.; Nepal, R.; Reynolds, Z. Do Solar Panels Increase Housing Rents in Australia? Hous. Stud. 2021, 1–18. [Google Scholar] [CrossRef]

- Chegut, A.; Eichholtz, P.; Holtermans, R.; Palacios, J. Energy Efficiency Information and Valuation Practices in Rental Housing. J. Real Estate Financ. Econ. 2020, 60, 181–204. [Google Scholar] [CrossRef] [Green Version]

- Nelson, T.; McCracken-Hewson, E.; Sundstrom, G.; Hawthorne, M. The Drivers of Energy-Related Financial Hardship in Australia—Understanding the Role of Income, Consumption and Housing. Energy Policy 2019, 124, 262–271. [Google Scholar] [CrossRef]

- Reames, T.G. Distributional Disparities in Residential Rooftop Solar Potential and Penetration in Four Cities in the United States. Energy Res. Soc. Sci. 2020, 69, 101612. [Google Scholar] [CrossRef]

- Sovacool, B.K.; Barnacle, M.L.; Smith, A.; Brisbois, M.C. Towards Improved Solar Energy Justice: Exploring the Complex Inequities of Household Adoption of Photovoltaic Panels. Energy Policy 2022, 164, 112868. [Google Scholar] [CrossRef]

- VREG Aantal Budgetmeters Met Actieve Stroombegrenzende Functie. Available online: https://dashboard.vreg.be/report/DMR_SODV%20DNB.html (accessed on 31 August 2022).

- Brankov, B.; Stanojević, A.; Nenković-Riznić, M.; Pucar, M. The Possibilities for Implementation of Photovoltaic Solar Panels in Multi-Family Housing Areas. In Proceedings of the 8th International Conference on Renewable Electrical Power Sources, Hong Kong, China, 7–8 December 2020; pp. 167–175. [Google Scholar]

- Komendantova, N.; Manuel Schwarz, M.; Amann, W. Economic and Regulatory Feasibility of Solar PV in the Austrian Multi-Apartment Housing Sector. AIMS Energy 2018, 6, 810–831. [Google Scholar] [CrossRef]

- Verhetsel, A.; Kessels, R.; Zijlstra, T.; Van Bavel, M. Housing Preferences among Students: Collective Housing versus Individual Accommodations? A Stated Preference Study in Antwerp (Belgium). J. Hous. Built Environ. 2017, 32, 449–470. [Google Scholar] [CrossRef]

- Vos, E.D.; Spoormans, L. Collective Housing in Belgium and the Netherlands: A Comparative Analysis. Urban Plan. 2022, 7, 336–348. [Google Scholar] [CrossRef]

- Flemish Government Algemene Cijfers over de Woningmarkt in Vlaanderen. Available online: https://www.wonenvlaanderen.be/woononderzoek-en-statistieken/algemene-cijfers-over-de-woningmarkt-vlaanderen (accessed on 30 August 2022).

- Flemish Government Nieuwe Woonvormen. Available online: https://www.vlaanderen.be/gemeenschappelijk-wonen-en-nieuwe-woonvormen (accessed on 31 August 2022).

- Ben-Al-Lal, I.; Gaukema, K.; Voets, T. Operational 2nd Life Solar Power System with Local Distribution Network Software System and User Feedback Tool at Waasland. 2020. Available online: https://joint-research-centre.ec.europa.eu/pvgis-photovoltaic-geographical-information-system_en (accessed on 30 August 2022).

- Helmig, B.; Jegers, M.; Lapsley, I. Challenges in Managing Nonprofit Organizations: A Research Overview. VOLUNTAS Int. J. Volunt. Nonprofit Organ. 2004, 15, 101–116. [Google Scholar] [CrossRef]

- VEB Over Ons. Available online: https://www.veb.be/over-ons (accessed on 31 August 2022).

- D’Adamo, I.; Falcone, P.M.; Gastaldi, M.; Morone, P. The Economic Viability of Photovoltaic Systems in Public Buildings: Evidence from Italy. Energy 2020, 207, 118316. [Google Scholar] [CrossRef]

- Grande-Acosta, G.K.; Islas-Samperio, J.M. Boosting Energy Efficiency and Solar Energy inside the Residential, Commercial, and Public Services Sectors in Mexico. Energies 2020, 13, 5601. [Google Scholar] [CrossRef]

- Silva, T.C.; Pinto, G.M.; de Souza, T.A.Z.; Valerio, V.; Silvério, N.M.; Coronado, C.J.R.; Guardia, E.C. Technical and Economical Evaluation of the Photovoltaic System in Brazilian Public Buildings: A Case Study for Peak and off-Peak Hours. Energy 2020, 190, 116282. [Google Scholar] [CrossRef]

- Pisman, A.; Vanacker, S.; Bieseman, H.; Vanongeval, L.; Van Steertegem, M.; Poelmans, L.; Van Dyck, K. Ruimterapport Vlaanderen 2021. Available online: https://www.vlaanderen.be/publicaties/ruimterapport-vlaanderen-rura-een-ruimtelijke-analyse-van-vlaanderen (accessed on 9 June 2022).

- Flemish Government Terra Patrimonium—En Energiedatabank Vlaanderen. Available online: https://www.vlaanderen.be/terra-patrimonium-en-energiedatabank-vlaanderen (accessed on 30 August 2022).

- Close, J. The Hong Kong Schools Solar Education Programme. Sol. Energy Mater. Sol. Cells 2003, 75, 739–749. [Google Scholar] [CrossRef]

- Gillani, A.A.; Khan, S.; Nasir, S.; Niaz, S. The Effectiveness of Installing Solar Panels at Schools in Pakistan to Increase Enrolment. J. Environ. Stud. Sci. 2022, 12, 505–514. [Google Scholar] [CrossRef]

- Mahmud, A.M. Evaluation of the Solar Hybrid System for Rural Schools in Sabah, Malaysia. In Proceedings of the 2010 IEEE International Conference on Power and Energy, Kuala Lumpur, Malaysia, 29 November–1 December 2010; pp. 628–633. [Google Scholar]

- Ciacci, C.; Banti, N.; Di Naso, V.; Bazzocchi, F. Evaluation of the Cost-Optimal Method Applied to Existing Schools Considering PV System Optimization. Energies 2022, 15, 611. [Google Scholar] [CrossRef]

- Korsavi, S.S.; Zomorodian, Z.S.; Tahsildoost, M. Energy and Economic Performance of Rooftop PV Panels in the Hot and Dry Climate of Iran. J. Clean. Prod. 2018, 174, 1204–1214. [Google Scholar] [CrossRef]

- Kolokotsa, D.; Vagias, V.; Fytraki, L.; Oungrinis, K. Energy Analysis of Zero Energy Schools: The Case Study of Child’s Asylum in Greece. Adv. Build. Energy Res. 2019, 13, 193–204. [Google Scholar] [CrossRef]

- Zeiler, W.; Boxem, G. Net-Zero Energy Building Schools. Renew. Energy 2013, 49, 282–286. [Google Scholar] [CrossRef]

- Shewbridge, C.; Fuster, M.; Rouw, R. Constructive Accountability, Transparency and Trust between Government and Highly Autonomous Schools in Flanders; OECD: Paris, France, 2019. [Google Scholar]

- Willems, T. Democratic Accountability in Public—Private Partnerships: The Curious Case of Flemish School Infrastructure. Public Adm. 2014, 92, 340–358. [Google Scholar] [CrossRef]

- AGION. Jaarverslag 2020. Available online: https://www.google.com.hk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&cad=rja&uact=8&ved=2ahUKEwin6p6Hltr6AhX0mlYBHWDMDtIQFnoECAsQAQ&url=https%3A%2F%2Fwww.agion.be%2Fsites%2Fdefault%2Ffiles%2Fimages%2FPDF_Jaarverslag2020.pdf&usg=AOvVaw2uDHNwofRchWhaz-Y8x1cD (accessed on 30 August 2022).

- Speidel, K. Solar Energy Utilization in Hospitals of Developing Countries. In Advances in Solar Energy Technology; Bloss, W.H., Pfisterer, F., Eds.; Pergamon: Oxford, UK, 1988; pp. 2745–2749. ISBN 978-0-08-034315-0. [Google Scholar]

- Olatomiwa, L.; Blanchard, R.; Mekhilef, S.; Akinyele, D. Hybrid Renewable Energy Supply for Rural Healthcare Facilities: An Approach to Quality Healthcare Delivery. Sustain. Energy Technol. Assess. 2018, 30, 121–138. [Google Scholar] [CrossRef] [Green Version]

- Ouedraogo, N.S.; Schimanski, C. Energy Poverty in Healthcare Facilities: A “Silent Barrier” to Improved Healthcare in Sub-Saharan Africa. J. Public Health Policy 2018, 39, 358–371. [Google Scholar] [CrossRef] [PubMed]

- Lagrange, A.; de Simón-Martín, M.; González-Martínez, A.; Bracco, S.; Rosales-Asensio, E. Sustainable Microgrids with Energy Storage as a Means to Increase Power Resilience in Critical Facilities: An Application to a Hospital. Int. J. Electr. Power Energy Syst. 2020, 119, 105865. [Google Scholar] [CrossRef]

- Raghuwanshi, S.S.; Arya, R. Reliability Evaluation of Stand-Alone Hybrid Photovoltaic Energy System for Rural Healthcare Centre. Sustain. Energy Technol. Assess. 2020, 37, 100624. [Google Scholar] [CrossRef]

- Vourdoubas, J. Possibilities of Using Renewable Energy Sources for Covering All the Energy Needs of Agricultural Greenhouses. J. Agric. Life Sci. 2015, 2, 111–118. [Google Scholar]

- De Smedt, L.; Pacolet, J. Financiering van de Vlaamse Social Profit. Een Nieuwe Satellietrekening Voor de Socialprofitsector in Vlaanderen; HIVA—KU Leuven: Leuven, Belgium, 2020; ISBN 978-90-5550-694-1. [Google Scholar]

- Ghaleb, B.; Asif, M. Assessment of Solar PV Potential in Commercial Buildings. Renew. Energy 2022, 187, 618–630. [Google Scholar] [CrossRef]

- Lang, T.; Ammann, D.; Girod, B. Profitability in Absence of Subsidies: A Techno-Economic Analysis of Rooftop Photovoltaic Self-Consumption in Residential and Commercial Buildings. Renew. Energy 2016, 87, 77–87. [Google Scholar] [CrossRef]

- Mah, D.N.; Wang, G.; Lo, K.; Leung, M.K.H.; Hills, P.; Lo, A.Y. Barriers and Policy Enablers for Solar Photovoltaics (PV) in Cities: Perspectives of Potential Adopters in Hong Kong. Renew. Sustain. Energy Rev. 2018, 92, 921–936. [Google Scholar] [CrossRef]

- Margolis, R.; Zuboy, J. Nontechnical Barriers to Solar Energy Use: Review of Recent Literature; National Renewable Energy Lab (NREL): Golden, CO, USA, 2006.

- Reindl, K.; Palm, J. Installing PV: Barriers and Enablers Experienced by Non-Residential Property Owners. Renew. Sustain. Energy Rev. 2021, 141, 110829. [Google Scholar] [CrossRef]

- Feldman, D.; Margolis, R. To Own or Lease Solar: Understanding Commercial Retailers’ Decisions to Use Alternative Financing Models; National Renewable Energy Lab (NREL): Golden, CO, USA, 2014.

- Amaducci, S.; Yin, X.; Colauzzi, M. Agrivoltaic Systems to Optimise Land Use for Electric Energy Production. Appl. Energy 2018, 220, 545–561. [Google Scholar] [CrossRef]

- Dinesh, H.; Pearce, J.M. The Potential of Agrivoltaic Systems. Renew. Sustain. Energy Rev. 2016, 54, 299–308. [Google Scholar] [CrossRef]

- Touil, S.; Richa, A.; Fizir, M.; Bingwa, B. Shading Effect of Photovoltaic Panels on Horticulture Crops Production: A Mini Review. Rev. Environ. Sci. Bio Technol. 2021, 20, 281–296. [Google Scholar] [CrossRef]

- Marrou, H. Co-Locating Food and Energy. Nat. Sustain. 2019, 2, 793–794. [Google Scholar] [CrossRef]

- Pascaris, A.S.; Schelly, C.; Burnham, L.; Pearce, J.M. Integrating Solar Energy with Agriculture: Industry Perspectives on the Market, Community, and Socio-Political Dimensions of Agrivoltaics. Energy Res. Soc. Sci. 2021, 75, 102023. [Google Scholar] [CrossRef]

- Sekiyama, T.; Nagashima, A. Solar Sharing for Both Food and Clean Energy Production: Performance of Agrivoltaic Systems for Corn, A Typical Shade-Intolerant Crop. Environments 2019, 6, 65. [Google Scholar] [CrossRef] [Green Version]

- Borchers, A.M.; Xiarchos, I.; Beckman, J. Determinants of Wind and Solar Energy System Adoption by U.S. Farms: A Multilevel Modeling Approach. Energy Policy 2014, 69, 106–115. [Google Scholar] [CrossRef]

- Flemish Government Visienota Zonneplan 2025. 2020. Available online: https://www.google.com.hk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&cad=rja&uact=8&ved=2ahUKEwiG1d3Kltr6AhXhslYBHdwkDc0QFnoECCMQAQ&url=https%3A%2F%2Fwww.energiesparen.be%2Fsites%2Fdefault%2Ffiles%2Fatoms%2Ffiles%2FZonneplan2025.pdf&usg=AOvVaw2Pj2k4HGKpV8tuUrz7h6fD (accessed on 30 August 2022).

- Flemish Government Zon Op Mijn Werk. 2018. Available online: https://www.acolad.com/en/news/flemish-government-wins-best-project-at-2018-e-gov-awards.html (accessed on 30 August 2022).

- Vimpari, J.; Junnila, S. Estimating the Diffusion of Rooftop PVs: A Real Estate Economics Perspective. Energy 2019, 172, 1087–1097. [Google Scholar] [CrossRef]

- Benson, D.; Lorenzoni, I. Examining the Scope for National Lesson-Drawing on Climate Governance. Political Q. 2014, 85, 202–211. [Google Scholar] [CrossRef]

- Leskinen, N.; Vimpari, J.; Junnila, S. Using Real Estate Market Fundamentals to Determine the Correct Discount Rate for Decentralised Energy Investments. Sustain. Cities Soc. 2020, 53, 101953. [Google Scholar] [CrossRef]

- Jeppesen, B. Rooftop Solar Power: The Solar Energy Potential of Commercial Building Rooftops in the USA. Refocus 2004, 5, 32–34. [Google Scholar] [CrossRef]

- Hoen, B.; Rand, J.; Elmallah, S. Commercial PV Property Characterization: An Analysis of Solar Deployment Trends in Commercial Real Estate; Technical Report; Lawrence Berkeley National Lab (LBNL): Berkeley, CA, USA, 2019.

- MacDougall, C.; Baum, F. The Devil’s Advocate: A Strategy to Avoid Groupthink and Stimulate Discussion in Focus Groups. Qual. Health Res. 1997, 7, 532–541. [Google Scholar] [CrossRef]

- Rabiee, F. Focus-Group Interview and Data Analysis. Proc. Nutr. Soc. 2004, 63, 655–660. [Google Scholar] [CrossRef] [PubMed]

- Sim, J.; Waterfield, J. Focus Group Methodology: Some Ethical Challenges. Qual. Quant. 2019, 53, 3003–3022. [Google Scholar] [CrossRef] [Green Version]

- Smithson, J. Using and Analysing Focus Groups: Limitations and Possibilities. Int. J. Soc. Res. Methodol. 2000, 3, 103–119. [Google Scholar] [CrossRef]

| Non-Homeowner Housing | Public and Social Infrastructure | Commercial Infrastructure | ||||||

|---|---|---|---|---|---|---|---|---|

| Social Rental | Private Rental | Collective Housing | Public Infrastructure | Schools | Health and Social Care | Companies | Commercial Real Estate | |

| Barriers | ||||||||

| Upfront investment (CAPEX) | x | x | x | |||||

| Split incentive problems | x | x | x | x | ||||

| Limited self-consumption | x | x | ||||||

| Diseconomies of scale | x | x | x | x | ||||

| Internal organizational barriers | x | x | x | x | ||||

| Roof quality | x | x | x | x | ||||

| Legal uncertainty | x | x | x | x | ||||

| No own roof | x | x | ||||||

| Enablers | ||||||||

| Energy savings | x | x | x | x | x | x | x | x |

| Energy sharing frameworks | x | x | x | x | x | x | x | x |

| Group purchasing/framework contracts | x | x | x | x | ||||

| Electrification of cars | x | x | ||||||

| Self-sufficiency | x | x | ||||||

| Green energy loans | x | x | ||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Van Opstal, W.; Smeets, A. Market-Specific Barriers and Enablers for Organizational Investments in Solar PV—Lessons from Flanders. Sustainability 2022, 14, 13069. https://doi.org/10.3390/su142013069

Van Opstal W, Smeets A. Market-Specific Barriers and Enablers for Organizational Investments in Solar PV—Lessons from Flanders. Sustainability. 2022; 14(20):13069. https://doi.org/10.3390/su142013069

Chicago/Turabian StyleVan Opstal, Wim, and Anse Smeets. 2022. "Market-Specific Barriers and Enablers for Organizational Investments in Solar PV—Lessons from Flanders" Sustainability 14, no. 20: 13069. https://doi.org/10.3390/su142013069