1. Introduction

Over the course of 2020, the COVID-19 pandemic has induced the most catastrophic economic recession since the Great Depression, which has, in turn, triggered the largest global downturn in economic activity since the burst of the South Sea Bubble in September of 1720 [

1,

2]. So far the stimulus responses by the majority of governments and central banks in advanced economies to this economic crisis can best be described as two-pronged with policies shifting from immediate crisis management measures, typified by policies that primarily act as direct cash injections to the economy often geared towards income support to individuals, to that of sector-specific macroeconomic stimulus, such as fiscal policies designed to bolster aggregate demand via planned investment [

3,

4,

5,

6]. Unfortunately, with regards to the latter, government investment particularly in the field of public infrastructure is renowned for long planning processes, deferred project approvals and regulatory postponements [

5]. These delays not only result in an implementation lag in the roll-out of public works projects, which ultimately lessen desired output responses, but have been found to be correlated with negative labour and output reactions to fiscal stimulus in the short run [

7]. At the ministerial level, there also remains a strong prevalence for suboptimal project selection, with governments often green-lighting or discarding public infrastructure projects owing to adjustments in political considerations [

8,

9,

10]. Even when these hurdles are overcome and public infrastructure projects are executed, it remains rare that they are completed not only ‘on-time’ and ‘on-budget’, but with their desired benefits being realized.

Indeed, an empirical study on the implementation of public transport infrastructure projects in China by Ansar et al. [

11] revealed that, from a solely benefits realization perspective, merely 10% of projects could be considered successful, while the frequency of cost overruns occurring on surveyed projects was 75% coupled with an average cost overrun of 30.6%. Their study further highlighted that there was statistically no significant difference in these cost overruns when compared to comparable observed projects executed in advanced economies [

11].

Considering the above, and while cognizant of the current perilous state of the global economy, it is perhaps a pertinent time to re-evaluate how governments approach the project evaluation process for planning and investing in public infrastructure. This exercise should be undertaken with the intent to ensure that sparse public capital is optimally invested and that successful benefits realization of executed projects is achieved. The G20, through their Leaders Communique at the 2019 Osaka Summit, has proposed that this be accomplished via placing an emphasis on the promotion of investment in ‘quality’ public infrastructure [

12]. As noted by one of the key architects of this document, Japanese Deputy Prime Minister and Minister of Finance Aso Taro, while a lot of the public discourse around public infrastructure investment has tended to focus on the various models of infrastructure financing; significantly less debate has surrounded the ‘quality aspects’ of public infrastructure development and implementation [

13]. Despite helping to facilitate a renewed global discussion on how governments should approach infrastructure investment, this document ultimately serves as a policy framework guideline. Though it does promote the concepts of transparency and good governance throughout the design and delivery phases of project rollouts, it provides no tangible methodology with regards to how governments might effectively evaluate prospective infrastructure projects to achieve optimal investment outputs.

Consequently, the aim of this study is to analyze the G20 policy framework on quality infrastructure investment and map its objectives against a leading project success evaluation method to ensure that investment in new infrastructure represents collective utility. The concept of ‘quality infrastructure’ does not only embrace economic considerations, but social, ethical and environmental consequences as well. The extent of agreement between policy and practice for delivering quality infrastructure projects is explored and discussed.

Section 2 underscores why fiscal stimulus is needed to mitigate the economic fallout from the COVID-19 pandemic.

Section 3 explores the literature for measuring the success of fiscal stimulus in terms of infrastructure investment decisions.

Section 4 describes the materials and methods adopted to compare the theory of quality infrastructure with the practice of project success evaluation via qualitative content analysis.

Section 5 presents the findings of this analysis and demonstrates that project success is an appropriate mechanism to measure the collective utility of infrastructure projects and thereby justify initial investment decisions.

Section 6 concludes the study and highlights the role that project managers can play in ensuring that fiscal success is realized.

Fiscal success is a term that is coined in this study to refer to the effective deployment of public money, collected by governments in the form of taxes, and which primarily takes place through the construction of major infrastructure projects. These projects lead to employment opportunities, future productive capacity, and support for a wide range of businesses within the global construction supply chain. However, effective deployment is critical. In the context of infrastructure, this means that monies must be well spent to realize new projects that add collective utility across the communities they serve.

2. COVID-19 and the Need for Fiscal Stimulus

Governments are engaged in unprecedented fiscal support, particularly regarding public infrastructure, as stimulus to economic recovery from the COVID-19 pandemic. It is a necessary response to increased unemployment and the collateral damage to consumer confidence and spending. Keeping people employed via nation-building projects and their supply chains is a key objective and delivers assets that support long-term productive capacity. Nevertheless, it is critical that public infrastructure is of appropriate quality to ensure projects are progressive, governments manage long-term benefits realization and critical resources are not wasted through hidden future liabilities.

The coronavirus outbreak has had a cataclysmic impact on the global economy. World output (as measured by GDP) decreased by 3.5% over the calendar year 2020, with the adverse effects being felt greater in advanced economies, where aggregate output contracted by 4.9% [

4]. In monetary terms, this is forecast to equate to a cumulative economic loss of more than USD 12 trillion over the 2020–2021 financial year—a figure which is equivalent to the entire yearly economic output of the Eurozone region [

14]. From a socioeconomic perspective, the pandemic-induced recession has brought about the greatest labour market disruption since the Great Depression, with the global reduction in working hours being four times larger than that experienced during the Global Financial Crisis [

15]. In the United Kingdom as of December 2020, over 9.9 million workers (approximately a quarter of the UK’s total workforce) had been furloughed and placed on the governments’ Job Retention Scheme (JRS), at a cost to the government of over GBP 46.4 billion [

16]. On a global level, it is estimated that in total 81% of the world’s workforce has been impacted by some form of either partial or full lockdown measures, resulting in the loss of 114 million jobs relative to 2019 [

15,

17].

The issue of how governments and central banks in advanced economies chose to enact policy responses to these troubles to mitigate their effects has been hampered by the comparative reduction in the effectiveness of crisis management tools available to them when compared to prior periods of financial crises. A former US Secretary of the Treasury acknowledged at the outset of the crisis that the advent of an era of either perpetually low zero-bound or negative interest rates has largely curtailed the beneficial impact of monetary policy, leaving central bankers with little leverage to ease rates [

18]. Existing data corroborates this viewpoint, with research showing that the initial enactment of monetary policy responses to the recession have been unable to contain the economic fallout [

3]. The revenue measures (taxation) component of fiscal policy toolsets has also been hamstrung, as the scale of the current recession limits their effectiveness as an automatic stabilizer of the economy. Automatic stabilizers, of which government taxation constitutes a major element, are adjustments in public spending and revenue deriving from the interaction between pre-existing government economic activity schedules and fluctuations in the broader economy, that possess a stabilizing influence on variations in aggregate demand and which automatically engage without explicit triggering actions from the government [

18,

19]. While revenue measures do act as an effective automatic stabilizer, there is empirical evidence from longitudinal studies that suggest at best they can only reduce initial economic shocks to GDP, and alone will not provide the requisite GDP growth required to offset current losses [

3,

20]. Moreover, as can be seen from the global labour figures, this is a very human economic crisis, and policy priorities should be aimed just as much on measures that combat rising unemployment as they might grow GDP. It is for these reasons that targeted discretionary fiscal stimulus policies are so vital in the effort to combat the harmful economic effects of the current recession.

Though fiscal stimulus measures are often criticized for necessitating budget deficits that lead to rising sovereign debt—which in turn entails compounding interest that needs to be serviced—the present economic climate poses a unique opportunity. That is, governments currently have greater economic leeway to enact fiscal stimulus than in prior periods of the financial crisis. The reason is the comparative robustness of financial markets (when compared to the Great Depression and the Global Financial Crisis) and historically low interest rates [

18,

21]. A Former Chair of the Council of Economic Advisors in the Obama Administration [

21] noted that ‘

in January 2009, the real interest rate on a ten-year government debt—the cost of borrowing after accounting for inflation—was roughly two percent […]

in January 2021, it is likely to be around negative one percent’ (p. 25). Consequently, while sovereign debt in many advanced economies is higher today, its associated carrying cost is significantly lower. As such, record low interest rates, the very thing which has hampered policymakers when trying to implement effectual monetary policy in response to the crisis, has alleviated the pressure off governments that choose to implement fiscal stimulus measures. The latitude this has provided has bolstered the capacity of governments to assume a greater volume of sovereign debt, thus allowing for expansive fiscal policy responses.

An example of this can be seen in Australia, where the federal government has legislated discretionary stimulus policies costing AUD 267 billion through to FY2023-24, a figure which is equivalent to 13.75% of national GDP [

4]. What is clear is that governments need to enact these fiscal measures promptly, to avert the enduring impacts of recessions, such as incessant unemployment and deteriorating productivity outputs. Trend analysis commissioned by the IMF and compiled from OECD data from the past fifty years reveals the lasting ill-effects recessions can have on advanced economies. The mean result three years post-recession was an output decline of 4.75% below trend, before signs of growth began to emerge [

1]. When further refined to modelling on large recessions alone, the trend analysis revealed a sustained decline in output relative to baseline projections, with GDP remaining on average 11% beneath trend five years post-recession [

1]. In this analysis, a large recession was defined as a period of economic decline where the initial shock to output was in the top quartile of recessions in the dataset, equating to a decrease greater than 4.25% [

1]. The latter of the two scenarios is the one which Australia, and indeed most advanced economies, are faced with. It is therefore imperative that governments move swiftly to implement nuanced fiscal policy measures focused on public investment.

5. Results and Discussion

The G20 principles begin by describing infrastructure as a driver of economic prosperity that provides a solid basis for strong, sustainable, balanced and inclusive growth and sustainable development. These are key goals of the G20 policy and critical for promoting global, national and local development priorities. The preamble to the G20 principles states that ‘

a renewed emphasis on quality infrastructure investment will build on the past G20 presidencies’ efforts to mobilize financing from various sources, particularly the private sector and institutional sources including multilateral development banks, thereby contribute to closing the infrastructure gap, develop infrastructure as an asset class, and maximizing the positive impacts of infrastructure investment according to country conditions’ [

62] (p. 1). They believe that quantity and quality can be complementary.

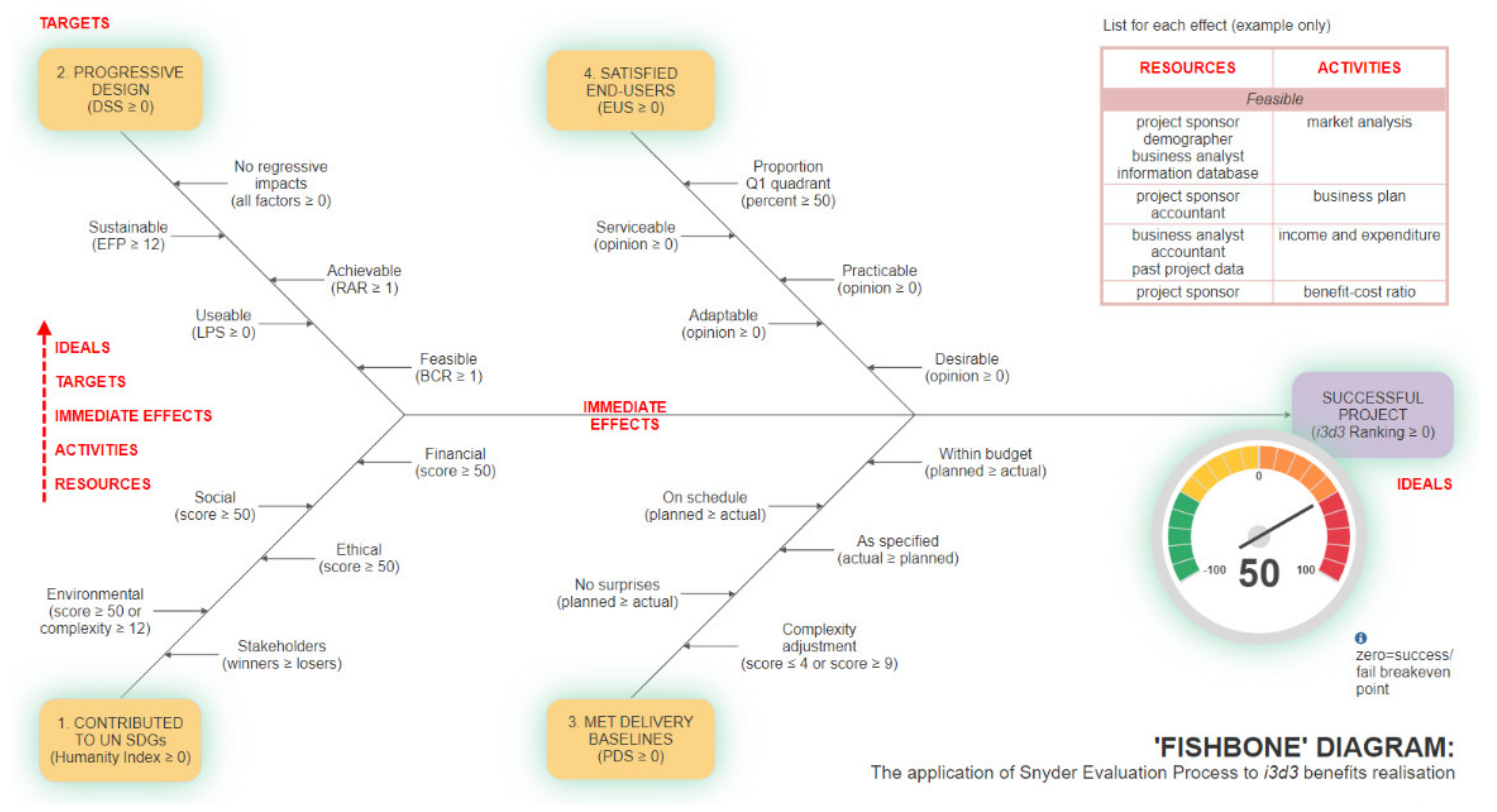

In contrast, the

i3d3 model is not confined to infrastructure but claims to potentially measure success for ‘

projects of any type, size, location or date’ [

83] (p. 17). Quality investment and success have some commonalities. The

i3d3 model defines success as doing the ‘right project right’ and incorporates the three phases of initiate (design), implement (deliver) and influence (delight) in the context of the passage of time and the different objectives of project stakeholders. It judges success as benefits realization (collective utility)—a key construct of social cost–benefit analysis. The

i3d3 model can use hindsight to audit performance as a means of ranking a portfolio of projects by success or be applied during project delivery to ensure that progress is on time, within budget, as specified and with no surprises.

There are six principles in the G20 framework that are specific to promoting quality infrastructure investment [

62]:

Principle 1 focuses on sustainable growth and development (see

Table 1). A key attribute of this principle is that infrastructure investments are progressive, not regressive and hence improve prosperity to the local community or region. The 17 United Nations SDGs are relevant here [

66].

Principle 2 focuses on economic efficiency (see

Table 2). A key attribute of this principle is that infrastructure assets have long lives and contribute to economic prosperity over time. The concept of life-cycle performance, often termed whole-of-life costs, is critical here.

Principle 3 focuses on the environmental impact (collateral damage) that can arise from infrastructure project development and operation (see

Table 3). A key attribute of this principle is that natural resources matter and must be used sustainably, appropriately valued and respected.

Principle 4 focuses on resilience (see

Table 4). A key attribute of this principle is asset security in the face of natural disasters or related risks.

Principle 5 focuses on the social benefits that infrastructure provides (see

Table 5). A key attribute of this principle is the utility that projects provide to human health and well-being. Social benefits are often intangible and hard to measure.

Principle 6 focuses on governance and transparency (see

Table 6). A key attribute of this principle is ethical behaviour and ensuring that investments are deployed wisely and not diverted from their intended use.

Generally, the i3d3 model characteristics seem to closely align with the G20 framework. Principle 1 maps against the net benefit calculations within i3d3, Principle 2 maps against ‘financial’ consequences across initiate, implement and influence phases, Principle 3 similarly maps against ‘environmental’ consequences, Principle 4 maps against the humanity index and the United Nations SDGs, Principle 5 maps against ‘social’ consequences across initiate, implement and influence phases, and Principle 6 similarly maps against ‘ethical’ consequences, although there is no specific attention paid to evaluating corruption should it occur. Yet, in the same way that optimism bias is called out in hindsight as part of the evaluation of design, corruption can be identified through an audit of benefits realization in practice.

There were 23 numbered G20 principles. Using the three-level scoring algorithm discussed earlier, the total thematic match with i3d3 was computed as 66. Principle 6.2 was scored as moderate (2) and Principle 6.3 was scored as low (1), while all other principles were scored as high (3). This translates to a synergy of 96%.

Two features of the

i3d3 model that are obvious and arguably advantageous comprise transparency and simplicity. Transparency is important but not always welcomed. It implies that decisions are traceable and their rationale can be comprehended even though not everyone will agree. The multidisciplinary nature of project management suggests that consensus can be demonstrated, and this is useful even where that consensus is not unanimous. Political imperatives are well understood to override rational independent recommendations, and in such cases, transparency might be challenged. On the other hand, simplicity enables evaluation to take place without significant time and cost impost and hence encourages the use of

i3d3 in practice. Likewise, this provides an opportunity for recommendations to be overridden on the grounds that there are other issues that should have been considered. A more comprehensive and rigorous evaluation could be adopted at the expense of both transparency and simplicity, which is probably what happens now on large-scale public infrastructure projects (for example, Infrastructure Australia [

84]).

Nevertheless,

i3d3 is a useful tool in the broader context of project comparison. Although its design could be debated, at least it applies a consistent lens for evaluation and ranking of project success. It remains to be seen if

i3d3 truly is agnostic to project type, size, location or date. However, there are shared case studies available online [

85,

86,

87] that suggest it can assess large public infrastructure projects for the purposes of comparison. Positive scores indicate success; negative scores suggest failure. The ability to trade-off good and bad performance typifies what generally happens in practice—there are no perfect solutions even though we strive to find them.

A key difference between i3d3 and many other evaluation models is that the latter are focused on forecasting future performance. Decisions are taken to ‘go’ or ‘no go’ based on this information. Such approaches require a robust benefits realization mechanism to ensure that envisaged outcomes indeed eventuate. Without that, quality infrastructure investment cannot be validated. These models aim to compare design options and assess the risks and rewards of each proposal. The i3d3 model also does this, but since the final score cannot be determined until at least one year after handover, the forecasts embedded in the initiation phase can be updated should some assumptions prove false. Optimism bias is removed. Quality investments cannot be known until after project completion. Forecasts of quality and proof of quality are two very different things.

Infrastructure projects, like any new initiative, are vehicles of change. Building situation awareness, as embedded in models such as ADKAR [

88] and DALI [

89], is fundamental to any change control plan. Therefore identifying, analyzing and managing negative risks and positive rewards will help make better decisions. Change also leads to process improvement so that project managers continually learn from their actions and pass this new knowledge to future projects in a systematic way. Quality infrastructure investments do not happen in isolation but arise from experience and organizational maturity over many years.

This research has assumed quality infrastructure investments are validated through project success evaluation. The G20 policy [

62] sets out a theoretical definition of the former, while the

i3d3 model [

83] sets out a solution to operationalize the theory into practice. While both were developed independently, albeit simultaneously, they have been shown in this study to have remarkable synergy. Of course, there are many principles that can be formulated, and many solutions invented to implement them, but the ones chosen are considered leading and recent examples that can support each other to improve fiscal success via process improvement.

There are several limitations that should be noted. First, the use of qualitative content analysis implies that findings are subjective based on the opinion of the researchers. Further studies could try and validate these opinions by surveying practitioners (who have experience in using both artefacts) using statistical means. This is still founded on subjectivity, but with greater numerical quantification than the simple 4-point scoring method employed in this study. It is too early to do this since both artefacts are new and not in widespread use. Second, evidence of collective utility from a range of infrastructure projects would provide more confidence in the efficacy of both artefacts. The case studies provided [

85,

86,

87] are useful beginnings, but a much larger dataset of successful projects, and failed ones, needs to be developed. Future research should aim to resolve these limitations. This study is therefore a first step along this journey.

COVID-19 is the reason quality infrastructure investments are needed. It is easy to throw money at new projects to keep the economy moving, but if these investments do not contribute to improvements in productive capacity, then the benefits that flow from them are diminished. The OECD has forecast that the effects of COVID-19 are likely to continue for some time, and given concurrent supply chain problems, rising interest rates and higher levels of inflation, an even more challenging environment in which to operate is created [

90]. The need to make better decisions and achieve fiscal success is now more important than ever. Project managers are well placed to routinely evaluate project success and such work should be considered as evidence of best practice.

6. Conclusions

The COVID-19 pandemic has engendered the worst economic recession since the Great Depression, triggering the largest global downturn in economic activity since 1720. Socioeconomically, this has resulted in a catastrophic labour market disruption, with 81% of the world’s workforce being impacted by lockdown measures causing a global reduction in working hours four times greater than that suffered during the GFC. In this context, public investment in infrastructure projects as a component of a broader fiscal stimulus package is put forward as an economic policy measure to combat the protracted ill-effects of this downturn. Transport infrastructure investment is of great interest, as it will deliver jobs and inject money that will circulate through local communities in the short-term while enabling an increase in aggregate productivity and delivering indirect economic benefits in line with Krugman’s NEG theory in the long term.

In order to ensure that the anticipated benefits of such a stimulus package would be realized upon project completion, the G20 Principles for Quality Infrastructure Investment were matched against the practical outcomes of the i3d3 project success evaluation method. Studies of this nature have not been undertaken before despite a broad range of economic tools available in the marketplace. It was found that i3d3 offers a ‘high’ thematic match (96%) against G20 policy principles and therefore provides an opportunity for project management practice to objectively validate strong, sustainable, balanced and inclusive growth and sustainable development that underpins the need for quality infrastructure investments. In this research, project success is seen as equivalent to fiscal success for public infrastructure projects. This directly enables project managers to contribute to outcomes that are progressive and take into consideration financial, social, ethical and environmental consequences. Further research is needed to extend this study through field validation and refinement.

It is thus recommended that project managers engage with the concept of quality infrastructure investment as the connection to project success is undeniable. Nevertheless, it is evident that project management success is not the same as project success, and hence the activities involved in successful implementation must be considered alongside the merits of initial design decisions and their acceptance by those whom the project intends to serve. This is difficult to do at a single point in time, such as when undertaking front-end planning and evaluating options, so the assessment of quality infrastructure is best completed in hindsight at least one year after project completion.

{kind=link}