The Impact of Logistics Corporate Social Responsibility on Supply Chain Performance: Using Supply Chain Collaboration as an Intermediary Variable

Abstract

:1. Introduction

1.1. Background

1.2. Literature Review

- (1)

- Most research on CSR is focused on whole supply chain companies and less on logistics enterprises. The impact of fulfilling the LCSR on SCP is a topic worth exploring.

- (2)

- In terms of indicator measurement, most scholars pay less attention to environmental protection, so the measurement of CSR and SCP is not comprehensive. Moreover, environmental protection is a global problem, and logistics activities such as warehousing [35], transportation, and packaging [36] have made significant contributions to greenhouse gas emissions. Adding environmental protection to the measurement indicators is of practical significance.

- (3)

- Supply chain collaboration (SCC) refers to collaborative activities carried out by enterprises to improve the overall competitiveness of the supply chain and achieve common goals. It improves collaborative advantage and has a bottom-line influence on firm performance [37]. However, there is not much research that introduces SCC as an intermediary variable to explore the relationship between LCSR and SCP.

2. Theoretical Basis and Research Hypothesis

2.1. Theoretical Basis

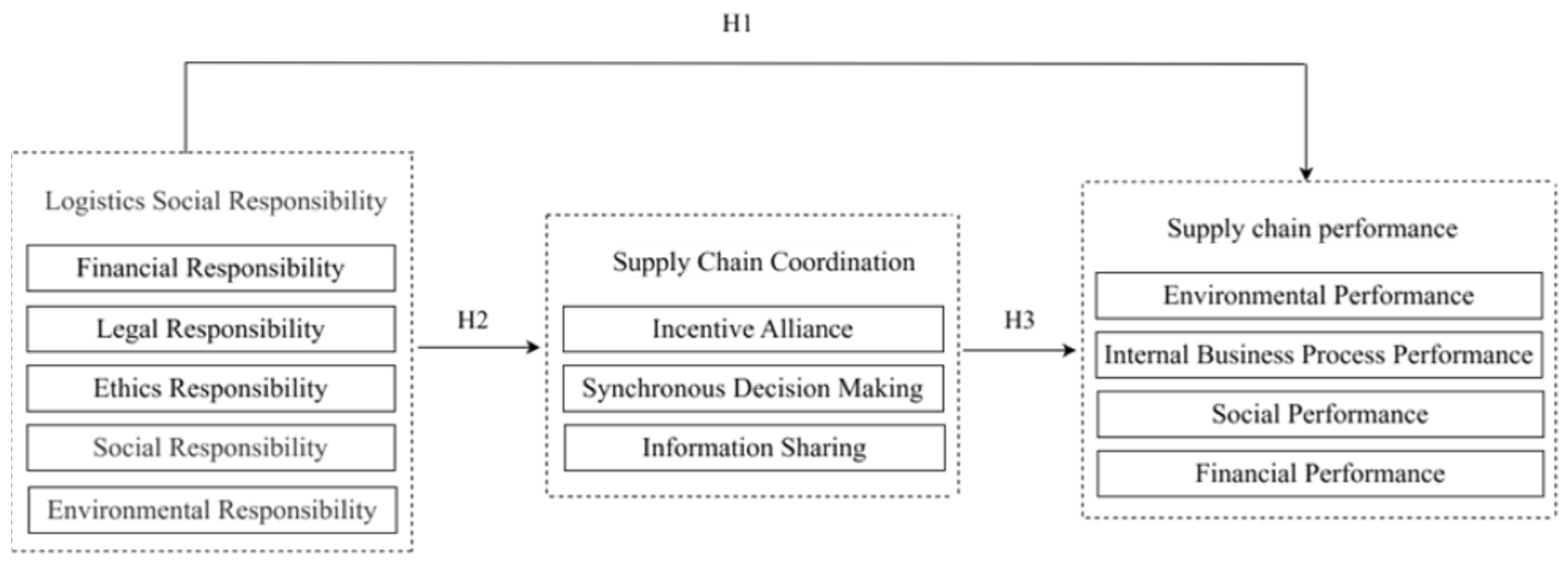

2.2. Research Hypothesis and Conceptual Model

2.2.1. Corporate Social Responsibility and Supply Chain Performance

2.2.2. Corporate Social Responsibility and Supply Chain Coordination

2.2.3. Supply Chain Collaboration and Supply Chain Performance

3. Research Method

3.1. Pre-Survey

3.2. Questionnaire Survey

3.3. Statistical Analysis

3.4. Structural Equation Method

3.5. Bootstrap Method

4. Data Analysis

4.1. Questionnaire Collection

4.2. Reliability and Validity Test of Questionnaire Data

4.3. Results

4.3.1. Direct Effect Significance Test

4.3.2. Mediation Effect Significance Test

4.4. Framework for Future Development

- (1)

- Logistics enterprises should improve their awareness of fulfilling CSR: gradually deepen the practice of social responsibility from a practical point of view; be responsible for shareholders and employees internally; provide employees with treatment, management, and welfare; follow the green and low-carbon development path; realize the efficient use of resources; be responsible for consumers, suppliers, governments, and communities externally; abide by national laws and regulations; provide social employment resources; support community construction; and provide more convenient services for the public, to increase the popularity of enterprises, accumulate corporate reputation, improve profitability, and ultimately achieve the mutual promotion of corporate development and social responsibility.

- (2)

- Logistics enterprises should cooperate with enterprises at different nodes in the supply chain to drive upstream and downstream industries to participate in it, strengthening the synchronous operation of logistics, business flow, capital flow, and information flow, and strengthening the overall supply chain’s rapid response to customers’ personalized needs to maximize benefits.

- (3)

- At the government level, it should play a supervisory and management role in the performance of the social responsibilities of logistics enterprises, actively guide them to correctly perform their CSR, enhance the collaborative operation of the supply chain, provide good environments and services for logistics enterprises to better perform their CSR, and formulate a system of information disclosure, evaluation, rewards, and punishment in line with the social responsibilities of logistics enterprises to push forward the growth of CSR in the logistics industry. Ultimately, this improves the performance of the whole supply chain.

4.5. Discussion

- (1)

- The evaluation of SCP as a cross-enterprise, complex, multidimensional, and comprehensive system cannot be limited to a single-dimension evaluation. Only by establishing an evaluation system from multiple perspectives can strategic objectives be achieved.

- (2)

- The SEM is a good analytical tool to deal with the relationship between latent variables and indicators. It has many advantages, such as the simultaneous handling of multiple sets of dependent variables and the separation of measurement errors. In researching LCSR, SCC, and SCP, it is necessary to analyze multiple latent and observed variables, and SEM has no limit on the number of variables compared with linear regression, which is more suitable for this situation.

- (3)

- The mechanism of action of different mediating variables is different, and the mediating effect produced is also different. SCC is a collaborative activity conducted by companies to enhance the overall competitiveness of the supply chain and achieve corporate aims. SCC plays a vital role in the relationship between CSR and SCP and cannot be ignored.

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Jiao, J.; Xu, X. Analysis of the Information Disclosure of Social Responsibility Accounting of Automobile Manufacturing Enterprises of China. In Proceedings of the 2nd International Seminar on Education Research and Social Science, Kuala Lumpur, Malaysia, 25–27 May 2019; Atlantis Press: Amsterdam, The Netherlands, 2019; pp. 286–289. [Google Scholar]

- Liu, C.; Chen, J.; Wang, X. Quantitative Evaluation Model of the Quality of Remanufactured Product. IEEE Trans. Eng. Manag. 2023, 1–12. [Google Scholar] [CrossRef]

- Liu, C.; Chen, J.; Cai, W. Data-driven remanufacturability evaluation method of waste parts. IEEE Trans. Ind. Inform. 2021, 18, 4587–4595. [Google Scholar] [CrossRef]

- Piecyk, M.I.; Björklund, M. Logistics service providers and corporate social responsibility: Sustainability reporting in the logistics industry. Int. J. Phys. Distrib. Logist. Manag. 2015, 45, 459–485. [Google Scholar] [CrossRef]

- Zimmer, K.; Fröhling, M.; Breun, P.; Schultmann, F. Assessing Social Risks of Global Supply Chains: A Quantitative Analytical Approach and its Application to Supplier Selection in the German Automotive Industry. J. Clean. Prod. 2017, 149, 96–109. [Google Scholar] [CrossRef]

- Cheng, H.; Ding, H. Dynamic game of corporate social responsibility in a supply chain with competition. J. Clean. Prod. 2021, 317, 128398. [Google Scholar] [CrossRef]

- Ahmadini AA, H.; Modibbo, U.M.; Shaikh, A.A.; Ali, I. Multi-objective optimization modelling of sustainable green supply chain in inventory and production management. Alex. Eng. J. 2021, 60, 5129–5146. [Google Scholar] [CrossRef]

- Činčalová, S. Evaluation of the Current Position of CSR in the Logistics Sector. In Proceedings of the Innovation Management, Entrepreneurship and Sustainability (IMES 2018), Prague, Czech Republic, 31 May–1 June 2018; Vysoká Škola Ekonomická v Praze: Prague, Czech Republic, 2018; pp. 154–165. [Google Scholar]

- Quan, C.; Yu, S.; Cheng, X.; Liu, F. Comprehensive efficiency evaluation of social responsibility of Chinese listed logistics enterprises based on DEA-Malmquist model. Oper. Manag. Res. 2022, 15, 1383–1398. [Google Scholar] [CrossRef]

- Chien, F. The role of corporate governance and environmental and social responsibilities on the achievement of sustainable development goals in Malaysian logistic companies. Econ. Res.-Ekon. Istraživanja 2023, 36, 1610–1630. [Google Scholar] [CrossRef]

- Činčalová, S. Empirical research on corporate social responsibility in the logistics company. Innovation management and education excellence through vision 2020. In Proceedings of the 31st International-Business-Information-Management-Association Conference, Milan, Italy, 25–26 April 2018. [Google Scholar]

- El Ghoul, S.; Karoui, A. Does corporate social responsibility affect mutual fund performance and flows? J. Bank. Financ. 2017, 77, 53–63. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. The balanced scorecard--measures that drive performance. Harv. Bus. Rev. 1992, 70, 71–79. [Google Scholar]

- Thanh, T.L.; Huan, N.Q.; Hong TT, T. Effects of corporate social responsibility on SMEs’ performance in emerging market. Cogent Bus. Manag. 2021, 8, 1878978. [Google Scholar] [CrossRef]

- Cruz, J.M. The impact of corporate social responsibility in supply chain management: Multicriteria decision-making approach. Decis. Support Syst. 2009, 48, 224–236. [Google Scholar] [CrossRef]

- Khan SA, R.; Qianli, D. Impact of green supply chain management practices on firms’ performance: An empirical study from the perspective of Pakistan. Environ. Sci. Pollut. Res. 2017, 24, 16829–16844. [Google Scholar] [CrossRef] [PubMed]

- Panda, S.; Modak, N.M.; Cárdenas-Barrón, L.E. Coordinating a socially responsible closed-loop supply chain with product recycling. Int. J. Prod. Econ. 2017, 188, 11–21. [Google Scholar] [CrossRef]

- Li, X. The effectiveness of internal control and innovation performance: An intermediary effect based on corporate social responsibility. PLoS ONE 2020, 15, e0234506. [Google Scholar] [CrossRef] [PubMed]

- Rjiba, H.; Jahmane, A.; Abid, I. Corporate social responsibility and firm value: Guiding through economic policy uncertainty. Financ. Res. Lett. 2020, 35, 101553. [Google Scholar] [CrossRef]

- Al-Shammari, M.A.; Banerjee, S.N.; Rasheed, A.A. Corporate social responsibility and firm performance: A theory of dual responsibility. Manag. Decis. 2022, 60, 1513–1540. [Google Scholar] [CrossRef]

- Mondal, C.; Giri, B.C. Optimizing price, quality and CSR investment under competing dual recycling channels in a sustainable closed-loop supply chain. CIRP J. Manuf. Sci. Technol. 2021, 35, 193–208. [Google Scholar] [CrossRef]

- Singh, N.P. Managing the adverse effect of supply chain risk on corporate reputation: The mediating role of corporate social responsibility practices. J. Gen. Manag. 2021, 46, 251–261. [Google Scholar] [CrossRef]

- Wu, X.; Li, S. Impacts of CSR Undertaking Modes on Technological Innovation and Carbon-Emission-Reduction Decisions of Supply Chain. Sustainability 2022, 14, 13333. [Google Scholar] [CrossRef]

- Henderson, D. The case against “corporate social responsibility”. Policy Cent. Indep. Stud. 2001, 17, 28–32. [Google Scholar]

- Nguyen, C.T.; Nguyen, L.T.; Nguyen, N.Q. Corporate social responsibility and financial performance: The case in Vietnam. Cogent Econ. Financ. 2022, 10, 2075600. [Google Scholar] [CrossRef]

- Dou, X. The lag effect of corporate social responsibility on financial performance—An Empirical Analysis Based on the panel data of Shanghai and Shenzhen listed companies. Ind. Econ. Res. 2015, 3, 74–81. [Google Scholar]

- Crisóstomo, V.L.; de Souza Freire, F.; De Vasconcellos, F.C. Corporate social responsibility, firm value and financial performance in Brazil. Soc. Responsib. J. 2011, 7, 295–309. [Google Scholar] [CrossRef] [Green Version]

- Yoon, B.; Chung, Y. The effects of corporate social responsibility on firm performance: A stakeholder approach. J. Hosp. Tour. Manag. 2018, 37, 89–96. [Google Scholar] [CrossRef]

- Kraus, S.; Rehman, S.U.; García, F.J.S. Corporate social responsibility and environmental performance: The mediating role of environmental strategy and green innovation. Technol. Forecast. Soc. Chang. 2020, 160, 120262. [Google Scholar] [CrossRef]

- Kong, Y.; Antwi-Adjei, A.; Bawuah, J. A systematic review of the business case for corporate social responsibility and firm performance. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 444–454. [Google Scholar] [CrossRef]

- Naseem, T.; Shahzad, F.; Asim, G.A.; Rehman, I.U.; Nawaz, F. Corporate social responsibility engagement and firm performance in Asia Pacific: The role of enterprise risk management. Corp. Soc.-Responsib. Environ. Manag. 2020, 27, 501–513. [Google Scholar] [CrossRef]

- Wang, C.; Zhang, Q.; Zhang, W. Corporate social responsibility, Green supply chain management and firm performance: The moderating role of big-data analytics capability. Res. Transp. Bus. Manag. 2020, 37, 100557. [Google Scholar] [CrossRef]

- Novitasari, M.; Wijaya, A.L.; Agustin, N.M.; Gunardi, A.; Dana, L. Corporate social responsibility and firm performance: Green supply chain management as a mediating variable. Corp. Soc.-Responsib. Environ. Manag. 2023, 30, 267–276. [Google Scholar] [CrossRef]

- Liu, Y.; Chen, Y.; Ren, Y.; Jin, B. Impact mechanism of corporate social responsibility on sustainable technological innovation performance from the perspective of corporate social capital. J. Clean. Prod. 2021, 308, 127345. [Google Scholar] [CrossRef]

- Datta, T.K. Effect of green technology investment on a production-inventory system with carbon tax. Adv. Oper. Res. 2017, 2017, 4834839. [Google Scholar] [CrossRef] [Green Version]

- Waltho, C.; Elhedhli, S.; Gzara, F. Green supply chain network design: A review focused on policy adoption and emission quantification. Int. J. Prod. Econ. 2019, 208, 305–318. [Google Scholar] [CrossRef]

- Cao, M.; Zhang, Q. Supply chain collaboration: Impact on collaborative advantage and firm performance. J. Oper. Manag. 2011, 29, 163–180. [Google Scholar] [CrossRef]

- Lys, T.; Naughton, J.P.; Wang, C. Signaling through corporate accountability reporting. J. Account. Econ. 2015, 60, 56–72. [Google Scholar] [CrossRef] [Green Version]

- Li, S.; Li, M.; Zhou, N.; Xin, B. Pricing and coordination in a dual-channel supply chain with a socially responsible manufacturer. PLoS ONE 2020, 15, e0236099. [Google Scholar] [CrossRef]

- Alduais, F.; Almasria, N.A.; Airout, R. The Moderating Effect of Corporate Governance on Corporate Social Responsibility and Information Asymmetry: An Empirical Study of Chinese Listed Companies. Economies 2022, 10, 280. [Google Scholar] [CrossRef]

- Kaipia, R.; Holmström, J.; Småros, J.; Rajala, R. Information sharing for sales and operations planning: Contextualized solutions and mechanisms. J. Oper. Manag. 2017, 52, 15–29. [Google Scholar] [CrossRef] [Green Version]

- Thi Mai Anh, N.; Hui, L.; Khoa, V.D.; Mehmood, S. Relational capital and supply chain collaboration for radical and incremental innovation: An empirical study in China. Asia Pac. J. Mark. Logist. 2019, 31, 1076–1094. [Google Scholar] [CrossRef]

- Baah, C.; Opoku Agyeman, D.; Acquah, I.S.K.; Agyabeng-Mensah, Y.; Afum, E.; Issau, K.; Ofori, D.; Faibil, D. Effect of information sharing in supply chains: Understanding the roles of supply chain visibility, agility, collaboration on supply chain performance. Benchmarking Int. J. 2022, 29, 434–455. [Google Scholar] [CrossRef]

- Vosooghidizaji, M.; Taghipour, A.; Canel-Depitre, B. Coordinating corporate social responsibility in a two-level supply chain under bilateral information asymmetry. J. Clean. Prod. 2022, 364, 132627. [Google Scholar] [CrossRef]

- Carroll, A.B.; Shabana, K.M. The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Simatupang, T.M.; Sridharan, R. The collaboration index: A measure for supply chain collaboration. Int. J. Phys. Distrib. Logist. Manag. 2005, 35, 44–62. [Google Scholar] [CrossRef]

- Carter, C.R.; Jennings, M.M. The role of purchasing in corporate social responsibility: A structural equation analysis. J. Bus. Logist. 2004, 25, 145–186. [Google Scholar] [CrossRef]

- Wisner, J.D. A structural equation model of supply chain management strategies and firm performance. J. Bus. Logist. 2004, 25, 1–26. [Google Scholar] [CrossRef]

- Hu, L.; Bentler, P.M. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Struct. Equ. Model. 1999, 6, 1–55. [Google Scholar] [CrossRef]

- Ali, H.Y.; Danish, R.Q.; Asrar-ul-Haq, M. How corporate social responsibility boosts firm financial performance: The mediating role of corporate image and customer satisfaction. Corp. Soc.-Responsib. Environ. Manag. 2020, 27, 166–177. [Google Scholar] [CrossRef]

- Preacher, K.J.; Hayes, A.F. SPSS and SAS procedures for estimating indirect effects in simple mediation models. Behav. Res. Methods 2004, 36, 717–731. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef] [Green Version]

- Preacher, K.J.; Hayes, A.F. Asymptotic and resampling strategies for assessing and comparing indirect effects in multiple mediator models. Behav. Res. Methods 2008, 40, 879–891. [Google Scholar] [CrossRef]

- Khan SA, R.; Sharif, A.; Golpîra, H.; Kumar, A. A green ideology in Asian emerging economies: From environmental policy and sustainable development. Sustain. Dev. 2019, 27, 1063–1075. [Google Scholar] [CrossRef]

- Chu, S.; Yang, H.; Lee, M.; Park, S. The Impact of Institutional Pressures on Green Supply Chain Management and Firm Performance: Top Management Roles and Social Capital. Sustainability 2017, 9, 764. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

| Facets | Index | Aggregate Validity | ||||

|---|---|---|---|---|---|---|

| Standard Load Factor | p-Value | CR | AVE | Cronbach’s α | ||

| Logistics social responsibility | Environmental responsibility | 0.862 | *** | 0.876 | 0.586 | 0.924 |

| Social responsibility | 0.749 | *** | ||||

| Ethical responsibility | 0.734 | *** | ||||

| Legal responsibility | 0.755 | *** | ||||

| Financial responsibility | 0.719 | *** | ||||

| Supply chain coordination | Incentive alliance | 0.777 | *** | 0.829 | 0.619 | 0.885 |

| Synchronous decision making | 0.757 | *** | ||||

| Information sharing | 0.824 | *** | ||||

| Supply chain performance | Environmental performance | 0.82 | *** | 0.888 | 0.664 | 0.924 |

| Internal business process performance | 0.802 | *** | ||||

| Social performance | 0.819 | *** | ||||

| Financial performance | 0.819 | *** | ||||

| Statistical Test Quantities | Symbol Meaning | Test Results | Fit Judgment |

|---|---|---|---|

| CMIN/DF | Chi-square value/degree of freedom | 2.818 | Pass |

| GFI | Goodness of fit index | 0.944 | Pass |

| IFI | Value-added fitting index | 0.97 | Pass |

| NFI | Canonical fit index | 0.955 | Pass |

| RMR | Root of mean square residual | 0.01 | Pass |

| RMSEA | Root-mean-square error of approximation | 0.068 | Pass |

| PNFI | Frugality norm fitting index | 0.738 | Pass |

| Variable | Point Estimates | Product of Coefficients | Bootstrapping 5000 Times 95% CI | ||||

|---|---|---|---|---|---|---|---|

| Bias Corrected | Percentile | ||||||

| SE | Z | Lower | Upper | Lower | Upper | ||

| Indirect effects | |||||||

| LCSR → SCP | 0.433 | 0.195 | 2.221 | 0.065 | 0.824 | 0.032 | 0.79 |

| Direct effects | |||||||

| LCSR → SCP | 0.605 | 0.226 | 2.677 | 0.192 | 1.067 | 0.209 | 1.082 |

| Total effect | |||||||

| LCSR → SCP | 1.038 | 0.067 | 15.493 | 0.908 | 1.171 | 0.909 | 1.172 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, L.; Fu, Y.; Liu, Y.; Wang, C. The Impact of Logistics Corporate Social Responsibility on Supply Chain Performance: Using Supply Chain Collaboration as an Intermediary Variable. Sustainability 2023, 15, 9613. https://doi.org/10.3390/su15129613

Chen L, Fu Y, Liu Y, Wang C. The Impact of Logistics Corporate Social Responsibility on Supply Chain Performance: Using Supply Chain Collaboration as an Intermediary Variable. Sustainability. 2023; 15(12):9613. https://doi.org/10.3390/su15129613

Chicago/Turabian StyleChen, Lu, Yueyue Fu, Yujia Liu, and Cui Wang. 2023. "The Impact of Logistics Corporate Social Responsibility on Supply Chain Performance: Using Supply Chain Collaboration as an Intermediary Variable" Sustainability 15, no. 12: 9613. https://doi.org/10.3390/su15129613