Corporate Governance and Financial Reporting Quality: The Mediation Role of IFRS

Abstract

1. Introduction

2. Literature Review and Hypothesis Development

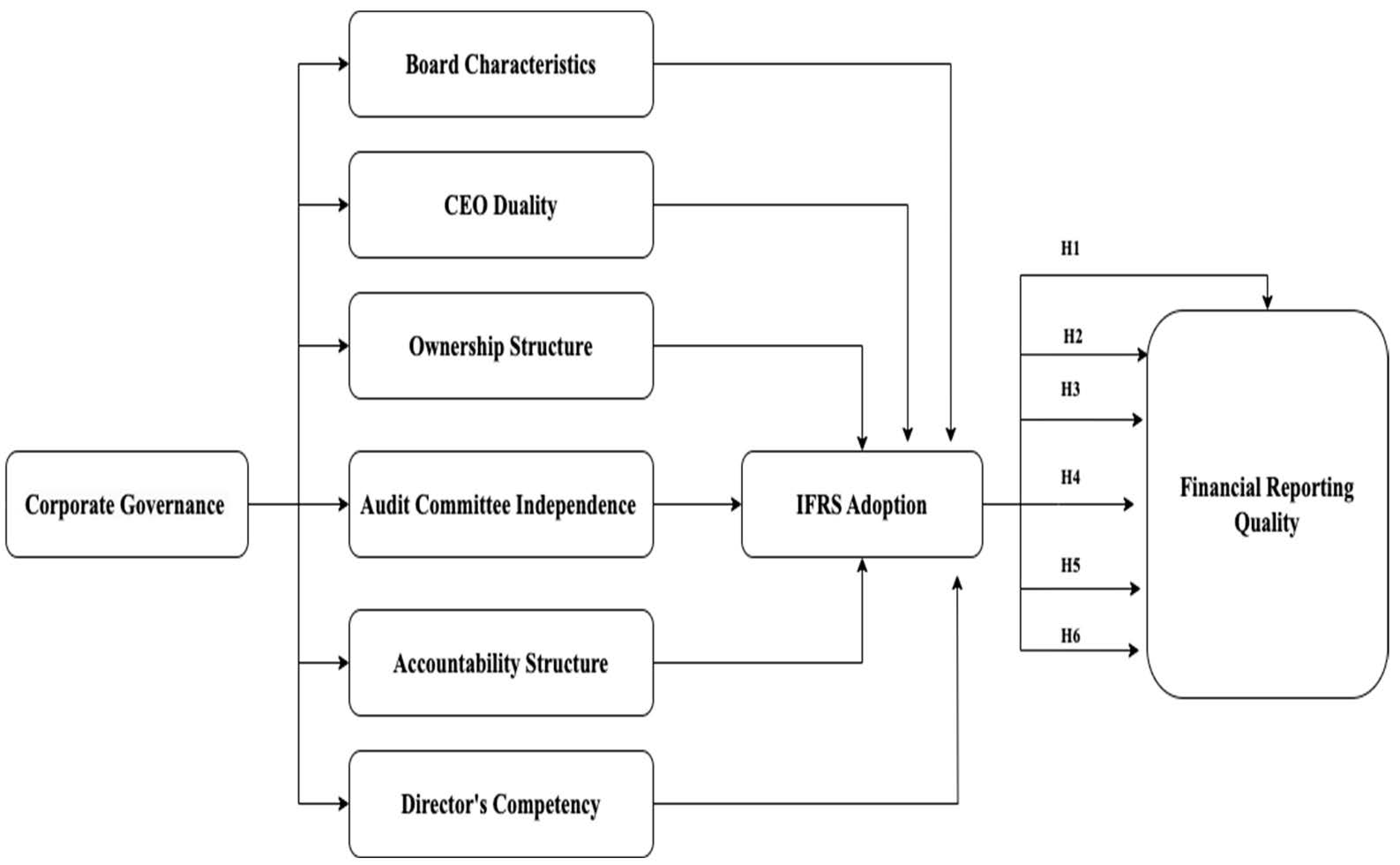

2.1. The Mediation Role of the Adoption of IFRS between Board Characteristics and Financial Reporting Quality

2.2. The Mediation Role of the Adoption of IFRS between CEO Duality and Financial Reporting Quality

2.3. The Mediation Role of the Adoption of IFRS between Ownership Structure and Financial Reporting Quality

2.4. The Mediation Role of the Adoption of IFRS between Audit Committee Independence and Financial Reporting Quality

2.5. The Mediation Role of the Adoption of IFRS between Accountability Structure and Financial Reporting Quality

2.6. The Mediation Role of the Adoption of IFRS between Directors’ Competency and Financial Reporting Quality

2.7. Conceptual Framework

3. Materials and Methods

3.1. Sample Size and Sampling Method

3.2. Data Collection

4. Results

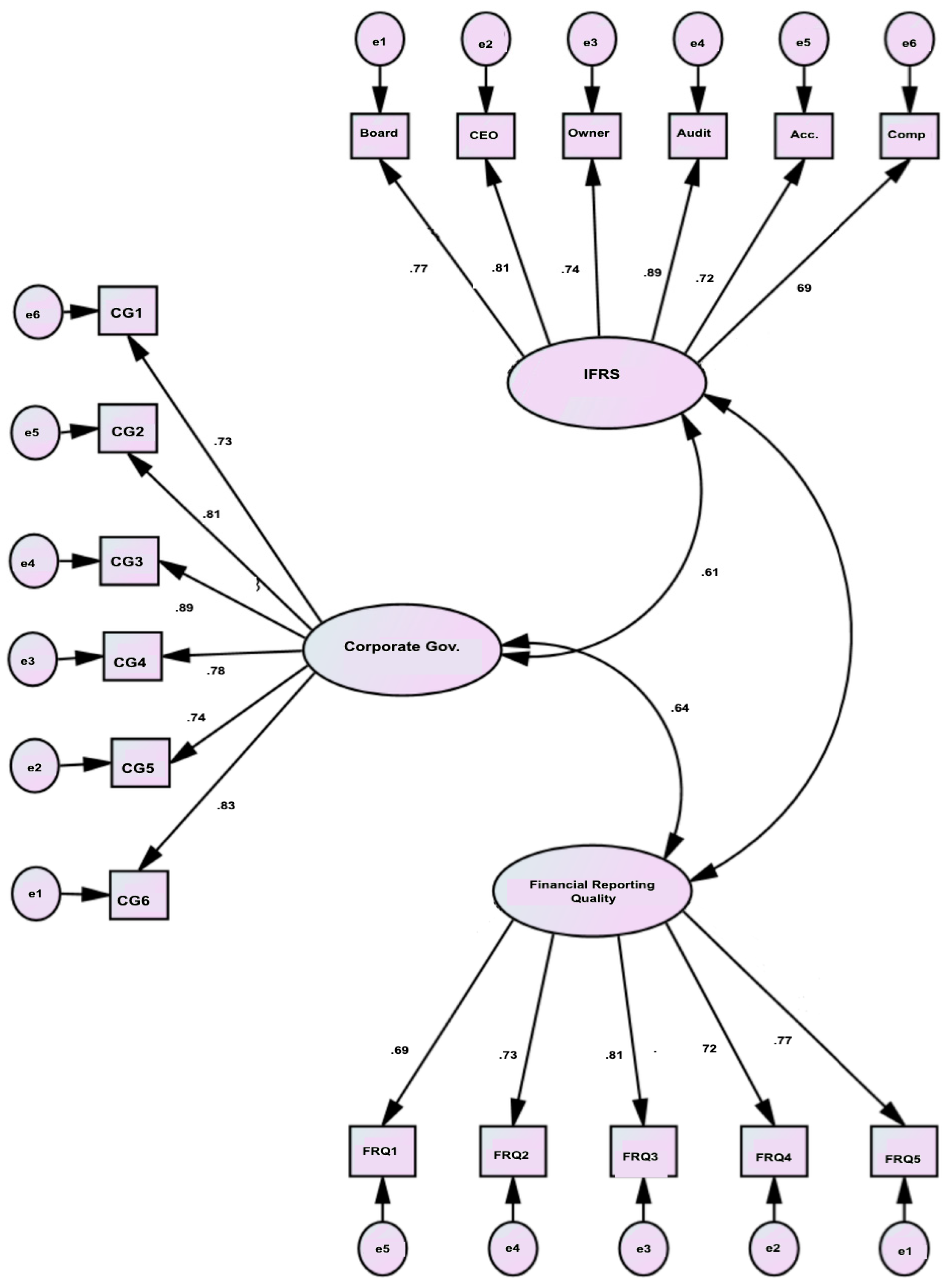

Confirmatory Factor Analysis (CFA)

5. Conclusions

5.1. Theoretical Implication

5.2. Practical Implication

5.3. Research Limitations

5.4. Future Studies

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Hasan, M.T.; Rahman, A.A. Conceptual framework for IFRS adoption, audit quality and earnings management: The case of Bangladesh. Int. Bus. Acc. Res. J. 2019, 3, 58–66. [Google Scholar] [CrossRef]

- Khlif, H.; Ahmed, K.; Alam, M. Accounting regulations and IFRS adoption in francophone North African countries: The experience of Algeria, Morocco, and Tunisia. Int. J. Acc. 2020, 55, 2050004. [Google Scholar] [CrossRef]

- Apochi, J.G.; Mustapha, L.O.I. FRS Adoption Financial Reporting Quality in Nigeria: A Conceptual Approach. Eur. J. Acc. Audit. Fin. Res. 2022, 10, 9–18. [Google Scholar]

- Li, B.; Siciliano, G.; Venkatachalam, M.; Naranjo, P.; Verdi, R.S. Economic consequences of IFRS adoption: The role of changes in disclosure quality. Contemp. Acc. Res. 2021, 38, 129–179. [Google Scholar] [CrossRef]

- Mensah, E. The effect of IFRS adoption on financial reporting quality: Evidence from listed manufacturing firms in Ghana. Econ. Res. Ekon. Istr. 2021, 34, 2890–2905. [Google Scholar] [CrossRef]

- Wijayana, S.; Gray, S.J. Institutional factors and earnings management in the Asia-Pacific: Is IFRS adoption making a difference? Manag. Int. Rev. 2019, 59, 307–334. [Google Scholar] [CrossRef]

- De Moura, A.A.F.; Altuwaijri, A.; Gupta, J. Did mandatory IFRS adoption affect the cost of capital in Latin American countries? J. Int. Acc. Audit. Tax. 2020, 38, 100301. [Google Scholar] [CrossRef]

- Mongrut, S.; Winkelried, D. Unintended effects of IFRS adoption on earnings management: The case of Latin America. Emerg. Mark. Rev. 2019, 38, 377–388. [Google Scholar] [CrossRef]

- DeFond, M.; Gao, X.; Li, O.Z.; Xia, L. IFRS adoption in China foreign institutional investments China. J. Acc. Res. 2019, 12, 1–32. [Google Scholar] [CrossRef]

- Krismiaji, K.; Surifah, S. Corporate governance, compliance level of IFRS disclosure and value relevance of accounting information–Indonesian evidence. J. Int. Stud. 2020, 13. [Google Scholar] [CrossRef]

- Boachie, C.; Mensah, E. The effect of earnings management on firm performance: The moderating role of corporate governance quality. Int. Rev. Fin. Anal. 2022, 83, 102270. [Google Scholar] [CrossRef]

- Bagais, O.; Aljaaidi, K. Corporate governance attributes and firm performance in Saudi Arabia. Accounting 2020, 6, 923–930. [Google Scholar] [CrossRef]

- Ogbeide, S.; Ogiugo, H.; Adesuyi, I. Corporate governance mechanisms and financial reporting quality of commercial banks in Nigeria. Insights Reg. Dev. 2021, 3, 136–146. [Google Scholar] [CrossRef]

- Dang, V.C.; Nguyen, Q.K. Internal corporate governance and stock price crash risk: Evidence from Vietnam. J. Sustain. Fin. Invest. 2021, 1–18. [Google Scholar] [CrossRef]

- Nguyen, Q.K.; Dang, V.C. Does the country’s institutional quality enhance the role of risk governance in preventing bank risk? Appl. Econ. Lett. 2022, 30, 850–853. [Google Scholar] [CrossRef]

- Abed, I.A.; Hussin, N.; Haddad, H.; Al-Ramahi, N.M.; Ali, M.A. The moderating effects of corporate social responsibility on the relationship between creative accounting determinants and financial reporting quality. Sustainability 2022, 14, 1195. [Google Scholar] [CrossRef]

- Nguyen, Q.K. Audit committee structure, institutional quality, and bank stability: Evidence from ASEAN countries. Fin. Res. Lett. 2022, 46, 102369. [Google Scholar] [CrossRef]

- Hashed, A.; Almaqtari, F. The impact of corporate governance mechanisms and IFRS on earning management in Saudi Arabia. Accounting 2021, 7, 207–224. [Google Scholar] [CrossRef]

- HRP, A.K.Z.; Siregar, R.A.; Muda, I. Islamic Corporate Governance and Financial Performance in Banks Listed in JII. Int. J. Econ. 2022, 1, 248–256. [Google Scholar]

- Istianingsih Earnings Quality as a link between Corporate Governance Implementation Firm Performance. Int. J. Manag. Sci. Eng. Manag. 2021, 16, 290–301.

- Key, K.G.; Kim, J.Y. IFRS and accounting quality: Additional evidence from Korea. J. Int. Acc. Audit. Tax. 2020, 39, 100306. [Google Scholar] [CrossRef]

- Khamidullina, M.; Makarova, S. The effect of the quality of corporate governance on the dividend policy of banks in the BRICS countries. BRICS J. Econ. 2021, 2, 84–106. [Google Scholar] [CrossRef]

- Kohler, H.; Pochet, C.; Gendron, Y. Networks of interpretation: An ethnography of the quest for IFRS consistency in a global accounting firm. Acc. Organ. Soc. 2021, 95, 101277. [Google Scholar] [CrossRef]

- Soliman WS, M.K. Investigating the effect of corporate governance on audit quality and its impact on investment efficiency. Invest. Manag. Fin. Innov. 2020, 17, 175–188. [Google Scholar]

- Mnif, Y.; Znazen, O. Corporate governance and compliance with IFRS 7: The case of Private banks listed in Canada. Manag. Audit. J. 2020, 35, 448–474. [Google Scholar] [CrossRef]

- Mohsin, M.; Nurunnabi, M.; Zhang, J.; Sun, H.; Iqbal, N.; Iram, R.; Abbas, Q. The evaluation of efficiency and value addition of IFRS endorsement towards earnings timeliness disclosure. Int. J. Fin. Econ. 2021, 26, 1793–1807. [Google Scholar] [CrossRef]

- Aburous, D. IFRS and institutional work in the accounting domain. Crit. Perspect. Account. 2019, 62, 1–15. [Google Scholar] [CrossRef]

- Cooray, T.; Gunarathne, A.N.; Senaratne, S. Does corporate governance affect the quality of integrated reporting? Sustainability 2020, 12, 4262. [Google Scholar]

- Jiang, F.; Kim, K.A. Corporate governance in China: A survey. Rev. Financ. 2020, 24, 733–772. [Google Scholar] [CrossRef]

- Hameedi, K.S.; Al-Fatlawi, Q.A.; Ali, M.N.; Almagtome, A.H. Financial performance reporting, IFRS implementation, and accounting information: Evidence from Iraqi banking sector. J. Asian Fin. Econ. Bus. 2021, 8, 1083–1094. [Google Scholar]

- Almuzaiqer, M.A.; Fatima, A.H.; Ahmad, M. Royal Family Members and Corporate Governance Characteristics: The Impact on Earnings Management in UA. Int. J. Bus. Soc. 2022, 23, 689–713. [Google Scholar] [CrossRef]

- Tsalavoutas, I.; Tsoligkas, F.; Evans, L. Compliance with IFRS mandatory disclosure requirements: A structured literature review. J. Int. Acc. Audit. Tax. 2020, 40, 100338. [Google Scholar] [CrossRef]

- Song, X.; Trimble, M. The historical and current status of global IFRS adoption: Obstacles and opportunities for researchers. Int. J. Acc. 2022, 57, 2250001. [Google Scholar] [CrossRef]

- Abdullah, H.; Tursoy, T. Capital structure and firm performance: Evidence of Germany under IFRS adoption. Rev. Manag. Sci. 2021, 15, 379–398. [Google Scholar] [CrossRef]

- Harisa, E.; Mohamad, A.; Meutia, I. Effect of Quality of Good Corporate Governance Disclosure, Leverage and Firm Size on Profitability of Isalmic Commercial Banks. Int. J. Econ. Fin. 2019, 9, 189. [Google Scholar] [CrossRef]

- Semenyshena, N.; Khorunzhak, N.; Zadorozhnyi, Z.M. The institutionalization of accounting: The impact of national standards on the development of economies. Indep. J. Manag. Prod. 2020, 11, 695–711. [Google Scholar] [CrossRef]

- He, X.; Pittman, J.A.; Rui, O.M.; Wu, D. Do social ties between external auditors and audit committee members affect audit quality? Acc. Rev. 2017, 92, 61–87. [Google Scholar] [CrossRef]

- Almaqtari, F.A.; Hashed, A.A.; Shamim, M. Impact of corporate governance mechanism on IFRS adoption: A comparative study of Saudi Arabia, Oman, and the United Arab Emirates. Heliyon 2021, 7, e05848. [Google Scholar] [CrossRef] [PubMed]

- Wahyuni, E.T.; Puspitasari, G.; Puspitasari, E. Has IFRS improved accounting quality in Indonesia? A Systematic Literature Review of 2010–2016. J. Acc. Investig. 2020, 21, 19–44. [Google Scholar] [CrossRef]

- Karaye, A.I.; Zaluki NA, A.; Badru, B.O. Literature Gap on Corporate Governance Mechanisms and Bank Asset Quality. Global Bus. Manag. Rev. 2021, 13, 51–67. [Google Scholar]

- Bouteska, A.; Mili, M. Does corporate governance affect financial analysts’ stock recommendations, target prices accuracy and earnings forecast characteristics? An empirical investigation of US companies. Empir. Econ. 2022, 63, 2125–2171. [Google Scholar] [CrossRef]

- Correa-Garcia, J.A.; Garcia-Benau, M.A.; Garcia-Meca, E. Corporate governance and its implications for sustainability reporting quality in Latin American business groups. J. Clean. Prod. 2020, 260, 121142. [Google Scholar] [CrossRef]

- El-Helaly, M.; Ntim, C.G.; Al-Gazzar, M. Diffusion theory, national corruption and IFRS adoption around the world. J. Int. Acc. Audit. Tax. 2020, 38, 100305. [Google Scholar] [CrossRef]

- Roychowdhury, S.; Shroff, N.; Verdi, R.S. The effects of financial reporting and disclosure on corporate investment: A review. J. Acc. Econ. 2019, 68, 101246. [Google Scholar] [CrossRef]

- Shaker, A.S.; Ezghayer, H.B.; Adam, M.A. Corporate Governance and Quality of Employees Performance: A Conceptual Analysis. Int. J. Psychosoc. Rehabil. 2020, 24, 4957. [Google Scholar]

- Boujelben, S.; Kobbi-Fakhfakh, S. Compliance with IFRS 15 mandatory disclosures: An exploratory study in telecom and construction sectors. J. Fin. Rep. Account. 2020, 18, 707–728. [Google Scholar] [CrossRef]

- Tran, T.; Ha, X.; Le, T.; Nguyen, N. Factors affecting IFRS adoption in listed banks: Evidence from Vietnam. Manag. Sci. Lett. 2019, 9, 2169–2180. [Google Scholar] [CrossRef]

- Wong, F.S.; Ganesan, Y.; Pitchay, A.A.; Haron, H.; Hendayani, R. Corporate governance and business performance: The moderating role of external audit quality. J. Gov. Integr. 2019, 2, 34–44. [Google Scholar] [CrossRef]

- Zahid, R.A.; Simga-Mugan, C. An analysis of IFRS and SME-IFRS adoption determinants: A worldwide study. Emerg. Mark. Fin. Trade 2019, 55, 391–408. [Google Scholar] [CrossRef]

- Ballas, P.; Garefalakis, A.; Lemonakis, C.; Balla, V. Quality of financial reporting under IFRS and corporate governance influence: Evidence from the Greek banking sector during crisis. J. Gov. Regul. 2019, 8. [Google Scholar] [CrossRef]

- Uwuigbe, O.R.; Olorunshe, O.; Uwuigbe, U.; Ozordi, E.; Asiriuwa, O.; Asaolu, T.; Erin, O. Corporate governance and financial statement fraud among listed firms in Nigeria. IOP Conf. Ser. Earth Environ. Sci. 2019, 331, 012055. [Google Scholar] [CrossRef]

- Dang, H.N.; Pham, C.D.; Nguyen, T.X.; Nguyen HT, T. Effects of corporate governance and earning quality on listed Vietnamese firm value. J. Asian Fin. Econ. Bus. 2020, 7, 71–80. [Google Scholar] [CrossRef]

- Arniati, T.; Puspita, D.A.; Amin, A.; Pirzada, K. The implementation of good corporate governance model and auditor independence in earnings’ quality improvement. Entrep. Sustain. Issues 2019, 7, 188. [Google Scholar] [CrossRef] [PubMed]

- Al-Gamrh, B.; Ku Ismail, K.N.I.; Ahsan, T.; Alquhaif, A. Investment opportunities, corporate governance quality, and firm performance in the UAE. J. Acc. Emerg. Econ. 2020, 10, 261–276. [Google Scholar] [CrossRef]

- Almagtome, A.; Khaghaany, M.; Önce, S. Corporate governance quality, stakeholders’ pressure, and sustainable development: An integrated approach. Int. J. Math. Eng. Manag. Sci. 2020, 5, 1077. [Google Scholar] [CrossRef]

- Alsaadi, M.A.; Tijjani, B.; Falgi, K.I. Corporate Governance and Quality of Financial Reporting of Listed Firms: Evidence from Saudi Arabia. Corp. Gov. 2021, 15, 392–410. [Google Scholar]

- Zulfiati, L.; Fadhillah, I.S. Effect of Corporate Governance and Financial Reporting Quality on Asymmetry Information. In Proceedings of the 5th Annual International Conference on Accounting Research (AICAR 2018), Manado, Indonesia, 8–9 August 2018; Atlantis Press: Dordrecht, The Netherlands, 2019; pp. 126–128. [Google Scholar]

{kind=link}

{kind=link}

| Gender | ||

|---|---|---|

| Frequency | Percent | |

| Male | 168 | 56.38%. |

| Female | 130 | 43.62%. |

| Total | 298 | 100.0 |

| Age | ||

| 20–29 | 82 | 27.52% |

| 30–39 | 53 | 17.79% |

| 40–49 | 55 | 18.46% |

| 50–59 | 65 | 21.81% |

| 60–69 | 43 | 14.43% |

| Total | 298 | 100.0 |

| Level of Education | ||

| Diploma | 22 | 7.38% |

| Bachelor | 113 | 37.92% |

| Master | 85 | 28.52% 65 |

| PhD | 65 | 21.81% |

| Others | 13 | 4.36% |

| Total | 298 | 100.0 |

| Reliability Statistics | ||

|---|---|---|

| Variables | Cronbach Alpha | n of Items |

| Board Characteristics | 0.749 | 8 |

| CEO Duality | 0.751 | 8 |

| Ownership Structure | 0.769 | 9 |

| Audit Committee Independence | 0.774 | 8 |

| Accountability Structure | 0.719 | 9 |

| Directors’ competency | 0.733 | 10 |

| Adoption of IFRS | 0.758 | 8 |

| Financial Reporting Quality | 0.791 | 10 |

| Correlation | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| BC | CD | OS | AC | AS | DC | AI | RFQ | ||

| Board Characteristics (BC) | Pearson Correlation | 1 | |||||||

| Sig. (2-tailed) | |||||||||

| n | 298 | ||||||||

| CEO Duality (CD) | Pearson Correlation | 0.489 ** | 1 | ||||||

| Sig. (2-tailed) | 0 | ||||||||

| n | 298 | 298 | |||||||

| Ownership Structure (OS) | Pearson Correlation | 0.594 ** | 0.601 ** | 1 | |||||

| Sig. (2-tailed) | 0.000 | 0.000 | |||||||

| n | 298 | 298 | 298 | ||||||

| Audit Committee (AC) | Pearson Correlation | 0.431 ** | 0.564 ** | 0.617 ** | 1 | ||||

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | ||||||

| n | 298 | 298 | 298 | 298 | |||||

| Accountability Structure (AS) | Pearson Correlation | 0.573 ** | 0.648 ** | 0.544 ** | 0.622 ** | 1 | |||

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| n | 298 | 298 | 298 | 298 | 298 | ||||

| Director’s Competency (DC) | Pearson Correlation | 0.668 ** | 0.539 ** | 0.448 ** | 0.395 ** | 0.366 ** | 1 | ||

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||||

| n | 298 | 298 | 298 | 298 | 298 | 298 | |||

| Adoption of IFRS (AI) | Pearson Correlation | 0.294 ** | 0.471 ** | 0.578 ** | 0.679 ** | 0.647 ** | 0.575 ** | 1 | |

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||

| n | 298 | 298 | 298 | 298 | 298 | 298 | 298 | ||

| Reporting Financial Quality (RFQ) | Pearson Correlation | 0.609 ** | 0.623 ** | 0.598 ** | 0.572 ** | 0.633 ** | 0.651 ** | 0.593 ** | 1 |

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| n | 298 | 298 | 298 | 298 | 298 | 298 | 298 | 298 | |

| Item | S.R.W | S.E. | C.R. | p |

|---|---|---|---|---|

| Board Characteristics | 0.701 | 0.036 | 6.881 | *** |

| CEO Duality | 0.723 | 0.033 | 5.312 | *** |

| Ownership Structure | 0.699 | 0.036 | 10.313 | *** |

| Audit Committee Independence | 0.714 | 0.076 | 11.382 | *** |

| Accountability Structure | 0.801 | 0.035 | 10.739 | *** |

| Directors’ competency | 0.872 | 0.032 | 5.675 | *** |

| Adoption of IFRS | 0.814 | 0.039 | 7.569 | *** |

| Corporate Governance | 0.787 | 0.041 | 6.734 | *** |

| Financial Reporting Quality | 0.773 | 0.039 | 4.643 | *** |

| Path | Effect Coefficient | S.E. | C.R. | p | ||

|---|---|---|---|---|---|---|

| Board Characteristics | <--- | Financial Reporting Quality | 0.576 | 0.042 | 2.51 | *** |

| CEO Duality | <--- | Financial Reporting Quality | 0.753 | 0.043 | 2.445 | *** |

| Ownership Structure | <--- | Financial Reporting Quality | 0.613 | 0.028 | 6.338 | *** |

| Audit Committee Independence | <--- | Financial Reporting Quality | 0.753 | 0.029 | 4.352 | *** |

| Accountability Structure | Financial Reporting Quality | 0.611 | 0.38 | 3.489 | *** | |

| Directors’ competency | Financial Reporting Quality | 0.732 | 0.026 | 2.371 | *** | |

| Hypotheses | Direction | Indirect | p Value | Mediation |

|---|---|---|---|---|

| H1 | BC → IFRS → FRQ | 0.519 ** | 0.000 | Supported |

| H2 | CD → IFRS → FRQ | 0.623 ** | 0.000 | Supported |

| H3 | OS → IFRS → FRQ | 0.701 ** | 0.000 | Supported |

| H4 | ACI → IFRS → FRQ | 0.663 ** | 0.000 | Supported |

| H5 | AS → IFRS → FRQ | 0.599 ** | 0.000 | Supported |

| H6 | DC → IFRS → FRQ | 0.801 ** | 0.000 | Supported |

| No. of Hypotheses | Hypothesis Statement | Status |

|---|---|---|

| H1 | H1: The adoption of IFRS has a mediating effect on the relationship between board characteristics and financial reporting quality. | Accepted |

| H2 | H2: The adoption of IFRS has a mediating effect on the relationship between CEO duality and financial reporting quality. | Accepted |

| H3 | H3: The adoption of IFRS has a mediating effect on the relationship between ownership structure and financial reporting quality. | Accepted |

| H4 | H4: The adoption of IFRS has a mediating effect on the relationship between audit committee independence and financial reporting quality | Accepted |

| H5 | H5: The adoption of IFRS has a mediating effect on the relationship between accountability structure and financial reporting quality. | Accepted |

| H6 | H6: The adoption of IFRS has a mediating effect on the relationship between directors’ competency and financial reporting quality. | Accepted |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gardi, B.; Aga, M.; Abdullah, N.N. Corporate Governance and Financial Reporting Quality: The Mediation Role of IFRS. Sustainability 2023, 15, 9869. https://doi.org/10.3390/su15139869

Gardi B, Aga M, Abdullah NN. Corporate Governance and Financial Reporting Quality: The Mediation Role of IFRS. Sustainability. 2023; 15(13):9869. https://doi.org/10.3390/su15139869

Chicago/Turabian StyleGardi, Bayar, Mehmet Aga, and Nabaz Nawzad Abdullah. 2023. "Corporate Governance and Financial Reporting Quality: The Mediation Role of IFRS" Sustainability 15, no. 13: 9869. https://doi.org/10.3390/su15139869

APA StyleGardi, B., Aga, M., & Abdullah, N. N. (2023). Corporate Governance and Financial Reporting Quality: The Mediation Role of IFRS. Sustainability, 15(13), 9869. https://doi.org/10.3390/su15139869