Abstract

The relationship between Sustainability Reporting and corporate financial performance is overlapping and multifaceted and it has been an interesting issue for both academics and professionals since the beginning of the millennium. Studies have found divergent results on this relation and the industrial differences are omitted in many papers. Moreover, studies considering developing countries are scarce. The purpose of this study is to shed light on the relationship between sustainability reporting and firm performance in a developing country context. The impact of sustainability reporting is investigated using pooled ordinary least square (OLS) method for panel data regression through two models based on Tobin’s Q and ROA. A total of 920 observations for 46 companies with 3 different impact levels based on their environmental effect and 5-year quarterly panel data between 2016–2020. The research used data from Borsa Istanbul (Istanbul Stock Exchange) and also independent variables such as leverage, risk, size, current ratio, growth, sustainability reporting, and the environmental impact level of companies. The results showed that sustainability reporting has a significant positive impact on financial performance according to the ROA model, and a significant negative correlation between risk and financial performance according to both ROA and Tobin’s Q models. Considering the environmental impact of companies, the results also reveal a positive relationship between high impact companies’ sustainability reporting and short-term financial performance as ROA is an accounting-oriented measure that reveals the company’s short-term financial performance. Further research should investigate the impact of sustainability reporting in different markets based on the impact level of companies and the development degree of countries.

1. Introduction

Sustainability reporting (SR) is one of the prominent research areas which has received exponentially increasing attention in recent years. SR covers environmental, social, and governance (ESG) issues and sustainability concerns that stakeholders demand from organizations to manage their risks and opportunities. To ensure accountability and transparency, there is a tendency to create a new global system for SR. In 2021 and 2022, tremendous advances have been realized concerning regulations and standards. In November 2021, the IFRS (International Financial Reporting Standards) Foundation Trustees released the establishment of the International Sustainability Standards Board (ISSB) to prepare a global sustainability-related standard. Meanwhile, the European Council in December 2022 accepted the Corporate Sustainability Reporting Directive (CSRD) which generated the release of European Sustainability Reporting Standards (ESRS) by the European Financial Reporting Advisory Group (EFRAG). The latter means that approximately 50,000 companies must disclose data according to ESRS, which will start applying between 2024 and 2028. With this fast evolution of the SR landscape, it is expected that this prevalently discussed topic will continue to be discussed as it has no consistent conclusions about its impact on corporate financial performance [1].

Sustainable reporting can be defined as the measurement, disclosure, and accountability of organizational performance in achieving sustainable development goals to internal and external stakeholders [2]. Thus, SR can reduce the information asymmetry and increase the transparency of the company’s sustainability activities and incite investors to direct their investments to companies with positive impacts. Moreover, SR gives a competitive advantage to the companies, in their market or industry [3]. Considering these advantages, companies try to profit from SR and publish their reports. However, the studies in the field also report an insignificant or inverse relationship between SR and financial performance. So, some studies report an increased financial performance [4,5,6,7], albeit others state an inverse [8,9] or an inconclusive relationship between them [10,11,12]. Ref. [13] affirmed on the impact of SR on financial performance that most of the studies pointed to a positive relationship between SR and financial performance. However, due to the mixed results, ref. [13] also recommended further research may yield more consistent findings. Thus, researchers have noticed that consequent to these different findings, sectoral analysis is scarce in SR [14,15]. Indeed, as the ESG factors vary from one sector to the other, analyzing the relationship between SR and financial performance without categorizing the sectors may be the reason behind these mixed results [16,17]. So, these studies with these divergent results lack a sectorial approach to sustainability reporting [18]. The sectorial differences, the development stage of the market in the study, and the measurement choices shape the impact of SR. Although many studies have considered the impact of SR from a holistic point of view [14], scant attention has been paid to sectorial differences on this topic.

It affirmed that the political, social, and economic characteristics of developing countries affect the SR approach of the companies in these countries [19]. Moreover, most of the world’s population lives in developing countries. Therefore, this study aims to elucidate the relationship between SR and firm performance in a developing country context. This paper synthesizes recent studies to use three sectorial levels (high, medium, and low impact sectors) and two different measures. This approach considers the accounting and market measures that show the short-term and long-term impact of SR on performance and the effect of the firm’s industry’s impact level on the environment.

The gap in the literature stems from the divergent results, the consideration of sectorial differences, and the developing country context. Accordingly, this study is expected to add to the literature and guide further research on this topic, especially with the two models of performance and classification of firms.

This study has several contributions to the literature. Firstly, it posits the impact of companies’ SR practices on the market-oriented as well as accounting-oriented measures, respectively, for long-term and short-term financial performance, specifically in a developing country. Secondly, although previous studies have made cross-sectoral analyses [20], this research categorizes sectors in terms of their environmental effects consisting of three categories covering industry groups. Finally, the results aim to broaden the insight into SR implications for a firm’s financial performance and shed light on sectoral divergence, which should help the stakeholders understand the meaning and the necessity of recently mandated SR.

This paper is presented as follows: we will review the relevant literature and describe the hypothesis, the data used, and the research methodology. The conclusion and the recommendations for future research are discussed in the final section.

2. Literature Review

The terms SR and ESG are used interchangeably and in an overlapping manner in the literature [21]. Some studies assess the link between financial performance and ESG factors [22], and some others fulfill this aim by using sustainability reports [23,24]. However, this is not entirely accurate. It must be emphasized that SR refers to the information that companies provide about their performance to the outside world on a regular basis in a structured way. Through sustainability reporting, companies communicate their performance and impact on a wide range of sustainability topics, spanning environmental, social, and governance parameters. ESG reports on the other side are reporting frameworks, disclosing environmental, social, and corporate governance data and they can be included in the Sustainability Reports.

According to the stakeholder theory, companies need to fulfill the expectations of diverse stakeholders, not only by disclosing financial, but also non-financial information. Hence, SR by providing transparency and accountability enables stakeholders to make informed and conscious decisions. In the meantime, organizations can identify where they are not meeting societal expectations and can take steps to solve these issues, which are in line with the legitimacy theory [25] and the stakeholder theory [26,27]. Therefore, from the perspective of stakeholder theory, companies can highlight their reputation, gain the support of the stakeholders, and attract investments, which lead to better financial performance [28,29,30]. The demonstration of the commitment to sustainability and building trust with stakeholders and thus, with society, will affect the financial success in the long term and create value, as legitimacy is vital for the long-run prosperity of the company [31,32].

In this line of research, mixed results are obtained based on accounting measures as well as market measures. Return on Assets (ROA) is widely used in numerous studies to measure the accounting aspects, and their relationship with SR disclosed, respectively, a positive relationship in some studies [33,34,35], a negative in some others [36], or insignificance [37,38]. Market performance is measured in many others with Tobins’ Q [39,40,41,42] to assure the accountability and transparency of the firm value. Table 1 resumes the recent studies about SR and firm performance.

Table 1.

Recent literature review of SR, ESG factors, and financial performance.

As shown in Table 1, recent studies use different measures on different markets. Although these studies have found mainly positive relationships between SR and firm performance indicators, previous studies have found insignificant and negative relationships and their focus is on developed markets. These recent studies suggest that managers should allocate a proportion of their resources towards reporting on their attempts to mitigate the harmful impacts of their business operations, especially those in high-impact industries whose operations could be remarkably destructive. Accordingly, firms are classified as high, medium, or low impact based on their environmental effect according to FTSE in our study. Moreover, our focus is on developing market firms and analysis is based on market and accounting measures.

3. Materials and Methods

XU100 and XUSRD are indices in Borsa Istanbul (BIST). BIST indices the companies that report their SR activities on BIST Sustainability Index (XUSRD). BIST 100 Index (XU100) is a capitalization-weighted index that tracks the financial performance of 100 primary companies chosen from the National Market. Accordingly, all firms in the sample are selected from XU100 and XUSRD indices to have accurate and detailed data.

The sample used in the research consists of a total of 46 firms all included in XU100. As the financial firms have different approaches in their financial statements, they are excluded from the analysis to prevent any bias. So, the firms used in the analysis are all in XU100 and non-financial. Thirty-one of them are publishing Sustainability Reports and they have been in the BIST Sustainability Index (XUSRD) for the whole 5-year period uninterruptedly. Fifteen others are also XU100 firms, but they do not practice SR or have continuously published Sustainability Reports for the research period. We finally have 920 observations for 46 companies and 5-year quarterly panel data between 2016–2020.

Our sample has 9 sectors and 15 industry groups. We use Standard and Poor’s Global Industry Classification Standard (GICS) to determine the sectors and industry groups, combine the data of the sector and industry group from Wharton Research Data Services, Compustat Global Database, and collect all financial data from Bloomberg Database. Similar databases have been widely applied in the literature by researchers and academicians examining the relation between SR and financial performance (e.g., [49,50,51,52,53]). Table 2 shows sample company classification by sector.

Table 2.

Company classification by sector.

Table 3 shows company classification by industry group.

Table 3.

Company classification by industry group.

Sample companies are classified as high, medium, or low impact based on their environmental effect according to FTSE (Financial Times Stock Exchange) Russell, which is in the London Stock Exchange Group. The FTSE sector classification is in Table 4.

Table 4.

Sector Classification.

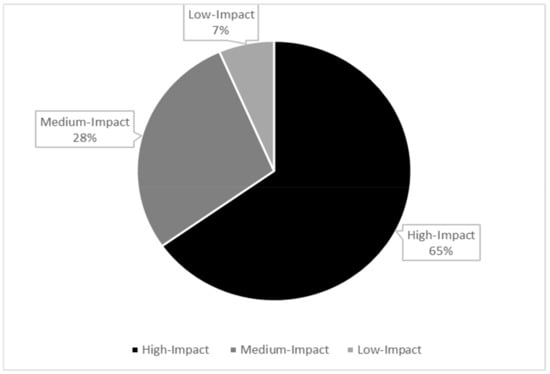

Our sample has 30 companies with high impact, 13 with medium impact, and 3 with low impact on the environment. Of the sample, 18 high-impact companies, 10 medium-impact companies, and 3 low-impact companies have corporate sustainability reporting. Figure 1 shows the sector impact percentages of companies in the total sample, with 65% high impact and 28% medium impact sector.

Figure 1.

Sector impact percentages.

Table 5 presents the variables of our two models. The dependent variables are Tobin’s Q and ROA. In Model 1, Tobin’s Q is a market-oriented measure for long-term financial performance [54,55], whereas ROA is an accounting-oriented measure that reveals the company’s short-term financial performance [56] in Model 2. The independent variables include leverage, risk, size, current ratio, growth, SR, high impact, medium impact, and low impact. SR is a dummy variable that takes the value 1 when the company is in XUSRD and 0 otherwise. These are variables used in similar studies in the literature to measure different aspects of performance (e.g., [57,58]). Moreover, high impact, medium impact, and low impact are dummy variables that have the value 1 when they belong to high, medium, and low effects on the environment, and others are 0. All variables were winsorized with 0.1 value to trim outliers. We use the pooled ordinary least square (OLS) method for panel data regression using Stata 15 for the analysis to estimate Models 1 and 2, testing the relationship between SR and financial performance [59]. As the results of the relationships between variables are mixed in the literature based on both accounting measures (ROA model) and market measures (Tobins’ Q model). The study aims to analyze the relationship between sustainability reporting and firm performance, using two equations based on accounting and market dimensions of performance. The models are constructed to encapsulate the effects of sustainability reporting on firm performance. They are as follows:

Table 5.

Variables.

(1) Tobin’s Q = β0 + β1 Riski,t + β2 Leverage,t + β3 Sizei,t + β4 Current Ratioi,t + β5 Growthi,t + β6 High Impacti,t + β7 Medium Impacti,t + β8 SRi,t + εi,t;

(2) ROA = β0 + β1 Riski,t + β2 Leverage,t + β3 Sizei,t + β4 Current Ratioi,t + β5 Growthi,t + β6 High Impacti,t + β7 Medium Impacti,t + β8 SRi,t + εi,t.

In these models, we used Robust standard errors to consider heteroscedasticity and autocorrelation in the panel dataset. The reason for robust standard errors in panel data is that the idiosyncratic errors can have heteroskedasticity or autocorrelation, or both. Robust standard errors account for heteroskedasticity in a model’s unexplained variation. That is, if the amount of variation in the outcome variable is correlated with the explanatory variables, robust standard errors can take this correlation into account to obtain unbiased standard errors of OLS coefficients. [45,60,61]. A length of 5 years is used in the analysis and the results turn out to be quite robust to changes in the selected length.

4. Results

First, we analyzed the descriptive statistics of panel data as presented in Table 6. There were no missing values in the panel data. According to our 920 observations, the data show that ROA has the lowest mean (0.57), while Tobin’s Q has (1.34) as the mean value and size has the highest value (15.82).

Table 6.

Descriptive statistics.

The mean variance inflation factor (VIF) is below 5 as shown in Table 7, so there is no multicollinearity in the model. Low-impact sectors were omitted because of collinearity in the regression analysis. We used robust regression because heteroscedasticity is present according to Breusch–Pagan/Cook–Weisberg test.

Table 7.

The mean variance inflation factor and VIF Values.

The results displayed in Table 8 show that Model 1 and Model 2 have a high explanatory power and statistical significance as they have F-tests with p values less than 5%. The results also reveal that the independent variables explain 27% of the variation of ROA and, respectively, 27.2% of the variation of Tobin’s Q according to the R-squared value.

Table 8.

Summary of regression analysis for panel data.

Tobin’s Q Model shows that risk (β = −0.0914), size (β = −0.117), and medium impact (β = −0.145) have a negative significant effect on Tobin’s Q, while leverage (β = 1.219), current ratio (β = 0.169), growth (β = 0.0190), high impact (β = 0.0850) have a positive significant effect on Tobin’s Q. Accordingly, the model indicates SR does not influence the long-term financial performance.

ROA Model indicates that risk (β = −0.0141) and size (β = −0.00411) have a negative significant effect on ROA, while current ratio (β = 0.0187), growth (β = 0.00353), high impact (β = 0.0236), and SR (β = 0.0281) have a positive significant effect on ROA. Moreover, the model shows that leverage and medium impact do not influence the company’s short-term financial performance.

5. Discussion

The purpose of the study is to analyze the relationship between SR and financial performance, taking into consideration the market-oriented and accounting-oriented measures that enable to have a long-term and short-term perspective in a developing country context. Although this method has been used in other similar studies using cross-sectoral analysis (e.g., [20]), this research categorized sectors into 3 groups in terms of their environmental effects. The analysis showed that market-oriented and accounting-oriented data both have an impact on financial performance. The SR showed a significant positive impact on ROA, a short-term oriented measure.

We used the data from listed companies in XU100 and XUSRD indices in Borsa Istanbul (BIST) as a research sample making a total of 920 observations for 46 companies and 5-year quarterly panel data between 2016–2020, covering 9 sectors and 15 industry groups.

Based on our empirical analysis, SR has a significant positive impact on financial performance according to ROA, the accounting-oriented model, although this relation seems to be conflicting, as suggested by Buallay (2021). SR and related activities can help companies build trust-based relationships with consumers and enhance corporate reputation to improve financial performance. The model also indicates SR does not influence long-term market performance [46,62].

In addition, there is a significant negative correlation between risk and financial performance according to both two ROA and Tobin’s Q models. Risk is related to the total obligations of the company. Accordingly, an increase in risk makes it difficult to reach credit with low interest and causes additional financial costs, decreasing ROA [48,63]. Concerning Tobin’s Q, we can affirm that the higher risk of a company affects market perception negatively.

Our sample is composed mainly of industrial and consumer discretionary sectors. In these sectors, it is not easy to reflect asset investments’ effect on profit in the short term. Thus, ROA and size are negatively related [22]. Accordingly, the market also responds negatively to the size as even in the long term; it is difficult to reach higher profits from an investment made by large companies. The companies in the sample are already at a certain size; therefore, investors do not expect extraordinary returns from total asset investments causing a negative relationship between size and Tobin’s Q [64].

Current ratio is an essential indicator of liquidity, and the consequently higher current ratio has a significant positive impact on ROA and Tobin’s Q [22]. Current ratio variations [22] and growth [64] affect Tobin’s Q in the same direction.

Considering the environmental impact of companies, the results reveal a positive relationship between higher impact and ROA as most companies in our sample report sustainability. Corporate sustainability reporting enhances the company’s reputation, improves stakeholders’ perception, and strengthens its position in the market to be more profitable [24,39,46,62,64]. The ROA model results encourage companies with sustainability-based organizational structures to have a higher short-term financial performance than the others [48].

High impact sector gives much more detailed information about the environmental issues such as the methods used for manufacturing or the minimum damage they are causing to the environment, for examples, whereas the medium-impact sector highlights primarily the social and governmental issues emphasizing gender equality, human rights, transparency, and accountability. Hence, this study reports that the stakeholders value high-impact sector SR in the short term and the long term significantly in terms of ROA and Tobin’s Q, which is in line with stakeholder and legitimacy theory, albeit the medium impact sector’s SR efforts are not considered as such by stakeholders. Environmental investments in medium-effect sectors do not convince investors of their necessity, unlike high-impact sectors.

Creditors and investors perceive high financial leverage as a sign of companies’ profit as it is used to amplify returns from an investment. Hence, demand for stock and stock price will increase [22]. However, the leverage level has no significant effect on ROA in the short-term as the investment generally produces an outcome in the long-term; therefore, it has a significant positive effect on Tobin’s Q.

Companies pursuing SR are well aware that SR facilitates their efforts in building and protecting their corporate reputation, satisfying their stakeholders through the SR while generating positive outcomes in diverse financial performance objectives. Even in a developing country market, where investors are more short-term oriented, SR has many positive outcomes in our work as companies legitimize their SR activities and affect the expectations of various stakeholders via SR [65]. This is because when a company is committed to SR, it strengthens its reputation and gains the trust of the stakeholders while maintaining operational, financial, and market performance. However, differently, in Tobin’s Q model, the SR variable has an insignificant effect, but the leverage has a positive impact. The effect of leverage comes from the positive expectations of market investors.

Our study shows that companies which practice SR have higher values of financial performance in the short term, in line with works such as [4]. According to the results, the current ratio, growth, and the impact degree of the companies have a significant positive impact both in the short and long term. SR is more considered in the short term and leverage in the long term. Thus, the analysis emphasizes the opinion that SR benefits companies with a better reputation and image and is more approved by markets even if they have a high impact, which instead reveals short and long-term benefits.

The risk and size variables both have significant negative effects. These results contribute to the relationship between SR and financial performance and show that profitability or the market is not affected negatively by sustainability initiatives based in an emerging market.

6. Implications and Further Research

The research has important implications for researchers who are interested in a more thorough exploration of the impact of SR on financial performance, as well as for practitioners who envision sustainability as the primary component of their business in the near future. The overall objective of this research is to understand the impact of SR on financial performance considering market and accounting measures and the industry of the firm in a developing country context. Although developing countries follow the developed ones in many issues, sustainability is very rapidly gaining importance in every market due to globalization and regulations. Future research can investigate this impact in different contexts. We, therefore, encourage future research to include other variables such as ownership structures and corporate governance indicators. Hence, future work might need to evaluate different firm-level or industry-level characteristics and the impact of SR on organizational outcomes. We also recommend that future research could consider a larger sample size or comparison of two or more different markets to have a larger perspective. Furthermore, future research can also consider the implications of new technologies such as blockchain on sustainability practices and their impact on firms’ financial performance.

This research offers genuine insights for practitioners who envision sustainability as a primary component of their business. The positive relationships shown in the results express the importance of sustainability reporting and its positive impact on many perspectives, especially on ROA. Moreover, the analysis also highlights that SR helps companies build a better reputation and image which is more approved by all stakeholders. So, practitioners must consider the results of this study in their decision-making. Theoretically, the study contributes to the literature primarily via the addition of results from a developing market and the classification of firms into three industry categories.

7. Conclusions

The findings deduced from the study highlight that SR positively affects the accounting measures of the leading non-financial firms of a developing country in accordance with the findings of many previous studies, e.g., [22,46]. This positive effect is also well valued by investors, especially for higher impact firms in the short and long term. Moreover, the growth and the current ratio variables also has a positive impact on ROA and Tobin’s Q as they are truly important for stakeholders. Accordingly, in this developing country context, stakeholders such as investors, shareholders, creditors, and debtors are recommended to increase their knowledge about SR and its importance in the business in order to make better investment choices. Furthermore, the risk and size variables display that profitability and the market are not affected negatively by SR. So, finally, we suggest that firms in developing countries focus more on sustainability reporting as a driver for better performance.

Author Contributions

Conceptualization, B.D., A.İ.K. and C.D.; methodology, B.D., A.İ.K. and C.D.; software, B.D., A.İ.K. and C.D.; validation, B.D., A.İ.K. and C.D.; formal analysis, B.D., A.İ.K. and C.D.; investigation, B.D., A.İ.K. and C.D.; resources, B.D., A.İ.K. and C.D.; data curation, B.D., A.İ.K. and C.D.; writing—original draft preparation, B.D., A.İ.K. and C.D.; writing—review and editing, B.D., A.İ.K. and C.D.; visualization, B.D., A.İ.K. and C.D.; supervision, B.D., A.İ.K. and C.D.; project administration, B.D., A.İ.K. and C.D.; funding acquisition, B.D., A.İ.K. and C.D. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data can be retrieved from mentioned databases.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Buallay, A.; Fadel, S.M.; Al-Ajmi, J.Y.; Saudagaran, S. Sustainability reporting and performance of MENA banks: Is there a trade-off? Meas. Bus. Excell. 2020, 24, 197–221. [Google Scholar] [CrossRef]

- Girón, A.; Kazemikhasragh, A.; Cicchiello, A.F. Sustainability Reporting and Firms’ Economic Performance: Evidence from Asia and Africa. J. Knowl. Econ. 2021, 12, 1741–1759. [Google Scholar] [CrossRef]

- Milne, M.J.; Gray, R. W(h)ither Ecology? The Triple Bottom Line, the Global Reporting Initiative, and Corporate Sustainability Reporting. J. Bus. Ethics 2013, 118, 13–29. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Dixon-Fowler, H.R.; Slater, D.J.; Johnson, J.L. Beyond “Does it Pay to be Green?” A Meta-Analysis of Moderators of the CEP–CFP Relationship. J Bus Ethics 2013, 112, 353–366. [Google Scholar] [CrossRef]

- Albertini, E. Does Environmental Management Improve Financial Performance? A Meta-Analytical Review. Organ. Environ. 2013, 26, 431–457. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Investig. 2015, 5, 210–233. [Google Scholar] [CrossRef]

- Duque-Grisales, E.; Aguilera-Caracuel, J. Environmental, Social, and Governance (ESG) Scores and Financial Performance of Multilatinas: Moderating Effects of Geographic International Diversification and Financial Slack. J. Bus. Ethics 2019, 168, 315–334. [Google Scholar] [CrossRef]

- Landi, G.; Sciarelli, M. Towards a More Ethical Market: The Impact of ESG Rating on Corporate Financial Performance. Soc. Responsib. J. 2019, 15, 11–27. [Google Scholar] [CrossRef]

- Ortas, E.; Roger, L.; José, B.; Moneva, M. Socially Responsible Investment and cleaner production in the Asia Pacific: Does it pay to be good? J. Clean. Prod. 2013, 52, 272–280. [Google Scholar] [CrossRef]

- Brooks, C.; Oikonomou, I. The effects of environmental, social and governance disclosures and performance on firm value: A review of the literature in accounting and finance. Br. Account. Rev. 2018, 50, 1–15. [Google Scholar] [CrossRef]

- Atan, R.; Alam, M.M.; Said, J.; Zamri, M. The Impacts of Environmental, Social, and Governance Factors on Firm Performance: Panel Study of Malaysian Companies. Manag. Environ. Qual. Int. J. 2018, 29, 182–194. [Google Scholar] [CrossRef]

- Aggarwal, P. Impact of Sustainability Performance of Company on its Financial Performance: A Study of Listed Indian Companies. Glob. J. Man. Bus. Res. 2013, 13, 11. [Google Scholar]

- Pojasek, R.B. A framework for business sustainability. Environ. Qual. Manag. 2007, 17, 81–88. [Google Scholar] [CrossRef]

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does It Pay to Be Good? A Meta-Analysis and Redirection of Research on the Relationship between Corporate Social and Financial Performance. Ann. Arbor. 2007, 1001, 1–68. [Google Scholar]

- Barnett, M.L. Stakeholder Influence Capacity and the Variability of Financial Returns to Corporate Social Responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Soana, M.G. The Relationship between Corporate Social Performance and Corporate Financial Performance in the Banking Sector. J. Bus. Ethics 2011, 104, 133–148. [Google Scholar] [CrossRef]

- Qiu, Y.; Shaukat, A.; Tharyan, R. Environmental and Social Disclosures: Link with Corporate Financial Performance. The Br. Account. Rev. 2016, 48, 102–116. [Google Scholar] [CrossRef]

- Haider, M.; Shannon, R.; Moschis, G.P. Sustainable Consumption Research and the Role of Marketing: A Review of the Literature (1976–2021). Sustainability 2022, 14, 3999. [Google Scholar] [CrossRef]

- Al Hawaj, A.Y.; Buallay, A.M. A Worldwide Sectorial Analysis of Sustainability Reporting and Its Impact on Firm Performance. J. Sustain. Financ. Investig. 2022, 12, 62–86. [Google Scholar] [CrossRef]

- Dinh, T.; Husmann, A.; Melloni, G. Corporate Sustainability Reporting in Europe: A Scoping Review. Account. Eur. 2023, 20, 1–29. [Google Scholar] [CrossRef]

- Thomas, C.J.; Tuyon, J.; Matahir, H.; Dixit, S. The impact of sustainability practices on firm financial performance: Evidence from Malaysia. Manag. Account. Rev. 2021, 20, 211–243. [Google Scholar]

- Buallay, A.; Al Marri, M. Sustainability disclosure and its impact on telecommunication and information technology sectors’ performance: Worldwide evidence. Int. J. Emerg. Serv. 2022, 11, 379–395. [Google Scholar] [CrossRef]

- Najjar, M.; Alsurakji, I.H.; El-Qanni, A.; Nour, A.I. The role of blockchain technology in the integration of sustainability practices across multi-tier supply networks: Implications and potential complexities. J. Sustain. Financ. Invest. 2023, 13, 744–762. [Google Scholar] [CrossRef]

- Patten, D.M. Exposure, legitimacy, and social disclosure. J. Account. Public Policy 1991, 10, 297–308. [Google Scholar] [CrossRef]

- Freeman, R.E. Divergent stakeholder theory. Acad. Manag. Rev. 1999, 24, 233–236. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strateg. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Diez-Cañamero, B.; Bishara, T.; Otegi-Olaso, J.R.; Minguez, R.; Fernández, J.M. Measurement of Corporate Social Responsibility: A Review of Corporate Sustainability Indexes, Rankings, and Ratings. Sustainability 2020, 12, 2153. [Google Scholar] [CrossRef]

- Ma, C.; Chishti, M.F.; Durrani, M.K.; Bashir, R.; Safdar, S.; Hussain, R.T. The Corporate Social Responsibility and Its Impact on Financial Performance: A Case of Developing Countries. Sustainability 2023, 15, 3724. [Google Scholar] [CrossRef]

- Buallay, A.; Al-Ajmi, J. The Role of Audit Committee Attributes in Corporate Sustainability Reporting: Evidence from Banks in the Gulf Cooperation Council. J. Appl. Account. Res. 2020, 21, 249–264. [Google Scholar] [CrossRef]

- Asa’d, I.A.A.; Nour, A.; Atout, S. The Impact of Financial Performance on Firm’s Value during Covid-19 Pandemic for Companies Listed in the Palestine Exchange (2019–2020). In EAMMIS 2022: From the Internet of Things to the Internet of Ideas: The Role of Artificial Intelligence; Musleh Al-Sartawi, A.M.A., Razzaque, A., Kamal, M.M., Eds.; Lecture Notes in Networks and Systems; Springer: Cham, Switzerland, 2023; Volume 557. [Google Scholar] [CrossRef]

- Fatemi, A.; Fooladi, I.; Tehranian, H. Valuation Effects of Corporate Social Responsibility. J. Bank. Financ. 2015, 59, 182–192. [Google Scholar] [CrossRef]

- Malik, M.S.; Ali, H.; Ishfaq, A. Corporate Social Responsibility and Organizational Performance: Empirical Evidence from Banking Sector. Pak. J. Commer. Soc. Sci. 2015, 9, 241–247. [Google Scholar]

- Lyon, T.; Lu, Y.; Shi, X.; Yin, Q. How Do Shareholders Respond to Sustainability Awards? Evidence from China. Ecol. Econ. 2013, 94, 1–8. [Google Scholar] [CrossRef]

- Horváthová, E. Does Environmental Performance Affect Financial Performance? A Meta-Analysis. Ecol. Econ. 2010, 70, 52–59. [Google Scholar] [CrossRef]

- Renneboog, L.; Ter Horst, J.; Zhang, C. The price of ethics and stakeholder governance: The performance of socially responsible mutual funds. J. Corp. Financ. 2008, 14, 302–322. [Google Scholar] [CrossRef]

- Yu, E.P.; Guo, C.Q.; Luu, B.V. Environmental, social and governance transparency, and firm value. Bus. Strategy Environ. 2018, 27, 987–1004. [Google Scholar] [CrossRef]

- Friske, W.; Hoelscher, S.A.; Nik, A. The impact of voluntary sustainability reporting on firm value: Insights from signaling theory. J. Acad. Mark. Sci. 2022, 50, 372–392. [Google Scholar] [CrossRef]

- Bose, S.; Shams, S.; Ali, M.J.; Mihret, D. COVID-19 impact, sustainability performance, and firm value: International evidence. Account. Financ. 2022, 62, 597–643. [Google Scholar] [CrossRef]

- Nour, A.; Bouqalieh, B.; Okour, S. The impact of institutional governance mechanisms on the dimensions of the efficiency of intellectual capital and the role of the size of the company in the Jordanian Shareholding industrial companies. An-Najah Univ. J. Res. B 2022, 36, 2181–2212. [Google Scholar]

- Mattera, M.; Alba Ruiz-Morales, C.; Gava, L.; Soto, F. Sustainable business models to create sustainable competitive advantages: Strategic approach to overcoming COVID-19 crisis and improve financial performance. Compet. Rev. 2022, 32, 455–474. [Google Scholar] [CrossRef]

- Oware, K.M.; Valacherry, A.K.; Mallikarjunappa, T. Do third-party assurance and mandatory reporting matter to philanthropic and financial performance nexus? Evidence from India. Soc. Responsib. J. 2022, 18, 897–917. [Google Scholar] [CrossRef]

- Buallay, A.; El Khoury, R.; Hamdan, A. Sustainability reporting in smart cities: A multidimensional performance measures. Cities 2021, 119, 103397. [Google Scholar] [CrossRef]

- Pham, D.C.; Do, T.N.A.; Doan, T.N.; Nguyen, T.X.H.; Pham, T.K.Y.; Tan, A.W.K. The impact of sustainability practices on financial performance: Empirical evidence from Sweden. Cogent Bus. Manag. 2021, 8, 1912526. [Google Scholar] [CrossRef]

- Buallay, A. Sustainability Reporting and Agriculture Industries’ Performance: Worldwide Evidence. J. Agribus. Dev. Emerg. Econ. 2021, 12, 769–790. [Google Scholar] [CrossRef]

- Buallay, A. Sustainability Reporting and Firm’s Performance: Comparative Study between Manufacturing and Banking Sectors. Int. J. Product. Perform. Manag. 2019, 69, 431–445. [Google Scholar] [CrossRef]

- Graves, S.B.; Waddock, S.A. Institutional owners and corporate social performance. Acad. Manag. J. 1994, 37, 1034–1046. [Google Scholar] [CrossRef]

- Turban, D.B.; Greening, D.W. Corporate social performance and organizational attractiveness to prospective employees. Acad. Manag. J. 1997, 40, 658–672. [Google Scholar]

- Mattingly, J.E.; Berman, S.L. Measurement of Corporate Social Action: Discovering Taxonomy in the Kinder Lydenburg Domini Ratings Data. Buss. Soc. 2006, 45, 20–46. [Google Scholar] [CrossRef]

- Godfrey, P.C.; Merrill, C.B.; Hansen, J.M. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strat. Manag. J. 2009, 30, 425–445. [Google Scholar] [CrossRef]

- Eccles, R.G.; Ioannis, I.; Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef]

- Kang, K.H.; Lee, S.; Huh, C. Impacts of positive and negative corporate social responsibility activities on company performance in the tourism industry. Int. J. Hosp. Manag. 2010, 29, 72–82. [Google Scholar] [CrossRef]

- Gentry, R.J.; Chen, W. The relationship between accounting and market measures of firm financial performance: How strong is it? J. Manag. Issues 2010, 17, 514–530. [Google Scholar]

- Inoue, Y.; Lee, S. Effects of different dimensions of corporate social responsibility on corporate financial performance in tourism-related industries. Tour. Manag. 2011, 32, 790–804. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Nour, A.-N.I. The Impact of Corporate Governance on Firm Performance during The COVID-19 Pandemic: Evidence from Malaysia. J. Asian Financ. Econ. Bus. 2021, 8, 943–952. [Google Scholar]

- Nour, A.; Alia, M.A.; Balout, M. The Impact of Corporate Social Responsibility Disclosure on the Financial Performance of Banks Listed on the PEX and the ASE. In ICGER 2021: Artificial Intelligence for Sustainable Finance and Sustainable Technology; Musleh Al-Sartawi, A.M.A., Ed.; Lecture Notes in Networks and Systems; Springer: Cham, Switzerland, 2022; Volume 423. [Google Scholar] [CrossRef]

- Callan, S.J.; Thomas, J.M. Corporate financial performance and corporate social performance: An update and reinvestigation. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 61–78. [Google Scholar] [CrossRef]

- Qoyum, A.; Sakti, M.R.P.; Thaker, H.M.T.; Alhashfi, R.U. Does the Islamic label indicate good environmental, social, governance (ESG) performance? Evidence from sharia-compliant firms in Indonesia and Malaysia. Borsa Istanb. Rev. 2022, 22, 306–320. [Google Scholar] [CrossRef]

- Bansal, M.; Samad, T.A.; Bashir, H.A. The sustainability reporting-firm performance nexus: Evidence from a threshold model. J. Glob. Responsib. 2021, 12, 491–512. [Google Scholar] [CrossRef]

- Velte, P. Does ESG Performance Have an Impact on Financial Performance? Evidence from Germany. J. Glob. Responsib. 2017, 8, 169–178. [Google Scholar] [CrossRef]

- Sharfman, M.P.; Fernando, C.S. Environmental risk management and the cost of capital. Strat. Manag. J. 2008, 29, 569–592. [Google Scholar] [CrossRef]

- Aouadi, A.; Marsat, S. Do ESG Controversies Matter for Firm Value? Evidence from International Data. J. Bus. Ethics 2018, 151, 1027–1047. [Google Scholar] [CrossRef]

- Haniffa, R.; Hudaib, M. Corporate governance structure and performance of Malaysian listed companies. J. Bus. Financ. Account. 2006, 33, 1034–1062. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).