The author would like to make the following corrections to the published paper [1]. The changes are as follows:

- (1)

- Replacing the word “60%” with the word “55%” in “Abstract”, the second last sentence:

The corrected sentences appears below:

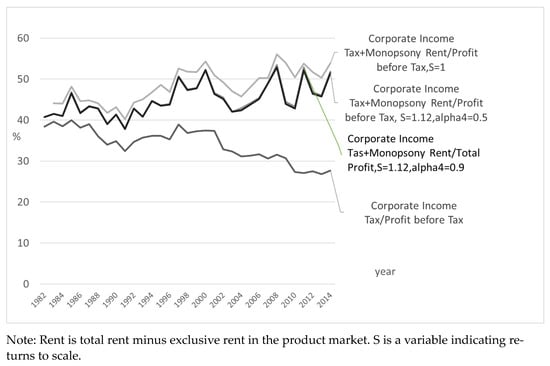

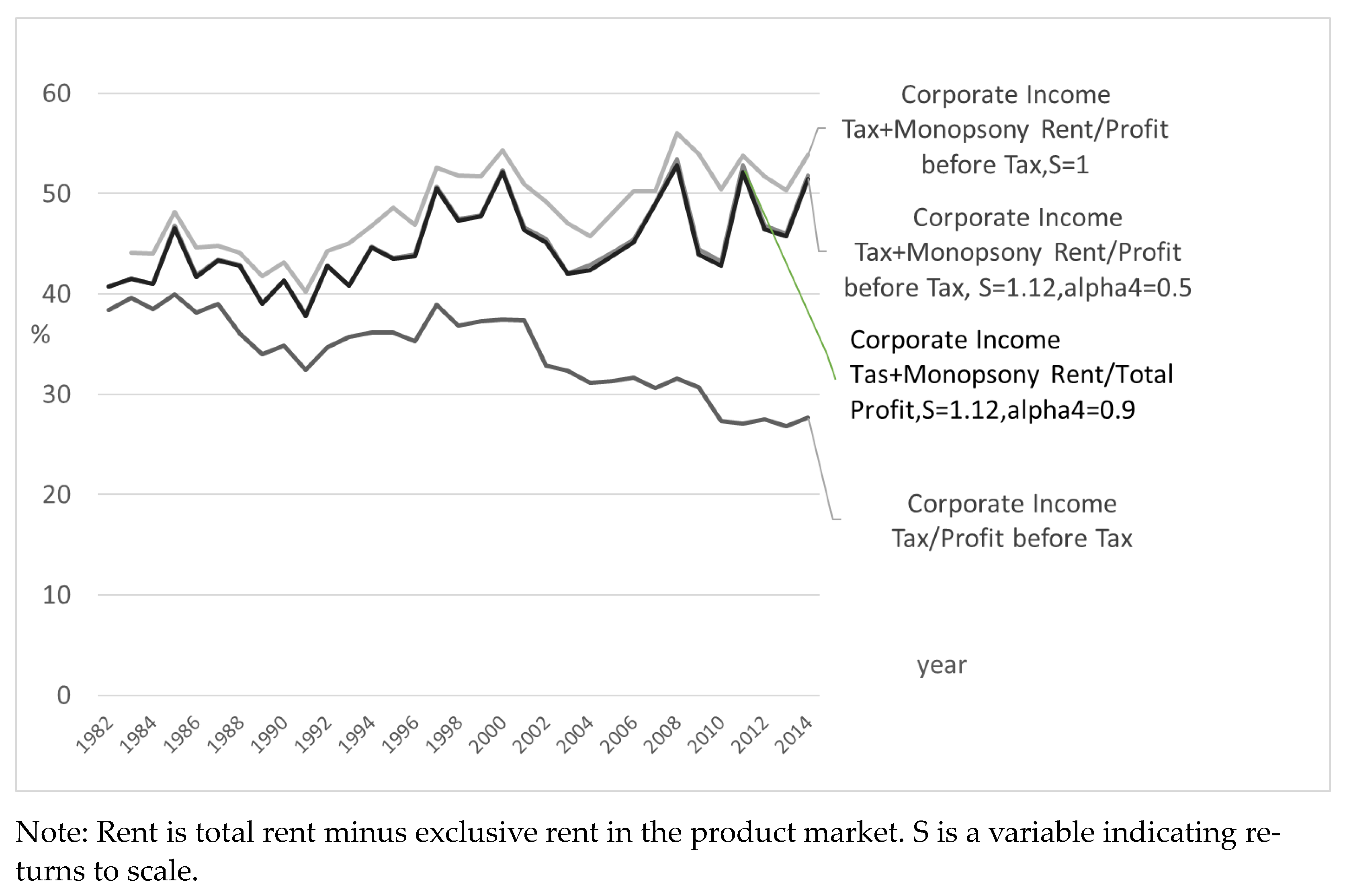

“The normative tax rates from 1982 to 2014 for these companies are stable at 40 to 55%, whereas corporate income tax has gradually decreased from 40% to less than 30%.”

- (2)

- Replacing the word “1.2” with the word “1.12” in “Section 2.3. Ingenuity to Apply Corporate Accounting Data to Production Functions for Calculation”, Paragraph 4 and should read:

“The calculation is performed by setting S to 1 (i.e., R = 1), and sensitivity analysis will be performed with S = 1.12, which can be regarded as the upper bound of induced returns to scale, as the return to scale in the U.S. in recent years was calculated to be 1.12 according to Boussemart et al. [45].”

- (3)

- Replacing the weblink in “Section 2.5. Data and Calculation”, Paragraph 1 and should read:

“https://data.mendeley.com/datasets/ds22hpy629/3, accessed on 4 February 2023.”

- (4)

- Replacing the third sentence in “Section 3.1. Differences between Corporate Tax Rates and Normative Corporate Tax Rates”, Paragraph 1 and should read:

“The results show that the banking, insurance, water transportation, gas, electric, and sanitary services industries, and stone, clay, glass, and concrete have almost zero rents, while the rest of the industries, not only manufacturing but also services, have rents ranging from around 10% to as high as 20% of pre-tax profits on average over the 33-year period.”

- (5)

- Replacing the last sentence in “Section 3.2. Time Series of Corporate Tax Rate and Normative Corporate Tax Rate”, Paragraph 1 and should read:

“Based on the above, we can see that the normative corporate tax rate for the past 30 years has been stable at approximately 45%, with a slight upward trend since the 1990s, when S = 1.12.”

- (6)

- Replacing the first and the second last sentences in “Section 4.1. Key Findings and Policy Recommendations”, Paragraph 3 and should read:

“The average corporate income tax rate for these companies gradually dropped from 38.4% in 1982 to 27.7% in 2014 according to the data.”

and

“Obviously, the normative corporate income tax rate has remained flat at approximately 40% to 55%, depending on the values of parameters.”

- (8)

- Replacing the word “1.2” with the word “1.12” in “Section 4.2. Limitations and Future Prospects”, Paragraph 1 and should read:

“For the case of S = 1.12, rents were calculated for = 0.5 and 0.9, and sensitivity analysis was performed.”

- (9)

- The author would like to change all the numbers of the table content, so we need to replace the original Table 1 with the following Table 1:

Table 1.

Corporate income tax including rent.

Table 1.

Corporate income tax including rent.

| S = 1 | S = 1.12 α4 = 0.9 | S = 1.12 α4 = 0.5 | ||

|---|---|---|---|---|

| Industry | W3/TI | (W3 + Rent)/TI | (W3 + Rent)/TI | (W3 + Rent)/TI |

| 2 Mining | 0.349 | 0.556 | 0.497 | 0.496 |

| 3 Construction | 0.348 | 0.490 | 0.453 | 0.450 |

| 4 Food, tobacco | 0.332 | 0.510 | 0.469 | 0.467 |

| 5 Textile, fabric, apparel | 0.293 | 0.488 | 0.430 | 0.428 |

| 6 Lumber, furniture, paper | 0.382 | 0.534 | 0.496 | 0.496 |

| 7 Printing, publishing | 0.089 | 0.229 | 0.324 | 0.216 |

| 8 Chemical | 0.267 | 0.500 | 0.459 | 0.455 |

| 9 Petroleum refining | 0.340 | 0.659 | 0.562 | 0.562 |

| 10 Rubber, miscellaneous plastics | 0.360 | 0.547 | 0.511 | 0.511 |

| 12 Stone, clay, glass, concrete | 0.311 | 0.349 | 0.341 | 0.341 |

| 13 Primary metal | 0.341 | 0.566 | 0.514 | 0.514 |

| 14 Fabricated metal products (except machinery, transportation equipment | 0.337 | 0.523 | 0.465 | 0.462 |

| 15 Industrial, commercial machinery, and computer equipment | 0.208 | 0.419 | 0.381 | 0.370 |

| 16 Electronic machinery except computers | 0.273 | 0.494 | 0.446 | 0.440 |

| 17 Transportation equipment | 0.325 | 0.461 | 0.428 | 0.424 |

| 18 Measuring, analyzing, controlling equipment | 0.286 | 0.492 | 0.463 | 0.458 |

| 19 Miscellaneous manufacturing industries | 0.282 | 0.508 | 0.463 | 0.460 |

| 20 Railroad, motor freight, postal service, airline, transportation | 0.356 | 0.488 | 0.448 | 0.448 |

| 21 Water transportation, gas, electric, sanitary services | 0.354 | 0.415 | 0.393 | 0.391 |

| 22 Communications | 0.358 | 0.552 | 0.479 | 0.478 |

| 23 Wholesale trade | 0.307 | 0.482 | 0.459 | 0.452 |

| 24 Retail trade | 0.390 | 0.633 | 0.585 | 0.583 |

| 25 Banking | 0.296 | 0.329 | 0.317 | 0.316 |

| 26 Insurance | 0.303 | 0.339 | 0.337 | 0.335 |

| 28 Real estate | 0.249 | 0.433 | 0.406 | 0.404 |

| 29 Health services | 0.384 | 0.651 | 0.588 | 0.589 |

| 30 Business services | 0.314 | 0.553 | 0.514 | 0.511 |

| 33 Public administration | 0.324 | 0.600 | 0.554 | 0.554 |

| Average | 0.313 | 0.493 | 0.456 | 0.450 |

| Note: W3 = corporate income tax, TI = profit before tax | ||||

| rent = rent excluding monopoly rent of product markets | ||||

- (10)

- The author would like to change the fold lines in the picture, so we need to replace the original Figure 3 with the following Figure 3:

Figure 3.

Time series of rent and corporate income tax.

Figure 3.

Time series of rent and corporate income tax.

The author and the Editorial Office would like to apologize for any inconvenience caused to the readers and state that the scientific conclusions are unaffected. The original article has been updated.

Reference

- Shimamoto, M. Normative Corporate Income Tax with Rent for SDGs’ Funding: Case of the U.S. Sustainability 2023, 15, 3176. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).