1. Introduction

Investments are important for every economy because they ensure development, innovation, and the satisfaction of needs at a higher level. Through investments in any sector (education, production, mining, health, social infrastructure, energy, circular economy, environment, etc.) investors contribute to the creation of a more inclusive and fair society, which strives for growth and development. Without investments, the economy would be deprived of the possibility of growth, innovation would be limited, and society would have limited opportunities for progress.

Investments in infrastructure, production, energy, new technologies, even human resources ensure GDP growth, new job creation opportunities and an increase in productivity in the invested industry [

1]. New inflows of capital strengthen the existing economic activities but also develop new opportunities and enhance the competitiveness of the economies globally. Through investments in new technologies and research and development, investors intend to create more profitable options in some industries and create new development options. In some cases, a firm’s investment behavior is affected by the policy of uncertainty which leads to an awareness of the need for the regulation of a certain area [

2]. When it comes to investments in renewable sources, the financial development of a certain economy has a positive impact on renewable energy production [

3] and vice versa [

4].

By investing in renewable energy sources, energy efficiency and environmental protection, investors contribute to the protection of natural resources and reduction in negative environmental impacts [

5]. Sustainable investments protect the environment but also open up new business opportunities in various sectors [

6] and set standards across industries. The literature is divided on whether a country with a clean environment attracts investments, or the lack of regulation and weak laws attract investment [

7]. Some studies have examined the impact of regulatory and macroeconomic determinants on renewable energy investments, primarily focusing developed countries, but Aziz and Jahan [

8] investigate whether the various levels of development or regulatory support have a significant influence on the renewable energy investment attraction.

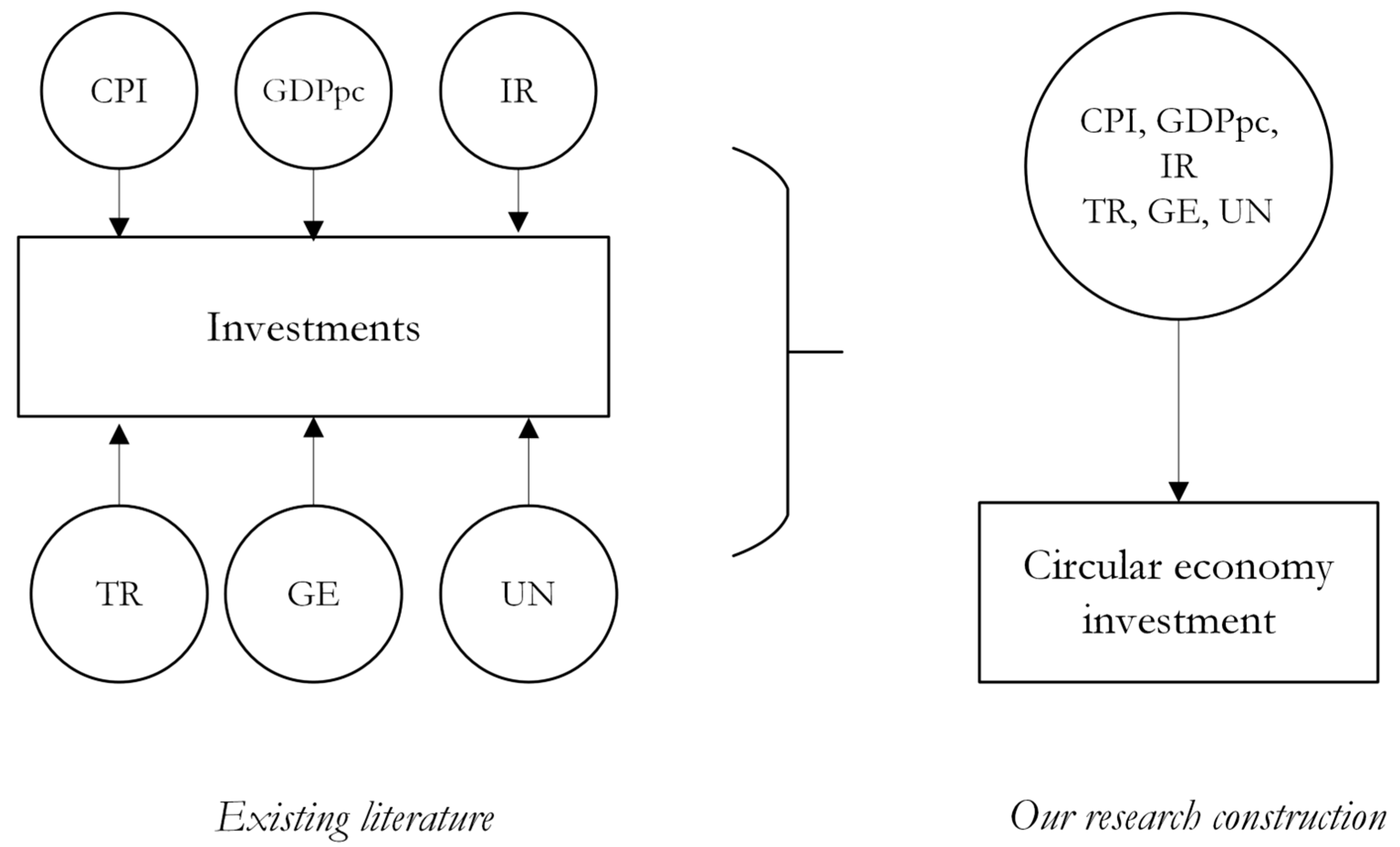

Understanding the determinants influencing investment decisions is crucial for developing strategies that promote economic growth and directing capital towards sustainable and innovative practices, such as the circular economy. In the literature, there is no consensus about the determinants of the investments, especially investments in the circular economy. There is a lack of studies considering which macroeconomic determinants are influencing investments in the circular economy. Previous studies considered mostly environmental determinants. This research aims to determine which of the considered determinants most influence investments in a circular economy. Therefore, this study expands the current theoretical opus of research related to investments in the circular economy. At the same time, the obtained results enable the identification of key determinants of investments in a circular economy and provide a new perspective on circular investments. Thus, it fills a specific gap related to the observation of the relationship between macroeconomic determinants and circular investments by identifying and explaining which factors and to what extent influence investments in this sector.

2. Literature Review

So far, the existing literature considers environmental factors that affect investments in a circular economy, and when it comes to general investments, it looks only at the impact of one specific variable on investments [

9]. This paper aims to cover the most used individual macroeconomic determinants that affect investments in general and gather and apply them to create a model that shows which macroeconomic determinants affect circular economy investments. In this sense, the contribution of this research is that it summarizes the individually used determinants of investments and observes their joint impact on investments in a circular economy. Studies related to investment determinants have shown that the level of investment depends on the level of development of the countries. It is to be expected that more developed countries invest more in circular economies than less developed ones. Therefore, specific macroeconomic determinants have a positive or negative impact on investments in some sectors. The following literature review shows an overview of the macroeconomic variables that have had a significant impact on certain types of investments.

Government spending represents one of the most essential issues for policymakers in both normal and exceptional circumstances [

10]. The impact of government spending on private investment has long been a key topic in fiscal policy discussions [

11] and the main determinant of attracting investments depending on the industry and the government support. Wang [

11] has explored the relationship between government expenditures and private investment in Canada from 1961 to 2000. He examined the effects of government spending on investment using a cointegration and error-correction framework for the analysis. The empirical findings indicated that government expenditure on education and health attracted private investment, whereas expenditure on capital and infrastructure have had a negative influence on private investments. In her study, Sinevičienė [

12] considered the relationship between government expenditure and private investment in Bulgaria, Estonia, Latvia, Lithuania, and Slovenia from 1996 to 2012. The finding has shown a weak relationship between the considered variables, and furthermore, the overall research results indicate that government expenditure crowds out private investment in some countries like Estonia, Latvia, Lithuania, and Slovenia. The “crowding out” effect on private investments was shown also by Bairam [

13] in the case of 19 of 25 OECD countries in the period from 1950 to 1988. Akinlo [

14] considered the effect of government expenditure on private investment in Nigeria 1980 to 2016. In this study, Akinlo [

14] also used error correction model analysis to explore the effects of the government expenditure, and other macroeconomic variables as control variables, on investments. The findings showed a long-term relationship among the variables. Interest rates and inflation have had a negative but significant impact on private investment in the long run. Government expenditure showed a positive but insignificant impact on private investment in the long term. In the short run, both interest rates and government expenditure had a positive significant effect on private investment, while GDP per capita and inflation negatively influenced private investment. The study concluded that government expenditure on infrastructure should increase to attract more investments.

To provide a greater level of expenditure in the mentioned sectors, it is necessary to collect enough revenue by taxation. Tax revenue mobilization demonstrates the governments’ capacity to collect adequate funds to finance government spending and public needs [

15]. Also, taxes should ensure consistent revenue collection without any adverse effects on economic development [

16]. Within that, investment in a circular economy can be supported by a portion of the collected revenue. Accordingly, tax revenue can affect investments in a circular economy through incentives or disincentives for businesses to apply sustainable practices. These incentives and disincentives can be guidelines for the behavior of businesses, consumers, and the public sector [

17]. Governments may opt to offer tax benefits or subsidies to companies that invest in environmentally friendly projects. Conversely, higher taxes on non-sustainable projects can discourage business from pursuing environmentally harmful activities. Specifically, Milios [

18] indicated that the tools that governments can employ to establish the necessary conditions for a circular economy can be divided into three categories: administrative (regulatory bans, standards, and targets), economic (taxes, tariffs, and subsidies) and informative (labels, campaigns, and certifications). It means that tax policy can play a significant role in shaping investment decisions towards a more sustainable and circular economy. Therefore, tax incentives could stimulate investment levels in a circular economy. In this way, the investment share in GDP will rise and enable favorable conditions for economic prosperity. Accordingly, the significant relationship between tax revenue and investment was confirmed in Southeast Asia and Visegrad group countries in the studies of Minh Ha et al. [

19] and Đurović Todorović et al. [

20].

As mentioned, private investment can contribute to economic growth by creating job opportunities, increasing productivity, and stimulating economic activity. Afonso and Aubyn [

21] determined the positive effect of private investment on economic growth in 17 OECD economies from 1960 to 2014. To provide positive implications of private investment, it is important to detect which determinants influence investment. Firstly, economic activity represents one of the most used determinants of private investment and it is often measured by gross domestic product. GDP is a measure of the economy size, [

12] and it serves as a significant indicator reflecting macroeconomic operations of the country [

22]. Similarly, it is one of the most key predictors of investment, especially foreign direct investment [

7]. A higher GDP value is usually associated with greater economic stability and progress, and it can create a conducive environment for private investment. It implies greater investor confidence in the long-term projects and positive implications on economic uncertainty. Therefore, gross domestic product can play a crucial role in shaping the investment climate in an economy. GDP per capita is an economic development indicator and its strong value can attract private investment by making a favorable economic ambiance. Accordingly, Acosta and Loza [

23] confirmed a positive and long-term relationship GDP with private investment in Argentina for the period 1970–2000, as well as Wang [

11] in Canada from 1961 to 2000. Similarly, Suyuan and Khurshid [

24] verified a positive relationship between GDP growth and investment in the economy of the Jiangsu Province of China. Romano and Scandurra [

25] verified the significant effect of GDP per capita on investments in renewable energy sources in the sample of 60 countries from 1980 to 2008, while Ahmad and Zhao [

1] found bidirectional positive causality between investment and growth on the sample of energy investment in China from 2001 to 2016. These studies suggested that these investment types can enhance economic growth. Similarly, Carvelli [

26] identified a positive long-term coefficient of GDP per capita on private investment in OECD countries for the period 1990–2019. On the other side, Akinlo and Oyeleke [

14] found a negative impact of GDP per capita on private investment in Nigeria, which was similar to empirical findings of the study by Ayeni [

27] and Dang et al. [

28] that confirmed that GDP negatively affects private investment in Gambia and Vietnam. Moreover, GDP does not have to be the decisive factor in stimulating private investment. For instance, Ghura and Goodwin [

29] pointed out that GDP growth stimulated private investment in Asia and Latin America compared to its insignificant effect in Sub-Saharan Africa. On the other hand, Aziz and Jahan [

8] argue that the effect of GDP is limited to a specific wealth range only.

Besides gross domestic product, inflation is a typical macroeconomic driver of private investment [

30] depending on its dynamics [

31]. Higher inflation can make uncertainty in the economy and be considered as a country’s inability to manage macroeconomic policy [

32], creating it difficult for investors to plan for current and future projects. The negative impact of inflation on private investment is confirmed in the studies of Karagoz [

33] and Akinlo and Oyeleke [

14]. Also, Ayeni [

27] indicated that inflation significantly and negatively affects investment only in the short term, which is not the case with a long-term period. These findings are related to Dang et al. [

28] whose study also confirmed that inflation is not a significant predictor for private investment in the long run. However, various effects of inflation were determined in study of Ghura and Goodwin [

29] that identified its negative influence in Latin America and its positive effect on private investment in Sub-Saharan Africa. Likewise, Omitogun [

34] found different inflation reactions on private investment from the aspect of impact on capital expenditure and recurrent expenditure in Nigeria.

The issue of unemployment’s influence on private investment can be explained from the aspect of economic uncertainty and the business cycle. Specifically, high unemployment levels can create instability in the economy and further discourage investors and their investment plans and projects. When it comes to the empirical relationship between investment and unemployment, Driver and Muñoz-Bugarin [

35] showed that capital investment has a significant and negative impact on labor share in the U.K. market over the period 1985–2017. Likewise, Hoon et al. [

36] found a negative coefficient of investment, which implies that an increase in investment share in GDP will reduce the unemployment rate in the sample of OECD countries over the period 1960–2017. Similarly, Atilaw Woldetensaye et al. [

37] highlighted that foreign direct investment negatively influenced the unemployment rate in selected countries from East Africa in the period 1996–2021. Conversely, Strat et al. [

38] found no causality between foreign direct investment and unemployment in EU member states (Cyprus, Poland, Slovenia, Croatia, Latvia, and Lithuania) in the period 1991–2012. Furthermore, this study verified unidirectional causality between these variables in Hungary, Malta, Bulgaria, Romania, Czech Republic, Estonia, and Slovakia in the analyzed period.

The linkage between interest rates and investments has been shown to be important when it comes to the financial structure of the investment. On one side, when interest rates are low, the cost of borrowing decreases. This makes loans more accessible and preferable sources of financing. In the situation of more available sources, investors are encouraged to invest in investment opportunities. Conversely, high interest rates raise the costs of borrowing. On the other hand, investment decisions are influenced by the expected returns compared to the cost of financing. In the case of low interest rates, the hurdle rate is also lower, which contributes to the fact that investments seem more profitable and give higher margins to the investors. The main driver of waste management according to Ilic and Nikolic [

39] is the availability of funds and budget. Bearing in mind this fact, countries that have a more developed financial market and more efficient [

40] and profitable [

41] financial institutions are expected to be leading in circular economy investments. The interest rate is also dependent on the inflation rate. As an act of active monetary policy, the authorities increase the real interest rate as a response to inflation [

42]. A passive monetary policy, where a one percentage point increase in inflation is followed by a less than one percentage point increase in the nominal interest rate, destabilizes the economy [

43]. Wuhan [

24] has examined the impact of interest rates on investment in Jiangsu Province, China, using error correction models in the period of 2003 to 2012. The results of this study indicated a long-term relationship among the considered variables. It is interesting to mention that this relationship is negative in the long run but positive in the short run. Studies [

44,

45,

46] have shown that the impact of the interest rate on investments depends on the variance in interest rates.

4. Empirical Results and Discussion

The following chapter provided in this paper offers an in-depth exposition of the analysis results and the interpretation of the possible outcomes, particularly focusing on the effective implementation of the model in both the short- and long-term periods of time.

The initial table in this section (

Table 2) presents the descriptive statistics and unit root testing pertaining to all variables under consideration. The first part of the table details fundamental characteristics of the variables within the generated dataset. The table also presents the results of the augmented Dickey–Fuller test (ADF test), which involves a data series to determine the presence of a unit root at the levels and the first difference. All mentioned variables are non-stationary at the levels, except for the data for the real GDP variable, which is excluded from the further modeling process. All variables have a unit root at the levels, but according to the results in the table, they are stationary at the first difference, which also means that they do not have a unit root at the first difference. As all series are I(1) series, meaning all of them are cointegrated of the same order, and further analysis can run the Johanson Fisher cointegration test.

The results in

Table 3 indicate that the null hypothesis is accepted at cointegration rank 2 in the case of both applied tests. The variables are integrated and cointegrated, where the cointegration rank shows the number of cointegration equations that can be formed between the specified variables. Since the presence of cointegration is identified, it indicates that the variables exhibit a long-run movement together, with any deviations from this balanced relationship likely to revert back to the mean.

The results of the simple correlation coefficients are presented in

Table 4 as an initial indicator of the relationships among variables, all with the aim of forming a suitable model. Observing the correlation matrix in

Table 4, it is established as an initial assumption that there is no multicollinearity issue among the independent variables due to the absence of a strong correlation between them, except on a few occasions. Additionally, the very low correlation coefficient between investments and the real GDP once again points to the necessity of omitting this macroeconomic indicator from further modeling processes.

The results presented in

Table 5 were estimated through the utilization of panel data methodology with the application of fixed effects. The application of this methodology is justified by the diagnostic results of the models listed in the following

Table 6. The models initially take the same time series data for both the long and short term. The coefficients show the significant and positive impact of government expenditure on investment in a circular economy. The stronger impact is noticed in the short-run model, similar to the findings in Akinlo’s study [

14]. The unemployment rate displays signs of a statistically significant negative association with investments in both short and long-run models. Unlike some findings [

14,

33], the consumer price index (CPI) has a high statistically significant positive effect on investment in both short and long-run models. The long-run effect of tax revenue is positive and highly statistically significant. Similar results were obtained for short-term effects, but the more significant impact of tax revenues in the long-term must be emphasized. The coefficient results associated with interest rate show that the mentioned indicator is negatively and significantly related to investments in a circular economy in both the short and long term. The findings in this case could play a crucial role in the economic analysis of the outcomes, as the interest rate often serves as a key mechanism connecting government activity to private industry [

26]. The error correction term is highly statistically significant in the presented model specification with the speed of adjustment to long-run equilibrium of −0.43592. This outcome serves as evidence of the existence of a cointegrating relationship between investments in a circular economy and the specified independent variables. The results show that only

H1 and

H4 can be rejected, and

H2,

H3,

H5 and

H6 can be accepted. Regarding

H4, it is important to mention that a significant effect is present but in the other direction. A positive effect of CPI on circular economy investment favors foreign investors who invest in another currencies.

In order to determine the quality of the estimating models, it is essential to conduct model diagnostics. The assessment of regression diagnostics involves examining the foundational statistical assumptions of the model, analyzing the structure of the model through the consideration of alternative formulations with varying numbers or types of explanatory variables, as well as investigating subgroups of data for outliers or observations with a significant impact on the model’s predictive capabilities. The results with a given denominator are depicted in

Table 6.

The long-term model demonstrates consistency with the data as it exhibits a high degree of model explainability with an over 78% value of R-squared. The inherent value of the degree of explanation is significant when considering a short-term model. This fact can be partially explained by the shorter memory of the model and the use of the first difference data in the model. In order to alleviate any doubts regarding the use of appropriate variables in explaining investments in the circular economy, the F test of the joint impact of independent variables on the dependent variable was applied. The results of the F-statistic suggest that the coefficients of the parameters jointly hold significance at a level of 1%.

The results of the multicollinearity test of the regressors calculated using the VIF test and presented in

Table 6 do not indicate any issues of multicollinearity among the recorded independent variables in the case of both models. The results of the χ

2 test conducted in the Hausman test indicate that the null hypothesis is rejected, confirming that the fixed effect model is suitable for both long and short-run models. The Breusch–Pagan LM test also yields comparable outcomes, refuting the null hypothesis for both models. In the next step of enhancing the existing model form, the Breusch–Pagan–Godfrey test was conducted to detect the presence of heteroscedasticity of the residuals. The confirmation of homoscedasticity of residuals is evident in the results of both models presented in

Table 6. To prevent asymmetry in the residuals, verification of the normality of the residual data series was conducted using the Jarque–Bera test. The results of the Jarque–Bera test for both models indicate that the null hypothesis regarding the presence of a normal distribution of residuals estimated from the long-term and short-term models is satisfied.

In context of a circular economy, Chen and Pao [

52] applied a vector error correction model to analyze the relationship between a circular economy and economic growth in the 25 EU countries. Their focus was not only macroeconomic factors. Therefore, their model results are not directly comparable with this research. ECM has been widely used for modeling investments in various fields of economics [

26,

53,

54], but the gap in the literature exists in the context of investments in a circular economy.

5. Conclusions

Investment in the circular economy has significant policy implications that can shape the transition towards a more sustainable and environmentally friendly economic model. It means that this type of investment could help in driving sustainable development and reducing environmental harmful effects. Consequently, by applying supportive policies and regulatory frameworks, governments can make an enabling environment for private sectors.

This paper investigated the macroeconomic determinants of investment in a circular economy in the European Union for the period 2004–2022. Analyzing estimated effects by determinants, the results indicate that government expenditure positively affects investment in a circular economy in the short and long run. Government should focus on productive expenditure that can support research and development in the circular economy, leading to new development processes and technologies, as well as business models that promote sustainable practices and resource efficiency. Having in mind identified a negative effect of unemployment on investment in a circular economy in the short and long run, this paper’s findings confirm that a higher unemployment level can hinder this investment type affected by a lower consumer demand for sustainable products and services. Also, a greater unemployment rate leads to economic uncertainty and instability, which reduces disposable income for investing and spending. The obtained findings confirmed the positive effect of the CPI on investment in a circular economy in the short and long run. If the CPI shows an increase in prices for sustainable products and services, investors might be more likely to invest in companies operating in a circular economy. Additionally, a rising CPI can reflect healthy economies with strong consumer purchasing power, which can make a favorable ambience for investment in sustainable projects and technologies.

Based on empirical results, tax revenue significantly affects the investment in a circular economy in the short and long run. Namely, more tax revenue provides governments financial sources needed to support and incentivize investment in sustainable activities and initiatives. Also, this can help to drive innovation in various sectors and create new opportunities for higher investments. Finally, interest rate negatively influences the investment in a circular economy in the short and long run, which is expected since higher interest rates lead to higher costs of capital. Consequently, borrowing money becomes more expensive for businesses looking to invest in a circular economy and reduces the potential return on investments. It can make it less attractive for companies to finance and support sustainable activities and projects. These findings revealed that EU countries must strive to ensure a higher level of government expenditure and tax revenue mobilization so that a certain portion of the funds can be directed towards circular investments. Additionally, a stable CPI enables a predictable economic environment for investments in this type of sector. A greater level of investment in circular economy allows a reduction in unemployment by employing new people and creating new jobs in this sector. Finally, a policy of lower interest rates opens space for greater investments in a circular economy, which will be accompanied by reduced or acceptable borrowing costs.

This empirical analysis provides valuable insights and recommendations for policymakers in the European Union, aiding in the identification of main determinants influencing investment in the circular economy. Furthermore, the study extends current theoretical opus on the investment determinants, with a special emphasis on investment in a circular economy. Also, it enables comprehensive overview of main macroeconomic determinants and their implications for observed investment type, as well as better understanding potential drivers of investment in a circular economy. This can be crucial for policymakers in the European Union when considering the potential implications of macroeconomic frameworks at the investment level in a circular economy. When it comes to policy recommendations, policymakers in the European Union should focus on further development of regulatory frameworks related to recycling, sustainable production methods, and the use of renewable resources. Also, market creation with developed financial support and defined international cooperation could enable a favorable environment for investment in a circular economy. Based on the facts mentioned above, it can be concluded that research enables both theoretical and practical implications in the field of investments in a circular economy. Specifically, the study delves into the identification of the main macroeconomic determinants of investments in a circular economy, enriching our comprehension of the factors influencing investment choices. This is not only advancing theoretical knowledge but also holds practical significance for policymakers and investors. This integrated approach fosters a more nuanced understanding of the dynamics within a circular economy, propelling the field forward and guiding strategies for sustainable economic growth and development.

As with any study, there are certain limitations here as well. These can be identified through the absence of the analysis of non-economic variables such as country risk, geopolitical changes, and crisis situations that were present during the observed period. Likewise, one limitation can be considered based on the fact that this empirical study includes only the European Union area and not the United States and Asian countries, the markets of which are favorable for investing in innovative technologies and projects. However, similar monetary policies and integrated economic frameworks in the European Union may have a direct influence on the investment decisions in a circular economy. Future research will include the United States and Asian countries to show a comparative overview of these regions. In this way, similarities and differences regarding the macroeconomic determinants of investments in a circular economy, as well as their implications, will be identified.

{kind=link}