1. Introduction

The development of human society cannot be separated from energy. Behind the high level of growth are high energy consumption and high emissions [

1]. The large-scale production of machines based on traditional fossil energy promotes economic development and builds modern forms of transportation, energy use, and industrial production. For a long time, high-pollution industries have been able to bring higher economic profits with lower production costs because they have not been responsible for the negative externalities of their production. Therefore, social capital has continued to flood into high-pollution industries, causing serious environmental damage. Against the backdrop of a traditional energy structure that cannot be transformed in the short term and a search for new and cleaner sources of energy that is fraught with challenges, balancing stable economic development and carbon emissions is a challenge that countries urgently need to address.

In order to curb the blind expansion of high-pollution and high-energy-consumption enterprises, the State Environmental Protection Administration of China issued the Opinions on the Implementation of Environmental Protection Policies and Regulations for the Prevention of Credit Risks in 2007, which pointed out that it is necessary to recognize the significance of green credit in the construction of a resource-saving and environmentally friendly society and to establish and improve the black and white list of enterprises’ environmental protection policies as well as the system for evaluating their environmental behavior. In 2016, China issued the Guiding Opinions on Building a Green Financial System, which stated that they will accelerate the construction of a green financial system, promote technological advances in environmental protection and new energy, guide and incentivize the inflow of social capital into green industry, improve the mechanism for restraining loans to the “two highs and one surplus” industry, establish a database for sharing information on environmental violations by enterprises, and provide information references to financial institutions for lending purposes.

Green finance contributes to the harmonization of economic, social, and environmental benefits [

2]. According to Li et al. [

3], green finance refers to the financial sector’s consideration of the potential environmental impacts of investment and financing projects in its business activities so as to obtain the greatest possible economic and social benefits at a relatively small environmental cost and to promote the sustainable development of the economy and society. He et al. [

4] believe that green finance is the use of financial institutions or financial markets as carriers to optimize the allocation of financial resources to green and low-carbon areas and that it is the application of the concept of sustainability in finance. Lee et al. [

5] believe that green finance is the financial support and financial services dedicated to green projects such as environmental improvement, climate change, energy transition, and resource conservation. It can be seen that there is no uniform definition of green finance, but most of them are centered on capital flow and investment and financing activities in the environmental field.

Green finance refers to investment and financing activities used to achieve cleaner production and to help highly polluting industries make a green transition, with the dual attributes of environmentalism and finance. First, environmental regulation is the embodiment of green attributes. On the one hand, green finance requires enterprises to disclose the environmental information of their projects and refuses to provide loan services to enterprises that generate negative externalities and are not responsible for them. To a certain extent, this increases the difficulty of obtaining funds for polluting projects and regulates the choice of economic activities, forcing enterprises to carry out cleaner economic activities. On the other hand, green finance requires financing firms to bear the negative externalities associated with their economic activities, which directly increases the costs of economic activities. While the internalization of corporate externalities increases the cost of project implementation, the benefits generated by green finance’s low-interest-rate loans are much higher than the costs associated with internalization, so companies have an incentive to undergo a green transformation in order to access green finance funds [

6]. Second, guiding the flow of funds is the embodiment of financial attributes. On the one hand, because green finance has the advantages of low interest rates and long lending times, while traditional high-pollution enterprises have large financing needs for green transformations and upgrades as well as long transformation times, green finance is very suitable for guiding high-pollution enterprises to green transformations. On the other hand, China’s green financial investment gap is large. According to an estimation by the Development Research Center of the State Council, the total investment in green development in 2015–2020 accounted for more than 14% of the total fiscal revenue [

7]. The government’s green investment alone cannot meet the capital demand of China’s green financial market [

8]. Therefore, it is necessary for green finance to play the leading role in government investment and private investment and to guide social capital to gradually withdraw from polluting industries and carry out clean projects to realize green and low-carbon development.

3. Theoretical Analysis and Research Hypothesis

Green finance is an emerging financial instrument used to reduce carbon emissions, helping to realize sustainable socio-economic development. At the macro level, green finance vigorously supports clean production and environmentally friendly industries; facilitates lending rates, loan tenure, financing constraints, etc.; restrains the supply of funds to highly polluting enterprises; inhibits excessive investment behavior; and forces enterprises to reduce highly polluting investments. In addition, green finance can strengthen the market access and exit mechanism, realize the dynamic retirement of highly polluting enterprises, and force highly polluting industries to decarbonize [

23]. At the micro level, green finance effectively solves the financing difficulties related to the green technology innovation of enterprises and promotes enterprises to choose clean technology, use clean energy, and choose clean investment portfolios to alleviate environmental problems [

24]. It helps to form corporate social responsibility and guide the internalization of corporate environmental externalities [

25]. Financial institutions also establish a credit accountability mechanism, formulate a one-vote veto rule for environmental protection, and realize the sustainable development of green finance through the dynamic clearance mechanism of enterprises [

26]. Therefore, this paper puts forward the following hypothesis:

Hypothesis 1. Green finance can significantly inhibit carbon emissions.

Green finance provides an internal driving force for green innovation. Its financial support promotes the green R&D and innovation of enterprises and forms the evolution route from biased technological progress to environmental technological progress and then to the stage of technological progress that generates technological spillovers [

27]. Green finance helps companies improve their R&D capabilities [

28] and gain a comparative advantage in reallocating green financial resources by complying with green governance [

29]. The green financial market has a large number of financial resources and local policy support, which can encourage enterprises to actively engage in green innovation [

30]. Green finance raises the cost of financing for highly polluting industries, making it difficult to raise funds and inhibiting new investment, which is conducive to directing funds to green and clean areas and optimizing the allocation of resources [

13].

Green finance, as an emerging financial instrument, requires a large amount of capital investment to improve the construction of the market. However, financial investment alone cannot meet the needs of the green financial market, and it is necessary to induce social capital to invest in the field of green production to alleviate financial pressure and broaden the channels of capital flow in the green financial market [

8]. Green financial policy reflects the government’s consideration of ecological protection and the industrial development direction arrangement, providing a clear direction for social capital flow, which can to a certain extent induce social capital to flow to the field of clean production and environmentally friendly industries [

15]. By inducing the flow of social capital, green finance can optimize the industrial structure, reduce the financial support for high-pollution industries, and lower the intensity of carbon emissions [

31].

Green finance supports projects with environmental benefits. It requires financing entities to disclose their specific environmental information and social responsibilities [

32], assess whether environmental risks may arise, and confirm that a project is environmentally friendly and that the financing entity is responsible for the environment before lending [

33], effectively inhibiting the development of high-pollution projects. The first goal of enterprises is profit. On the one hand, the disclosure of social responsibility and environmental information may affect the green reputations of enterprises [

34]. On the other hand, the internalization of externalities of production increases the operating costs of enterprises. The interest rate, approval time, and loan period of traditional finance do not distinguish the financing subjects, while green finance has the advantages of low-interest-rate loans and high approval efficiency. The benefits brought to enterprises are far greater than the costs brought by social responsibility and negative environmental externalities. Therefore, ‘two high and one surplus’ enterprises do not have enough motivation to disclose their social responsibilities on time and with adequate quality due to the risk of not obtaining green financial support. Therefore, this paper puts forward the following hypothesis:

Hypothesis 2. Green finance can indirectly reduce carbon emissions by improving green technology innovation, inducing social investment, and strengthening social responsibility information disclosure.

To a certain extent, the environmental attention of local governments represents the attitude of local governments towards the environment. Under the influence of the GDP promotion championship model, the government’s attention has been biased towards economic development for a long time. Region-oriented thinking has been solidified, and a development mode emphasizing development and neglecting the environment has caused a series of environmental problems [

35]. A government work report describes the development situation in a region in the previous stage and the development direction in the next stage and is the baton for regional resource allocation and policy making [

36]. Reflecting the ecological environment, the government’s attention to the environment influences the formulation and implementation of environmental regulatory policies and energy policies and affects whether green finance can effectively guide capital into clean production and environmentally friendly industries. The government’s attention to the environment can effectively send signals to enterprises about their priorities and resource allocation and can encourage them to implement more carbon emission reduction actions [

37].

The traditional financial industry is the foundation for the development of green finance, and green finance is traditional finance with environmental significance [

4]. Taking green credit as an example, the approval body of green financial resources is the same as that of traditional financial loans, and the relevant approval system and process need not be duplicated, so the development level of the regional financial industry can, to a certain extent, promote the development of green finance. In addition, regions with a higher level of development in the financial industry have very effective financial transmission channels and feedback mechanisms. Financial institutions are able to effectively capture the majority of financing needs [

38] and are more capable of completing assessments of the objective financing conditions of green finance, as well as obtaining better services and resources, which contribute to the development of green finance. Therefore, this paper puts forward the following hypothesis:

Hypothesis 3. The environmental attention of the local government and the scale of the regional financial industry have heterogeneous effects on the emission reduction benefits of green finance, and high levels of financial industry scale and local government environmental attention help to strengthen the carbon emission reduction effect of green finance.

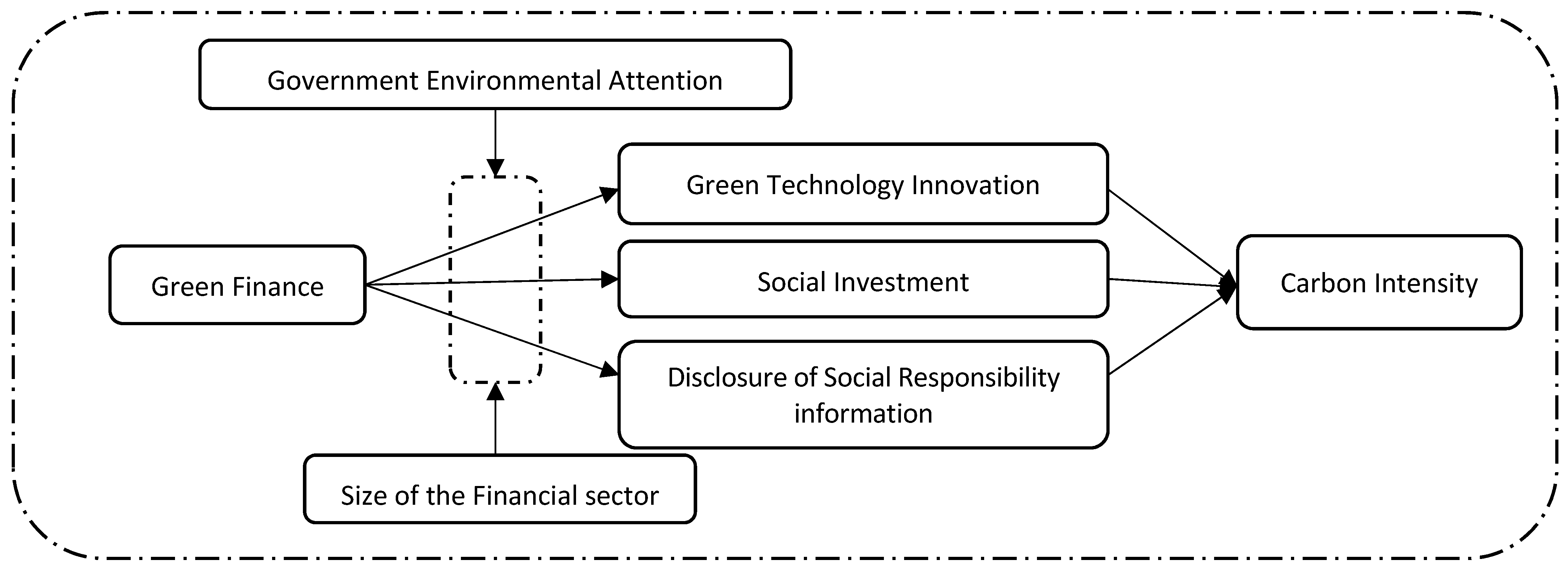

In summary, it is relatively rare to study the carbon emission reduction mechanism of green finance from the perspective of inducing social investment and enhancing corporate social responsibility information disclosure. In this paper, green finance is used to improve green technological innovation, induce social capital investment, and promote corporate social responsibility information disclosure as an influence mechanism to study how green finance can reduce carbon emissions. This paper also considers the influence of government environmental attention and regional financial industry development on the emission reduction benefits of green finance.

Figure 1 reports the theoretical mechanism by which green finance affects carbon emission intensity. The remaining sections of this paper are arranged as follows: model construction is carried out in

Section 4 to explain the data sources, the emission reduction mechanism and influence pathway of green finance are empirically tested in

Section 5, a robustness test is carried out in

Section 6, a heterogeneity analysis is carried out in

Section 7, and conclusions and recommendations are presented in

Section 8.

4. Model and Data

4.1. Model Building

Referring to the benchmark model construction in the related literature [

20,

39], this paper constructs the following two-way fixed-effects model:

where i indicates the province and city; t indicates the year; CE is the carbon emission intensity; GF is green finance; Controls are the relevant control variables;

and

represent province fixed effects and time fixed effects, respectively; and

is a random perturbation term.

In order to test the mechanism of green finance affecting carbon emission intensity, based on the related literature [

40], the following mediation model is constructed:

represents mechanism variables, including green technology innovation (GT), social investment (SI), social responsibility disclosure (SR), and others, as above.

In addition, in order to test the moderating effect of the mediation model, based on the related literature [

41], a mediation effect model with moderation is constructed:

where Z is a moderating variable that includes the size of the financial sector and government environmental attention.

4.2. Variable Descriptions

Explained variables: carbon emission intensity refers to the ratio of CO

2 emissions to output value compared with the total amount of CO

2 emissions, taking into account the scale of the economy and representing the quality and efficiency of economic development to a certain extent [

42]. Therefore, the explanatory variable in this paper is carbon emission intensity (CE), which is expressed as the ratio of CO

2 emissions to GDP in each province and city in the current year.

Explanatory variables: the explanatory variable in this paper is the level of green financial development (GF). Based on the relevant literature [

15,

43] and the

Guiding Opinions on Building a Green Financial System issued by China, this paper selects four sub-dimensions of green finance to be synthesized using the entropy method, which are green credit, green insurance, green support, and green investment. Green credit is expressed as the ratio of interest expenditure to total industrial interest expenditure of the six major energy-consuming industries (the six major energy-intensive industries include the processing of petroleum, coal, and other fuels; manufacturing chemical raw materials and chemical products; the non-metallic mineral product industry; the ferrous metal smelting and rolling processing industry; the non-ferrous metal smelting and rolling processing industry; and the electricity, heat, gas, and water production and supply industry). The greater the green credit, the more funds the high-energy-consumption industries obtain and the lower the level of green financial development, so it is a negative indicator. Green insurance is expressed as the ratio of agricultural insurance income to the total agricultural output value. As an important part of green insurance, agricultural insurance helps to prevent major natural disasters, so the higher the proportion, the better the development of green finance. Green support is measured as the proportion of environmental protection expenditures compared to general budget expenditures. Areas with a high proportion have poor environmental conditions and weak development of green finance. Green investment is expressed as the proportion of completed investments in industrial pollution control compared to GDP. Industrial pollution control is the short board of environmental governance, so the higher the investment in governance, the better the environmental control brought by green finance.

Mechanism variables: After the above analysis, green technology innovation, social investment, and social responsibility information disclosure are selected as mechanism variables. The green technology patent applications in a year are representative of green technology innovation and use, including green invention patents and green utility patents. Social investment is characterized by the proportion of the total assets of non-state-owned industrial enterprises compared to the total assets of industrial enterprises. Social responsibility information disclosure is characterized by the number of enterprises announcing social responsibility system construction and improvement measures in the annual reports of listed companies compared to the total number of enterprises.

Moderating variables: The moderating variables in this paper are government environmental attention (EA) and the financial industry development scale (FS). EA extracts the total frequency of keywords from provincial and municipal government work report documents, including 23 environmental terms (the 23 environmental protection words are emission reduction, cleaning, greening, green, recycling, environment, energy consumption, low carbon, emission, environmental protection, intensive, energy saving, sustainable, consumption, energy consumption, pollution, saving, consumption reduction, atmosphere, nature, restoration, sewage, and energy) such as environment, energy saving, emission reduction, sustainability, etc. The FS is expressed as the added value of the financial industry in the current year, and the larger the FS, the larger the scale of the financial industry in a region.

Control variables: the control variables in this paper refer to the related literature [

14,

44]. They are the urbanization rate (Urban), the proportion of secondary industry in the GDP (SE), the total amount of imported and exported goods (Trade), per capita GDP (PG), and human capital (HC). The urbanization rate is expressed as the proportion of the urban population to the total population, the total amount of imported and exported goods is expressed as the logarithm of the total trade in goods in the year, the GDP per capita represents the development of the local area and is expressed as its logarithmic value, and human capital is expressed as the number of students per 10,000 secondary school students.

4.3. Data Sources

The data related to CO

2 emissions used in this paper are from the China Carbon Accounting Database (CEADS), the data related to government environmental attention are from the China Research Data Service Platform (CNRDS), and the data related to social responsibility disclosure are from the Cathay Pacific Database (CSMAR). All other data are from the China Regional Economic Database (CRED), China Industrial Economic Database (CIED), China Macroeconomic Database (CMED), China Environmental Database (CED), China Financial Database (CFD), and Cathay Pacific Database (CSMAR). Since some data are missing and the relevant statistical yearbooks have not been updated to make up for them, this paper uses the 2003–2021 inter-provincial unbalanced panel for a regression. The descriptive statistics of the main variables are shown in

Table 1.

5. Benchmark Regression and Mechanism Testing

Column (1) of

Table 2 reports the regression results of the baseline regression, from which it can be seen that green finance can significantly reduce carbon emission intensity [

45]. Urbanization, the share of secondary industry, and the total amount of imported and exported goods are positive but not significant, which is consistent with the empirical evidence that large amounts of resources flow to cities in the process of urbanization and that the intensification of the economic activities in cities, which are mainly based on rough development, causes serious environmental problems and results in increases in carbon emissions. Secondary industry, which uses fossil fuels such as coal and oil as its main energy sources, produces a large amount of carbon dioxide in its economic activities, so regions with a higher proportion of secondary industry also have higher carbon emissions. The larger the total amount of import and export of goods, the more frequent a region’s foreign economic activities. Production and transportation processes produce large amounts of carbon dioxide, leading to higher carbon emissions. Regions with high GDP per capita have a better level of economic development, relatively rapid urbanization, and local governments that are beginning to pay attention to environmental issues. The establishment of environmental regulations has led to the relocation of a large number of polluting enterprises, and the regional industrial structure has been upgraded in the direction of advancement so that carbon emissions can be reduced. Regions with more human capital tend to choose low-carbon products and low-carbon traveling [

46].

In order to study how green finance reduces carbon emission intensity, this paper elaborates on the following three mechanisms: green technology innovation, social investment, and environmental information disclosure.

Table 2 reports the regression results of these three mechanisms. According to column (2) of

Table 2, green finance promotes green technological innovation at the 1% significance level; green patent applications reflect the intensity and input of green R&D in the current period; and from the point of view of green technological innovation itself, its own green attributes are able to reduce energy inputs in production, increase the efficiency of raw material utilization, and improve existing production technology in order to improve energy efficiency and reduce the intensity of carbon emissions [

47]. From the perspective of its environmental effect, green technology innovation can accelerate the green upgrading of industries, promote the transformation of energy structures, and thus reduce the intensity of carbon emissions [

48,

49]. Based on its environmental effect, green technological innovation can accelerate the green upgrading of industries, promote the transformation of energy structures, and thus reduce the intensity of carbon emissions. Therefore, it is concluded that green finance can reduce carbon emission intensity through green technological innovation. According to column (3) of

Table 2, green finance, which represents the government’s willingness to invest in green investments, significantly induces social capital investment, can attract private capital, and can promote the formation and improvement of the green financial market [

15]. Green financial investment mainly oriented to government finance can improve the industrial layout, can induce private investment to reduce carbon emission intensity, and can allow green finance to reduce carbon emission intensity by inducing private investment. Green finance can reduce carbon emission intensity by inducing social investment. According to column (4) of

Table 2, green finance significantly increases the percentage of social responsibility disclosure of listed companies. Social responsibility disclosure can improve the energy structure [

50], reduce the use of high-carbon energy, and strengthen the exit mechanism of the market [

51]. It also reduces the implementation of polluting projects and allows high-pollution enterprises to reduce carbon emissions. Therefore, green finance can reduce carbon emissions by improving social responsibility disclosure.

7. Heterogeneity Analysis

In order to study the heterogeneous effects of green finance on carbon emission intensity, this paper selects the government’s environmental attention (EA) and the scale of the financial sector (FS). According to EA and the FS, values greater than the annual means are recorded as 1, and those lower than the means are recorded as 0. They are then multiplied by green finance to obtain the regression results of the mediation effect model with regulation. In

Table 5, columns (1)–(3) are the regulation results of the government’s environmental attention, and columns (4)–(6) are the regulation results of the size of the financial industry. It can be seen that EA contributes to improvements in social investment and social responsibility information disclosure, but the promotion effect on green technological innovation is not significant. The FS contributes to improvements in green technological innovation and social investment, but the promotion effect on social responsibility information disclosure is not significant.

The government’s attention to the environment represents a region’s concern for the environment. The more the government cares about the environment, the better the development of green finance will be, which in turn will stimulate social investment to reduce the intensity of carbon emissions. The greater the government’s attention to the environment, the better it can promote the formation of corporate social responsibility and improve the social responsibility disclosure system, laws, and regulations, thus reducing carbon emission intensity. Green finance itself has financial attributes. The scale of the financial industry reflects the level of regional financial development, and a financial industry with a larger scale is conducive to the development of green finance, which in turn helps to alleviate the financial constraints of enterprises so that more enterprises can carry out green technological innovation. The better the development of the financial industry, the better the industry norms and requirements. Green finance requires enterprises to be responsible for the environment, which helps the disclosure of corporate social responsibility information. So far, Hypothesis 3 has been verified.

8. Conclusions and Recommendations

This paper analyzed the carbon emission reduction effect of green finance and its internal mechanism based on provincial unbalanced panel data from 2003 to 2021. It found that green finance has a significant carbon emission reduction effect, which can boost the regional green and low-carbon transformation, and this conclusion was still robust after excluding the impact of related environmental policies and instrumental variables to alleviate the endogeneity problem. The mechanism test found that green technology innovation, inducing social investment, and promoting the disclosure of the social responsibility information of listed companies are important paths to realize the carbon emission reduction effect of green finance. Heterogeneity analysis revealed that the government’s environmental attention and the level of financial industry development have heterogeneous effects on green technological innovation, social investment, and social responsibility disclosure. A high level of government environmental attention significantly induces social investment and promotes the social responsibility disclosure of listed companies but does not have a significant effect on green technological innovation. A high level of financial industry development can significantly promote green technology innovation and induce social investment but has no significant effect on social responsibility information disclosure, as shown in

Table 6.

Based on these findings, this paper makes the following policy recommendations:

First, the government should actively play the guiding role of green finance in the scientific and technological innovation of the “two high and one surplus” industry, carry out the green bond market to support low-carbon projects, and require enterprises to disclose emission data to guide investment to low-carbon direction. Encourage financial institutions to increase medium and long-term financial support for high-tech green technology research and development, and promote enterprises to implement substantive green innovation. Accelerate the development of green financial products for “two high and one surplus” enterprises, and broaden the investment and financing channels of high-emission enterprises by guiding asset securitization and other means. Promote enterprises to participate in the green bond market, provide personalized green loans, encourage transparent disclosure of carbon emissions data, and promote sustainable financial development.

Secondly, the government should establish and improve the sources of funds in the green financial market and guide the society to invest in green financial products through tax policies and incentives. While green financial products guide the capital of all sectors of society to flow into the field of green production, it is necessary to pay attention to the environmental supervision of green financial support projects. Financial institutions should innovate green financial products, provide sustainable investment choices, and guide social capital to tilt toward low-carbon industries.

Thirdly, the government can formulate regulations to require enterprises to disclose detailed carbon emission data in social responsibility reports, strengthen the social responsibility information disclosure mechanism of listed companies, establish a social responsibility information disclosure database of listed companies, link it with green finance, and provide information basis for the approval of green financial products such as green credit. Encourage listed companies to disclose social responsibility information and play a benchmark driving effect. The government can support financial institutions to establish a carbon emission verification system to ensure that investment projects meet emission reduction requirements. Financial institutions should provide professional consulting services to enhance the transparency of green financial products and jointly promote carbon emission reduction and sustainable development.

{kind=link}