1. Introduction

The South African agricultural sector, while modest in its overall contribution to the national economy, plays a pivotal role in ensuring accessible food and fostering economic growth, and serves as a significant employment source, particularly in rural areas [

1]. The sector’s diversity, encompassing field crops, horticulture, and animal production, significantly shapes the nation’s food security landscape. According to DALRRD [

1], the livestock industry is a dominant contributor, constituting 41.7% of South Africa’s total agricultural gross value, followed closely by field crops and horticulture, which contribute 31.5% and 26.8%, respectively.

The interconnections between livestock and field crops in South Africa are notable, with ties established through supply and demand dynamics in feed-related channels. Field crops like maize and soybeans are essential feed sources for the livestock industry. According to AFMA [

2], livestock feeds in South Africa mainly consist of maize (51.22%) and various oilcake (20.63%), with soybean oilcake contributing around 71% to the total oilcake percentage. Furthermore, NAMC [

3] indicated that approximately 70% of South Africa’s yellow maize demand during the 2022–2023 marketing year was attributed to the livestock industry. In the same marketing year, 9% of the total demand for soybeans in South Africa was attributed to full-fat soybeans, while 77% was attributed to soybean oilcake, both essential components in livestock feed. The statistics presented strongly suggest a significant interdependence between the grain and livestock industries in South Africa, indicating a noteworthy relationship that is still relatively unexplored in the literature. According to Gardebroek et al. [

4], the close interconnection among agricultural commodities stems from their roles as substitutes in demand, common input costs, competition for limited natural resources, and access to shared market information. Understanding the livestock and grain industry relationship is crucial for ensuring food security, supporting economic growth, and promoting sustainable agricultural and food systems.

One crucial dimension in considering the various aspects of food security involves examining the inter-price relations within commodity markets [

5]. Surging price spillovers have the potential to lead to high inflation rates, large trade deficits, and unfavorable macroeconomic environments, especially in developing economies [

6]. A thorough understanding of commodity price spillovers is essential for navigating global markets [

7], predicting trends [

8], managing financial risks [

9,

10], and fostering sustainable agricultural practices [

11] to enhance economic resilience and food security overall. The importance of investigating price and volatility transmission dynamics across diverse commodity markets is evident based on the attention it has consistently received in the literature over time.

However recent black swan events such as the COVID-19 pandemic and the Russia–Ukraine invasion have renewed interest in commodity price volatility and dynamic spillovers [

10,

11,

12,

13,

14,

15,

16,

17]. This renewed interest underscores the importance of further investigating price and volatility transmission dynamics across diverse commodity markets. Notably, studies in South Africa have examined various aspects of price transmissions over time, encompassing both vertical and horizontal price spillover dynamics within the agricultural sector.

Moreover, complementary to this broader examination, studies have specifically explored vertical price transmissions within South African value chains. For instance, Alemu [

18] examined the relationship between producer and retail markets within South Africa’s food market. Similarly, research has investigated vertical transmission within key sectors such as the South African poultry industry [

19], providing valuable insights into the interactions between different stages of production and distribution. Additionally, a study conducted by Lombaard [

20] explored the South African beef value chain, offering further understanding of the vertical transmission mechanisms within the beef sector. In addition, Mosese [

21] specifically examined vertical transmission in the South African potato value chain, while Louw [

22] investigated price transmission in wheat-to-bread and maize-to-maize meal value chains.

In contrast, other studies have focused on horizontal price spillovers, exploring how price changes among related products influence one another within the same level of the supply chain. Kirsten [

23] examined how international commodity markets impact local prices in South Africa, specifically investigating the dynamic relationships between global maize and wheat prices and their counterparts in South Africa. Abidoye and Labuschagne [

24] studied the transmission of world maize prices to South African maize prices. Pierre and Kaminski [

25] focused on price transmission in South Africa’s maize markets and those of other African countries. Mokumako and Baliyan [

26] investigated the price dynamics between the South African and Botswanan maize markets. Myers [

27] studied maize price transmission between South Africa and Zambia. Mphateng [

28] assessed the transmission prices between world wheat prices and South African wheat prices. Ramoroka [

29] investigated inter-commodity producers’ price transmission between wheat and maize in South Africa. Pierre and Kaminski [

25] explored short-run price shock propagation among Sub-Saharan African maize markets, of which South Africa formed a part.

Despite the aforementioned research efforts directed at understanding the various dimensions of price transmissions within South Africa’s agricultural sector, a significant gap in the literature is evident. There remains a significant gap regarding the dynamics of important grain feed prices and their impact on the livestock market in South Africa. Given the interconnected nature of South Africa’s livestock and grain industry and the possible consequences of significant price spillovers, it is essential to develop a comprehensive understanding of the inter-price dynamics of these markets. Failure to understand the relationship between South Africa’s grain and livestock markets hinders effective policymaking, strategic planning by industry stakeholders, and academic advancements within the South African agricultural context. Therefore, considering this gap, the objective of this study is to provide a comprehensive understanding of the interdependence and dynamics between the livestock and grain markets in South Africa. The primary research question guiding our investigation is: What are the dynamics of price transmissions between these two markets, and how can understanding these dynamics contribute to enhancing market efficiency and stability within the South African agricultural context? The findings obtained from our research are anticipated to be valuable for informing decision-making and enhancing understanding of the dynamics within the South African agricultural sector. Specifically, by investigating the dynamics of price transmissions between these key markets, our research not only addresses a critical knowledge gap but also provides valuable insights that directly contribute to improving South Africa’s food security landscape. Understanding price dynamics in these sectors helps identify potential disruptions or vulnerabilities that could affect food availability and affordability, ultimately impacting food security.

The paper is structured as follows:

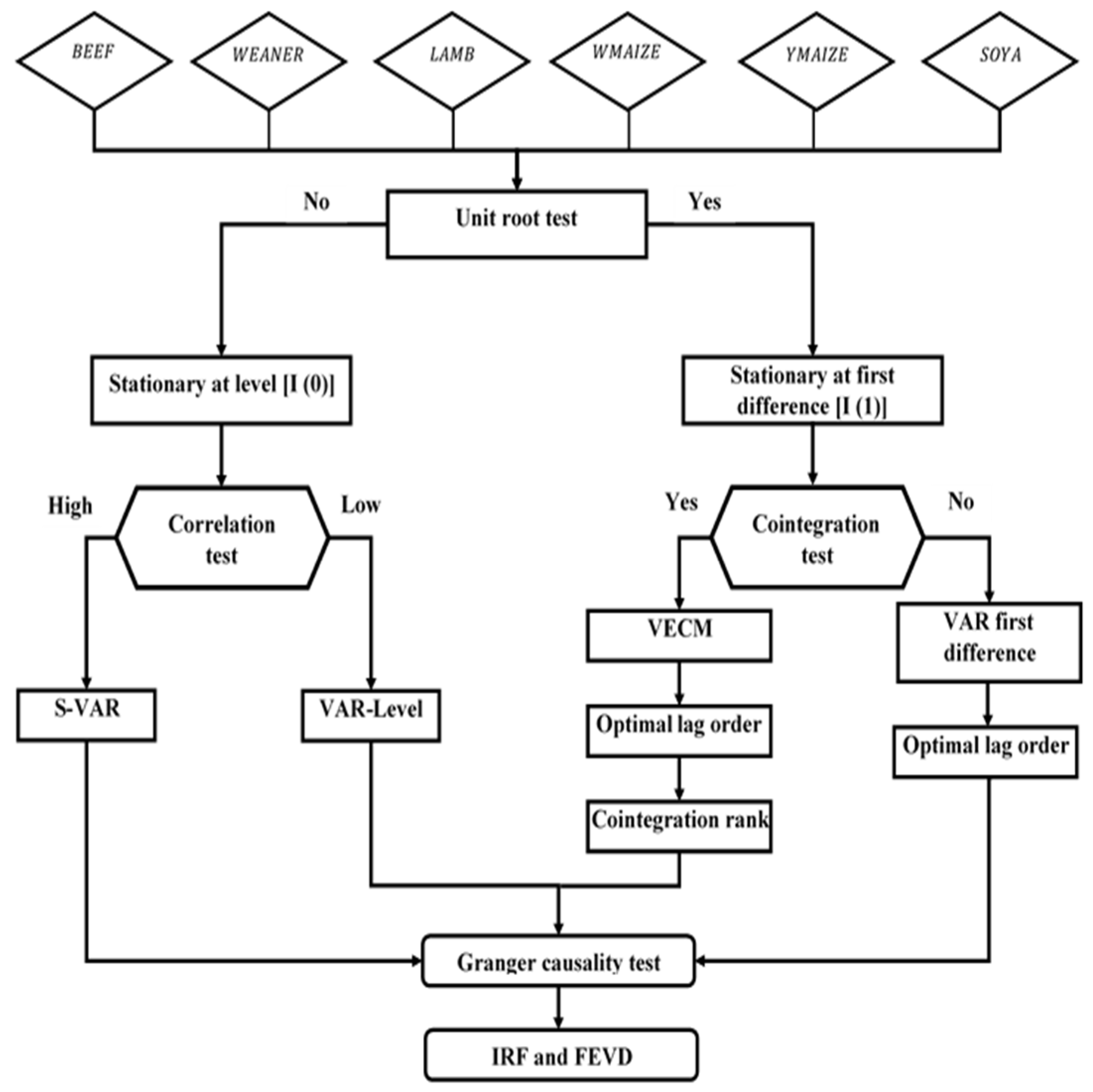

Section 2 presents the methods and data utilized in the study.

Section 3 discusses the empirical results. In

Section 4, the findings are analyzed and discussed. Finally,

Section 5 provides the concluding remarks.

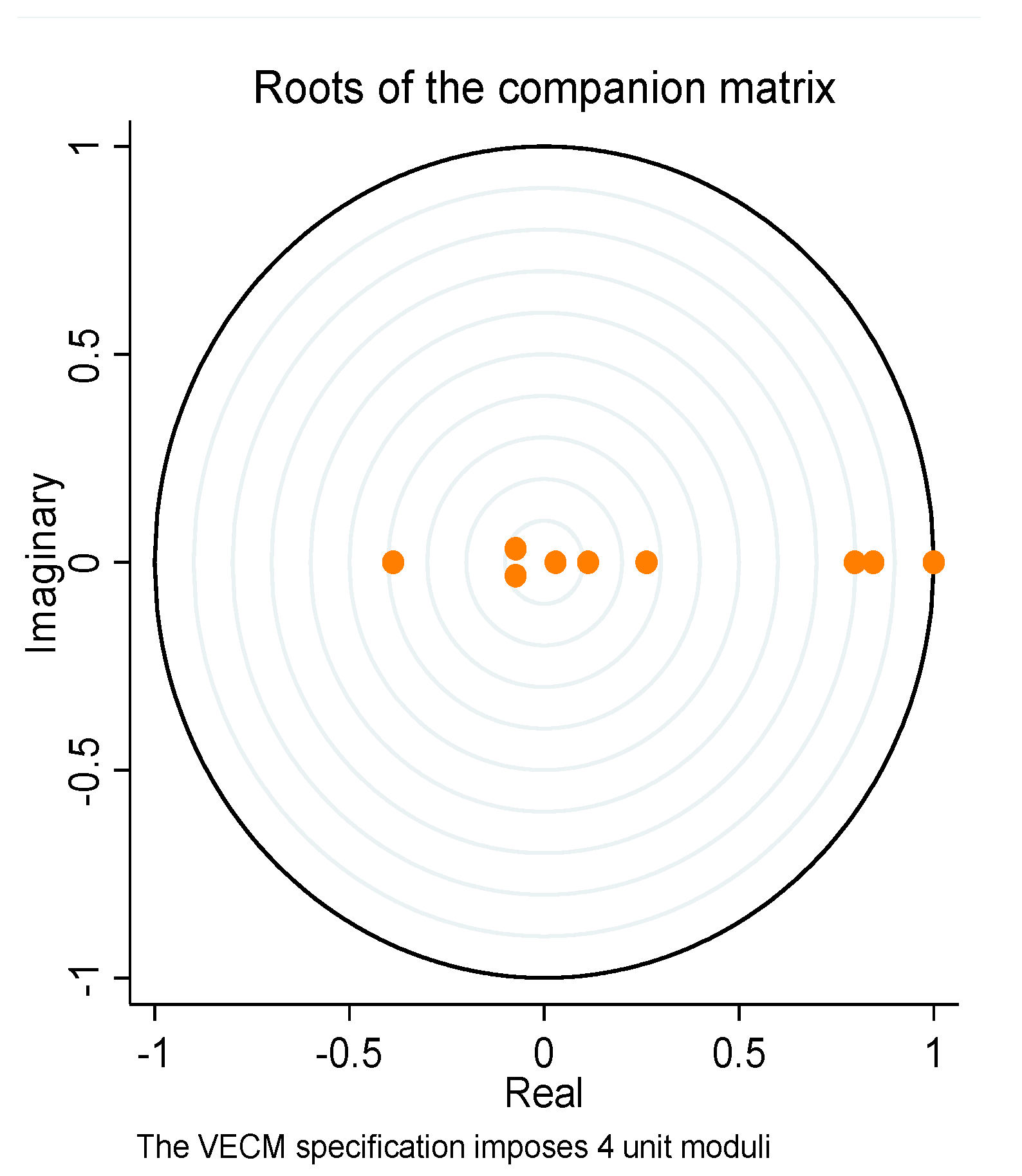

4. Discussion

In this article, using the Johansen cointegration test, it was established that there is a long-run relationship among the study variables. This contrasts with Musunuru’s [

41] findings, where the author observed no long-run relationship between grain and meat prices, only identifying short-run relationships. This disparity underscores how commodity market dynamics can vary across different countries or regions.

Furthermore, the consistently low error correction terms obtained from the VECM estimates (

Table 7) imply that deviations from the long-run equilibrium take time to correct in the short term. Our study’s identification of consistently low error correction terms aligns with the research conducted by De Zhou and Koemle [

42], who found comparable slow adjustment dynamics in China’s hog and feed markets. Our study focused on live weaner prices as our primary livestock variable, whereas De Zhou and Koemle’s [

42] research centered on China’s hog market. Despite the difference in livestock species, our comparative analysis highlights different dynamics between live animal variables. De Zhou and Koemle’s [

42] findings suggest an 11-month adjustment period for hog prices, whereas our study revealed a 3.5-month correction period for live weaner prices in South Africa. Additionally, slow adjustments were also observed in other livestock markets. For instance, Ajjan et al. [

43] found that the maize and poultry market in India is cointegrated, with the highest speed of adjustment found in their study for egg prices at 12% per week, translating roughly to 2 months to fully correct a deviation from the long-run equilibrium. This comparison further underscores broader patterns in market dynamics across livestock sectors and geographical regions.

Moreover, our examination revealed differing rates of adjustment among our study variables, suggesting an asymmetrical transmission of prices within South Africa’s grain and livestock sector. This parallels De Zhou and Koemle’s [

42] research, which similarly identified varying adjustment speeds across different markets in China, encompassing hogs, maize, and soybeans. The variations in adjustment speeds across different variables suggest potential inefficiencies within the grain and livestock markets, warranting further investigation into the factors driving these differences.

In addition, our study confirmed a long-term positive relationship between yellow maize and soybean prices and live weaner prices. This finding is similar to Ozdemir’s [

44] observations regarding the significant influence of grain feed prices on the beef market in the U.S. Additionally, our analysis resembles the insights of Wang et al. [

45] in China, which highlight the impact of minor increases in hog prices on breeding costs and overall hog prices. Moreover, Tejeda and Goodwin’s [

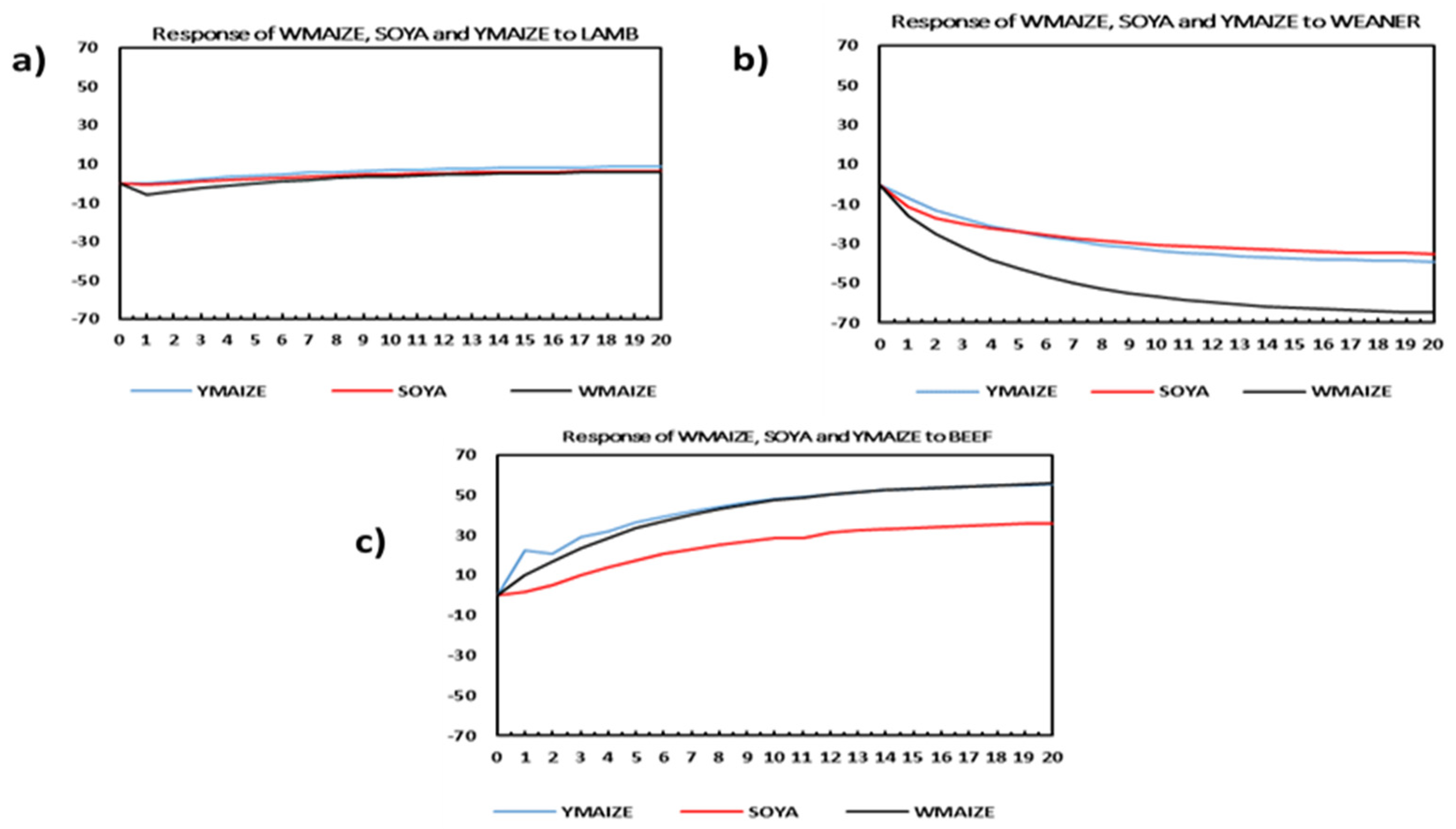

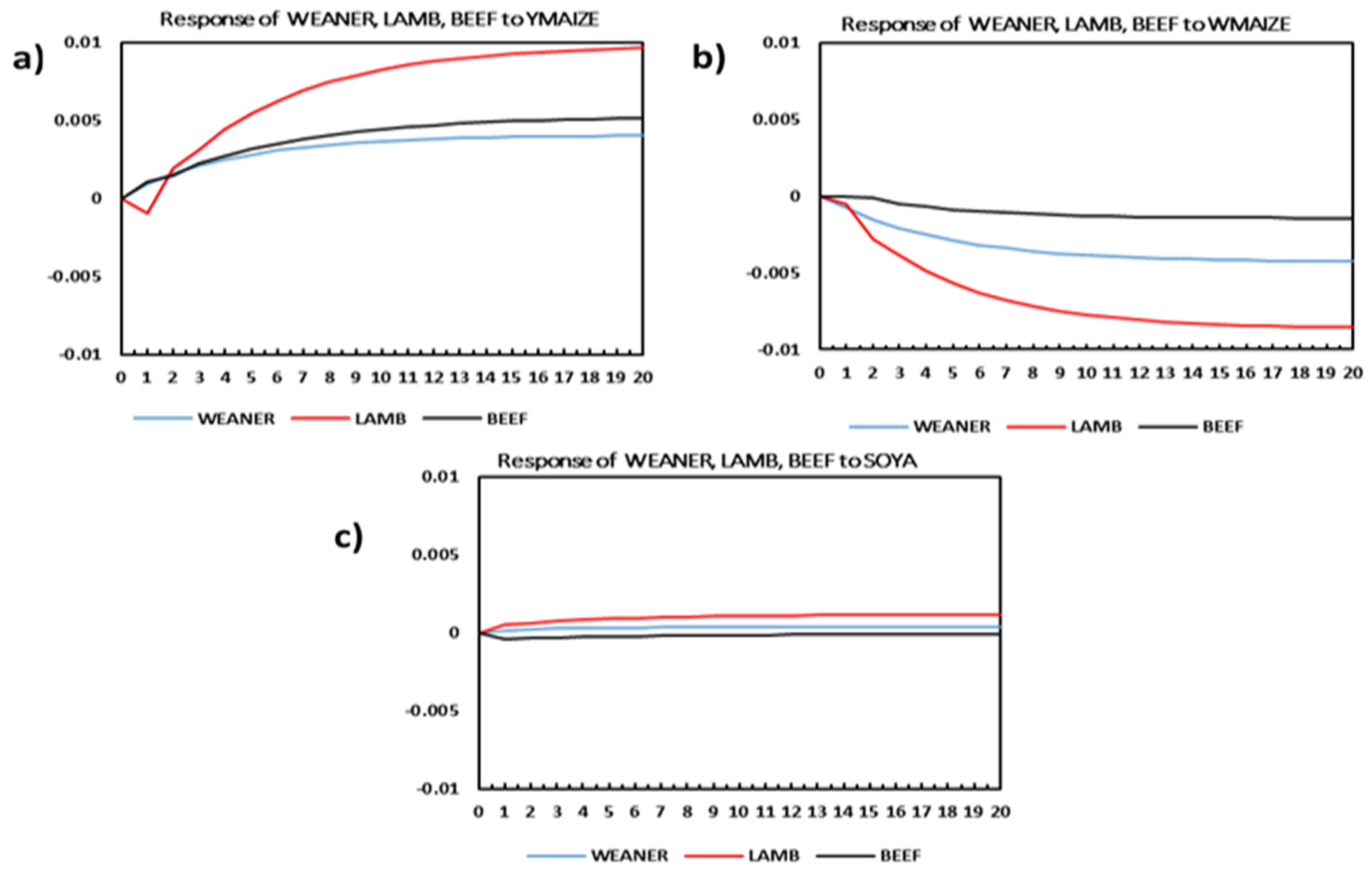

46] research underscores the broader implications of input price increases on livestock and food prices, a concept further supported by our findings. Particularly, our impulse response functions demonstrate the direct effect of South African yellow maize market shocks on livestock prices. Thus, although each study offers unique insights, our findings contribute to a more comprehensive understanding of the universal importance of grain prices in shaping livestock markets, particularly emphasizing the significance of yellow maize and soybean prices in our analysis.

Our study results also revealed a positive long-run relationship between beef carcass prices and live weaner prices. This finding is supported by Oosthuizen [

47], who suggested that high beef carcass prices incentivize feedlots to purchase more weaners for feeding and eventual slaughter. The second cointegration equation (Equation (13)) further supports this relationship by indicating that as beef and lamb carcass prices increase over the long run, yellow maize prices also increase. This suggests that higher carcass prices stimulate demand for live weaners, subsequently leading to increased demand for feed commodities like yellow maize. Spies [

48] also observed significant price transmissions downward from retail to producer levels in the South African beef value chain, aligning with our findings on the influence of beef carcass prices on live weaners. The findings from our study, complemented by the studies of Oosthuizen [

47] and Spies [

48], contribute to a deeper understanding of how pricing dynamics operate within the livestock sector.

Furthermore, the long-term positive impact of beef and lamb carcass prices on yellow maize prices aligns with the findings of Seok et al. [

49], who observed a significant influence of beef prices on yellow maize prices in the U.S. Seok et al. [

49] attributed this connection to the substantial size of the beef market in the U.S., which exerts significant demand pressure on yellow maize prices. Marsh [

50] also observed that the yellow maize sector in the U.S. benefits from increased demand in the beef retail market, leading to heightened demand for animal feeds. South Africa is suspected to share a similar situation to the U.S. regarding a significant portion of the demand for yellow maize originating from the livestock industry. According to the NAMC [

3], the livestock sector in South Africa accounts for approximately 70% of the demand for yellow maize and 86% of the demand for soybeans. Considering our results and the statistics provided by NAMC [

3], it appears that the South African beef market exercises price leadership in the South African yellow maize market. These insights indicate the intricate dynamics between livestock and grain markets, highlighting the lasting influence of livestock prices on yellow maize prices in both the U.S. and South Africa.

Also notable from the second cointegrating equation (Equation (13)) is that an increase in live weaner prices has a negative effect on yellow maize prices. Although the beef carcass market plays a dominant role in the South African yellow maize market, it seems that fluctuations in weaner calf prices also play a role in shaping this relationship. Marsh [

50] noted that North America’s 2003 bovine spongiform encephalopathy (BSE) outbreaks negatively affected feeder cattle, slaughter cattle, and corn markets. Though not explicitly mentioned by Marsh [

50], it can be inferred that BSE reduced the number of live weaners, consequently diminishing the demand for yellow maize. This inference supports our finding that higher live weaner prices negatively impact yellow maize prices, as reduced demand corresponds with weaner calf price fluctuations. South Africa’s livestock market is susceptible to disease outbreaks such as foot and mouth disease (FMD), which detrimentally affects industry productivity [

51,

52,

53]. Therefore, our findings and those of Marsh [

50] highlight the critical importance of understanding livestock–grain market dynamics, external factors like disease outbreaks, and informed decision-making for enhancing market stability and resilience in South Africa’s agricultural sector.

The error correction term for soybean prices lacks statistical significance, indicating that deviations from long-run equilibrium do not significantly affect soybean prices. Our causality tests confirmed that other variables do not affect soybean prices significantly. Additionally, impulse response function analysis suggests minimal impact of soybean market shocks on livestock prices. Our results are comparable to those of Fiszeder and Orzeszko [

54], who similarly observed limited causal relationships involving soybean prices relative to the livestock market in the U.S. The isolation of soybean prices from livestock variables in our study may be attributed to unique factors in the South African livestock and grain markets. Firstly, according to AFMA [

2], soybeans constitute only about 15% of the total feed content in South Africa, suggesting its limited direct impact on overall livestock production. Similarly, Fiszeder and Orzeszko [

54] attributed the lack of causal effects between livestock market and soybean price to the fact that cattle are not a huge consumer of soybeans, and therefore such a result is expected. The low usage of soybeans in livestock feeds is attributed to soybean’s status as one of the most expensive protein sources in feed rations [

55]. Secondly, South Africa’s soybean production has experienced significant growth in recent years, accompanied by a substantial increase in soybean processing capacity. However, the South African soybean market can be considered to be in its infancy, with connections between the soybean and livestock industries yet to reach full maturity. As production stabilizes and market dynamics evolve, more significant interactions may emerge in the future.

Also notable from the results is the low FEVD of white maize due to its past shocks, suggesting that external factors significantly influence South Africa’s white maize market. Previous studies have identified various external factors as key drivers of white maize prices in South Africa [

24,

56,

57,

58]. Therefore, our results support the notion of the importance of considering external influences when analyzing white maize price dynamics in South Africa.

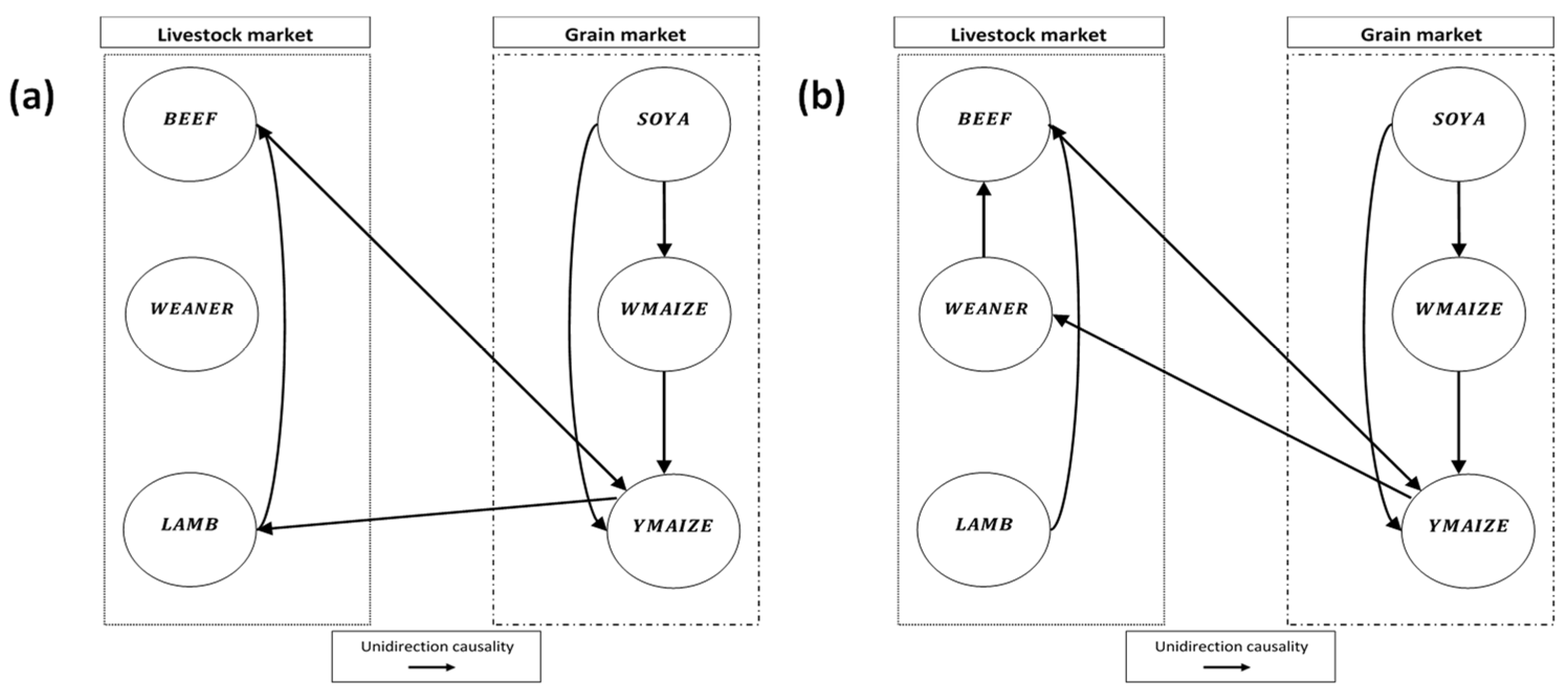

Our study, employing the Toda–Yamamoto causality test, revealed significant short-run relationships, particularly within the grain market, where all causal links converge on yellow maize. This aligns with the statistics provided by the AFMA [

2] highlighting yellow maize’s dominant role in South Africa’s livestock feed sector. Importantly, our findings underscore the pivotal role of yellow maize as the sole grain variable influenced by the livestock market, thus serving as a crucial bridge between the grain and livestock sectors, a perspective also emphasized by the AFMA’s [

2] data. Interestingly, our results parallel those of Tegle [

59], who similarly found limited causal relationships between grain and livestock variables but identified strong causal relationships among various grains. However, our study diverges from Tegle’s [

59] findings in one key aspect. Whereas Tegle [

59] found that other grain variables also impact soybeans, our results indicate that none of our study variables influenced soybeans. Overall, our causality results underscore pivotal role of yellow maize in facilitating market linkages between the grain and livestock sectors in South Africa.

Furthermore, elaborating on the Toda–Yamamoto causality test results in the livestock market, lamb carcass and live weaner prices were found to Granger cause beef carcass prices, while beef carcass prices influenced yellow maize prices in the grain market. The unidirectional causal effect from lamb to beef carcass prices is consistent with the findings of Lawrence et al. [

60] on cross-commodity price transmission between beef and mutton in the U.S. Pozo and Schroeder [

61] observed that consumer preferences and disposable income also drive the substitution effect between beef and lamb consumption. Ogundeji and Maré [

62] also noted that the substitution between beef and lamb particularly occurs in market situations with relatively high beef prices. Our Toda–Yamamoto causality test also identified a unidirectional causal relationship from live weaner prices to beef carcass prices, consistent with the upward causal relationships observed in the South African beef value chain by spies [

48].

5. Conclusions

This study has shed light on the complex interactions between South Africa’s livestock and grain markets, uncovering noteworthy findings with important implications for policymakers and stakeholders. Specifically addressing the research question posed in the introduction, our research has provided a comprehensive examination of the dynamics of price transmissions between these markets, offering valuable insights for policymakers and stakeholders to consider when addressing challenges and capitalizing on opportunities within the agricultural sector. Firstly, the confirmation of a long-run relationship among the study variables underscores the interconnectedness within the South African grain and livestock markets. Additionally, the observed consistently low error correction terms highlight the slow adjustment dynamics, indicative of asymmetric price transmission. To address these findings, policymakers should prioritize the implementation of measures aimed at stabilizing both grain and livestock markets. Specifically for the grain market, regulations could focus on ensuring fair pricing mechanisms, promoting transparency in trading, and preventing market manipulation. Similarly, for the livestock market, policies could be implemented to address issues such as animal welfare standards, disease control measures, and fair-trade practices. By fostering market resilience and mitigating the impact of asymmetries in price transmission, these measures can enhance the overall stability and sustainability of the South African agricultural sector, ensuring more robust market conditions for stakeholders across the value chain.

Secondly, the observation regarding the significant influence of external factors on South Africa’s white maize market highlights a critical concern, especially considering its status as a staple food source for South Africa and other SADC members reliant on imports from South Africa. Given the global predominance of yellow maize production and the limited availability of white maize, South Africa could face challenges in securing reliable sources for white maize imports during shortages and drought. Policymakers need to strategize to increase white maize hectares without compromising yellow maize production, considering the country’s significant yellow maize exports. Balancing these priorities is essential to ensure food security and stability in South Africa and among other African countries reliant on South Africa.

Thirdly, our findings indicate that soybean prices in South Africa are relatively insulated from the influence of other study variables, as evidenced by the lack of statistical significance in the error correction term and causality test results. The minimal impact of soybean market shocks on livestock prices further underscores this independence. These findings emphasize the importance for stakeholders to acknowledge the emerging nature of the soybean industry in South Africa. These results suggest a need for stakeholders to explore diversification opportunities in livestock feed sources. By reducing dependency on specific inputs like soybeans, the livestock market can enhance its resilience and mitigate risks associated with fluctuations in the emerging South African soybean market.

In addition, it might be noteworthy for policymakers to also encourage collaboration between the grain and livestock sectors in South Africa for fostering better market understanding, facilitating policy formulation, and enhancing overall agricultural sustainability. Although Grain South Africa (Grain SA) and the Red Meat Producers Organization (RPO) hold separate annual congress meetings for their respective members, there is a pressing need to encourage collaborative efforts between these sectors to maximize the effectiveness of policymaking and industry development initiatives. Therefore, policymakers should consider facilitating a collaborative effort between these two sectors annually, as they are highly interrelated, as highlighted by our results.

Acknowledging certain limitations, this study highlights areas for future consideration. Firstly, the analysis, conducted within a VAR/VECM framework, requires further robustness to address potential endogeneity issues arising from policy changes or exogenous shocks affecting grain and livestock markets. Secondly, our reliance on economic variables overlooks influential factors such as environmental impact and government policies, which could significantly influence price dynamics. Lastly, our focus on price relationships neglects other critical factors, such as supply–demand dynamics, technological advancements, and international trade policies, which could enhance the comprehensiveness of our understanding of the grain–livestock market dynamics in South Africa. Future research should strive to incorporate these factors for a more comprehensive understanding of market dynamics. Additionally, future research should consider extending the time frame beyond the five-year period analyzed in this study. A more extensive time frame could further contribute to our understanding of the grain–livestock dynamics in South Africa by capturing long-term trends and fluctuations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}