How to Improve the Environmental, Social and Governance Performance of Chinese Construction Enterprises Based on the Fuzzy Set Qualitative Comparative Analysis Method

Abstract

:1. Introduction

2. Literature Review

2.1. Analysis of the Conditions in the Environmental Dimension

2.2. Analysis of the Conditions in the Social Dimension

2.3. Analysis of the Conditions in the Governance Dimension

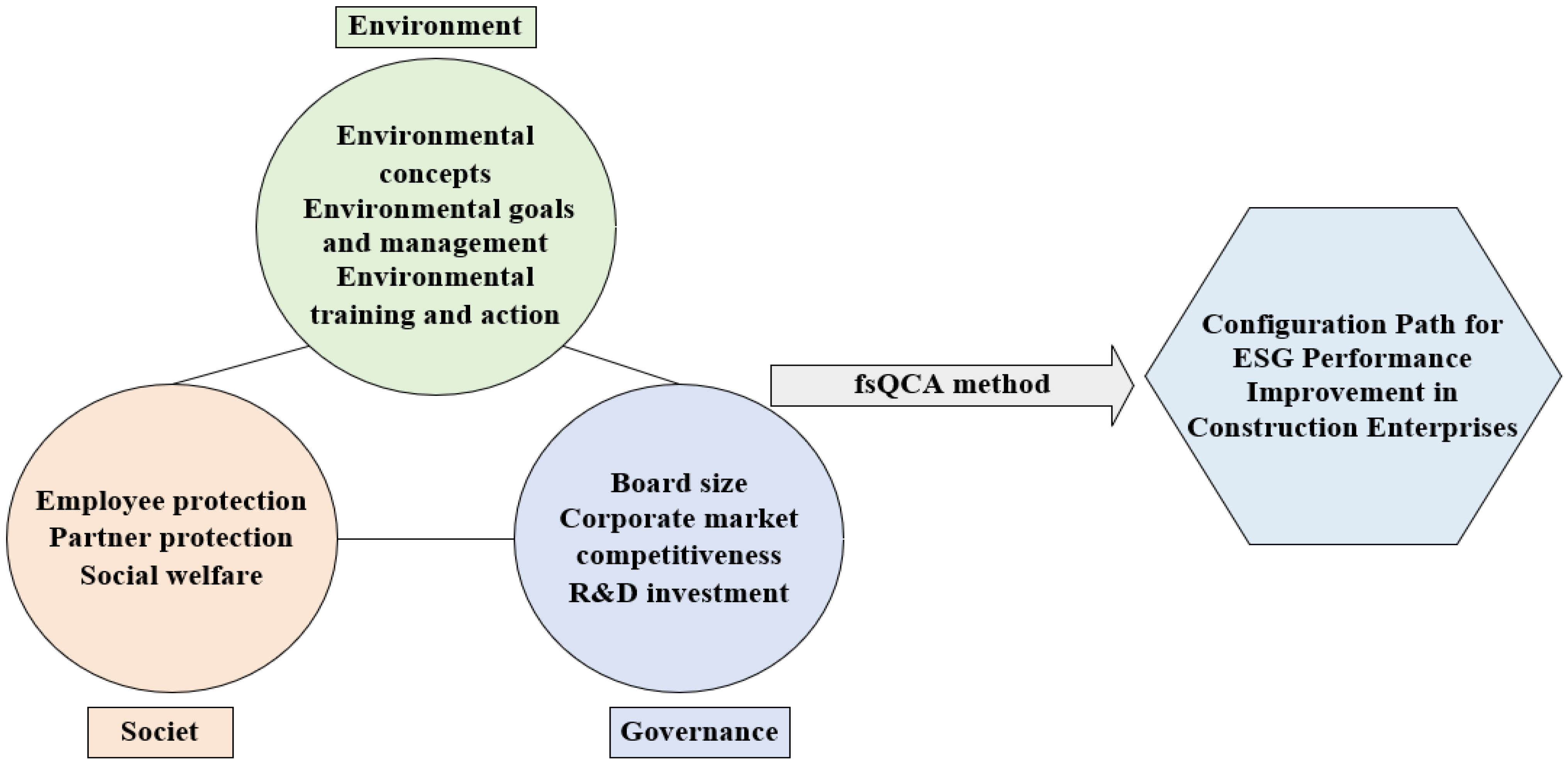

3. Research Design

3.1. Research Method

- ESG improvement in construction enterprises is subject to the synergistic effect of multiple variables. The fsQCA method is able to study the causal relationship of multiple conditions in terms of configuration perspective [36]. This helps to further explore the core role of relevant configuration conditions in enhancing the ESG performance of construction enterprises;

- Compared with ordinary regression analysis, the fsQCA method can determine whether the conditions are core or marginal variables [37];

- The fsQCA has a significant advantage in discussing the complementary substitution effects of different conditions. It provides an important reference for enterprises to adjust ESG improvement paths according to the characteristics of the industry [38].

3.2. Data Sources

3.3. Variable Measurement

- Outcome variables: The ESG ratings in the Wind database reflect the environmental performance, social performance and corporate governance of enterprises. The indicators which incorporate the characteristics of the industry avoid the homogenization of the ratings [39]. Therefore, the behavior regarding green products, low-carbon goals or social actions of enterprises can be evaluated more accurately. This paper assigned ESG ratings (C-AAA: nine ratings in total) sequentially from 1 to 9 to represent enterprise ESG performance [40].

- Conditional variables: At the environmental level, this paper selected three indicators: environmental concepts (ECs), environmental goals and management (EGM) and environmental training and action (ETA). For the measurement of the three indicators, this paper chose to semantically analyze the contents of the annual reports or ESG reports of enterprises [41]. If the report stated that the enterprise had an environmental concept, then it was determined that the enterprise would take a value of 1 for the EC indicator; otherwise, it would take a value of 0. If the report indicates that the enterprise has an environmental goal, environmental management system and environmental emergency response, then 1 point is awarded. The maximum number of points for EGM is 3 and the minimum is 0. Similarly, if the report shows that the enterprise has organized environmental training or environmental protection activities, it will receive 1 point. Then, the ETA indicator will show at most 2 points and at least 0 points.

4. Empirical Analysis and Results

4.1. Calibration

4.2. Analysis of Necessary Conditions

4.3. Configuration Analysis of Conditions

- C1 (EC*EP*SW*EGM*ETA*PP*~Lerner) shows that environmental goals and management play a central role. Environmental concepts, environmental training and action, employee protection, partner protection and social welfare are complementary to ESG performance. In particular, as governments continue to tighten environmental regulations, enterprises are being forced to meet government inspections [50]. The setting of environmental protection goals and management systems can be managed through the green design of products, the procurement of green materials, production and other processes [51]. By managing environmental protection in the whole process of construction, enterprises can reduce the risk of environmental pollution and environmental accidents [52].

- 2.

- C2 (EC*EP*SW*EGM*ETA*PP*RDR) shows that environmental training and actions play a central role. Environmental concepts, environmental goals and management, employee protection, partner protection, social welfare and R&D investment are supportive to ESG performance. The agency theory suggests that corporations can make commitments to the environment, thereby reducing the gap between ownership and control [55]. For example, when enterprise incentives are rewarded for environmentally beneficial governance, the managers are more likely to develop ESG performance in operations and strategies [55]. For employees, environmental training organized by the enterprise can enhance employees’ environmental awareness and motivation [56,57]. Environmental training provides employees with specialized skills and knowledge to address the complexities and challenges of environmental sustainability [57]. The efficiency of employees in practice will increase, which is favorable to improving the ESG performance [58]. Enterprises can guide employees to practice energy conservation in their work, such as by strengthening paperless office practices and purchasing green materials and products. Employees increase the possibility of green construction in practice, thus promoting excellent ESG performance.

- 3.

- C3 (EC*EP*SW*EGM*PP*~BS*~Lerner*~RDR) indicates that the core conditions are environmental concepts and partner protection. Environmental goals and management, employee protection and social welfare play a supporting role. The environmental concepts represent the attitude of construction enterprises to energy conservation and environmental protection. When environmental concepts penetrate into corporate culture, the environmental awareness of the enterprise will gradually strengthen. The long-term development strategy of an enterprise is also no longer confined to financial indicators [59]. During project construction, the promotion of green environmental concepts has not only become a new “business card” to help enterprises expand their market share, but also a means of support for enterprises to fulfill environmental protection practices in the process.

- 4.

- C4 (EC*EP*SW*ETA*PP*~BS*~Lerner*~RDR) argues that construction enterprises can utilize the synergies of environmental concepts, environmental training and actions, the protection of employees and partners and social welfare to improve ESG performance. As a dangerous industry, it is essential to focus on protecting the rights of employees in construction [28]. There are a variety of measures protecting employees, such as health and safety protection, welfare protection, career development training and cultural communication [60]. These behaviors build a harmonious labor relationship and cohesive solidarity within the enterprise [61]. Employees gain a sense of fulfillment and happiness at work, which can have a positive effect on improving ESG performance and financial performance [62].

- 5.

- C5 (EC*~EP*SW*EGM*~ETA*~PP*BS*~Lerner*RDR) reveals that construction enterprises can improve ESG performance by leveraging synergies between environmental concepts, environmental goals and management, partner protection, social welfare, board size and R&D investment. C6 (EC*EP*SW*EGM*~ETA*PP*BS*Lerner*~RDR) demonstrates that enterprises can also improve their ESG performance through the synergies of environmental concepts, environmental goals and management, employee protection, partner protection, social good, board size and corporate market competitiveness.

4.4. Robustness Test

5. Conclusions

5.1. Research Findings

- (1)

- In Chinese construction enterprises, none of the individual conditional variables are necessary to lead to high ESG performance alone. This suggests that improving ESG performance in construction enterprises is a synergistic and complex process. It requires the collaboration of multiple conditions.

- (2)

- The results show that the path to achieving high ESG performance consists of six types of configuration conditions. They are the environmental goals and management-led improvement path, the environmental training and action-led improvement path, the environmental concept and partner protection joint-led improvement path, the environmental and social level synergistic improvement path and the two multifactorial composite improvement paths. Among them, the environmental goals and management-led improvement path covers the largest number of enterprises. This indicates that setting feasible environmental goals and establishing a complete environmental management system play a more significant role in improving the high ESG performance for construction enterprises.

- (3)

- Finally, environmental concepts, environmental goals and management, environmental training and action and partner protection are core conditions in C1, C2 and C3, respectively. This suggests that construction enterprises should first focus on the role of the environmental dimension and partner protection in improving ESG performance.

5.2. Research Implications

5.3. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Liao, P.C.; Liao, J.Q.; Wu, G.; Wu, C.-L.; Zhang, X.-L.; Ma, M.-C. Comparing international contractors’ CSR communication patterns: A semantic analysis. J. Clean. Prod. 2018, 203, 353–366. [Google Scholar] [CrossRef]

- Zhao, X.; Ma, S.; Liu, Y.; Chen, X.; Cai, H.; Zheng, H.; Shen, Y. ESG Performance, R&D Innovation and High Quality Development of Corporate: A Perspective Based on Firm Performance. Ind. Eng. Innov. Manag. 2022, 5, 23–34. [Google Scholar]

- Brooks, C.; Oikonomou, I. The effects of environmental, social and governance disclosures and performance on firm value: A review of the literature in accounting and finance. Br. Account. Rev. 2018, 50, 1–15. [Google Scholar] [CrossRef]

- Nekhili, M.; Boukadhaba, A.; Nagati, H.; Chtioui, T. ESG performance and market value: The moderating role of employee board representation. Int. J. Hum. Resour. Manag. 2021, 32, 3061–3087. [Google Scholar] [CrossRef]

- Sun, G.; Guo, C.; Ye, J.; Ji, C.; Xu, N.; Li, H. How ESG contribute to the high-quality development of state-owned enterprise in China: A multi-stage FsQCA method. Sustainability 2022, 14, 15993. [Google Scholar] [CrossRef]

- Zumente, I.; Bistrova, J. ESG importance for long-term shareholder value creation: Literature vs. practice. J. Open Innov. Technol. Mark. Complex. 2021, 7, 127. [Google Scholar] [CrossRef]

- Hua, Z.; Oguz Erkal, E.D. Exploring the Landscape: Environmental, Social, and Governance (ESG) in the Construction Industry. In Proceedings of the Construction Research Congress, Des Moines, IA, USA, 20–23 March 2024; pp. 86–95. [Google Scholar]

- Morea, D.; Mango, F.; Cardi, M.; Paccione, C.; Bittucci, L. Circular economy impact analysis on stock performances: An empirical comparison with the euro stoxx 50® ESG index. Sustainability 2022, 14, 843. [Google Scholar] [CrossRef]

- Guo, H.; Lu, W. How Do Chinese International Construction Companies View Corporate Social Responsibility? In Proceedings of the 25th International Symposium on Advancement of Construction Management and Real Estate, Wuhan, China, 28–30 November 2020; Springer: Singapore, 2021; pp. 1407–1419. [Google Scholar]

- Li, S.; Yin, P.; Liu, S. Evaluation of ESG ratings for Chinese listed companies from the perspective of stock price crash risk. Front. Environ. Sci. 2022, 10, 933639. [Google Scholar] [CrossRef]

- Liao, P.C.; Shih, Y.N.; Wu, C.L.; Zhang, X.-L.; Wang, Y. Does corporate social performance pay back quickly? A longitudinal content analysis on international contractors. J. Clean. Prod. 2018, 170, 1328–1337. [Google Scholar] [CrossRef]

- Li, Z.F.; Lu, X.; Wang, J. Corporate Social Responsibility and Goodwill Impairment: Evidence from Charitable Donations of Chinese Listed Companies. SSRN 2023, 4337571. [Google Scholar] [CrossRef]

- Xie, J.; Nozawa, W.; Yagi, M.; Fujii, H.; Managi, S. Do environmental, social, and governance activities improve corporate financial performance? Bus. Strategy Environ. 2019, 28, 286–300. [Google Scholar] [CrossRef]

- Chen, S.; Song, Y.; Gao, P. Environmental, social, and governance (ESG) performance and financial outcomes: Analyzing the impact of ESG on financial performance. J. Environ. Manag. 2023, 345, 118829. [Google Scholar] [CrossRef] [PubMed]

- Xia, Q.; Liu, Y.; Wei, F. How can ESG funds improve their performance?—Based on the DEA-Malmquist productivity index and fsQCA method. JUSTC 2023, 53, 0803. [Google Scholar] [CrossRef]

- Xu, J.; Liu, F.; Shang, Y. R&D investment, ESG performance and green innovation performance: Evidence from China. Kybernetes 2021, 50, 737–756. [Google Scholar]

- WCED. Our Common Future; Oxford University Press: Oxford, UK, 1987; pp. 34–44. [Google Scholar]

- Zhou, G.; Liu, L.; Luo, S. Sustainable development, ESG performance and company market value: Mediating effect of financial performance. Bus. Strategy Environ. 2022, 31, 3371–3387. [Google Scholar] [CrossRef]

- Aras, G.; Crowther, D. Governance and sustainability: An investigation into the relationship between corporate governance and corporate sustainability. Manag. Decis. 2008, 46, 433–448. [Google Scholar] [CrossRef]

- Bozec, Y.; Bozec, R. Corporate governance quality and the cost of capital. Int. J. Corp. Gov. 2011, 2, 217–236. [Google Scholar] [CrossRef]

- Jiang, W.; Wong, J.K. Key activity areas of corporate social responsibility (CSR) in the construction industry: A study of China. J. Clean. Prod. 2016, 113, 850–860. [Google Scholar] [CrossRef]

- Ojo, L.D.; Oladinrin, O.T.; Obi, L. Critical barriers to environmental management system implementation in the Nigerian construction industry. Environ. Manag. 2021, 68, 147–159. [Google Scholar] [CrossRef]

- Ge, G.; Xiao, X.; Li, Z.; Dai, Q. Does ESG performance promote high-quality development of enterprises in China? The mediating role of innovation input. Sustainability 2022, 14, 3843. [Google Scholar] [CrossRef]

- Porter, M.E.; Linde, C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Xia, J. A Systematic Review: How Does Organisational Learning Enable ESG Performance (from 2001 to 2021)? Sustainability 2022, 14, 16962. [Google Scholar] [CrossRef]

- Claessens, S.; Yurtoglu, B.B. Corporate Governance and Development: An Update; World Bank Group: Washington, DC, USA, 2012. [Google Scholar]

- Hadro, D.; Fijałkowska, J.; Daszyńska-Żygadło, K.; Zumente, I.; Mjakuškina, S. What do stakeholders in the construction industry look for in non-financial disclosure and what do they get? Meditari Account. Res. 2022, 30, 762–785. [Google Scholar] [CrossRef]

- Husted, B.W.; de Sousa-Filho, J.M. The impact of sustainability governance, country stakeholder orientation, and country risk on environmental, social, and governance performance. J. Clean. Prod. 2017, 155, 93–102. [Google Scholar] [CrossRef]

- Yu, E.P.Y.; Van Luu, B.; Chen, C.H. Greenwashing in environmental, social and governance disclosures. Res. Int. Bus. Financ. 2020, 52, 101192. [Google Scholar] [CrossRef]

- Chen, H. Corporate Board Diversity and ESG Performance in the Context of Big Data Management. In Proceedings of the 2023 3rd International Conference on Public Management and Intelligent Society (PMIS 2023), Wuhan, China, 24–26 March 2023; Atlantis Press: Amsterdam, The Netherlands, 2023; pp. 326–343. [Google Scholar]

- Suttipun, M. The influence of board composition on environmental, social and governance (ESG) disclosure of Thai listed companies. Int. J. Discl. Gov. 2021, 18, 391–402. [Google Scholar] [CrossRef]

- Anyigbah, E.; Kong, Y.; Edziah, B.K.; Ahoto, A.T.; Ahiaku, W.S. Board Characteristics and Corporate Sustainability Reporting: Evidence from Chinese Listed Companies. Sustainability 2023, 15, 3553. [Google Scholar] [CrossRef]

- Zheng, J.; Khurram, M.U.; Chen, L. Can green innovation affect ESG ratings and financial performance? evidence from Chinese GEM listed companies. Sustainability 2022, 14, 8677. [Google Scholar] [CrossRef]

- Ghoul, S.E.; Guedhami, O.; Kim, Y. Country-level institutions, firm value, and the role of corporate social responsibility initiatives. J. Int. Bus. Stud. 2017, 48, 360–385. [Google Scholar] [CrossRef]

- Fiss, P.C. A set-theoretic approach to organizational configurations. Acad. Manag. Rev. 2007, 32, 1180–1198. [Google Scholar] [CrossRef]

- Ma, T.; Liu, Y. Multiple paths to enhancing the resilience of project-based organizations from the perspective of CSR configuration: Evidence from the Chinese construction industry. Eng. Constr. Archit. Manag. 2024, 31, 835–865. [Google Scholar] [CrossRef]

- Fiss, P.C. Building better causal theories: A fuzzy set approach to typologies in organization research. Acad. Manag. J. 2011, 54, 393–420. [Google Scholar] [CrossRef]

- Pappas, I.O.; Woodside, A.G. Fuzzy-set Qualitative Comparative Analysis (fsQCA): Guidelines for research practice in Information Systems and marketing. Int. J. Inf. Manag. 2021, 58, 102310. [Google Scholar] [CrossRef]

- Liu, P.; Zhu, B.; Yang, M.; Chu, X. ESG and financial performance: A qualitative comparative analysis in China’s new energy companies. J. Clean. Prod. 2022, 379, 134721. [Google Scholar] [CrossRef]

- Lu, Y.; Xu, C.; Zhu, B.; Sun, Y. Digitalization transformation and ESG performance: Evidence from China. Bus. Strategy Environ. 2024, 33, 352–368. [Google Scholar] [CrossRef]

- Wang, Z.; Deng, Y.; Xie, W. Influential Factors of Digital Innovation in Manufacturing Enterprises Based on the fsQCA Method. Sci. Technol. Manag. Res. 2023, 43, 20–30. [Google Scholar]

- Lewellyn, K.; Muller-Kahle, M. ESG leaders or laggards? A configurational analysis of ESG performance. Bus. Soc. 2023, 63, 00076503231182688. [Google Scholar] [CrossRef]

- Hottenrott, H.; Peters, B. Innovative capability and financing constraints for innovation: More money, more innovation? Rev. Econ. Stat. 2012, 94, 1126–1142. [Google Scholar] [CrossRef]

- Tan, J.; Wei, J. Configurational Analysis of ESG Performance, Innovation Intensity, and Financial Leverage: A Study on Total Factor Productivity in Chinese Pharmaceutical Manufacturing Firms. J. Knowl. Econ. 2023, 1–25. [Google Scholar] [CrossRef]

- Schmitt, A.K.; Grawe, A.; Woodside, A.G. Illustrating the power of fsQCA in explaining paradoxical consumer environmental orientations. Psychol. Mark. 2017, 34, 323–334. [Google Scholar] [CrossRef]

- Lyu, T.; Shen, Q. A fuzzy-set qualitative comparative analysis (fsQCA) study on the formation mechanism of Internet platform companies’ social responsibility risks. Electron. Mark. 2024, 34, 5. [Google Scholar] [CrossRef]

- Ragin, C.C. Redesigning Social Inquiry: Fuzzy Sets and Beyond; University of Chicago Press: Chicago, IL, USA, 2009. [Google Scholar]

- Rihoux, B.; Ragin, C.C. Configurational Comparative Methods: Qualitative Comparative Analysis (QCA) and Related Techniques; Sage Publications: Thousand Oaks, CA, USA, 2008. [Google Scholar]

- Wang, S.; Esperança, J.P. Can digital transformation improve market and ESG performance? Evidence from Chinese SMEs. J. Clean. Prod. 2023, 419, 137980. [Google Scholar] [CrossRef]

- He, X.; Jing, Q.; Chen, H. The impact of environmental tax laws on heavy-polluting enterprise ESG performance: A stakeholder behavior perspective. J. Environ. Manag. 2023, 344, 118578. [Google Scholar] [CrossRef]

- Wong, C.W.; Wong, C.Y.; Boon-itt, S. Environmental management systems, practices and outcomes: Differences in resource allocation between small and large firms. Int. J. Prod. Econ. 2020, 228, 107734. [Google Scholar] [CrossRef]

- Bravi, L.; Santos, G.; Pagano, A.; Murmura, F. Environmental management system according to ISO 14001: 2015 as a driver to sustainable development. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2599–2614. [Google Scholar] [CrossRef]

- Bernardo, M.; Simon, A.; Tarí, J.J.; Molina-Azorín, J.F. Benefits of management systems integration: A literature review. J. Clean. Prod. 2015, 94, 260–267. [Google Scholar] [CrossRef]

- CCCG. Social Responsibility Report 2022; China Communications Construction Group Ltd.: Beijing, China, 2022; Available online: https://www.ccccltd.cn/shzr/zrbg/202311/P020231122619351166471.pdf (accessed on 2 November 2023).

- Khatib, S.F.; Al Amosh, H. Corporate Governance, Management Environmental Training, and Carbon Performance: The UK Evidence. J. Knowl. Econ. 2023, 1–23. [Google Scholar] [CrossRef]

- Willard, B. The New Sustainability Advantage: Seven Business Case Benefits of a Triple Bottom Line; New Society Publishers: Gabriola, BC, Canada, 2012. [Google Scholar]

- Singh, S.K.; Chen, J.; Del Giudice, M.; El-Kassar, A.N. Environmental ethics, environmental performance, and competitive advantage: Role of environmental training. Technol. Forecast. Soc. Chang. 2019, 146, 203–211. [Google Scholar] [CrossRef]

- Jin, M.; Kim, B. The effects of ESG activity recognition of corporate employees on job performance: The case of South Korea. J. Risk Financ. Manag. 2022, 15, 316. [Google Scholar] [CrossRef]

- Li, J.; Li, S. Environmental protection tax, corporate ESG performance, and green technological innovation. Front. Environ. Sci. 2022, 10, 982132. [Google Scholar] [CrossRef]

- Zhang, Q.; Oo, B.L.; Lim, B.T.H. Key practices and impact factors of corporate social responsibility implementation: Evidence from construction firms. Eng. Constr. Archit. Manag. 2023, 30, 2124–2154. [Google Scholar] [CrossRef]

- Li, X.S. Exploration on the localization management of Chinese enterprises’ international construction—Taking the Dubai market as an example. J. Shijiazhuang Railw. Univ. (Soc. Sci. Ed.) 2021, 15, 23–26. [Google Scholar]

- Zhang, T.; Zhang, J.; Tu, S. An Empirical Study on Corporate ESG Behavior and Employee Satisfaction: A Moderating Mediation Model. Behav. Sci. 2024, 14, 274. [Google Scholar] [CrossRef]

- Wang, T.K.; Zhang, Q.; Chong, H.Y.; Wang, X. Integrated supplier selection framework in a resilient construction supply chain: An approach via analytic hierarchy process (AHP) and grey relational analysis (GRA). Sustainability 2017, 9, 289. [Google Scholar] [CrossRef]

- Mahmood, Z.; Kouser, R.; Ali, W.; Ahmad, Z.; Salman, T. Does corporate governance affect sustainability disclosure? A mixed methods study. Sustainability 2018, 10, 207. [Google Scholar] [CrossRef]

- Husted, B.W.; de Sousa-Filho, J.M. Board structure and environmental, social, and governance disclosure in Latin America. J. Bus. Res. 2019, 102, 220–227. [Google Scholar] [CrossRef]

- Jensen, M.C. The modern industrial revolution, exit, and the failure of internal control systems. J. Financ. 1993, 48, 831–880. [Google Scholar] [CrossRef]

- Chang, A.S.; Paramosa, L.S.; Tsai, C.Y. Linking key topics to environmental indicators in corporate social responsibility reports of construction companies. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 1335–1347. [Google Scholar] [CrossRef]

- Gao, L.; Deng, X.; Yang, W.; Chang, T. Exploring Critical Factors Affecting Contractors’ Coopetition Relationship in International Construction Projects. Adv. Civ. Eng. 2021, 2021, 8897395. [Google Scholar] [CrossRef]

- Zhong, S.; Gao, W. Exploring the relationship of ESG score and firm value using fsQCA method: Cases of the Chinese manufacturing enterprises. Front. Psychol. 2022, 13, 1019469. [Google Scholar] [CrossRef]

- Schneider, C.Q.; Wagemann, C. Set-Theoretic Methods for the Social Sciences: A Guide to Qualitative Comparative Analysis; Cambridge University Press: Cambridge, UK, 2012. [Google Scholar]

- Leppänen, P.; George, G.; Alexy, O. When do novel business models lead to high performance? A configurational approach to value drivers, competitive strategy, and firm environment. Acad. Manag. J. 2023, 66, 164–194. [Google Scholar] [CrossRef]

{kind=link}

| Type | Variable | Calibration Information | |||

|---|---|---|---|---|---|

| N1 | N2 | N3 | |||

| Conditional variables | Environmental concepts | ECs | 1 | — | 0 |

| Environmental goal and management | EGM | 2.99 | 0.99 | 0.01 | |

| Environmental training and action | ETA | 1.99 | 0.99 | 0.01 | |

| Employee protection | EP | 1 | — | 0 | |

| Partner protection | PP | 1.99 | 0.99 | 0.01 | |

| Social welfare | SW | 1 | — | 0 | |

| Board size | BS | 10.99 | 8.99 | 4.99 | |

| Corporate market competitiveness | Lerner | 1.13 | 0.93 | 0.81 | |

| R&D investment | RDR | 0.054 | 0.029 | 0.003 | |

| Outcome variable | ESG | 5.99 | 4.99 | 3.99 | |

| Conditional Variables | High ESG Performance | Low–High ESG Performance | ||

|---|---|---|---|---|

| Consistency | Coverage | Consistency | Coverage | |

| ECs | 0.728 | 0.482 | 0.581 | 0.518 |

| ~ECs | 0.272 | 0.325 | 0.419 | 0.675 |

| EP | 0.733 | 0.517 | 0.508 | 0.483 |

| ~EP | 0.267 | 0.288 | 0.492 | 0.713 |

| SW | 0.982 | 0.445 | 0.910 | 0.555 |

| ~SW | 0.018 | 0.127 | 0.090 | 0.873 |

| EGM | 0.640 | 0.755 | 0.366 | 0.582 |

| ~EGM | 0.645 | 0.430 | 0.845 | 0.760 |

| ETA | 0.463 | 0.828 | 0.207 | 0.499 |

| ~ETA | 0.720 | 0.403 | 0.929 | 0.700 |

| PP | 0.849 | 0.576 | 0.631 | 0.577 |

| ~PP | 0.377 | 0.431 | 0.536 | 0.827 |

| BS | 0.614 | 0.665 | 0.524 | 0.765 |

| ~BS | 0.783 | 0.550 | 0.771 | 0.729 |

| Lerner | 0.615 | 0.549 | 0.685 | 0.823 |

| ~Lerner | 0.802 | 0.653 | 0.625 | 0.686 |

| RDR | 0.687 | 0.592 | 0.580 | 0.673 |

| ~RDR | 0.621 | 0.523 | 0.648 | 0.736 |

| Conditional Variables | Configurations | |||||

|---|---|---|---|---|---|---|

| C1 | C2 | C3 | C4 | C5 | C6 | |

| ECs | ● | ● | ● | ● | ● | ● |

| EGM | ● | ● | ● | ● | ● | |

| ETA | ● | ● | ● | ⊗ | ⊗ | |

| EP | ● | ● | ● | ● | ⊗ | ● |

| PP | ● | ● | ● | ● | ⊗ | ● |

| SW | ● | ● | ● | ● | ● | ● |

| BS | ⊗ | ⊗ | ● | ● | ||

| Lerner | ⊗ | ⊗ | ⊗ | ⊗ | ● | |

| RDR | ● | Δ | ⊗ | ● | ⊗ | |

| Consistency | 0.981 | 0.997 | 0.981 | 0.992 | 0.955 | 1.000 |

| Raw coverage | 0.242 | 0.237 | 0.228 | 0.196 | 0.060 | 0.124 |

| Unique coverage | 0.004 | 0.032 | 0.022 | 0.032 | 0.060 | 0.010 |

| Overall solution consistency | 0.960 | |||||

| Overall solution coverage | 0.439 | |||||

| Conditional Variables | Configurations | |

|---|---|---|

| C1 | C2 | |

| ECs | ● | ● |

| EGM | ● | ● |

| ETA | ● | |

| EP | ● | ● |

| PP | ● | ● |

| SW | ● | ● |

| BS | ⊗ | |

| Lerner | ⊗ | ⊗ |

| RDR | ⊗ | |

| Consistency | 0.981 | 0.981 |

| Raw coverage | 0.242 | 0.228 |

| Unique coverage | 0.076 | 0.063 |

| Overall solution consistency | 0.976 | |

| Overall solution coverage | 0.305 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dang, X.; Peng, J.; Deng, X. How to Improve the Environmental, Social and Governance Performance of Chinese Construction Enterprises Based on the Fuzzy Set Qualitative Comparative Analysis Method. Sustainability 2024, 16, 3153. https://doi.org/10.3390/su16083153

Dang X, Peng J, Deng X. How to Improve the Environmental, Social and Governance Performance of Chinese Construction Enterprises Based on the Fuzzy Set Qualitative Comparative Analysis Method. Sustainability. 2024; 16(8):3153. https://doi.org/10.3390/su16083153

Chicago/Turabian StyleDang, Xiaoxu, Jin Peng, and Xiaopeng Deng. 2024. "How to Improve the Environmental, Social and Governance Performance of Chinese Construction Enterprises Based on the Fuzzy Set Qualitative Comparative Analysis Method" Sustainability 16, no. 8: 3153. https://doi.org/10.3390/su16083153