1. Introduction

As global economies continue to develop and the industrialization process continues to advance, worldwide environmental and social concerns are becoming increasingly prominent; thereby, they are attracting widespread attention from all walks of life. As a consequence, sustainable development has become a pivotal research topic. In 2016, in order to control ecological pollution, and due to the commitment to peak carbon by 2030, the State Council proposed to construct a green financial system in China to accelerate the development of a global consensus on green finance. Meanwhile, stakeholder integration of sustainable development with corporate strategy shall serve as the direction of ESG development [

1]. Specifically, ESG performance helps to reflect the development of green finance, while its concepts persist in taking hold.

Noticeably, ESG performance acts as a third-party evaluation system that focuses on environmental protection, social responsibility, and corporate governance (CG), while organically combining and harmonizing the economic and social benefits of enterprises. At present, regulators across the globe attach vital significance to ESG policies, regulations, and guidelines. In the meantime, the ESG system has gradually evolved as a result of green finance supported by the previously well-known notion of socially responsible investment.

High ESG performance promotes corporate green innovation [

2]. High-tech industries in China, such as the new energy industry, are majorly financed by the government instead of the market at the early stage of development. Nonetheless, government support can also entail severe issues such as a shortage of funds [

3]. Owing to the limitations of the traditional financial system, the state support mechanism cannot replace the market mechanism [

4]. In general, ESG ratings extend green funds for enterprise credit assessment, while the alleviation of financial constraints makes the enterprises’ development enter a virtuous circle.

Prior to the establishment of the ESG system, corporations were unable to precisely estimate their costs and environmental benefits. Consistent with this, it was difficult for the beneficial behavior of the corporation to reflect its financial performance. Simultaneously, it was challenging for investors to ascertain the ecological protection efforts of firms and determine whether the enterprise reflected a sound corporate image; thus, it was difficult for them to engage in rational investment behaviors. Reportedly, ESG third-party rating agencies evaluated the ESG performance of companies and published ESG score data. Accordingly, enterprises that had long been committed to ecological protection, social responsibility, and CG scored comparatively high in terms of their ESG performance, which established that their corporate image was relatively better and more favorable to investors, which is conducive to promoting an improvement in CFP.

In terms of research on ESG performance and firm development, several studies have explored the relationship between ESG performance and firms’ green innovation [

5,

6,

7]. The innovation of enterprise technology is very important for the sustainable development of the enterprise, but the business condition of the enterprise is also an important factor that managers need to consider. Currently, there are relatively few studies on the impact of ESG performance on corporate financial performance, and scholars’ views on the relationship between ESG performance and financial performance are not uniform. R.M. Ammar Zahid (2023) [

8] found that ESG performance has a negative impact on firms’ financial performance. Nidhi Agarwala (2024) [

9] found a U-shaped relationship between ESG and financial performance. In addition, some scholars have researched and found only that ESG performance has a positive impact on financial performance, but the mechanism of its impact has not been studied in depth [

10]. The definition of social responsibility is not uniform. Some scholars in previous studies have argued that CSR encompasses corporate governance-level factors such as environmental practices, executives, etc. [

11]. As a result, some scholars have studied financial performance, focusing only on the social responsibility perspective in ESG performance [

12]. China is the second largest economy in the world, but the rapid economic development has also brought serious environmental problems. Some enterprises believe that investing in environmental protection equipment will increase costs, which in turn will affect corporate profits [

13]. With China’s commitment to peak carbon by 2030, this is a critical time for companies to make a green transition. ESG rating data is one of the most important indicators of corporate sustainability. Most of the research on ESG and financial performance focuses on developed countries, while China’s market is somewhat different from the West. China’s stock market is regulated by the government, and listed companies are subject to certain restrictions when issuing shares [

14], and non-state-owned enterprises are also affected to a certain extent. Therefore, this study focuses on whether ESG performance has a positive impact on corporate financial performance.

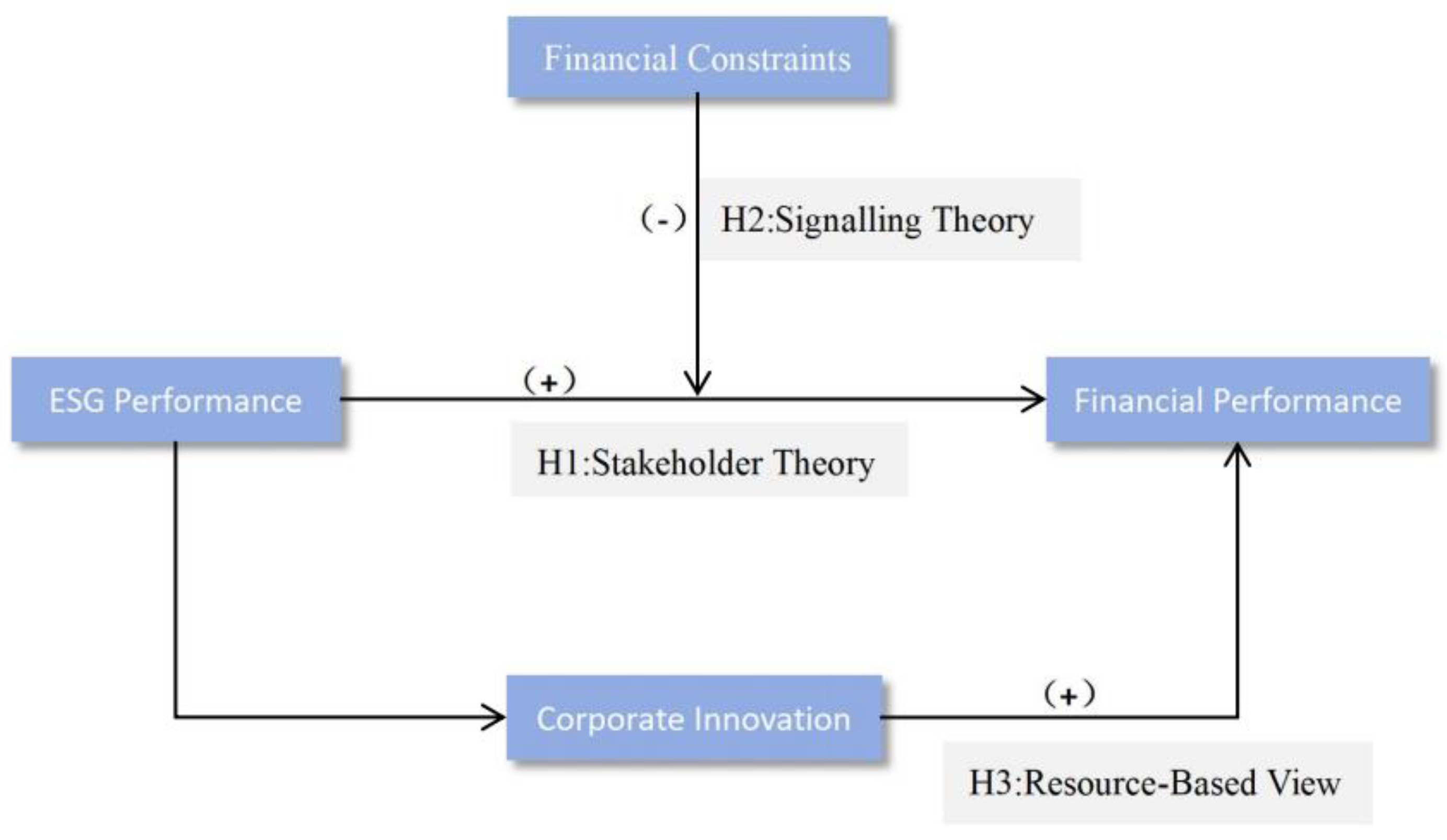

Considering that the China Securities Regulatory Commission (CSRC) issued guidelines on social responsibility reporting for listed companies in 2009, social factors have been included in the scope of China’s corporate management, and the information of ESG rating indexes has been further improved. Therefore, this study selects Chinese A-share listed companies in Shanghai and Shenzhen from 2009 to 2021 as the research sample. We not only investigate the two mechanisms through which ESG performance affects financial performance, financing constraints and financial performance, but also analyze heterogeneity in terms of firm ownership and industry characteristics. Specifically, we explore whether the impact of ESG performance on financial performance differs between non-state-owned firms and state-owned firms when firms are under financing constraints. As well, we separately investigate the impact of ESG performance on the financial performance of heavily polluting firms, such as thermal power, versus non-heavily polluting firms, to provide some insights into the green development of firms.

Exploring the effect of ESG performance on CFP is imperative for accelerating the development of a green economy [

15]. The key contributions of this research study are as follows. First, this paper explores whether CFP is influenced by ESG performance, while identifying the economic benefits of ESG performance at the micro level, thereby complementing the existing literature on financial performance. Typically, the present literature on ESG performance concentrates on well-developed markets. Moreover, past studies on ESG performance focus on the effect on investment, such as IPO price suppression [

16], green bonds [

17], and other relevant studies. However, there are relatively few studies on how ESG performance impacts corporate financial performance. This research study not only assists in filling this gap but also helps to enrich the current literature on ESG performance in developing economies. Secondly, this paper further expands on the influencing factors of CFP by emphasizing the value of corporate innovation capabilities, consequently offering a novel perspective on the influence of ESG performance on CFP. Accordingly, the mediation effect model is adopted in this study to identify and test the path of “ESG performance-firm innovation capability-financial performance”, which supplements the research on the economic impact of ESG performance and the relevant mechanisms. Hence, this enriches the present studies on the factors influencing financial performance. Thirdly, the estimation of enterprise innovation capability is expanded in this paper. Predominantly, past studies have emphasized the amount of R&D investment in forecasting enterprise innovation capability, but since the disclosure rules of R&D data in China have not been perfected at present, this research paper utilizes the number of applications for design patents, invention patents, and utility model patents in order to predict the innovation capability of firms, which will help to lead to more meaningful research topics. Fourthly, this study uncovers the potential mechanisms by which ESG performance impacts CFP in the context of both financial constraints and firms’ innovation capabilities, offering effective empirical support for comprehending the feasible path for ESG performance to drive the real economy. Fifthly, the heterogeneous effect of ESG performance is explored in terms of CFP based on the different ownership and industry characteristics of corporations. This contribution extends effective suggestions for the sustainable development of enterprises as well as innovative ideas for regulators, in order to formulate differentiated policies.

The remainder of this research paper is organized as follows:

Section 2 reviews the extant literature and postulates research hypotheses. Afterward,

Section 3 represents the research design. Subsequently,

Section 4 empirically tests the influence of ESG performance on CFP. Further, this section not only analyses the intrinsic mechanisms by which ESG performance affects financial performance but also performs the heterogeneity analysis. Finally,

Section 5 puts forward the study conclusions and policy implications.

5. Conclusions and Policy Implications

5.1. Conclusions

Using A-share listed enterprises spanning from 2009 to 2021, this study investigates the relationship between ESG performance and CFP as well as the corresponding influential mechanism. The study draws the following major conclusions.

Sound ESG performance improves corporate financial performance. Additionally, ESG performance lags by one period, and its contribution to CFP is more pronounced. This may be the result of effective ESG performance in the short term, which promptly establishes a sound reputation for the firm. Presently, information dissemination is rapid, which assists investors in making rapid decisions in a short time period, while promoting improvement in the CFP. Concurrently, there exists a lag effect, in that CFP does not significantly improve when enterprises invest substantial funds in ESG performance in the short term.

ESG performance influences CFP mainly through two different mechanisms, namely: alleviating the financing constraints of listed enterprises and improving the innovation ability of corporations. In the meantime, financing constraints have a negative moderating influence between ESG performance and CFP. Further, this corporate innovation ability plays a partial mediating effect between ESG performance and CFP. Noticeably, ESG performance transmits sound social image information to stakeholders, which assists in supporting trust and resolving principal–agent conflicts between the two parties of interest, thereby improving CFP.

Heterogeneity analysis confirms that financing constraints demonstrate a more profound inhibitory impact on financial performance improvement in NRHEs. In non-heavily polluting firms, corporate ESG performance exerts a significant effect on CFP improvement. However, ESG performance fails to enhance financial performance in heavily polluting firms.

5.2. Policy Implications

Government agencies should improve the ESG performance evaluation system. Compared with Western developed countries, China’s ESG disclosure system is not yet comprehensive, and the quality of ESG disclosure varies. Due to the imperfection of the ESG disclosure system, the ESG information reported by some enterprises may be false. We also recommend that third-party ESG rating agencies harmonize their evaluation criteria. The environmental and other problems that arise in heavily polluting companies tend to negatively affect their reputation and do not promote the improvement of their financial performance. Therefore, government agencies should make corresponding penalties for enterprises with poor ESG performance and put forward corresponding rectification suggestions, and for enterprises with good ESG performance, government agencies should make incentives and endeavor to improve the ESG performance of enterprises. Currently, our financial system is not perfect. SMEs face financing constraints due to information asymmetry problems, and may have to bear additional costs, which may also make it more difficult for SMEs to access the capital market [

43]. Therefore, we recommend improving the relevant laws.

5.3. Practical Managerial Implications

At the corporate level, the benefits of ESG investment exceed the cost of investment, and non-SOEs should augment their ESG investment. Eventually, the sound ESG performance of enterprises improves their own images. Therefore, enterprises should not only expand diversified financing channels to alleviate financing constraints but also develop trust in testing times. On the same note, enterprise managers should take improving ESG performance as the strategic goal of the enterprise, improve environmental awareness, effectively realize energy saving and emission reduction, increase investment in innovation, and improve the innovation ability of the enterprise, in order to ensure that the CFP can be significantly improved over the course of time. Similarly, strengthening CSR and information disclosure is not only needed for enterprises to integrate external and internal resources, in order to facilitate high-quality development, but is also a response to the growing demand of the public for sustainable development. Moreover, enterprises should set up a long-term goal. Corporate innovation can improve corporate reputations and images and create greater corporate value, but the process of innovation is long. Therefore, on the one hand, in the short term, a good ESG performance improves financial performance, but on the other hand, over time, a good ESG performance improves financial performance more significantly.

At the investor level, prior to making investment decisions, investors should take into account the ESG performance of firms while paying due attention to their CFP. From the perspective of sustainable development, investors present substantial external supervisors and governors who promote listed corporations to not only actively fulfill their social responsibilities but also improve CG.

5.4. Limitations and Future Research

There are some limitations to our study, but these limitations may also provide some insights for future research. Firstly, there are limitations in the selection of variables in this study. We used firm size and age to construct a model to calculate the financing constraint index, which was earlier derived by scholars based on a sample of U.S. firms under the assumption that younger firms may be more constrained, as well as that a firm’s poor track record could be assessed by selecting size and age as variables that translate into a reluctance on the part of banks to grant credit [

71]. Therefore, we believe that the selection of a sample of Chinese firms may be affected by these assumptions. In future research, we will try to measure financing constraints by constructing credit rating scores using multiple indicators. Second, there are limitations in exploring the mechanisms of influence. This study only explores the mechanism of the external factors of corporate finance and innovation in the relationship between ESG performance and financial performance. Attempts can be made in future studies to explore whether executives within a firm have an impact on ESG performance and financial performance. Finally, the research object of this study only involves China; in the future, we can try to study other emerging economies to provide more of a basis for studying the impact of ESG performance on corporate sustainability.

{kind=link}