The Impact of Environmental Management Capabilities on the Economic Value Added of Industrial Enterprises—Empirical Evidence from China

Abstract

:1. Introduction

2. Literature Review

2.1. The Meaning and Assessment of Corporate Environmental Management

2.2. Economic Value Added

2.3. The Relationship between Corporate Environmental Performance and Economic Outcomes

2.4. The Literature Gap

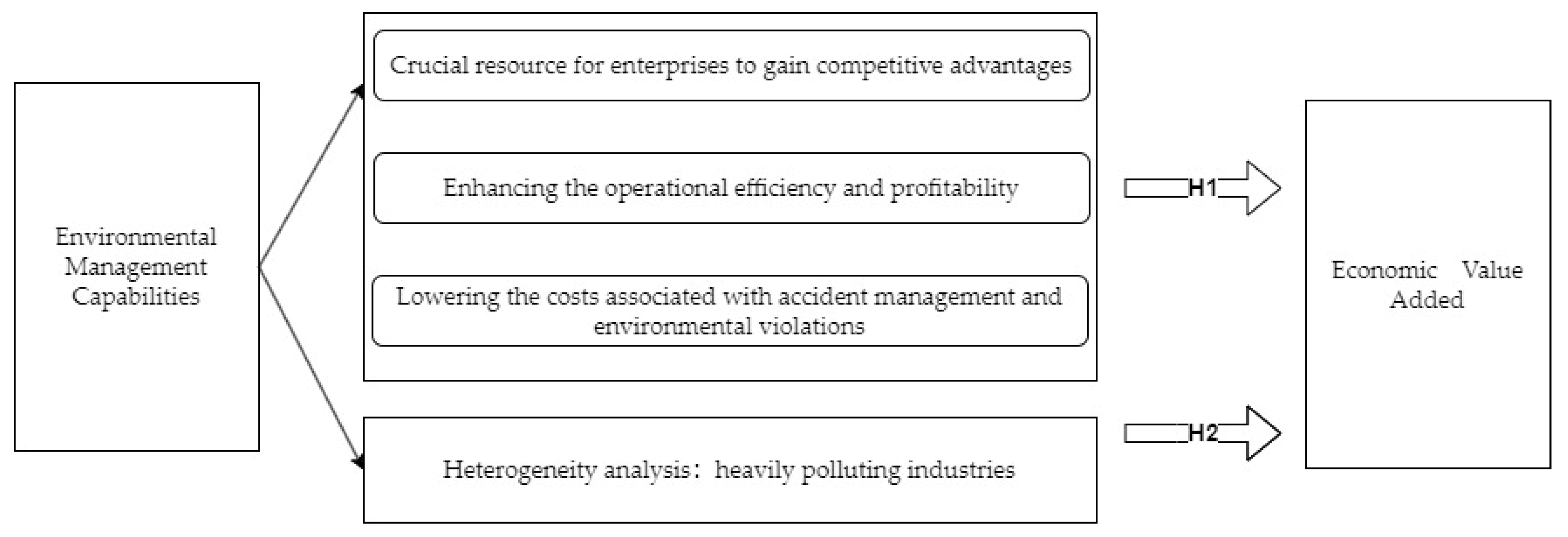

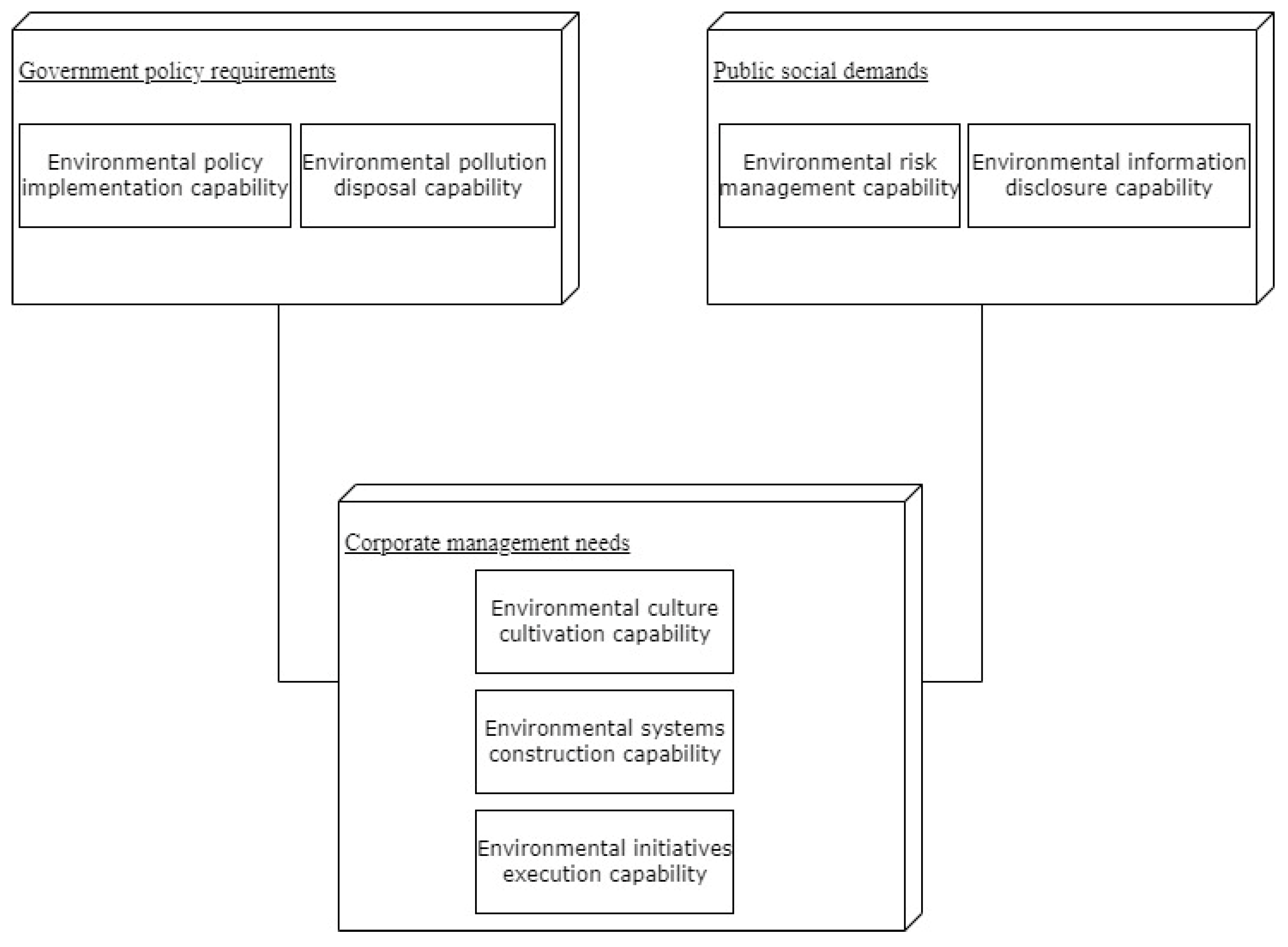

3. Theoretical Framework and Research Hypotheses

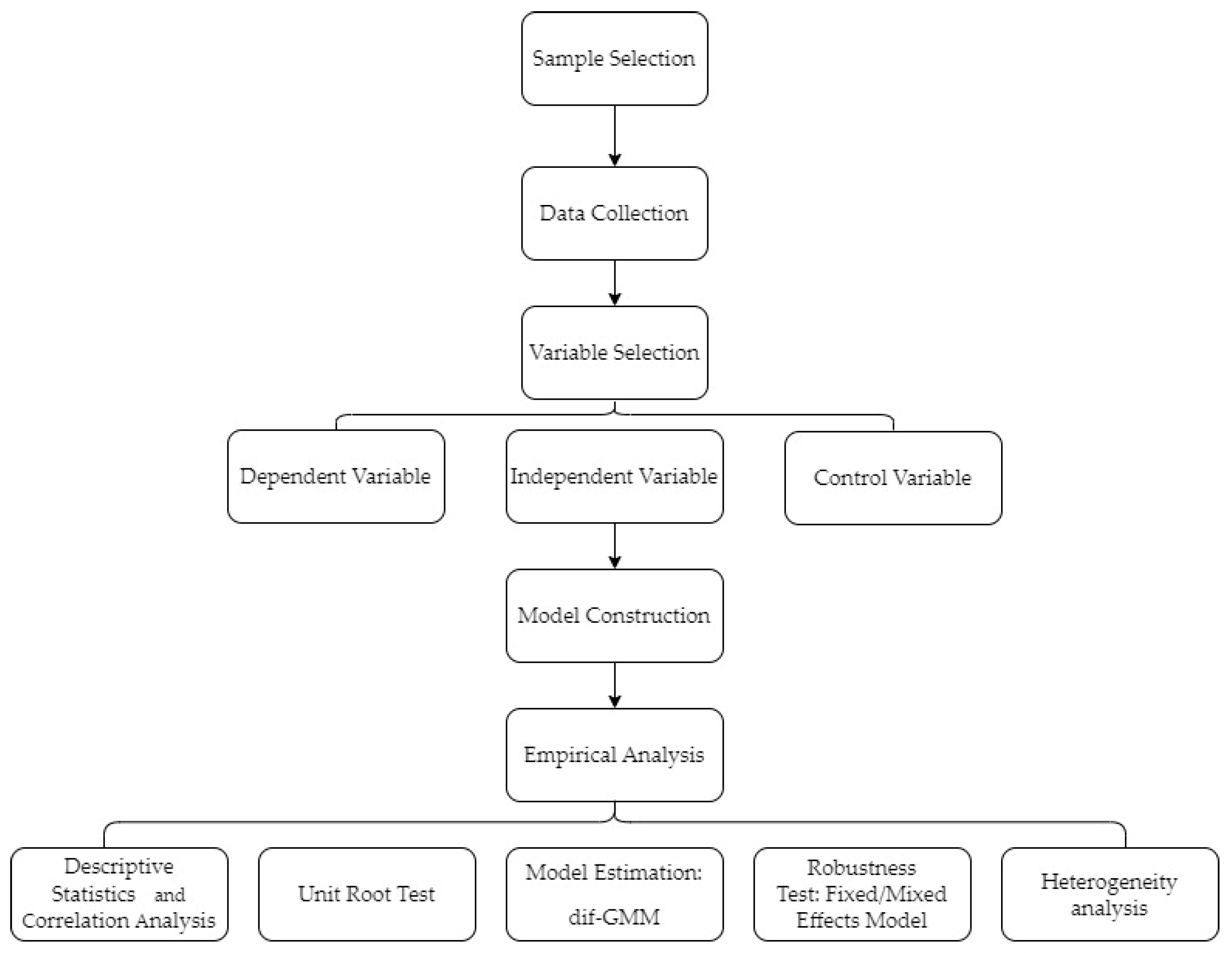

4. Methodology and Research Design

4.1. Sample Selection and Data Source

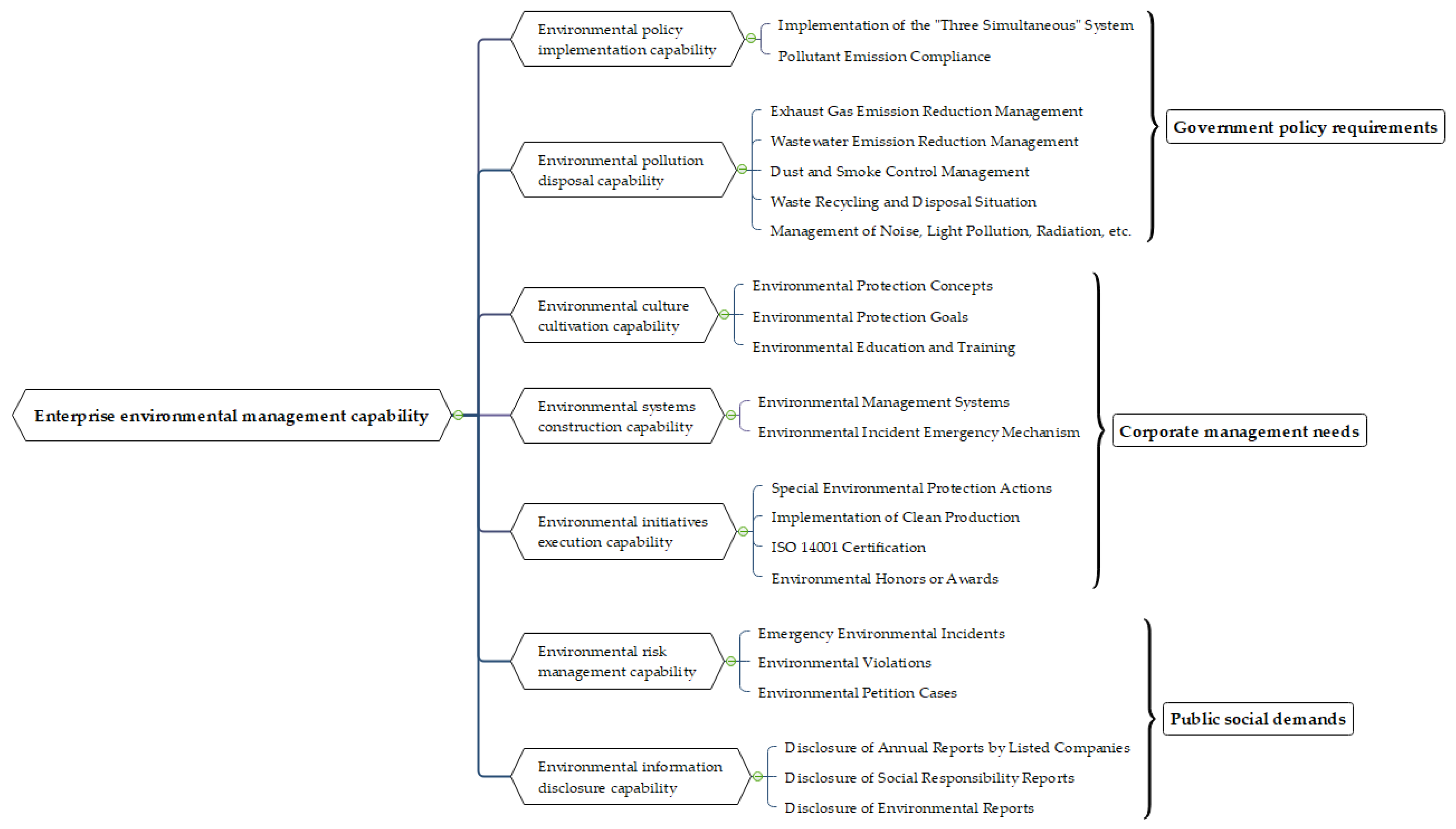

4.2. Variable Selection

4.2.1. Dependent Variable

4.2.2. Independent Variable

4.2.3. Control Variable

4.3. Model Construction

5. Empirical Testing and Result Analysis

5.1. Descriptive Statistics and Correlation Analysis

5.2. Unit Root Test

5.3. Model Estimation

5.4. Robustness Test

5.5. Heterogeneity Analysis

6. Conclusions and Recommendations

6.1. Research Conclusions

6.2. Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Bao, C.; Wang, J. Environmental Management in China Facing Ecological Civilization: Historical Mission and Academic Discourse. Chin. J. Environ. Manag. 2019, 11, 5–10. [Google Scholar]

- Gattiker, T.F.; Carter, C.R. Understanding project champions’ ability to gain intra-organizational commitment for environmental projects. J. Oper. Manag. 2010, 28, 72–85. [Google Scholar] [CrossRef]

- Su, D. How Does Global Value Chain Embedding Affect the Environmental Performance of Chinese Firms? Nankai Econ. Stud. 2020, 5, 66–86. [Google Scholar]

- Luo, E. Fiscal and tax incentives, green technology innovation and corporate environmental performance. Commun. Financ. Account. 2020, 20, 46–49. [Google Scholar]

- Deng, L. Research on Relationship among Environmental Disclosure, Environmental Performance, and Economic Performance. Master’s Thesis, Chongqing University, Chongqing, China, 2007. [Google Scholar]

- Cui, C.; Wang, L. An empirical study on the impact of environmental accounting information disclosure quality on enterprise value—A case study of mining listed companies. Res. Financ. Account. 2017, 38, 49–56. [Google Scholar]

- Hu, Q. Research on Relationship Between Environmental Performance and Financial Performance of Chinese Listed Companies. China Popul. Resour. Environ. 2012, 22, 23–32. [Google Scholar]

- Zhang, Z.; Zhang, C.; Pei, X. Research on Environmental Management System Certification and Corporate Environmental Performance. Chin. J. Manag. 2020, 17, 1043–1051. [Google Scholar]

- Lv, J.; Han, K. Impact of environmental performance on financial performance of coal enterprises under strong environmental constraints. Coal Eng. 2020, 52, 188–192. [Google Scholar]

- Hamilton, J.T. Pollution as news—Media and stock-market reactions to the toxics release inventory data. J. Environ. Econ. Manag. 1995, 28, 98–113. [Google Scholar] [CrossRef]

- Cordeiro, J.J.; Sarkis, J. Environmental proactivism and firm performance: Evidence from security analyst earnings forecasts. Bus. Strategy Environ. 1997, 6, 104–114. [Google Scholar] [CrossRef]

- Muhammad, N.; Scrimgeour, F.; Reddy, K.; Abidin, S. The relationship between environmental performance and financial performance in periods of growth and contraction: Evidence from Australian publicly listed companies. J. Clean. Prod. 2015, 102, 324–332. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Overell, M.B.; Chapple, L. Environmental Reporting and its Relation to Corporate Environmental Performance. Abacus 2011, 47, 27–60. [Google Scholar] [CrossRef]

- Filbeck, G.; Gorman, R.F. The relationship between the environmental and financial performance of public utilities. Environ. Resour. Econ. 2004, 29, 137–157. [Google Scholar] [CrossRef]

- Heras-Saizarbitoria, I.; Molina-Azorín, J.F.; Dick, G. ISO 14001 certification and financial performance: Selection-effect versus treatment-effect. J. Clean. Prod. 2011, 19, 1–12. [Google Scholar] [CrossRef]

- Cañón-de-Francia, J.; Garcés-Ayerbe, C. ISO 14001 Environmental Certification: A Sign Valued by the Market? Environ. Resour. Econ. 2009, 44, 245–262. [Google Scholar] [CrossRef]

- Qiao, Y.; Qiao, P.; Xue, H. Construction of enterprise environmental performance evaluation index system. Financ. Account. Mon. 2006, 11, 19–20. [Google Scholar]

- Sun, Z.; Wu, Q. Economic Added Value: Thinking under the high reputation. Account. Res. 2003, 24, 8–14. [Google Scholar]

- Tang, H.; Li, X.E. Traditional Accounting Index and Listed Company’s Share Price Performance—A Typical Case Study Based on Kweichow Moutai Company. J. Financ. Dev. Res. 2017, 36, 38–43. [Google Scholar]

- Hu, Y. Economic added value: The insight to identify whether an enterprise creates value or destroys value. Financ. Account. 2008, 30, 11–13. [Google Scholar]

- Jin, Y. Research on performance evaluation of software industry based on EVA. Bus. Inf. 2021, 39, 7–9. [Google Scholar]

- Gao, S.; Wang, J. Research on the effectiveness of EVA in evaluating the performance of pharmaceutical listed companies. Friends Account. 2018, 36, 26–29. [Google Scholar]

- Li, H.; Zhang, D.; Cao, X.; Zhang, X. An Empirical Research on the Validity of EVA Performance Evaluation Index-Based on 2004 Data of 454 Listed Companies in SSE. China Soft Sci. 2006, 10, 150–157. [Google Scholar]

- Qiao, H.; Zhang, S. The correlation between firm value and economic added value: An empirical study of listed companies in China. J. World Econ. 2001, 24, 42–45. [Google Scholar]

- Chi, G.; Wang, Z.; Yang, J. Has EVA Assessment Improved Firm Value?—Empirical Evidence from State-owned Listed Companies of China. Account. Res. 2013, 34, 60–66. [Google Scholar]

- Liu, F.; Li, Q. Market Competition, EVA Evaluation and Corporate Over-investment. Account. Res. 2013, 2, 54–62. [Google Scholar]

- Telle, K. “It Pays to be Green”—A Premature Conclusion? Environ. Resour. Econ. 2006, 35, 195–220. [Google Scholar] [CrossRef]

- Dowell, G.; Hart, S.; Yeung, B. Do Corporate Global Environmental Standards Create or Destroy Market Value? Manag. Sci. 2000, 46, 1059–1074. [Google Scholar] [CrossRef]

- Liu, D. Research on the Impact of Environmental Costs on Corporate Performance—Empirical Evidence from the Mining Listed Companies. Master’s Thesis, Anhui University, Hefei, China, 2016. [Google Scholar]

- Sheng, C.; Niu, X.; Guan, J. Moderating Effect of Institutional Investors on the Relationship between Environmental Management and Enterprise Performance of Forestry Enterprises. Issues For. Econ. 2021, 41, 1–7. [Google Scholar]

- Schaltegger, S.; Synnestvedt, T. The link between ‘green’ and economic success: Environmental management as the crucial trigger between environmental and economic performance. J. Environ. Manag. 2002, 65, 339–346. [Google Scholar]

- Zhang, Q.; Ma, Y. The impact of environmental management on firm economic performance: The mediating effect of green innovation and the moderating effect of environmental leadership. J. Clean. Prod. 2021, 292, 126057. [Google Scholar] [CrossRef]

- Delmas, M.; Hoffmann, V.H.; Kuss, M. Under the Tip of the Iceberg: Absorptive Capacity, Environmental Strategy, and Competitive Advantage. Bus. Soc. 2011, 50, 116–154. [Google Scholar] [CrossRef]

- Tao, P.; Zhang, Q.Y. Study on Relationship between Environmental Performance and Corporate Financial Performance-Based on Listed Companies in Heavy Polluting Industries. In Proceedings of the 2014 International Conference on Management Science & Engineering (ICMSE), Helsinki, Finland, 17–19 August 2014; pp. 1127–1134. [Google Scholar]

- Earnhart, D. The Effect of Corporate Environmental Performance on Corporate Financial Performance. Annu. Rev. Resour. Econ. 2018, 10, 425–444. [Google Scholar] [CrossRef]

- Pereira-Moliner, J.; Font, X.; Molina-Azorin, J.F.; Tarí, J.J.; Lopez-Gamero, M.D.; Pertusa-Ortega, E.M. The Holy Grail Environmental management, competitive advantage and business performance in the Spanish hotel industry. Int. J. Contemp. Hosp. Manag. 2015, 27, 714–738. [Google Scholar] [CrossRef]

- Gil, M.; Jiménez, J.B.; Lorente, J. An analysis of environmental management, organizational context and performance of Spanish hotels. Omega-Int. J. Manag. Sci. 2001, 29, 457–471. [Google Scholar]

- Chen, X.L. An empirical study of corporate environmental liability performance, industry characteristics and financial performance. In Proceedings of the 16th International Conference on Service Systems and Service Management (ICSSSM), Shenzhen, China, 13–15 July 2019. [Google Scholar]

- Lu, X.; Yin, G. Corporate Responsibility Competitiveness: Disscussing The Theory Deepening And Quantitative Evaluation. China Sustain. Trib. 2017, 16, 56–62. [Google Scholar]

- Russo, M.V.; Fouts, P.A. A resource-based perspective on corporate environmental performance and profitability. Acad. Manag. J. 1997, 40, 534–559. [Google Scholar] [CrossRef]

- Xie, J.; Nozawa, W.; Yagi, M.; Fujii, H.; Managi, S. Do environmental, social, and governance activities improve corporate financial performance? Bus. Strateg. Environ. 2019, 28, 286–300. [Google Scholar] [CrossRef]

- Ambec, S.; Lanoie, P. Does It Pay to Be Green? A Systematic Overview. Acad. Manag. Perspect. 2008, 23, 45–62. [Google Scholar]

- Bansal, P. Evolving sustainably: A longitudinal study of corporate sustainable development. Strateg. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- Peloza, J. Using corporate social responsibility as insurance for financial performance. Calif. Manag. Rev. 2006, 48, 52. [Google Scholar] [CrossRef]

- King, A.A.; Shaver, J.M. Are aliens green? Assessing foreign establishments’ environmental conduct in the United States. Strateg. Manag. J. 2001, 22, 1069–1085. [Google Scholar] [CrossRef]

- Wang, L.; Yao, Z.; Li, C. Quasi-natural experimental study on new environmental protection law on the performance of listed industrial enterprise. Ind. Econ. Res. 2021, 20, 115–128. [Google Scholar]

- Yao, S.; Pan, X. Research on the Relationship between Environmental Information Disclosure and Corporate Debt Costs—Based on the Data of A-share Listed Companies in China’s Manufacturing Industry. Friends Account. 2018, 36, 68–73. [Google Scholar]

- Li, X.; Li, M. Research on Green Investment and Corporate Environmental Governance Under the Target of Carbon Neutrality-Test of Intermediary Effect Based on Technological Innovation. Forum Sci. Technol. China 2022, 38, 118–127. [Google Scholar]

- Lu, Y.J.; Abeysekera, I. Stakeholders’ power, corporate characteristics, and social and environmental disclosure: Evidence from China. J. Clean. Prod. 2014, 64, 426–436. [Google Scholar] [CrossRef]

- Ma, G.; Zhang, T. Low-carbon policy pilot, green technology innovation and corporate environmental performance. Stat. Decis. 2024, 40, 177–182. [Google Scholar]

- Yang, G.; Du, Y.; Liu, Y. Business Performance, Media Attention and Environmental Information Disclosure. Bus. Manag. J. 2020, 42, 55–72. [Google Scholar]

- GB/T 4754-2017; Industrial Classification for National Economic Activities. Standardization Administration of China: Beijing, China, 2017.

- Deng, H.; Yin, R. Research on the Function and Institutional Construction of China’s Carbon Emissions Trading under the Vision of Carbon Neutrality. North. Leg Sci. 2022, 16, 5–15. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Industry Code | Industry Name | Industry Code | Industry Name |

|---|---|---|---|

| C39 | Computer, communications and other electronic equipment manufacturing industry | C28 | Chemical fibre manufacturing industry |

| C26 | Manufacturing of chemical raw materials and chemical products industry | C23 | Printing and recording media reproduction industry |

| C38 | Electrical machinery and equipment manufacturing industry | C41 | Other manufacturing industry |

| C27 | Pharmaceutical manufacturing industry | C43 | Metal products, machinery, and equipment repair industry |

| C35 | Special equipment manufacturing industry | C25 | Petroleum processing, coking, and nuclear fuel processing industries |

| C34 | General equipment manufacturing | C21 | Furniture manufacturing industry |

| C36 | Automobile manufacturing industry | C42 | Waste resources comprehensive utilisation industry |

| C30 | Non-metallic mineral products industry | C24 | Arts, teaching, art, sports, and entertainment goods manufacturing industry |

| C22 | Paper and paper products industry | C19 | Leather, fur, feathers, and their products and footwear industry |

| C29 | Rubber and plastic products industry | C20 | Wood processing and wood bamboo rattan palm grass products industry |

| C32 | Nonferrous metal smelting and rolling industry | B11 | Mining auxiliary activity industry |

| C33 | Metal products industry | B09 | Non-ferrous metal mining industry |

| C37 | Railway, Marine, aerospace and other transportation equipment manufacturing | B06 | Coal mining and washing industry |

| C17 | Textile industry | B07 | Oil and gas extraction industry |

| C13 | Agricultural and sideline food processing industry | B08 | Ferrous metal mining industry |

| C15 | Wine, beverage, and refined tea manufacturing | B10 | Non-metallic mining and beneficiation industry |

| C40 | Instrumentation manufacturing industry | D45 | Gas production and supply industry |

| C14 | Food manufacturing industry | D46 | Water production and supply industry |

| C31 | Ferrous metal smelting and rolling industry | D44 | Electricity and heat production and supply industry |

| C18 | Textile and garment industry |

| Variable Symbol | Meaning | Source and Calculation Method | Unit |

|---|---|---|---|

| Economic Value Added | Equation (1) | RMB | |

| Net Operating Profit After Taxes | Equation (2) | RMB | |

| Weighted Average Cost of Capital | Equation (4) | 1 | |

| Invested Capital | Equation (3) | RMB | |

| Operating Revenue | Compiled from annual reports disclosed by listed mining companies | RMB | |

| Operating Profit | RMB | ||

| Income Tax Expense | RMB | ||

| Interest Expense | RMB | ||

| Impairment Loss on Assets | RMB | ||

| Development Expenditure | RMB | ||

| Deferred Income Tax Liabilities | RMB | ||

| Deferred Income Tax Assets | RMB | ||

| Increase in Deferred Income Tax Liabilities | RMB | ||

| Increase in Deferred Income Tax Assets | RMB | ||

| Allowance for Asset Impairment | RMB | ||

| Short-term Borrowings | RMB | ||

| Total Owners’ Equity | RMB | ||

| Construction in Progress | RMB | ||

| Impairment Provision for Construction in Progress | RMB | ||

| Trading Financial Liabilities | RMB | ||

| Current Maturities of Non-current Liabilities | RMB | ||

| Long-term Borrowings | RMB | ||

| Bonds Payable | RMB | ||

| Long-term Payables | RMB | ||

| Debt Capital | RMB | ||

| Equity Capital | RMB | ||

| Cost of Bond Capital | One-year loan interest rate | RMB | |

| Cost of Equity Capital | Based on the capital asset pricing model | RMB |

| Indicator | Method of Valuation |

|---|---|

| Implementation of the “Three Simultaneous” System | Disclose the company’s implementation of the “Three Simultaneities” system. Assign 1 if applicable; otherwise, assign 0. |

| Pollutant Emission Compliance | Assign 1 if pollutant emissions meet standards; otherwise, assign 0. |

| Exhaust Gas Emission Reduction Management | 0 = No description; 1 = qualitative description; 2 = quantitative description. |

| Wastewater Emission Reduction Management | |

| Dust and Smoke Control Management | |

| Waste Recycling and Disposal Situation | |

| Management of Noise, Light Pollution, Radiation, etc. | |

| Environmental Protection Concepts | Disclose the company’s environmental concepts, environmental policies, environmental management organisational structure, development models for circular economy, and green development initiatives. Assign 1 if applicable; otherwise, assign 0. |

| Environmental Protection Goals | Disclose the company’s past environmental goal achievements and future environmental goals. Assign 1 if applicable; otherwise, assign 0. |

| Environmental Education and Training | Disclose the company’s participation in environmental education and training. Assign 1 if applicable; otherwise, assign 0. |

| Environmental Management Systems | Disclose the series of management systems established by the company, including relevant environmental management systems, frameworks, regulations, and responsibilities. Assign 1 if applicable; otherwise, assign 0. |

| Environmental Incident Emergency Mechanism | Disclose the establishment of emergency mechanisms for significant environmental incidents by the company, including emergency measures taken and the treatment of pollutants. Assign 1 if applicable; otherwise, assign 0. |

| Special Environmental Protection Actions | Disclose the company’s participation in special environmental activities and other social welfare activities related to environmental protection. Assign 1 if applicable; otherwise, assign 0. |

| Implementation of Clean Production | 0 = No Description; 1 = Qualitative Description; 2 = Quantitative Description. |

| ISO 14001 Certification | Assign 1 if certified; otherwise, assign 0. |

| Environmental Honors or Awards | Disclose the honours or awards received by the company in environmental protection. Assign 1 if applicable; otherwise, assign 0. |

| Emergency Environmental Incidents | Assign 0 if such events exist; otherwise, assign 1. |

| Environmental Violations | |

| Environmental Petition Cases | |

| Disclosure of Annual Reports by Listed Companies | Indicate whether environment-related information is disclosed. 1 = Yes; 0 = No. |

| Disclosure of Social Responsibility Reports | |

| Disclosure of Environmental Reports | Indicate whether the listed company separately discloses an environmental report. 1 = Yes; 0 = No. |

| Variable Properties | Variable Symbol | Meaning |

|---|---|---|

| Explained Variables | The economic value-added (EVA) of the listed company in the year | |

| Explanatory Variables | The environmental management capability index (EMI) of the listed company in the year. | |

| Control Variables | The debt-to-net-worth ratio of the listed company in the year | |

| The operating income growth rate of the listed company in the year. | ||

| The increase rate of main business revenue of the listed company in the year | ||

| The natural logarithm of total assets at the end of the year of the listed company in the year | ||

| The total assets growth rate of the listed company in the year |

| Variable | N | Maximum | Minimum | Mean | Std. Dev. |

|---|---|---|---|---|---|

| 31,843 | 1041.038 | −621.3602 | 2.104485 | 25.86897 | |

| 31,843 | 28.00000 | 2.000000 | 9.190748 | 4.818786 | |

| 31,843 | 178.3455 | −0.194698 | 0.438491 | 1.298748 | |

| 31,843 | 944.0996 | −1.000000 | 0.419429 | 8.881446 | |

| 31,843 | 108.3657 | −51.29776 | 0.034297 | 0.791679 | |

| 31,843 | 28.63649 | 13.07597 | 21.99464 | 1.301169 | |

| 31,843 | 45.46043 | −1.000000 | 0.223074 | 0.723578 |

| Covariance Probability | EVA | EMI | LEV | OIGR | ROA | SIZE | TAGE |

|---|---|---|---|---|---|---|---|

| EVA | 1 | ||||||

| ----- | |||||||

| EMI | 0.131312 | 1 | |||||

| 0 | ----- | ||||||

| LEV | −0.008508 | −0.000674 | 1 | ||||

| 0.1291 | 0.9044 | ----- | |||||

| OIGR | 0.002915 | −0.014424 | 0.002104 | 1 | |||

| 0.6031 | 0.0101 | 0.7074 | ----- | ||||

| ROA | 0.026263 | 0.009094 | −0.332864 | 0.002415 | 1 | ||

| 0 | 0.1048 | 0 | 0.6666 | ----- | |||

| SIZE | 0.257331 | 0.47155 | −0.006164 | 0.00665 | 0.011414 | 1 | |

| 0 | 0 | 0.2716 | 0.2355 | 0.0418 | ----- | ||

| TAGE | 0.014093 | −0.063764 | −0.036046 | 0.06994 | 0.028016 | −0.021317 | 1 |

| 0.0119 | 0 | 0 | 0 | 0 | 0.0001 | ----- |

| Variable | ||||

|---|---|---|---|---|

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| 0.0000 | 0.6547 *** | 0.0001 | 0.0000 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| 0.334829 | 0.000724 | 462.6607 | 0.0000 | |

| 0.923902 | 0.057012 | 16.2053 | 0.0000 | |

| 6.871911 | 1.098377 | 6.256423 | 0.0000 | |

| 0.324388 | 0.21052 | 1.540884 | 0.1234 | |

| 36.38219 | 3.822326 | 9.518337 | 0.0000 | |

| −1.732957 | 0.232215 | −7.46272 | 0.0000 | |

| 4.87777 | 0.746296 | 6.535972 | 0.0000 | |

| Mean dependent var | 0.174288 | S.D. dependent var | 16.52153 | |

| S.E. of regression | 37.09420 | Sum squared resid | 33,463,830 | |

| J-statistic | 385.9647 | Instrument rank | 210 | |

| Prob(J-statistic) | 0.000000 | |||

| Variable | Fixed Effects Model | Mixed Effects Model | ||

|---|---|---|---|---|

| Coefficient | p-Value | Coefficient | p-Value | |

| −39.39625 | 0.0000 | −108.8811 | 0.0000 | |

| 0.133888 | 0.0001 | 0.075535 | 0.0222 | |

| 0.060328 | 0.4704 | 0.029621 | 0.7958 | |

| 0.020629 | 0.0937 | 0.00003 | 0.9985 | |

| 0.747621 | 0.0000 | 0.75864 | 0.0001 | |

| 1.820867 | 0.0000 | 5.005069 | 0.0000 | |

| 0.701359 | 0.0000 | 0.706685 | 0.0003 | |

| Durbin-Watson stat | 1.210567 | 0.461062 | ||

| 0.645555 | 0.067277 | |||

| 0.595574 | 0.067101 | |||

| Test Order | m-Statistic | rho | SE(rho) | Prob. |

|---|---|---|---|---|

| −2.817628 | −8,069,000.016 | 2,863,756.307 | 0.0048 | |

| −0.562815 | −574,577.8552 | 1,020,899.956 | 0.5736 |

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| 0.358855 | 0.000532 | 674.0974 | 0.0000 | |

| 1.708911 | 0.040043 | 42.67639 | 0.0000 | |

| 26.05241 | 2.24139 | 11.62333 | 0.0000 | |

| 0.250234 | 0.14837 | 1.686547 | 0.0917 | |

| 95.0614 | 4.637622 | 20.49788 | ||

| −3.282878 | 0.366469 | −8.958137 | 0.0000 | |

| 8.182731 | 1.568786 | 5.215963 | 0.0000 | |

| 0.358855 | 0.000532 | 674.0974 | 0.0000 | |

| Mean dependent var | 0.364429 | S.D. dependent var | 22.42847 | |

| S.E. of regression | 51.76067 | Sum squared resid | 29,816,450 | |

| J-statistic | 282.6828 | Instrument rank | 210 | |

| Prob(J-statistic) | 0.000183 | |||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| 0.179689 | 0.003650 | 49.22358 | 0.0000 | |

| 0.246987 | 0.035154 | 7.025858 | 0.0000 | |

| 1.713456 | 0.528463 | 3.242340 | 0.0012 | |

| 0.886480 | 0.152972 | 5.795046 | 0.0000 | |

| 7.247469 | 1.667615 | 4.346008 | ||

| −0.768585 | 0.161781 | −4.750778 | 0.0000 | |

| 1.104109 | 0.310581 | 3.554983 | 0.0000 | |

| 0.179689 | 0.003650 | 49.22358 | 0.0004 | |

| Mean dependent var | 0.001774 | S.D. dependent var | 8.524356 | |

| S.E. of regression | 13.35598 | Sum squared resid | 2,294,531 | |

| J-statistic | 275.6335 | Instrument rank | 210 | |

| Prob(J-statistic) | 0.000521 | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Feng, K.; Bao, C. The Impact of Environmental Management Capabilities on the Economic Value Added of Industrial Enterprises—Empirical Evidence from China. Sustainability 2024, 16, 3356. https://doi.org/10.3390/su16083356

Feng K, Bao C. The Impact of Environmental Management Capabilities on the Economic Value Added of Industrial Enterprises—Empirical Evidence from China. Sustainability. 2024; 16(8):3356. https://doi.org/10.3390/su16083356

Chicago/Turabian StyleFeng, Ke, and Cunkuan Bao. 2024. "The Impact of Environmental Management Capabilities on the Economic Value Added of Industrial Enterprises—Empirical Evidence from China" Sustainability 16, no. 8: 3356. https://doi.org/10.3390/su16083356