A Novel Evaluation Approach for Emissions Mitigation Budgets and Planning towards 1.5 °C and Alternative Scenarios

Abstract

:1. Introduction

1.1. Background

1.2. Contribution of the Study

1.3. Structure of the Study

2. Review of Literature

2.1. Emissions Mitigation Planning and Budgeting—An Overview

2.2. Emissions Budgeting and the Use of Marginal Abatement Cost

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Study Summary | Method | Key Indicators | Climate Scenario | Ref. |

|---|---|---|---|---|---|

| World (For 41 regions, including 165 countries) | Emissions mitigation costs and their determinants were studied. The results showed that energy consumption, financial crisis, CO2 emissions rate, and GDP were great determinants and that, as the globe’s CO2 emissions continue to rise due to increasing GDP, reducing emissions is becoming more expensive | Gravity model and quadratic directional output distance function | MAC | No | [42] |

| Global | The different MAC methods used in climate change policy to evaluate alternatives and costs were comprehensively reviewed. The study classifies MAC techniques and presents an applicability path analysis for the estimation of MACs. The study suggests that complex methods may not always be better than simplified ones, and MACs could be more reliable by ranking the relative value of options. | Review | MAC | Yes | [43] |

| Global | The projected annual abatement costs of achieving national climate plans (NDCs) were estimated based on domestic action, land, land use change, and forestry (LULUCF) exclusion. The result showed conditions varying significantly across countries and achieving 2 °C being more expensive. | IMAGE integrated assessment model | MAC | Yes | [44] |

| China | A low-cost path for China to peak its carbon emissions was explored. For each region before 2030, it calculates carbon emission efficiency and marginal carbon abatement cost using the parametric directional distance function. Rapid economic expansion increases marginal abatement costs, with developed areas sustaining development patterns and central and western regions adopting emission reduction responsibilities. The work stresses that the current emissions reduction path may yield an increasing MAC in the future. | Parametric directional distance function | Carbon emission efficiency and MAC | No | [45] |

| China (441 industries) | The correlation between MAC and carbon intensity varies among industries, with energy-intensive industries showing a significant S-shaped relationship. | Functional data analysis | MAC, Carbon intensity | No | [46] |

| China and India | The costs and benefits of India’s and China’s NDCs were compared. It was found that India’s original carbon MACCs are generally higher than China’s, but revised MACCs are slightly higher. Yet, India has more significant cost-saving effects, while China faces difficulties in reducing emissions. | Computable general equilibrium model | MAC and CB | Only NDC Scenario | [47] |

| India | The study compares India’s National Development Goals (NDC) and global temperature stabilization targets, finding significant emissions disparities. Delaying abatement measures could increase mitigation costs. | Computable general equilibrium model | MAC | Yes | [48] |

| USA | The study examines the US climate policy’s costs and benefits, focusing on CO2 emissions levies and tax relief. Cost–benefit values vary from USD 150 to 1250 per household, while policy costs average less than 0.5%, demonstrating significant heterogeneity across space and income. The research shows a marginal welfare cost and cost–benefit of USD 31/tCO2 and a climate benefit of USD 27/tCO2 or less to justify a USD 25/tCO2 tax rise at 5%. | Computable general equilibrium model | MAC and CB | Yes | [49] |

| USA | The results showed that zero-carbon US electricity infrastructure would incur additional MAC, which can be reduced by employing low-carbon resources, and technologies with negative emissions show a financial benefit. | Sequential optimization model | MAC | Yes | [50] |

| EU | The paper analyzes the least-cost GHG emission abatement pathways in EU countries. A correlation was established between 2030 abatement objectives of varying ambition and a country’s probability of accomplishing a strong 2050 aim. | Constrained optimization model | Emission target, MAC | Only NDC Scenario | [51] |

| US, EU, China, and India, | According to the study’s hypothesis, nations with relatively low marginal costs of carbon emissions could end up paying an enormous cost to combat climate change. The analysis estimates the total and marginal costs of abatement for the US, EU, China, and India based on the outcomes of the 22nd Energy Modelling Forum. | EMF-22 models | Emission target, MAC | Yes | [52] |

| EU | This study explores decarbonization possibilities that combine energy systems analysis with marginal abatement cost curves (MACs). The findings indicate that MACs rely on model assumptions, with bioenergy and CCS technology being important factors. Important mitigating actions are categorized into three groups: resilient, tipping-point, and niche. | A novel analytical technique | Energy System Analysis, MAC | Only NDC Scenario | [53] |

| Developing countries | This study examines developing nation emission goals, abatement costs, and energy use in 2020. The findings showed that, by 2050, developing nations would have tougher emission objectives and higher abatement costs. | Integrated modelling framework FAIR | Emission targets, MAC, and energy consumption | Only NDC Scenario | [17] |

| World, China, EU, India, and the USA | This study examines the emissions targets from 2023 to 2050 under the climate scenarios for the World, China, EU, India, and the USA. The results show the comparative time values of different investment decisions towards the selected climate scenarios. | Developed in the Study (a simplified budgeting model approach) for evaluation of the attractiveness of emissions investment policies | MAC, NPV, CB, Avoided Emissions Cost Growth | Yes | This study |

2.3. Rationale of Emissions Budgeting (EB) Model

3. Methodology

3.1. Overview

3.2. Model Inputs, Assumption, and Computation Strategy

3.3. Selection of Relevant Policy Scenarios and Corresponding Emissions Budgets

3.4. Categorization and Monetization of Emissions

3.5. EB Model Fitness

4. Results and Discussion

4.1. Results—Global Policy Scenario

4.2. Illustrative Application of Emissions Budgeting Model to Other Cases

4.3. Results–Other Cases

5. Model Validation and Limitations

6. Conclusions, Policy Implications, and Recommendations

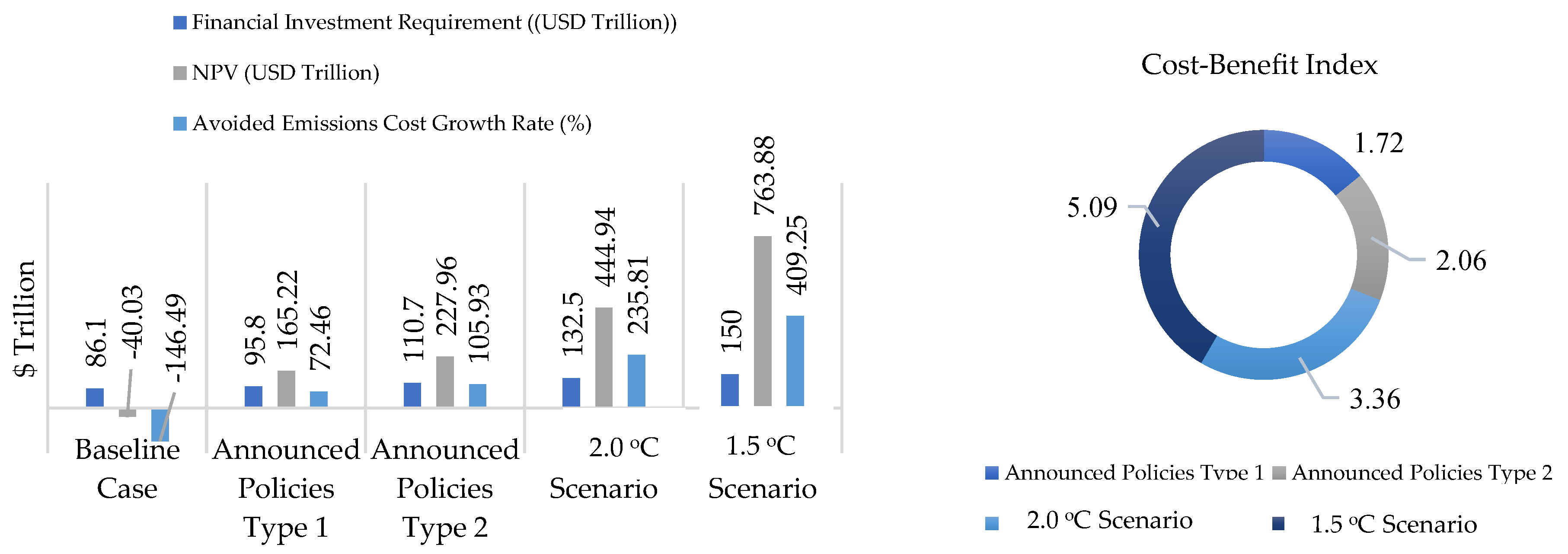

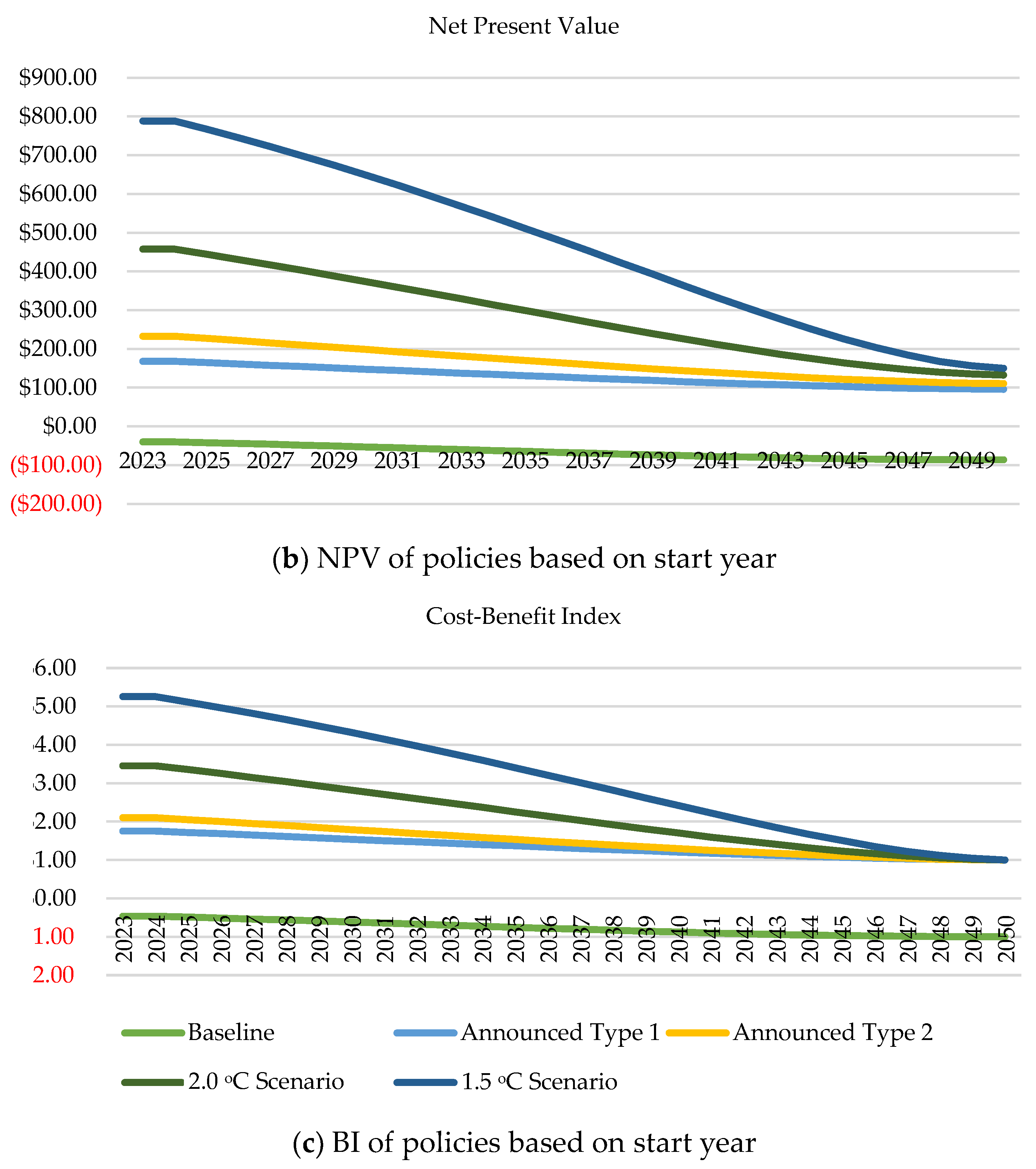

- In the global scenario simulation and at the first case of no emissions discount growth, the 1.5 °C scenario achieved a higher NPV of USD 841.22 trillion and BI of 5.6, with an initial investment requirement of USD 150 trillion, compared with the 2.0 °C scenario having an NPV of USD 458.08 and BI of 3.66, yet with the initial financial requirement of USD 132 trillion. The baseline scenario resulted in negative NPV and BI, hence showing the consequences of the world continuing with the business-as-usual approach to emissions reduction. Meanwhile, the announced policies types 1 and 2 yielded positive NPV, implying that such investments could create economic and social benefits. However, it is not adequate to keep the world within the IPCC’s desired temperature levels.

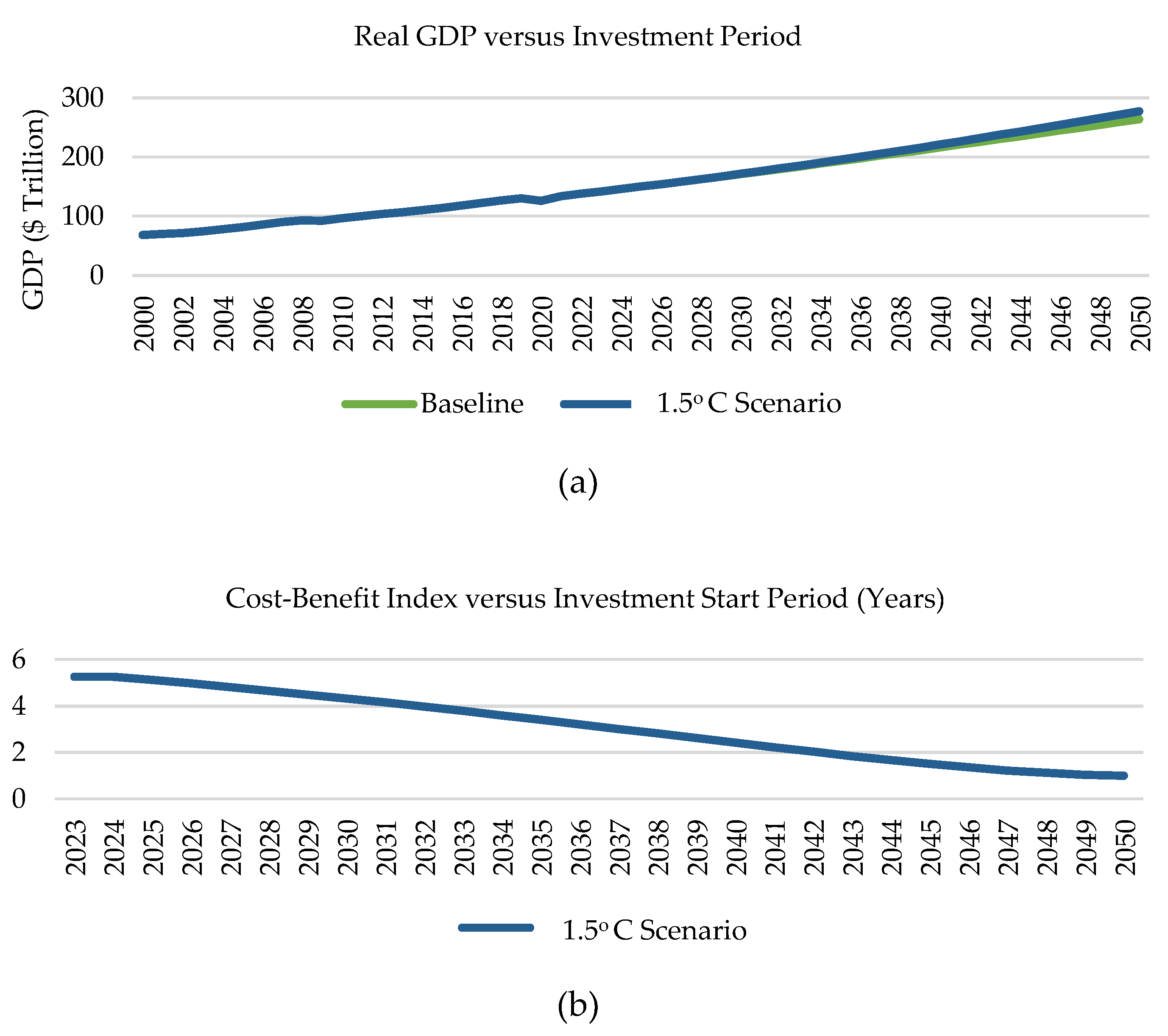

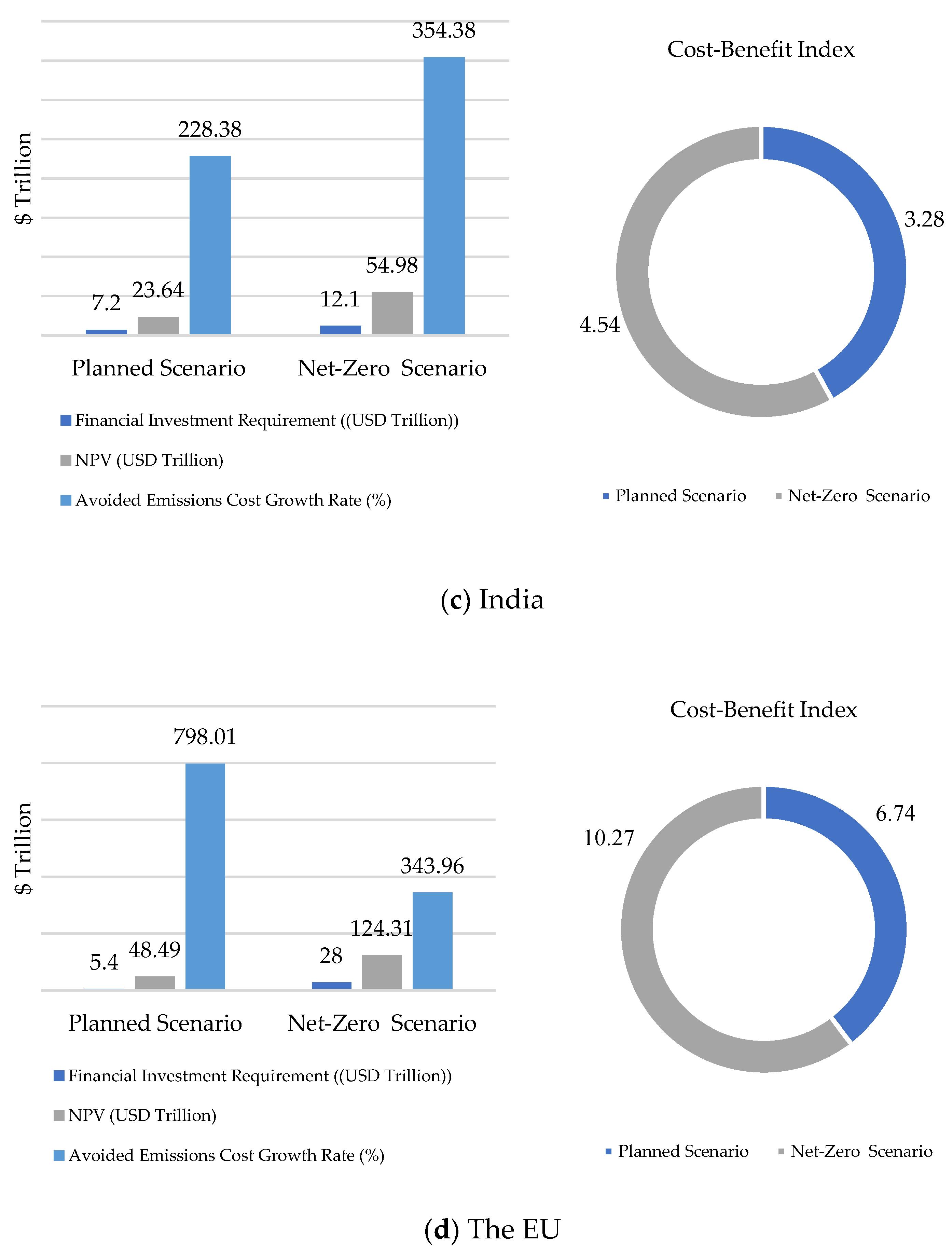

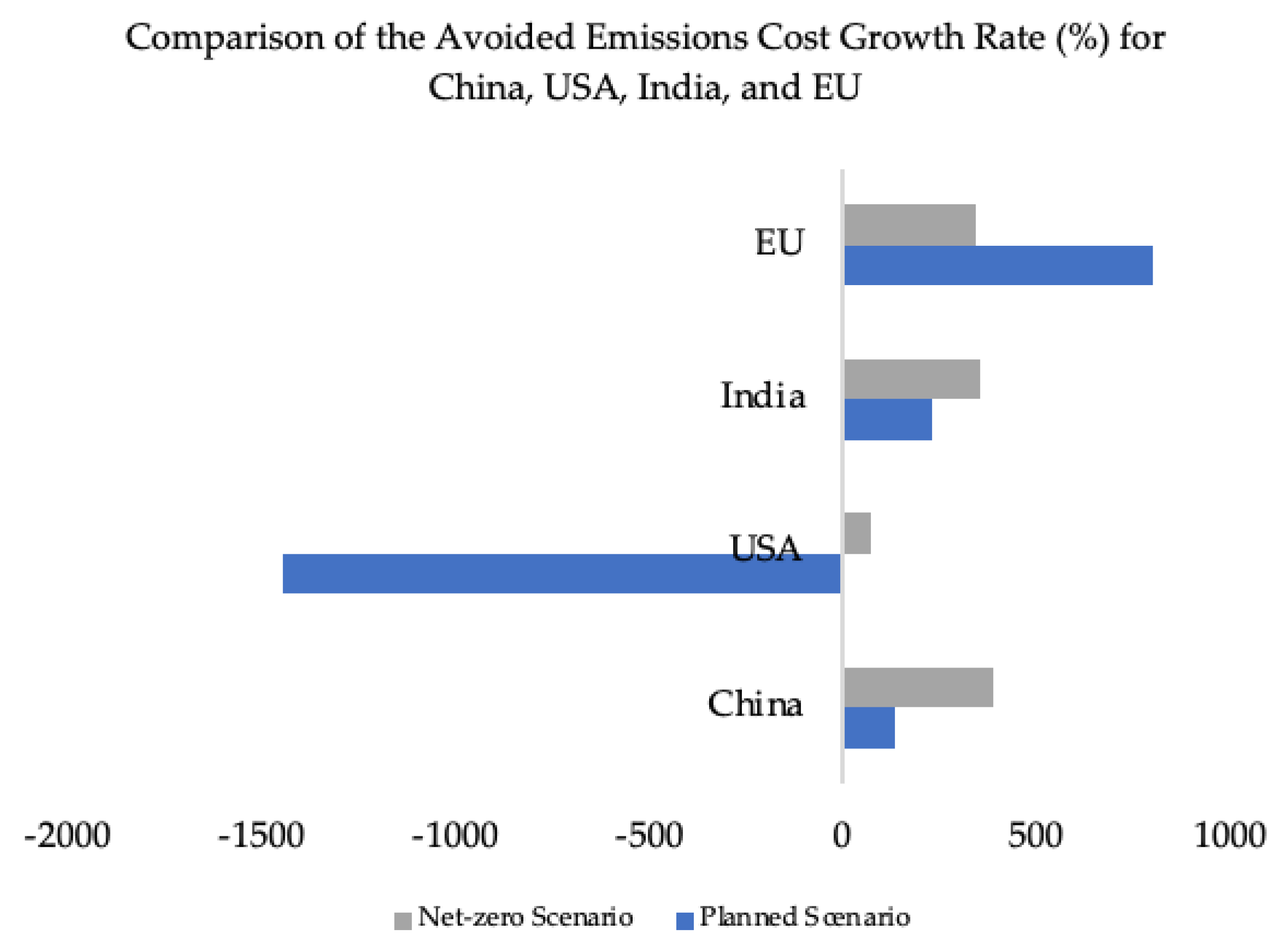

- In the illustrative case studies, according to the model’s estimation in Section 4.2 and results of the illustrative application of the model to China, the USA, India, and the EU in Section 4.3, investment options towards the global temperature rise show that, apart from the environmental advantages of the 1.5 °C and net-zero scenarios, the present economic value is also very high compared with the other scenarios. In all the planned scenarios for China, India, and the EU, the emissions reductions achieved are insufficient to meet the net-zero scenario target. For the USA, the current commitments are not only insufficient but capable of resulting in increasing emissions costs as the avoided emissions growth rate would be continually reduced. This finding provides valuable information for stakeholders and policymakers to view the investment option towards the 1.5 °C scenario as beneficial and capable of producing sustainable economic and social development.

- Globally, the findings demonstrate that the emissions cost growth rate was reduced alongside the NPV and BI regarding the policy with a higher-increasing GDP. The change can be attributed to the real-world situation of increasing capital costs for a delayed investment due to increasing high financial risks. A study by Gryglewicz S and Hartman-Glaser B. [90] supports this assertion that delaying investment for large projects incurs costs. Hence, using the model of this study, growth opportunities towards emissions reduction, such as the ones that largely affect global temperature levels, can be accessed using different risk factors, such as inflation, incentive costs, and taxes/subsidy changes.

- Integration into Existing Climate Models: The models employed in this study may be linked or integrated to other established climate models that address the environmental impact of different policy scenarios for integrated evaluation that should also involve the economic attractiveness of each policy option. For instance, the C-ROAD model and several other integrated climate assessment models hardly or do not explain the economic benefits of different emissions mitigation policies.

- Application Scalability in Other Countries, Cities, and Households: The narrative in this study using a unit cost of avoided and unavoided emissions for the world, China, USA, Europe, and India has shown that delayed emissions mitigation may likely be more expensive if actions are delayed. Therefore, this same model approach can be applied to other cities, countries, industrial facilities, and even households to show the present value of different decisions and the likely future costs of emissions.

- Insight for Establishing the Linearity of the Interconnectedness of Emissions Mitigation Pathways in Sectors and Consequences with Climate Scenarios: The exact value of the contribution from individual sectors (i.e., for instance, building, power, transport, and industry) needed for the 1.5 °C scenario continues to pose challenges in policy decisions. Hence, further studies can concentrate on establishing the direct relationship of investment attractiveness of individual sectoral contributions, technology advancements, and transitions for a sustainable low-carbon future towards the 1.5 °C and other alternative scenarios. In addition, this direct relationship at sectoral levels should also show the consequences of each sector’s avoided and unavoided emissions costs on the institutions and social welfare of the population.

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

| S/N | Steps | Highlights |

|---|---|---|

| 1 | Selection of relevant policy scenarios | Based on Table S2 |

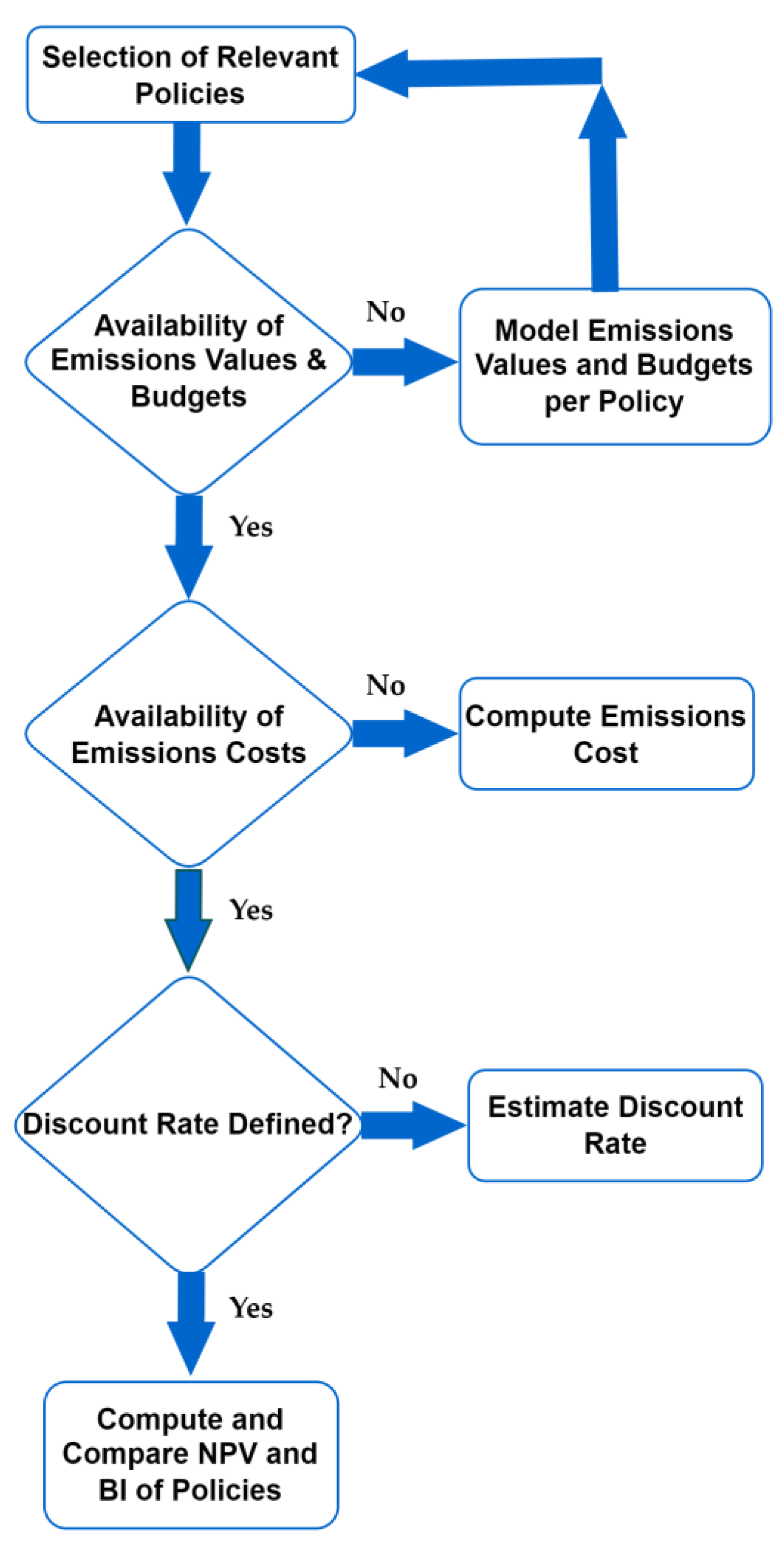

| 2 | Identification of emissions costs | Based on Equations (3) and (4) |

| 3 | Assigning monetary values to the emissions cost flows per annum. | Based on Equations (5) and (6) |

| 4 | Estimation of emissions cost based on emissions cost flows per annum from each policy scenario. | Based on Equation (11) |

| 5 | Estimation of emission cost discount rate | Based on Equations (7) and (8) |

| 6 | Calculation of the net present value of each investment based on the emissions cost. | Based on Equation (9) |

| 7 | Calculate cost profitability/benefit index and payback period. | Based on Table S2 |

| Finance Term | Study Adapted Term | Definition |

|---|---|---|

| N/A | Unit base cost of emissions removal | The cost of reducing or removing 1 ton of CO2 eq, defined by Equations (3) and (4) |

| Non-discounted cash flow | Unavoided emissions cost | Defined by Equation (6) |

| Discounted cash flow | Avoided emissions cost | Defined by Equation (7) |

| Profitability Index | Cost–benefit index | Defined by Equation (8) |

| Scenarios | Global Temperature Rise (°C) | Finance Requirement (USD Trillion) |

|---|---|---|

| Baseline Case | 3.32 | 86.1 |

| 1.5 °C Scenario (net-Zero scenario) | 1.5 | 150 |

| 2.0 °C Scenario | 2.0 | 132.5 |

| Announced Policies Type 2 (planned scenario) | 2.62 | 103 |

| Announced Policies Type 1 | 3.05 | 95.8 |

| Countries/Regions | Finance Requirement (USD Trillion) (Planned Scenario) | Finance Requirement (USD Trillion) (Net-Zero) | Reported Ideal Duration of Financial Commitment | Reference for Finance Requirement Data |

|---|---|---|---|---|

| China | 15.3 | 22 | 2021–2050 | [23] |

| USA | 3.92 | 18.2 | 2022–2050 | [25] |

| India | 7.2 | 12.1 | 2022–2050 | [26,92] |

| Europe | 5.4 | 28 | 2020–2050 | [24] |

| Rest of the World | - | 69.7 | 2020–2050 | Subtracted from the summation of China, USA, India, and Europe, and compared with the global financial requirement in the world energy investment report by IEA in [68] |

| World Total | 103 | 150 | 2023–2050 | [68] |

References

- Iyer, G.C.; Edmonds, J.A.; Fawcett, A.A.; Hultman, N.E.; Alsalam, J.; Asrar, G.R.; Calvin, K.V.; Clarke, L.E.; Creason, J.; Jeong, M.; et al. The contribution of Paris to limit global warming to 2 °C. Environ. Res. Lett. 2015, 10, 125002. [Google Scholar] [CrossRef]

- Benveniste, H.; Boucher, O.; Guivarch, C.; Le Treut, H.; Criqui, P. Impacts of nationally determined contributions on 2030 global greenhouse gas emissions: Uncertainty analysis and distribution of emissions. Environ. Res. Lett. 2018, 13, 014022. [Google Scholar] [CrossRef]

- IRENA; CPI. Global Landscape of Renewable Energy Finance 2023. 2023. Available online: https://www.irena.org/Publications/2023/Feb/Global-landscape-of-renewable-energy-finance-2023 (accessed on 10 October 2023).

- IEA. World Energy Investment 2023. 2023. Available online: https://iea.blob.core.windows.net/assets/8834d3af-af60-4df0-9643-72e2684f7221/WorldEnergyInvestment2023.pdf (accessed on 25 September 2023).

- IEA; World Bank; World Economic Forum. Financing Clean Energy Transitions in Emerging and Developing Economies-World Energy Investment 2021 Special Report. 2023. Available online: https://www.iea.org/reports/financing-clean-energy-transitions-in-emerging-and-developing-economies (accessed on 19 October 2023).

- Lee, C.-C.; Li, X.; Yu, C.-H.; Zhao, J. The contribution of climate finance toward environmental sustainability: New global evidence. Energy Econ. 2022, 111, 106072. [Google Scholar] [CrossRef]

- Zhang, L.; Saydaliev, H.B.; Ma, X. Does green finance investment and technological innovation improve renewable energy efficiency and sustainable development goals. Renew. Energy 2022, 193, 991–1000. [Google Scholar] [CrossRef]

- Zhang, D.; Mohsin, M.; Taghizadeh-Hesary, F. Does green finance counteract the climate change mitigation: Asymmetric effect of renewable energy investment and R&D. Energy Econ. 2022, 113, 106183. [Google Scholar] [CrossRef]

- Akpan, J.; Olanrewaju, O. Sustainable Energy Development: History and Recent Advances. Energies 2023, 16, 7049. [Google Scholar] [CrossRef]

- Dickau, M.; Matthews, H.D.; Tokarska, K.B. The Role of Remaining Carbon Budgets and Net-Zero CO2 Targets in Climate Mitigation Policy. Curr. Clim. Chang. Rep. 2022, 8, 91–103. [Google Scholar] [CrossRef]

- Morfeldt, J.; Larsson, J.; Andersson, D.; Johansson, D.J.A.; Rootzén, J.; Hult, C.; Karlsson, I. Emission pathways and mitigation options for achieving consumption-based climate targets in Sweden. Commun. Earth Environ. 2023, 4, 342. [Google Scholar] [CrossRef]

- The World Bank. Turn Down the Heat: Climate Extremes, Regional Impacts, and the Case for Resilience Heat the, Washington DC, June 2013. Available online: https://documents1.worldbank.org/curated/en/843011468325196264/pdf/784220WP0Engli0D0CONF0to0June019090.pdf (accessed on 28 September 2023).

- Dhar, S.; Pathak, M.; Shukla, P. Transformation of India’s transport sector under global warming of 2 °C and 1.5 °C scenario. J. Clean. Prod. 2018, 172, 417–427. [Google Scholar] [CrossRef]

- Climate Resource. MAGICCS. Climate Resource PTY LTD. 2021. Available online: https://live.magicc.org/scenarios/9742acaa-4b02-4f1a-b9bb-507066c06ff5/overview (accessed on 15 October 2023).

- Campiglio, E.; Dafermos, Y.; Monnin, P.; Ryan-Collins, J.; Schotten, G.; Tanaka, M. Climate change challenges for central banks and financial regulators. Nat. Clim. Chang. 2018, 8, 462–468. [Google Scholar] [CrossRef]

- Battiston, S.; Dafermos, Y.; Monasterolo, I. Climate risks and financial stability. J. Financ. Stab. 2021, 54, 100867. [Google Scholar] [CrossRef]

- Elzen, M.G.J.D.; Beltran, A.M.; Hof, A.F.; van Ruijven, B.; van Vliet, J. Reduction targets and abatement costs of developing countries resulting from global and developed countries’ reduction targets by 2050. Mitig. Adapt. Strat. Glob. Chang. 2013, 18, 491–512. [Google Scholar] [CrossRef]

- Maslin, M.; Parikh, P.; Chin-Yee, S. Five Major Outcomes from the Latest UN Climate Summit. The Conversation. Available online: https://theconversation.com/five-major-outcomes-from-the-latest-un-climate-summit-219655 (accessed on 13 December 2023).

- UNFCCC. Summary of Global Climate Action at COP 28. 2023. Available online: https://unfccc.int/sites/default/files/resource/Summary_GCA_COP28.pdf (accessed on 16 December 2023).

- Lahn, B. A history of the global carbon budget. Wiley Interdiscip. Rev. Clim. Chang. 2020, 11, e636. [Google Scholar] [CrossRef]

- Matthews, H.D.; Landry, J.-S.; Partanen, A.-I.; Allen, M.; Eby, M.; Forster, P.M.; Friedlingstein, P.; Zickfeld, K. Estimating Carbon Budgets for Ambitious Climate Targets. Curr. Clim. Chang. Rep. 2017, 3, 69–77. [Google Scholar] [CrossRef]

- Akpan, J.; Olanrewaju, O. Towards the 1.5 °C Climate Scenario: Global Emissions Reduction Commitment Simulation and the Way Forward. In Global Warming—A Concerning Component of Climate Change [Working Title], 1st ed.; IntechOpen: London, UK, 2023. [Google Scholar] [CrossRef]

- The World Bank Group. China-Country Climate and Development Report. Washington, October 2022. Available online: https://openknowledge.worldbank.org/server/api/core/bitstreams/35ea9337-dfcf-5d60-9806-65913459d928/content (accessed on 19 October 2023).

- McKinsey & Company. How the European Union Could Achieve Net-Zero Emissions at Net-Zero Cost. New York, December 2020. Available online: https://www.mckinsey.com/capabilities/sustainability/our-insights/how-the-european-union-could-achieve-net-zero-emissions-at-net-zero-cost (accessed on 19 October 2023).

- McKinsey & Company. Navigating America’s Net-Zero Frontier: A Guide for Business Leaders. New York, May 2022. Available online: https://www.mckinsey.com/capabilities/sustainability/our-insights/navigating-americas-net-zero-frontier-a-guide-for-business-leaders (accessed on 19 October 2023).

- Rajat, G.; Shirish, S.; Naveen, U.; Divy, M. Decarbonising India Charting a Pathway for Sustainable Growth-Updated. October 2023. Available online: https://www.mckinsey.com/~/media/mckinsey/business%20functions/sustainability/our%20insights/decarbonizing%20india%20charting%20a%20pathway%20for%20sustainable%20growth/Decarbonising-India-Charting-a-pathway-for-sustainable-growth-ES-Oct-2022.pdf (accessed on 13 October 2023).

- van Vuuren, D.P.; van Soest, H.; Riahi, K.; Clarke, L.; Krey, V.; Kriegler, E.; Rogelj, J.; Schaeffer, M.; Tavoni, M. Carbon budgets and energy transition pathways. Environ. Res. Lett. 2016, 11, 075002. [Google Scholar] [CrossRef]

- Alcaraz, O.; Balfegó, M.; Cruanyes, C.; Retamal, C.; Sureda, B.; Turon, A. Equity in the Paris Agreement Regime Are Current NDCs Built on Equity? How to Operationalize Equity in GST? STH Sustainability, Technology, and Humanitarian UPC Singular Research Group. 2022. Available online: https://www.climatewatchdata.org (accessed on 23 August 2023).

- von Stechow, C.; Minx, J.C.; Riahi, K.; Jewell, J.; McCollum, D.L.; Callaghan, M.W.; Bertram, C.; Luderer, G.; Baiocchi, G. 2 °C and SDGs: United they stand, divided they fall? Environ. Res. Lett. 2016, 11, 034022. [Google Scholar] [CrossRef]

- Liu, J.-Y.; Fujimori, S.; Masui, T. Temporal and spatial distribution of global mitigation cost: INDCs and equity. Environ. Res. Lett. 2016, 11, 114004. [Google Scholar] [CrossRef]

- Jabbari, M.; Motlagh, M.S.; Ashrafi, K.; Abdoli, G. Global carbon budget allocation based on Rawlsian Justice by means of the Sustainable Development Goals Index. Environ. Dev. Sustain. 2019, 22, 5465–5481. [Google Scholar] [CrossRef]

- Gignac, R.; Matthews, H.D. Allocating a 2 °C cumulative carbon budget to countries. Environ. Res. Lett. 2015, 10, 075004. [Google Scholar] [CrossRef]

- Kanitkar, T.; Jayaraman, T.; Souza, M.D. Carbon budgets for climate change mitigation-a GAMS-based emissions model. Curr. Sci. 2013, 104, 1200–1206. [Google Scholar]

- Berg, N.J.v.D.; van Soest, H.L.; Hof, A.F.; Elzen, M.G.J.D.; van Vuuren, D.P.; Chen, W.; Drouet, L.; Emmerling, J.; Fujimori, S.; Höhne, N.; et al. Implications of various effort-sharing approaches for national carbon budgets and emission pathways. Clim. Chang. 2020, 162, 1805–1822. [Google Scholar] [CrossRef]

- Plötz, P.; Wachsmuth, J.; Sprei, F.; Gnann, T.; Speth, D.; Neuner, F.; Link, S. Greenhouse gas emission budgets and policies for zero-Carbon road transport in Europe. Clim. Policy 2023, 23, 343–354. [Google Scholar] [CrossRef]

- Alcaraz, O.; Buenestado, P.; Escribano, B.; Sureda, B.; Turon, A.; Xercavins, J. The global carbon budget and the Paris agreement. Int. J. Clim. Chang. Strat. Manag. 2019, 11, 310–325. [Google Scholar] [CrossRef]

- Fong, W.-K.; Matsumoto, H.; Lun, Y.-F. Establishment of City Level Carbon Dioxide Emission Baseline Database and Carbon Budgets for Developing Countries with Data Constraints. J. Asian Arch. Build. Eng. 2008, 7, 403–410. [Google Scholar] [CrossRef]

- IPCC. Summary for Policymakers. In Climate Change 2023: Synthesis Report. Contribution of Working Groups I, II and III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Core Writing Team; Lee, H., Romero, J., Eds.; IPCC: Geneva, Switzerland, 2023; pp. 1–34. [Google Scholar] [CrossRef]

- Elliston, B.; Riesz, J.; MacGill, I. What cost for more renewables? The incremental cost of renewable generation—An Australian National Electricity Market case study. Renew. Energy 2016, 95, 127–139. [Google Scholar] [CrossRef]

- Wu, F.; Wang, S.; Zhou, P. Marginal abatement cost of carbon dioxide emissions: The role of abatement options. Eur. J. Oper. Res. 2023, 310, 891–901. [Google Scholar] [CrossRef]

- Morris, J.; Paltsev, S.; Reilly, J. Marginal Abatement Costs and Marginal Welfare Costs for Greenhouse Gas Emissions Reductions: Results from the EPPA Model. Environ. Model. Assess. 2012, 17, 325–336. [Google Scholar] [CrossRef]

- Liu, J.-Y.; Feng, C. Marginal abatement costs of carbon dioxide emissions and its influencing factors: A global perspective. J. Clean. Prod. 2018, 170, 1433–1450. [Google Scholar] [CrossRef]

- Huang, S.K.; Kuo, L.; Chou, K.-L. The applicability of marginal abatement cost approach: A comprehensive review. J. Clean. Prod. 2016, 127, 59–71. [Google Scholar] [CrossRef]

- Hof, A.F.; Elzen, M.G.D.; Admiraal, A.; Roelfsema, M.; Gernaat, D.E.; van Vuuren, D.P. Global and regional abatement costs of Nationally Determined Contributions (NDCs) and of enhanced action to levels well below 2 °C and 1.5 °C. Environ. Sci. Policy 2017, 71, 30–40. [Google Scholar] [CrossRef]

- Li, W.; Ma, H.; Lu, C. Research on the economic abatement pathway of carbon peaking in China based on marginal abatement costs and abatement tasks allocation. Environ. Sci. Pollut. Res. 2023, 30, 7956–7972. [Google Scholar] [CrossRef] [PubMed]

- Shi, C.; Xian, Y.; Wang, Z.; Wang, K. Marginal abatement cost curve of carbon emissions in China: A functional data analysis. Mitig. Adapt. Strat. Glob. Chang. 2023, 28, 13. [Google Scholar] [CrossRef]

- Jiang, H.-D.; Purohit, P.; Liang, Q.-M.; Dong, K.; Liu, L.-J. The cost-benefit comparisons of China’s and India’s NDCs based on carbon marginal abatement cost curves. Energy Econ. 2022, 109, 105946. [Google Scholar] [CrossRef]

- Mittal, S.; Liu, J.-Y.; Fujimori, S.; Shukla, P.R. An Assessment of Near-to-Mid-Term Economic Impacts and Energy Transitions under “2 °C” and “1.5 °C” Scenarios for India. Energies 2018, 11, 2213. [Google Scholar] [CrossRef]

- Woollacott, J. The economic costs and co-benefits of carbon taxation: A general equilibrium assessment. Clim. Chang. Econ. 2018, 9, 1840006. [Google Scholar] [CrossRef]

- Qiu, Y.; Cohen, S.; Suh, S. Decarbonization scenarios of the U.S. Electricity system and their costs. Appl. Energy 2022, 325, 119679. [Google Scholar] [CrossRef]

- Sotiriou, C.; Zachariadis, T. Optimal Timing of Greenhouse Gas Emissions Abatement in Europe. Energies 2019, 12, 1872. [Google Scholar] [CrossRef]

- Stern, D.I.; Pezzey, J.C.V.; Lambie, N.R. Where in the world is it cheapest to cut carbon emissions? Aust. J. Agric. Resour. Econ. 2012, 56, 315–331. [Google Scholar] [CrossRef]

- Yue, X.; Deane, J.; O’Gallachoir, B.; Rogan, F. Identifying decarbonisation opportunities using marginal abatement cost curves and energy system scenario ensembles. Appl. Energy 2020, 276, 115456. [Google Scholar] [CrossRef]

- Sureka, R.; Kumar, S.; Colombage, S.; Abedin, M.Z. Five decades of research on capital budgeting—A systematic review and future research agenda. Res. Int. Bus. Financ. 2022, 60, 101609. [Google Scholar] [CrossRef]

- Fleten, S.-E.; Linnerud, K.; Molnár, P.; Nygaard, M.T. Green electricity investment timing in practice: Real options or net present value? Energy 2016, 116, 498–506. [Google Scholar] [CrossRef]

- Žižlavský, O. Net Present Value Approach: Method for Economic Assessment of Innovation Projects. Procedia Soc. Behav. Sci. 2014, 156, 506–512. [Google Scholar] [CrossRef]

- Zore, Ž.; Čuček, L.; Širovnik, D.; Pintarič, Z.N.; Kravanja, Z. Maximizing the sustainability net present value of renewable energy supply networks. Chem. Eng. Res. Des. 2018, 131, 245–265. [Google Scholar] [CrossRef]

- Pintarič, Z.N.; Kravanja, Z. The importance of proper economic criteria and process modeling for single- and multi-objective optimizations. Comput. Chem. Eng. 2015, 83, 35–47. [Google Scholar] [CrossRef]

- Ryan, P.; Glenn, P.R. Capital Budgeting Practices of the Fortune 1000: How Have Things Changed? J. Bus. Manag. 2002, 8, 355–364. Available online: https://www.researchgate.net/publication/228701185 (accessed on 3 October 2023).

- Hermes, N.; Smid, P.; Yao, L. Capital budgeting practices: A comparative study of the Netherlands and China. Int. Bus. Rev. 2007, 16, 630–654. [Google Scholar] [CrossRef]

- Bennouna, K.; Meredith, G.G.; Marchant, T. Improved capital budgeting decision making: Evidence from Canada. Manag. Decis. 2010, 48, 225–247. [Google Scholar] [CrossRef]

- Mubashar, A.; Bin Tariq, Y. Capital budgeting decision-making practices: Evidence from Pakistan. J. Adv. Manag. Res. 2019, 16, 142–167. [Google Scholar] [CrossRef]

- Graham, J.R.; Harvey, C.R. The theory and practice of corporate finance: Evidence from the field. J. Financial Econ. 2001, 60, 187–243. [Google Scholar] [CrossRef]

- Brounen, D.; de Jong, A.; Koedijk, K. Corporate Finance in Europe Confronting Theory with Practice [Internet]. ERIM Report Series Research in Management. Report No.: ERS-2004-002-F&A. 2004. Available online: http://hdl.handle.net/1765/1111 (accessed on 13 December 2023).

- Özekenci, S.Y.; Düzakin, H. Capital Budgeting Methods Used in Investment Project Evaluation: The Example of Top 500 Industrial Enterprises of Turkey. Fiscaoeconomia 2023, 7, 2149–2176. [Google Scholar] [CrossRef]

- Maáji, M.M.; Barnett, C. Determinants of Capital Budgeting Practices and Risks Adjustment among Cambodian Companies. Arch. Bus. Res. 2019, 7, 171–182. [Google Scholar] [CrossRef]

- Alkaraan, F.; Northcott, D. Strategic capital investment decision-making: A role for emergent analysis tools? A study of practice in large UK manufacturing companies. Br. Account. Rev. 2006, 38, 149–173. [Google Scholar] [CrossRef]

- IRENA. World Energy Transitions Outlook 2023: 1.5 °C Pathway; Preview. Dubai, June 2023. Available online: https://www.irena.org/Publications/2023/Jun/World-Energy-Transitions-Outlook-2023 (accessed on 19 October 2023).

- OECD. Real GDP Long-Term Forecast. Available online: https://data.oecd.org/gdp/real-gdp-long-term-forecast.htm (accessed on 17 October 2023).

- Rychłowska-Musiał, E. Sustainable Investments as Real Options. In Sustainable Finance in the Green Economy ICFS 2019 Springer Proceedings in Business and Economics; Bem, A., Daszynska-Zygadlo, K., Hajdíková, T., Jáki, E., Ryszawska, B., Eds.; Springer: Cham, Switzerland, 2022; pp. 191–200. [Google Scholar] [CrossRef]

- Wiesemann, W.; Kuhn, D. The Stochastic Time-Constrained Net Present Value Problem. In Handbook on Project Management and Scheduling; Springer International Publishing: Cham, Switzerland, 2015; Volume 2, pp. 753–780. [Google Scholar] [CrossRef]

- Wang, Z.; Chen, H.; Huo, R.; Wang, B.; Zhang, B. Marginal abatement cost under the constraint of carbon emission reduction targets: An empirical analysis for different regions in China. J. Clean. Prod. 2020, 249, 119362. [Google Scholar] [CrossRef]

- Akimoto, K.; Sano, F.; Tehrani, B.S. The analyses on the economic costs for achieving the nationally determined contributions and the expected global emission pathways. Evol. Institutional Econ. Rev. 2017, 14, 193–206. [Google Scholar] [CrossRef]

- Huang, L.; Liu, L.; Dang, J.; Wei, C.; Miao, X. Efficiency or equality? The utilitarianism–egalitarianism trade-off determines carbon allocation preference. Br. J. Soc. Psychol. 2023, 1–22. [Google Scholar] [CrossRef] [PubMed]

- Schneider, S.; Paráda, E.; Sengl, D.; Baptista, J.; Oliveira, P.M. Allocation of national renewable expansion and sectoral demand reduction targets to municipal level. Front. Sustain. Cities 2023, 5, 1294361. [Google Scholar] [CrossRef]

- Büchs, M.; Cass, N.; Mullen, C.; Lucas, K.; Ivanova, D. Emissions savings from equitable energy demand reduction. Nat. Energy 2023, 8, 758–769. [Google Scholar] [CrossRef]

- Fyson, C.L.; Baur, S.; Gidden, M.; Schleussner, C.-F. Fair-share carbon dioxide removal increases major emitter responsibility. Nat. Clim. Chang. 2020, 10, 836–841. [Google Scholar] [CrossRef]

- Hales, R.; Mackey, B. Carbon Budgeting Post-COP21: The Need for an Equitable Strategy for Meeting CO2e Targets. In Pathways to a Sustainable Economy; Springer: Cham, Switzerland, 2018; pp. 209–220. [Google Scholar] [CrossRef]

- Zimm, C.; Mintz-Woo, K.; Brutschin, E.; Hanger-Kopp, S.; Hoffmann, R.; Kikstra, J.S.; Kuhn, M.; Min, J.; Muttarak, R.; Pachauri, S.; et al. Justice considerations in climate research. Nat. Clim. Chang. 2024, 14, 22–30. [Google Scholar] [CrossRef]

- Dziejarski, B.; Krzyżyńska, R.; Andersson, K. Current status of carbon capture, utilization, and storage technologies in the global economy: A survey of technical assessment. Fuel 2023, 342, 127776. [Google Scholar] [CrossRef]

- Lin, Q.; Zhang, X.; Wang, T.; Zheng, C.; Gao, X. Technical Perspective of Carbon Capture, Utilization, and Storage. Engineering 2022, 14, 27–32. [Google Scholar] [CrossRef]

- Taconet, N.; Méjean, A.; Guivarch, C. Influence of climate change impacts and mitigation costs on inequality between countries. Clim. Chang. 2020, 160, 15–34. [Google Scholar] [CrossRef]

- Tørstad, V.; Sælen, H.; Bøyum, L.S. The domestic politics of international climate commitments: Which factors explain cross-country variation in NDC ambition? Environ. Res. Lett. 2020, 15, 024021. [Google Scholar] [CrossRef]

- Olabi, A.; Abdelkareem, M.A. Renewable energy and climate change. Renew. Sustain. Energy Rev. 2022, 158, 112111. [Google Scholar] [CrossRef]

- Aghahosseini, A.; Solomon, A.; Breyer, C.; Pregger, T.; Simon, S.; Strachan, P.; Jäger-Waldau, A. Energy system transition pathways to meet the global electricity demand for ambitious climate targets and cost competitiveness. Appl. Energy 2023, 331, 120401. [Google Scholar] [CrossRef]

- Debebe, Y.; Kifetew, M.; Argaw, M. An Overview of Climate Change Mitigation, Mitigation Strategies, and Technologies to Reduce Atmospheric Greenhouse Gas Concentrations: A Review. Earth Environ. Sci. Res. Rev. 2023, 6, 1–9. [Google Scholar]

- Dioha, M.O.; Abraham-Dukuma, M.C.; Bogado, N.; Okpaleke, F.N. Supporting climate policy with effective energy modelling: A perspective on the varying technical capacity of South Africa, China, Germany and the United States. Energy Res. Soc. Sci. 2020, 69, 101759. [Google Scholar] [CrossRef]

- Noreen, B.; Jan Corfee, M.; Ogunlade, D.; Yaw, A.-O.; Lwazikazi, T.; Fatma, D.; Youba, S.; Philippe, T.J.; Lèbre, L.R.E.; Jyoti, K.P.; et al. Linkages between Climate Change and Sustainable Development. Clim. Policy 2002, 2, 129–144. [Google Scholar] [CrossRef]

- Halsnæs, K.; Shukla, P.R.; Garg, A. Sustainable development and climate change: Lessons from country studies. Clim. Policy 2008, 8, 202–219. [Google Scholar] [CrossRef]

- Gryglewicz, S.; Hartman-Glaser, B. Investment Timing and Incentive Costs. Rev. Financ. Stud. 2019, 33, 309–357. [Google Scholar] [CrossRef]

- Vecchi, V.; Hellowell, M. Securing a Better Deal From Investors in Public Infrastructure Projects: Insights from capital budgeting. Public Manag. Rev. 2013, 15, 109–129. [Google Scholar] [CrossRef]

- Birol, F.; Kant, A. India’s Clean Energy Transition is Rapidly Underway, Benefiting the Entire World. New York. January 2022. Available online: https://www.iea.org/commentaries/india-s-clean-energy-transition-is-rapidly-underway-benefiting-the-entire-world (accessed on 18 December 2023).

| S/N | Key Outcome | Summary | Implications | Resolution Level |

|---|---|---|---|---|

| 1 | The end of fossil fuels? |

|

| BAU except with a little advancement towards emissions mitigation |

| 2 | Loss and damage |

|

| BAU πexcept with little or almost no advancement to climate disaster management |

| 3 | Renewable energy and transitional fuels |

|

| BAU except with increased ambitions, yet less financial commitment |

| 4 | Oil and gas decarbonization charter |

|

| An increased commitment towards decarbonization |

| 5 | Global stocktake—1.5 °C is at risk |

|

| BAU as there is no centralized agreement on emissions mitigation cap for each country |

| S/N | Budgeting Indices (BI) | CBI > 0 | CBI = 0 CBI = 1 | CBI < 0 | CBI > 0 (With All Investment Scenarios or Options) |

|---|---|---|---|---|---|

| 1 | NPV | Accept investment | NPV = 0, no investment attractiveness | Reject investment | Rank investment options from highest to lowest BI value and choose the highest |

| 2 | PI | Accept investment | PI = 1, no investment attractiveness | Reject investment | Rank investment options from highest to lowest BI value and choose the highest |

| 3 | IRR | Accept investment | ARR = minimum required RoR, no investment attractiveness | Reject investment | Rank investment options from highest to lowest BI value and choose the highest |

| 4 | ARR | Accept investment | ARR = minimum required RoR, no investment attractiveness | Reject investment | Rank investment options from highest to lowest BI value and choose the highest |

| 5 | PBP | Accept investment | - | Reject investment | Rank investment options from highest to lowest BI value and choose the highest |

| Country/Organization | CBT Indices | Summary | Implications of Findings | Ref. |

|---|---|---|---|---|

| Fortune 1000 companies | NPV, PI, IRR, ARR, PBP, and other supplementary indices | The study compared the use of CBT for 1000 Fortune-rated companies and revealed that NPV was the most preferred tool compared with IRR, which had been often preferred in earlier years. | The findings indicate a better alignment between academic and business perspectives that had always debated the preference of one over the other. | [59] |

| China and Netherlands | NPV, IRR, ARR, and PBP | This article establishes a link between capital budgeting and economic growth. The authors claim that economic markets have made DCF approaches more useful, practical, and necessary, maximizing shareholder value. The study tested this theory using 42 Dutch and 45 Chinese enterprises. | The primary findings were that Dutch CFOs utilize the NPV approach more than Chinese ones, employ ARR more, and estimate the cost of equity less often. IRR utilization is similar in both nations. Further study and larger datasets are recommended for comprehension. | [60] |

| Canada | NPV, IRR, and Real Options | In this article, 88 large Canadian enterprises are surveyed by mail on CBT decision making. The result shows that most corporations have NPV and IRR, whereas 17% do not use discounted cash flow (DCF). | The paper describes a theory–practice gap in DCF capital budgeting decision processes, suggesting increased attention to DCF. | [61] |

| Pakistan | NPV, IRR, and Real Options | The study used 200 firms listed on Pakistan’s stock exchange to evaluate CBT use. The result showed that most firms employed DCF models favoring NPV over IRR. | The theory–practice gap was low. The study found that Pakistani firms scarcely use real option indices. | [62] |

| USA and Canada | NPV, PBP, IRR, ARR | The summary of the different studies from 392 firms in Europe showed that large-scale businesses and investments often adopt NPV more. | The use of CBT depends largely on the size of the organization | [63] |

| Europe (France, Germany, Netherlands, and the UK) | NPV, PBP, IRR, ARR | The summary of the different studies from 313 firms in Europe showed that large-scale businesses and investments often adopt NPV more. | The use of CBT depends largely on the size of the organization | [64] |

| Turkey | NPV, PBP, IRR, ARR | The study reveals that the NPV method is the most preferred capital budgeting method for Turkey’s Top 500 Industrial Enterprises when evaluating investment projects. | The results emphasize fixed capital investments’ significance across a range of industries, including employment, value-added goods, R&D, and manufacturing. | [65] |

| Cambodia | NPV, PBP, IRR, ARR | A study of CBT practices in 53 manufacturing companies in Cambodia found PB to be the most preferred method, followed by NPV, DPB, and ARR. | Companies with longer existence and higher capital investment are more likely to use NPV methods. | [66] |

| No. | Cases | Values (%) |

|---|---|---|

| 1 | Use of the initial emissions cost discounting rate used for the simulation of policies in the previous study. | P1 (2.29), P2 (2.31), P3 (2.33), P4 (2.39), and P5 (2.48) |

| 2 | Increase in the emissions cost discounting rate of case 1 by 10% | P1 (2.52), P2 (2.54), P3 (2.57), P4 (2.62), and P5 (2.73) |

| 3 | Increase in the emissions cost discounting rate of case 1 by 15% | P1 (2.64), P2 (2.66), P3 (2.68), P4 (2.74), and P5 (2.85) |

| No. | Assumptions | Description | References |

|---|---|---|---|

| 1 | Use of Global Values | The unit cost of abating emissions value of 1 Gtons CO2.eq, which represents USD 2.42 trillion, is used. | Calculation as per Equations (3) and (4) |

| 2 | Use of National Values | The GDP growth rate was used as an emissions cost discounting rate and calculated at the country/regional level. | Calculation as per Equation (12) with data from OECD in [69] |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Akpan, J.; Olanrewaju, O. A Novel Evaluation Approach for Emissions Mitigation Budgets and Planning towards 1.5 °C and Alternative Scenarios. Atmosphere 2024, 15, 227. https://doi.org/10.3390/atmos15020227

Akpan J, Olanrewaju O. A Novel Evaluation Approach for Emissions Mitigation Budgets and Planning towards 1.5 °C and Alternative Scenarios. Atmosphere. 2024; 15(2):227. https://doi.org/10.3390/atmos15020227

Chicago/Turabian StyleAkpan, Joseph, and Oludolapo Olanrewaju. 2024. "A Novel Evaluation Approach for Emissions Mitigation Budgets and Planning towards 1.5 °C and Alternative Scenarios" Atmosphere 15, no. 2: 227. https://doi.org/10.3390/atmos15020227

APA StyleAkpan, J., & Olanrewaju, O. (2024). A Novel Evaluation Approach for Emissions Mitigation Budgets and Planning towards 1.5 °C and Alternative Scenarios. Atmosphere, 15(2), 227. https://doi.org/10.3390/atmos15020227