A Work Breakdown Structure for Estimating Building Life Cycle Cost Aligned with Sustainable Assessment—Application to Functional Costs

Abstract

1. Introduction

2. State of the Art

2.1. Analysis of Existing CICS

- (1)

- Scope of use: Sets the geographic scale of use for which the classification model is created.

- (2)

- Purpose of the classification model: Initial step in the classification of objects. Identifies the interest for which the classification model has been made [25].

- (3)

- Conceptual framework: The framework on which the classification model is built. Related to higher-level information classification models.

- (4)

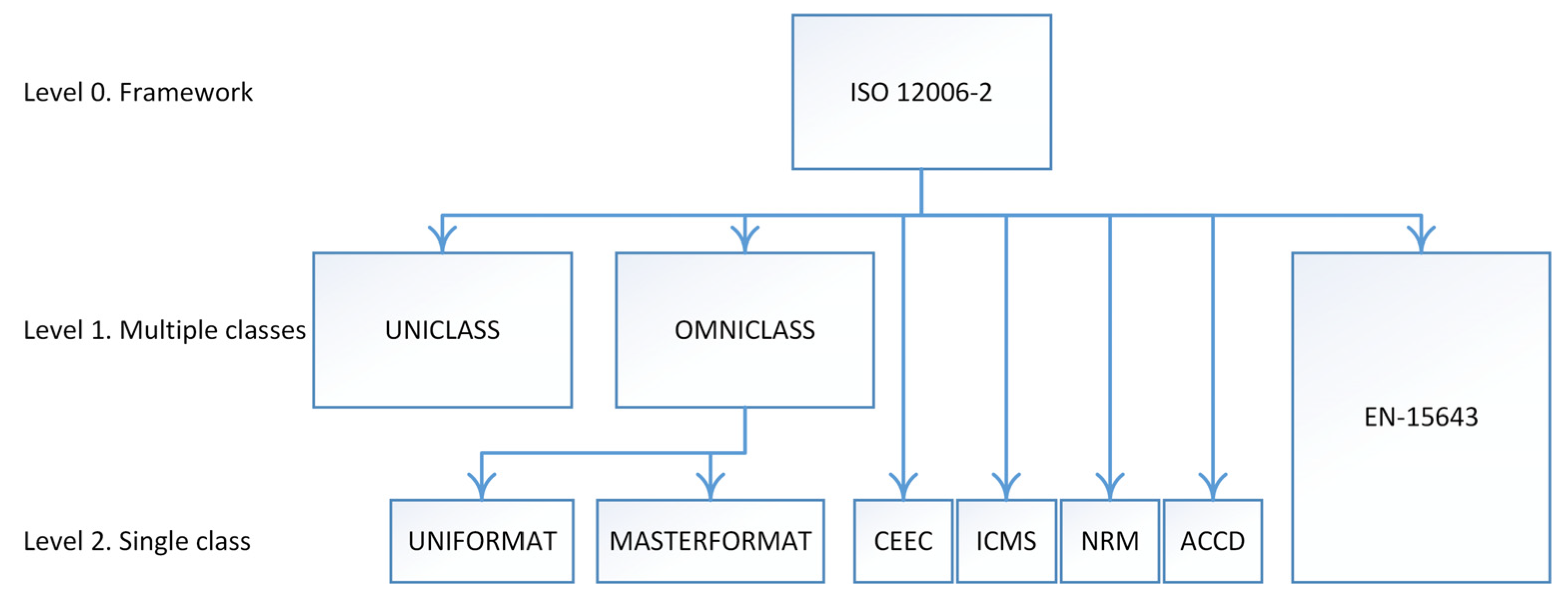

- Grouping principle: This defines whether the grouping is single or multiple, related to the vision of grouping and classifying objects [24], by adding whether the classification model is itself a conceptual framework. ISO 12006-2 [21] classification is employed: resources, processes, results, and properties.

- (5)

- Organisation: This defines the item classification organisation in order to distinguish items within a collection [25]. Specifically, these are the information levels of development.

- (6)

- Coding: This establishes the coding type, numeric or alphanumeric, of the classification model.

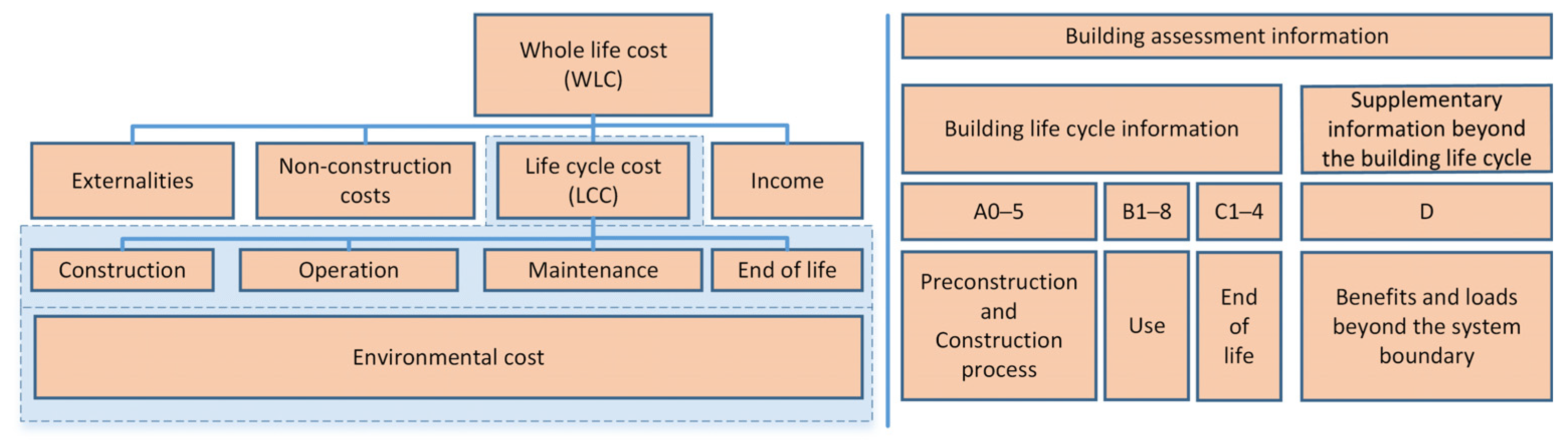

- (7)

- Life cycle: This defines the temporal boundaries of the information incorporated into the classification model according to the stages of the building’s life cycle.

- (8)

- Scope boundaries: This establishes the physical boundaries of the information incorporated into the classification model. It determines whether the information is about the endogenous and/or exogenous costs of building elements. Endogenous costs refer to the costs related directly to the construction site, while exogenous costs are those necessary for the completion of the project but take place away from the construction site.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Level 0: Conceptual framework | ||||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |

| ISO | Int | Classification per class of objects in the building (objects = resources, processes, result, or property) | General frame | Mult | 12 classification proposals grouped into resources, processes, results, and building properties | None | Yes | En. and Ex. |

| Level 1: Multiple Classes | ||||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |

| OMC | NA | Organisation and classification of all the information regarding the products of the objects in the building environment in their life cycle | ISO 12006-2 ISO 12006-3 [26] MasterFormat, Uniformat, EPIC | Mult | 15 tables representing different visions of building | Num | Yes | En. and Ex. |

| UNC | UK | Classification system for all aspects of design and construction process | ISO 12006-2, SfB, CAWS, EPIC, CESMM | Mult | 11 tables | Alpha | No | En. and Ex. |

| EN | EU | Framework for the evaluation of the sustainability of buildings and civil works | Compatible with ISO 12006-2 | Mult | Unique classification system | Alpha | Yes | En. and Ex. |

| Level 2: Single Class | ||||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |

| ICMS | Int | International Cost Classification System | NRM [27] ISO 12006-2 | U | Three classification levels, cost category, cost group, cost sub-group | Num | Yes | En. and Ex. |

| CEEC | EU | Exchange of international construction cost information | Construction Professionals | U | One level | Num | Yes | En. and Ex. |

| UNI | NA | Organisation of the information around the functional elements of the building. Mainly used for cost estimation | Construction professionals. WTO. | U | 4 hierarchical levels of development | Num | No | En. |

| MAS | NA | List for the organisation of executed units of work, requirements, products and activities. Mainly used in bids and specifications of work units. | Construction Industry Uses | U | 4 hierarchical levels | Num | No | En. |

| ACCD | S | Work units for execution projects | Spanish Public Procurement Legislation | U | Three cost tables (basics-2 levels, auxiliary-3 levels, and unit costs-4 levels) | Alpha | No | En. |

2.2. Coding of the CICSs

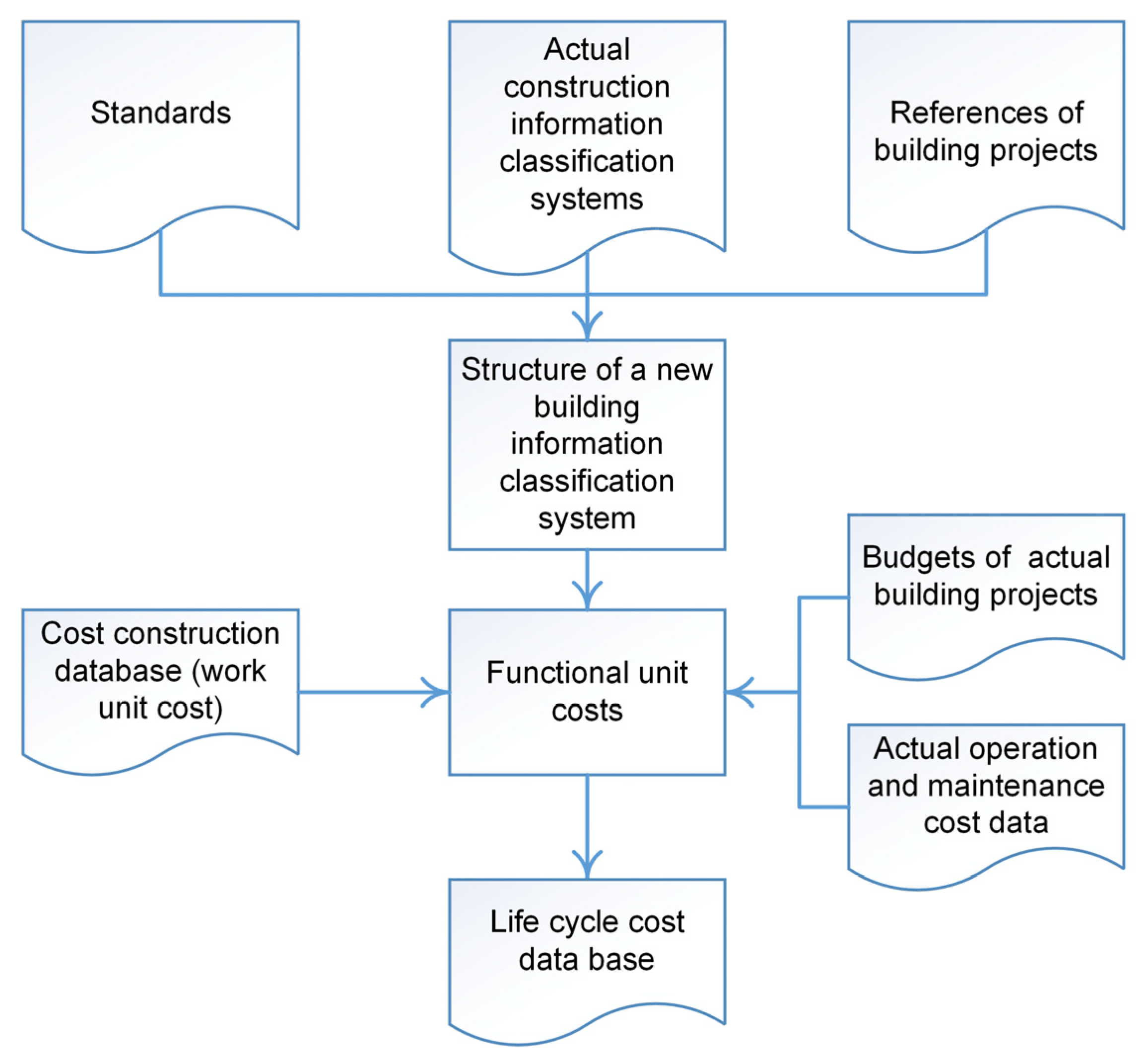

3. Methodology

3.1. The Structure of the New Classification System

3.1.1. Level 1—Life Cycle Categories

- -

- Pre-construction: costs from the completion of the preliminary studies, the acquisition of the land, and its transformation, until the moment at which the construction of the building begins. If the cycle begins with the acquisition of an existing building, only the work prior to its rehabilitation or transformation is included.

- -

- Construction: all costs incurred from the beginning of the construction of the building until it is made available for use.

- -

- Use: all costs dedicated to the use and maintenance of the building until the construction reaches its end of life.

- -

- End of life: all costs necessary for the demolition or deconstruction of the building and the treatment of the waste generated.

- -

- 01. Preliminary actions: The costs related to the purchase of the land where a new building is to be constructed or where an existing building is located. These costs also include all the necessary actions, fees, and management expenses of the developer before the start of the construction work.

- -

- 09, 19, 29, and 39. Property developer’s income, taxation, professional fees, and other expenses: All professional fees, taxes, management expenses, and general expenses of the developer.

- -

- 11. Building and outdoor spaces: All expenses related to the construction of the building related to the developer–construction contract.

- -

- 21. Building use expenses: All contracted expenses and services not included in other sub-categories of building use (e.g., security, alarm, voice, and data installations).

- -

- 22. Maintenance: All expenses for inspection, preventive and scheduled maintenance of the building so that it retains its characteristics of use (e.g., cleaning and painting).

- -

- 23. Repair: Repair costs for unscheduled breakage or defects of building elements.

- -

- 24. Replacement: The costs arising from the replacement of building elements that end their useful life before the end of the useful life of the building.

- -

- 25. Refurbishment: Costs of major building modifications. These are only applicable in anticipation of legal or technological changes. In this research, transformations are not contemplated since they are considered to significantly alter the useful life of the building and to define a new life cycle of the building.

- -

- 26. Operational energy use: Costs due to the building’s energy consumption. Income from surplus energy production is considered in sub-category 29.

- -

- 27. Operational water use: Costs for water consumption.

- -

- 28. Occupant activities. Costs related to users or occupants of the building.

- -

- 31. Demolition–deconstruction: Incorporates the costs of demolishing the building.

- -

- 34. Waste management or landfill: Considers the costs of waste transport and management of any treatment, such as reuse, recycling, and landfill deposit. Income received from selling waste is considered a negative cost, as in ACCD [36].

3.1.2. Level 2—Functional Groups

3.1.3. Level 3—Building Typologies

3.2. Costs of Functional Spaces

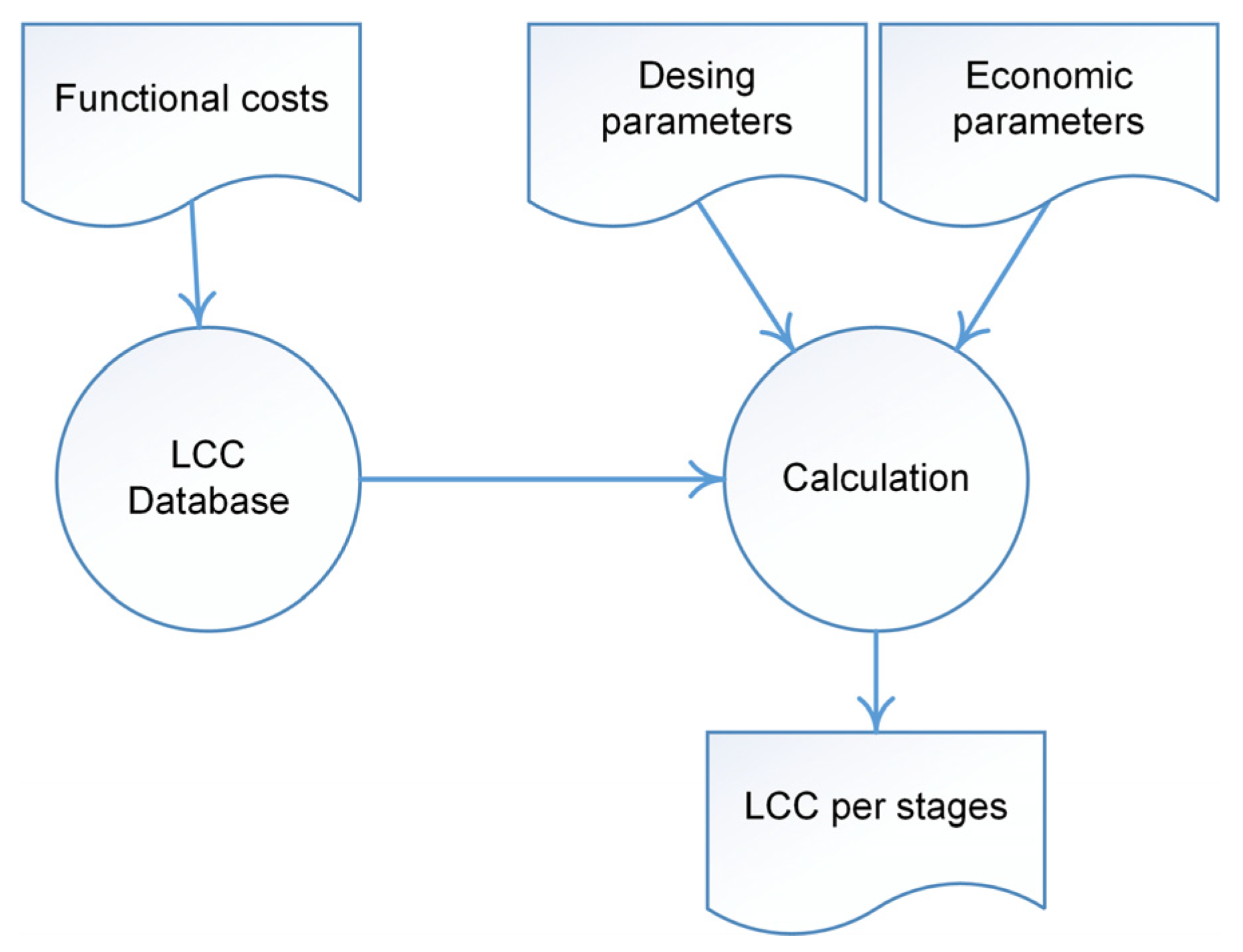

3.3. Case Study

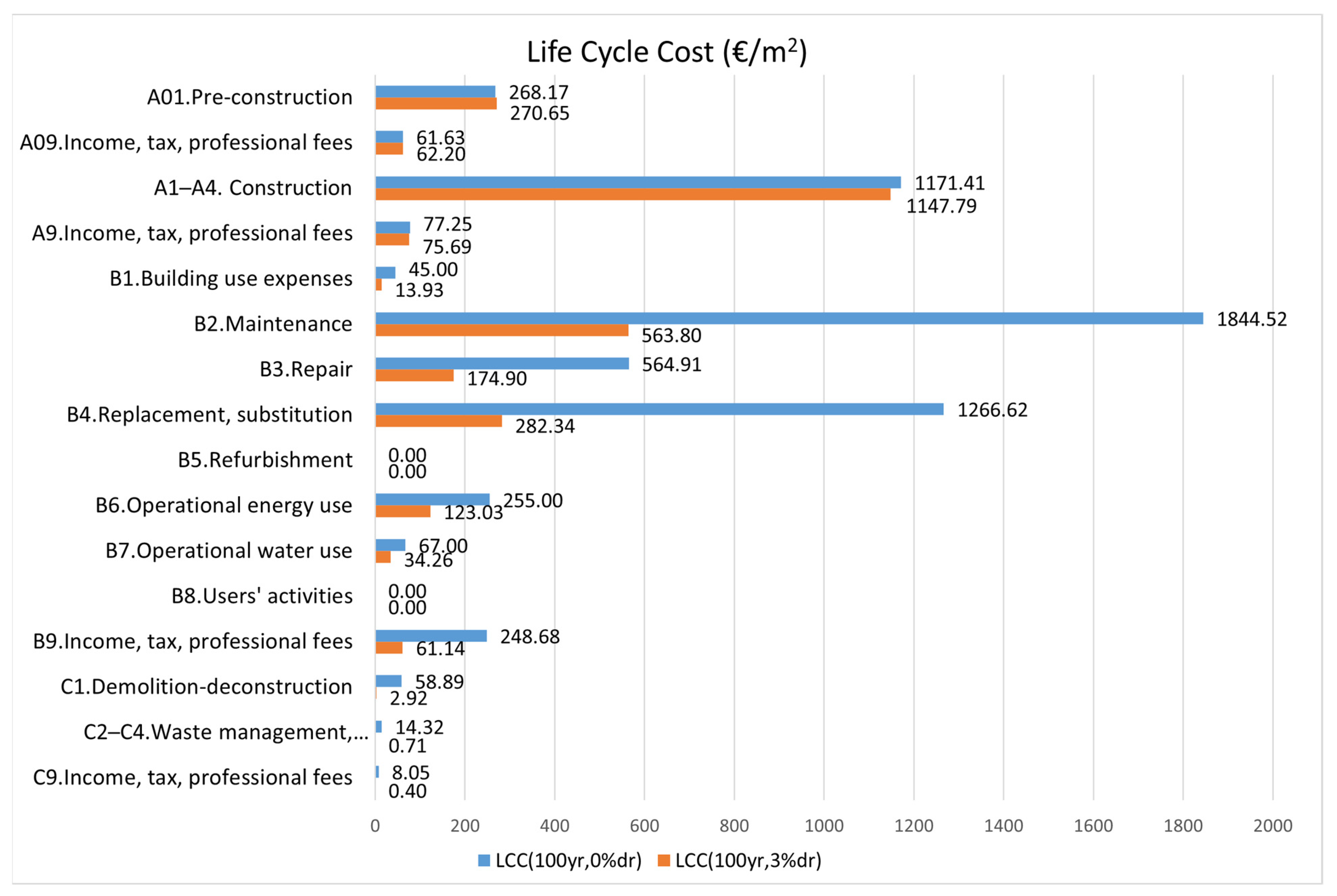

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

| Classification | Boundaries | |

|---|---|---|

| 1 | Commercial, offices, and parking | Buildings intended for commercial use, offices, and parking |

| 11 | Bureaux | Buildings with the purpose of providing professional, management or administrative services |

| 111 | Bank | Buildings for the purpose of providing banking services |

| 112 | Administrative | Buildings for the purpose of providing professional or administrative services |

| 113 | Institutional | Institution Management Building |

| 119 | Others | Office buildings not previously contemplated |

| 12 | Commercial | Buildings intended for the sale of products or services |

| 121 | Commercial premises | Buildings intended for the sale of products or services located on the ground floor |

| 122 | Shopping centre | Buildings intended for a group of shops or that are a single shop on several floors |

| 129 | Others | Commercial buildings not previously contemplated |

| 13 | Parking | Buildings or spaces intended for vehicle parking |

| 131 | Underground parking | Below-ground parking building |

| 132 | High-rise parking | Building for parking above ground |

| 139 | Others | Other types of parking buildings |

| 19 | Others | Commercial buildings or offices not included above |

| 199 | Others | Other buildings |

| 2 | Sports facilities | Buildings intended for sport activities |

| 21 | Golf courses | Ground area and buildings intended for golf |

| 211 | Golf course | Ground used for golf |

| 219 | Others | Others |

| 22 | Tracks | Ground area and buildings intended for outdoor sports on tracks |

| 221 | Arid | Tracks of arid material |

| 222 | Lawn | Natural grass courts |

| 223 | Monolayer | Single-layer rigid tracks |

| 224 | Multilayer | Multi-layered tracks |

| 225 | Special | Natural grass courts |

| 229 | Others | Other Clues |

| 23 | Stadiums and grandstands | Buildings intended to house the public for sporting events |

| 231 | Stadiums | Large enclosure with grandstands for sports activities |

| 232 | Covered grandstands | Covered area to accommodate the public |

| 233 | Outdoor grandstands | Uncovered enclosure to accommodate the public |

| 239 | Others | Others |

| 24 | Pools | Buildings intended for water sports developed in swimming pools |

| 241 | Indoors | Indoor swimming pool area |

| 242 | Outdoors | Outdoor swimming pool enclosure |

| 249 | Others | Others |

| 25 | Sports hall | Buildings intended for the exercise of various indoor sports |

| 251 | Sports hall | Buildings intended for the exercise of various indoor sports |

| 259 | Others | Others |

| 26 | Gymnasium | Buildings where gymnastics is practiced |

| 261 | Gymnasium | Buildings where gymnastics is practiced |

| 269 | Others | Others |

| 29 | Others | Sports buildings not described above |

| 299 | Others | Others |

| 3 | Hospitality industry | Buildings intended for hotel and restaurant use |

| 31 | Lodging | Buildings intended for the accommodation of people |

| 311 | Tourist apartments | Residential space or building dedicated to hospitality in an urban environment |

| 312 | Bed and Breakfasts | Residential space or building dedicated to hospitality in a rural environment |

| 313 | 5-star hotels | 5-star hotel category |

| 314 | 4-star hotels | 4-star hotel category |

| 315 | Other hotels, and hostels | Other categories of hotels or hostels |

| 319 | Others | Others |

| 32 | Catering | Spaces or buildings intended for the consumption of beverages and food |

| 321 | Bars | Drinks service taken while standing |

| 322 | Cafes | Food and beverage service without kitchen |

| 323 | Restaurants | Meal service with tables and kitchen |

| 329 | Others | Others |

| 39 | Others | Hospitality spaces or buildings not mentioned above |

| 399 | Others | Others |

| 4 | Warehouses | Large-capacity buildings intended for manufacturing, storage, agricultural production, or commerce |

| 41 | Open | Warehouse with an open façade |

| 411 | Agricultural | Warehouse for agricultural use |

| 419 | Others | Warehouse not previously described |

| 42 | Closed | Warehouse with all façades closed |

| 421 | Agricultural | Warehouse for agricultural use |

| 422 | Industrial | Warehouse for industrial use |

| 423 | Commercial | Warehouse for commercial use |

| 424 | Warehouse | Warehouse for storage |

| 425 | Logistics | Warehouse for logistics storage |

| 429 | Others | Others |

| 49 | Others | Warehouse not previously described |

| 499 | Others | Others |

| 5 | Leisure | Buildings intended for both indoor and outdoor leisure |

| 51 | Covered | Buildings intended for indoor leisure |

| 511 | Social club | Meeting Spaces |

| 512 | Discotheques | Rooms dedicated to nightlife |

| 513 | Gaming floors and casinos | Spaces intended for gambling |

| 514 | Theatres and cinemas | Exhibition space for theatrical or cinematographic works |

| 515 | Palais des Congrès | Building for holding congresses and exhibitions |

| 519 | Others | Other leisure spaces not identified above |

| 52 | Open air | Outdoor spaces or buildings |

| 521 | Auditorium | A space dedicated to the gathering and representation of artistic works in the open air |

| 522 | Bullring | Space dedicated to the practice of bullfighting |

| 529 | Others | Others |

| 59 | Others | Other typologies not described above |

| 599 | Others | Others |

| 6 | Teaching and cultural | Buildings designed to house educational and cultural spaces |

| 61 | Teaching buildings | Building intended for pre-university teaching activity |

| 611 | Nursery schools | Space dedicated to teaching between 0- and 2-year-olds |

| 612 | Infants and primary | Building dedicated to teaching between 3- and 12-year-olds |

| 613 | Secondary school | Building dedicated to teaching between 13- and 17-year-olds |

| 614 | Vocational training cycles | Building dedicated to professional education |

| 619 | Others | Others |

| 62 | University | Building intended for university teaching activity |

| 621 | Lecture Hall | Building intended for university face-to-face teaching |

| 622 | Faculty or School | A building intended for the university teaching of certain subjects |

| 623 | Research Centre | Building for research in the university environment |

| 629 | Others | Others |

| 63 | Cultural | Building for cultural activities not idle |

| 631 | Libraries | Building for archiving, classifying, and consulting bibliographic material |

| 632 | Municipal art centres | Building intended for cultural uses |

| 633 | Museums | Exhibition space for artistic objects |

| 639 | Others | Various cultural buildings |

| 64 | Religious | Building or space intended for religious worship |

| 641 | Religious | Building for worship and religious gatherings |

| 649 | Others | Others religious buildings |

| 69 | Others | Educational, cultural, and institutional buildings not included above |

| 699 | Others | Others |

| 7 | Residential | Buildings intended for residential use |

| 71 | Residential block | High-rise multi-family residential buildings |

| 711 | Isolated | High-rise dwellings without party walls in common with another building |

| 712 | Attached | High-rise dwellings with party walls in common with another building |

| 719 | Others | Others |

| 72 | Single-Family homes | Single-family residential buildings |

| 721 | Isolated | Single-family homes without party walls in common with another building |

| 722 | Attached | Single-family homes with party walls in common with another building |

| 729 | Others | Others |

| 79 | Others | Other type of residential building |

| 799 | Others | Others |

| 8 | Health and welfare | Buildings intended for health or welfare use |

| 81 | Clinic and health centres | Buildings or spaces dedicated to primary care or family medicine |

| 811 | Consulting room | Spaces for consultations and patient care |

| 812 | Health Centre | Building for outpatient consultations and treatment |

| 819 | Others | Miscellaneous primary care |

| 82 | Hospitals | Building for the diagnosis, treatment, and accommodation of patients |

| 821 | Hospitals | Building for the diagnosis, treatment, and accommodation of patients |

| 829 | Others | Others |

| 83 | Health clinics | Establishment dedicated to the diagnosis and treatment of diseases |

| 831 | Physiotherapy | Establishment dedicated to the treatment of trauma or injury |

| 832 | Dentistry | Establishment dedicated to dental treatment |

| 833 | Ophthalmology | Establishment dedicated to eye treatment |

| 834 | Radiology | Diagnostic facility using radiology |

| 839 | Others | Others |

| 84 | Geriatrics | Building intended for geriatric accommodation |

| 841 | Day care centres | Geriatric day-stay building |

| 842 | Geriatric residence | Geriatric housing building |

| 849 | Others | Others |

| 85 | Funeral | Building intended for the burial or treatment of corpses |

| 851 | Funeral homes | Building intended for the treatment of corpses prior to burial |

| 852 | Cemetery | Space for the burial of corpses |

| 859 | Others | Others |

| 86 | Prison | Construction of a prison for offenders |

| 861 | Prison | Construction of a prison for offenders |

| 862 | Juvenile offenders centre | Construction of detention centre for juvenile offenders |

| 869 | Others | Others |

| 87 | Veterinarian | Space for the treatment of animals |

| 871 | Veterinarian | Space for the treatment of animals |

| 879 | Others | Others |

| 89 | Others | Other healthcare spaces not included above |

| 899 | Others | Other healthcare spaces not included above |

| 9 | Urbanisation | Land preparation for building plots (only actions that cannot be assigned to a single building) |

| 91 | Terrain | Preparation of rural land for its transition to urban |

| 911 | Terrain | Develop a plot of land |

| 919 | Others | Others |

| 99 | Others | Others |

| 999 | Others | Others |

Appendix B

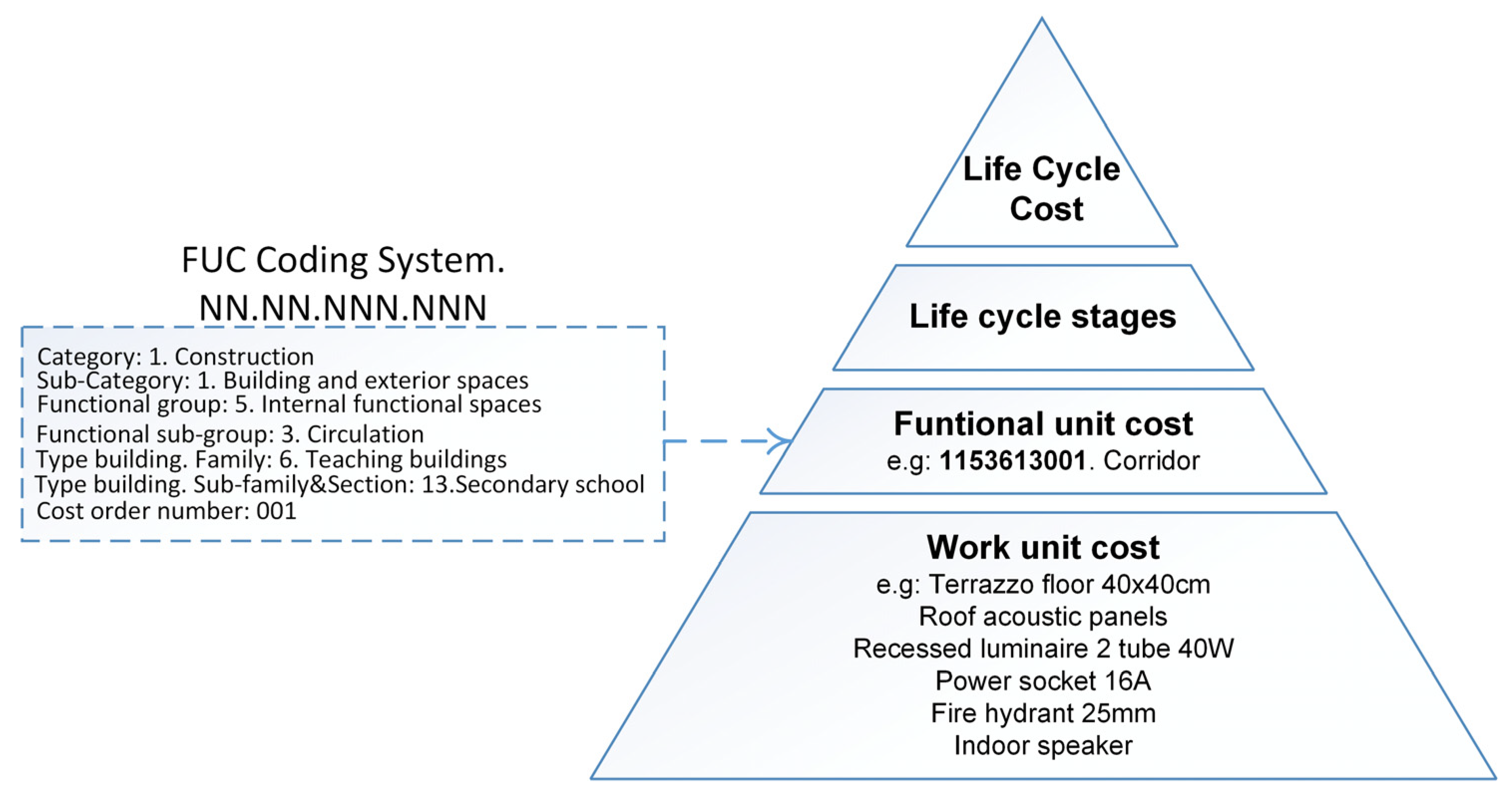

| 1153613001 | m2 | Corridor | |||

| Corridor of a secondary school, including cladding (except partitions with uses) and installations from distribution. Measured in terms of usable area. | |||||

| Code | Unit | Concept | Quantity | Cost (€) | Amount (€) |

| 10STS90010 | m2 | Terrazzo floor with small grain 40 cm × 40 cm | 1.00000 | 21.28 | 21.28 |

| 10SER00001 | m2 | Stainless steel skirting board 2 mm and 7 cm | 1.00000 | 11.64 | 11.64 |

| 09TSS00010 | m2 | Insulation of rigid polyester plank floors Extended 20 mm | 1.00000 | 6.74 | 6.74 |

| 10TWW90013 | m2 | Roof acoustic panels, removable and concealed truss | 0.53776 | 62.81 | 33.78 |

| 10TWW00011 | m2 | Continuous ceiling with laminated plasterboard | 0.46224 | 20.15 | 9.31 |

| 09TTT00100 | m2 | Insulated felt roofs with fibreglass, 20 mm | 1.00000 | 15.94 | 15.94 |

| 13EAA00001 | m2 | Smooth acrylic elastomer paint | 0.46224 | 3.67 | 1.70 |

| 08ETT00003 | unit | 16 A recessed power socket with 2.5 mm2 | 0.03789 | 37.06 | 1.40 |

| 08PIS00031 | unit | Emergency lighting and signal equipment, 160 lumens | 0.04547 | 72.68 | 3.30 |

| 08WII00135 | unit | Recessed luminaire 2 tubes 40 W. 30 mm × 30 mm | 0.09095 | 125.28 | 11.39 |

| 08PID00101 | unit | Push button for manual surface alarm triggering | 0.01137 | 22.07 | 0.25 |

| 08PIE90023 | unit | Mobile fire extinguisher, ABC powder, 6 kg | 0.03032 | 28.74 | 0.87 |

| 08PID90200 | unit | Indoor buzzer | 0.01137 | 21.89 | 0.25 |

| 08PIS90107 | unit | Label 297 mm × 210 mm | 0.06442 | 10.74 | 0.69 |

| 08PIE90013 | unit | Fire hydrant 25 mm diameter and cabinet | 0.01137 | 501.84 | 5.71 |

| 08DA00201 | unit | Indoor speaker | 0.02274 | 120.29 | 2.74 |

| Total | 126.99 | ||||

Appendix C

| 2353613001 | m2 | Annual Corridor Maintenance | |||

| Annual maintenance of corridors including the revision and maintenance of fire extinguishers and BIEs. Measured in terms of usable ground area | |||||

| Code | Unit | Concept | Quantity | Cost | Amount |

| 20IPC00001 | unit | Revision and maintenance of manual fire extinguisher up to 6 kg | 0.03032 | 3.79 | 0.11 |

| 20IPC00005 | unit | Overhaul and maintenance of equipped fire hydrants | 0.01137 | 7.57 | 0.09 |

| Total | 0.20 | ||||

Appendix D

| 2353613001 | m2 | Corridor repairs annually | ||||

| Annual repairs in the corridor of a secondary school including cladding (except divisions with uses) and installations from distribution. Measured in terms of usable ground area of the functional space | ||||||

| Code | Unit | Concept | % Rep. | Quantity | Cost | Amount |

| 10STS90010 | m2 | Terrazzo floor with small grain 40 cm × 40 cm | 0.13 | 0.00130 | 21.28 | 0.03 |

| 10SER00001 | m2 | Stainless steel skirting board 2 mm and 7 cm | 0.13 | 0.00130 | 11.64 | 0.02 |

| 09TSS00010 | m2 | Insulation of floor with rigid polyester plank, 20 mm thick | 0.13 | 0.00130 | 6.74 | 0.01 |

| 10TWW90013 | m2 | Roof acoustic panels, removable and concealed truss | 0.08 | 0.00043 | 62.81 | 0.03 |

| 10TWW00011 | unit | Continuous ceiling with laminated plasterboard | 0.08 | 0.00037 | 20.15 | 0.01 |

| 09TTT00100 | unit | Roof Insulation with fibreglass felt, 20 mm thick | 0.08 | 0.00080 | 15.94 | 0.01 |

| 13EAA00001 | unit | Smooth acrylic elastomer paint | 0.08 | 0.00037 | 3.67 | 0.00 |

| 08ETT00003 | unit | 16 A recessed power socket with 2.5 mm2 | 1.00 | 0.00038 | 37.06 | 0.01 |

| 08PIS00031 | unit | Emergency lighting and signal equipment, 160 lumens | 1.50 | 0.00068 | 72.68 | 0.05 |

| 08WII00135 | unit | Recessed luminaire 2 tubes 40 W, 30 mm × 30 mm | 1.50 | 0.00136 | 125.28 | 0.17 |

| 08PID00101 | unit | Push button for manual surface alarm triggering | 1.00 | 0.00011 | 22.07 | 0.00 |

| 08PIE90023 | unit | Mobile fire extinguisher, ABC powder, 6 kg | 8.30 | 0.00252 | 28.74 | 0.07 |

| 08PID90200 | unit | Indoor buzzer | 1.00 | 0.00011 | 21.89 | 0.00 |

| 08PIS90107 | unit | Label 297 mm × 210 mm | 2.00 | 0.00129 | 10.74 | 0.01 |

| 08PIE90013 | unit | Fire hydrant 25 mm diameter and cabinet | 2.00 | 0.00023 | 501.84 | 0.12 |

| 08DA00201 | unit | Indoor speaker | 2.00 | 0.00045 | 120.29 | 0.05 |

| Total | 0.59 | |||||

Appendix E

| 2353613071 | m2 | Replacements year 70. Corridors | |||

| Year 70 replacements in corridors of construction elements including floors, ceilings and installations including demolition, excluding floor insulation and painting (maintenance). Measured in terms of usable ground area of the functional space | |||||

| Code | Unit | Concept | Quantity | Cost | Amount |

| 10STS90010 | m2 | Terrazzo floor with small grain 40 cm × 40 cm | 1.00000 | 21.28 | 21.28 |

| 10SER00001 | m2 | Stainless steel skirting board 2 mm and 7 cm | 1.00000 | 11.64 | 11.64 |

| 10TWW90013 | m2 | Roof acoustic panels, removable and concealed truss | 0.53776 | 62.81 | 33.78 |

| 10TWW00011 | m2 | Continuous ceiling with laminated plasterboard | 0.46224 | 20.15 | 9.31 |

| 09TTT00100 | m2 | Roof Insulation with fibreglass felt, 20 mm thick | 1.00000 | 15.94 | 15.94 |

| 13EAA00001 | m2 | Smooth acrylic elastomer paint | 0.46224 | 3.67 | 1.70 |

| 08ETT00003 | unit | 16 A recessed power outlet with 2.5 mm2 | 0.03789 | 37.06 | 1.40 |

| 08PIS00031 | unit | Emergency lighting and signal equipment, 160 lumens | 0.04547 | 72.68 | 3.30 |

| 08WII00135 | unit | Recessed luminaire 2 tubes 40 W, 30 mm × 30 mm | 0.09095 | 125.28 | 11.39 |

| 08PID00101 | unit | Push button for manual surface alarm triggering | 0.01137 | 22.07 | 0.25 |

| 08PIE90023 | unit | Mobile fire extinguisher, ABC powder, 6 kg | 0.03032 | 28.74 | 0.87 |

| 08PID90200 | unit | Indoor buzzer | 0.01137 | 21.89 | 0.25 |

| 08PIS90107 | unit | Label 297 mm × 210 mm | 0.06442 | 10.74 | 0.69 |

| 08PIE90013 | unit | Fire hydrant 25 mm diameter and cabinet | 0.01137 | 501.84 | 5.71 |

| 08KIA00201 | unit | Indoor speaker | 0.02274 | 120.29 | 2.74 |

| 01RST90002 | unit | Selective demolition with mechanical means of terrazzo flooring and skirting boards | 1.00000 | 5.86 | 5.86 |

| 01RTE90100 | unit | Selective demolition of continuous plasterboard ceiling | 1.00000 | 3.40 | 3.40 |

| 01IEW90055 | unit | Massive manual demolition of electrical installation in functional space < 100 m2 | 1.00000 | 0.57 | 0.57 |

| Total | 130.08 | ||||

Appendix F

| 1150613001 | m2 | Functional area of circulations in a secondary school | |||

| Understanding the spaces of corridors and stairs of communication between floors of the building. Measured in terms of usable ground area of the functional space | |||||

| Code | Unit | Concept | Quantity | Cost | Amount |

| 1153613001 | m2 | Corridor | 0.76351 | 166.23 | 126.92 |

| 1153613002 | m2 | Staircase starting section with storage | 0.10135 | 465.04 | 47.13 |

| 1153613003 | m2 | Staircase on the middle floor | 0.03378 | 450.31 | 15.21 |

| 1153613004 | m2 | Landing space stairway | 0.10135 | 224.00 | 22.70 |

| Total | 211.96 | ||||

References

- Oxford Economics. Future of Construction—A Global Forecast for Construction to 2030; Oxford Economics: London, UK, 2021. [Google Scholar]

- Eurostats Construction Sector. Available online: https://ec.europa.eu/eurostat/cache/digpub/housing/bloc-3a.html?lang=en (accessed on 29 October 2023).

- Rivero-Camacho, C.; Martín-del-Río, J.J.; Marrero-Meléndez, M. Evolution of the Life Cycle of Residential Buildings in Andalusia: Economic and Environmental Evaluation of Their Direct and Indirect Impacts. Sustain. Cities Soc. 2023, 93, 104507. [Google Scholar] [CrossRef]

- MITMA. Licitación Oficial En Construcción. Año 2021; MITMA: Madrid, Spain, 2021. [Google Scholar]

- European parlament Directive 2014/24/EU of The European Parliament and of the Council of 26 February 2014 on Public Procurement and Repealing Directive 2004/18/EC (Text with EEA Relevance). Off. J. Eur. Union 2014, 94, 65–242.

- Dodd, N.; Donatello, S.; Cordella, M. Level(s)-A Common EU Framework of Core Sustainability Indicators for Office and Residential Buildings User Manual 1: Introduction to the Level(s) Common Framework (Publication Version 1.1); European Commission: Brussels, Belgium, 2021. [Google Scholar]

- BREEAM-SE. BREEAM-SE New Construction v6.0 Technical Manual 1.1; Sweden Green Building Council: Stockholm, Sweden, 2023. [Google Scholar]

- Sherif, Y.S.; Kolarik, W.J. Life Cycle Costing: Concept and Practice. Omega 1981, 9, 287–296. [Google Scholar] [CrossRef]

- ISO-15686-5; ISO Buildings and Constructed Assets—Service Life Planning—Part 5: Life-Cycle Costing. ISO: Geneva, Switzerland, 2017; p. 52.

- EN 15643:2021; Sustainability of Construction Works—Framework for Assessment of Buildings and Civil Engineering Works. CEN: Brussels, Belgium, 2021; p. 48.

- Goh, B.H.; Sun, Y. The Development of Life-Cycle Costing for Buildings. Build. Res. Inf. 2016, 44, 319–333. [Google Scholar] [CrossRef]

- Islam, H.; Jollands, M.; Setunge, S. Life Cycle Assessment and Life Cycle Cost Implication of Residential Buildings—A Review. Renew. Sustain. Energy Rev. 2015, 42, 129–140. [Google Scholar] [CrossRef]

- Al-Kasasbeh, M.; Abudayyeh, O.; Liu, H. A Unified Work Breakdown Structure-Based Framework for Building Asset Management. J. Facil. Manag. 2020, 18, 437–450. [Google Scholar] [CrossRef]

- AbouHamad, M.; Abu-Hamd, M. Framework for Construction System Selection Based on Life Cycle Cost and Sustainability Assessment. J. Clean. Prod. 2019, 241, 118397. [Google Scholar] [CrossRef]

- Hromada, E.; Vitasek, S.; Holcman, J.; Heralova, R.S.; Krulicky, T. Residential Construction with a Focus on Evaluation of the Life Cycle of Buildings. Buildings 2021, 11, 524. [Google Scholar] [CrossRef]

- Zanni, M.; Sharpe, T.; Lammers, P.; Arnold, L.; Pickard, J. Developing a Methodology for Integration of Whole Life Costs into BIM Processes to Assist Design Decision Making. Buildings 2019, 9, 114. [Google Scholar] [CrossRef]

- Gobierno de España. Ley 9/2017, de 8 de Noviembre, de Contratos Del Sector Público; Gobierno de España: Madrid, Spain, 2017; Volume 2014, pp. 1–233. [Google Scholar]

- Ramírez de Arellano Agudo, A. Presupuestación de Obras; Universidad de Sevilla, Secretariado de Publicaciones: Sevilla, Spain, 2014; ISBN 9788447212057. [Google Scholar]

- Cerezo-Narváez, A.; Pastor-Fernández, A.; Otero-Mateo, M.; Ballesteros-Pérez, P. Integration of Cost and Work Breakdown Structures in the Management of Construction Projects. Appl. Sci. 2020, 10, 1386. [Google Scholar] [CrossRef]

- Vázquez-López, E.; Garzia, F.; Pernetti, R.; Solís-Guzmán, J.; Marrero, M. Assessment Model of End-of-Life Costs and Waste Quantification in Selective Demolitions: Case Studies of Nearly Zero-Energy Buildings. Sustainability 2020, 12, 6255. [Google Scholar] [CrossRef]

- ISO 12006-2; Building Construction—Organization of Information about Construction Works. ISO: Geneva, Switzerland, 2015.

- Soust-Verdaguer, B.; Bernardino Galeana, I.; Llatas, C.; Montes, M.V.; Hoxha, E.; Passer, A. How to Conduct Consistent Environmental, Economic, and Social Assessment during the Building Design Process. A BIM-Based Life Cycle Sustainability Assessment Method. J. Build. Eng. 2022, 45, 103516. [Google Scholar] [CrossRef]

- Marrero, M.; Rivero-Camacho, C.; Alba-Rodríguez, M.D. What Are We Discarding during the Life Cycle of a Building? Case Studies of Social Housing in Andalusia, Spain. Waste Manag. 2020, 102, 391–403. [Google Scholar] [CrossRef] [PubMed]

- Afsari, K.; Eastman, C.M. A Comparison of Construction Classification Systems Used for Classifying Building Product Models; In Proceedings of the 52nd ASC Annual International Conference Proceedings, Provo, UT, USA, 13–16 April 2016.

- Ekholm, A. A Conceptual Framework for Classification of Construction Works. Electron. J. Inf. Technol. Constr. 1996, 1, 25–50. [Google Scholar]

- ISO 12006-3:2022; Building Construction—Organization of Information about Construction Works—Part 3: Framework for Object-Oriented Information. ISO: Geneva, Switzerland, 2022.

- RICS. NRM 1: Order of Cost Estimating and Cost Planning for Capital Building Works; RICS: London, UK, 2012; ISBN 978-1-84219-716-5. [Google Scholar]

- CSI&CSC. Masterformat; CSI: Alexandria, VA, USA, 2016. [Google Scholar]

- Gelder, J. The Principles of a Classification System for BIM: Uniclass 2015. In Proceedings of the 49th International Conference of the Architectural Science Association, Melbourne, VIC, Australia, 2–4 December 2015; Volume 1, pp. 287–297. [Google Scholar]

- NBS Uniclass 2015 | NBS. Available online: https://www.thenbs.com/our-tools/uniclass-2015 (accessed on 26 November 2019).

- European Committee of Construction Economists. Code of Measurement for Cost Planning CEEC; European Committee of Construction Economists: Brussels, Belgium, 2014; pp. 1–20. [Google Scholar]

- Davis Langdon Management Consulting. Life Cycle Costing (LCC) as a Contribution to Sustainable Construction: A Common Methodology; Davis Langdon Management Consulting: London, UK, 2007. [Google Scholar]

- Pernetti, R.; Kystallidi, K. D2.3: Structured Repository of Existing LCC Calculation Tools; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- ICMS SSC. International Construction Measurement Standards: Global Consistency in Presenting Construction Costs; ICMS: London, UK, 2019. [Google Scholar]

- FIEBDC. Formato de Intercambio de Datos Estandar de Base de Datos de Construcción; FIEBDC: Madrid, Spain, 2020. [Google Scholar]

- Junta de Andalucía Base de Costes de La Construcción de Andalucía (BCCA)—Junta de Andalucía. Available online: https://www.juntadeandalucia.es/organismos/fomentoarticulaciondelterritorioyvivienda/areas/vivienda-rehabilitacion/planes-instrumentos/paginas/vivienda-bcca.html (accessed on 3 October 2023).

- Makarfi Ibrahim, Y.; Kaka, A.; Aouad, G.; Kagioglou, M. Framework for a Generic Work Breakdown Structure for Building Projects. Constr. Innov. 2009, 9, 388–405. [Google Scholar] [CrossRef]

- Gobierno de España. Real Decreto 1020/1993 de 25 de Junio, Por El Que Se Aprueban Las Normas Técnicas de Valoración y El Cuadro Marco de Valores Del Suelo y de Las Construcciones Para Determinar El Valor Catastral de Los Bienes Inmuebles de Naturaleza Urbana; Gobierno de España: Madrid, Spain, 1993. [Google Scholar]

- RAE Edificio | Definición | Diccionario de La Lengua Española | RAE—ASALE. Available online: https://dle.rae.es/edificio (accessed on 15 January 2020).

- ASTM E631; Standard Terminology of Building Constructions. ASTM International: West Conshohocken, PA, USA, 2015.

- ISO 6707-1; Buildings and Civil Engineering Works Vocabulary Part 1: General Terms. ISO: Geneva, Switzerland, 2020.

- Lufkin, P.S.; Miller, J.; Romani, L.; Towers, M. The Whitestone Facility Maintenance and Repair Cost Reference, 2010th ed.; Whitestone Research: Santa Barbara, CA, USA, 2009; ISBN 978-0-9670629-9-0. [Google Scholar]

- EN-15459-1; Energy Performance of Buildings. Economic Evaluation Procedure for Energy Systems in Buildings. Part-1. Calculation Procedures, Module M1-14. CEN: Brussels, Belgium, 2017.

- Junta de Andalucía Anexo, I. Programas de Necesidades Para Los Diferentes Tipos de Centros Docentes; Junta de Andalucía Anexo, I: Sevilla, Spain, 2003; p. 12. [Google Scholar]

- Gobierno de España. Real Decreto 1247/2008. Instrucción de Hormigón Estructural (EHE-08); Gobierno de España: Madrid, Spain, 2008. [Google Scholar]

- Ministerio de Fomento Boletín Estadístico Online—Información Estadística—Ministerio de Fomento. Available online: https://apps.fomento.gob.es/BoletinOnline2/?nivel=2&orden=36000000 (accessed on 12 May 2021).

- Ayuntamiento de Sevilla. Ordenanza Fiscal Por Prestación de Servicios Urbanísticos; Ayuntamiento de Sevilla: Sevilla, Spain, 2018; p. 30. [Google Scholar]

| Name | Code |

|---|---|

| Uniclass | ZZ-NN-NN-NN-NN |

| ACCD | NN-Z-Z-Z-NNNNN |

| EN-15643 | Z-N |

| CEEC | Z |

| ICMS | NN-N-NN-NNN |

| Uniclass Levels | ||||

| Table | Denomination | Level | Description | |

| Entities | Group | N1 | Grouping of buildings per use | |

| Sub-group | N2 | Sub-division of buildings per use | ||

| Section | N3 | Types of buildings | ||

| Functional Spaces | Group | N1 | Grouping of spaces or locations | |

| Sub-group | N2 | Spaces and locations | ||

| Functional Elements | Group | N1 | Grouping of Building Elements and Functions | |

| Sub-group | N2 | Elements and functions of the building | ||

| ICMS Levels | ||||

| Main Levels | Level | Description | ||

| Project | N1 | Types of construction (building and civil) | ||

| Cost Categories | N2 | Division according to construction life cycle | ||

| Cost Groups | N3 | Construction Division | ||

| Cost sub-group | N4 | Sub-division of Cost Groups | ||

| New Proposal Levels | ||||

| Main Levels | Level | Secondary Levels | ||

| Life cycle Categories | N1 | n.1.1. | Categories | |

| n.1.2. | Sub-categories | |||

| Functional Groups | N2 | n.2.1. | Functional Groups | |

| n.2.2. | Functional sub-groups | |||

| Type of building | N3 | n.3.1. | Type of Family | |

| n.3.2. | Type of Sub-family | |||

| n.3.3. | Type of Section | |||

| Level | Digits | Description | ||||

|---|---|---|---|---|---|---|

| N1 | NN | Life Cycle | ||||

| N2 | NN | Functional elements of the building | ||||

| N3 | NNN | Type of building | ||||

| N4 | NNN | Order Number | ||||

| N1. | N2. | N3. | N4. | |||

| NN. | NN. | NNN. | NNN | |||

| Category | Sub-Category | ||

|---|---|---|---|

| 0 | Pre-construction | 01 | Preliminary work |

| 09 | Income, taxation, professional fees, and other expenses of the developer | ||

| 1 | Construction | 11 | Building and outdoor spaces |

| 19 | Income, taxation, professional fees, and other expenses of the developer | ||

| 2 | Use | 21 | Expenses of the building use |

| 22 | Maintenance | ||

| 23 | Repair | ||

| 24 | Replacement | ||

| 25 | Refurbishment | ||

| 26 | Operational energy use | ||

| 27 | Operational water use | ||

| 28 | User activities | ||

| 29 | Income, taxation, professional fees, and other expenses of the developer | ||

| 3 | End of Life | 31 | Demolition–deconstruction |

| 34 | Waste management and/or landfill fees | ||

| 39 | Income, taxation, professional fees, and other expenses of the developer |

| Functional Group N and Sub-Group NN | Boundaries | |

|---|---|---|

| 0 | Pre-work and demolition | Activities prior to construction, replacement or repair work not related to building functions |

| 00 | Preliminary work and demolition | Functional areas of pre-work and demolition |

| 01 | Previous work | Preliminary work on the land or building not directly applicable to another functional element (e.g., prospecting). |

| 02 | Massive demolition | Massive demolition work of any existing functional element (no waste separation takes place during the demolition process) |

| 03 | Selective dismantling or demolition | Dismantling or selective demolition work (with separation of waste during the demolition process) |

| 06 | Waste management | Waste management during pre-work and demolition |

| 07 | Quality control | Quality control of previous work |

| 08 | Health and safety | Health and safety of previous work |

| 09 | Others | Other functional elements of pre-work and demolition |

| 1 | Sub-structures | Construction elements that transmit the building’s loads to the ground, including earthworks and sanitary slabs and braced slabs |

| 10 | Sub-structures | Functional areas of sub-structures |

| 11 | Special | Special foundations, such as diaphragm walls |

| 12 | Surface | Foundation made by surface elements, such as footings or slabs, and the elements that support them directly (e.g., sanitary slabs and braced slabs) |

| 13 | Deep | Foundation made by deep elements, such as piles |

| 16 | Waste management | Foundation waste management |

| 17 | Quality control | Quality control of foundations |

| 18 | Health and safety | Health safety of foundations |

| 19 | Others | Other functional elements of foundations |

| 2 | Structures | Construction elements that transmit the loads of the use of the spaces to the foundations |

| 20 | Structure | Functional areas of structure |

| 21 | Porticoes | Structures made of porticoes and slabs |

| 22 | Space | Spatial structures |

| 23 | Vaulted | Spatial structures made by means of vaults |

| 26 | Waste management | Structure waste management |

| 27 | Quality Control | Structure quality control |

| 28 | Health and Safety | Structure health and safety |

| 29 | Others | Other functional elements of the structure |

| 3 | Installations | Construction elements that are responsible for facilitating use and maintaining comfort |

| 30 | Installations | Functional areas of installations |

| 31 | Affected | Elements from the external network to centralisation |

| 32 | Centralisation | Elements from connection to distribution |

| 33 | Distribution | Elements from centralisation to functional spaces |

| 34 | Production | Elements for the production of a supply |

| 36 | Waste management | Installation waste management |

| 37 | Quality Control | Installation quality control |

| 38 | Health and Safety | Installation Health and Safety |

| 39 | Others | Other functional elements of the installations |

| 4 | Envelope | Transitional construction elements between the exterior and interior spaces of the building |

| 40 | Envelope | Enclosure functional areas |

| 41 | Flat roofs | Upper building envelope with <5% inclination |

| 42 | Pitched roofs | Upper building envelope with high inclination >5% |

| 43 | Monolithic façades | Vertical building envelope in a single layer |

| 44 | Chambered or ventilated façades | Vertical envelope of several layers separated by air |

| 45 | Curtain walls | Vertical self-supporting enclosure, usually glazed |

| 46 | Waste management | Enclosure waste management |

| 47 | Quality Control | Enclosure quality control |

| 48 | Health and Safety | Enclosure health and safety |

| 49 | Others | Other functional elements of enclosures |

| 5 | Indoor Spaces | Construction elements that define the interior spaces of the building |

| 50 | Indoor spaces | Functional areas of indoor spaces |

| 51 | Specific | Use-specific functional spaces |

| 52 | Complementary | Functional spaces that complement specific spaces |

| 53 | Circulations | Transitional spaces that connect to interior spaces |

| 56 | Waste management | Indoor waste management |

| 57 | Quality control | Quality control of interior spaces |

| 58 | Health and safety | Health and safety of indoor spaces |

| 59 | Others | Other functional elements of interior spaces |

| 6 | Outdoor spaces | Construction elements outside the occupation of the building within the plot |

| 60 | Outdoor spaces | Functional areas of spaces outside the building within the plot |

| 61 | Plot enclosure | Transition element between the interior and exterior of the plot |

| 62 | Plot cover | Covered outdoor spaces |

| 63 | Open | Uncovered outdoor spaces |

| 66 | Waste management | Waste management of outdoor spaces |

| 67 | Quality control | Quality control of outdoor spaces |

| 68 | Health and safety | Health and safety of outdoor spaces |

| 69 | Others | Other functional elements of outdoor spaces |

| Functional Group N and Sub-Group NN | Boundaries | |

|---|---|---|

| 1 | Land preliminary work | |

| 10 | Land preliminary work | In functional areas, this is the preliminary land work referring to the land purchased |

| 11 | Rural land | Purchase of non-urban land |

| 12 | Management of urban transformations | Management, assignments, and agreements of urban transformations |

| 13 | Urban transformation work | Urban transformation work |

| 14 | Urban land | Acquisition of land that does not require urban transformations |

| 19 | Others | Other functional land-related functional areas |

| 2 | Preliminary building actions | |

| 20 | Preliminary actions in building | In functional areas, these are preliminary actions related to the building purchased to transform |

| 21 | Building | Acquisition of an existing building to be rehabilitated or conserved |

| 22 | Pre-rehabilitation work | Urgent consolidation and stabilisation work not related to the main work |

| 29 | Others | Other functional cells related to building |

| Functional Group/Sub-Group | Boundaries | |

|---|---|---|

| 1 | Income | |

| 10 | Income | Functional areas of the revenue generated by the site or building |

| 11 | Exploitation of assets | Income received from the operation of the building or land |

| 12 | Sale of goods | Partial sale of buildings or land that do not form part of the post-construction building |

| 13 | Other royalties or property rights | These include advertising revenue, rights to use the land, and easements at any stage of the life cycle |

| 14 | Grants | Grant income |

| 19 | Others | Income not covered above |

| 2 | Studies, projects, and directions | |

| 20 | Studies, projects, and directions | Functional areas of expenditure for study, projects, and management services |

| 21 | Feasibility studies | These include any previous studies (economic, environmental, or technical) |

| 22 | Urban or environmental studies and projects | These include any study and project (technical or environmental) linked to the urban transformation of the land related to the building |

| 23 | Blueprints | Preliminary studies of the design of the building |

| 24 | Building projects | Basic and execution project of the building |

| 25 | Site management | This includes professional services, such as construction management, health and safety coordination, quality control, and technical advice on the construction site |

| 26 | Comprehensive project management | Includes professional services for comprehensive project management |

| 29 | Others | Any expense not contemplated in previous sections of professional services |

| 3 | Developer’s other expenses | |

| 30 | Developer’s other expenses | Functional area of the developer’s other expenses |

| 31 | Assessment | Expenses for the appraisal of the building during the life cycle |

| 32 | Marketing | Expenses related to the marketing of the building |

| 33 | Notary, registries, and cadastre | Expenses related to legal operations of transmissions and registry of the building |

| 34 | Insurance | Property insurance expenses and their transformations |

| 35 | Financial expenses | Fees and interest expenses related to financial transactions |

| 38 | Developer overhead | The developer’s own expenses not related to a specific building |

| 39 | Others | Any expense not contemplated in previous sections of the property developer |

| 4 | Taxation | |

| 40 | Fees and taxes | Functional areas of the fees and taxes supported by the construction of a building |

| 41 | City fees and taxes | Municipal fees and taxes |

| 42 | Regional fees and taxes | Regional fees and taxes |

| 43 | State fees and taxes | State Fees and taxes |

| 49 | Others | Other functional cell fees and taxes |

| Project General Characteristic | Floor Area (m2) |

|---|---|

| Lot size | 6.000 |

| Gross external/usable area coefficient | 1.15 |

| Total gross external area of buildings | 3.450 |

| Total surface area occupied by outdoor spaces | 3.942 |

| Total building floor area | 2.058 |

| Breakdown indoor spaces (usable area) | |

| Specific functional spaces | 1510 |

| Multipurpose classrooms | 720 |

| Music Lessons classrooms | 60 |

| Special education classrooms | 50 |

| Plastic art classrooms | 60 |

| Workshop classrooms | 100 |

| Laboratory rooms | 60 |

| Integration support rooms | 60 |

| Sport rooms | 400 |

| Complementary spaces | 750 |

| Circulations spaces | 740 |

| Total indoor spaces | 3000 |

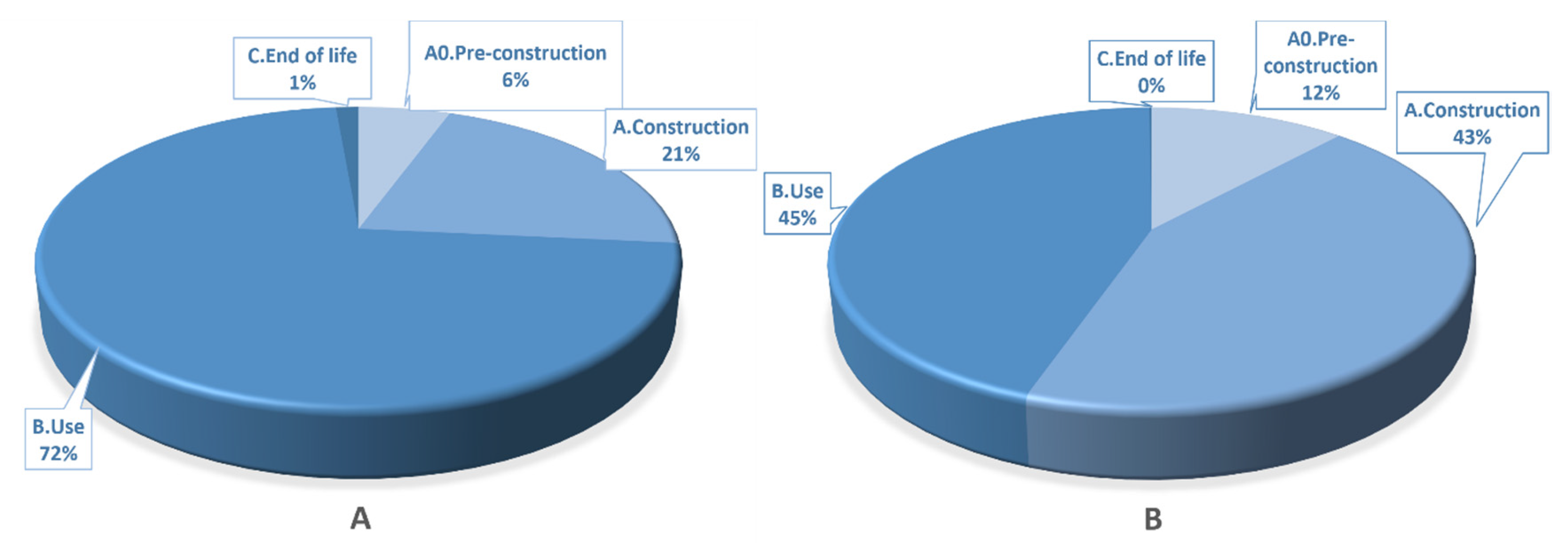

| Stage | Secondary School % (€/m2) | Four Stories Residential % (€/m2) |

|---|---|---|

| A0. Pre-construction | 5.5 (329.81) | 11.3 (329.81 *) |

| A. Construction | 21.0 (1248.66) | 21.9 (635.29) |

| B. Use | 72.1 (4291.73) | 65.5 (1904.80) |

| C. End of life | 1.4 (81.26) | 1.3 (37.36) |

| LCC | 100 (5951.45) | 100 (2907.26) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vázquez-López, E.; Solís-Guzmán, J.; Marrero, M. A Work Breakdown Structure for Estimating Building Life Cycle Cost Aligned with Sustainable Assessment—Application to Functional Costs. Buildings 2024, 14, 1119. https://doi.org/10.3390/buildings14041119

Vázquez-López E, Solís-Guzmán J, Marrero M. A Work Breakdown Structure for Estimating Building Life Cycle Cost Aligned with Sustainable Assessment—Application to Functional Costs. Buildings. 2024; 14(4):1119. https://doi.org/10.3390/buildings14041119

Chicago/Turabian StyleVázquez-López, Eduardo, Jaime Solís-Guzmán, and Madelyn Marrero. 2024. "A Work Breakdown Structure for Estimating Building Life Cycle Cost Aligned with Sustainable Assessment—Application to Functional Costs" Buildings 14, no. 4: 1119. https://doi.org/10.3390/buildings14041119

APA StyleVázquez-López, E., Solís-Guzmán, J., & Marrero, M. (2024). A Work Breakdown Structure for Estimating Building Life Cycle Cost Aligned with Sustainable Assessment—Application to Functional Costs. Buildings, 14(4), 1119. https://doi.org/10.3390/buildings14041119