Review of Offline Payment Function of CBDC Considering Security Requirements

, ,

, ,

Abstract

:1. Introduction

1.1. Central Bank Digital Currency

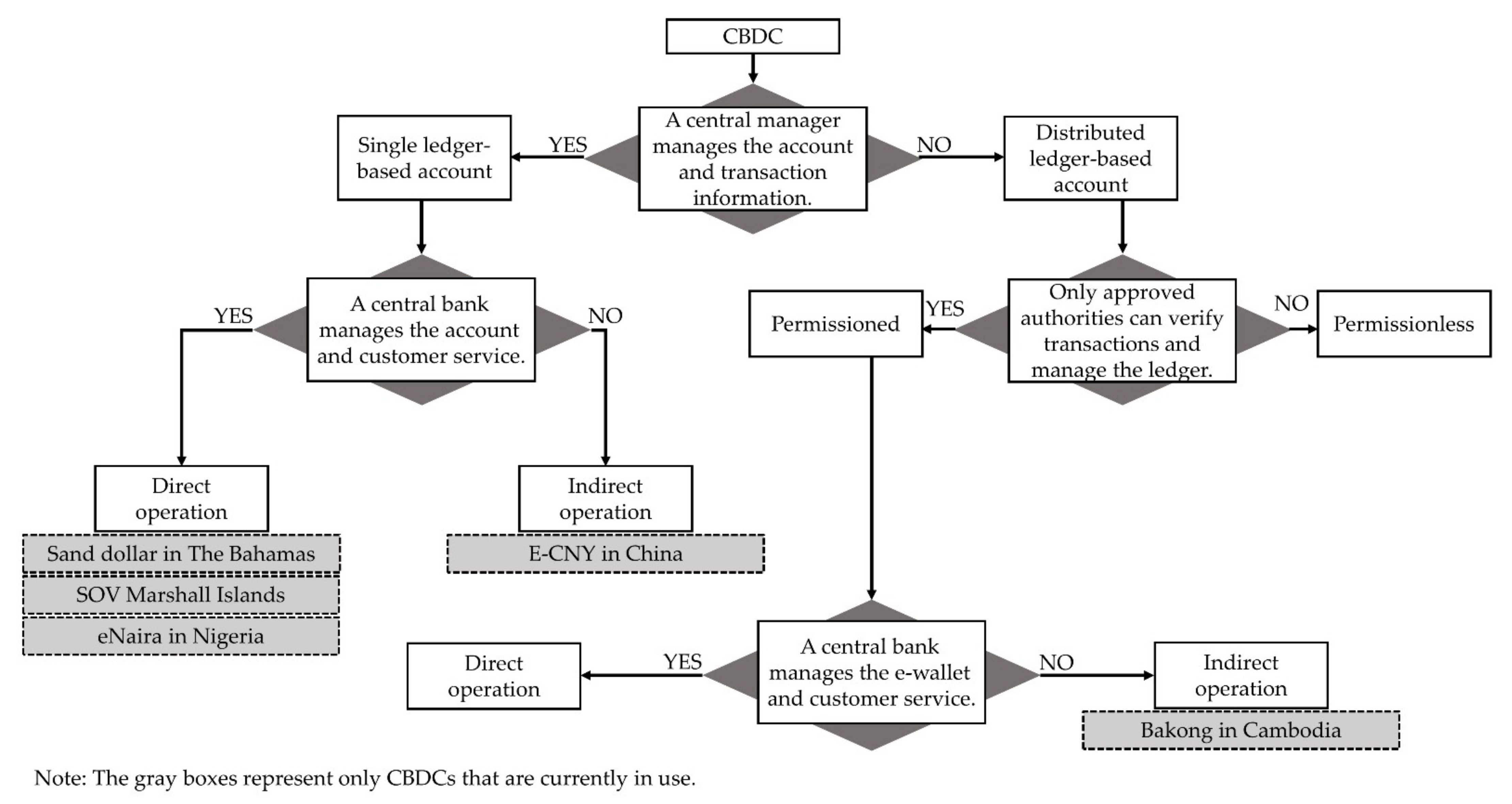

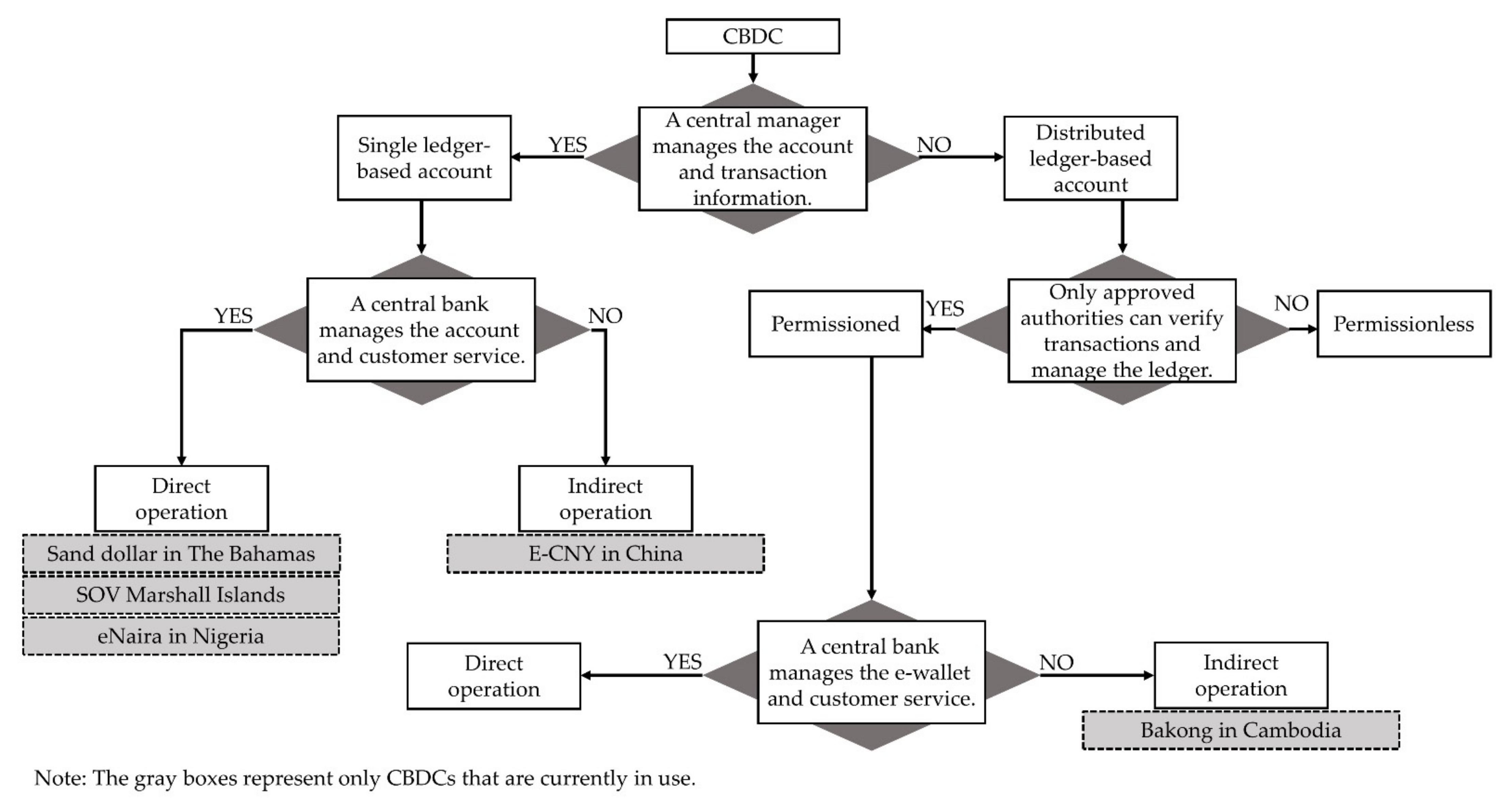

1.2. Countries Developing CBDCs and Types of CBDCs

1.3. Importance of the Offline Payment Function of CBDCs and Security Requirements

1.4. Methodology and Limitation

- What are the security requirements that the offline payment function of electronic financial systems should meet?

- What are the methods that can be applied to electronic financial systems to meet the security requirements?

- How well do the methods proposed in the research studies of offline payment functions of electronic financial systems meet the security requirements?

- What solutions can be suggested for improving TEE-based methods for the offline payment functions of electronic financial systems?

2. Security Requirements for CBDC and Digital Currencies

2.1. No Double Spending

- Step 1. The attacker purchases products/services using a cryptocurrency;

- Step 2. The seller checks whether the attacker’s purchase in Step 1 is in the main blockchain and waits for other confirmation blocks to be added to the main chain blockchain that contains the record of the purchase in Step 1;

- Step 3. In the meantime, while avoiding the seller’s eyes, the attacker processes mining in a fake chain; the transaction in Step 1 is not included;

- Step 4. If the process in Step 2 is completed, the seller sends the attacker products/services;

- Step 5. After receiving products/services, the attacker secretly continues mining and lengthens the fake chain in Step 3 to be longer than the main chain;

- Step 6. As the longest chain is adopted as the main chain, miners will accept the fake chain that the attacker created as the new main chain, and the future proof of work will be conducted based on the new main chain;

- Step 7. Since the new main chain does not include the record of the purchase in Step 1, the attacker can use the cryptocurrency used in Step 1 again.

2.2. Unforgeability

2.3. Non-Repudiation

- The entity that received the digital currency insists that the signature on the digital currency is a forgery;

- The signature is not a forgery, but the entity that received the digital currency insists that the cash was obtained via:

- Unconscionable conduct during transactions;

- Fraud instigated by a third party;

- The undue influence exerted by a third party.

- A service that provides proof of the integrity and origin of data, both in an unforgeable relationship, which any third party can verify at any time during the authentication process;

- An authentication with high assurance that cannot subsequently be refuted.

- FNRP should provide the payer non-repudiation of receipt to verify the transaction from the Adjudicator;

- FNRP should provide the payee non-repudiation of origin to verify the transaction from the Adjudicator;

- When FNRP ends, the transaction parties should obtain both non-repudiation of receipt and non-repudiation of origin (all together, the non-repudiation evidence, NRE). If the receipt and origin evidence are not obtained, the transaction can be seen as problematic;

- FNRP with the trusted third party (TTP) must individually create an NRE regardless of TTP involvement;

- FNRP that does not use the trusted third party (TTP) should present fairness probabilistically;

- FNRP can be terminated by the transaction parties who have confirmed that FNRP has secured fairness after a reasonable period.

2.4. Verifiability

2.5. Anonymity

2.6. Other Considerations: The DDoS Attack Prevention Plan

2.7. Summary

3. Offline Payment Function after Types of Currency

- A currency that can be exchanged even in the absence of a network connection;

- A transaction that can be established without a third party acting as an arbitrator.

3.1. Offline Payment Function with E-Cash Proposed by Camenisch

- Withdrawal phase: a transaction phase that involves a bank and a customer (payer);

- Payment phase: a transaction phase that involves a customer (payer) and a shop (payee);

- Deposit phase: a transaction phase that involves a shop (payee) and a bank.

- The shop (payee): must be assured that the bank will accept the payment [72];

- The customer (payer): must be assured that the withdrawn money will later be accepted for payment and that the bank cannot claim that the money has already been spent. Furthermore, they may require that their privacy be protected [72].

- The trustee can communicate only with the customer;

- It should be impossible for the bank to obtain and track payment information, even if the bank subsequently obtains information related to the customer through the trustee.

3.2. Offline Payment Function with Cryptocurrency Proposed by Dmitrienko

3.2.1. Issues and Suggestions for the Large Capacity of the Blockchain

- and as timestamps when the i-th and i+n-th blocks are created, respectively;

- as a security parameter;

- The transaction should be finished if, and only if,

3.2.2. Issues and Suggestions When Hosting Platform Has Malicious Intent

- Stage of storing pre-loading transactions for future use (validation parameters are not verified at this stage);

- Stage in which the recipient directly checks the validation parameters.

3.2.3. Issues and Suggestions for the Absence of a Timer

3.2.4. Issues and Suggestions for Wallet Damage

3.3. Offline Payment Function with CBDC Proposed by Christodorescu

3.3.1. TEE Model and UA

3.3.2. Components of Offline Payment System

- OPS Server TA: Deployed in the server, manages customer accounts, and sets up customer devices;

- OPS Sender UA: Deployed in the sender’s device, provides offline payment interface to users by interacting with OPS TA and registers UA and TEE by interacting with the server;

- OPS Receiver UA: Deployed in the receiver’s device, provides an interface to check receiver interface and offline payment;

- OPS TA: Deployed in the sender’s secure device in TEE, manages the user’s offline balance only for secure access.

3.3.3. Protocol for Preparing Offline Payment System

3.3.4. Protocols Included in the Transaction Process of Offline Payment System

- Deduction of the amount of money to be sent from the balance of the sender’s offline account;

- Addition of the received amount of money to the recipient’s account.

3.3.5. Security Enhancement of Devices through Cryptographic Technology

- Stage 1 User A requests a certificate from RA, and RA sends a certificate issued by the CA to A through communication with the CA;

- Stage 2 CA publishes A’s certificate through the directory service, and B verifies A’s published certificate;

- Stage 3 After completing B’s certificate verification, the transaction between A and B proceeds.

- Stage 1 User A creates a signing key pair—;

- Stage 2 Send information related to to the server to issue a certificate—;

- Stage 3 Save in , which is the server’s storage.

4. Security Requirements in Current Offline Payment Functions

4.1. Offline Payment Function with E-Cash Proposed by Camenisch

4.2. Offline Payment Function with Cryptocurrency Proposed by Dmitrienko

4.3. Offline Payment Function with CBDC Proposed by Christodorescu

5. Discussion

5.1. Limitations in Satisfying Security Requirements for Offline Payment Function

5.1.1. Applying Blockchain Technology

5.1.2. Trusted Third Party (TTP) Involvement

5.1.3. Pre-Certification for Members Participating in the Transaction or Post-Certification of Transaction Confirmation

5.1.4. Tracking Flow of Money

5.1.5. Using Cryptographic Technique

5.2. Discussion to Satisfy Security Requirements for Offline Payment Function—Focusing on the Research about Offline Payment Protocol of CBDC

5.2.1. Solutions to Satisfy Security Requirement of Unforgeability

- Dmitrienko et al.’s [93] method: In the case of CBDC, using the distributed ledger scheme, forgery attacks can be prevented through the time-based transaction confirmation verification mechanism proposed by Dmitrienko et al. [93]. In the blockchain methods available, n—confirmation blocks had to be created to confirm the transaction. Based on this method, in an offline situation using the time-based transaction confirmation verification mechanism, the attacker is forced to create n—confirmation blocks within the time limit . Thus, the probability of forgery is reduced. The probabilistic relationship between delta and the probability of forgery is described in detail in Section 4.2.

- Method of modifying the increasing conditions of a counter of a device and using sync: In this method, after modification of the increasing conditions of a counter of a device, it is possible to confirm that a forgery attack has occurred through sync. Table 4 shows the description of the variables used.

5.2.2. Solutions to Satisfy Security Requirements of DDoS Attack Prevention

- Method of charging a fee when using the withdrawal or deposit function: The charging system used in the withdraw and deposit protocol can be applied [85]. In the current digital payment system, the profit considered when charging a fee that an attacker can be charged is designed to be less than the cost of a DDoS attack. In the model proposed by Christodorescu et al. [95], when using the withdraw and deposit protocol, the motive for attempting a DDoS attack can be eliminated by charging a fee.

- Method of limiting the number of transactions when using withdraw or deposit function: There is also a way to limit the number of transactions, as shown in Figure 6. The source is blocked so that the withdraw/deposit protocol to generate traffic to the server cannot be intentionally used excessively. DDoS attacks can be prevented through this method.

5.2.3. Additional Considerations to Strengthen the Security Requirements

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- De Almeida, P.; Fazendeiro, P.; Inácio, P.R. Societal risks of the end of physical cash. Futures 2018, 104, 47–60. [Google Scholar] [CrossRef]

- Who Prints Money in the U.S.? Available online: https://www.investopedia.com/ask/answers/082515/who-decides-when-print-money-us.asp (accessed on 11 April 2022).

- Recent Federal Reserve Monetary Policy. Available online: https://www.youtube.com/watch?v=0PmXbTcOVhU (accessed on 11 April 2022).

- Tobin, J. Financial Innovation and Deregulation in Perspective; Cowles Foundation for Research in Economics at Yale University: New Haven, CT, USA, 1986; pp. 19–29. [Google Scholar]

- Hofmann, C. The changing concept of money: A threat to the monetary system or an opportunity for the financial sector? Eur. Bus. Organ. Law Rev. 2020, 21, 37–68. [Google Scholar] [CrossRef]

- Garcia-Swartz, D.D.; Hahn, R.W.; Layne-Farrar, A. The move toward a cashless society: A closer look at payment instrument economics. Rev. Netw. Econ. 2006, 5. [Google Scholar] [CrossRef]

- Coyle, K.; Kim, L.; O’Brien, S. 2021 Findings from the Diary of Consumer Payment Choice; Federal Reserve Bank of San Francisco: San Francisco, CA, USA, 2021. [Google Scholar]

- Khiaonarong, T.; Humphrey, D. Cash use across countries and the demand for central bank digital currency. J. Paym. Strategy Syst. 2019, 13, 32–46. [Google Scholar]

- World Cash Report: 2018. Available online: https://www.g4scashreport.com/ (accessed on 11 April 2022).

- Zandi, M.; Singh, V.; Irving, J. The Impact of Electronic Payments on Economic Growth. Moody’s Anal. Econ. Consum. Credit. Anal. 2013, 217. [Google Scholar]

- Why Central Bank Digital Currencies? Available online: https://libertystreeteconomics.newyorkfed.org/2021/12/why-central-bank-digital-currencies/ (accessed on 11 April 2022).

- How e-Wallets Charge Fees: Every Step of the Process. Available online: https://www.sticpay.com/news/news_detail/how-e-wallets-charge-fees-every-step-of-the-process (accessed on 11 April 2022).

- Equifax Hack: 5 Biggest Credit Card Data Breaches. Available online: https://www.investopedia.com/news/5-biggest-credit-card-data-hacks-history/ (accessed on 11 April 2022).

- Huge South Korean Data Leak Affects almost Half the Country. Available online: https://www.businessinsider.com/south-korea-data-leak-2014-1 (accessed on 11 April 2022).

- Turvey, C.G.; Xiong, X. Financial inclusion, financial education, and e-commerce in rural china. Agribusiness 2017, 33, 279–285. [Google Scholar] [CrossRef]

- Gill, W.; Hara, S.; Whitney, L. Study on Risks and Opportunities of Digitalization for Financial Inclusion; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- Kiff, M.J.; Alwazir, J.; Davidovic, S.; Farias, A.; Khan, M.A.; Khiaonarong, M.T.; Malaika, M.; Monroe, H.; Sugimoto, N.; Tourpe, H.; et al. A Survey of Research on Retail Central Bank Digital Currency; International Monetary Fund: Washington, DC, USA, 2020. [Google Scholar]

- J.P. Morgan Releases Unlocking $120 Billion in Cross-Border Payments Report. Available online: https://www.jpmorgan.com/news/jpmorgan-central-bank-digital-currency-report (accessed on 11 April 2022).

- Progress of Research & Development of E-CNY in China. Available online: http://www.pbc.gov.cn/en/3688110/3688172/4157443/4293696/2021071614584691871.pdf (accessed on 11 April 2022).

- The Number of Americans with Bank Accounts Rises. Available online: https://www.experian.com/blogs/ask-experian/research/the-decline-of-the-unbanked-and-underbanked/ (accessed on 11 April 2022).

- Central Bank Digital Currency Can Contribute to Financial Inclusion but Cannot Solve Its Root Causes. Available online: https://www.atlanticcouncil.org/blogs/geotech-cues/central-bank-digital-currency-can-contribute-to-financial-inclusion-but-cannot-solve-its-root-causes/ (accessed on 11 April 2022).

- Sweden Takes Another Step Toward a Digital Currency. Available online: https://www.investopedia.com/sweden-takes-another-step-toward-a-digital-currency-5092069 (accessed on 31 January 2022).

- The e-Krona and the Macroeconomy. Available online: https://www.econstor.eu/handle/10419/232929 (accessed on 11 April 2022).

- Riksbank, S. Special Issue on the e-Krona. In Sveriges Riksbank Economic Review; Sveriges Riksbank: Stockholm, Sweden, 2018. [Google Scholar]

- Armelius, H.; Guibourg, G.; Levin, A.; Söderberg, G. The rationale for issuing e-krona in the digital era. Sver. Riksbank Econ. Rev. 2020, 2, 6–18. [Google Scholar]

- Lee, J.Y. Central Bank Digital Currency. Bank of Korea. Available online: http://www.bok.or.kr/portal/bbs/B0000232/view.do?nttId=10049812&menuNo=200706&pageIndex=2 (accessed on 11 April 2022).

- Licandro, G. Uruguayan e-Peso on the Context of Financial Inclusion; Banco Central Del Uruguay: Montevideo, Uruguay, 2018.

- About Sand Dollar—Bahamas. Available online: https://www.sanddollar.bs/about (accessed on 11 April 2022).

- What Is SOV? Available online: https://sov.foundation/ (accessed on 11 April 2022).

- Marshall Islands Readies to Make Waves in Digital Currency. Available online: https://www.centralbanking.com/fintech/7697246/marshall-islands-readies-to-make-waves-in-digital-currency (accessed on 11 April 2022).

- With 56 bln Yuan in Transactions, Where is China’s Heading? Available online: http://www.news.cn/english/2021-11/10/c_1310303262.htm (accessed on 11 April 2022).

- Distributed Ledger Technology and the Future of Money and Banking. Available online: https://www.degruyter.com/document/doi/10.1515/ael-2019-0095/html (accessed on 11 April 2022).

- Distributed Ledgers. Available online: https://www.investopedia.com/terms/d/distributed-ledgers.asp (accessed on 11 April 2022).

- Rejeb, A.; Rejeb, K.; Keogh, J.G. Centralized vs. decentralized ledgers in the money supply process: A SWOT analysis. Quant. Financ. Econ. 2021, 5, 40–66. [Google Scholar] [CrossRef]

- Permissioned Blockchain. Available online: https://www.investopedia.com/terms/p/permissioned-blockchains.asp (accessed on 11 April 2022).

- Permissioned vs. Permissionless Blockchains. Available online: https://101blockchains.com/permissioned-vs-permissionless-blockchains/#prettyPhoto (accessed on 11 April 2022).

- The Technology of Retail Central Bank Digital Currency. Available online: https://www.bis.org/publ/qtrpdf/r_qt2003j.htm (accessed on 11 April 2022).

- Soderberg, G.; Bechara, M.; Bossu, W.; Che, N.X.; Kiff, J.; Lukonga, I.; Griffoli, T.M.; Sun, T.; Yoshinaga, A. Behind the Scenes of Central Bank Digital Currency: Emerging Trends, Insights, and Policy Lessons. FinTech Notes 2022, 2022, 35. [Google Scholar]

- RBI Releases Framework for Facilitating Small Value Digital Payments in Offline Mode. Available online: https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=53038 (accessed on 11 April 2022).

- Han, X.; Yuan, Y.; Wang, F. A Blockchain-based Framework for Central Bank Digital Currency. In Proceedings of the 2019 IEEE International Conference on Service Operations and Logistics, and Informatics (SOLI), Zhengzhou, China, 6–8 November 2019. [Google Scholar]

- Chohan, U.W. The Double Spending Problem and Cryptocurrencies. SSRN 2021, 3090174. [Google Scholar] [CrossRef]

- Brands, S. Untraceable Off-line Cash in Wallet with Observers. In Proceedings of the Annual International Cryptology Conference, CRYPTO 1993: Advances in Cryptology—CRYPTO’ 93, Santa Barbara, CA, USA, 22–26 August 1993. [Google Scholar]

- Krsul, I.V.; Mudge, J.C.; Demers, A.J. Method of Electronic Payments that Prevents Double-Spending. Patent US5839119A, 17 November 1998. [Google Scholar]

- Pointcheval, D.; Stern, J. Security Arguments for Digital Signatures and Blind Signatures. J. Cryptol. 2000, 13, 361–396. [Google Scholar] [CrossRef]

- Savolainen, V.; Soria, J. Too Big to Cheat: Mining Pools’ Incentives to Double Spend in Blockchain Based Cryptocurrencies. SSRN 2019, 3506748. [Google Scholar] [CrossRef] [Green Version]

- Karame, G.O.; Androulaki, E.; Capkun, S. Double-spending fast payments in bitcoin. In Proceedings of the 2012 ACM Conference on Computer and Communications Security (CCS ’12), Raleigh, NC, USA, 16–18 October 2012. [Google Scholar]

- Bentov, I.; Lee, C.; Mizrahi, A.; Rosenfeld, M. Proof of activity: Extending bitcoin’s proof of work via proof of stake [extended abstract] y. ACM SIGMETRICS Perform. Eval. Rev. 2014, 42, 34–37. [Google Scholar] [CrossRef]

- Armelius, H.; Claussen, C.A.; Hull, I. On the possibility of a cash-like CBDC. In Sveriges Riksbank Staff Memo; Sveriges Riksbank: Stockholm, Sweden, 2021. [Google Scholar]

- Okamoto, T.; Ohta, K. Universal Electronic Cash. In Proceedings of the Annual International Cryptology Conference, CRYPTO 1991: Advances in Cryptology—CRYPTO ’91, Santa Barbara, CA, USA, 11–15 August 1991. [Google Scholar]

- Franklin, M.; Yung, M. Secure and efficient off-line digital money (extended abstract). In Proceedings of the International Colloquium on Automata, Languages, and Programming, ICALP 1993: Automata, Languages and Programming, Lund, Sweden, 5–9 July 1993. [Google Scholar]

- Lockett, N. Legal perspectives on digital money in Europe. Eur. Bus. Rev. 1999, 99, 235–241. [Google Scholar] [CrossRef]

- Al-Laham, M.; Al-Tarawneh, H.; Abdallat, N. Development of electronic money and its impact on the central bank role and monetary policy. Issues Inf. Sci. Inf. Technol. 2009, 6, 339–349. [Google Scholar]

- Shoaib, M.; Ilyas, M.; Khiyal, M.S.H. Official digital currency. In Proceedings of the Eighth International Conference on Digital Information Management (ICDIM 2013), Islamabad, Pakistan, 10–12 September 2013. [Google Scholar]

- Mckinney, R.E., Jr.; Shao, L.P.; Rosenlieb, D.C., Jr.; Shao, D.H. Counterfeiting in cryptocurrency: An emerging problem. In Handbook of Digital Currency; Academic Press: Cambridge, MA, USA, 2015; pp. 173–187. [Google Scholar]

- Crosby, M.; Pattanayak, P.; Verma, S.; Kalyanaraman, V. Blockchain technology: Beyond bitcoin. Appl. Innov. 2016, 2, 6–10. [Google Scholar]

- Velde, F. Bitcoin: A Primer. 2013. Available online: https://www.chicagofed.org/publications/chicago-fed-letter/2013/december-317 (accessed on 11 April 2022).

- McCullagh, A.; Caelli, W. Non-Repudiation in the Digital Environment. 2000. Available online: https://firstmonday.org/ojs/index.php/fm/article/download/778/687?inline=1 (accessed on 11 April 2022).

- Coffey, T.; Saidha, P. Non-repudiation with mandatory proof of receipt. ACM SIGCOMM Comput. Commun. Rev. 1996, 26, 6–17. [Google Scholar] [CrossRef]

- Zhou, J.; Gollmann, D. A fair non-repudiation protocol. In Proceedings of the 1996 IEEE Symposium on Security and Privacy (IEEE), Oakland, CA, USA, 6–8 May 1996. [Google Scholar]

- Zhang, N.; Shi, Q. Achieving non-repudiation of receipt. Comput. J. 1996, 39, 844–853. [Google Scholar] [CrossRef]

- Kremer, S.; Markowitch, O.; Zhou, J. An intensive survey of fair non-repudiation protocols. Comput. Commun. 2002, 25, 1606–1621. [Google Scholar] [CrossRef]

- Nakamoto, S.; Bitcoin, A. Bitcoin: A Peer-to-Peer Electronic Cash System. Decentralized Bus. Rev. 2008, 21260. [Google Scholar]

- Message Digests and Digital Signatures. Available online: https://www.ibm.com/docs/en/ibm-mq/7.5?topic=concepts-message-digests (accessed on 11 April 2022).

- Robinson, P. The merits of using ethereum mainnet as a coordination blockchain for ethereum private sidechains. Knowl. Eng. Rev. 2020, 35, e30. [Google Scholar] [CrossRef]

- Security of a CBDC. Available online: https://www.bankofcanada.ca/2020/06/staff-analytical-note-2020-11/ (accessed on 11 April 2022).

- Payeras-Capellà, M.M.; Ferrer-Gomila, J.L.; Huguet-Rotger, L. Anonymous payment in a fair e-commerce protocol with verifiable TTP. In Proceedings of the International Conference on Trust, Privacy and Security in Digital Business, Copenhagen, Denmark, 22–26 August 2005; Springer: Berlin/Heidelberg, Germany, 2005. [Google Scholar]

- Seo, M.; Kim, K. Electronic funds transfer protocol using domain-verifiable signcryption scheme. In Proceedings of the International Conference on Information Security and Cryptology, Seoul, Korea, 9–10 December 1999; Springer: Berlin/Heidelberg, Germany, 1999. [Google Scholar]

- Dorsala, M.R.; Sastry, V.N.; Chapram, S. Fair Protocols for Verifiable Computations Using Bitcoin and Ethereum. In Proceedings of the 2018 IEEE 11th International Conference on Cloud Computing (CLOUD), San Francisco, CA, USA, 2–8 July 2018. [Google Scholar]

- Sánchez, D.C. Raziel: Private and verifiable smart contracts on blockchains. arXiv 2018, arXiv:1807.09484 2018. [Google Scholar]

- Everything You Need to Know about Central Bank Digital Currencies (CBDCs) and What It Means for Financial Institutions. Available online: https://ripjar.com/cbdcs-central-bank-digital-currencies/ (accessed on 4 April 2022).

- Benshalom, I. Taxing Cash. Columbia J. Tax Law 2012, 4, 65. Available online: https://heinonline.org/HOL/LandingPage?handle=hein.journals/colujoutl4&div=4&id=&page= (accessed on 11 April 2022).

- Camenisch, J.; Maurer, U.; Stadler, M. Digital payment systems with passive anonymity-revoking trustees. J. Comput. Secur. 1997, 5, 69–89. [Google Scholar] [CrossRef]

- Möser, M. Anonymity of Bitcoin Transactions. In Proceedings of the Münster Bitcoin Conference, Münster, Germany, 17–18 July 2013. [Google Scholar]

- Reid, F.; Harrigan, M. An analysis of anonymity in the bitcoin system. In Security and Privacy in Social Networks; Springer: New York, NY, USA, 2013; pp. 197–223. [Google Scholar]

- Exploring Anonymity in Central Bank Digital Currencies. Available online: https://www.ecb.europa.eu/home/html/index.en.html (accessed on 4 April 2022).

- Mirkovic, J.; Reiher, P. A taxonomy of DDoS attack and DDoS defense mechanisms. ACM SIGCOMM Comput. Commun. Rev. 2004, 34, 39–53. [Google Scholar] [CrossRef]

- Urs, B.A. Security issues and solutions in e-payment systems. Fiat Iustitia 2015, 1, 172–179. [Google Scholar]

- Wang, B.; Zheng, Y.; Lou, W.; Hou, Y.T. DDoS attack protection in the era of cloud computing and software-defined networking. Comput. Netw. 2015, 81, 308–319. [Google Scholar] [CrossRef]

- Dwivedi, A.; Dwivedi, A.; Kumar, S.; Pandey, S.K.; Dabra, P. A cryptographic algorithm analysis for security threats of Semantic E-Commerce Web (SECW) for electronic payment transaction system. In Advances in Computing and Information Technology; Springer: Berlin/Heidelberg, Germany, 2013; pp. 367–379. [Google Scholar]

- Huang, Y.; Geng, X.; Whinston, A.B. Defeating DDoS attacks by fixing the incentive chain. ACM Trans. Internet Technol. (TOIT) 2007, 7, 5–es. [Google Scholar] [CrossRef]

- Douligeris, C.; Mitrokotsa, A. DDoS attacks and defense mechanisms: Classification and state-of-the-art. Comput. Netw. 2004, 44, 643–666. [Google Scholar] [CrossRef]

- Mankins, D.; Krishnan, R.; Boyd, C.; Zao, J.; Frentz, M. Mitigating distributed denial of service attacks with dynamic resource pricing. In Proceedings of the Seventeenth Annual Computer Security Applications Conference (IEEE), New Orleans, LA, USA, 10–14 December 2001. [Google Scholar]

- Johnson, B.; Laszka, A.; Grossklags, J.; Vasek, M.; Moore, T. Game-theoretic analysis of DDoS attacks against Bitcoin mining pools. In Proceedings of the International Conference on Financial Cryptography and Data Security, Christ Church, Barbados, 3–7 March 2014; Springer: Berlin/Heidelberg, Germany, 2014. [Google Scholar]

- Wu, S.; Chen, Y.; Li, M.; Luo, X.; Liu, Z.; Liu, L. Survive and thrive: A stochastic game for ddos attacks in bitcoin mining pools. IEEE/ACM Trans. Netw. 2020, 28, 874–887. [Google Scholar] [CrossRef]

- 4 Key Cybersecurity Threats to New Central Bank Digital Currencies. Available online: https://www.weforum.org/agenda/2021/11/4-key-threats-central-bank-digital-currencies/ (accessed on 4 April 2022).

- Abrazhevich, D. Classification and characteristics of electronic payment systems. In Proceedings of the International Conference on Electronic Commerce and Web Technologies, Munich, Germany, 4–6 September 2001; Springer: Berlin/Heidelberg, Germany, 2001. [Google Scholar]

- Chaum, D.; Brands, S. Minting electronic cash. IEEE Spectr. 1997, 34, 30–34. [Google Scholar] [CrossRef]

- Eslami, Z.; Talebi, M. A new untraceable off-line electronic cash system. Electron. Commer. Res. Appl. 2011, 10, 59–66. [Google Scholar] [CrossRef]

- Wang, C.; Sun, H.; Zhang, H.; Jin, Z. An improved off-line electronic cash. In Proceedings of the International Conference on Computational and Information Sciences (IEEE), Shiyang, China, 21–23 June 2013. [Google Scholar]

- Van Damme, G.; Wouters, K.M.; Karahan, H.; Preneel, B. Offline NFC payments with electronic vouchers. In Proceedings of the 1st ACM Workshop on Networking, Systems, and Applications for Mobile Handhelds, Barcelona, Spain, 17 August 2009. [Google Scholar]

- Nigeria’s OyaPay Now Integrates the Use of Bluetooth and QR Payments for Offline Use. Available online: https://innov8tiv.com/nigerias-oyapay-now-integrates-the-use-of-bluetooth-and-qr-payments-for-offline-use/ (accessed on 4 April 2022).

- Visa Proposes CBDC Protocol That Lets Consumers Exchange Digital Cash via Bluetooth or NFC. Available online: https://www.nfcw.com/2020/12/18/369783/visa-proposes-cbdc-protocol-that-lets-consumers-exchange-digital-cash-via-bluetooth-or-nfc/ (accessed on 4 April 2022).

- Dmitrienko, A.; Noack, D.; Yung, M. Secure Wallet-Assisted Offline Bitcoin Payments with Double-Spender Revocation. In Proceedings of the 2017 ACM on Asia Conference on Computer and Communications Security (ASIA CCS ’17), Abu Dhabi, United Arab Emirates, 2–6 April 2017. [Google Scholar]

- China DC/EP Research and Perspectives of CBDC in Japan. Available online: https://www.nri.com/en/knowledge/publication/fis/special/lst/2020/07/07 (accessed on 31 January 2022).

- Christodorescu, M.; Gu, W.C.; Kumaresan, R.; Minaei, M.; Ozdayi, M.; Price, B.; Raghuraman, S.; Saad, M.; Sheffield, C.; Xu, M.; et al. Towards a Two-Tier Hierarchical Infrastructure: An Offline Payment System for Central Bank Digital Currencies. arXiv 2012, arXiv:2012.08003. [Google Scholar]

- Wiseman, S.A. Property or currency: The tax dilemma behind Bitcoin. Utah Law Rev. 2016, 417. Available online: https://heinonline.org/HOL/LandingPage?handle=hein.journals/utahlr2016&div=15&id=&page= (accessed on 11 April 2022).

- Central Bank Digital Currency and the Future: Visa Publishes New Research. Available online: https://usa.visa.com/visa-everywhere/blog/bdp/2020/12/17/central-bank-digital-1608165518834.html (accessed on 4 April 2022).

- Sabt, M.; Achemlal, M.; Bouabdallah, A. Trusted execution environment: What it is, and what it is not. In Proceedings of the 2015 IEEE Trustcom/BigDataSE/ISPA, Washington, DC, USA, 20–22 August 2015. [Google Scholar]

- McGillion, B.; Dettenborn, T.; Nyman, T.; Asokan, N. Open-TEE—An open virtual trusted execution environment. In Proceedings of the 2015 IEEE Trustcom/BigDataSE/ISPA, Washington, DC, USA, 20–22 August 2015. [Google Scholar]

- Jang, J.S.; Kong, S.; Kim, M.; Kim, D.; Kang, B.B. Secret: Secure channel between rich execution environment and trusted execution environment. In Proceedings of the NDSS, San Diego, CA, USA, 8–11 February 2015. [Google Scholar]

- Busch, M.; Westphal, J.; Müller, T. Unearthing the {TrustedCore}: A Critical Review on {Huawei’s} Trusted Execution Environment. In Proceedings of the 14th USENIX Workshop on Offensive Technologies (WOOT 20), Boston, MA, USA, 10–11 August 2020. [Google Scholar]

- Weise, J. Public Key Infrastructure Overview; Sun BluePrints OnLine: Palo Alto, CA, USA, 2001; pp. 1–27. [Google Scholar]

- Distributed Ledger Technology: Current Situation and Major Issues. Available online: https://www.bok.or.kr/viewer/skin/doc.html?fn=FILE_201803300855017061.pdf&rs=/webview/result/E0000654/201701 (accessed on 4 April 2022).

- Execution is the Key to Success of CBDC Using Blockchain and DLT. Available online: https://www.thehindubusinessline.com/opinion/execution-is-the-key-to-success-of-cbdc-using-blockchain-and-dlt/article65207913.ece#comments_65207913 (accessed on 4 April 2022).

- Bank of Korea Opens Bidding for CBDC DLT Technology Provider. Available online: https://www.ledgerinsights.com/bank-of-korea-opens-bidding-for-cbdc-dlt-technology-provider-won/ (accessed on 4 April 2022).

- World Bank. Central Band Digital Currencies for Cross-Border Payments: A Review of Current Experiments and Ideas; World Bank: Washington, DC, USA, 2021. [Google Scholar]

- World Economic Forum. Privacy and Confidentiality Options for Central Bank Digital Currency; World Economic Forum: Cologny, Switzerland, 2021. [Google Scholar]

- Are Central Bank Digital Currencies (CBDCs) the Money of Tomorrow? Available online: https://www2.deloitte.com/ie/en/pages/financial-services/articles/central-bank-digital-currencies-money-tomorrow.html (accessed on 4 April 2022).

- Löber, K.; Houben, A. Committee on Payments and Market Infrastructures Markets Committee; Bank for International Settlements: Basel, Switzerland, 2018. [Google Scholar]

- Riksbank: DLT Tokens Don’t Provide Cash-Like CBDC Benefits. Available online: https://www.ledgerinsights.com/riksbank-dlt-tokens-dont-provide-cash-like-cbdc-benefts/ (accessed on 4 April 2022).

- Richards, T.; Thompson, C.; Dark, C. Retail central bank digital currency: Design considerations, rationales and implications. In 1. 1 Managing the Risks of Holding Self-Securitisations as Collateral 2. 11 Government Bond Market Functioning and COVID-19 3. The Economic Effects of Low Interest Rates and Unconventional 21 Monetary Policy 4. Retail Central Bank Digital Currency: Design Considerations, Rationales; Australia; 2020. Available online: https://www.rba.gov.au/publications/bulletin/2020/sep/pdf/bulletin-2020-09.pdf#page=35 (accessed on 4 April 2022).

- Central Bank Digital Currencies: System Design and Interoperability. Available online: https://www.bis.org/publ/othp42.htm (accessed on 11 April 2022).

- Offline Payments Eliminate the Risk of Disruptions and Downtime. Available online: https://www.crunchfish.com/offline-payments-eliminate-the-risk-of-disruptions-and-downtime/ (accessed on 11 April 2022).

- CBDC Technology Considerations. Available online: https://www.weforum.org/reports/digital-currency-governance-consortium-white-paper-series/cbdc-tech-considerations (accessed on 11 April 2022).

- CBDC-Powered Offline Payment Systems—A True Rival to Cryptocurrencies? Available online: https://rafaelbelchior.medium.com/cbdc-powered-offline-payment-systems-a-true-rival-to-cryptocurrencies-38d13b5d3767 (accessed on 11 April 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| CBDCs in Use Worldwide | Types | Reasons |

|---|---|---|

| Sand Dollar (The Bahamas) | Single ledger | No external organizations are involved in managing the ledger. |

| Direct | The central bank provides financial services directly. | |

| SOV (Republic of the Marshall Islands) | Single ledger | No external organizations are involved in managing the ledger. |

| Direct | The central bank provides financial services directly. | |

| eNaira (Nigeria) | Single ledger | The central bank directly manages the ledger. |

| Direct | The central bank provides financial services directly. | |

| E-CNY (China) | Single ledger | The central bank directly manages the ledger. |

| Indirect | Commercial and private banks are designated as operating institutions to provide financial services. | |

| Bakong (Cambodia) | Distributed ledger | Operated using the Iroha blockchain, which is based on Hyperledger. |

| Permissioned | Iroha uses a permissioned blockchain. | |

| Indirect | Various digital banks provide financial services. |

| No Double Spending | Unforgeability | Non-Repudiation | Verifiability | Anonymity | DDoS Attack Prevention | |

|---|---|---|---|---|---|---|

| Camenisch et al. [72] | O | X | X | O | O | X |

| Dmitrienko et al. [93] | O | O | X | X | X | X |

| Christodorescu et al. [95] | O | X | O | O | O | X |

| Security Enhancement Plan | Research | Security Requirements | Detail |

|---|---|---|---|

| Blockchain technology | Savolainen and Soria [45] | No double spending | Prevention of double spending through proof of work (A method for users to check whether the transaction is true or false). * Not applicable when an attacker has over 50% of hashing power. |

| Crosby et al. [55] | Unforgeability | Transparency to the supply chain through BlockVerify using blockchain’s distributed ledger technology and security. | |

| Velde [56] | Unforgeability | Solution for issues over counterfeiting currency with proof of work. | |

| Nakamoto [62] | Non-repudiation | Proposal of methodology difficult to maliciously modify and delete Bitcoin’s transaction history recorded in a blockchain. | |

| Dorsala et al. [68] | Verifiability | Methods to cut off the possibility of a fraudulent act within a transaction by saving all trade conducted in a network on a block. | |

| Reid and Harrigan [74] | Anonymity | Reinforcement of user anonymity by creating only the necessary numbers of the public key for each user. | |

| Trusted third party | Karame et al. [46] | No double spending | Monitoring double spending by adopting the “inserting observers” method to solve problems caused by Bitcoin’s fast payment. |

| Payeras-Capellà et al. [66] | Verifiability | Introduction of a trusted third party, who becomes directly involved when there is inappropriate behavior within the transaction. | |

| Certification of the transaction members | Krsul et al. [43] | No double spending | Proposal of the transaction system, tolerating the transactions for the buyer and seller with only the serial numbers matching. |

| Kremer et al. [61] | Non-repudiation | Proposal of the transaction system tolerating the entities capable of NRE formulation and the system issuing non-repudiation of receipt to the payer and original non-repudiation receipt to the payee. | |

| Tracking of transaction records | Brands [42] | No double spending | Improvement of the security system for the traceability history of e-cash trade, examining one-show blind signatures and wallets with the observer’s method. |

| Camenisch et al. [72] | Anonymity | Suggestions on the improvement of the system tracking the user, using anonymity revocation when irrelevant behavior within the e-cash system is detected. | |

| Cryptographic techniques | Pointcheval and Stern [44] | No double spending | Proposal of the cryptographic technique for the users to use a blind RSA signature to prevent double spending. |

| Seo and Kim [67] | Verifiability | Suggestion for the improvement of cryptographic technique considering the transaction security, utilizing the domain-verifiable signcryption scheme that only gives a predetermined n number of EFT protocol participants access to check the transaction. | |

| Robinson [64] | Non-repudiation | Proposal of the security system with Keccak-256 and a hash value to prevent malicious changes during the transaction process in block contents. | |

| Sánchez [69] | Verifiability | Improvement of the security system for the transaction process with a combination of MPC protocol and ZKP to guarantee verifiability without revealing personal information. | |

| Möser [73] | Anonymity | Proposal of the system creating an environment with a pseudonym via Ethereum’s hash value address that hides personal information in the pseudonymity. |

| Variable | Definition | Function |

|---|---|---|

| T.i | A counter in a device | A variable that increases by 1 when a withdraw protocol or deposit protocol occurs, indicating how many times both protocols have progressed. |

| S.i | A counter in a server | A variable that increases by 1 when a withdraw protocol or deposit protocol occurs along with T.i. |

| T.bal | Account balance of a device | The amount of money the offline payment device holds to make a transaction. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chu, Y.; Lee, J.; Kim, S.; Kim, H.; Yoon, Y.; Chung, H. Review of Offline Payment Function of CBDC Considering Security Requirements. Appl. Sci. 2022, 12, 4488. https://doi.org/10.3390/app12094488

Chu Y, Lee J, Kim S, Kim H, Yoon Y, Chung H. Review of Offline Payment Function of CBDC Considering Security Requirements. Applied Sciences. 2022; 12(9):4488. https://doi.org/10.3390/app12094488

Chicago/Turabian StyleChu, Yeonouk, Jaeho Lee, Sungjoong Kim, Hyunjoong Kim, Yongtae Yoon, and Hyeyoung Chung. 2022. "Review of Offline Payment Function of CBDC Considering Security Requirements" Applied Sciences 12, no. 9: 4488. https://doi.org/10.3390/app12094488

APA StyleChu, Y., Lee, J., Kim, S., Kim, H., Yoon, Y., & Chung, H. (2022). Review of Offline Payment Function of CBDC Considering Security Requirements. Applied Sciences, 12(9), 4488. https://doi.org/10.3390/app12094488