Assessing Financial Literacy and Farmland Abandonment Relationship in Ghana

, and

, and

Abstract

:1. Introduction

2. Theoretical Analysis

3. Why Ghana?

4. Methodology

4.1. Source of Data and Key Variables Definitions

4.2. Empirical Model

5. Results and Discussions

5.1. Descriptive Statistics

5.2. Empirical Analysis

5.2.1. Determinants of Financial Literacy

5.2.2. Financial Literacy and Farmland Abandonment Association Estimate

5.2.3. Additional Estimates

6. Conclusions, Policy Implications, and Limitations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Question | Answers |

|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Variables | First Stage Selection Equation | Second Stage Farmland Abandonment Equation | |

|---|---|---|---|

| Financially Literate | Financially Literate | Financially Illiterate | |

| Gender | 0.024 (0.010) * | 0.036 (0.018) * | 0.061 (0.076) |

| Age | 0.172 (0.263) | −0.097 (0.046) * | −0.043 (0.067) |

| Education | 0.291 (0.075) *** | 0.003 (0.000) ** | 0.011 (0.018) |

| Self-reported health | 0.016 (0.086) | −0.055 (0.027) * | −0.113 (0.107) |

| Household Dependency ratio | −0.039 (0.055) | −0.086 (0.220) | 0.063 (0.031) * |

| Family size | 0.066 (0.049) | −0.006 (0.009) | −0.056 (0.024) * |

| Smartphone use | 0.078 (0.027) ** | 0.048 (0.022) * | 0.145 (0.177) |

| Mechanization | 0.044 (0.091) | −0.086 (0.030) ** | −0.064 (0.014) *** |

| FBOs membership | 0.051 (0.080) | −0.079 (0.041) | −0.060 (0.013) *** |

| Credit constraint | 0.096 (0.047) * | 0.033 (0.112) | 0.095 (0.011) *** |

| Land size | −0.029 (0.115) | 0.042 (0.017) ** | 0.011 (0.007) |

| Land registration | 0.088 (0.030) | 0.021 (0.059) | 0.061 (0.045) * |

| Financial education (IV) | 0.183 (0.017) *** | ||

| Residual (smartphone use) | 0.155 (0.429) | 0.063 (0.056) | 0.018 (0.069) |

| Constant | 1.272 (0.630) * | 3.261 (1.282) ** | 1.774 (0.708) ** |

| Regional dummies | Yes | Yes | Yes |

| 0.170 (0.147) | |||

| 0.613 (0.451) | |||

| 0.072 (0.019) *** | |||

| −0.032 (0.113) | |||

| LR test of indep. eqns.: 4.26 **; Log likelihood = −887.839; Observations = 572 | |||

| Variables | Correlation Coefficient | p-Value |

|---|---|---|

| Financial literacy | 0.049 ** | 0.016 |

| RE adoption | 0.186 | 0.112 |

References

- Lambin, E.F.; Meyfroidt, P. Global land use change, economic globalization, and the looming land scarcity. Proc. Natl. Acad. Sci. USA 2011, 108, 3465–3472. [Google Scholar] [CrossRef] [Green Version]

- Benayas, J.M.R.; Martins, A.; Nicolau, J.M.; Schulz, J.J. Abandonment of agricultural land: An overview of drivers and consequences. CAB Rev. Perspect. Agric. Vet. Sci. Nutr. Nat. Resour. 2007, 2, 57. [Google Scholar] [CrossRef] [Green Version]

- Sileika, A.S.; Stålnacke, P.; Kutra, S.; Gaigalis, K.; Berankiene, L. Temporal and spatial variation of nutrient levels in the Nemunas River (Lithuania and Belarus). Environ. Monit. Assess. 2006, 122, 335–354. [Google Scholar] [CrossRef]

- Viana, C.M.; Freire, D.; Abrantes, P.; Rocha, J.; Pereira, P. Agricultural land systems importance for supporting food security and sustainable development goals: A systematic review. Sci. Total Environ. 2022, 806, 150718. [Google Scholar] [CrossRef]

- Wang, X.; Shao, S.; Li, L. Agricultural inputs, urbanization, and urban-rural income disparity: Evidence from China. China Econ. Rev. 2019, 55, 67–84. [Google Scholar] [CrossRef]

- Zhou, T.; Koomen, E.; Ke, X. Determinants of Farmland Abandonment on the Urban–Rural Fringe. Environ. Manag. 2020, 65, 369–384. [Google Scholar] [CrossRef] [Green Version]

- Blair, D.; Shackleton, C.M.; Mograbi, P.J. Cropland abandonment in South African smallholder communal lands: Land cover change (1950–2010) and farmer perceptions of contributing factors. Land 2018, 7, 121. [Google Scholar] [CrossRef] [Green Version]

- Ankrah Twumasi, M.; Jiang, Y.; Ntiamoah, E.B.; Akaba, S.; Darfor, K.N.; Boateng, L.K. Access to credit and farmland abandonment nexus: The case of rural Ghana. Nat. Resour. Forum 2021, 46, 3–20. [Google Scholar] [CrossRef]

- Gellrich, M.; Baur, P.; Koch, B.; Zimmermann, N.E. Agricultural land abandonment and natural forest re-growth in the Swiss mountains: A spatially explicit economic analysis. Agric. Ecosyst. Environ. 2007, 118, 93–108. [Google Scholar] [CrossRef]

- Prishchepov, A.A.; Müller, D.; Dubinin, M.; Baumann, M.; Radeloff, V.C. Determinants of agricultural land abandonment in post-Soviet European Russia. Land Use Policy 2013, 30, 873–884. [Google Scholar] [CrossRef] [Green Version]

- Li, H.; Song, W. Cropland abandonment and influencing factors in Chongqing, china. Land 2021, 10, 1206. [Google Scholar] [CrossRef]

- Díaz, G.I.; Nahuelhual, L.; Echeverría, C.; Marín, S. Drivers of land abandonment in Southern Chile and implications for landscape planning. Landsc. Urban Plan. 2011, 99, 207–217. [Google Scholar] [CrossRef]

- Deng, X.; Xu, D.; Qi, Y.; Zeng, M. Labor Off-Farm Employment and Cropland Abandonment in Rural China: Spatial Distribution and Empirical Analysis. Int. J. Environ. Res. Public Health 2018, 15, 1808. [Google Scholar] [CrossRef] [Green Version]

- Xu, D.; Deng, X.; Guo, S.; Liu, S. Labor migration and farmland abandonment in rural China: Empirical results and policy implications. J. Environ. Manag. 2019, 232, 738–750. [Google Scholar] [CrossRef]

- Ankrah Twumasi, M.; Zheng, H.; Asiedu-Ayeh, L.O.; Siaw, A.; Jiang, Y. Access to Financial Services and Its Impact on Household Income: Evidence from Rural Ghana. Eur. J. Dev. Res. 2022, 1–22. [Google Scholar] [CrossRef]

- Lahiani, A.; Mefteh-Wali, S.; Shahbaz, M.; Vo, X.V. Does financial development influence renewable energy consumption to achieve carbon neutrality in the USA? Energy Policy 2021, 158, 112524. [Google Scholar] [CrossRef]

- Ankrah Twumasi, M.; Asante, D.; Asante, I.O.; Addai, B.; Jiang, Y. Assessing fish farm economic performance and access to financial services nexus: Empirical evidence from Ghana. Aquac. Econ. Manag. 2022, 1–18. [Google Scholar] [CrossRef]

- Du, J.; Zeng, M.; Xie, Z.; Wang, S. Power of Agricultural Credit in Farmland Abandonment: Evidence from Rural China. Land 2019, 8, 184. [Google Scholar] [CrossRef] [Green Version]

- Lefebvre, M.; Nikolov, D.; Gomez-y-Paloma, S.; Chopeva, M. Determinants of insurance adoption among Bulgarian farmers. Agric. Financ. Rev. 2014, 74, 326–347. [Google Scholar] [CrossRef]

- Gao, Y.; Shu, Y.; Cao, H.; Zhou, S.; Shi, S. Fiscal policy dilemma in resolving agricultural risks: Evidence from China’s agricultural insurance subsidy pilot. Int. J. Environ. Res. Public Health 2021, 18, 7577. [Google Scholar] [CrossRef]

- Pan, J. Financial support and the development of agricultural mechanization in China. J. Adv. Oxid. Technol. 2018, 21, 1–15. [Google Scholar]

- Zheng, H.; Ma, W.; Zhou, X. Renting-in cropland, machinery use intensity, and land productivity in rural China. Appl. Econ. 2021, 53, 5503–5517. [Google Scholar] [CrossRef]

- Lusardi, A.; Tufano, P. Debt literacy, financial experiences, and overindebtedness. J. Pension Econ. Financ. 2015, 14, 332–368. [Google Scholar] [CrossRef] [Green Version]

- Xu, N.; Shi, J.; Rong, Z.; Yuan, Y. Financial literacy and formal credit accessibility: Evidence from informal businesses in China. Financ. Res. Lett. 2019, 36, 101327. [Google Scholar] [CrossRef]

- Ankrah Twumasi, M.; Jiang, Y.; Wang, P.; Ding, Z.; Frempong, L.N.; Acheampong, M.O. Does financial literacy inevitably lead to access to finance services? Evidence from rural Ghana. Ciência Rural 2022, 52, 1–16. [Google Scholar] [CrossRef]

- Klapper, L.; Lusardi, A. Financial literacy and financial resilience: Evidence from around the world. Financ. Manag. 2020, 49, 589–614. [Google Scholar] [CrossRef]

- Ankrah Twumasi, M.; Asante, D.; Fosu, P.; Essilfie, G.; Jiang, Y. Residential renewable energy adoption. Does financial literacy matter? J. Clean. Prod. 2022, 361, 132210. [Google Scholar] [CrossRef]

- Askar, M.W.; Quattara, B. Financial Literacy and Poverty Reduction: The Case of Indonesia. Ikonomika 2020, 2, 1–16. [Google Scholar]

- Akoto, G.O.; Appiah, K.O.; Turkson, J.K. Financial literacy of cocoa farmers in Ghana. Int. J. Account. Financ. 2017, 7, 11. [Google Scholar] [CrossRef]

- Ellis, E. Willingness to Pay for Index Based Crop Insurance in Ghana. Asian Econ. Financ. Rev. 2017, 7, 700–721. [Google Scholar] [CrossRef] [Green Version]

- Wang, M.; Ye, T.; Shi, P. Factors Affecting Farmers’ Crop Insurance Participation in China. Can. J. Agric. Econ. 2016, 64, 479–492. [Google Scholar] [CrossRef]

- Su, G.; Okahashi, H.; Chen, L. Spatial pattern of farmland abandonment in Japan: Identification and determinants. Sustainability 2018, 10, 3676. [Google Scholar] [CrossRef] [Green Version]

- Li, S.; Li, X. Global understanding of farmland abandonment: A review and prospects. J. Geogr. Sci. 2017, 27, 1123–1150. [Google Scholar] [CrossRef]

- Renwick, A.; Jansson, T.; Verburg, P.H.; Revoredo-Giha, C.; Britz, W.; Gocht, A.; McCracken, D. Policy reform and agricultural land abandonment in the EU. Land Use Policy 2013, 30, 446–457. [Google Scholar] [CrossRef]

- Huffman, W.E. Agricultural household models: Survey and critique. In Multiple Job-Holding among Farm Families; Iowa State University Press: Ames, IA, USA, 1991. [Google Scholar]

- Ankrah Twumasi, M.; Jiang, Y.; Ding, Z.; Wang, P.; Abgenyo, W. The Mediating Role of Access to Financial Services in the Effect of Financial Literacy on Household Income: The Case of Rural Ghana. SAGE Open 2022, 12, 1–13. [Google Scholar] [CrossRef]

- Martey, E.; Wiredu, A.N.; Etwire, P.M.; Kuwornu, J.K.M. The impact of credit on the technical efficiency of maize-producing households in Northern Ghana. Agric. Financ. Rev. 2019, 79, 304–322. [Google Scholar] [CrossRef] [Green Version]

- Bonjean, I. Heterogeneous incentives for innovation adoption: The price effect on segmented markets. Food Policy 2019, 87, 101741. [Google Scholar] [CrossRef]

- Nwafor, C.U.; Ogundeji, A.A.; van der Westhuizen, C. Adoption of ICT-based information sources and market participation among smallholder livestock farmers in South Africa. Agriculture 2020, 10, 44. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, A.; Mitchell, O.S. The Economic Importance of Financial Literacy: Theory and Evidence. J. Econ. Lit. 2014, 52, 5–44. [Google Scholar] [CrossRef] [Green Version]

- Han, L.; Fraser, S.; Storey, D.J. Are good or bad borrowers discouraged from applying for loans? Evidence from US small business credit markets. J. Bank. Financ. 2009, 33, 415–424. [Google Scholar] [CrossRef]

- Watanapongvanich, S.; Khan, M.S.R.; Putthinun, P.; Ono, S.; Kadoya, Y. Financial Literacy and Gambling Behavior in the United States. J. Gambl. Stud. 2021, 38, 445–463. [Google Scholar] [CrossRef]

- Morgan, P.J.; Long, T.Q. Financial literacy, financial inclusion, and savings behavior in Laos. J. Asian Econ. 2020, 68, 101197. [Google Scholar] [CrossRef]

- Ankrah Twumasi, M.; Jiang, Y.; Adhikari, S.; Adu Gyamfi, C.; Asare, I. Financial literacy and its determinants: The case of rural farm households in Ghana. Agric. Financ. Rev. 2022, 82, 641–656. [Google Scholar] [CrossRef]

- Klapper, L.; Lusardi, A.; Van Oudheusden, P. Financial Literacy around the World: Insights from the S&P Global FinLit Survey; World Bank: Washington, DC, USA, 2015; pp. 1–27. [Google Scholar]

- Atakora, A. Measuring the Effectiveness of Financial Literacy Programs in Ghana. Int. J. Manag. Bus. Res. 2016, 3, 135–148. [Google Scholar]

- Koomson, I.; Villano, R.A.; Hadley, D. The role of financial literacy in households’ asset accumulation process: Evidence from Ghana. Rev. Econ. Househ. 2022, 1–24. [Google Scholar] [CrossRef]

- Chowa, G.; Despard, M.; Osei-Akoto, I. Financial knowledge and attitudes of youths in Ghana. YouthSave Res. Br. 2012, 12, 1–7. [Google Scholar]

- Ministry of Food and Agriculture. Facts and Figures; Ministry of Food and Agriculture: Accra, Ghana, 2015.

- Andoh, F.K.; Nunoo, J.; Darfor, K.N. Sustaining Small and Medium Enterprises through Financial Service Utilization: Does Financial Literacy Matter? J. Bus. Entrep. Dev. 2015, 5, 74–94. [Google Scholar] [CrossRef]

- Niu, G.; Zhou, Y. Financial literacy and retirement planning: Evidence from China. Appl. Econ. Lett. 2018, 25, 619–623. [Google Scholar] [CrossRef]

- Deng, X.; Zeng, M.; Xu, D.; Wei, F.; Qi, Y. Household Health and Cropland Abandonment in Rural China: Theoretical Mechanism and Empirical Evidence. Int. J. Environ. Res. Public Health 2019, 16, 3588. [Google Scholar] [CrossRef] [Green Version]

- Murendo, C.; Mutsonziwa, K. Financial literacy and savings decisions by adult financial consumers in Zimbabwe. Int. J. Consum. Stud. 2017, 41, 95–103. [Google Scholar] [CrossRef] [Green Version]

- Ma, W.; Zhu, Z. A Note: Reducing Cropland Abandonment in China—Do Agricultural Cooperatives Play a Role? J. Agric. Econ. 2020, 71, 929–935. [Google Scholar] [CrossRef]

- Zhou, X.; Ma, W. Agricultural mechanization and land productivity in China. Int. J. Sustain. Dev. World Ecol. 2022, 29, 530–542. [Google Scholar] [CrossRef]

- Ma, W.; Nie, P.; Zhang, P.; Renwick, A. Impact of Internet use on economic well-being of rural households: Evidence from China. Rev. Dev. Econ. 2020, 24, 503–523. [Google Scholar] [CrossRef]

- Tesfaye, W.; Tirivayi, N. The impacts of postharvest storage innovations on food security and welfare in Ethiopia. Food Policy 2018, 75, 52–67. [Google Scholar] [CrossRef]

- Ankrah Twumasi, M.; Jiang, Y.; Zhou, X.; Addai, B.; Darfor, K.N.; Akaba, S.; Fosu, P. Increasing Ghanaian fish farms’ productivity: Does the use of the internet matter? Mar. Policy 2021, 125, 104385. [Google Scholar] [CrossRef]

- Ma, W.; Zhu, Z. Internet use and willingness to participate in garbage classification: An investigation of Chinese residents. Appl. Econ. Lett. 2020, 28, 788–793. [Google Scholar] [CrossRef]

- Lokshin, M.; Sajaia, Z. Maximum Likelihood Estimation of Endogenous Switching Regression Models. Stata J. 2004, 4, 282–289. [Google Scholar] [CrossRef] [Green Version]

- Rees, H.; Maddala, G.S. Limited-Dependent and Qualitative Variables in Econometrics. Econ. J. 1985, 95, 493. [Google Scholar] [CrossRef]

- Greene, W.W.H. Econometric Analysis, 7th ed.; Prentice-Hall: Hoboken, NJ, USA, 2012; ISBN 978-0-273-75356-8. [Google Scholar]

- Heckman, J.J. Sample Selection Bias as a Specification Error. Econometrica 1979, 47, 153. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Control function methods in applied econometrics. J. Hum. Resour. 2015, 50, 420–445. [Google Scholar] [CrossRef]

- Bucher-Koenen, T.; Lusardi, A.; Alessie, R.; van Rooij, M. How Financially Literate Are Women? An Overview and New Insights. J. Consum. Aff. 2017, 51, 255–283. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Financial literacy and planning: Implications for retirement wellbeing. In Financial Literacy: Implications for Retirement Security and the Financial Marketplace; NBER: Cambridge, MA, USA, 2013; ISBN 9780199696819. [Google Scholar]

- Khanal, A.R.; Mishra, A.K. Financial performance of small farm business households: The role of internet. China Agric. Econ. Rev. 2016, 8, 553–571. [Google Scholar] [CrossRef]

- Ma, W.; Renwick, A.; Nie, P.; Tang, J.; Cai, R. Off-farm work, smartphone use and household income: Evidence from rural China. China Econ. Rev. 2018, 52, 80–94. [Google Scholar] [CrossRef]

- Van Rooij, M.; Lusardi, A.; Alessie, R. Financial literacy and stock market participation. J. Financ. Econ. 2011, 101, 449–472. [Google Scholar] [CrossRef] [Green Version]

- Wooldridge, J.M. Introductory Econometrics; Cengage Learning: Mason, OH, USA, 2013; ISBN 9780324581621. [Google Scholar]

- Fernandez-Cornejo, J.; Mishra, A.; Nehring, R.; Hendricks, C.; Southern, M.; Gregory, A. Off-Farm Income, Technology Adoption, and Farm Economic Performance; Economic Research Report; Economic Research Service, USDA: Washington, DC, USA, 2007.

- Li, M.; Gan, C.; Ma, W.; Jiang, W. Impact of cash crop cultivation on household income and migration decisions: Evidence from low-income regions in China. J. Integr. Agric. 2020, 19, 2571–2581. [Google Scholar] [CrossRef]

- Saqib, S.E.; Khan, H.; Panezai, S.; Ali, U.; Ali, M. Credit Fungibility and Credit Margin of Investment: The Case of Subsistence Farmers in Khyber Pakhtunkhwa. Sarhad J. Agric. 2017, 33, 661–667. [Google Scholar] [CrossRef]

| Variables | Description | Mean | Std. Dev |

|---|---|---|---|

| Farmland abandonment | Area of cropland abandonment in acres in 2017 | 0.96 | 2.04 |

| Financial literacy | Farmer is financially literate (1 = Yes; 0 = No) | 0.31 | 0.44 |

| Gender | Farmer is a male (1 = Yes; 0 = No) | 0.69 | 0.46 |

| Age | Farmer’s age | 41.66 | 12.20 |

| Education | Farmers’ number of years of education | 5.28 | 4.24 |

| Self-reported health | Farmer’s health status is good (1 = Yes; 0 = No) | 0.43 | 0.51 |

| Household Dependency ratio | Number of older adults (60 years and above) and children below 12 years in the farmer’s family | 3.29 | 1.17 |

| Family size | Number of household size | 6.60 | 3.20 |

| Smartphone use | Farmer uses smartphone (1 = Yes; 0 = No) | 0.29 | 0.33 |

| Mechanization | Farmer used any farming machine (1 = Yes; 0 = No) | 0.35 | 0.42 |

| FBOs membership | Farmer is FBO member (1 = Yes; 0 = No) | 0.41 | 0.49 |

| Credit constraint | Farmer was credit constrained 2017 (1 = Yes; 0 = No) | 0.34 | 0.47 |

| Land size | Total farmland size of the farmer (acres) | 3.85 | 1.74 |

| Land registration | Farmer’s household land is officially registered (1 = Yes; 0 = No) | 0.36 | 19.82 |

| Financial education (IV) | Farmer has a relative/friend with an economics or financial education background (1 = Yes, 0 = No) | 0.27 | 0.35 |

| Northern | Farmer resident is in Northern region (1 = Yes; 0 = No) | 0.18 | 0.37 |

| BA | Farmer resident is in BA region (1 = Yes; 0 = No) | 0.26 | 0.43 |

| Eastern | Whether the farmer resident is in the Eastern region (1 = Yes; 0 = No) | 0.27 | 0.44 |

| Central | Farmer resident is in Central region (1 = Yes; 0 = No) | 0.29 | 0.45 |

| Variable | Literate | Illiterate | Differences (Normalized) |

|---|---|---|---|

| Farmland abandonment | 0.71 | 1.27 | −0.07 ** |

| Gender | 0.77 | 0.63 | 0.11 * |

| Age | 43.75 | 40.52 | 0.09 |

| Education | 7.03 | 3.62 | 0.16 ** |

| Self-reported health | 0.44 | 0.43 | 0.02 |

| Household Dependency ratio | 3.98 | 2.66 | 0.30 |

| Family size | 5.34 | 7.95 | −0.08 |

| Smartphone use | 0.35 | 0.27 | 0.13 * |

| Mechanization | 0.37 | 0.34 | 0.06 |

| FBOs membership | 0.38 | 0.45 | −0.11 |

| Credit constraint | 0.25 | 0.43 | −0.23 *** |

| Land size | 3.12 | 4.63 | 0.29 |

| Land registration | 0.43 | 0.31 | 0.20 * |

| Financial education (IV) | 0.36 | 0.22 | 0.22 ** |

| Observations | 177 | 395 | Total = 572 |

| Variables | Coefficients | Robust Standard Errors |

|---|---|---|

| Gender | 0.024 | 0.010 * |

| Age | 0.172 | 0.263 |

| Education | 0.291 | 0.075 *** |

| Self-reported health | 0.016 | 0.086 |

| Household Dependency ratio | −0.039 | 0.055 |

| Family size | 0.066 | 0.049 |

| Smartphone use | 0.078 | 0.027 ** |

| Mechanization | 0.044 | 0.091 |

| FBOs membership | 0.051 | 0.080 |

| Credit constraint | 0.096 | 0.047 * |

| Land size | −0.029 | 0.115 |

| Land registration | 0.088 | 0.030 |

| Financial education (IV) | 0.183 | 0.017 *** |

| Residual (smartphone use) | 0.155 | 0.429 |

| Constant | 1.272 | 0.630 * |

| Regional dummies | Yes | Yes |

| Observations | 572 |

| Mean Area of Farmland Abandoned (ESR) | Treatment Effect | t-Value | ||

|---|---|---|---|---|

| Financially literate | Financially illiterate | |||

| Financially literate | 0.682 | 1.142 | ATT = −0.460 | −4.19 *** |

| Financially illiterate | 1.105 | 1.328 | ATU = −0.223 | −10.17 *** |

| Heterogeneity effects | −0.423 | −0.186 | −0.237 | ATE = −0.646 |

| Mean area of farmland abandoned PSM a | ||||

| Financially literate | 0.707 | 1.086 | ATT = −0.379 | −2.97 *** |

| Variables | Average Farmland Abandonment | ATTESR | t-Value | Change | ||

|---|---|---|---|---|---|---|

| Financially Literate | Financially Illiterate | |||||

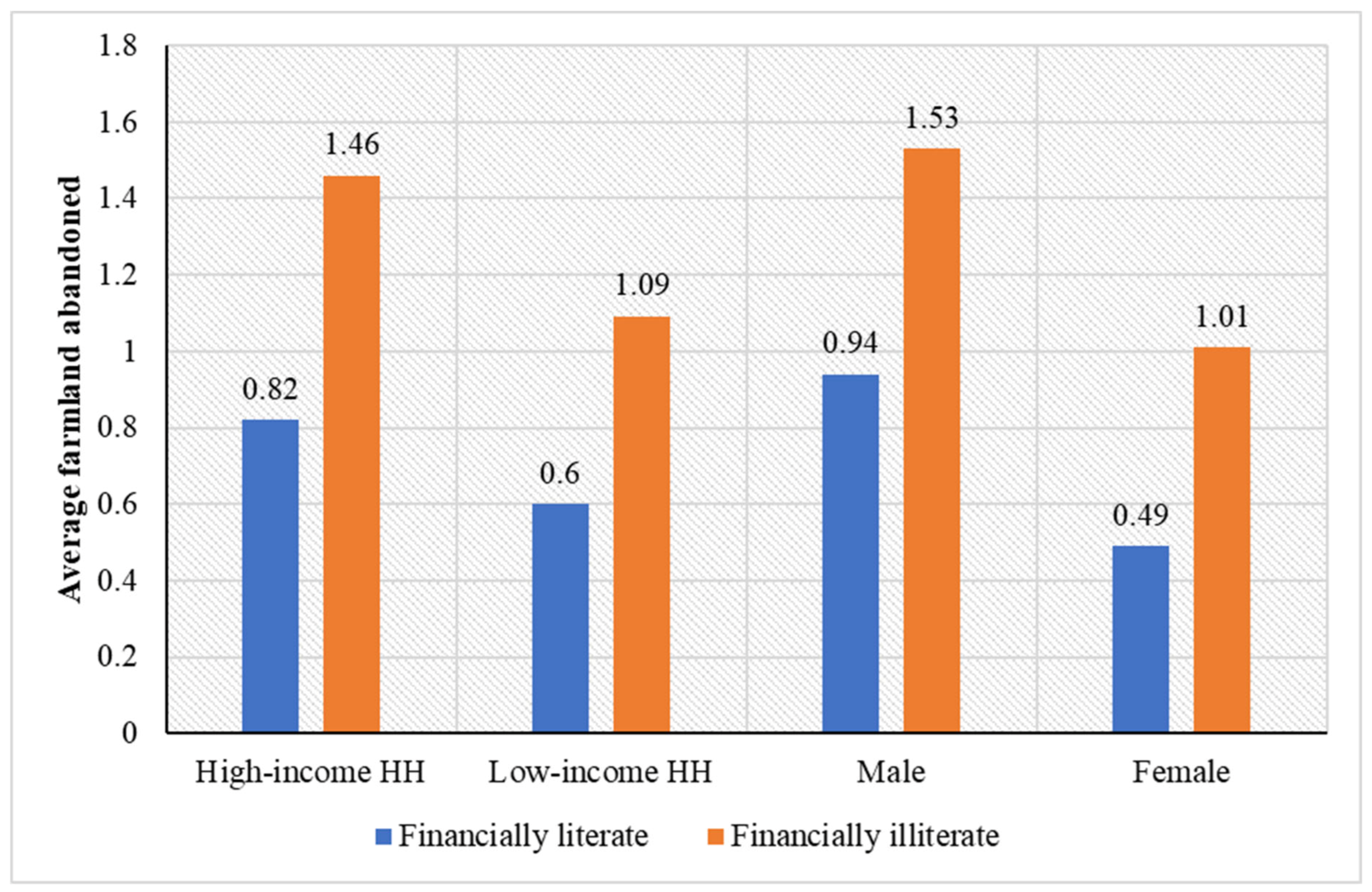

| Household income level | High | 0.634 | 0.735 | −0.101 | −3.84 *** | 13.74% |

| Low | 0.574 | 0.712 | −0.138 | −6.89 *** | 19.38% | |

| Gender | Male | 1.005 | 1.184 | −0.179 | −2.31 * | 15.12% |

| Female | 0.733 | 0.918 | −0.185 | −4.70 *** | 20.15% | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ankrah Twumasi, M.; Dogbe, B.S.; Ankrah, E.K.; Ding, Z.; Jiang, Y. Assessing Financial Literacy and Farmland Abandonment Relationship in Ghana. Agriculture 2023, 13, 580. https://doi.org/10.3390/agriculture13030580

Ankrah Twumasi M, Dogbe BS, Ankrah EK, Ding Z, Jiang Y. Assessing Financial Literacy and Farmland Abandonment Relationship in Ghana. Agriculture. 2023; 13(3):580. https://doi.org/10.3390/agriculture13030580

Chicago/Turabian StyleAnkrah Twumasi, Martinson, Bright Senyo Dogbe, Ernest Kwarko Ankrah, Zhao Ding, and Yuansheng Jiang. 2023. "Assessing Financial Literacy and Farmland Abandonment Relationship in Ghana" Agriculture 13, no. 3: 580. https://doi.org/10.3390/agriculture13030580