Abstract

In this paper, we analyzed a dataset of over 2000 crypto-assets to assess their credit risk by computing their probability of death using the daily range. Unlike conventional low-frequency volatility models that only utilize close-to-close prices, the daily range incorporates all the information provided in traditional daily datasets, including the open-high-low-close (OHLC) prices for each asset. We evaluated the accuracy of the probability of death estimated with the daily range against various forecasting models, including credit scoring models, machine learning models, and time-series-based models. Our study considered different definitions of “dead coins” and various forecasting horizons. Our results indicate that credit scoring models and machine learning methods incorporating lagged trading volumes and online searches were the best models for short-term horizons up to 30 days. Conversely, time-series models using the daily range were more appropriate for longer term forecasts, up to one year. Additionally, our analysis revealed that the models using the daily range signaled, far in advance, the weakened credit position of the crypto derivatives trading platform FTX, which filed for Chapter 11 bankruptcy protection in the United States on 11 November 2022.

Keywords:

daily range; bitcoin; crypto-assets; cryptocurrencies; credit risk; default probability; probability of death; ZPP; cauchit; random forests JEL Classification:

C32; C35; C51; C53; C58; G12; G17; G32; G33

1. Introduction

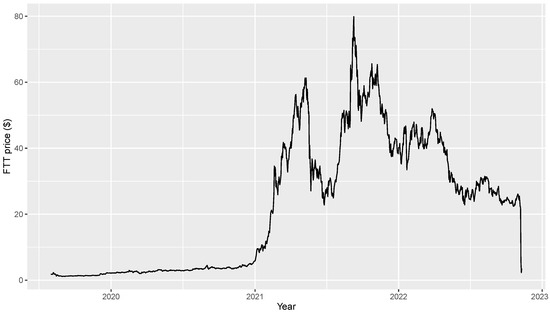

FTX was a Bahamas-based cryptocurrency exchange that at its peak in July 2021, had over one million users and was the third-largest cryptocurrency exchange by volume [1]. A revelation at the beginning of November 2022 that FTX’s partner trading firm Alameda Research held a significant portion of its assets in FTX’s native token FTT [2] prompted the rival exchange Binance to sell its holdings of this token. This event was immediately followed by customer withdrawals from FTX so large that FTX was unable to meet their demand [3]. On 11 November 2022, FTX, FTX.US (a separate associated exchange for US residents), Alameda Research, and more than 100 affiliates filed for bankruptcy in Delaware [4]. The price of the FTX token that reached a maximum of 80$ in September 2021 for a total market capitalization of almost 10 billion $ fell to single digits after the FTX bankruptcy and was still trading at the end of December 2022 close to 1$.

Aside from the significant financial losses incurred, the FTX bankruptcy is similar to numerous failed cryptocurrency projects in the past. These failures have been attributed to deficient corporate governance standards, inadequate cybersecurity measures, and inadequate management of credit and liquidity risks. It is noteworthy that Samuel Bankman-Fried, the former CEO of FTX, acknowledged that dedicating more time to risk management could have potentially prevented the collapse of the company, as stated on 30 November 2022 (see [5]).

Unfortunately, there is a lack of interest in credit risk management for crypto-assets, which is reflected in the scarce academic financial literature on the topic. This can be attributed to two main factors: the absence of sufficient financial and accounting data, and the need to use a different definition of credit risk. In this regard, in [6], a new definition of credit risk for crypto-assets was proposed based on their “death”, which occurs when their price drops significantly and they become illiquid. It is worth noting that there is no unique definition for a dead asset, either in the professional or academic literature, as outlined in [7,8,9,10,11]. Furthermore, even when a crypto-asset is considered dead, it may still show some minimal trading volumes (as is the case with the current trading of the FTX token at the end of December 2022), either due to the possibility of recovering a small amount of the initial investment or simply to speculate on its possible revival. It is also worth noting that the “death” state of a crypto-asset may be temporary rather than permanent: indeed, in [10], it was demonstrated that some coins were abandoned and subsequently “resurrected” up to five times over several years.

This paper proposes for the first time to forecast the probability of death (PD) of a crypto-asset using the daily range, which employs all the information provided in traditional daily datasets such as open-high-low-close (OHLC) prices instead of only close-to-close prices that are used by low-frequency volatility models. Recent literature has revived the interest in range-based estimators that employ OHLC prices by showing that volatility models using high-frequency data outperformed low-frequency volatility models using range-based estimators only for short-term forecasts (usually for 1-day-ahead forecasts), while this was not the case for longer horizons (see [12,13]). This is particularly important for crypto-assets where the possibility to find long time series of high-frequency data is usually confined to a small number of well-established crypto-assets, such as Bitcoin and Ethereum.

The first contribution of this paper is a set of models to forecast the probability of death that combines the daily range with the zero-price-probability (ZPP) model byy [14], which is a methodology to compute the probabilities of default using only market prices. Recent literature has shown that the ZPP models tend to outperform the competing models in terms of default probability estimation over a 1-year horizon; see [6,15,16,17,18] for more details.

The second contribution of this paper is a large-scale forecasting exercise using a set of 2003 crypto coins that were active from the beginning of 2014 until the end of May 2020, which was first examined by [11]. We considered a large set of competing models ranging from credit scoring models to machine learning and time- series-based models, with different definitions of dead coins and different forecasting horizons. Our empirical evidence showed that credit-scoring models and machine-learning methods using lagged trading volumes and online searches were the best models for short-term horizons up to 30 days ahead. Meanwhile, time-series models using the daily range were better choices for longer-term forecasts up to 1-year ahead.

The third contribution of the paper is a robustness check to examine how the best forecasting models for the probability of death over a 1-year-ahead horizon behaved when modeling the token of the crypto trading platform FTX, which filed for the Chapter 11 bankruptcy protection in the United States on 11 November 2022.

The paper is organized as follows: Section 2 reviews the literature devoted to the credit risk of crypto-assets, crypto exchanges, and the daily range, while the methods proposed to model and forecast the probability of death of crypto-assets are discussed in Section 3. The empirical results are reported in Section 4, while robustness checks are discussed in Section 5. Section 6 concludes the paper.

2. Literature Review

2.1. Credit Risk of Crypto-Assets

The financial literature dealing with the credit risk involved in crypto-assets is very small, and, as of the time of writing this paper, only five papers have examined the topic of dead coins, while only three of these have proposed methods to forecast the probability of a coin death. In this regard, we remark that there is no unique definition of dead coins: in the professional literature, some define dead coins as those whose value drops below 1 cent (https://www.investopedia.com/news/crypto-carnage-over-800-cryptocurrencies-are-dead/, accessed on 1 December 2022), while others consider a coin dead if there is no trading volume, no nodes running, and no active community and if the coin has been delisted from (almost) all exchanges (https://www.coinopsy.com/dead-coins/, accessed on 1 December 2022).

The work by [7] (the original workshop proceedings by [7] were later published as [10]) was the first to propose a formal definition of dead coins in the academic literature based on a complex formula involving price and volumes peaks and rolling time windows. Moreover, their approach allows a coin to be “resurrected” if there is a resurgence of trading volumes.

In Ref. [9], a simplified version of the previous method by [7] was proposed, where a crypto-currency can be considered as dead if its average daily trading volume for a given month is lower or equal to 1% of its past historical peak. dead crypto-currency is classified as “resurrected” if this average daily trading volume reaches a value of more or equal to 10% of its past historical peak again. We remark that [9] presented this method as the [7] approach when, in reality, the latter involves many more restrictions. The methodology used by [9] in their work is much simpler, and it assumes that a coin is (temporarily) dead if data gaps are present in its time series.

In [6,8,11], the first and only models to predict crypto-currency defaults/deaths were proposed. In [8], an in-sample analysis was performed using 146 proof-of-work-based cryptocurrencies that started trading before 2015 whose performance was followed until December 2018. It was found that about 60% of those cryptocurrencies died. The authors used linear discriminant analysis to forecast these defaults and found that their model could predict most of the crypto-currency bankruptcies but not the crypto-currencies that remained alive. Interestingly, the authors of [8] had to discard several variables to build a meaningful dataset because this information was not available for most dead coins.

Other authors [6] proposed a set of models to estimate the probability of death for a group of 42 crypto-currencies using the zero-price-probability (ZPP) model, as well as credit-scoring models and machine-learning methods. They found that credit-scoring models performed better in the training sample, whereas the models’ performances were much closer in the validation sample.

The authors of [11] were the first to examine a very large dataset of over two thousand crypto-coins observed between 2015 and 2020 to estimate their credit risk by computing their probability of death using different definitions of dead coins, different forecasting models, and different horizons. They found that the choice of the coin-death definition affected the set of the best forecasting models to compute the probability of death, but this choice was not critical, and the best models were the same in most cases. They showed that the cauchit and the ZPP based on the random walk or the MS-GARCH(1,1) were the best models for newly established coins, while credit-scoring models and machine-learning methods performed better for older coins.

Finally, we remark that the dead coins collected in online repositories such as coinopsy.com or deadcoins.com are indeed dead, but they are not useful for credit risk management because their technical information and historical market data are no longer available for almost all of them. Therefore, it is better to use the methods proposed by [7,9] to detect dead crypto-assets or the professional rule that defines a crypto-asset as dead if its value drops below 1 cent: as highlighted by [11], even if there is still some trading for the assets defined as “dead” according to these methods, this is not a problem but an advantage because we can still analyze them when market data and other information are still available.

2.2. Credit Risk of Crypto Exchanges

Similar to crypto-assets, the financial literature dealing with the credit risk involved in crypto exchanges is very small and as of the writing of this paper, only five works have examined the main determinants that can lead to the closure/default of an exchange.

The authors of [19] used a dataset of 40 exchanges and found that exchanges that processed more transactions were less likely to shut down, whereas past security breaches and an antimoney laundering indicator were not statistically significant. The authors of [20] extended the work by [19] through considering data between 2010 and March 2015 and up to 80 exchanges, using a panel logit model with an expanded set of explanatory variables. They found that a security breach increases the odds that the exchange will close the same quarter, while an increase in the daily transaction volume significantly decreases the probability that the exchange will shut down that quarter. A significant negative time trend that decreases the probability of closure over time was also reported. Moreover, they showed that exchanges receive most of their transaction volume from fiat currencies traded by few other exchanges are 91% less likely to close than are other exchanges that trade fiat currencies with higher competition. Similarly to the findings in [19], an antimoney laundering indicator and two-factor authentication were found to not be significant.

The authors of [21] used the dataset first examined by [19] to propose several alternative approaches to forecast the probability of closure of a crypto exchange, ranging from credit scoring models to machine learning methods, but without any comprehensive forecasting analysis.

The authors of [22] considered a dataset of 144 exchanges active from the first quarter of 2018 to the first quarter of 2021 to analyze the determinants surrounding the decision to close an exchange using credit-scoring and machine-learning techniques. They found that having a public developer team is by far the most important determinant, followed by the CER cybersecurity grade, the age of the exchange, and the number of traded cryptocurrencies available on the exchange. Both in-sample and out-of-sample forecasting confirmed these findings.

The authors of [23] built a database containing eight publicly available characteristics for 238 cryptocurrency exchanges. They used four popular machine learning classifiers to predict which digital markets remained open and which faced closure. Their best model was the random forest classifier, while the most important variables in terms of feature importance across multiple algorithms were the exchange lifetime, the transacted volume, and cybersecurity measures such as security audit, cold storage, and bug bounty programs.

Finally, we remark that if an exchange issues tokens representing ownership and they are traded daily, or even if these tokens are simply utility tokens (such as is the FTX token), then the probability of default/closure of the exchange can be forecast using the methods for crypto-assets discussed in Section 2.1; see [21] for a discussion at the textbook level.

2.3. Daily Range

The price range has long been known in both the academic and professional literature. For example, the opening, highest, lowest, and closing (OHLC) prices of an asset have been used in Japanese candlestick charting techniques since the 19th century [24], while the first applications in the financial literature can be traced to Mandelbrot [25]. Several authors, starting from [26], then developed volatility measures based on the daily range that were more efficient than were return-based volatility estimators; see [27] for an extensive review and the references therein.

Recent literature has revived interest in range-based estimators that employ OHLC prices to estimate the daily volatility; see [27,28,29,30]. Interestingly, the authors of [12] found that high-frequency volatility models outperformed low-frequency volatility models using range-based estimators only for short-term forecasts (usually for 1-day-ahead forecasts). As the forecast horizon increased (up to one month), the difference in forecast accuracy became statistically indistinguishable for most market indices.

Similarly, in [13], the role of high-frequency data in multivariate volatility forecasting was examined for investors with different investment horizons. The authors found that that models using high-frequency data significantly outperformed models with low-frequency data over the daily forecasting horizon, but this evidence decreased when longer horizons were considered. Moreover, they showed that investors may not obtain significant economic benefits from using high-frequency data depending on the type of economic loss they employ.

This encouraging evidence about the daily range stimulated our work of using this volatility estimator to model and forecast the probability of death for crypto-assets, given that finding high-frequency data for all 2003 crypto coins in our dataset was impossible.

3. Materials and Methods

In the context of crypto-assets, credit risk refers to the potential for gains and losses on the value of an abandoned and deemed “dead” cryptocurrency that can potentially be revived; see [6] for more details. This scenario occurs when the price of the crypto-asset plummets close to or to zero, as evidenced by a lack of trading activity for an extended period. Despite being considered dead, crypto-assets may continue to be traded as investors attempt to recover a portion of their initial investment or bet on the potential revamp of the asset.

Three criteria have been employed in the literature to classify crypto-assets as dead or alive [11]: (1) This first is the restrictive approach by [7,10]. According to this approach, first a “candidate peak” is defined as a day where the 7-day rolling price average is greater than any value 30 days before or after. A candidate peak is considered valid only if it is at least 50% greater than the minimum value in the 30 days prior to the candidate peak and at least 5% of the cryptocurrency’s maximum peak. Using this peak data, the authors of [7,10] classified a coin as abandoned or dead if the average daily volume for a given month is less than or equal to 1% of the peak volume. A coin’s status is changed to “resurrected” if the average daily trading volume for the month following a peak is greater than 10% of the peak value and the coin is currently considered dead). (2) The simplified approach proposed by [9] classifies a cryptocurrency as dead if its average daily trading volume for a given month is lower than or equal to 1% of its historical peak, while it is considered “resurrected” if this average daily trading volume reaches a value of 10% or more of its historical peak. The third criterion (3) is the professional rule, which considers a coin dead if its value drops below 1 cent.

The aim of this work is to propose a new model to forecast the probability of death (PD) of a crypto-asset using the daily range computed with open-high-low-close (OHLC) prices, a departure from traditional models that use only close-to-close prices. A simple way to use the OHLC prices for the computation of the PD of crypto-assets is to combine the daily range with the zero-price-probability (ZPP) model by [14], which is a methodology to compute the probabilities of default using only market prices . This method calculates the market-implied probability of the stock’s or crypto-asset’s price being less than or equal to zero within a specified time horizon (), considering that the price of a traded asset is a truncated variable that cannot fall below zero. The ZPP represents the probability of the price falling below the truncation level of zero, serving as a default indicator; see [14] for further details. For a univariate time series, the ZPP can be computed as follows:

- Establish a conditional model for the price differences, without log transformation, , where , and and are the conditional mean and standard deviation, respectively.

- Simulate a large number N of price trajectories up to time , utilizing the estimated time-series model from step 1. We will consider the 1-day-ahead, 30-day-ahead, and 365-day0ahead probability of death for each crypto-asset, that is , respectively.

- The probability of default for a crypto-asset is computed as , where n is the number of times among N simulations when the simulated price touches or crosses the zero barrier for a specified time interval , and .

In this study, we introduce, for the first time, the use of a price range estimator to model the conditional standard deviation of the price differences in the ZPP model. As we discussed in the literature review, there is an increasing amount of literature that has revived the interest in range-based estimators that employ OHLC prices to estimate the daily volatility; see [27,28,29,30].

We adopt the Garman–Klass [31] volatility estimator, which [29] found to be the best volatility estimator based on large-scale simulation studies. The authors of [29] showed that the Garman–Klass estimator is capable of producing standardized returns that are normally distributed and that the estimates obtained from daily data are comparable to those obtained from high-frequency data. This is important for crypto-assets, which have high-frequency data availability for only a limited number of assets. The Garman–Klass estimator assumes a Brownian motion with zero drift and no opening jumps, which is appropriate for crypto-assets since most of them eventually become worthless (see, e.g., [32,33]) and are traded 24/7. However, in the event of an opening jump (as may occur for illiquid assets), the jump-adjusted Garman–Klass volatility estimator described in [29] was used. In addition, we also evaluated the Yang and Zhang volatility estimator [34], which is unbiased, independent of drift, and consistent in the presence of opening price jumps. This estimator is interesting because it can be used to calculate the average daily volatility over multiple days, which could be more appropriate for crypto-assets used for trading strategies that involve dividing large orders over several days (these kind of strategies are often used by miners and “whales”, where the latter are entities or people that hold enough crypto-assets to influence their market prices, see [35,36] for more details). Moreover, the author wants to thank three anonymous professional traders in crypto-assets for highlighting this issue). After evaluating different values of n, we found that produced the best results.

The formulas for the jump-adjusted Garman–Klass (GK) volatility estimator and the Yang and Zhang (YZ) volatility estimator, to be used for the daily conditional variance of the price differences without log transformation, are presented below.

We employed four competing models to forecast the dynamics of the range-based daily volatilities : the simple random walk model by [27], the HAR model by [37], the ARFIMA model by [38], and the CARR model by [39].

The random walk model by [27] simply assumes that the log of the daily volatility follows a random walk without drift, so the the best prediction of tomorrow’s log-volatility is today’s log-volatility. The “no-change” forecast is a traditional benchmark used in several fields of research; see [40] for a comprehensive survey.

The HAR model by [37] assumes that the daily volatility is influenced by the past volatility over different time periods and is represented as follows:

and , , and stand for the daily, weekly, and monthly volatility components, respectively. We used 7 and 30 days for the weekly and monthly volatilities instead of the usual 5 and 22 days, as cryptocurrency exchanges operate continuously without weekends.

The auto-regressive fractional integrated moving average model, ARFIMA(p,d,q), was proposed by [38] to forecast the daily realized volatility, and it can be used to model the range-based volatility estimates as follows:

where L is the lag operator, and , , and form the fractional differencing operator defined by

where is the gamma function. Given our large dataset, we employed the ARFIMA(1,d,1) model to keep the computational burden tractable and with consideration to its past empirical prowess; see [41] and the references therein.

The CARR(1,1) model by [39] can be used to model the conditional standard deviation computed using range-based estimators as follows:

where is the conditional mean of , and is the error term which has an exponential density function with a unit mean. The exponential distribution is a common choice for the conditional distribution of because it takes positive values. Moreover, it allows the parameters of the CARR model to be estimated using the quasi-maximum likelihood method; see [39] for more details.

Finally, we remark that the conditional mean of the price difference was set to zero when the Garman—Klass volatility estimator was used, while it was set to the sample mean of the price differences when the Yang and Zhang volatility estimator was employed.

In this work, we will compare our novel models based on the daily range to the traditional models used in credit risk management such as credit-scoring models, machine learning, and time-series methods that rely on close-to-close prices for the ZPP model. A brief overview of these models is provided below.

Credit scoring models employ a set of variables to build a quantitative score, which is then used to estimate the probability of default/death. The standard form of a credit scoring model is represented as follows:

where is the probability of death for the crypto-asset i over a time period of given that it is not dead at time t, and is a vector of variables. Three popular models used in credit risk management are the logit model, the probit model, and the cauchit model, each obtained by using the logistic, standard normal, or standard Cauchy cumulative distribution function for , respectively. The parameters of these models can be estimated through maximum likelihood methods; see [42] for more details. The logit and probit models are commonly used in credit risk management (see [43,44,45,46]), while the cauchit model is favored under high levels of sparseness in the input space due to its ability to handle more extreme values; see [47,48].

In this study, we will also use machine learning (ML) techniques to analyze data and develop a system for modeling and forecasting complex patterns. Specifically, we will employ the random forest algorithm proposed by [49,50], which was found to be the best model for short-term forecasting of the PD for crypto-assets with a long time series in [11]. Moreover, it has an excellent past track record in forecasting binary variables; see [22,51,52,53] for more details. This algorithm aggregates multiple decision trees into a “forest”, where each tree is constructed differently from the others to decrease the correlation among trees and prevent overfitting. The probability of death is then computed using a majority vote among the trees in the forest.

Finally, following [11], we will also consider zero price probability (ZPP) models that utilize only close-to-close prices. This includes a simple random walk with drift model with constant variance (i.e., ) and a GARCH(1,1) model with normal errors, both of which have closed-form solutions for ZPP computation, as described in [6]. Additionally, we will consider the case of a GARCH(1,1) model with Student’s t errors, as introduced in [14]. We will also evaluate the ZPP using the GARCH(1,1) model with errors following the generalized hyperbolic skewed Student distribution, which has a polynomial behavior in one tail and exponential behavior in the other, as proposed in [54]. Finally, we will examine the ZPP computed using the two-regime Markov-switching GARCH model introduced in [55,56].

4. Results

4.1. Data

Our study analyzed a dataset consisting of 2003 crypto-assets that were either alive or dead (according to different criteria) between January 2014 and May 2020. This dataset was first used in [11]. The daily data, obtained from Coinmarketcap.com and Google Trends, included daily open, high, low, and close prices; volume; market capitalization; and the search volume index that shows the number of searches performed for a particular keyword or topic on Google within a specific time frame and region. The dataset was divided into two groups: “young coins” with fewer than 750 observations and “old coins” with more than 750 observations. The young coin group was used to forecast the 1-day and 30-day probabilities of death, while the old coin group was used to forecast the 1-day, 30-day, and 365-day probabilities of death. The dataset used in this paper is the same one introduced in [11] and is currently the largest dataset available on crypto-asset credit risk. It is unique in that the data for several crypto-assets are no longer available, and we had to reconstruct them through extensive online searches.

To assess the normality of the price differences of each crypto-asset, the Jarque–Bera and Kolmogorov–Smirnov statistics were computed. The same tests were employed with the standardized price differences, which were obtained by dividing the price differences by the daily volatility estimated using range-based methods . The results of the normality tests, represented as the percentage of p-values higher than 5%, are presented in Table 1 for both young and old coins.

Table 1.

Number of times (in percentage) when the p-values of the Jarque–Bera (J.B.) and the Kolmogorov–Smirnov (K.S.) tests were higher than 5% for the price differences and for the price differences standardized with the squared root of the range-based daily volatility . GK = Garman—Klass volatility estimator. YZ = Yang and Zhang volatility estimator.

The price differences of cryptocurrencies are not normally distributed. However, when standardized using the squared root of the Garman–Klass volatility estimator, the majority of cryptocurrencies display normality. Only a small fraction of price differences standardized with the Yang and Zhang volatility estimator seem to be normally distributed. This evidence supports the findings of [29], who demonstrated that the Garman–Klass estimator is the only one that can yield standardized returns that are normally distributed.

To classify a cryptocurrency as “dead” or “alive,” three criteria were employed as discussed in Section 3 and listed here:

- The approach proposed by [7];

- The approach proposed by [9];

- The professional rule that defines an asset as dead if its value drops below 1 cent and alive if its value rises above 1 cent.

The total number of coins available each day and the number of dead coins each day computed using these criteria are presented in Figure A1 and Figure A2 in Appendix A. For convenience, the approach proposed by [7] will be referred to as “restrictive”, the simplified approach proposed by [9] will be referred to as “simple”, and the professional rule will be referred to as “1 cent”.

The approach of [7] was found to be the most restrictive, as it identified fewer dead coins. On the other hand, the professional rule, which defines a coin as dead if its value drops below 1 cent, was found to be more lenient, leading to a higher number of identified dead coins. In [9], a simplified version of the [7] approach is proposed, which falls in between the two previously mentioned methods for young coins. However, for old coins, it was found to be the least restrictive approach. Moreover, the restrictive approach proposed by [7] is the most stable, whereas the professional rule is the most volatile.

In this study, credit scoring models and machine learning methods employed the lagged average monthly trading volume and the lagged average monthly search volume index obtained from Google Trends as predictors. The future probabilities of death were directly forecast by using 1-day-lagged predictors to forecast the 1-day-ahead probability of death, 30-day-lagged predictors to forecast the 30-day-ahead probability of death, and so on. To account for potential structural breaks, two types of estimation windows were considered: a rolling fixed window of 100,000 observations and an expanding window.

The time-series models for each coin were estimated separately using zero-point progression (ZPP) with and without the daily range, based on an expanding window approach. The first estimation sample consisted of 30 observations, and full estimation details can be found in [11]. The probabilities of deaths for various forecast horizons were calculated by employing recursive forecasts. It should be noted that the datasets utilized for credit scoring and machine learning models were distinct from those used for the time-series models, which resulted in some dates for which forecasts from all models were not available. Although this did not have an impact on the calculation of the area under the curve (AUC) metrics, it did affect the estimation of the model confidence sets and Brier scores, as detailed in the following section. Therefore, only those dates that were common across all models were used to calculate these metrics.

4.2. Forecasting Analysis

In accordance with [11], two groups of crypto-assets were considered:

- A total of 1165 young coins with a total of 537,693 observations, listed in Table A1, Table A2, Table A3 in Appendix B, were used to forecast the 1-day- and 30-day-ahead probabilities of death.

- A total of 838 old coins with a total of 987,018 observations, listed in Table A4 and Table A5 in Appendix B, were used to forecast the 1-day-, 30-day-, and 365-day-ahead probabilities of death.

The classification performance of the models was evaluated using the area under the receiver operating characteristic curve (AUC or AUROC), which measures the ability of the model to discriminate between alive and dead crypto-assets regardless of the discrimination threshold. A higher AUC score, close to 1, indicates a better performing model, as detailed in [57] pages869–875 and references therein. Due to limitations of the AUC, as discussed in [58], the model confidence set (MCS) proposed by [59] and extended by [60] was also used. This method selects the best forecasting models among a group of models based on a confidence level using an evaluation rule that is based on a loss function, in this case the Brier’s score [61].

The Rdata file, which contains the forecasts of the probability of deaths across all horizons (1-, 30-, and 365-day ahead) for the three definitions of “dead coins” (restricted [7], simple [9], and 1 cent [professional rule]) for both small young coins (SCs) and old big coins (BCs), along with the binary dependent variable, is now available on the author’s website: https://drive.google.com/file/d/1hVZYt6W_nwvvTtqicsUJFoBzUJfX0kJH/view?usp=share_link, accessed on 28 February 2023. This dataset includes the merged forecasts that were used to compute the model confidence set and the Brier scores for all models. The ZPPs were computed using functions from the R package bitcoinFinance (https://github.com/deanfantazzini/bitcoinFinance, accessed on 1 December 2022) and straightforward modifications of these functions. The random forest model was computed using the R package randomForest, while the credit scoring models were computed using the function from the R package stats.

The results of the AUC scores, the models included in the MCS, the Brier scores, and the percentage of times when the models failed to reach numerical convergence are reported in Table 2 for young coins and in Table 3 and Table 4 for old coins for all three criteria used to classify a crypto-asset as dead or alive.

Table 2.

Young coins: AUC scores (highest values are in bold fonts), Brier scores (smallest values are in bold fonts), models included in the MCS, and numerical convergence failures in percentage across three competing criteria to classify a coin as dead or alive. Ref. [7] approach = “restrictive”; simplified [7] approach = “simple”; professional rule = “1 cent”; D.R. = daily range-based estimator. Highest AUC, lowest Brier score and model included in the MCS are reported in bold font.

Table 3.

Old coins: AUC scores (highest values are in bold fonts), Brier scores (smallest values are in bold fonts), models included in the MCS, and numerical convergence failures in percentage across three competing criteria to classify a coin as dead or alive. Ref. [7] approach = “restrictive”; simplified [7] approach = “simple”; professional rule = “1 cent”; D.R. = daily range-based estimator. Highest AUC, lowest Brier score and model included in the MCS are reported in bold font.

Table 4.

Old coins (continuation): AUC scores (highest values are in bold fonts), Brier scores (smallest values are in bold fonts), models included in the MCS, and numerical convergence failures in percentage across three competing criteria to classify a coin as dead or alive. Ref. [7] approach = “restrictive”; simplified [7] approach = “simple”; professional rule = “1 cent”; D.R. = daily range-based estimator. Highest AUC, lowest Brier score and model included in the MCS are reported in bold font.

In the case of young crypto-assets, the results confirm the findings of [11], in that the cauchit model is the best model for all forecast horizons and across most classification criteria. Additionally, the ZPP computed using an MS-GARCH(1,1) model remains the best model when using the professional rule that defines a dead coin as one whose value drops below 1 cent, while the ZPP computed with the simple random walk provides good forecasts for all horizons and classification criteria.

For old coins, the random forests model with an expanding estimation window remains the best model for forecasting the probability of death up to 30 days ahead, but differently from [11], the ZPP models computed with the range-based estimators are the best models for forecasting the 365-day-ahead probability of death. This horizon is crucial for risk management, as it is the horizon considered by national regulations and international agreements, such as the Basel 2 and Basel 3 agreements.

The estimated AUCs for the models without the daily range in Table 2, Table 3 and Table 4 are consistent with the findings reported in [11] (using the same dataset). However, this is not the case for the model confidence sets (MCS) and the Brier scores, which now incorporate models using range-based volatility estimators. Due to significant numerical convergence failures of some models, such as the GARCH model with the generalized hyperbolic skewed Student distribution and ARFIMA models, the number of forecasts used to calculate the MCS and the Brier scores is significantly lower than those used to calculate the AUC. The former metrics require common data for all models, whereas the latter can be calculated individually. Therefore, for our dataset, the AUC is probably a more appropriate evaluation metric than are the MCS and the Brier score. However, we also provide the latter for completeness and interest.

Our results suggest that ZPP models utilizing range-based volatility estimators are generally more effective for long-term forecasts, supporting the evidence presented in [12], which found that high-frequency volatility models outperformed low-frequency models using range-based estimators only for short-term forecasts but not for longer horizons. In [12], it is posited that volatility exhibits long memory and changes gradually over time, so an accurate estimate of current day’s volatility is useful in predicting the following day’s volatility but less so for forecasts several weeks ahead. A similar dynamic may apply here: lagged trading volumes and online search data utilized by credit scoring models and ML methods are useful for short-term PD forecasts up to 30 days ahead but less so for 1-year-ahead forecasts, which are the standard in credit risk management. In this case, range-based estimators with long-memory models or the simple random walk may be sufficient. Furthermore, given the lack of a single ZPP model that is best across all classification criteria, this empirical evidence supports the possibility of improved forecasts through forecast combinations methods, which we leave as a topic for future research.

Regarding the differences between range-based estimators, we observe that the Yang–Zhang estimator produces better AUC forecasts than does the Garman–Klass estimator, particularly for long-term forecasts. However, this is not universally true for all forecasting models, and the Yang–Zhang estimator has significantly worse Brier scores than does the Garman–Klass estimator. This highlights the potential for improved forecasts through forecast combinations methods, and we leave this as an interesting topic for future research.

Finally, we wish to emphasize the poor numerical performance of the ARFIMA models, which failed to converge in almost 70% of cases. It is well established in the literature that the estimation of the fractional parameter d in ARFIMA() models is challenging, as documented in large simulation studies; see [62,63,64,65,66]. We used the exact maximum likelihood procedure with normal errors proposed in [67], which is theoretically efficient and has quasi-maximum likelihood properties. Unfortunately, the noisy nature and short time series of most crypto-assets had a significant impact on the numerical performance of this model. To keep the computational time within reasonable limits, we did not attempt alternative model estimators, leaving this as an interesting avenue for future research.

5. A Robustness Check: Forecasting the 1-Year-Ahead PD of the Crypto Trading Platform FTX

We evaluated the performance of the best forecasting models for the probability of death (PD) over the one-year horizon in modeling the token of the crypto trading platform FTX (symbol: FTT), which filed for Chapter 11 bankruptcy protection in the United States. on 11 November 2022. FTT, the native cryptocurrency token of FTX, was launched on 8 May 2019 and initially served as a reward for exchange transactions. However, over time, the list of functions for the FTT token expanded, and it became mainly used for reducing trading fees and securing futures positions. Further details can be found in a comprehensive summary available at coinmarketcap.com/currencies/ftx-token (accessed on 1 December 2022). Figure 1 displays the price in US dollars of the FTX token over the time sample from 1 August 2019 to 11 November 2022.

Figure 1.

Price in USD of the FTX token over the time sample 1 August 2019/11 November 2022.

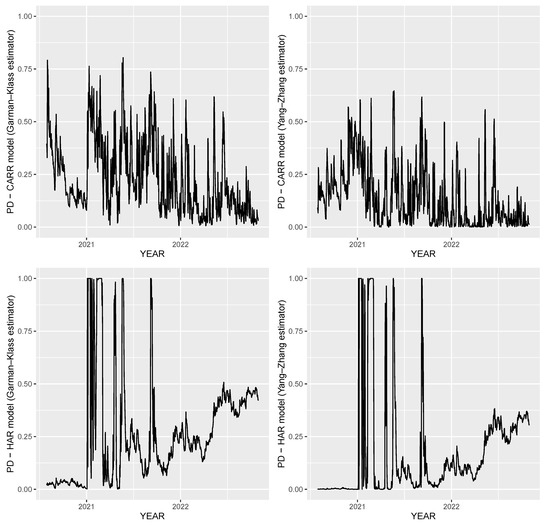

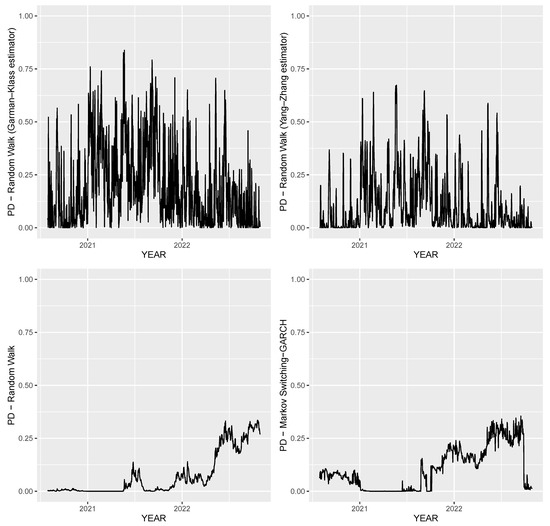

We computed the 1-year-ahead PD using the ZPP with all the range-based estimators, as well as the ZPP based on the random walk or the Markov-switching GARCH(1,1), which were found to be the best models for long-term PD forecasts in [11]. All models were estimated using an expanding window with the first estimation sample consisting of 365 observations. The estimated probabilities of death for all models are reported in Figure 2 and Figure 3 from July 2020 until the end of October 2022, which is 11 days prior to the official bankruptcy of FTX.

Figure 2.

One-year-ahead probability of death (PD) estimated over the time sample 30 July 2020/30 October 2022 using an expanding window with the first estimation sample consisting of 365 observations for these ZPP models: CARR model with the Garman—Klass estimator, CARR model with the Yang—Zhang estimator, HAR model with the Garman—Klass estimator, and HAR model with the Yang—Zhang estimator.

Figure 3.

One-year-ahead probability of death (PD) estimated over the time sample 30 July 2020/30 October 2022 using an expanding window with the first estimation sample consisting of 365 observations for these ZPP models: random walk with Garman—Klass estimator), random walk with Yang—Zhang estimator, random walk, and Markov-switching GARCH.

The 1-year-ahead probabilities of death computed with range-based volatility estimators reached their highest values approximately one year prior to the official bankruptcy of FTX, thereby indirectly confirming why they were the best models for forecasting the 1-year-ahead PD in the baseline case. However, both the HAR models with the daily range and the models using close-to-close prices showed steadily increasing probabilities of death from the end of 2021 until just before the bankruptcy.

In general, it is noted that models using range-based estimators resulted in much noisier signals compared to models using close-to-close prices. Furthermore, the HAR models experienced numerical instability at the beginning of the sample due to the small sample size, while ARFIMA models with daily range were not reported because they failed to converge several times in the sample, thereby confirming the estimation problems discussed in Section 4.2.

This empirical evidence leads to two conclusions: first, the market was pricing a potential credit event related to FTX well in advance of the official bankruptcy. Second, this evidence supports the potential for forecasting gains by combining the estimates of the PD obtained from different methods. We leave this topic as an interesting avenue for future research.

Finally, we would like to note that, in line with the methodology outlined in [11], we tested the robustness of our findings using different data samples, including data prior to and after 2017, and by stratifying crypto-assets based on their market capitalization. Specifically, the authors of [11] separated their dataset into two subsamples consisting of data before and after 10 December 2017 to investigate how their models’ forecasting performances would change in these two subsamples. This date was chosen because it marked the introduction of the first bitcoin futures on the CBOE, and there is a significant body of literature demonstrating that there was a financial bubble in bitcoin prices in 2016–2017 that burst at the end of 2017, potentially triggered by the introduction of these new bitcoin futures (see [11] and references therein for more details). We conducted the same robustness check using range-based volatility estimators and found no significant differences between the two subsamples. Additionally, as per [11], we conducted a second robustness check where we separated the 100 crypto coins with the largest market capitalization from all other coins with a smaller market capitalization. We did not identify any qualitative differences from the baseline case. While the tables containing the results of these robustness checks were quite extensive, they did not contribute anything new to our findings and are not reported here. However, they are available on the author’s webpage at https://docs.google.com/spreadsheets/d/1pqM0HdBPPyZAzBKsgiarkisCoQhmbCae/edit?usp=share_link&ouid=103750598646225124705&rtpof=true&sd=true, accessed on 28 February 2023.

6. Discussion and Conclusions

This paper aimed to estimate the credit risk of crypto-assets by computing their probability of death using the daily range data, which incorporate all the information available in traditional daily datasets, such as the open-high-low-close prices.

To achieve this aim, we first proposed a set of models to forecast the probability of death that combines the daily range with the zero-price probability (ZPP) model, which is an approach to compute these probabilities using only market prices. Then, we conducted a comprehensive forecasting exercise using a sample of 2003 crypto coins active from 2014 to 2020, as previously examined by [11]. We employed a wide range of competing models, including credit-scoring models, machine-learning models, and time-series-based models, with various definitions of dead coins and forecasting horizons. The results showed that credit-scoring models and machine-learning methods using lagged trading volumes and online searches were the most effective models for short-term forecasts, up to 30 days ahead, whereas time-series models using the daily range were better suited for longer-term forecasts, up to 1 year ahead. Furthermore, we conducted a robustness check and found that our best models for forecasting the 1-year-ahead probability of death indicated that the market was anticipating a potential credit event related to FTX well before its official bankruptcy, which occurred on 11 November 2022.

The main recommendation for investors is to use credit-scoring and machine-learning models for short-term forecasting up to 30 days ahead, particularly the cauchit and the random forest models first suggested by [11]. Meanwhile, ZPP-based models using range-based volatility estimators are a better choice for long-term forecasts up to 1 year ahead, which is the traditional horizon for credit risk management. This evidence is consistent with the results reported in [12,13], which found that high-frequency volatility models outperformed low-frequency models using range-based estimators only for short-term forecasts but not for longer horizons.The authors of [12] argued that volatility exhibits long memory and changes gradually over time, so an accurate estimate of the current day’s volatility is useful in predicting the following day’s volatility but less so for forecasts several weeks ahead. A similar dynamic may apply in our case, where lagged trading volumes and online search data utilized by credit scoring models and ML methods are useful for short-term PD forecasts up to 30 days ahead but less so for 1-year-ahead forecasts, which is the standard horizon in credit risk management. In this case, range-based estimators with long-memory models or the simple random walk can be sufficient.

Our research findings strongly support the notion of improving credit risk reporting for crypto-assets. Our stance aligns with similar proposals made by [6,11,21]. We recommend that crypto exchanges be mandated to publish daily death probability estimates for their traded crypto-assets, utilizing either one of the models discussed in this paper or any other methodology that regulators deem appropriate. Such information would facilitate more informed investment decisions for investors interested in crypto-assets. Furthermore, the collapse of FTX and its associated trading firm, Alameda Research, highlights the need for more stringent regulations regarding reserve assets for crypto exchanges. National and international regulators should consider including fiat currencies, precious metals, or tangible assets, such as power plants, in the list of potential capital reserves. Conversely, digitally generated tokens that function as discount cards should not be used as reserve assets.

It is important to also highlight the limitations of this study. Firstly, we did not attempt to model the returns of crypto-assets. Modeling the volatility of assets is generally more important for risk modeling purposes than is modeling the returns, as discussed in [68] and the references therein. However, recent advances in time series forecasting and nonlinear modeling may aid in producing more accurate risk estimates; see [69,70,71,72,73] for more details. Moreover, we focused on end-of-day data due to its availability for all crypto-assets. However, exploring how our results may differ when using high-frequency data would be of interest. We leave these matters as future research possibilities.

Our work leaves a number of other issues for future research: the computational problems that emerged in this work seem to suggest Bayesian methods as a possible solution for smoothing noisy data and improving the model’s computation in the case of small-time series. Moreover, several instances in our empirical analysis highlighted the possibility of forecasting gains by combining the estimated PDs obtained from different methods. We leave all these issues as avenues of future work.

Funding

The author gratefully acknowledges financial support from the grant of the Russian Science Foundation (no. 20-68-47030).

Conflicts of Interest

The author declares no conflict of interest.

Appendix A. Daily Number of Total Available Coins and of Dead Coins

Figure A1.

Young coins: Daily number of total available coins and the daily number of dead coins computed using the previous three criteria. The data are from [11]. For convenience, the approach proposed by [7] is referred to as “restrictive”, the simplified approach proposed by [9] as “simple”, and the professional rule as “1 cent”.

Figure A1.

Young coins: Daily number of total available coins and the daily number of dead coins computed using the previous three criteria. The data are from [11]. For convenience, the approach proposed by [7] is referred to as “restrictive”, the simplified approach proposed by [9] as “simple”, and the professional rule as “1 cent”.

Figure A2.

Old coins: Daily number of total available coins and the daily number of dead coins computed using the previous three criteria. The data are from [11]. For convenience, the approach proposed by [7] is referred to as “restrictive”, the simplified approach proposed by [9] as “simple”, and the professional rule as “1 cent”.

Figure A2.

Old coins: Daily number of total available coins and the daily number of dead coins computed using the previous three criteria. The data are from [11]. For convenience, the approach proposed by [7] is referred to as “restrictive”, the simplified approach proposed by [9] as “simple”, and the professional rule as “1 cent”.

Appendix B. Lists of Young and Old Coins

Table A1.

Names of the 1165 young coins: coins 1–400.

Table A1.

Names of the 1165 young coins: coins 1–400.

| 1 | Bitcoin SV | 101 | Band Protocol | 201 | TROY | 301 | ETERNAL TOKEN |

| 2 | Crypto.com Coin | 102 | PLATINCOIN | 202 | Anchor | 302 | Pirate Chain |

| 3 | Acash Coin | 103 | UNI COIN | 203 | ShareToken | 303 | USDQ |

| 4 | UNUS SED LEO | 104 | Qubitica | 204 | QuarkChain | 304 | Electronic Energy Coin |

| 5 | USD Coin | 105 | MX Token | 205 | Content Value Network | 305 | VNDC |

| 6 | HEX | 106 | Ocean Protocol | 206 | Gemini Dollar | 306 | Egretia |

| 7 | Cosmos | 107 | BitMax Token | 207 | FLETA | 307 | Bitcoin Rhodium |

| 8 | VeChain | 108 | Origin Protocol | 208 | Cred | 308 | IPChain |

| 9 | HedgeTrade | 109 | XeniosCoin | 209 | Metadium | 309 | Digital Asset Guarantee Token |

| 10 | INO COIN | 110 | Project Pai | 210 | Cocos-BCX | 310 | BQT |

| 11 | OKB | 111 | WINk | 211 | MEXC Token | 311 | LINKA |

| 12 | FTX Token | 112 | Function X | 212 | Sport and Leisure | 312 | UGAS |

| 13 | VestChain | 113 | Fetch.ai | 213 | Nectar | 313 | Pundi X NEM |

| 14 | Paxos Standard | 114 | 1irstcoin | 214 | Morpheus.Network | 314 | Yap Stone |

| 15 | MimbleWimbleCoin | 115 | Wirex Token | 215 | Dimension Chain | 315 | Ondori |

| 16 | PlayFuel | 116 | Grin | 216 | Kleros | 316 | Lykke |

| 17 | Hedera Hashgraph | 117 | Aurora | 217 | Hxro | 317 | BOX Token |

| 18 | Algorand | 118 | Karatgold Coin | 218 | StakeCubeCoin | 318 | Sense |

| 19 | Largo Coin | 119 | SynchroBitcoin | 219 | Dusk Network | 319 | Newscrypto |

| 20 | Binance USD | 120 | DAD | 220 | Wixlar | 320 | CUTcoin |

| 21 | Hyperion | 121 | Ecoreal Estate | 221 | Diamond Platform Token | 321 | 1SG |

| 22 | The Midas Touch Gold | 122 | AgaveCoin | 222 | Aencoin | 322 | Global Social Chain |

| 23 | Insight Chain | 123 | Folgory Coin | 223 | Aladdin | 323 | Agrocoin |

| 24 | ThoreCoin | 124 | BOSAGORA | 224 | VITE | 324 | MVL |

| 25 | TAGZ5 | 125 | Tachyon Protocol | 225 | VNX Exchange | 325 | Robotina |

| 26 | Elamachain | 126 | Ultiledger | 226 | AMO Coin | 326 | Nyzo |

| 27 | MINDOL | 127 | Nash Exchange | 227 | XMax | 327 | Akropolis |

| 28 | Dai | 128 | NEXT | 228 | FNB Protocol | 328 | Trade Token X |

| 29 | Baer Chain | 129 | Loki | 229 | Aergo | 329 | VeriDocGlobal |

| 30 | HUSD | 130 | BigONE Token | 230 | CoinEx Token | 330 | Verasity |

| 31 | Flexacoin | 131 | WOM Protocol | 231 | QuickX Protocol | 331 | BitCapitalVendor |

| 32 | Velas | 132 | BitKan | 232 | Moss Coin | 332 | Kryll |

| 33 | Metaverse Dualchain Network Architecture | 133 | CONTRACOIN | 233 | Safe | 333 | EURBASE |

| 34 | ZB Token | 134 | Rocket Pool | 234 | Perlin | 334 | Cryptocean |

| 35 | GlitzKoin | 135 | IDEX | 235 | LiquidApps | 335 | GoCrypto Token |

| 36 | botXcoin | 136 | Egoras | 236 | OTOCASH | 336 | Sentivate |

| 37 | Divi | 137 | LuckySevenToken | 237 | Sentinel Protocol | 337 | Ternio |

| 38 | Terra | 138 | Jewel | 238 | LCX | 338 | CryptoVerificationCoin |

| 39 | DxChain Token | 139 | Celer Network | 239 | Tellor | 339 | VeriBlock |

| 40 | Quant | 140 | Bonorum | 240 | MixMarvel | 340 | VINchain |

| 41 | Seele-N | 141 | Kusama | 241 | CoinMetro Token | 341 | PCHAIN |

| 42 | Counos Coin | 142 | General Attention Currency | 242 | Levolution | 342 | Cardstack |

| 43 | Nervos Network | 143 | Everipedia | 243 | Endor Protocol | 343 | Tokoin |

| 44 | Matic Network | 144 | CryptalDash | 244 | IONChain | 344 | AmonD |

| 45 | Blockstack | 145 | Bitcoin 2 | 245 | HyperDAO | 345 | MargiX |

| 46 | Energi | 146 | Apollo Currency | 246 | #MetaHash | 346 | S4FE |

| 47 | Chiliz | 147 | BORA | 247 | Digix Gold Token | 347 | SnapCoin |

| 48 | QCash | 148 | Cryptoindex.com 100 | 248 | Effect.AI | 348 | EOSDT |

| 49 | BitTorrent | 149 | GoChain | 249 | Darico Ecosystem Coin | 349 | ZVCHAIN |

| 50 | ABBC Coin | 150 | MovieBloc | 250 | GreenPower | 350 | FansTime |

| 51 | Unibright | 151 | TOP | 251 | PlayChip | 351 | EOS Force |

| 52 | NewYork Exchange | 152 | Bit-Z Token | 252 | Cosmo Coin | 352 | ContentBox |

| 53 | Beldex | 153 | IRISnet | 253 | Atomic Wallet Coin | 353 | Maincoin |

| 54 | ExtStock Token | 154 | Machine Xchange Coin | 254 | IQeon | 354 | BaaSid |

| 55 | Celsius | 155 | CWV Chain | 255 | HYCON | 355 | Constant |

| 56 | Bitbook Gambling | 156 | NKN | 256 | LNX Protocol | 356 | USDx stablecoin |

| 57 | SOLVE | 157 | ZEON | 257 | Prometeus | 357 | PumaPay |

| 58 | Sologenic | 158 | Neutrino Dollar | 258 | V-ID | 358 | NIX |

| 59 | Tratin | 159 | WazirX | 259 | suterusu | 359 | JD Coin |

| 60 | RSK Infrastructure Framework | 160 | Nimiq | 260 | T.OS | 360 | FarmaTrust |

| 61 | v.systems | 161 | BHPCoin | 261 | XYO | 361 | Futurepia |

| 62 | PAX Gold | 162 | Fantom | 262 | ChronoCoin | 362 | Themis |

| 63 | BitcoinHD | 163 | Newton | 263 | YOU COIN | 363 | IntelliShare |

| 64 | Elrond | 164 | The Force Protocol | 264 | Telos | 364 | Content Neutrality Network |

| 65 | Bloomzed Token | 165 | COTI | 265 | Contents Protocol | 365 | BitMart Token |

| 66 | THORChain | 166 | ILCoin | 266 | EveryCoin | 366 | Vipstar Coin |

| 67 | Joule | 167 | Ethereum Meta | 267 | Ferrum Network | 367 | Humanscape |

| 68 | Xensor | 168 | TrustVerse | 268 | LINA | 368 | CanonChain |

| 69 | CRYPTOBUCKS | 169 | sUSD | 269 | Origo | 369 | Litex |

| 70 | STEM CELL COIN | 170 | VideoCoin | 270 | Atlas Protocol | 370 | Waves Enterprise |

| 71 | APIX | 171 | Ankr | 271 | VIDY | 371 | Spectre.ai Utility Token |

| 72 | Tap | 172 | Chimpion | 272 | Ampleforth | 372 | Esportbits |

| 73 | Bankera | 173 | Rakon | 273 | GNY | 373 | Beaxy |

| 74 | Breezecoin | 174 | Travala.com | 274 | ChainX | 374 | SINOVATE |

| 75 | FABRK | 175 | ThoreNext | 275 | DAPS Coin | 375 | SIX |

| 76 | Bitball Treasure | 176 | BitForex Token | 276 | Zano | 376 | Phantasma |

| 77 | BHEX Token | 177 | Wrapped Bitcoin | 277 | 0Chain | 377 | BetProtocol |

| 78 | Theta Fuel | 178 | ZBG Token | 278 | GAPS | 378 | pEOS |

| 79 | Gatechain Token | 179 | Orchid | 279 | DigitalBits | 379 | MIR COIN |

| 80 | STASIS EURO | 180 | TTC | 280 | HitChain | 380 | Winding Tree |

| 81 | Kava | 181 | LTO Network | 281 | WeShow Token | 381 | Grid+ |

| 82 | BTU Protocol | 182 | MicroBitcoin | 282 | apM Coin | 382 | BlockStamp |

| 83 | Thunder Token | 183 | Contentos | 283 | Sakura Bloom | 383 | BOLT |

| 84 | Beam | 184 | Lambda | 284 | Clipper Coin | 384 | INLOCK |

| 85 | Swipe | 185 | Constellation | 285 | FOAM | 385 | CEEK VR |

| 86 | Reserve Rights | 186 | Ultra | 286 | qiibee | 386 | Nuggets |

| 87 | Digitex Futures | 187 | FIBOS | 287 | Nestree | 387 | Lition |

| 88 | Orbs | 188 | DREP | 288 | SymVerse | 388 | Rublix |

| 89 | Buggyra Coin Zero | 189 | Invictus Hyperion Fund | 289 | ROOBEE | 389 | Spendcoin |

| 90 | IoTeX | 190 | CONUN | 290 | CryptoFranc | 390 | Bitrue Coin |

| 91 | inSure | 191 | Standard Tokenization Protocol | 291 | DDKoin | 391 | HoryouToken |

| 92 | Davinci Coin | 192 | Mainframe | 292 | Zel | 392 | RealTract |

| 93 | USDK | 193 | Chromia | 293 | Metronome | 393 | BidiPass |

| 94 | Super Zero Protocol | 194 | ARPA Chain | 294 | NPCoin | 394 | PlayCoin [ERC20] |

| 95 | Huobi Pool Token | 195 | REPO | 295 | ProximaX | 395 | MultiVAC |

| 96 | Harmony | 196 | Carry | 296 | NOIA Network | 396 | Artfinity |

| 97 | Poseidon Network | 197 | Valor Token | 297 | Eminer | 397 | EXMO Coin |

| 98 | Handshake | 198 | Zenon | 298 | Observer | 398 | Credit Tag Chain |

| 99 | 12Ships | 199 | Elitium | 299 | Baz Token | 399 | Wowbit |

| 100 | Vitae | 200 | Emirex Token | 300 | KARMA | 400 | RSK Smart Bitcoin |

Table A2.

Names of the 1165 young coins: coins 401–800.

Table A2.

Names of the 1165 young coins: coins 401–800.

| 401 | PegNet | 501 | ZeuxCoin | 601 | SPINDLE | 701 | Raise |

| 402 | Trias | 502 | TurtleCoin | 602 | Proton Token | 702 | Arbidex |

| 403 | PIBBLE | 503 | WPP TOKEN | 603 | Swap | 703 | W Green Pay |

| 404 | PLANET | 504 | Linkey | 604 | Olive | 704 | Digital Insurance Token |

| 405 | Snetwork | 505 | Noku | 605 | ImageCoin | 705 | Essentia |

| 406 | Cryptaur | 506 | Coineal Token | 606 | Infinitus Token | 706 | BioCoin |

| 407 | Aryacoin | 507 | Hashgard | 607 | ATMChain | 707 | Zen Protocol |

| 408 | Safe Haven | 508 | Fast Access Blockchain | 608 | WinStars.live | 708 | ZUM TOKEN |

| 409 | Rotharium | 509 | MEET.ONE | 609 | Alpha Token | 709 | Celeum |

| 410 | Traceability Chain | 510 | DACSEE | 610 | Grimm | 710 | MTC Mesh Network |

| 411 | Abyss Token | 511 | Kambria | 611 | TouchCon | 711 | TrueFeedBack |

| 412 | Naka Bodhi Token | 512 | ADAMANT Messenger | 612 | Lobstex | 712 | ZCore |

| 413 | Eterbase Coin | 513 | Merculet | 613 | Bitblocks | 713 | Agrolot |

| 414 | CashBet Coin | 514 | SBank | 614 | Sapien | 714 | Jobchain |

| 415 | Azbit | 515 | QChi | 615 | NOW Token | 715 | Global Awards Token |

| 416 | ZumCoin | 516 | YGGDRASH | 616 | GAMB | 716 | FidentiaX |

| 417 | MenaPay | 517 | Ouroboros | 617 | Xriba | 717 | Nerva |

| 418 | Fatcoin | 518 | Insureum | 618 | Alphacat | 718 | Scorum Coins |

| 419 | Netbox Coin | 519 | Sparkpoint | 619 | BitNewChain | 719 | Patron |

| 420 | VNT Chain | 520 | LHT | 620 | FLIP | 720 | TCASH |

| 421 | Cajutel | 521 | MassGrid | 621 | Nebula AI | 721 | ALL BEST ICO |

| 422 | Vexanium | 522 | QuadrantProtocol | 622 | OVCODE | 722 | wave edu coin |

| 423 | Callisto Network | 523 | KuboCoin | 623 | Plair | 723 | Membrana |

| 424 | Smartlands | 524 | Hashshare | 624 | Auxilium | 724 | PlayGame |

| 425 | TERA | 525 | Ivy | 625 | RED | 725 | Rapidz |

| 426 | GoWithMi | 526 | Banano | 626 | EUNO | 726 | Eristica |

| 427 | Egoras Dollar | 527 | DABANKING | 627 | NeuroChain | 727 | CryptoPing |

| 428 | Tolar | 528 | Ubex | 628 | Rivetz | 728 | x42 Protocol |

| 429 | Vetri | 529 | Bitsdaq | 629 | Coinsuper Ecosystem Network | 729 | Cubiex |

| 430 | WinCash | 530 | VegaWallet Token | 630 | BZEdge | 730 | OSA Token |

| 431 | 1World | 531 | Ecobit | 631 | Bancacy | 731 | EvenCoin |

| 432 | Airbloc | 532 | Liquidity Network | 632 | CrypticCoin | 732 | CREDIT |

| 433 | Pigeoncoin | 533 | Eden | 633 | Evedo | 733 | Coinlancer |

| 434 | OneLedger | 534 | Beetle Coin | 634 | Niobium Coin | 734 | EXMR FDN |

| 435 | DEX | 535 | Merebel | 635 | LocalCoinSwap | 735 | TrueDeck |

| 436 | Pivot Token | 536 | Open Platform | 636 | EBCoin | 736 | AC3 |

| 437 | Kuai Token | 537 | Locus Chain | 637 | Moneytoken | 737 | DAV Coin |

| 438 | Mcashchain | 538 | TEAM (TokenStars) | 638 | CoinUs | 738 | Jarvis+ |

| 439 | Leverj | 539 | Proxeus | 639 | Enecuum | 739 | 3DCoin |

| 440 | Databroker | 540 | BonusCloud | 640 | Noir | 740 | Silent Notary |

| 441 | Unification | 541 | Business Credit Substitute | 641 | BeatzCoin | 741 | IP Exchange |

| 442 | Blue Whale EXchange | 542 | MalwareChain | 642 | Quasarcoin | 742 | Moneynet |

| 443 | Color Platform | 543 | IQ.cash | 643 | Graviocoin | 743 | OWNDATA |

| 444 | Flowchain | 544 | Digital Gold | 644 | Max Property Group | 744 | uPlexa |

| 445 | CoinDeal Token | 545 | Brickblock | 645 | Ethereum Gold | 745 | StarCoin |

| 446 | PlatonCoin | 546 | MARK.SPACE | 646 | TigerCash | 746 | Mithril Ore |

| 447 | Krios | 547 | Conceal | 647 | DPRating | 747 | Ryo Currency |

| 448 | Nasdacoin | 548 | SafeCoin | 648 | Almeela | 748 | StarterCoin |

| 449 | LikeCoin | 549 | Spiking | 649 | Nexxo | 749 | CryptoBonusMiles |

| 450 | Okschain | 550 | COVA | 650 | smARTOFGIVING | 750 | MMOCoin |

| 451 | Bitex Global XBX Coin | 551 | PUBLISH | 651 | On.Live | 751 | FSBT API Token |

| 452 | Colu Local Network | 552 | Sessia | 652 | XcelToken Plus | 752 | PAL Network |

| 453 | Caspian | 553 | DOS Network | 653 | 0xcert | 753 | Shadow Token |

| 454 | BOOM | 554 | NeoWorld Cash | 654 | Block-Logic | 754 | Scanetchain |

| 455 | Raven Protocol | 555 | ESBC | 655 | Actinium | 755 | BlitzPredict |

| 456 | DECOIN | 556 | BitBall | 656 | MineBee | 756 | Truegame |

| 457 | Gleec | 557 | Gold Bits Coin | 657 | eXPerience Chain | 757 | EurocoinToken |

| 458 | Amoveo | 558 | CoTrader | 658 | TurtleNetwork | 758 | Typerium |

| 459 | Teloscoin | 559 | Coinsbit Token | 659 | HashCoin | 759 | Ether-1 |

| 460 | Zipper | 560 | Lisk Machine Learning | 660 | VeriSafe | 760 | TrakInvest |

| 461 | Quanta Utility Token | 561 | USDX | 661 | ZENZO | 761 | GoNetwork |

| 462 | IG Gold | 562 | SureRemit | 662 | Paytomat | 762 | Blockparty (BOXX Token) |

| 463 | ROAD | 563 | SnowGem | 663 | Seal Network | 763 | OptiToken |

| 464 | Midas | 564 | 0xBitcoin | 664 | SnodeCoin | 764 | Bigbom |

| 465 | Cloudbric | 565 | Rate3 | 665 | Bittwatt | 765 | Bethereum |

| 466 | Stronghold Token | 566 | Faceter | 666 | SpectrumCash | 766 | Sharpay |

| 467 | X-CASH | 567 | FREE Coin | 667 | WebDollar | 767 | Amino Network |

| 468 | Iconiq Lab Token | 568 | Qwertycoin | 668 | TV-TWO | 768 | PTON |

| 469 | Blockchain Certified Data Token | 569 | Gene Source Code Chain | 669 | Master Contract Token | 769 | MFCoin |

| 470 | Fountain | 570 | Golos Blockchain | 670 | BetterBetting | 770 | DeVault |

| 471 | MB8 Coin | 571 | ICE ROCK MINING | 671 | BitScreener Token | 771 | GoldFund |

| 472 | Origin Sport | 572 | REAL | 672 | Smartshare | 772 | Leadcoin |

| 473 | Tixl | 573 | PAYCENT | 673 | Vodi X | 773 | Carboneum [C8] Token |

| 474 | ParkinGo | 574 | StableUSD | 674 | Naviaddress | 774 | iDealCash |

| 475 | Ether Zero | 575 | NEXT.coin | 675 | FortKnoxster | 775 | Alt.Estate token |

| 476 | Asian Fintech | 576 | UpToken | 676 | HorusPay | 776 | EnergiToken |

| 477 | Bitcoin Confidential | 577 | SafeInsure | 677 | Ulord | 777 | MorCrypto Coin |

| 478 | DreamTeam Token | 578 | Eureka Coin | 678 | Q DAO Governance token v1.0 | 778 | Hyper Speed Network |

| 479 | nOS | 579 | DEEX | 679 | ODUWA | 779 | eSDChain |

| 480 | HashBX | 580 | ZPER | 680 | RedFOX Labs | 780 | DogeCash |

| 481 | TEMCO | 581 | Bob’s Repair | 681 | XPA | 781 | Daneel |

| 482 | Axe | 582 | Tarush | 682 | Birake | 782 | Gravity |

| 483 | BOMB | 583 | Mallcoin | 683 | savedroid | 783 | Kuende |

| 484 | HyperExchange | 584 | MIB Coin | 684 | TOKPIE | 784 | Kuverit |

| 485 | AIDUS TOKEN | 585 | Skychain | 685 | Halo Platform | 785 | Decentralized Machine Learning |

| 486 | Amon | 586 | Qredit | 686 | DeltaChain | 786 | Winco |

| 487 | Education Ecosystem | 587 | Project WITH | 687 | Mindexcoin | 787 | Monarch |

| 488 | X8X Token | 588 | Zippie | 688 | View | 788 | DOWCOIN |

| 489 | TRONCLASSIC | 589 | FYDcoin | 689 | Swace | 789 | Relex |

| 490 | Footballcoin | 590 | Howdoo | 690 | Ubcoin Market | 790 | Bitcoin CZ |

| 491 | Block-Chain.com | 591 | MidasProtocol | 691 | OLXA | 791 | Omnitude |

| 492 | SafeCapital | 592 | Shivom | 692 | Maximine Coin | 792 | Bee Token |

| 493 | POPCHAIN | 593 | Cashbery Coin | 693 | Webflix Token | 793 | RightMesh |

| 494 | Vision Industry Token | 594 | Lunes | 694 | Trittium | 794 | Catex Token |

| 495 | Opacity | 595 | Bitcoin Free Cash | 695 | Thrive Token | 795 | Bridge Protocol |

| 496 | Titan Coin | 596 | Honest | 696 | Bitcoin Incognito | 796 | Birdchain |

| 497 | Blocktrade Token | 597 | Safex Cash | 697 | Bitfex | 797 | BLOC.MONEY |

| 498 | Semux | 598 | GMB | 698 | FNKOS | 798 | Business Credit Alliance Chain |

| 499 | Uptrennd | 599 | PIXEL | 699 | Rapids | 799 | Alchemint Standards |

| 500 | Veil | 600 | Vezt | 700 | ebakus | 800 | Dynamite |

Table A3.

Names of the 1165 young coins: coins 801–1165.

Table A3.

Names of the 1165 young coins: coins 801–1165.

| 801 | Mainstream For The Underground | 901 | Blockburn | 1001 | BitRent | 1101 | Dash Green |

| 802 | WandX | 902 | LOCIcoin | 1002 | Decentralized Asset Trading Platform | 1102 | Joint Ventures |

| 803 | Blockpass | 903 | OPCoinX | 1003 | ROIyal Coin | 1103 | WXCOINS |

| 804 | ZMINE | 904 | BitCoen | 1004 | ShareX | 1104 | e-Chat |

| 805 | CryptoAds Marketplace | 905 | FUZE Token | 1005 | RefToken | 1105 | iBTC |

| 806 | CROAT | 906 | Commercium | 1006 | SHPING | 1106 | VikkyToken |

| 807 | BoatPilot Token | 907 | Hurify | 1007 | ETHplode | 1107 | CPUchain |

| 808 | Storiqa | 908 | Impleum | 1008 | Bitcoin Classic | 1108 | MiloCoin |

| 809 | Rupiah Token | 909 | Transcodium | 1009 | Bitcoin Adult | 1109 | BunnyToken |

| 810 | Ifoods Chain | 910 | Knekted | 1010 | GenesisX | 1110 | Electrum Dark |

| 811 | AiLink Token | 911 | No BS Crypto | 1011 | Intelligent Trading Foundation | 1111 | Playgroundz |

| 812 | Parachute | 912 | BlockMesh | 1012 | Zenswap Network Token | 1112 | Kora Network Token |

| 813 | Swapcoinz | 913 | PluraCoin | 1013 | Signatum | 1113 | Ragnarok |

| 814 | ONOToken | 914 | Aigang | 1014 | MetaMorph | 1114 | Escroco Emerald |

| 815 | Helium Chain | 915 | Arqma | 1015 | ShowHand | 1115 | Helper Search Token |

| 816 | Fire Lotto | 916 | Regalcoin | 1016 | 4NEW | 1116 | Fivebalance |

| 817 | The Currency Analytics | 917 | Thar Token | 1017 | GoldenPyrex | 1117 | 1X2 COIN |

| 818 | Matrexcoin | 918 | Mobile Crypto Pay Coin | 1018 | RPICoin | 1118 | Crystal Clear |

| 819 | BitClave | 919 | XMCT | 1019 | EOS TRUST | 1119 | Xenoverse |

| 820 | Zennies | 920 | Xuez | 1020 | Gold Poker | 1120 | VectorAI |

| 821 | BBSCoin | 921 | Ethouse | 1021 | Neural Protocol | 1121 | Bitcoinus |

| 822 | Civitas | 922 | Kind Ads Token | 1022 | EtherInc | 1122 | PAXEX |

| 823 | Aston | 923 | CommunityGeneration | 1023 | Sola Token | 1123 | MNPCoin |

| 824 | Bitnation | 924 | Agora | 1024 | SkyHub Coin | 1124 | Apollon |

| 825 | SRCOIN | 925 | nDEX | 1025 | Global Crypto Alliance | 1125 | Project Coin |

| 826 | PYRO Network | 926 | BTC Lite | 1026 | Level Up Coin | 1126 | Crystal Token |

| 827 | Veles | 927 | PUBLYTO Token | 1027 | Havy | 1127 | Veltor |

| 828 | BEAT | 928 | EtherSportz | 1028 | QUINADS | 1128 | Decentralized Crypto Token |

| 829 | Streamit Coin | 929 | Freyrchain | 1029 | EUNOMIA | 1129 | Fintab |

| 830 | Oxycoin | 930 | NetKoin | 1030 | EagleX | 1130 | Flit Token |

| 831 | HeartBout | 931 | REBL | 1031 | Asura Coin | 1131 | MoX |

| 832 | Atonomi | 932 | Vivid Coin | 1032 | Castle | 1132 | LiteCoin Ultra |

| 833 | SwiftCash | 933 | EveriToken | 1033 | Tourist Token | 1133 | Qbic |

| 834 | PDATA | 934 | UChain | 1034 | Gexan | 1134 | PAWS Fund |

| 835 | Artis Turba | 935 | Bitsum | 1035 | UOS Network | 1135 | Bitvolt |

| 836 | Rentberry | 936 | Cheesecoin | 1036 | Authorship | 1136 | Cannation |

| 837 | Plus-Coin | 937 | APR Coin | 1037 | WITChain | 1137 | BROTHER |

| 838 | Bitcoin Token | 938 | Soverain | 1038 | Netrum | 1138 | Silverway |

| 839 | ProxyNode | 939 | HyperQuant | 1039 | Eva Cash | 1139 | Staker |

| 840 | Signals Network | 940 | Bitcoin Zero | 1040 | YoloCash | 1140 | Cointorox |

| 841 | Giant | 941 | Narrative | 1041 | Cyber Movie Chain | 1141 | Secrets of Zurich |

| 842 | RoBET | 942 | HOLD | 1042 | TRAXIA | 1142 | Zoomba |

| 843 | XDNA | 943 | Italo | 1043 | Beacon | 1143 | Orbis Token |

| 844 | TENA | 944 | Gossip Coin | 1044 | KWHCoin | 1144 | Dinero |

| 845 | EtherGem | 945 | BLAST | 1045 | InterCrone | 1145 | Helpico |

| 846 | Vanta Network | 946 | ZeusNetwork | 1046 | ALAX | 1146 | X12 Coin |

| 847 | Linfinity | 947 | Japan Content Token | 1047 | Phonecoin | 1147 | Concoin |

| 848 | StrongHands Masternode | 948 | HYPNOXYS | 1048 | GINcoin | 1148 | LitecoinToken |

| 849 | Voise | 949 | Biotron | 1049 | Spectrum | 1149 | Xchange |

| 850 | Kalkulus | 950 | UNICORN Token | 1050 | Octoin Coin | 1150 | iBank |

| 851 | CryptoSoul | 951 | BUDDY | 1051 | Save Environment Token | 1151 | Benz |

| 852 | WOLLO | 952 | Guider | 1052 | Magic Cube Coin | 1152 | Abulaba |

| 853 | Cashpayz Token | 953 | InternationalCryptoX | 1053 | AceD | 1153 | Dystem |

| 854 | InterValue | 954 | InvestFeed | 1054 | CustomContractNetwork | 1154 | Storeum |

| 855 | WIZBL | 955 | BitStash | 1055 | ConnectJob | 1155 | QYNO |

| 856 | Ethereum Gold Project | 956 | IOTW | 1056 | Stakinglab | 1156 | Coin-999 |

| 857 | Asgard | 957 | Stipend | 1057 | wys Token | 1157 | Posscoin |

| 858 | VULCANO | 958 | CyberMusic | 1058 | Bulleon | 1158 | LRM Coin |

| 859 | Wavesbet | 959 | Herbalist Token | 1059 | GoPower | 1159 | Elliot Coin |

| 860 | HeroNode | 960 | Thingschain | 1060 | SONDER | 1160 | UltraNote Coin |

| 861 | Gentarium | 961 | Arion | 1061 | Provoco Token | 1161 | Newton Coin Project |

| 862 | Webcoin | 962 | WABnetwork | 1062 | Cryptrust | 1162 | HarmonyCoin |

| 863 | SignatureChain | 963 | EZOOW | 1063 | Atheios | 1163 | TerraKRW |

| 864 | Bitcoin Fast | 964 | Arepacoin | 1064 | ArbitrageCT | 1164 | Bitpanda Ecosystem Token |

| 865 | Fiii | 965 | Waletoken | 1065 | INDINODE | 1165 | EmberCoin |

| 866 | CrowdWiz | 966 | Datarius Credit | 1066 | TokenDesk | ||

| 867 | Fox Trading | 967 | TrustNote | 1067 | EnterCoin | ||

| 868 | Verify | 968 | Data Transaction Token | 1068 | P2P Global Network | ||

| 869 | Klimatas | 969 | CYBR Token | 1069 | FidexToken | ||

| 870 | PRASM | 970 | FantasyGold | 1070 | ICOBID | ||

| 871 | MODEL-X-coin | 971 | IGToken | 1071 | Fantasy Sports | ||

| 872 | Menlo One | 972 | Coinchase Token | 1072 | Simmitri | ||

| 873 | Arionum | 973 | Micromines | 1073 | CryptoFlow | ||

| 874 | BlockCAT | 974 | Exosis | 1074 | JavaScript Token | ||

| 875 | Version | 975 | SteepCoin | 1075 | ARAW | ||

| 876 | KAASO | 976 | TOKYO | 1076 | EthereumX | ||

| 877 | CyberFM | 977 | Galilel | 1077 | FUTURAX | ||

| 878 | Ethersocial | 978 | MesChain | 1078 | Nyerium | ||

| 879 | Neutral Dollar | 979 | Bitcoiin | 1079 | Natmin Pure Escrow | ||

| 880 | Paymon | 980 | PRiVCY | 1080 | BitMoney | ||

| 881 | Taklimakan Network | 981 | CFun | 1081 | Quantis Network | ||

| 882 | HashNet BitEco | 982 | Zealium | 1082 | onLEXpa | ||

| 883 | Netko | 983 | Connect Coin | 1083 | Akroma | ||

| 884 | ZINC | 984 | GoHelpFund | 1084 | Carebit | ||

| 885 | Asian Dragon | 985 | xEURO | 1085 | TravelNote | ||

| 886 | IFX24 | 986 | BitStation | 1086 | CCUniverse | ||

| 887 | KanadeCoin | 987 | Italian Lira | 1087 | Alpha Coin | ||

| 888 | Elementeum | 988 | Iungo | 1088 | TrueVett | ||

| 889 | LALA World | 989 | MESG | 1089 | Couchain | ||

| 890 | SiaCashCoin | 990 | Parkgene | 1090 | Absolute | ||

| 891 | CYCLEAN | 991 | BitNautic Token | 1091 | MASTERNET | ||

| 892 | Bitether | 992 | SCRIV NETWORK | 1092 | Luna Coin | ||

| 893 | INMAX | 993 | FundRequest | 1093 | BitGuild PLAT | ||

| 894 | Thore Cash | 994 | JSECOIN | 1094 | XOVBank | ||

| 895 | Guaranteed Ethurance Token Extra | 995 | AirWire | 1095 | Peerguess | ||

| 896 | Niobio Cash | 996 | Kabberry Coin | 1096 | EVOS | ||

| 897 | Social Activity Token | 997 | Digiwage | 1097 | Eurocoin | ||

| 898 | Iridium | 998 | Ether Kingdoms Token | 1098 | ICOCalendar.Today | ||

| 899 | SF Capital | 999 | BitRewards | 1099 | Dragon Option | ||

| 900 | Elysian | 1000 | BitcoiNote | 1100 | Crowdholding |

Table A4.

Names of the 838 old coins: coins 1–420.

Table A4.

Names of the 838 old coins: coins 1–420.

| 1 | Bitcoin | 106 | DeviantCoin | 211 | Peercoin | 316 | Insights Network |

| 2 | Ethereum | 107 | Storj | 212 | Namecoin | 317 | Sentinel |

| 3 | Tether | 108 | Polymath | 213 | Quark | 318 | Aeron |

| 4 | XRP | 109 | Fusion | 214 | MOAC | 319 | ChatCoin |

| 5 | Bitcoin Cash | 110 | Waltonchain | 215 | Quantum Resistant Ledger | 320 | Red Pulse Phoenix |

| 6 | Litecoin | 111 | PIVX | 216 | Stakenet | 321 | Blockmason Credit Protocol |

| 7 | Binance Coin | 112 | Cortex | 217 | Steem Dollars | 322 | Hydro Protocol |

| 8 | EOS | 113 | Storm | 218 | Kcash | 323 | Tidex Token |

| 9 | Cardano | 114 | FunFair | 219 | United Traders Token | 324 | Litecoin Cash |

| 10 | Tezos | 115 | Enigma | 220 | All Sports | 325 | Refereum |

| 11 | Chainlink | 116 | CasinoCoin | 221 | EDUCare | 326 | Counterparty |

| 12 | Stellar | 117 | Dent | 222 | CargoX | 327 | MintCoin |

| 13 | Monero | 118 | XinFin Network | 223 | Genesis Vision | 328 | MediShares |

| 14 | TRON | 119 | Hellenic Coin | 224 | BnkToTheFuture | 329 | Incent |

| 15 | Huobi Token | 120 | TrueChain | 225 | Neumark | 330 | PolySwarm |

| 16 | Ethereum Classic | 121 | Loom Network | 226 | SIRIN LABS Token | 331 | Nucleus Vision |

| 17 | Neo | 122 | Metal | 227 | Tokenomy | 332 | Blackmoon |

| 18 | Dash | 123 | Acute Angle Cloud | 228 | TE-FOOD | 333 | NAGA |