Analysis of the Influence of Online Public Opinion on Corporate Brand Value: An Efficient Way to Avoid Unexpected Shocks from the Internet

Abstract

:1. Introduction

- Analyzing the impact of OPOs on fluctuations in CBV to determine the feasibility of constructing a dynamic EWEM.

- Constructing a dynamic EWEM for CBV by developing a CBV monitoring index system based on OPOs.

- Validating the effectiveness of the proposed evaluation model using the vector auto-regressive (VAR) model.

2. Literature Review

2.1. Corporate Brand Value Evaluation Indicators

2.2. Online Public Opinion Analysis Indicators

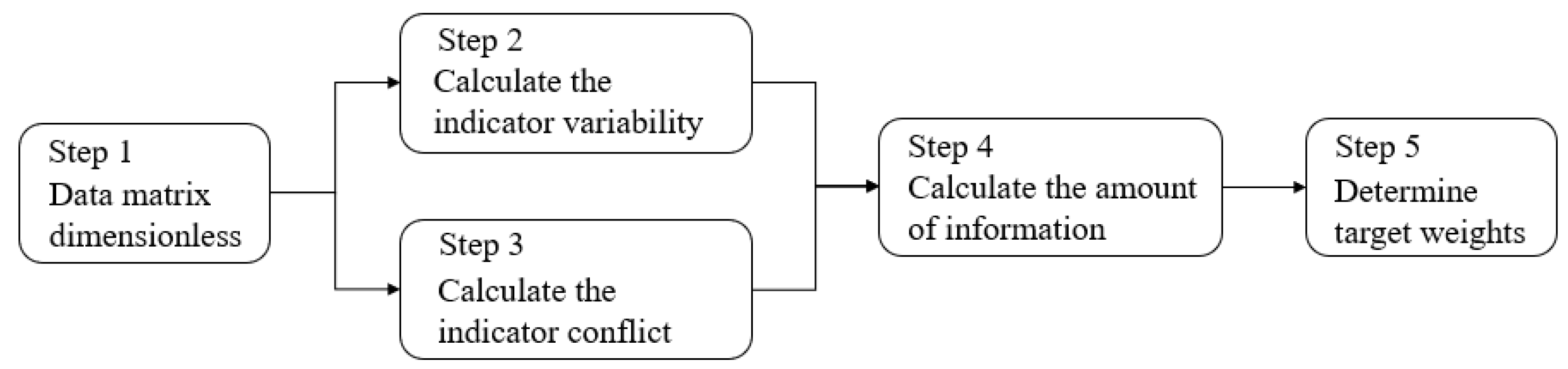

3. Method

3.1. Research Framework

3.2. Define OPO Indicators

3.3. Determine Weights of Selected OPO Indicators

4. Case Studies

4.1. Detailed Case Study: Yuyue Medical

- (1)

- Posts relevant to “Yueyue Medical” were collected from Weibo, including the corresponding number of likes, comments, and retweets. A total of 3998 posts were retrieved, and after removing duplicate content and irrelevant data, 3540 posts were deemed usable for feeding into the CBV EWEM model.

- (2)

- Posts from the official Weibo account of “Yuyue Medical”, along with their corresponding number of likes, comments, and retweets, were collected. A total 23 official posts were gathered during the observation period.

- (3)

- The daily brand Baidu index was collected from the Baidu platform.

- (4)

- Yuyue Medical’s stock price was collected from Eastmoney, a financial and securities portal in China.

4.2. Construction of the OPO Indicators System

4.2.1. Definition of OPO Indicators

4.2.2. Determination of Indicator Weights

4.3. Validation of the Constructed CBV EWEM

4.3.1. VAR Model for Early Warning Capability Evaluation

4.3.2. Selection and Estimation of Lag Order in VAR Model

4.3.3. Johansen Cointegration Test

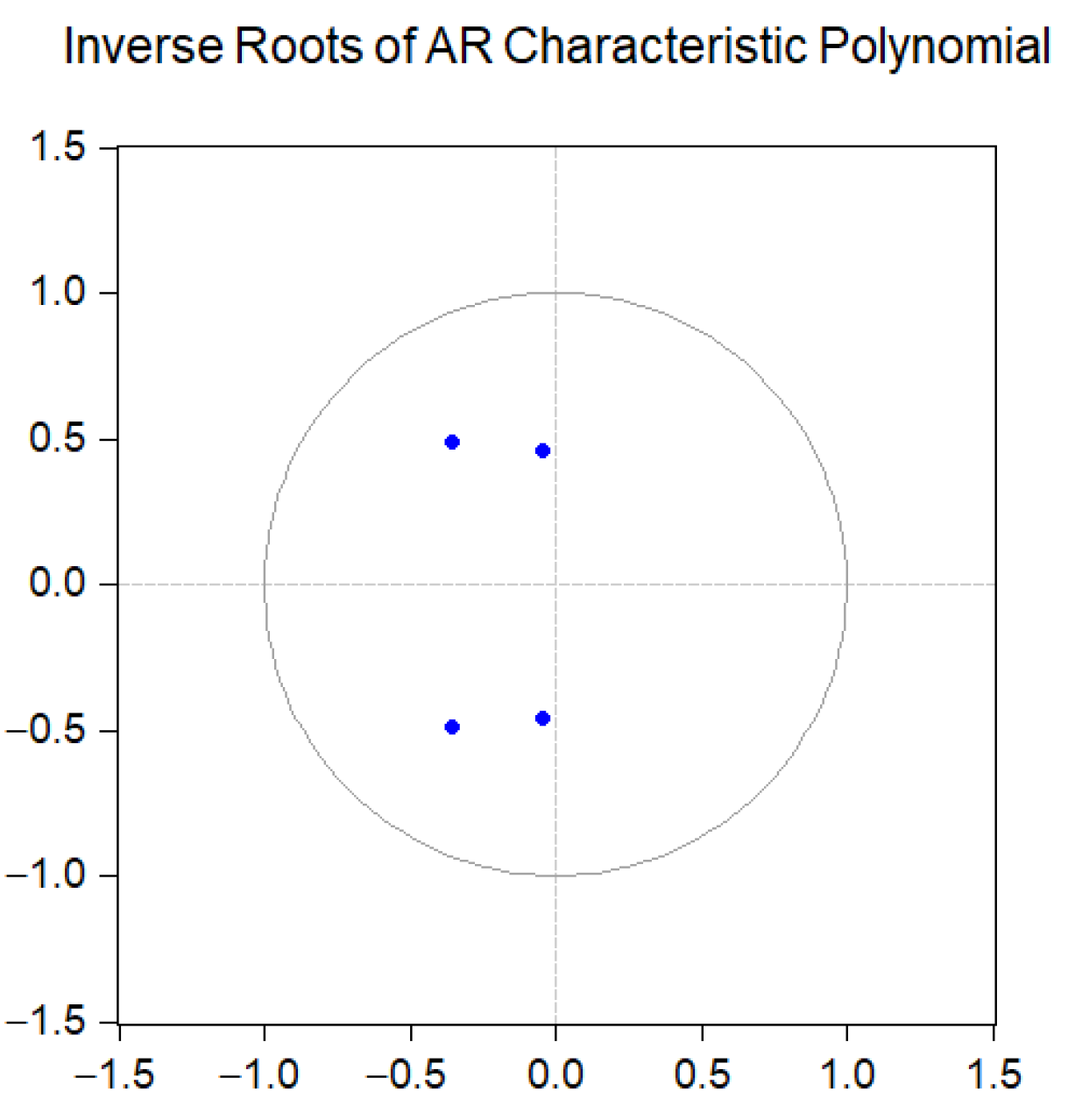

4.3.4. Stability Test of the VAR Model

4.3.5. Impulse Response Analysis

4.4. Comparisons across Different Brands

5. Discussion

6. Conclusions

- a.

- Integrating existing big data-based research on brands and OPO early warning indicators, this study employs principles of dynamism, accessibility, quantifiability, and scientific rigor to preliminarily screen indicators and constructs a set of OPO indicators related to CBV. Correlation analysis is used to assess the impact of each indicator on CBV. The improved CRITIC method is then applied to calculate the weights of these indicators, leading to the development of a CBV EWEM. The study finds that, except for the number of negative blog posts, likes, retweets, comments, and retweets on official blog posts, all other indicators are positively correlated with CBV. The number of likes on official blog posts carries the highest weight among all indicators.

- b.

- Combining the VAR model and impulse response analysis, this study investigates the dynamic impact of OPO on CBV. Impulse response analysis reveals that OPO affects CBV in the same direction, with the greatest impact on CBV in the early stage of OPO development. Subsequently, the impact shows a long-term, gradual, and stable decline. These results highlight the influence of OPO on fluctuations in CBV, demonstrating the effectiveness of the proposed evaluation model.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Rust, R.T.; Rand, W.; Huang, M.H.; Stephen, A.T.; Brooks, G.; Chabuk, T. Real-time brand reputation tracking using social media. J. Mark. 2021, 85, 21–43. [Google Scholar] [CrossRef]

- Fossen, B.L.; Schweidel, D.A. Measuring the impact of product placement with brand-related social media conversations and website traffic. Mark. Sci. 2019, 38, 481–499. [Google Scholar] [CrossRef]

- Labrecque, L.I.; Markos, E.; Yuksel, M.; Khan, T.A. Value creation (vs. value destruction) as an unintended consequence of negative comments on [innocuous] brand social media posts. J. Interact. Mark. 2022, 57, 115–140. [Google Scholar] [CrossRef]

- Bakirtas, H.; Gulpinar Demirci, V. Can Google Trends data provide information on consumer’s perception regarding hotel brands? Inf. Technol. Tour. 2022, 24, 57–83. [Google Scholar] [CrossRef]

- Parris, D.L.; Guzman, F. Evolving brand boundaries and expectations: Looking back on brand equity, brand loyalty, and brand image research to move forward. J. Prod. Brand Manag. 2023, 32, 191–234. [Google Scholar] [CrossRef]

- Oliveira, M.O.R.d.; Heldt, R.; Silveira, C.S.; Luce, F.B. Brand equity chain and brand equity measurement approaches. Mark. Intell. Plan. 2023, 41, 442–456. [Google Scholar] [CrossRef]

- Melović, B.; Vukčević, M.; Dabić, M. The Midas touch of branding: Banks’ brand value, intellectual capital and the optimization of the Interbrand methodology. J. Intellect. Cap. 2021, 22, 92–120. [Google Scholar] [CrossRef]

- Bharadwaj, N.; Hanssens, D.M.; Rao, R.K. Corporate brand value and cash holdings. J. Brand Manag. 2020, 27, 408–420. [Google Scholar] [CrossRef]

- He, J.; Calder, B.J. The experimental evaluation of brand strength and brand value. J. Bus. Res. 2020, 115, 194–202. [Google Scholar] [CrossRef]

- Cuesta-Valino, P.; Gutierrez-Rodriguez, P.; Sierra-Fernandez, M.P.; Aguirre Garcia, M.B. Measuring a multidimensional green brand equity: A tool for entrepreneurship development. Br. Food J. 2021, 123, 3326–3343. [Google Scholar] [CrossRef]

- Wang, W.; Wu, D. Construction of rural tourism brand value management model from the perspective of big data. Comput. Intell. Neurosci. 2022, 2022, 5623782. [Google Scholar] [CrossRef] [PubMed]

- Sankaran, R.; Chakraborty, S. Measuring consumer perception of overall brand equity drivers for m-payments. Int. J. Bank Mark. 2023, 41, 130–157. [Google Scholar] [CrossRef]

- Huang, Y.; Yang, S.; Zhu, Q. Brand equity and the COVID-19 stock market crash: Evidence from US listed firms. Financ. Res. Lett. 2021, 43, 101941. [Google Scholar] [CrossRef]

- Swaminathan, V.; Gupta, S.; Keller, K.L.; Lehmann, D. Brand actions and financial consequences: A review of key findings and directions for future research. J. Acad. Mark. Sci. 2022, 50, 639–664. [Google Scholar] [CrossRef]

- Farhang, M.; Kamran-Disfani, O.; H. Zadeh, A. Brand equity and stock performance in time of crisis: Evidence from the COVID-19 pandemic. J. Prod. Brand Manag. 2023, 32, 420–435. [Google Scholar] [CrossRef]

- Laghi, E.; Di Marcantonio, M.; Cillo, V.; Paoloni, N. The relational side of intellectual capital: An empirical study on brand value evaluation and financial performance. J. Intellect. Cap. 2022, 23, 479–515. [Google Scholar] [CrossRef]

- Bhaskaran, R.K.; Sujit, K.S.; Waheed, K.A. Linkage Between Brand Value and Firm Performance: An Empirical Examination Using Fuzzy Set Qualitative Comparative Analysis. SAGE Open 2023, 13. [Google Scholar] [CrossRef]

- Wang, H.; Luo, L.; Liu, T. Applying the DEMATEL- ANP Fuzzy Comprehensive Model to Evaluate Public Opinion Events. Appl. Sci. 2023, 13, 5737. [Google Scholar] [CrossRef]

- Peng, L.J.; Shao, X.G.; Huang, W.M. Research on the early-warning model of network public opinion of major emergencies. IEEE Access 2021, 9, 44162–44172. [Google Scholar] [CrossRef]

- Meng, F.; Xiao, X.; Wang, J. Rating the crisis of online public opinion using a multi-level index system. arXiv 2022, arXiv:2207.14740. [Google Scholar] [CrossRef]

- Chen, M.; An, L.; Li, G.; Yu, C. Severity assessment and the early warning mechanism of public events based on the comparison of microblogging characteristics. Inf. Technol. People 2023, 36, 2543–2562. [Google Scholar] [CrossRef]

- Shen, Y.; Bian, S.; Song, X.; Geng, X. Research on Risk Assessment of Enterprise Public Opinion in Cross Social Media Context and Sustainable Development Strategies. Sustainability 2024, 16, 1700. [Google Scholar] [CrossRef]

- Chung, S.; Shin, D.; Park, J. Predicting firm market performance using the social media promoter score. Mark. Lett. 2022, 33, 545–561. [Google Scholar] [CrossRef]

- Kafeza, E.; Rompolas, G.; Kyriazidis, S.; Makris, C. Time-Series Clustering for Determining Behavioral-Based Brand Loyalty of Users Across Social Media. IEEE Trans. Comput. Soc. Syst. 2022, 10, 1951–1965. [Google Scholar] [CrossRef]

- Urolagin, S.; Patel, S. User-specific loyalty measure and prediction using deep neural network from Twitter Data. IEEE Trans. Comput. Soc. Syst. 2024, 11, 1046–1061. [Google Scholar] [CrossRef]

- Song, J.; Zhu, X. Research on public opinion guidance of converging media based on AHP and transmission dynamics. Math Biosci Eng 2021, 18, 6857–6886. [Google Scholar] [CrossRef]

- Ouyang, Z.s.; Lai, Y. Systemic financial risk early warning of financial market in China using Attention-LSTM model. N. Am. J. Econ. Financ. 2021, 56, 101383. [Google Scholar] [CrossRef]

- Zhang, M.; Xu, H.; Ma, N.; Pan, X. Intelligent vehicle sales prediction based on online public opinion and online search index. Sustainability 2022, 14, 10344. [Google Scholar] [CrossRef]

- Han, W.; Xiao, L.; Wu, X.; He, D.; Wang, Z.; Li, S. Construction of the social network information dissemination index system based on CNNs. Front. Phys. 2022, 10, 807099. [Google Scholar] [CrossRef]

- Yang, S. Analysis of Network Public Opinion in New Media Based on BP Neural Network Algorithm. Mob. Inf. Syst. 2022, 2022, 3202099. [Google Scholar] [CrossRef]

- Krebs, I.; Lischka, J.A. Is audience engagement worth the buzz? The value of audience engagement, comment reading, and content for online news brands. Journalism 2019, 20, 714–732. [Google Scholar] [CrossRef]

- Zhu, R.; Ding, Q.; Yu, M.; Wang, J.; Ma, M. Early warning scheme of COVID-19 related internet public opinion based on RVM-L model. Sustain. Cities Soc. 2021, 74, 103141. [Google Scholar] [CrossRef]

- Kontokosta, C.E.; Freeman, L.; Lai, Y. Up-and-Coming or Down-and-Out? Social Media Popularity as an Indicator of Neighborhood Change. J. Plan. Educ. Res. 2024, 44, 662–673. [Google Scholar] [CrossRef]

- Zhang, Z.; Xiao, Y.; Fu, Z.; Zhong, K.; Niu, H. A study on early warnings of financial crisis of Chinese listed companies based on DEA–SVM model. Mathematics 2022, 10, 2142. [Google Scholar] [CrossRef]

- Li, J.; Ma, Y.; Xu, X.; Pei, J.; He, Y. A study on epidemic information screening, prevention and control of public opinion based on health and medical big data: A case study of COVID-19. Int. J. Environ. Res. Public Health 2022, 19, 9819. [Google Scholar] [CrossRef]

- Ma, Y.; Wu, P.; Ling, C.; Ding, S. Research on public opinion effecting on stock price during crises based on model checking. Expert Syst. Appl. 2024, 249, 123442. [Google Scholar] [CrossRef]

- Yang, Z.; Jiang, H.; Huang, L.; Liu, Y. Multi Feature Extraction and Trend Prediction for Weibo Topic Dissemination Network. J. Signal Process. Syst. 2024, 96, 1–17. [Google Scholar] [CrossRef]

- Ren, R.; Wu, D. An innovative sentiment analysis to measure herd behavior. IEEE Trans. Syst. Man Cybern. Syst. 2018, 50, 3841–3851. [Google Scholar] [CrossRef]

- Shapiro, A.H.; Sudhof, M.; Wilson, D.J. Measuring news sentiment. J. Econom. 2022, 228, 221–243. [Google Scholar] [CrossRef]

- Xu, Y.; Wang, J.; Chen, Z.; Liang, C. Sentiment indices and stock returns: Evidence from China. Int. J. Financ. Econ. 2023, 28, 1063–1080. [Google Scholar] [CrossRef]

- Xu, L.; Lin, H.; Pan, Y.; Ren, H.; Chen, J. Constructing the affective lexicon ontology. J. China Soc. Sci. Tech. Inf. 2008, 27, 180–185. [Google Scholar]

- Krishnan, A.R.; Kasim, M.M.; Hamid, R.; Ghazali, M.F. A modified CRITIC method to estimate the objective weights of decision criteria. Symmetry 2021, 13, 973. [Google Scholar] [CrossRef]

- Jiang, C.; Wang, J.; Tang, Q.; Lyu, X. Investigating the effects of dimension-specific sentiments on product sales: The perspective of sentiment preferences. J. Assoc. Inf. Syst. 2021, 22, 459. [Google Scholar] [CrossRef]

- Ahmed, S.F.; Mohsin, A.; Islam, K.Z.; Hossain, S.F.A. Relationship between greenfield investment and economic growth: Evidence from Bangladesh. Heliyon 2023, 9, e17547. [Google Scholar] [CrossRef] [PubMed]

- Sohaib, M.; Han, H. Building value co-creation with social media marketing, brand trust, and brand loyalty. J. Retail. Consum. Serv. 2023, 74, 103442. [Google Scholar] [CrossRef]

- Seifert, C.; Kwon, W.S. SNS eWOM sentiment: Impacts on brand value co-creation and trust. Mark. Intell. Plan. 2020, 38, 89–102. [Google Scholar] [CrossRef]

- Wang, X.; Wang, Y.; Lin, X.; Abdullat, A. The dual concept of consumer value in social media brand community: A trust transfer perspective. Int. J. Inf. Manag. 2021, 59, 102319. [Google Scholar] [CrossRef]

- Lim, J.S.; Pham, P.; Heinrichs, J.H. Impact of social media activity outcomes on brand equity. J. Prod. Brand Manag. 2020, 29, 927–937. [Google Scholar] [CrossRef]

- Xu, J.; Guo, D.; Liu, S. How social media expedites the crisis spillover effect: A case study of Tesla’s recall event. Public Relations Rev. 2024, 50, 102432. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| OPO Indicators | Occurrence Frequency | Literatures on CBV | Literatures on OPO |

|---|---|---|---|

| posts | 0.6875 | [23,24,25] | [18,19,20,21,22,26,27,28,29,30] |

| comments | 0.6875 | [3,31] | [18,19,20,21,22,26,27,29,30,32] |

| retweets | 0.625 | [23,25] | [18,19,20,21,22,26,29,30,32] |

| positive posts | 0.625 | [25] | [18,20,21,22,28,29,30,33,34] |

| negative posts | 0.625 | [23] | [18,20,21,22,28,29,30,33,34] |

| sentiment | 0.5625 | [23,24,25] | [21,22,29,30,34,35,36,37] |

| likes | 0.5625 | [23,25] | [18,19,20,21,26,29,30,32] |

| search | 0.5 | [4] | [18,19,20,22,28,36,37] |

| OPO Indicators | BB Indicators |

|---|---|

| posts | number of positive blog posts |

| number of negative blog posts | |

| positive increment in blog posts | |

| comments | number of positive blog comments |

| number of negative blog comments | |

| positive increment in blog comments | |

| comments on official blog posts | |

| retweets | number of positive blog retweets |

| number of negative blog retweets | |

| positive increment in blog retweets | |

| number of retweets on official blog posts | |

| sentiment | sentiment tendency |

| trust tendency | |

| likes | number of positive blog likes |

| number of negative blog likes | |

| positive increment in blog likes | |

| number of likes on official blog posts | |

| search | total search volume of brand keywords |

| Independent Variable | Correlation Coefficient (Significance) |

|---|---|

| number of positive blog posts | 0.304 (0.001 ***) |

| number of positive blog likes | 0.264 (0.005 ***) |

| number of positive blog retweets | 0.198 (0.043 **) |

| number of positive blog comments | 0.322 (0.001 ***) |

| number of negative blog posts | 0.077 (0.433) |

| number of negative blog likes | 0.035 (0.726) |

| number of negative blog retweets | 0.056 (0.585) |

| number of negative blog comments | 0.068 (0.497) |

| positive increment in blog posts | 0.209 (0.027 **) |

| positive increment in blog likes | 0.192 (0.037 **) |

| positive increment in blog retweets | 0.164 (0.088 *) |

| positive increment in blog comments | 0.262 (0.005 ***) |

| sentiment tendency | 0.213 (0.023 **) |

| trust tendency | 0.271 (0.004 ***) |

| number of likes on official blog posts | 0.229 (0.025 **) |

| number of retweets on official blog posts | 0.061 (0.561) |

| number of comments on official blog posts | 0.217 (0.034 **) |

| total search volume of brand keywords | 0.246 (0.006 ***) |

| Indicators | Variability | Conflict | Amount of Information | Weights |

|---|---|---|---|---|

| number of positive blog posts | 0.182 | 0.417 | 0.076 | 0.074 |

| number of positive blog likes | 0.132 | 0.454 | 0.060 | 0.059 |

| number of positive blog retweets | 0.162 | 0.424 | 0.069 | 0.067 |

| number of positive blog comments | 0.144 | 0.416 | 0.060 | 0.059 |

| positive increment in blog posts | 0.131 | 0.435 | 0.057 | 0.056 |

| positive increment in blog likes | 0.120 | 0.382 | 0.046 | 0.045 |

| positive increment in blog retweets | 0.117 | 0.376 | 0.043 | 0.043 |

| positive increment in blog comments | 0.142 | 0.407 | 0.058 | 0.057 |

| sentiment tendency | 0.206 | 0.595 | 0.123 | 0.120 |

| trust tendency | 0.150 | 0.577 | 0.086 | 0.085 |

| number of likes on official blog posts | 0.191 | 0.737 | 0.141 | 0.138 |

| number of comments on official blog posts | 0.169 | 0.685 | 0.116 | 0.114 |

| total search volume of brand keywords | 0.193 | 0.441 | 0.085 | 0.083 |

| Information Criteria | Formula |

|---|---|

| AIC | AIC = |

| BIC | BIC = |

| HQ | HQ = |

| FPE | FPE = |

| Variable | ADF Statistic | 1% Level | 5% Level | 10% Level | Conclusion |

|---|---|---|---|---|---|

| STOCK | −2.074 | −3.551 | −2.914 | −2.595 | unstable |

| D(STOCK) | −3.024 *** | −3.568 | −2.921 | −2.599 | stable |

| BVPOI | −2.383 | −3.555 | −2.916 | −2.596 | unstable |

| D(BVPOI) | −4.268 *** | −3.585 | −2.928 | −2.602 | stable |

| Lag Order | AIC | SC | HQ | FPE |

|---|---|---|---|---|

| 0 | −4.32 | −4.249 | −4.292 | 0.013 |

| 1 | −5.867 | −5.651 * | −5.783 | 0.003 |

| 2 | −5.986 * | −5.625 | −5.846 * | 0.003 * |

| 3 | −5.94 | −5.429 | −5.743 | 0.003 |

| 4 | −5.798 | −5.135 | −5.542 | 0.003 |

| 5 | −5.648 | −4.83 | −5.333 | 0.004 |

| Null Hypothesis | Eigenvalue | Trace | 10% Level | 5% Level | 1% Level |

|---|---|---|---|---|---|

| None | 0.18 | 16.105 | 13.429 | 15.494 | 19.935 |

| At most 1 | 0.09 | 5.195 | 2.705 | 3.841 | 6.635 |

| Lag Order | AIC | SC | HQ | FPE |

|---|---|---|---|---|

| 0 | −1.059 | −0.991 | −1.033 | 0.347 |

| 1 | −3.369 | −3.163 * | −3.288 | 0.034 |

| 2 | −3.425 | −3.079 | −3.289 * | 0.033 |

| 3 | −3.446 * | −2.957 | −3.254 | 0.032 * |

| 4 | −3.283 | −2.649 | −3.036 | 0.038 |

| 5 | −3.151 | −2.369 | −2.846 | 0.043 |

| Brand Name | Correlation Coefficient (BVPOI and Stock) | Lag Order | Time Lag between BVPOI and Stock (Impulse Response Analysis) |

|---|---|---|---|

| Yuyue Medical | 0.359 *** | 2 | Reaches its peak in the 3rd period |

| LI-NING | 0.567 *** | 3 | Reaches its peak in the 6th period |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fei, H.; Zhu, J. Analysis of the Influence of Online Public Opinion on Corporate Brand Value: An Efficient Way to Avoid Unexpected Shocks from the Internet. Systems 2024, 12, 337. https://doi.org/10.3390/systems12090337

Fei H, Zhu J. Analysis of the Influence of Online Public Opinion on Corporate Brand Value: An Efficient Way to Avoid Unexpected Shocks from the Internet. Systems. 2024; 12(9):337. https://doi.org/10.3390/systems12090337

Chicago/Turabian StyleFei, Hongying, and Jinyin Zhu. 2024. "Analysis of the Influence of Online Public Opinion on Corporate Brand Value: An Efficient Way to Avoid Unexpected Shocks from the Internet" Systems 12, no. 9: 337. https://doi.org/10.3390/systems12090337