Sustainability Reporting Based on GRI Standards within Organizations in Romania

Abstract

:1. Introduction

- Climate action, reducing emissions to reduce global warming

- Decent work and economic growth, ensuring sustainable development through innovation and infrastructure investments, eliminating inequality in the workplace, ensuring a child exploitation prevention policy

- Clean energy at affordable prices, encouraging the use of alternative energy sources with reduced environmental impact

- Responsible consumption and production, optimization of technological processes, analysis of suppliers and supply chains

- Health and well-being, policies regarding labor protection, and ensuring a clean environment are essential to ensure a healthy life

- Aquatic life, the actions that companies take, such as the discharge of residual substances, should not endanger marine resources

- Terrestrial life, organizations should not affect existing ecosystems with their actions.

- Gender equality, company policies shall consider ensuring gender equality at all hierarchical levels

- Quality education, by promoting continuous learning, organizations obtain qualified personnel and contribute thus to educating the community

- Peace, justice, and efficient institutions entail transparency in the policies on anti-corruption and tax evasion.

2. Literature Review

- Standards regarding the economic dimension (GRI 200) tackle market presence, economic performance, indirect economic impact, anti-corruption practices, anti-competitive behavior, taxes, etc.

- Standards regarding the environmental dimension (GRI 300) include several topics: recycled materials, direct and indirect energy and water consumption, biodiversity, emissions, waste, etc.

- Standards regarding the social dimension (GRI 400) include several topics referring to employment, work relations, workplace health and safety, formation and education, equal benefits for both men and women, investment and public procurement practices, local communities, customer health, and security, etc.

3. Research Methodology

- Collecting sustainability reports

- Analyzing the correlations between the information on sustainability and the economic profile of the companies: total incomes, total expenses, net profit, etc.

- Establishing the results.

- 0 for the consumer goods and services sector

- 1 for the industry, oil and gas sector

- 2 for the financial sector

4. Data Analysis

- H0: μ1 = μ2 there are no statistically significant differences as regards the sustainability reporting performance expressed by the sustainability score (T) depending on the industrial sector (SE).

- H1: μ1 <> μ2 there are statistically significant differences as regards the sustainability reporting performance expressed by the sustainability score (T) depending on the industrial sector (SE).

- There is a moderate direct correlation between the sustainability report score (T) and total incomes (LOG_TV) at a 0.249 coefficient, slightly smaller than the moderate direct correlation between the sustainability report score (T) and total expenses (LOG_CH) at a 0.254 coefficient. We found that the sustainability report score has a moderately positive impact on two important indicators that measure the economic activity of a company—its income and expenses. The two indicators are two essential pillars for the net profit of companies.

- There is a moderate inverse correlation between the industry’s environmental sensitivity (SE) and the organization’s profit (LOG_PN) at a coefficient of −0.372. Therefore, organizations operating in environmentally sensitive industries (oil and gas) have a lower yield than those working in sectors that are not ecologically sensitive.

- There is no statistically significant correlation between the page count of a sustainability report and the other variables. Therefore, the analysis reveals that the page count of a sustainability report has no impact on the reliability of sustainability reporting or the economic performance of companies.

- There are statistically significant high direct correlations between the variables (LOG_PN, LOG_TV, LOG_CH) for the companies’ economic profile, reflecting the consistency of the financial data and their interdependence.

- H2. The company’s economic performance, expressed by the net profit, is influenced positively by the company policies on waste management, expressed by the GRI index in the sustainability report.

- H3. The company’s economic performance, expressed by the net profit, is influenced positively by the company policies on the optimization of supply chains, expressed by the GRI index in the sustainability report.

- H4. The company’s economic performance, expressed by the net profit, is influenced positively by the company’s procurement policies, expressed by the GRI index in the sustainability report.

5. Conclusions and Limitations

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Borges, F.M.M.G.; Rampasso, I.S.; Quelhas, O.L.G.; Leal Filho, W.; Anholon, R. Addressing the UN SDGs in Sustainability Reports: An Analysis of Latin American Oil and Gas Companies. Environ. Chall. 2022, 7, 100515. [Google Scholar] [CrossRef]

- ONU Transforming Our World: The 2030 Agenda for Sustainable Development | Department of Economic and Social Affairs. Available online: https://sdgs.un.org/2030agenda (accessed on 20 December 2022).

- Boiral, O.; Heras-Saizarbitoria, I. Sustainability Reporting Assurance: Creating Stakeholder Accountability through Hyperreality? J. Clean. Prod. 2020, 243, 118596. [Google Scholar] [CrossRef]

- Tschopp, D.; Nastanski, M. The Harmonization and Convergence of Corporate Social Responsibility Reporting Standards. J. Bus. Ethics 2014, 125, 147–162. [Google Scholar] [CrossRef]

- Toman, M.; Pezzey, J. The Economics of Sustainability: A Review of Journal Articles; Resources for the Future: Washington, DC, USA, 2002. [Google Scholar]

- Kolk, A.; van der Veen, M.; Hay, K.; Wennink, D. KPMG International Survey of Corporate Sustainability Reporting 2002; De Meern: KPMG: Utrecht, The Netherlands, 2002. [Google Scholar]

- GRI—Home. Available online: https://www.globalreporting.org/ (accessed on 19 December 2022).

- Matuszak, Ł.; Różańska, E. Towards 2014/95/EU Directive Compliance: The Case of Poland. Sustain. Account. Manag. Policy J. 2021, 12, 1052–1076. [Google Scholar] [CrossRef]

- Barbosa, C.D.F.; Francato, A.L.; Barbosa, P.S.F. Towards Brazilian Corporations Better Stock Price Valuation and Operational Performance with Corporate Social Responsibility and Environmental Socio Responsibility. In Corporate Social Responsibility in Brazil; Springer International Publishing: Berlin/Heidelberg, Germany, 2019. [Google Scholar]

- European Court Of Auditors Rapid Case Review: Reporting on Sustainability: A Stocktake of EU Institutions and Agencies. Available online: https://www.eca.europa.eu/Lists/ECADocuments/RCR_Reporting_on_sustainability/RCR_Reporting_on_sustainability_EN.pdf (accessed on 19 December 2022).

- Roca, L.C.; Searcy, C. An Analysis of Indicators Disclosed in Corporate Sustainability Reports. J. Clean. Prod. 2012, 20, 103–118. [Google Scholar] [CrossRef]

- Pati, S. Sustainability Reporting Pathway—Is It a True Reflection of Organisational Safety Culture: Insights from Oil and Gas and Process Sector of India. Saf. Sci. 2023, 159, 106006. [Google Scholar] [CrossRef]

- The International Integrated Reporting Council (IIRC) Investors Support Integrated Reporting as a Route to Better Understanding of Performance. Available online: https://www.integratedreporting.org/wp-content/uploads/2017/09/Investor-statement_FinalS.pdf (accessed on 21 December 2022).

- Novick, B.; Fink, L. A Fundamental Reshaping of Finance. Harvard Law School Forum on Corporate Governance, 16 January 2020. [Google Scholar]

- Grassmann, M. The Relationship between Corporate Social Responsibility Expenditures and Firm Value: The Moderating Role of Integrated Reporting. J. Clean. Prod. 2021, 285, 124840. [Google Scholar] [CrossRef]

- Ching, H.; Gerab, F.; Toste, T. Analysis of Sustainability Reports and Quality of Information Disclosed of Top Brazilian Companies. Int. Bus. Res. 2013, 6, 62. [Google Scholar] [CrossRef] [Green Version]

- European Commission (EC) Directive 2014/95/EU of the European Parliament and the Council of 22 October 2014 Amending Directive 2013/34/EU as Regards Disclosure of Non-Financial and Diversity Information by Certain Large Undertakings and Groups. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:32014L0095 (accessed on 21 December 2022).

- Gray, R.; Javad, M.; Power, D.M.; Sinclair, C.D. Social and Environmental Disclosure and Corporate Characteristics: A Research Note and Extension. J. Bus. Financ. Account. 2001, 28, 327–356. [Google Scholar] [CrossRef]

- European Commission (EC) Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 Amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as Regards Corporate Sustainability Reporting (Text with EEA Relevance). Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv%3AOJ.L_.2022.322.01.0015.01.ENG&toc=OJ%3AL%3A2022%3A322%3ATOC (accessed on 21 December 2022).

- Carmo, C.; Ribeiro, C. Mandatory Non-Financial Information Disclosure under European Directive 95/2014/EU: Evidence from Portuguese Listed Companies. Sustainability 2022, 14, 4860. [Google Scholar] [CrossRef]

- Karaman, A.S.; Orazalin, N.; Uyar, A.; Shahbaz, M. CSR Achievement, Reporting, and Assurance in the Energy Sector: Does Economic Development Matter? Energy Policy 2021, 149, 112007. [Google Scholar] [CrossRef]

- Gray, R.; Kouhy, R.; Lavers, S. Corporate Social and Environmental Reporting: A Review of the Literature and a Longitudinal Study of UK Disclosure. Account. Audit. Account. J. 1995, 8, 47–77. [Google Scholar] [CrossRef]

- Yadava, R.N.; Sinha, B. Scoring Sustainability Reports Using GRI 2011 Guidelines for Assessing Environmental, Economic, and Social Dimensions of Leading Public and Private Indian Companies. J. Bus. Ethics 2016, 138, 549–558. [Google Scholar] [CrossRef]

- Ministry of Public Finance Order Regarding the Modification and Completation of Some Accounting Regulations No. 1938/2016 of 17 August 2016. Off. Gaz. 2016, 680. Available online: https://static.anaf.ro/static/10/Anaf/legislatie/OMFP_1938_2016.pdf (accessed on 10 December 2022).

- Lungu, C.I.; Caraiani, C.; Dascălu, C. Research on Corporate Social Responsibility Reporting. Amfiteatru Econ. J. 2011, 13, 117–131. [Google Scholar]

- Tiron-Tudor, A.; Nistor, C.S.; Ştefănescu, C.A.; Zanellatto, G. Encompassing Non-Financial Reporting in A Coercive Framework for Enhancing Social Responsibility: Romanian Listed Companies’ Case. Amfiteatru Econ. 2019, 21, 590–606. [Google Scholar] [CrossRef]

- Galant, A.; Cerne, K. Non-Financial Reporting in Croatia: Current Trends Analysis and Future Perspectives. Management 2017, 12, 41–58. [Google Scholar] [CrossRef]

- Gunawan, J.; Permatasari, P.; Fauzi, H. The Evolution of Sustainability Reporting Practices in Indonesia. J. Clean. Prod. 2022, 358, 131798. [Google Scholar] [CrossRef]

- Garcia, A.S.; Mendes-Da-Silva, W.; Orsato, R.J. Sensitive Industries Produce Better ESG Performance: Evidence from Emerging Markets. J. Clean. Prod. 2017, 150, 135–147. [Google Scholar] [CrossRef]

- Sierra-Garcia, L.; Garcia-Benau, M.A.; Bollas-Araya, H.M. Empirical Analysis of Non-Financial Reporting by Spanish Companies. Adm. Sci. 2018, 8, 29. [Google Scholar] [CrossRef] [Green Version]

- GRI—GRI Standards English Language. Available online: https://www.globalreporting.org/how-to-use-the-gri-standards/gri-standards-english-language/ (accessed on 19 December 2022).

- Opferkuch, K.; Caeiro, S.; Salomone, R.; Ramos, T.B. Circular Economy Disclosure in Corporate Sustainability Reports: The Case of European Companies in Sustainability Rankings. Sustain. Prod. Consum. 2022, 32, 436–456. [Google Scholar] [CrossRef]

- Perello-Marin, M.R.; Rodríguez-Rodríguez, R.; Alfaro-Saiz, J.-J. Analysing GRI Reports for the Disclosure of SDG Contribution in European Car Manufacturers. Technol. Forecast. Soc. Chang. 2022, 181, 121744. [Google Scholar] [CrossRef]

- Ibáñez- Forés, V.; Martínez-Sánchez, V.; Valls-Val, K.; Bovea, M.D. Sustainability Reports as a Tool for Measuring and Monitoring the Transition towards the Circular Economy of Organisations: Proposal of Indicators and Metrics. J. Environ. Manag. 2022, 320, 115784. [Google Scholar] [CrossRef] [PubMed]

- Michalska-Szajer, A.; Klimek, H.; Dąbrowski, J. A Comparative Analysis of CSR Disclosure of Polish and Selected Foreign Seaports. Case Stud. Transp. Policy 2021, 9, 1112–1121. [Google Scholar] [CrossRef]

- Ibáñez-Forés, V.; Martínez-Sánchez, V.; Valls-Val, K.; Bovea, M.D. How Do Organisations Communicate Aspects Related to Their Social Performance? A Proposed Set of Indicators and Metrics for Sustainability Reporting. Sustain. Prod. Consum. 2023, 35, 157–172. [Google Scholar] [CrossRef]

- Patara, S.; Dhalla, R. Sustainability Reporting Tools: Examining the Merits of Sustainability Rankings. J. Clean. Prod. 2022, 366, 132960. [Google Scholar] [CrossRef]

- Al-Shaer, H.; Hussainey, K. Sustainability Reporting beyond the Business Case and Its Impact on Sustainability Performance: UK Evidence. J. Environ. Manag. 2022, 311, 114883. [Google Scholar] [CrossRef] [PubMed]

- Yan, M.; Jia, F.; Chen, L.; Yan, F. Assurance Process for Sustainability Reporting: Towards a Conceptual Framework. J. Clean. Prod. 2022, 377, 134156. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Does It Pay to Be Really Good? Addressing the Shape of the Relationship between Social and Financial Performance. Strateg. Manag. J. 2012, 33, 1304–1320. [Google Scholar] [CrossRef]

- Pekovic, S.; Grolleau, G.; Mzoughi, N. Environmental Investments: Too Much of a Good Thing? Int. J. Prod. Econ. 2018, 197, 297–302. [Google Scholar] [CrossRef]

- Duran, I.J.; Rodrigo, P. Why Do Firms in Emerging Markets Report? A Stakeholder Theory Approach to Study the Determinants of Non-Financial Disclosure in Latin America. Sustainability 2018, 10, 3111. [Google Scholar] [CrossRef] [Green Version]

- Venturelli, A.; Caputo, F.; Cosma, S.; Leopizzi, R.; Pizzi, S. Directive 2014/95/EU: Are Italian Companies Already Compliant? Sustainability 2017, 9, 1385. [Google Scholar] [CrossRef]

- Amin, M.A.; Islam, M.R.; Halim, M.A. Sustainability Reporting Based on GRI Indicators. J. Sustain. Bus. Econ. 2022, 5, 1–13. [Google Scholar] [CrossRef]

- Top Companies from Romania. Available online: https://www.topfirme.com/numar-angajati/ (accessed on 21 December 2022).

- Ministry of Public Finance Order Regarding the Modification and Completation of Some Accounting Regulations, No. 3456/2018. Off. Gaz. 2018, 942. Available online: https://static.anaf.ro/static/10/Anaf/legislatie/OMFP_3456_2018.pdf (accessed on 10 December 2022).

- The Jamovi Project Jamovi—Open Statistical Software for the Desktop and Cloud (Version 2.3). Available online: https://www.Jamovi.Org (accessed on 20 December 2022).

- Ministry of Justice; National Trade Register Office. Sindla.com Classification of Activities in the National Economy. Available online: https://caen.ro (accessed on 20 December 2022).

- 2020 Corruption Perceptions Index—Explore Romania’s Results. Available online: https://www.transparency.org/en/cpi/2020 (accessed on 19 December 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable Code | Variable Name/Description | Reference |

|---|---|---|

| A. Variables for the economic profile of the companies | ||

| LOG_TV | Natural logarithm of the total incomes at the end of the fiscal year. It is an essential indicator for shareholders, as a part of the net income is granted to shareholders as dividends. | [42] |

| LOG_CH | Natural logarithm of the total expenses at the end of the fiscal year. | |

| LOG_PN | Natural logarithm of the net profit at the end of the fiscal year. | [41] |

| SE | Industry environmental sensitivity: “0” (consumer goods and services); “1” (industry, oil & gas); “2” (financial) | [26,28,30] |

| B. Variables for sustainability reporting | ||

| RepPages | The page count of the sustainability reportIt may reflect the degree to which sustainability concerns are detailed. | [25] |

| T | Sustainability report scoreIt is calculated only for separate sustainability reports based on the scores given to each specific GRI index (0—not specified, 1—includes a description of the index without setting the GRI standard, and 2—the index is presented and the GRI standard is specified) | [42,43,44] |

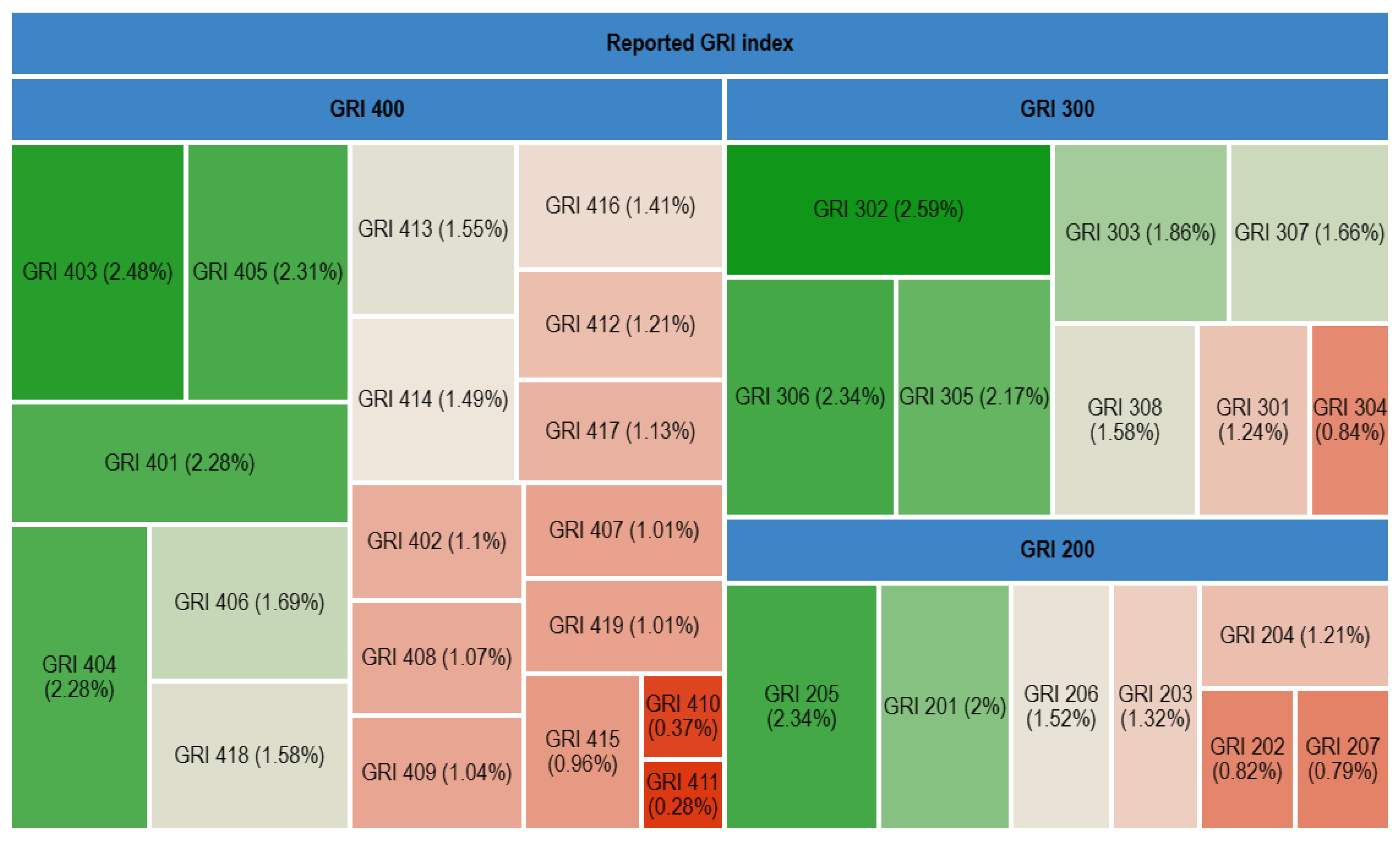

| GRI Standard | Specific Indexes | |

|---|---|---|

| GRI 100P resentation Three indexes | GRI 101 Foundation | GRI 103 Management Approach |

| GRI 102 General Disclosures | ||

| GRI 200 Economic Seven indexes | GRI 201_ Economic Performance | GRI 205_ Anti-Corruption |

| GRI 202_ Market Presence | GRI 206_ Anti-Competitive Behavior | |

| GRI 203_ Indirect Economic Impacts | GRI 207_ Tax | |

| GRI 204_ Procurement Practices | ||

| GRI 300 Environmental Eight indexes | GRI 301_ Materials | GRI 305_ Emissions |

| GRI 302_ Energy | GRI 306_ Effluents and Waste | |

| GRI 303_ Water and Effluents | GRI 307_Environmental Compliance (removed from version 2021) | |

| GRI 304_ Biodiversity | GRI 308_ Supplier Environmental Assessment | |

| GRI 400 Social 19 indexes | GRI 401_ Employment | GRI 411_ Rights of Indigenous Peoples |

| GRI 402_ Labor/Management Relations | GRI 412: HUMAN RIGHTS ASSESSMENT (removed from version 2021) | |

| GRI 403_ Occupational Health and Safety | GRI 413_ Local Communities | |

| GRI 404_ Training and Education | GRI 414_ Supplier Social Assessment | |

| GRI 405_ Diversity and Equal Opportunity | GRI 415_ Public Policy | |

| GRI 406_ Non-Discrimination | GRI 416_ Customer Health and Safety | |

| GRI 407_ Freedom of Association and Collective Bargaining | GRI 417_ Marketing and Labeling | |

| GRI 408_ Child Labor | GRI 418_ Customer Privacy | |

| GRI 409_ Forced or Compulsory Labor | GRI 419_Socioeconomic Compliance (removed from version 2021) | |

| GRI 410_ Security Practices | ||

| Code | Industry Name | Industry’s Environmental Sensitivity |

|---|---|---|

| A | Agriculture, forestry, and fishing | 0-Consumer goods |

| B | Extractive industry | 1-Industry |

| C | Manufacturing industry | 1-Industry |

| D | Production and supply of electricity and thermal energy, gas, hot water, and air conditioning | 1-Industry |

| E | Water distribution; sanitation, waste management, decontamination activities | 1-Industry |

| F | Construction | 1-Industry |

| G | Wholesale and retail trade; motor vehicle and motorcycle repair | 0-Consumer goods |

| H | Transport and storage | 0-Consumer goods |

| I | Hotels and restaurants | 0-Consumer goods |

| J | Information and Communications | 0-Consumer goods |

| K | Financial intermediation and insurance | 2-Financial |

| L | Real estate transactions | 0-Services |

| M | Professional, scientific, and technical activities | 0-Services |

| N | Administrative service activities and support service activities | 0-Services |

| O | Public administration and defense; social insurance from the public system | 0-Services |

| P | Education | 0-Services |

| R | Performing cultural and recreational activities | 0-Services |

| S | Other service activities | 0-Services |

| T | Activities of private households as employers of domestic staff; activities of private homes producing goods and services intended for own consumption | 0-Consumer goods |

| U | Activities of extraterritorial organizations and bodies | 0-Services |

| Industry | Number of Organizations | % from Total Organizations | Organizations that Published Sustainability Reports Using the GRI Standard |

|---|---|---|---|

| A | 3 | 0.60 | 1 |

| B | 6 | 1.20 | 3 |

| C | 189 | 37.80 | 42 |

| D | 17 | 3.40 | 11 |

| E | 29 | 5.8 | 0 |

| F | 18 | 3.60 | 2 |

| G | 62 | 12.40 | 11 |

| H | 40 | 8 | 5 |

| I | 6 | 1.20 | 2 |

| J | 35 | 7 | 6 |

| K | 1 | 0.20 | 1 |

| L | 2 | 0.40 | 0 |

| M | 21 | 2.20 | 6 |

| N | 52 | 10.20 | 4 |

| O | 5 | 1 | 0 |

| Q | 7 | 1.4 | 2 |

| R | 7 | 1.4 | 0 |

| Total | 500 | 100 | 96 |

| No. | Description | Score (0–3) |

|---|---|---|

| 1. | No sustainability report/no information included in the annual non-financial report | 0 |

| 2. | No sustainability report, but there are sustainability data included in the annual non-financial report | 1 |

| 3. | There is a sustainability report, but it does not have the GRI standards structure | 2 |

| 4. | There is a sustainability report according to the GRI standards | 3 |

| No. | Details | Score (0–2) |

|---|---|---|

| 1. | No specific index is mentioned | 0 |

| 2. | A short statement about the specific indexes for the dimension | 1 |

| 3. | Detailed data on the specific indexes and the GRI standard are specified | 2 |

| T | RepPages | |

|---|---|---|

| 96 | 96 | |

| Missing | 0 | 0 |

| Mean | 42.8 | 103 |

| Median | 44 | 87 |

| Standard deviation | 15.6 | 65 |

| Variance | 243 | 4224 |

| Minimum | 6 | 9 |

| Maximum | 74 | 338 |

| Statistic | df | p | Mean Difference | SE Difference | ||

|---|---|---|---|---|---|---|

| T | Student’s t | −0.903 | 94 | 0.369 | −2.94 | 3.25 |

| Welch’s t | −0.886 | 74 | 0.379 | −2.94 | 3.32 | |

| Mann–Whitney U | 959 | 0.283 | −4.00 |

| LOG_PN | LOG_TV | LOG_CH | T | SE | RepPages | ||

|---|---|---|---|---|---|---|---|

| LOG_PN | Pearson’s r | - | |||||

| p-value | - | ||||||

| LOG_TV | Pearson’s r | 0.583 *** | - | ||||

| p-value | <0.001 | - | |||||

| LOG_CH | Pearson’s r | 0.49 *** | 0.983 *** | - | |||

| p-value | <0.001 | <0.001 | - | ||||

| T | Pearson’s r | 0.131 | 0.249 * | 0.254 * | - | ||

| p-value | 0.251 | 0.014 | 0.013 | - | |||

| SE | Pearson’s r | −0.372 *** | −0.198 | −0.157 | 0.093 | - | |

| p-value | <0.001 | 0.053 | 0.126 | 0.369 | - | ||

| RepPages | Pearson’s r | 0.133 | 0.152 | 0.141 | 0.035 | 0.026 | - |

| p-value | 0.244 | 0.139 | 0.171 | 0.735 | 0.799 | - |

| Model | R | R2 | F | df1 | df2 | p |

|---|---|---|---|---|---|---|

| 1 | 0.61 | 0.372 | 4.54 | 9 | 69 | <0.001 |

| Predictor | VIF | Tolerance |

|---|---|---|

| GRI_204 | 1.12 | 0.896 |

| GRI_207 | 1.51 | 0.661 |

| GRI_301 | 1.49 | 0.671 |

| GRI_306 | 1.31 | 0.765 |

| GRI_308 | 2.02 | 0.496 |

| GRI_407 | 2.27 | 0.44 |

| GRI_409 | 2.21 | 0.452 |

| GRI_412 | 1.8 | 0.556 |

| GRI_414 | 2.48 | 0.403 |

| Predictor | Estimate | SE | t | p |

|---|---|---|---|---|

| Intercept | 6.945 | 0.2021 | 34.37 | <0.001 |

| GRI_204 | 0.237 | 0.0764 | 3.1 | 0.003 |

| GRI_207 | −0.27 | 0.0988 | −2.73 | 0.008 |

| GRI_301 | −0.184 | 0.0881 | −2.08 | 0.041 |

| GRI_306 | 0.409 | 0.111 | 3.68 | <0.001 |

| GRI_308 | −0.298 | 0.103 | −2.89 | 0.005 |

| GRI_407 | 0.513 | 0.1134 | 4.52 | <0.001 |

| GRI_409 | −0.278 | 0.1111 | −2.5 | 0.015 |

| GRI_412 | −0.211 | 0.0972 | −2.17 | 0.033 |

| GRI_414 | 0.461 | 0.1135 | 4.07 | <0.001 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mihai, F.; Aleca, O.E. Sustainability Reporting Based on GRI Standards within Organizations in Romania. Electronics 2023, 12, 690. https://doi.org/10.3390/electronics12030690

Mihai F, Aleca OE. Sustainability Reporting Based on GRI Standards within Organizations in Romania. Electronics. 2023; 12(3):690. https://doi.org/10.3390/electronics12030690

Chicago/Turabian StyleMihai, Florin, and Ofelia Ema Aleca. 2023. "Sustainability Reporting Based on GRI Standards within Organizations in Romania" Electronics 12, no. 3: 690. https://doi.org/10.3390/electronics12030690

APA StyleMihai, F., & Aleca, O. E. (2023). Sustainability Reporting Based on GRI Standards within Organizations in Romania. Electronics, 12(3), 690. https://doi.org/10.3390/electronics12030690