A Class of Fractional Stochastic Differential Equations with a Soft Wall

Abstract

:1. Introduction

2. Main Results

- (A)

- Linear growth of f for any and any

- (B)

- Lipschitz continuity of fin space: for any and

- (C)

- Hölder continuity in time: there exists such that for any and any

- (D)

- Function D is strictly monotonic and surjective.

- (E)

- Constant exists, such that

3. Remarks on the Condition (E)

4. Proofs of Theorems

4.1. Proof of Theorems 1 and 2

4.2. Proof of Theorems 4 and 5

5. Example: Fractional Pearson Diffusion Process with Soft Wall

6. Modelling: Fractional Vasicek Process

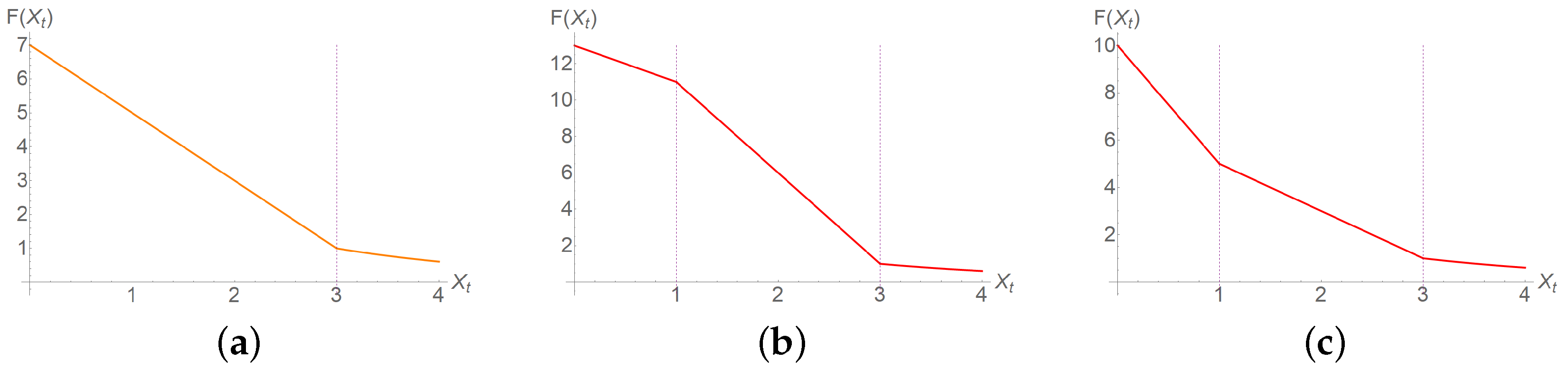

6.1. Profile of Soft-Wall Resistant Force

6.2. Process Trajectories Simulation under Soft-Wall conditions

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Estimation of Hurst Parameter

Appendix B. Supplementary Results

Appendix B.1. Limit Results on fBm

Appendix B.2. Hölder Continuous Paths

Appendix B.3. Pathwise Integration

Appendix B.4. Gronwall’s lemma

References

- Nualart, D.; Ouknine, Y. Regularization of differential equations by fractional noise. Stoch. Process Their Appl. 2002, 102, 103–116. [Google Scholar] [CrossRef] [Green Version]

- Nualart, D.; Rǎşcanu, A. Differential equations driven by fractional Brownian motion. Collect. Math. 2002, 53, 55–81. [Google Scholar]

- Xu, L.; Luo, J. Stochastic differential equations driven by fractional Brownian motion. Stat. Probab. Lett. 2018, 142, 102–108. [Google Scholar] [CrossRef]

- Fuliński, A. Fractional Brownian Motions. Acta Phys. Pol. B 2020, 51, 1097–1129. [Google Scholar] [CrossRef]

- Capasso, V.; Wieczorek, R. A hybrid stochastic model of retinal angiogenesis. Math. Methods Appl. Sci. 2020, 43, 10578–10592. [Google Scholar] [CrossRef]

- Vojta, T.; Halladay, S.; Skinner, S.; Janušonis, S.; Guggenberger, T.; Metzler, R. Reflected fractional Brownian motion in one and higher dimensions. Phys. Rev. E 2020, 102, 032108. [Google Scholar] [CrossRef] [PubMed]

- Duncan, T.; Nualart, D. Existence of strong solutions and uniqueness in law for stochastic differential equations driven by fractional Brownian motion. Stoch. Dyn. 2009, 9, 423–435. [Google Scholar] [CrossRef]

- Guerra, J.; Nualart, D. Stochastic differential equations driven by fractional Brownian motion and standard Brownian motion. Stoch. Anal. Appl. 2008, 26, 1053–1075. [Google Scholar] [CrossRef] [Green Version]

- Kubilius, K. The existence and uniqueness of the solution of an integral equation driven by a p-semimartingale of special type. Stoch. Process. Appl. 2002, 98, 289–315. [Google Scholar] [CrossRef] [Green Version]

- Li, Z.; Zhan, W.; Xu, L. Stochastic differential equations with time-dependent coefficients driven by fractional Brownian motion. Phys. A 2019, 530, 121565. [Google Scholar] [CrossRef]

- Mishura, Y.; Shevchenko, G. Mixed stochastic differential equations with long-range dependence: Existence, uniqueness and convergence of solutions. Comput. Math. Appl. 2012, 64, 3217–3227. [Google Scholar] [CrossRef]

- Pei, B.; Xu, Y. On the non-Lipschitz stochastic differential equations driven by fractional Brownian motion. Adv. Differ. Equ. 2016, 194. [Google Scholar] [CrossRef] [Green Version]

- Da Silva, J.L.; Erraoui, M.; Essaky, E.H. Mixed Stochastic Differential Equations: Existence and Uniqueness Result. J. Theor. Probab. 2018, 31, 1119–1141. [Google Scholar] [CrossRef] [Green Version]

- Vojta, T.; Wada, A.H.O. Fractional Brownian motion with a reflecting wall. Phys. Rev. E 2018, 97, 020102. [Google Scholar]

- Leonenko, G.M.; Phillips, T.N. High-order approximation of Pearson diffusion processes. J. Comput. Appl. Math. 2012, 236, 2853–2868. [Google Scholar] [CrossRef] [Green Version]

- Chen, Y.; Ying, L.; Pei, X. Parameter estimation for Vasicek model driven by a general Gaussian noise. Commun. Stat.-Theory Methods 2021, 1–17. [Google Scholar] [CrossRef]

- Kubilius, K.; Mishura, Y.; Ralchenko, K. Parameter Estimation in Fractional Diffusion Models; Bocconi & Springer Series; Springer: Berlin/Heidelberg, Germany, 2017. [Google Scholar]

- Holte, J.M. Discrete Gronwall lemma and applications. In Proceedings of the MAA North Central Section Meeting at UND, Grand Forks, ND, USA, 24 October 2009. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kubilius, K.; Medžiūnas, A. A Class of Fractional Stochastic Differential Equations with a Soft Wall. Fractal Fract. 2023, 7, 110. https://doi.org/10.3390/fractalfract7020110

Kubilius K, Medžiūnas A. A Class of Fractional Stochastic Differential Equations with a Soft Wall. Fractal and Fractional. 2023; 7(2):110. https://doi.org/10.3390/fractalfract7020110

Chicago/Turabian StyleKubilius, Kęstutis, and Aidas Medžiūnas. 2023. "A Class of Fractional Stochastic Differential Equations with a Soft Wall" Fractal and Fractional 7, no. 2: 110. https://doi.org/10.3390/fractalfract7020110

APA StyleKubilius, K., & Medžiūnas, A. (2023). A Class of Fractional Stochastic Differential Equations with a Soft Wall. Fractal and Fractional, 7(2), 110. https://doi.org/10.3390/fractalfract7020110