Abstract

This paper introduces the fractional Heston-type (fHt) model as a stochastic system comprising the stock price process modeled by a geometric Brownian motion. In this model, the infinitesimal return volatility is characterized by the square of a singular stochastic equation driven by a fractional Brownian motion with a Hurst parameter . We establish the Malliavin differentiability of the fHt model and derive an expression for the expected payoff function, revealing potential discontinuities. Simulation experiments are conducted to illustrate the dynamics of the stock price process and option prices.

1. Introduction

Allowing volatility to be stochastic in a financial market model was one of the great achievements in the history of quantitative finance. This innovation led to stochastic volatility modeling, as previously discussed by Heston [1] and several other researchers, addressing shortcomings in the standard Black–Scholes model (see, for example, Alos et al. [2] for a summary). In the context of Heston [1], the stock price process is described by a geometric Brownian motion of the form:

where and represent a constant drift and the stochastic variance of the instantaneous rate of return , respectively. The stochastic process takes the form of the standard Cox–Ingersoll–Ross process, satisfying the following stochastic differential equation:

The parameter represents the speed of reversion of the stochastic process towards its long-run mean , and the parameter represents the volatility of the stochastic variance . The Brownian motions and are assumed to be correlated. This model is well known in the literature as the Heston model.

It has recently been demonstrated that volatility and the volatility of volatility exhibit rough behaviors. This implies that the paths tend to be rougher, showing short-range dependency and can be effectively modelled using fractional Brownian motion with a Hurst parameter . For further insights, refer to studies such as Alos et al. [3], Fukasawa [4], Gatheral et al. [5], Livieri et al. [6], Takaishi [7], Fukasawa [8], Brandi and Di Matteo [9], and related findings.

On the other hand, volatility persistence is also associated with long-memory properties, indicated by the slow decay of the autocorrelation function. In this regard, Comte and Renault [10] demonstrated that long-memory stochastic volatility models are better suited to reproduce the gradual flattening of implied volatility skews and smiles observed in financial market data. This finding has been corroborated and tested by several other researchers, including Chronopoulou and Viens [11], Chronopoulou and Viens [12], Tripathy [13], and subsequent studies. In contrast to rough volatility, this modeling approach involves using fractional Brownian motion with a Hurst parameter .

From the above, we may notice a contradiction regarding whether volatility is rough or exhibits long-range dependency, a subject of debate in the literature. However, Alos and Lorite [14] observed that both properties are not mutually exclusive. A process can exhibit both long and short dependency properties, with each dominating at different scales, and consequently, at different maturities in the implied volatility surface. This idea is supported by Funahashi and Kijima [15], who demonstrated that if the volatility where and are the fractional Ornstein–Uhlenbeck process driven by fractional Brownian motions with Hurst parameters and , respectively, then does not have an impact on the ATM short-time limit skew.

To incorporate both roughness and long-range dependency properties into the Heston model, the standard Brownian motion is replaced by a fractional Brownian motion with a Hurst parameter or , resulting in the fractional Heston model. For further details, refer to studies such as Alos and Yang [16], Mishura and Yurchenko-Tytarenko [17], Mehrdoust and Fallah [18], Tong and Liu [19], Richard et al. [20], along with the references therein. In this context, the volatility process can be represented by:

The stochastic process is well-known as the fractional Cox–Ingersoll–Ross (fCIR) process. The Equation (1) is well defined only when as shown by Mishura et al. [21]. This limitation was overcome by defining fCIR process as a square of a stochastic process with additive fBm. In other words, the stochastic process can be written as the square of a stochastic process that verifies

The stochastic volatility process described above gives rise to complex models in option pricing or risk analysis, which are not easily manageable, particulary when the volatility drift is not constant. In this paper, we propose a general form of the fractional Heston-type model in a simple and natural manner. As before, we assume that the stock price process is driven by a geometric Brownian motion , satisfying the following stochastic differential equation:

where represents the volatility of the infinitesimal log-return with a fractional Cox–Ingersoll–Ross (fCIR) process that captures both long and short-range dependency. We adopt the definition provided by Mishura and Yurchenko-Tytarenko [22] or Mpanda et al. [23] and describe the stochastic process as

where the stochastic process is referred to as a general form of the fCIR process that satisfies the following differential equation:

and is the first time the process hits zero, defined by

It was shown in Mpanda et al. [23] that the stochastic process satisfies . This implies that the function can be defined as the drift of the volatility process . Additionally, the stochastic process is well-known as fractional Brownian motion (fBm) with Hurst parameter H, defined as a centered Gaussian process with a covariance function:

There exist several representations of fBm. Nourdin [24] summarized them. In financial volatility modelling, the Volterra representation is widely used, particulary due to its simplicity. In this representation, the fBm is written in terms of a standard Brownian motion in the time interval as follows:

where is a standard Brownian motion and where is a square integrable kernel that may take different forms. One effective expression is through the Euler hypergeometric integral with given by

with and being the gamma and Gaussian hypergeometric functions, respectively. A truncated expression of the kernel (9) was suggested by Decreusefond and Üstünel [25] where . This representation is referred to as a Type II fBm or Riemann–Liouville fBm. Here, is defined by

This representation was used by Gatheral et al. [5] to model rough volatility. The standard Brownian motions and are assumed to be correlated, meaning there exists such that This implies that there exists a Brownian motion independent to , that is , such that

A new and natural way of defining a fractional Heston-type (fHt) model as singular stochastic differential equation driven by a fractional Brownian motion is through the following stochastic system:

The existence of the stochastic process in (5) was previously discussed by Nualart and Ouknine [26]. They proposed that for , the drift function must satisfy the linear growth condition, and for , must verify the Hölder continuity condition. Additionally, particular cases of fHt model (12) has been previously investigate by Alos and Yang [16], Mishura and Yurchenko-Tytarenko [17], Bezborodov et al. [27] for . One can use the same idea of Bezborodov et al. [27] (Theorem 3.6) to show that the fHt model is free of arbitrage. The above stochastic model is also a generalisation of the rough volatility model previously discussed by Gatheral et al. [5] with , and the Type II fBm of the form (10) with small Hurst parameters.

The remainder of this paper is structured as follows: Section 2 constructs approximating sequences of stock prices and fCIR processes. Malliavin differentiability within the fHt model is discussed in Section 3. Finally, Section 4 derives the expected payoff function and performs simulations of option prices.

2. Approximating Sequences in fHt Model

The main purpose of introducing approximating sequences of both fractional volatility and stock price processes relies on their positiveness. The following theorems discuss the positiveness of and before this, we consider the following assumption below.

Assumption 1.

- (i)

- The function defined by is continuous and admits a continuous partial derivative with respect to x on .

- (ii)

- for any , there exists such that

Under this assumption, the following theorems follow.

Theorem 1.

Let be a stochastic process that verifies (5) with and is a continuous function that satisfies Assumption 1. Then,

where

Proof.

Here, we highlight the proof of this theorem by contradiction, and we refer the reader to Mpanda et al. [23] for a complete and comprehensive proof. Let be the first time that the process hits zero and be the last time hits before reaching zero. In addition, define

where and is any point chosen between zero and the initial value of , that is, and . Then, from (5), we have:

and by Hölder continuity of fBm, we have

which yields the following inequality

for some constant . Define

then we have

On the other hand, the critical point of the function is given by

and

where

and

One may notice that there exists such that for all . This goes in contradiction with (13). □

Theorem 2.

Consider for each , the stochastic process defined by

where Then, for any and ,

Proof.

The proof can be carried out as previously shown by defining and where For more details, refer to Mpanda et al. [23]. □

2.1. Approximating Sequences of

Inspired by Alos and Ewald [28], we construct an approximating sequence of the fCIR process that satisfies the following differential equation:

where the function in (14) is defined by

It is easy to verify that for all . As a straight consequence, the drift of is also positive. In addition, , , and

The next step is to show that for every , the sequence converges to in as .

Proposition 3.

The sequence of estimated random variables converges to in for all .

Proof.

- Case 1. . This case was discussed previously by Alos and Ewald [28] (Proposition 2.1) and can be easily extended to the case where is defined by (15).

- Case 2. For , the dominated convergence theorem shall be applied. Firstly, we need to show the pointwise convergence of the approximated stochastic process towards , that is . For this, let be the first time the process hits . Since the sample paths of the stochastic process are positive everywhere almost surely as in Theorem 1, then and consequently, almost surely.Next, denote the stochastic process up to stopping time . Then, for all and using the definition of given by (16), almost surely when since the drift function is monotonic.Again, the positiveness of means that We may conclude that almost surely and for all .On the other hand, the result from Hu et al. [29] (Theorem 3.1) shows that for a fixed and for all ,where is a non-random constant taking the formwhere , , and are nonrandom constants depending on parameters , andThis result also implies thatIt follows that which yields the desired convergence.

- Case 3. For , we consider a sequence of an increasing drift function and define the stochastic process as follows:where is defined by (15) and is the first time that the stochastic process hits zero. If we now define be the first time the process hits , then from Theorem 2, for any fixed , as . This implies that a.s. This is because the process remains positive up to time which is not necessary equal to infinity unlike the previous case.After using similar arguments for Case 2, one may conclude that for all . Next, we need to show that . To achieve this, we borrow some ideas from Mishura and Yurchenko-Tytarenko [30].Firstly, let be a small positive value less than the initial value such that and let be the last time the stochastic process hits (or before hits) , that is,Technically, there exists a constant such that . Now we can consider two cases: and .Case 3.1: . By triangle inequality, we haveBy applying the Callebaut’s inequality theorem, it will be easy to show that for all ,Since the drift function satisfies the linear growth condition, this means there exists a positive constant k such that . It follows thatOn the other hand, recall that (See e.g., Nourdin [24]) and sincethen it follows thatFrom the Grönwall–Bellman inequality theorem, we obtainwhich can be shortly written as where is a non-random constant in parameters , and H taking the following formwhere and are non-random constants defined byandCase 3.2: with DefineThen we have:As previously stated, the integral in the last inequality of (24) can be expressed as followsOn the other hand, we may observe thatIt follows that,

This concludes the proof of the proposition. □

Assumption 2.

The volatility function is strictly positive and Lipschitz continuous.

Corollary 4.

Under Assumption 2, and for any ,

Proof.

This follows immediately from the previous proposition. □

Remark 1.

One may use similar arguments to Mishura and Yurchenko-Tytarenko [30] to show that the stochastic process is strictly positive almost surely for all . Consequently, it is also well suitable for rough volatility processes, that is, a fractional volatility process with .

2.2. Approximating Sequences of Stock Price Process

With , let us construct the approximating sequence of the stock price process defined by the following geometric Brownian motion:

where

with the approximating sequence that satisfies (14). The next step is to show that converges to in .

Proposition 5.

Set and . Then, the sequence converges to in for all .

Proof.

Firstly, we have from Itô formula that

where . Then, for some non-random constant , one may have:

Set

and

Then it follows firstly that from Corollary 4. To analyse convergence of , the Burkholder-Davis-Gundy inequality can be used and one may deduce that

which also converges to zero from Corollary 4. It follows that

that implies the desired convergence of to and to . □

Remark 2.

- 1.

- The stochastic process is a unique solution of a geometric Brownion motion of the formthat can be found using the standard Itô formula, yielding:

- 2.

- The approximated stochastic volatility and stock price processes will be compulsory for and optional for . However, for the sake of consistency, we shall use the approximated sequences (14) with for and with for .

3. Malliavin Differentiability

Nowadays, the application of Malliavin calculus in stochastic volatility modelling has increased, particularly due to the introduction of fBm, which exacerbates the complexity of derivative pricing models. In this section, we discuss the Malliavin differentiability of both the stock price process and its stochastic volatility as given in the stochastic system (12). This analysis will pave the way for the first application, which involves deriving the expected payoff function.

3.1. Preliminaries on Malliavin Calculus for fBm

Malliavin calculus, initially introduced by Paul Malliavin in the 1970s, is a powerful mathematical tool used to analyze stochastic processes and their associated functionals. It provides a systematic framework for differentiating stochastic processes with respect to underlying Brownian motions, enabling the analysis of complex stochastic systems. Malliavin calculus finds wide application in quantitative finance for pricing and hedging financial derivatives, risk management, and portfolio optimization. In this section, we provide some preliminaries on Malliavin calculus for fBm. for a complete background in Malliavin calculus, we refer the reader to Nualart [31] and Da Prato [32]. For applications in quantitative finance, we refer to Nunno et al. [33] and Alos and Lorite [14].

On the time interval , consider the Hilbert space constructed with the closure of the set of real-valued step functions on denoted by with respect to the scalar product . If the fBm takes the Volterra representation (8), then its covariance function is given by

where is a Kernel taking the form (9) or (10). The covariance function (30) can be further developed to reach the following expression:

where . For any step function , one may generalise the above as

The mapping can be extended to an isometry between the Hilbert space and the Gaussian space denoted by spanned by . Now, consider the operator that provides the previous isometry between and defined by

then, for any ,

Denote , where is the operator defined by:

The space represents the fractional version of the Cameron–Martin space. Additionally, let be the operator defined as:

Moreover, it is important to note that is Holder continuous of order H. This leads to the definition of the Malliavin derivative as presented by Nualart [31].

Definition 1.

Consider a space of smooth random variables of the form

where . Then, the Malliavin derivative of F denoted by is a random variable given by

The domain of (denoted by ) is a Sobolev space defined as the closure of the space of smooth random variables , with respect to the norm:

The directional Malliavin derivative is defined as the scalar product

In other words, the directional Malliavin derivative is the derivative at of the smooth random variable F composed with the shifted process .

The Malliavin derivatives have several important properties. Bouleau and Hirsch [34] showed that if and a.s., then the law of F has a density with respect to the Lebesgues measure on . In addition, the following properties were also proved in Nualart [31]:

- (1)

- Integration by parts, in the sense that for all ,

- (2)

- Chain rule, that is, for , then the smooth functionand

- (3)

- The future Malliavin derivative of an adapted process is zero, that is, for all ,

As an example, the computation of Malliavin derivative of fBm (represented by (8)) with respect to Brownian motion is given by , and for (that is, the future derivative), . We may write this shortly as . Similarly, under the stochastic system (12), , , , and

When the kernel is defined as in (10), the computation of the Malliavin derivative is straightforward and is given by:

Since fBm can be represented in terms of standard Brownian motion, it is worth mentioning how the Malliavin derivative of stochastic differential equations is computed. There are several approaches in the literature; one of them was previously presented by Detemple et al. [35] based on a transformation to a volterra integral equation, and was proven to be more efficient in the numerical estimation of Malliavin derivatives. In this approach, consider a stochastic differential equation of the form:

Define such that

and set

Then,

For more details see Detemple et al. [35], Mishura and Yurchenko-Tytarenko [17] and Alos and Lorite [14]. The computation of the Malliavin derivative of the standard Heston model was presented by Alos and Ewald [28], where this approach was utilised. With the above background, we can now discuss the Malliavin derivatives of both stochastic processes and of the stochastic system (12).

3.2. Differentiability of Stochastic Processes and

Proposition 6.

Proof.

First, let us show the expression (45). We have

As in Detemple et al. [35], we set , then we retrieve the following Volterra integral equation of the second kind with the kernel function and unknown function . For any , this equation takes the form:

to which the solution is given by

which yields (45). Similarly, to find the expression (47), we may compute through the Volterra integral equation of the form:

The derivation of (47) is straightforward; we just have to apply the integration by parts formula and chain rules to , which takes the following form:

We obtain

which yields

To demonstrate the absolute continuity of with respect to the Lebesgue measure over any finite interval , we first note that the solution to the stochastic differential Equation (14) takes the following form:

where the function (with ) belongs to the class . This expression arises from the intricate nature of the set , which is associated with the level sets of fBm particularly for small Hurst parameters. For further insights, refer to Mukeru [36] and Mishura and Yurchenko-Tytarenko [30]. We have:

The Taylor expansion of (51) yields:

where

for some . The solution to Equation (52) is obtained using Expression (31). We have:

which yields the following:

and therefore,

This holds almost surely in , and consequently:

as previously, and

It follows that , and consequently, according to Bouleau and Hirsch [34], the law of stochastic process is absolutely continuous with respect to the Lebesgue measure over any finite interval . Similar reasoning can also be applied to the stock price process . □

4. Expected Payoff Function

The aim of this section is to derive the expected payoff function by using some results from Malliavin calculus. We follow Altmayer and Neuenkirch [37] closely.

4.1. Differentiability of Expected Payoff Function

Let be the payoff function that satisfies the following assumption.

Assumption 3.

The payoff function and its antiderivative denoted by (such that ) are bounded and verify the Lipschitz condition.

Proposition 7.

.

Proof.

Firstly, it is straightforward to check that since also verifies the linear growth condition and the law of stock price process are bounded almost surely. On the other hand, since L verifies Assumption 3 and the sample paths of the stock price process is absolutely continuous with respect to the Lebesgue measure on (See Proposition 6), then from the chain rule formula for Malliavin derivatives, we may deduce

It follows that

The first inequality is due to Holder inequality and the finiteness of the last expression makes sense since as discussed previously. It follows that , which concludes the proof. □

Lemma 8.

Let be a payoff function that satisfies Assumption 3 and denote with its antiderivative that also satisfies the Lipschitz condition. Set

Then,

and

where and

Proof.

We follow the idea of Altmayer and Neuenkirch [37]. To establish the equality (54), we rewrite as

From Proposition 7, we may deduce that and

We now obtain

In addition, from Proposition 6,

and since the integral is well defined from Assumption 2, then we have:

and defining by (53), we obtain (54). To establish (55), we rewrite the function (which is the antiderivative of ) as follows

where C is a constant taking the form and by using the standard integration by part formula, one may obtain

With this setting, we have

□

4.2. Some Simulations

4.2.1. Simulations of Stock Price Process

For simulating the stock price process, one can use the Euler–Maruyama approximation scheme. This involves dividing the time interval into N sub-intervals of equal length, where with and the lag . The estimated stock price at time denoted by and the estimated volatility are, respectively, given by:

where and are, respectively, the increment of Brownian motions , , and fBm. In addition, fBm is represented by the Volterra stochastic integral (7), which can be discretized as follows:

for all and where is the increment of standard Brownian motion with . Here, is a discretised square integrable kernel (9) given by

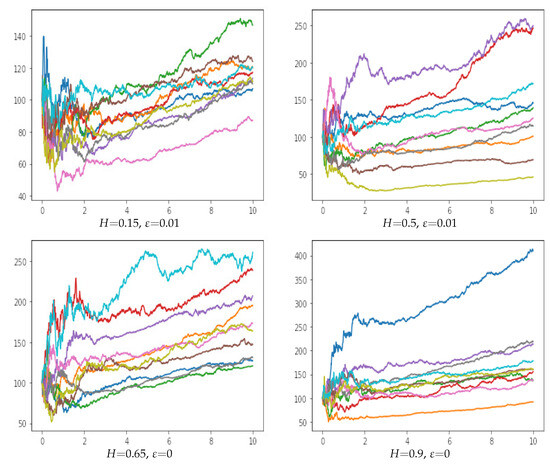

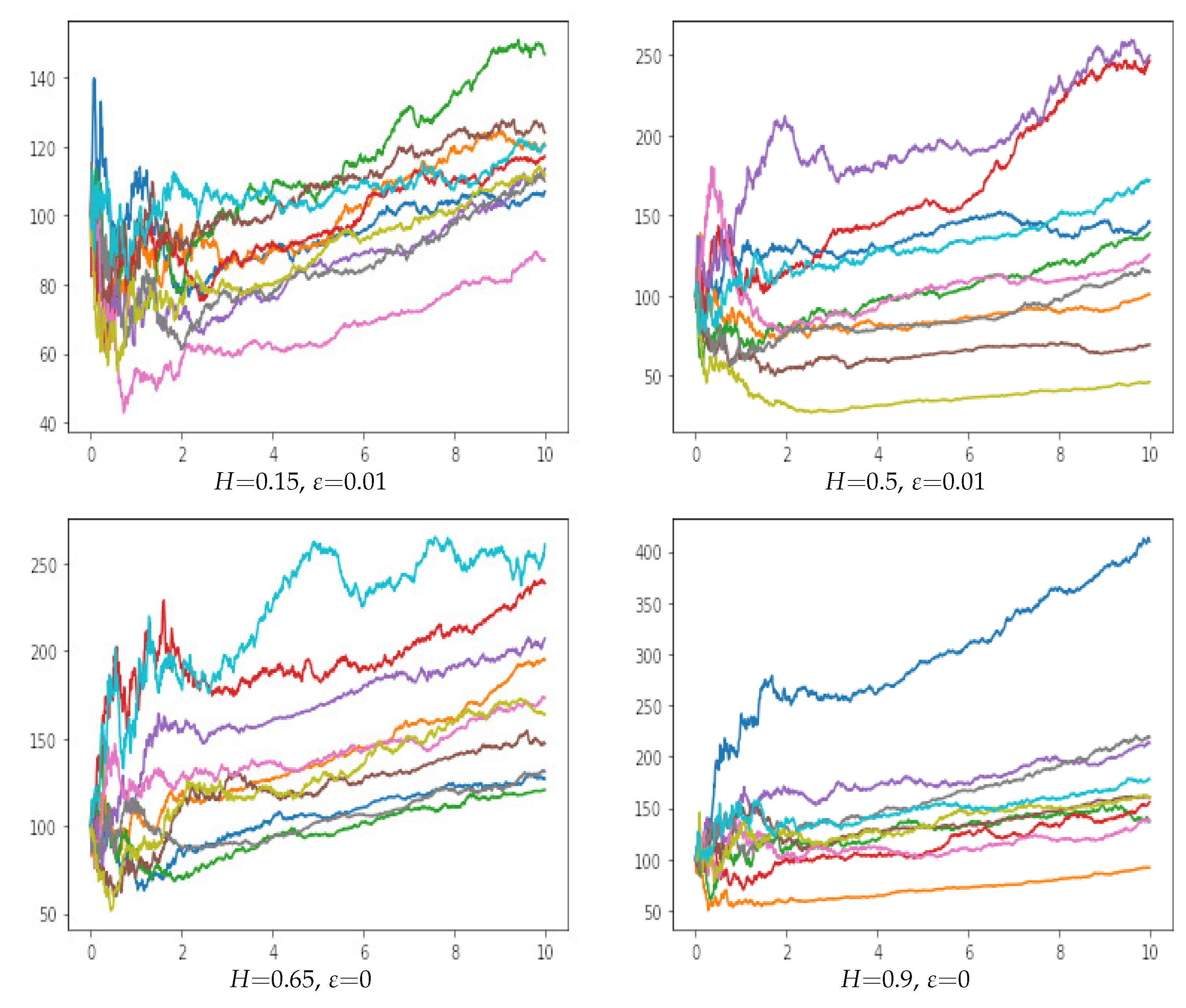

As an illustrative example, the following figures represent 10 sample paths of the stock price process on the interval with . The drift of the fractional volatility process is defined by

with . Referring to remark (2), we will choose when , and for , we set as shown in Figure 1 below.

4.2.2. Payoff Function with Volatility Taking the Form of Ornstein–Uhlenbeck and Standard fCIR Processes

To the scheme (57), we associate the discrete approximation of the integral provided below, which will be used in the computation of the expression (55).

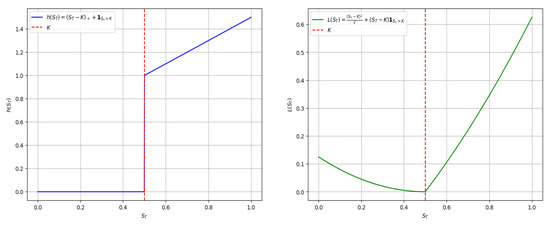

Firstly, we consider the stochastic process defined as a fractional Ornstein–Uhlenbeck process, specifically with where is a positive parameter, and . Under these settings, one may recover the model discussed by Bezborodov et al. [27] with instead. In this case, the volatility process may not necessarily be positive almost surely, as it violates the Assumption 1, rendering Theorems 1 and 2 inapplicable. To address this, the volatility function is chosen to be strictly positive. In addition, we define the payoff function as a combination of European and binary options with the same strike price K and time to maturity T, that is,

The expression for can be readily deduced from (56) as follows:

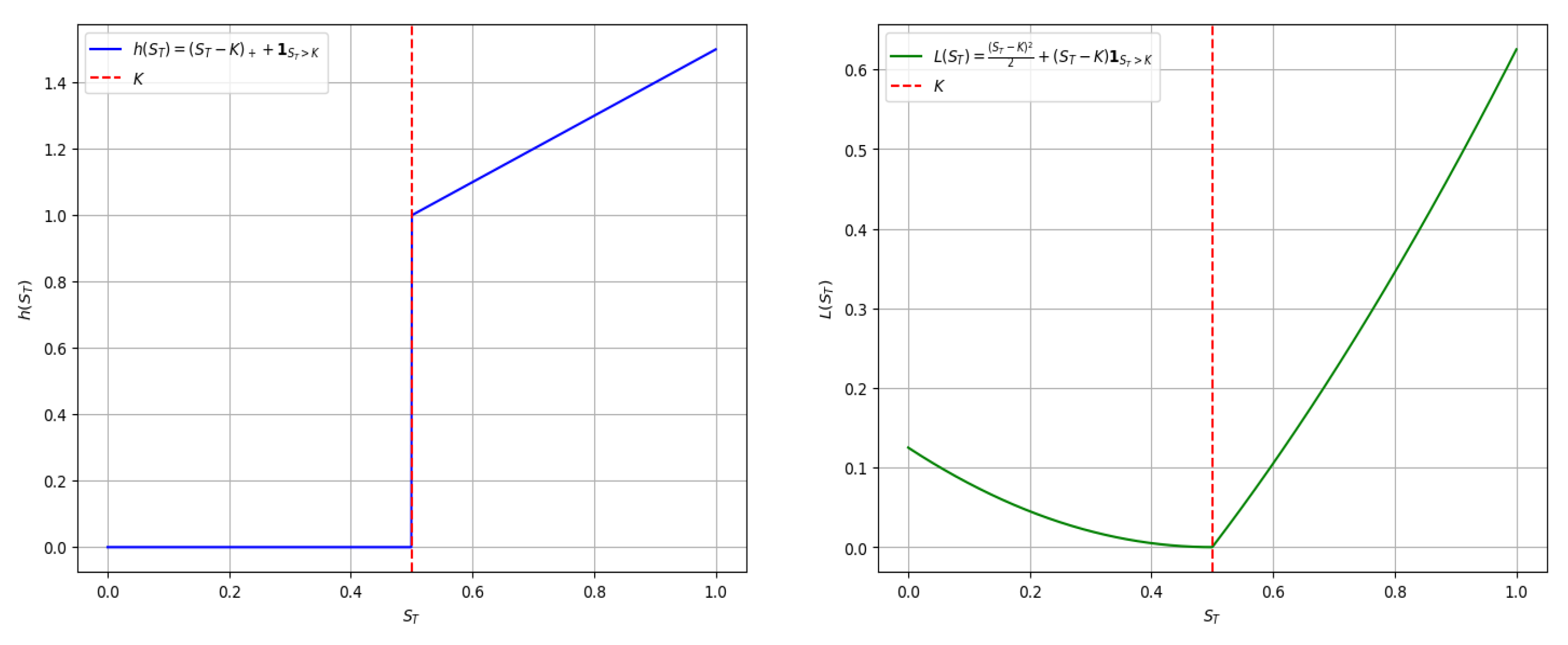

The payoff function and can be visualised in the Figure 2 below with strike price .

Figure 2.

The payoff function and with K = 0.5.

Now, to find expected values of the payoff function, we use the same parameters () with different forms of volatility process of the infinitesimal log-return process as in Bezborodov et al. [27]. Since the fCIR process of the form (4) and (5) cannot be used as the drift function for all , we consider the direct form of the stochastic volatility that takes the form of the Ornstein–Uhlenbeck process satisfying the following differential equation:

In this case, we observe that the values of option prices are not significantly different for and from Bezborodov et al. [27]. The option prices increase or decrease when is positive or negative, respectively.

Next, consider the fractional volatility process described by a standard fCIR process, that is, with and correlation between infinitesimal returns and volatility, the option prices are simulated with and .

The following tables present the mean prices and their corresponding coefficients of variation for a European–Binary option with the payoff function defined by Equation (62) under different Hurst parameters. The mean values are obtained from an average of trials, along with their respective coefficients of variation and option prices are calculated using the expected payoff function discounted by the net present value. We employ two approaches to compute the expectation of the payoff function:

- 1.

- The direct expectation , for a fixed strike price .

- 2.

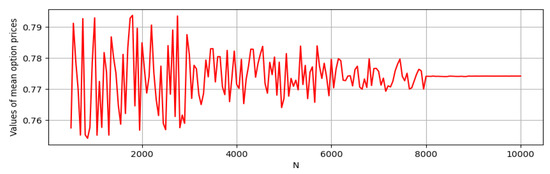

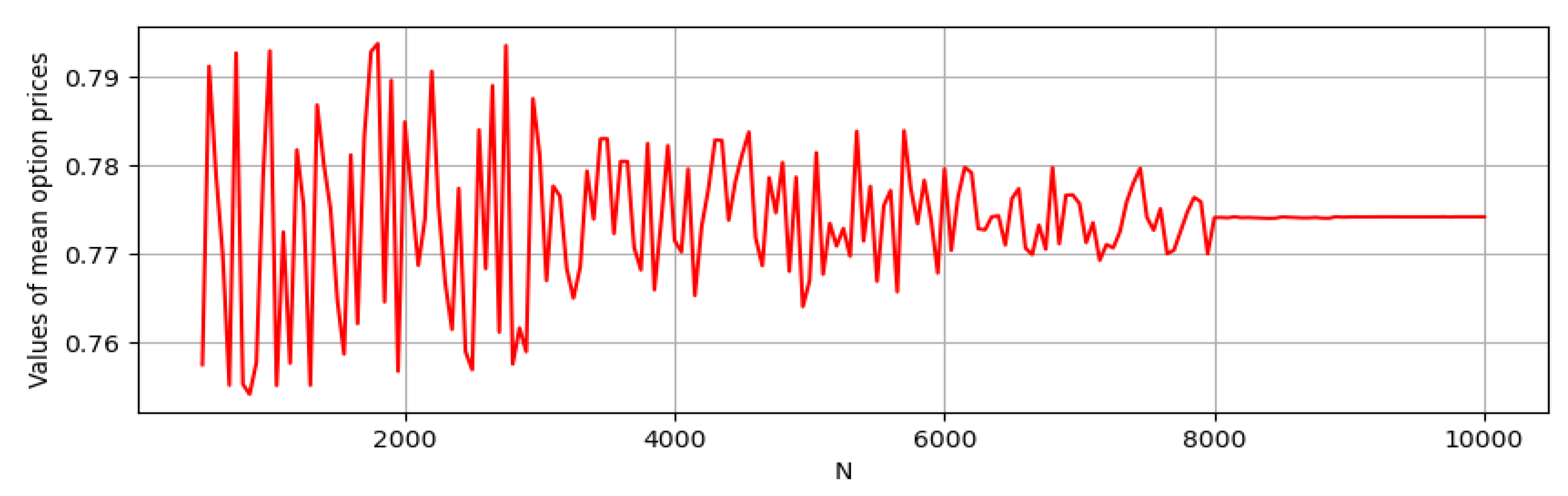

In Table 1, the payoff values at the maturity date T are obtained by performing simulations. We observe that the direct estimation of expected values tends to stabilize starting from (where N represents the number of steps between 0 and T). For example, with and , the expected values for different values of N are represented in Figure 3.

Table 1.

Option prices under direct estimations.

Figure 3.

Values of mean option prices for different N under direct estimations.

In Table 2 below, we perform simulations again, this time using the expressions (55), (62), and (63).

Table 2.

Option prices using Formula (55).

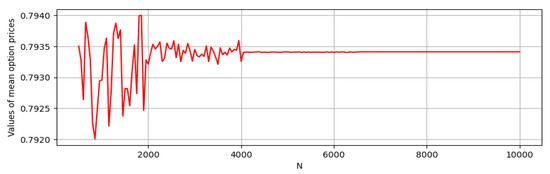

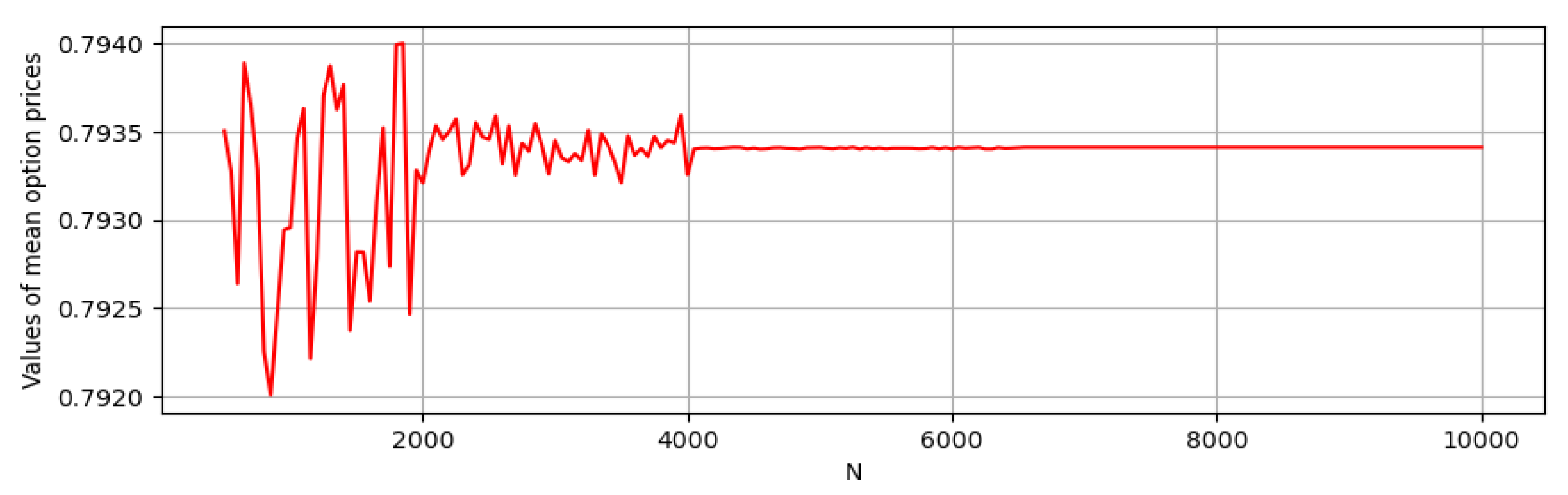

We may observe that the expected option values are slightly different from those in the previous table. However, the following table demonstrates that the values of the expected payoff function stabilize starting from . One of the main reasons attributed to these satisfactory observations is that the expression of the expectation (55) includes a continuous functional of the stock price process along with a weight term that is independent of the functional. This property is even more efficient for discontinuous payoff functions . As in the previous example, choose the Hurst and the volatility function , the expected values for different values of N under the formula (55) are represented in Figure 4.

Figure 4.

Values of mean option prices for different N through Formula (55).

4.2.3. Expected Payoff Function with Volatility Taking the Form of fCIR Process with Time-Varying Parameters

In this section, we perform some simulations of option prices under the fractional Heston model with time-varying parameters. For this, the drift function is given by , where and . It follows that

We shall use . To keep positiveness of the stochastic process for all , we shall rather use its approximated stochastic process defined by (14), that is

where the function is defined by

with for and for . As previously stated, the fBm is simulated by using the formula (58) and (59). We perform again trials for simulations and various time-steps on the time interval . We get the mean of option prices with their corresponding coefficient of variations for different volatility functions under the European–Binary option as given in Table 3 for direct estimations and in Table 4 by using (55).

Table 3.

Option prices using direct estimations.

Table 4.

Option prices using (55).

Note that observations from the previous sections also apply to this one.

5. Conclusions

In this paper, we have constructed the fractional Heston-type model as a stochastic system comprising the stock price process modeled by a geometric Brownian motion. The volatility of this process is represented as a strictly positive and Lipschitz continuous function of fractional Cox–Ingersoll–Ross process , which is characterized by the square of a stochastic process that satisfies a stochastic differential equation with additive fractional Brownian motion.

To ensure the positivity of the stochastic process for all Hurst parameters , we have considered an approximating sequence converging to in for all . This construction also enables us to demonstrate that , , and the payoff function are Malliavin differentiable. Furthermore, we establish that the law of the stochastic processes and is absolutely continuous with respect to the Lebesgue measure over any finite interval .

To support our findings, we conducted simulations. Firstly, we modeled volatility using the Ornstein–Uhlenbeck process, corroborating the results found in Bezborodov et al. [27]. Secondly, we explored the fractional Cox–Ingersoll–Ross process with time-varying parameters. Our observations indicate that option prices exhibit greater stability under the expected value of option prices obtained through Malliavin calculus.

Funding

The APC was funded by the University of South Africa.

Data Availability Statement

No new data were created or analyzed in this study. Data sharing is not applicable to this article.

Acknowledgments

I sincerely thank my supervisors, Safari Mukeru and Mmboniseni Mulaudzi, for their invaluable guidance and support. I also appreciate the anonymous reviewers for their valuable suggestions.

Conflicts of Interest

The author declares no conflits of interest.

References

- Heston, S.L. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 1993, 6, 327–343. [Google Scholar] [CrossRef]

- Alòs, E.; Mancino, M.E.; Wang, T.H. Volatility and volatility-linked derivatives: Estimation, modeling, and pricing. Decis. Econ. Financ. 2019, 42, 321–349. [Google Scholar] [CrossRef]

- Alos, E.; León, J.A.; Vives, J. On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Financ. Stochastics 2007, 11, 571–589. [Google Scholar] [CrossRef]

- Fukasawa, M. Asymptotic analysis for stochastic volatility: Martingale expansion. Financ. Stochastics 2011, 15, 635–654. [Google Scholar] [CrossRef]

- Gatheral, J.; Jaisson, T.; Rosenbaum, M. Volatility is rough. Quant. Financ. 2018, 18, 933–949. [Google Scholar] [CrossRef]

- Livieri, G.; Mouti, S.; Pallavicini, A.; Rosenbaum, M. Rough volatility: Evidence from option prices. Iise Trans. 2018, 50, 767–776. [Google Scholar] [CrossRef]

- Takaishi, T. Rough volatility of Bitcoin. Financ. Res. Lett. 2020, 32, 101379. [Google Scholar] [CrossRef]

- Fukasawa, M. Volatility has to be rough. Quant. Financ. 2021, 21, 1–8. [Google Scholar] [CrossRef]

- Brandi, G.; Di Matteo, T. Multiscaling and rough volatility: An empirical investigation. Int. Rev. Financ. Anal. 2022, 84, 102324. [Google Scholar] [CrossRef]

- Comte, F.; Renault, E. Long memory in continuous-time stochastic volatility models. Math. Financ. 1998, 8, 291–323. [Google Scholar] [CrossRef]

- Chronopoulou, A.; Viens, F.G. Hurst index estimation for self-similar processes with long-memory. In Recent Development in Stochastic Dynamics and Stochastic Analysis; World Scientific: Singapore, 2010; pp. 91–117. [Google Scholar]

- Chronopoulou, A.; Viens, F.G. Estimation and pricing under long-memory stochastic volatility. Ann. Financ. 2012, 8, 379–403. [Google Scholar] [CrossRef]

- Tripathy, N. Long memory and volatility persistence across BRICS stock markets. Res. Int. Bus. Financ. 2022, 63, 101782. [Google Scholar] [CrossRef]

- Alòs, E.; Lorite, D.G. Malliavin Calculus in Finance: Theory and Practice; Chapman and Hall/CRC: Boca Raton, FL, USA, 2021. [Google Scholar]

- Funahashi, H.; Kijima, M. A solution to the time-scale fractional puzzle in the implied volatility. Fractal Fract. 2017, 1, 14. [Google Scholar] [CrossRef]

- Alòs, E.; Yang, Y. A fractional Heston model with H>1/2. Stochastics 2017, 89, 384–399. [Google Scholar] [CrossRef]

- Mishura, Y.; Yurchenko-Tytarenko, A. Approximating Expected Value of an Option with Non-Lipschitz Payoff in Fractional Heston-Type Model. Int. J. Theor. Appl. Financ. 2020, 23, 2050031. [Google Scholar] [CrossRef]

- Mehrdoust, F.; Fallah, S. On the calibration of fractional two-factor stochastic volatility model with non-Lipschitz diffusions. Commun. -Stat.-Simul. Comput. 2022, 51, 6332–6351. [Google Scholar] [CrossRef]

- Tong, K.Z.; Liu, A. The valuation of barrier options under a threshold rough Heston model. J. Manag. Sci. Eng. 2023, 8, 15–31. [Google Scholar] [CrossRef]

- Richard, A.; Tan, X.; Yang, F. On the discrete-time simulation of the rough Heston model. Siam J. Financ. Math. 2023, 14, 223–249. [Google Scholar] [CrossRef]

- Mishura, Y.; Piterbarg, V.; Ralchenko, K.; Yurchenko-Tytarenko, A. Stochastic representation and path properties of a fractional Cox–Ingersoll–Ross process. Theory Probab. Math. Stat. 2018, 97, 167–182. [Google Scholar] [CrossRef]

- Mishura, Y.; Yurchenko-Tytarenko, A. Fractional Cox–Ingersoll–Ross process with non-zero “mean”. Mod. Stochastics Theory Appl. 2018, 5, 99–111. [Google Scholar] [CrossRef]

- Mpanda, M.M.; Mukeru, S.; Mulaudzi, M. Generalisation of fractional Cox–Ingersoll–Ross process. Results Appl. Math. 2022, 15, 100322. [Google Scholar] [CrossRef]

- Nourdin, I. Selected Aspects of Fractional Brownian Motion; Springer: Berlin/Heidelberg, Germany, 2012; Volume 4. [Google Scholar]

- Decreusefond, L.; Üstünel, A.S. Stochastic analysis of the fractional Brownian motion. Potential Anal. 1999, 10, 177–214. [Google Scholar] [CrossRef]

- Nualart, D.; Ouknine, Y. Regularization of differential equations by fractional noise. Stoch. Processes Their Appl. 2002, 102, 103–116. [Google Scholar] [CrossRef]

- Bezborodov, V.; Di Persio, L.; Mishura, Y. Option pricing with fractional stochastic volatility and discontinuous payoff function of polynomial growth. Methodol. Comput. Appl. Probab. 2019, 21, 331–366. [Google Scholar] [CrossRef]

- Alos, E.; Ewald, C.O. Malliavin differentiability of the Heston volatility and applications to option pricing. Adv. Appl. Probab. 2008, 40, 144–162. [Google Scholar] [CrossRef]

- Hu, Y.; Nualart, D.; Song, X. A singular stochastic differential equation driven by fractional Brownian motion. Stat. Probab. Lett. 2008, 78, 2075–2085. [Google Scholar] [CrossRef]

- Mishura, Y.; Yurchenko-Tytarenko, A. Fractional Cox–Ingersoll–Ross process with small Hurst indices. Mod. Stochastics Theory Appl. 2019, 6, 13–39. [Google Scholar] [CrossRef]

- Nualart, D. The Malliavin Calculus and Related Topics; Springer: Berlin/Heidelberg, Germany, 2006; Volume 1995. [Google Scholar]

- Da Prato, G. Introduction to Stochastic Analysis and Malliavin Calculus; Springer: Berlin/Heidelberg, Germany, 2014; Volume 13. [Google Scholar]

- Nunno, G.D.; Øksendal, B.; Proske, F. Malliavin Calculus for Lévy Processes with Applications to Finance; Springer: Berlin/Heidelberg, Germany, 2008. [Google Scholar]

- Bouleau, N.; Hirsch, F. Dirichlet Forms and Analysis on Wiener Space; Walter de Gruyter: Berlin, Germany, 2010; Volume 14. [Google Scholar]

- Detemple, J.; Garcia, R.; Rindisbacher, M. Representation formulas for Malliavin derivatives of diffusion processes. Financ. Stochastics 2005, 9, 349–367. [Google Scholar] [CrossRef]

- Mukeru, S. The zero set of fractional Brownian motion is a Salem set. J. Fourier Anal. Appl. 2018, 24, 957–999. [Google Scholar] [CrossRef]

- Altmayer, M.; Neuenkirch, A. Multilevel Monte Carlo quadrature of discontinuous payoffs in the generalized Heston model using Malliavin integration by parts. Siam J. Financ. Math. 2015, 6, 22–52. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).