On the Analysis of Wealth Distribution in the Context of Infectious Diseases

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

- (i)

- (ii)

- Our trading rules are different from those in [18]. The trading rule in [18] introduces a random variable , requiring its mathematical expectations . In this work, we consider the effect of differences of wealth between agents during infectious diseases by setting and , where is a proportional constant and w stand for the wealth of two agents (for a detailed explanation of and , see Boghosian et al. [20]).

- (iii)

2. Wealth Dynamics in Epidemiologic Models

3. When

3.1. Steady-State Solution of

3.2. Steady-State Solution of

4. When

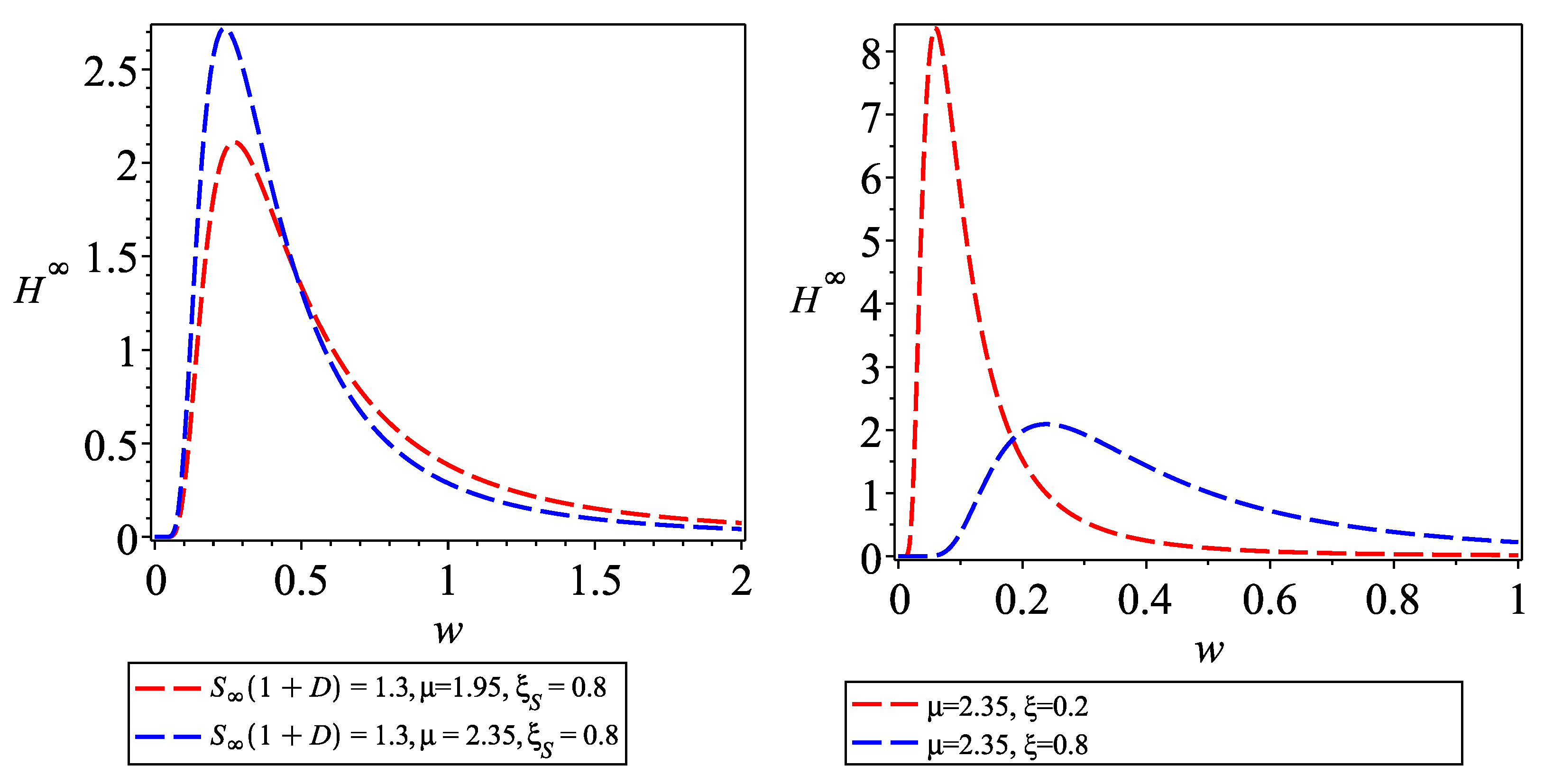

5. Numerical Experiments

6. Summarization

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Chahuán-Jiménez, K.; Rubilar, R.; De La Fuente-Mella, H.; Leiva, V. Breakpoint analysis for the COVID-19 pandemic and its effect on the stock markets. Entropy 2021, 23, 100. [Google Scholar] [CrossRef] [PubMed]

- Wang, L.; Liu, M.; Lai, S. Wealth exchange and decision-making psychology in epidemic dynamics. Math. Biosci. Eng. 2023, 20, 9839–9860. [Google Scholar] [CrossRef] [PubMed]

- Goenka, A.; Liu, L.; Nguyen, M.H. Infectious diseases and economic growth. J. Math. Econ. 2014, 50, 34–53. [Google Scholar] [CrossRef]

- Bai, J.; Wang, X.; Wang, J. An epidemic-economic model for COVID-19. Math. Biosci. Eng. 2022, 19, 9658. [Google Scholar] [CrossRef] [PubMed]

- Camera, G.; Gioffré, A. The economic impact of lockdowns: A theoretical assessment. J. Math. Econ. 2021, 97, 102552. [Google Scholar] [CrossRef]

- Dimarco, G.; Perthame, B.; Toscani, G.; Zanella, M. Kinetic models for epidemic dynamics with social heterogeneity. J. Math. Biol. 2021, 83, 4. [Google Scholar] [CrossRef]

- Hosseinpoor, A.R.; Bergen, N.; Mendis, S.; Harper, S.; Verdes, E.; Kunst, A.; Chatterji, S. Socioeconomic inequality in the prevalence of noncommunicable diseases in low-and middle-income countries: Results from the World Health Survey. BMC Public Health 2012, 12, 474. [Google Scholar] [CrossRef] [PubMed]

- Zhang, D.; Hu, M.; Ji, Q. Financial markets under the global pandemic of COVID-19. Financ. Res. Lett. 2020, 36, 101528. [Google Scholar] [CrossRef]

- Bernardi, E.; Pareschi, L.; Toscani, G.; Zanella, M. Effects of vaccination efficacy on wealth distribution in kinetic epidemic models. Entropy 2022, 24, 216. [Google Scholar] [CrossRef]

- Düring, B.; Toscani, G. International and domestic trading and wealth distribution. Commun. Math. Sci. 2008, 6, 1043–1058. [Google Scholar] [CrossRef]

- Quevedo, D.S.; Quimbay, C.J. Non-conservative kinetic model of wealth exchange with saving of production. Eur. Phys. J. B 2020, 93, 186. [Google Scholar] [CrossRef]

- Toscani, G.; Brugna, C.; Demichelis, S. Kinetic models for the trading of goods. J. Stat. Phys. 2013, 151, 549–566. [Google Scholar] [CrossRef]

- Toscani, G.; Tosin, A.; Zanella, M. Multiple-interaction kinetic modelling of a virtualitem gambling economy. Phys. Rev. E 2019, 100, 012308. [Google Scholar] [CrossRef] [PubMed]

- Pareschi, L.; Toscani, G. Self-similarity and power-like tails in nonconservative kinetic models. J. Stat. Phys. 2006, 124, 747–779. [Google Scholar] [CrossRef]

- Della, M.R.; Loy, N.; Menale, M. Intransigent vs. volatile opinions in a kinetic epidemic model with imitation game dynamics. Math. Med. Biol. 2023, 40, 111–140. [Google Scholar] [CrossRef]

- Loy, N.; Tosin, A. A viral load-based model for epidemic spread on spatial networks. Math. Biosci. Eng. 2021, 18, 5635–5663. [Google Scholar] [CrossRef]

- Hethcote, H.W. Three Basic Epidemiological Models; Springer: Berlin, Germany, 1989. [Google Scholar] [CrossRef]

- Cordier, S.; Pareschi, L.; Toscani, G. On a kinetic model for a simple market economy. J. Stat. Phys. 2005, 120, 253–277. [Google Scholar] [CrossRef]

- Dimarco, G.; Pareschi, L.; Toscani, G.; Zanella, M. Wealth distribution under the spread of infectious diseases. Phys. Rev. E 2020, 102, 022303. [Google Scholar] [CrossRef]

- Boghosian, B.M.; Devitt-Lee, A.; Johnson, M.; Li, J.; Jeremy, A.M.; Wang, H. Oligarchy as a phase transition: The effect of wealth-attained advantage in a Fokker–Planck description of asset exchange. Physica A 2017, 476, 15–37. [Google Scholar] [CrossRef]

- Pareschi, L.; Toscani, G. Interacting Multiagent Systems: Kinetic Equations and Monte Carlo Methods; Oxford Press: Oxford, UK, 2013; Available online: https://searchworks.stanford.edu/view/13529761 (accessed on 9 September 2024).

- Düring, B.; Pareschi, L.; Toscani, G. Kinetic models for optimal control of wealth inequalities. Eur. Phys. J. B 2018, 91, 265. [Google Scholar] [CrossRef]

- Gini, C. Measurement of inequality of incomes. Econ. J. 1921, 31, 124–125. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, T.; Lai, S.; Zhao, M. On the Analysis of Wealth Distribution in the Context of Infectious Diseases. Entropy 2024, 26, 788. https://doi.org/10.3390/e26090788

Zhang T, Lai S, Zhao M. On the Analysis of Wealth Distribution in the Context of Infectious Diseases. Entropy. 2024; 26(9):788. https://doi.org/10.3390/e26090788

Chicago/Turabian StyleZhang, Tingting, Shaoyong Lai, and Minfang Zhao. 2024. "On the Analysis of Wealth Distribution in the Context of Infectious Diseases" Entropy 26, no. 9: 788. https://doi.org/10.3390/e26090788

APA StyleZhang, T., Lai, S., & Zhao, M. (2024). On the Analysis of Wealth Distribution in the Context of Infectious Diseases. Entropy, 26(9), 788. https://doi.org/10.3390/e26090788