Abstract

The main objective of this paper is to present an algorithm of pricing perpetual American put options with asset-dependent discounting. The value function of such an instrument can be described as where is a family of stopping times, is a discount function and is an expectation taken with respect to a martingale measure. Moreover, we assume that the asset price process is a geometric Lévy process with negative exponential jumps, i.e., . The asset-dependent discounting is reflected in the function, so this approach is a generalisation of the classic case when is constant. It turns out that under certain conditions on the function, the value function is convex and can be represented in a closed form. We provide an option pricing algorithm in this scenario and we present exact calculations for the particular choices of such that takes a simplified form.

MSC:

60G40; 60J60; 91B28

JEL Classification:

G13; C61

1. Introduction

In this paper, we consider a perpetual American put option with asset-dependent discounting. We consider a standard stochastic background for this problem, i.e., we define a complete filtered risk-neutral probability space , on which we define the asset price process . Then, is a natural filtration of satisfying the usual conditions and is a risk-neutral measure under which the discounted (with respect to the risk-free interest rate ) asset price process is a local martingale. A family of -stopping times is denoted by while denotes the expectation with respect to when . The value function of the perpetual American put option with asset-dependent discounting can be represented by

The asset-dependent discounting is reflected in the function, which is our key concept considered in this article. We underline here that the discount function for various economical reasons can be different from the risk-free interest rate ; see Al-Hadad and Palmowski (2021) for further explanation. The way we choose discounting is to model strong dependence of discount factor with the asset price. The goal is to understand various economical phenomena that might appear in this extreme case. Our approach differs from typical studies considered in the literature, where the interest rate is independent from the asset price or there is a weak dependence between these two factors. Therefore, this research is noteworthy not only in the context of option pricing, but also in other areas where optimisation problems appear.

Our main motivation comes from the work of Linetsky (1999) who considers up-and-out put options traded mainly over-the-counter. In these options, the discounting factor depends exponentially on the cumulative excursion time above or below a given barrier during the entire life of the option. In other words, where . Similar step-like options were considered in Rodosthenous and Zhang (2018) where the discounting is related to the occupation time of the asset price below a fixed level y exceeding an independent exponential random variable with mean . This discounting corresponds to the special choice of , where r is a risk-free interest rate. In general, one can think of as the general knock-out (or knock-in) rate depending on the asset price of some vanilla options. This additional feature might allow us to customise the financial product according to the demand of the risk management.

Moreover, we assume that the asset price process is a geometric Lévy process with negative exponential jumps, i.e.,

with

where and are constant, is the Poisson process with intensity independent of Brownian motion , and are i.i.d. random variables independent of and having exponential distribution with mean . Under the martingale measure , the drift parameter is of the form

Note that when , then we end up with the classical Black–Scholes model. However, empirical studies show that stock prices have a heavier left tail than normal distribution. Note that the negative jumps underline the market crashes that appear once per while. Therefore, nowadays many books and articles concern, as we do in this work, pricing of derivative securities in market models based on Lévy processes; see Cont and Tankov (2004) for more details. Still, to get a complete picture, we analyse here the case of as well. Our model of asset price is a particular case of the Kou model where the logarithm of the price process is a jump diffusion; see Kou (2002).

The main objective of this paper is to present an algorithm of pricing perpetual American put options with asset-dependent discounting with the value function defined in (1) and the asset price process given in (2). Furthermore, we take into account some specific scenarios (e.g., when or ), and, for these cases, we are able to derive analytical forms of the value function, while for more complex examples, we show how to handle them numerically.

Detailed theoretical results of the analysed problem were already developed in Al-Hadad and Palmowski (2021), where the authors presented the approach of deriving a closed form of value function (1) for even a more general setting than it is considered here. Therefore, in this paper, we focus more on numerical side of this problem and analyse, in detail, a few particular cases where more explicit results can be derived.

Still, before we present the option pricing method in our set-up, we recall the most important theoretical issues on which our article is based on. A key step in deriving a closed form of (1) is identifying the form of the optimal stopping rule for which the supremum in (1) is attained. It turns out that under certain conditions on the discount function , which are presented in the next section, the value function is convex. By combining this fact with the classical optimal stopping theory presented, e.g., in Peskir and Shiryaev (2006), it allows us to conclude that the optimal stopping region is an interval and hence

for some optimal thresholds . Observe that for the non-negative discount function , we have (since waiting is not beneficial). Therefore, in this case a single continuation region appears. In general, for the negative , we can observe a double continuation region; for more details, see De Donno et al. (2020).

The optimal boundary levels and can be found by application of standard methods of maximising the function

over l and . To find , we use exit identities for spectrally negative Lévy processes containing so-called omega scale functions introduced in Li and Palmowski (2018).

As shown in (Al-Hadad and Palmowski 2021, Theorem 9), another way of finding the optimal thresholds is to apply the classical smooth and continuous fit conditions.

Typically, a price of the option is a solution to a certain Hamiltonian–Jacobi–Bellman (HJB) system, and the optimal thresholds are identified using the smooth fit conditions. We want to underline that our approach is different, although still finding the omega scale functions is carried out via solving certain ordinary differential equations.

The paper is organised as follows. In Section 2, we introduce basic theory and notation. Section 2.4 provides the main theoretical results of this paper. In Section 3, we present some specific examples where the option price can be expressed in the explicit way. Section 4 focuses on the purely numerical analysis. We also show there that these two approaches are consistent. The last section includes our conclusions.

2. Preliminaries

2.1. Assumptions

It the beginning, we note that the analysed American put option will not be realised when its payoff is equal to 0. Hence, we can transform the form of the value function given in (1) into the following one

We work under the same assumptions as those formulated in (Al-Hadad and Palmowski 2021, Section 2.2). However, this time we consider slightly more specific assumptions on the function, namely, that

Assumption 1.

A discount function ω is concave, nondecreasing and bounded from below.

From (Al-Hadad and Palmowski 2021, Remark 3) we can then conclude that under Assumption 1, the value function is convex.

2.2. Optimal Stopping Time

From (Al-Hadad and Palmowski 2021, Section 2.4), it follows that the optimal exercise time is the first entrance of the process into some interval, that is, it has the following form

Moreover, we denote the optimal stopping time by

where and realise the supremum above. As shown in (Al-Hadad and Palmowski 2021, Theorem 9), another way of identifying the critical points and can be achieved via application of the smooth fit property. In that case, and satisfy

2.3. Scale Functions

By applying the fluctuation theory of Lévy processes, we can find a closed form of (5), and hence of (4), in terms of the so-called omega scale functions.

To introduce them formally, first let us define the Laplace exponent of via

which is well-defined for since our is a spectrally negative Lévy process. In the case of given in (3), the Laplace exponent takes the form

By , we denote the right inverse of , i.e.,

where .

The first scale function is defined as a continuous and increasing function such that for all , while for , it is defined via the following Laplace transform

for . We define also the related scale function by

where . From Cohen et al. (2013), we know that for given in (3), we have

where is the set the real solutions to . In turn, is as follows

If we take or in (7), then and take simplified forms

and

for and being again the real solutions to .

The generalisation of and are the -scale functions , , where is an arbitrary measurable function. They are defined as the unique solutions to the following equations

where is a classical zero scale function.

To simplify notation, we introduce also the following counterparts of the scale functions (11) and (12)

where .

For , for which the Laplace exponent is well-defined, we can define a new probability measure via

By Palmowski and Rolski (2002) and (Kyprianou 2006, Cor. 3.10), under , the process is again a spectrally negative Lévy process with the new Laplace exponent

where

For the new probability measure , we can define the -scale functions which are denoted by the adding subscript to the regular counterparts, i.e., , .

Lastly, we define the following auxiliary functions

2.4. Theoretical Representation of the Price

The starting point for our entire analysis is the following results. The first one is a corollary from (Al-Hadad and Palmowski 2021, Theorem 15).

Theorem 1.

Let Assumption 1 hold, and assume that ω is non-negative. Then, the optimal stopping region is of the form and we have

- 1.

- For and

- 2.

- For and

- 3.

- For andwhere

Remark 1.

Remark 2.

To find the option price , we have to identify

where is given in (16), and the case of corresponds to and .

Observe that we need to find the above -scale functions for under measure , i.e., we have to identify and . This is equivalent to taking our asset price process of the form of (2) but with the new parameters given in (15).

The second key result for our numerical analysis follows straightforward from (Al-Hadad and Palmowski 2021, Theorem 16) and allows us to identify the above omega scale functions using ordinary differential equations.

3. Option Pricing—Analytical Approach

In this section, we present some examples of discount functions for which we are able to determine the analytical form of the value function .

3.1. Constant Discount Function

The case when function is constant, i.e., is the standard example which appears in the literature quite extensively. However, this case is quite special, as it turns out that the second term of the sum in (19) simplifies and we do not need to deal with the measure (and thus to calculate the limit for ) to find . This fact is stated in the below theorem.

Theorem 3.

Assume that . Then

Proof.

Note that

corresponds to the continuous transition of the process to the interval or, in other words, continuous exit from half-line . We define

It turns out that formula (23) is equivalent to

for details, see (Al-Hadad and Palmowski 2021, Proof of Theorem 7).

Then, using (Loeffen et al. 2014, (13)) for , and together with the fact that (see (Kyprianou 2006, 8.5 (ii), p. 235)), we obtain

Lastly, taking limit and applying L’Hospital’s Rule, complete the proof. □

Ultimately, value function (19) for the constant discount function can be written as

Remark 3.

For the case of , using (22), one can show that value function (18) simplifies to the well-known formula for the value function in the Black–Scholes model, i.e.,

where we substituted and . Therefore, we are not forced to apply the smooth fit condition in order to find the optimal value of u. We can do this analytically by finding the maximum of with respect to u.

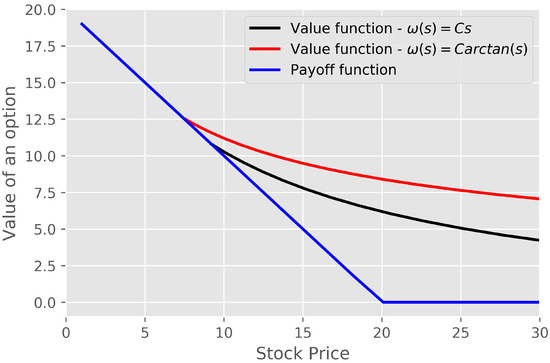

Figure 1.

The value and payoff functions for the given set of parameters: , , , , and .

Based on Figure 1, we can simply note that a higher value of the discount function results in a smaller value of , which is in line with the financial intuition.

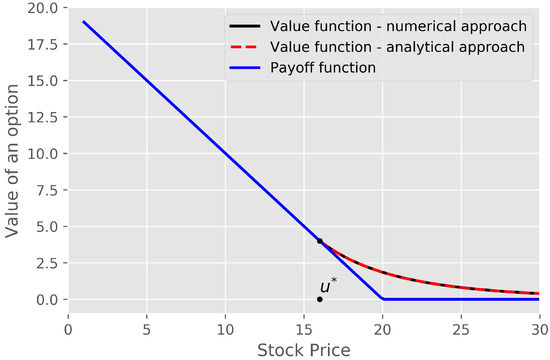

Figure 2.

The value and payoff functions for the given set of parameters: , , , , and .

The resulting relation between these functions is again consistent with the economical expectations.

3.2. Linear Discount Function

In this subsection, we consider a linear discount function of the form for some positive constant C.

3.2.1.

Let us consider the case of . Then, the asset price process jumps into the interval , which means from Theorem 1 that

where . Equivalently, (24) can be rewritten as

where and .

To find a closed form of value function (25), we need to identify the scale functions and . From Theorem 2, it follows that both and solve the following ordinary differential equation

with , and , while the initial conditions are as follows

and

Substituting and to (26), we obtain the Kummer’s equation of the form

where and .

If b is not an integer, then the general solution to (29) has the form

where and are the constants that can be found based on the initial conditions, , , , , while is the Kummer confluent hypergeometric function.

We denote by , and , the constants corresponding to and , respectively. Using initial conditions (27) and (28), we can simply calculate these constants for both and . By shifting these functions by , we simply produce and .

The asymptotic behaviour of for is as follows

3.2.2.

Let us consider the case of . In this case, the asset price process enters the interval in a continuous way only. Therefore, from Theorem 1

which is equivalent to

It suffices to find now and . From Theorem 2, it follows that and solve

with , and . The initial conditions have the following form

and

Substituting and to (35), we obtain the Bessel differential equation of the form

where . The general solution to (38) is equal to

and therefore

Based on the form of (39) and the fact that does not depend on , we can simply note that value function (34) is also independent of . Therefore, we can take an arbitrary value of in (35). Thanks to this key observation, its solution (39) can take a simplified form. Indeed, for , Equation (35) is equal to

where and . Hence, the general solution to (40) takes the following form

For , where and , Equation (41) reduces to

If we take the following sample parameters and , we obtain and therefore

3.3. Power Discount Function

This time, we take into account a power function of the form for and C being some positive contant. This case is a generalisation of a linear discount function.

3.3.1.

Similar to the case of a linear discount function, the scale functions and solve

with , and , while the initial conditions are the same as those provided in (27) and (28). Applying a substitution and , we transform (44) into

where and . The general solution to (45) has the same form as was provided in (30).

Therefore, for both the linear and the power discount function , the form of the value function is identical.

3.3.2.

As in the above case, the idea of finding a closed form of the value function can be borrowed from the linear case. This time, the scale functions and satisfy the equation

with , and , while the initial conditions are of the form (36) and (37). If we substitute and , we receive the Bessel differential equation for with the solution

Therefore, we have

where . We can show, as in the prevoius section, that the value function which arises in this scenario does not depend on . Thus, for , (46) takes the form

Again, having exact formulas for the scale functions, we can easily represent the form of the value function. All results are presented in Section 4.

4. Option Pricing—Numerical Approach

In this section, we show how to numerically identify the value function for arbitrary discount function . We present some figures corresponding to the various discount functions as well.

4.1. Different Discount Functions

For some discount functions , we are unable to find the analytical forms of , , and , which are the solutions to the ordinary differential equations occurring in Theorem 2. That is, formally we cannot identify explicitly the value function either. In such a situation, we can proceed a numerical analysis of these equations.

In general, solving a high-order ordinary differential equation consists of transforming it into first-order vector form and then applying an appropriate algorithm that returns the numerical solution of the -dimensional system of first-order ordinary differential equations. For practical purposes, however—such as in financial engineering—numeric approximations to the solutions of ordinary differential equations are often sufficient. In this paper, we focus on the Higher-Order Taylor Method. This method employs the Taylor polynomial of the solution to the equation. It approximates the 0-th order term by using the previous step’s value (which is the initial condition for the first step), and the subsequent terms of the Taylor expansion by using the differential equation.

4.1.1.

For the case of , we showed in the previous section how to derive the value function for the linear discount function . Figure 3 presents comparison of the value function given in (24) when the scale functions were calculated analytically (as shown in Section 3.2.1) and numerically by solving differential ordinary Equation (26). In this example, a linear discount function was chosen, i.e., . The difference between these functions is so small that this is negligible.

Figure 3.

Comparison of value function (24) for for both methods of determining the scale functions—analytical and numerical one. The chosen set of parameters is as follows: , , , , .

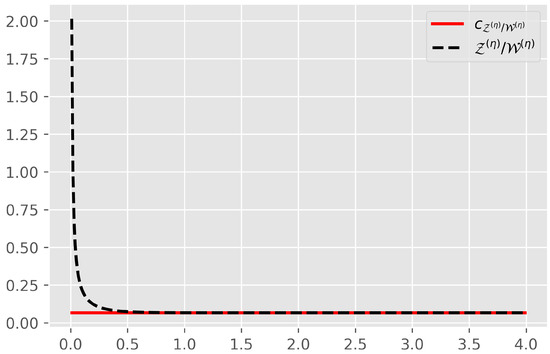

Moreover, Figure 4 illustrates the constant obtained in (32) together with the quotient of the functions and .

Figure 4.

Comparison of the constant and the ratio of and for a linear discount function and , , , , .

As we mentioned at the beginning of this section, we are not always able to get an analytical solution to an ordinary differential equation. This is the case, for example, when the discount function is of the form for some positive C. Then, we can only obtain the scale functions numerically. Figure 5 shows two value functions, for and , respectively. Since for all positive s we have , then we expect that the value function corresponding to takes greater values rather than for . We can also note that the difference between these functions becomes greater for higher values of s, which is in line with economical intuition since the difference between and also extends as s increases.

Figure 5.

Comparison of value function (24) for both and and for the given set of parameters: , , , , .

4.1.2.

The case of corresponds to the situation when the stock price process (2) does not have any jumps. Then, the value function takes the form (18). From the numerical point of view, the problem lies in choosing a sufficiently large value of in (18) to obtain the final and right form of the value function. In this section, we avoid this problem by selecting discount functions for which the value function is independent of the parameter.

Figure 6 presents a comparison of the value function given in (33) for and for the scale functions obtained analytically and numerically. As shown in Section 3.2.2, in this case, we can take an arbitrary value of and obtain a simplified form of the value function and ordinary differential equation that the scale functions solve. Similar to the previous example, we again can observe a negligible difference between these two value functions.

Figure 6.

Comparison of value function (33) for for both methods of determining the scale functions–analytical and numerical one. The chosen set of parameters is as follows: , , , .

Figure 7.

Comparison of the constant and the ratio of and for a linear discount function and , , , .

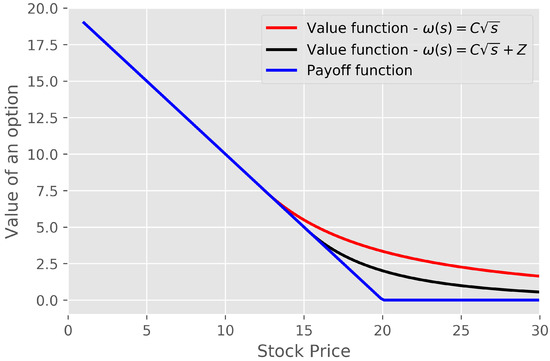

Lastly, in Figure 8, we can observe the value functions for both and for some positive Z, i.e., we compare two discount functions that differ in shift. This time, we can see that the value functions obtained in this way also differ only in shift, which confirms financial intuition.

Figure 8.

Comparison of value function (33) for both and and for the given set of parameters: , , , , .

4.1.3. and

The most general case is when and . Then, the considered value function is given by (19). It can be also represented as the function of x variable:

For the linear discount function , the scale functions and occurring in (47) are the solutions to the following ordinary differential equation

with , , , .

The initial conditions for and are as follows

and

Thus, and solve

with , , , , . The initial conditions for and are as follows

and

In this case, we are not able to identify explicit solutions to third-order ordinary differential Equations (48) and (49). Therefore, we are forced to use only the numerical method to find the scale functions and, hence, the value function.

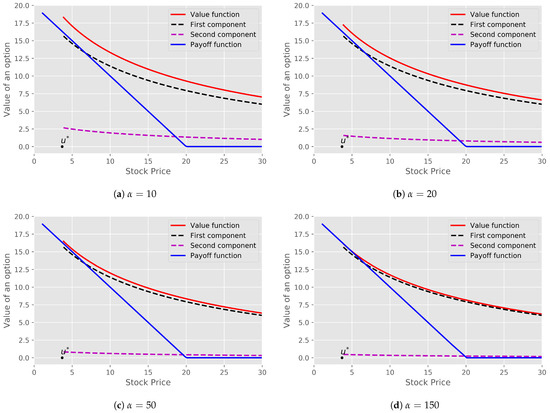

Figure 9 shows several graphs of the value function (19) for different values of parameter together with the first and second component occurring in (19).

Figure 9.

Comparison of value function (19) for the particular choice of , and for the given set of parameters: , , , , , .

5. Conclusions

In this paper, we have presented a novel approach to pricing the perpetual American put options with asset-dependent discounting. For the asset price process being the geometric spectrally negative Lévy process, we have shown that the value function (1) is the solution of the ordinary differential equations given in Theorem 2. We have used these theoretical results to perform extended numerical analysis for some key financial examples. In particular, for some cases, we have managed to produce some explicit formulas for the value function. In the cases where it was impossible to do so, we have used the numerical analysis of the above-mentioned ordinary differential equations based on the Higher-Order Taylor Method. We have presented many figures of the value functions that arise in various scenarios.

One can think of further generalisations; for example, when the discount factor is randomised. Thia can be achieved in different ways, e.g., by introducing additional Markov economical environment. One can also think about other very realistic models for financial assets, for example, based on generalised hyperbolic distributions and their subclasses; see Prause (1999), for more details. This type of research is left for future investigations.

Author Contributions

Methodology, J.A.-H. and Z.P.; Formal Analysis, J.A.-H. and Z.P.; Investigation, J.A.-H. and Z.P.; Writing—Original Draft Preparation, J.A.-H.; Writing—Review and Editing, Z.P.; Visualization, J.A.-H.; Supervision, Z.P.; Project Administration, Z.P.; Funding Acquisition, Z.P. All authors have read and agreed to the published version of the manuscript.

Funding

This paper is supported by the National Science Centre under the grant 2016/23/B/HS4/00566 (2017–2020).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

Both authors thank the anonymous referees for their helpful comments.

Conflicts of Interest

The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript, or in the decision to publish the results.

References

- Al-Hadad, Jonas, and Zbigniew Palmowski. 2021. Perpetual American Options with Asset-Dependent Discounting. Submitted for Publication. Available online: https://arxiv.org/abs/2007.09419 (accessed on 18 July 2020).

- Cohen, Serge, Alexey Kuznetsov, Andreas Kyprianou, and Victor Rivero. 2013. Lévy Matters II. Berlin/Heidelberg: Springer. [Google Scholar]

- Cont, Rama, and Peter Tankov. 2004. Financial Modelling with Jump Processes. Boca Raton: Chapman & Hall. [Google Scholar]

- De Donno, Marzia, Zbigniew Palmowski, and Joanna Tumilewicz. 2020. Double continuation regions for American and Swing options with negative discount rate in Lévy models. Mathematical Finance 30: 196–227. [Google Scholar] [CrossRef]

- Kou, Steven G. 2002. A Jump-Diffusion Model for Option Pricing. Management Science 48: 1086–1101. [Google Scholar] [CrossRef]

- Kyprianou, Andreas E. 2006. Introductory Lectures on Fluctuations of Lévy Processes with Applications. Berlin/Heidelberg: Springer. [Google Scholar]

- Li, Bo, and Zbigniew Palmowski. 2018. Fluctuations of omega–killed spectrally negative Lévy processes. Stochastic Processes and their Applications 128: 3273–99. [Google Scholar] [CrossRef]

- Linetsky, Vadim. 1999. Step options. Mathematical Finance 9: 55–96. [Google Scholar] [CrossRef]

- Loeffen, Ronnie L., Jean-François Renaud, and Xiaowen Zhou. 2014. Occupation times of intervals until first passage times for spectrally negative Lévy processes. Stochastic Processes and their Applications 124: 1408–143. [Google Scholar] [CrossRef]

- Palmowski, Zbigniew, and Tomasz Rolski. 2002. A technique for exponential change of measure for Markov processes. Bernoulli 8: 767–85. [Google Scholar]

- Peskir, Goran, and Albert Shiryaev. 2006. Optimal Stopping and Free–Boundary Problems. Basel: Birkhäuser. [Google Scholar]

- Prause, Karsten. 1999. The Generalized Hyperbolic Model: Estimation, Financial Derivatives, and Risk Measures. Ph.D. thesis, University of Freiburg, Breisgau, Germany. Available online: https://d-nb.info/961152192/34 (accessed on October 1999).

- Rodosthenous, Neofytos, and Hongzhong Zhang. 2018. Beating the omega clock: An optimal stopping problem with random time-horizon under spectrally negative Lévy models. Annals of Applied Probability 28: 2105–40. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).