Abstract

In this study, the impact of arbitrage resulting from Covered Interest Parity (CIP) deviations on Korea’s long-term interest rates was analyzed, utilizing Vector Error Correction (VEC) models for Granger Causality and Impulse Response Function analyses. This analysis covered the period from February 2002 to September 2023, with a comparative analysis of the periods before and after the Global Financial Crisis (GFC). The Granger Causality analysis indicated that changes in the swap basis reflecting CIP deviation presented a significant Granger causal relationship with the variations in domestic long-term interest rates. Notably, in the post-GFC period, when CIP deviations were relatively pronounced, the incentives for arbitrage trading exhibited a stronger leading effect in terms of inducing changes in domestic long-term interest rates. The Impulse Response Function analysis showed that domestic long-term interest rates significantly and negatively responded to the positive shocks in the swap basis. This response was even more pronounced during the period following the GFC. Additionally, foreign long-term interest rates and monetary policy variables also demonstrated a significant impact on domestic long-term interest rates. These findings imply that the adjustment path back to equilibrium from CIP deviations, driven by arbitrage, was developed more through changes in domestic interest rates rather than exchange rate fluctuations, especially after the GFC.

1. Introduction

The evaluation of the Covered Interest Rate Parity (CIP) condition has long been considered a fundamental principle in the international financial markets. According to CIP theory, under the assumption of free capital movement, the yields of identical financial assets denominated in different currencies equalize through arbitrage and exchange risk hedging. However, if transaction costs associated with capital movement are high or if there are capital controls, CIP deviations may occur.

Examining existing studies analyzing CIP imbalances, substantial results supporting the validity of CIP were reported in research before the Global Financial Crisis (GFC). However, studies analyzing the periods during and after the GFC (2008–2009) reported that due to factors such as financial regulations, risk aversion, monetary policies, and liquidity constraints, significant CIP deviations occurred (Du et al. 2019; Baba et al. 2008; Cerutti et al. 2020; Liao 2019). When CIP deviations occur due to domestic or international financial shocks, they act as arbitrage incentives for global investors.

This study primarily aims to analyze the impact of arbitrage resulting from CIP deviations on domestic long-term interest rates in Korea. The adjustment path from CIP deviations to CIP equilibrium can be formed through adjustments in exchange rates or domestic interest rates. The hypothesis of this study is that the adjustment path from CIP deviations to equilibrium is largely generated through changes in domestic long-term interest rates. Additionally, this study aims to examine other factors influencing domestic long-term interest rates.

The validity or deviation of the CIP condition also has implications for monetary policy. If CIP conditions hold, emerging market countries, with the aim of controlling long-term interest rates, can enact monetary policies more independently from monetary central countries such as the United States (Bernanke 2017). However, if significant CIP deviations occur, the ability of emerging market countries to control long-term interest rates independently of external factors may weaken.

In the context of Korea’s economic structure, which is still considered a small open economy, significant CIP deviations may pose a risk of instability in domestic financial markets and long-term interest rates due to external factors such as international arbitrage and global interest rates.

To achieve the research objectives, this study analyzes the impact of CIP deviations and domestic and international variables on domestic long-term Treasury bond yields. Analyzing long-term bond yields is suitable for investigating CIP theory because, unlike stock trading, bond trading involves almost all global transactions hedging against exchange risk. Moreover, analyzing domestic long-term Treasury bond yields allows for understanding the major determinants of long-term interest rates, which have closer links with the real economy.

As of October 2023, foreign investors held KRW 241.6 trillion in listed bonds, with Treasury bonds accounting for approximately 91% (Korea Financial Supervisory Service 2023). The trading volume of foreign investors in domestic bonds (the sum of buying and selling) accounts for about 20% of the outstanding Treasury bond issuance, making their impact on the domestic market significant.

Previous research on CIP deviations or imbalances often used variables of swap rates (forward exchange rate—spot exchange rate/spot exchange rate) or differences between internal-external interest rate differentials and swap rates as arbitrage incentive variables reflecting CIP deviations. Recent studies have focused on analyzing the CIP deviation issue from the perspective of imbalances in supply and demand in interest rate swaps and currency swap markets, where global bond investors actually trade (Sushko et al. 2016; Avdjiev et al. 2019; Hong et al. 2021; Du et al. 2018). Similarly, this study utilizes actual arbitrage incentive data arising from bond investments when global investors engage in hedging transactions in the swap market to analyze the effects of CIP deviations.

This study differs from existing research in several aspects. While previous studies have primarily focused on analyzing the presence of and reasons for CIP deviation, this study examines the impact of CIP deviation on domestic long-term interest rates by linking it to the swap market. Additionally, it distinguishes between pre- and post-global financial crisis periods to compare and analyze the effects of CIP deviation. These differences contribute to a more comprehensive understanding of how CIP deviation can vary over time and in different contexts, providing insights into monetary policy and the interactions between various markets.

To analyze the impact of arbitrage incentive variables resulting from CIP deviations on domestic long-term Treasury bond yields, this study models the determinants of long-term interest rates by applying previous research on the subject. Previous studies on the determinants of long-term interest rates can be divided into recent views that emphasize the role of global capital movement and traditional views that assert the importance of the role of fundamentals and the term structure of interest rates.

The view that global capital movement plays a crucial role in determining long-term interest rates has been supported by studies related to the GFC and those discussing global interest rate synchronization. According to GFC-related studies, the significant inflow of global capital into the U.S. long-term government bond market in the mid-2000s, along with large-scale investments by East Asian countries with large current account surpluses, caused a decline in U.S. long-term interest rates (Beltran et al. 2013; Warnock and Warnock 2009; Hunt 2008; Bernanke 2017). Studies on global interest rate synchronization suggest that, in the current environment of free capital movement, there is a form of interest rate synchronization where the long-term interest rates of advanced countries influence those of emerging market countries. These studies argue that various forms of large-scale capital movements are causing an international synchronization of long-term interest rates and that, even if emerging market countries adopt floating exchange rate systems, it is hard to suppress interest rate synchronization and maintain the independence of a monetary policy (Rey 2016; Turner 2014; Bruno and Shin 2012; Obstfeld 2015).

On the other hand, the traditional view that emphasizes fundamentals and the term structure argues that factors such as business fluctuations, the expected inflation rate, and risk factors determine long-term interest rates by forming term premiums (Backus and Wright 2007; Kozicki and Sellon 2005; Clostermann and Seitz 2005; Cochrane 2007; Graeve et al. 2009; Bonser and Morley 1997; Estrella et al. 2003).

In this paper, I comprehensively analyze not only arbitrage incentive variables reflecting CIP deviations but also domestic and international fundamental factors according to the research objectives explained above. The empirical analysis period covers February 2002 to September 2023, and I divide it into two periods for comparison: pre-GFC (February 2002 to June 2007) and post-GFC (January 2010 to September 2023).

The structure of this paper is as follows: In Section 2, I examine the phenomenon of CIP deviations from the perspective of the exchange risk hedging market. Section 3 provides explanations of the data used and the analytical model settings. In Section 4, I examine the empirical analysis results, and in Section 5, I present my conclusions.

2. CIP Deviation and Swap Market Hedging

In this chapter, I examine the significance of CIP deviation and explore the relationship between CIP deviation and the imbalance of demand and supply in the swap market. When CIP equilibrium is maintained, the yield of financial assets denominated in different currencies but with the same maturity and risk, in trading with exchange rate risk hedging, becomes equal. For instance, if a Korean investor invests in U.S. Treasury bonds while hedging exchange rate risk, the yield of Korean Treasury bonds will be equal to the yield of U.S. Treasury bonds plus the forward premium.

The corresponding formula is represented as follows:

Here, R*t,t+k is the yield of foreign bonds with maturity k at time t, Rt,t+k is the yield of domestic bonds with maturity k at time t, Ft,t+k is the forward exchange rate with maturity k at time t, and St is the spot exchange rate at time t. When domestic investors invest in foreign bonds, with forward exchange hedging, the total yield of foreign bonds is R*t,t+k + (Ft,t+k − St)/St, and the yield from domestic bond investment is Rt,t+k.

In global bond trading, as currency conversion is involved, institutions mostly acquire different currencies through the swap market or foreign exchange market. While the foreign exchange market does not involve hedging exchange rate risk, the swap market allows hedging, so institutional investors mostly acquire different currencies through the swap market. That is, global bond investors acquire different currencies, hedging currency risk though spot buying/forward selling (buy & sell) or spot selling/forward buying (sell & buy) in the FX swap or currency swap market.

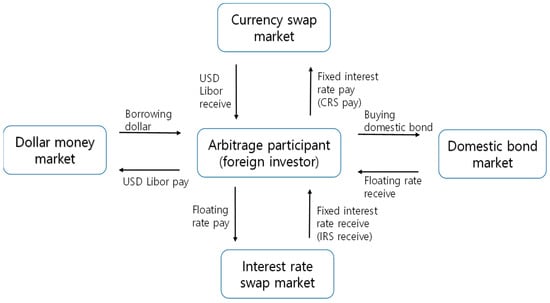

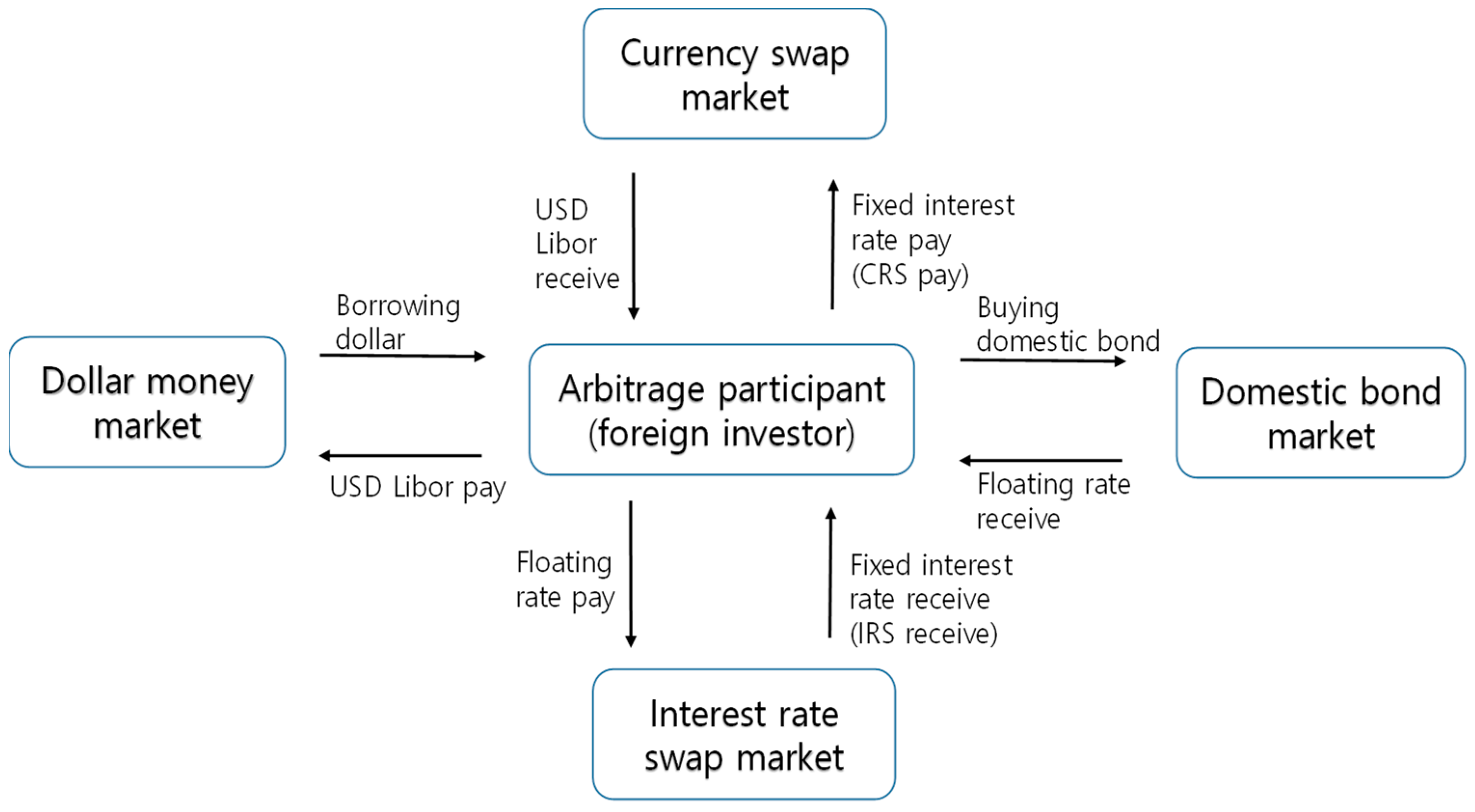

As shown in Figure 1, when foreign investors invest in domestic bonds, they acquire KRW through the currency swap market, paying the Currency Swap Rate (CRS) and receiving the London Interbank Offered Rate (Libor), taking a CRS payment position. This process results in an initial profit equal to the Swap Spread, which represents the difference between the domestic bond yield (variable rate) and the CRS rate. And then foreign investors take an IRS reception position in which they pay a floating interest rate accrued from domestic bonds and receive fixed interest rates through IRS (Interest Rate Swap) transactions. So, foreign investors investing in domestic bonds profit by subtracting the CRS from the IRS, that is, negative (−) the swap basis.

Figure 1.

Structure of arbitrage through swap market.

In actual dollar-funding markets, when a gap arises between the dollar-funding rate and the swap market rate, this gap is considered the extent of CIP deviation and is reflected in the swap basis (Baba et al. 2008). Thus, the swap basis reflects the incentive for risk-free arbitrage transactions that arise while hedging exchange rate risk. Also, the swap basis reflects the demand for dollar funding (Iida et al. 2018). The swap basis, which represents the IRS deducted from the CRS, is mostly negative. When the absolute value of the negative swap basis increases, the incentive for foreign investors investing in domestic bonds increases, while the funding and hedging costs for Korean investors investing in foreign bonds increase. Conversely, if the swap basis in the swap market between USD and KRW shows a positive value, the funding cost for Korean investors investing in foreign bonds decreases, while the KRW funding rate for foreign investors investing in domestic bonds increases.

Studies on CIP deviation and its causes have shown that before the Global Financial Crisis (GFC), results supporting the validity of CIP equilibrium were predominant. Frenkel and Levich (1975, 1977) argued that the cause of CIP deviation was the increase in transaction costs in the foreign exchange market due to differences in exchange rate systems. McCormick (1979) claimed that the notion of a CIP equilibrium was valid and that the main cause of CIP deviation was capital controls on international capital flows. Akram et al. (2008) argued that before the GFC, CIP conditions were maintained because small arbitrage opportunities were quickly exhausted.

In studies covering the GFC period and the post-GFC period, results indicating the existence of CIP deviation rather than CIP equilibrium have been reported. The main causes of CIP deviation in these studies are attributed to an increased demand for USD due to factors such as financial regulations, monetary policy, and risk aversion. Du et al. (2019) reported that the main cause of CIP deviation after the GFC was the increase in the cost of dollar funding due to the strengthening of financial regulations on financial institutions. Baba et al. (2008) and Cerutti et al. (2020) argued that during the GFC period and the post-GFC period, the deterioration of the credit risk of trading counterparties in the currency swap market caused global investors to exhibit risk aversion, a major factor in CIP deviation. On the other hand, Bräuning and Puria (2017) and Liao (2019) argued that during the GFC and the post-GFC period, the main cause of CIP deviation was the increase in demand for USD in the swap market due to different directions of monetary policy between major countries.

3. Data and Estimation Model

The basic estimation model for the empirical analysis of the impact of CIP deviation and domestic and foreign factors on domestic long-term interest rates is based on uncovered interest rate parity, as shown in Equations (3) and (4).

In these equations, ∆R represents the change in the yield of Korean Treasury bonds with 5-year maturity, and ∆S denotes the change in the nominal exchange rate for the Korean won against the U.S. dollar. {εrt} and {εst} are assumed to be uncorrelated white-noise disturbances. Equations (3) and (4) suggest a bidirectional relationship between exchange rate movements and domestic long-term bond yields, attributable to the free movement of international capital in an open financial market environment. Analyzing the bidirectional relationships among these variables through ordinary least squares (OLS) estimation would lead to simultaneous equation bias. Hence, a Vector Autoregression (VAR) model, as depicted in Equation (5), was employed for such analysis.

where the vector xt is [∆Rt, ∆St]’, Ai is the parameter vector representing the relationships between variables over time, c is the vector of constants, and the error term vector is [, ]’.

For the purpose of this study, an extended model was established and estimated by incorporating swap basis reflecting CIP deviation and other variables that can affect long-term interest rates into the above basic model. The variables used in the extended model were adapted from research by Warnock and Warnock (2009).

The empirical analysis period covers from February 2002 to September 2023, considering the availability of data for some variables. Additionally, given the significant changes in global dollar liquidity conditions during the Global Financial Crisis (GFC), the analysis was conducted separately for the pre-GFC period (February 2002 to June 2007) and the post-GFC period (January 2010 to September 2023) for comparison.

In the extended model, composing vector xt contains nine endogenous variables:

Here, Rt is the nominal long-term interest rate in Korea, using the yield of Korean Treasury bonds (5-year maturity) for empirical analysis. Callt represents the monetary policy variable, using the call interest rate. According to the transmission effect theory of monetary policy, the call interest rate has a significant impact on long-term interest rates. However, if factors such as global capital flows and the synchronization of domestic and foreign long-term interest rates have a substantial influence, the effect of the call interest rate on long-term interest rates may become uncertain.

In Equation (6), St represents the exchange rate, using the (nominal) exchange rate for the Korean won against the U.S. dollar. As explained earlier, it is expected that the exchange rate and domestic long-term interest rates will show a significant relationship due to Covered Interest Rate Parity (CIP). However, if CIP deviation is largely adjusted through changes in domestic long-term interest rates and the sensitivity of the exchange rate movements to CIP deviation decreases significantly, the impact of exchange rate movements on domestic long-term interest rates may become uncertain.

RPt is the domestic risk variable, and CDS (credit default swap) premium data for Foreign Exchange Equalization Bonds were used. Foreign investors trade CDS premiums on Foreign Exchange Equalization Bonds as a derivative product to hedge potential losses based on Korea’s credit risk. Therefore, the CDS premium is commonly used as a variable reflecting domestic risk. It is expected that an increase in domestic risk will raise domestic long-term interest rates.

Rf,t is the foreign (nominal) long-term interest rate, using the yield of U.S. Treasury notes (5-year maturity). The expected analysis result is that, similar to existing studies advocating the phenomenon of synchronization between Korean and U.S. long-term interest rates, U.S. long-term rates will have a significant positive impact on Korean long-term rates.

SBt is the swap basis, using data for the swap basis against the U.S. dollar for the Korean won (3-year maturity). As mentioned earlier, the swap basis variable can be used to analyze the impact of arbitrage incentives from CIP deviation on domestic long-term interest rates. According to the hypothesis of this study, a significant portion of CIP deviation is adjusted through changes in domestic long-term interest rates. If the absolute value of the swap basis, which mostly assumes a negative (−) value, increases, the arbitrage incentive for the dollar supplier (foreign investor) increases. An increase (decrease in absolute value) in the swap basis indicates an adjustment from CIP deviation to CIP equilibrium. The adjustment to CIP equilibrium can occur through changes in exchange rates (swap rates) or domestic interest rates. Therefore, the coefficient of the swap basis, according to the hypothesis of this study, is expected to show a negative (−) value for domestic long-term interest rates.

Gt represents fiscal balance. To reflect short-term factors affecting the supply side of long-term government bonds, a fiscal balance variable was added. An increase in the fiscal balance deficit may increase the supply of bonds, raising domestic long-term interest rates. However, the deterioration of the fiscal balance can also undermine confidence in government bonds among global investors, so the impact of the fiscal balance on domestic long-term interest rates will vary depending on the relative size of such factors.

πet is the expected inflation rate, and it was included in the model based on the Fisher equation. As there are insufficient data on expected inflation rates, the Consumer Price Index (CPI) inflation rate calculated by the Bank of Korea was used as the expected inflation rate. Yt is the economic growth rate. Since there are no monthly data on the economic growth rate, the growth rate of the seasonally adjusted Industrial Production Index was used as a proxy variable. The growth rate of the Industrial Production Index is highly correlated with the economic growth rate. The expected impact of πet and Yt on domestic long-term interest rates is positive (+), according to the Fisher equation.

In the extended model, the set of exogenous variables were included. GFC is a dummy variable reflecting the Global Financial Crisis (GFC) period (July 2007 to December 2009), and Covid is a dummy variable reflecting the period of the COVID-19 pandemic (February 2020 to June 2021).

When conducting OLS regression analysis for Equation (6), using non-stationary time series data can lead to spurious results. Therefore, unit root tests were conducted to determine the stationarity of each time series dataset. Table 1 shows the results of the Augmented Dickey–Fuller (ADF) unit root tests. The results indicate that all the variables follow an I(1) process and are not stable.

Table 1.

Unit root test results.

There was a concern that, to ensure the stability of unstable variables, simply differencing variables in OLS or VAR analysis may lead to a loss of dynamic information in time-series variables. Therefore, in this study, I first conducted cointegration analysis to understand the long-term equilibrium relationships between variables. Subsequently, I proceeded with an error-correction model (ECM) based on cointegration, utilizing VEC Granger Causality tests and Impulse Response Function (IRF) analysis to analyze the dynamic effects of CIP deviation and how each variable influences domestic long-term interest rates.

For cointegration testing, Johansen’s cointegration test was employed, as expressed in Equation (7). The vector xt comprises the nine variables included in Equation (6), denoted as xt = [Rt Callt St RPt Rf,t SBt Gt πet Yt]’, and Equation (7) represents the long-term equilibrium relationship.

Vector yt includes constants and exogenous variables. The parameter vector γ signifies the cointegrating vector, and the short-term relationships between variables can be expressed as follows:

Here, ut represents the equilibrium error, which is stationary. Therefore, the system can deviate from long-term equilibrium in the short term.

Table 2 displays the results of the cointegration test for the entire sample period (February 2002 to September 2023). Both the trace test statistic and the maximum eigenvalue test statistic reject the null hypothesis of there being no cointegrating vector at the 5% significance level, indicating the existence of cointegration relationships.

Table 2.

Cointegration test results.

Since cointegration relationships exist, a vector error correction model (VEC) was established:

where vector xt consists of nine variables, i.e., xt = [Rt Callt St RPt Rf,t SBt Gt πet Yt]’, and vector yt comprises exogenous variables, including the dummy variable (GFC) for the global financial crisis and the dummy variable (Covid) for the COVID-19 pandemic periods. Here, ψt represents the error correction term, which is zero in long-term equilibrium. However, when the system deviates from long-term equilibrium, the error correction term is non-zero, and vector xt undergoes a partial adjustment process to return to long-term equilibrium. Therefore, the parameter vector δ signifies the speed of adjustment to long-term equilibrium. Also, c represents the constant term, and vt represents the white-noise disturbance term. The lag length was determined using the Schwarz Information Criterion (SIC), and the ordering of variables in the VEC model was chosen based on Granger causality.

Subsequently, Granger Causality analysis and Impulse Response Function analysis based on the error correction model (ECM) expressed in Equation (9) were conducted. Granger Causality analysis was employed to identify whether the CIP deviation variable exhibited a significant leading relationship concerning the movements of each variable in the VEC model. Due to limitations in directly assessing the direction and magnitude of influence between variables through Granger Causality analysis, Impulse Response Function analysis was additionally conducted. This Impulse Response Function analysis aimed to examine the dynamic movements of domestic long-term interest rates in response to shocks of one standard deviation in each variable within the VEC model over several months.

4. Estimation Results

Table 3, Table 4 and Table 5 present the results of the Vector Error Correction (VEC) Granger Causality analysis. The VEC (Vector Error Correction) Granger causality test was conducted to ascertain whether lags of one independent variable created any other dependent variables within the system. The null hypothesis for this test posits that the independent variables do not cause the dependent variable in terms of Granger causality. The significance level typically used for this test is 5% (p-value: 0.05), indicating that if the p-value is less than 0.05, the null hypothesis can be rejected, suggesting the presence of Granger causality in the equation.

Table 3.

VEC Granger causality Wald Test results: entire sample period.

Table 4.

VEC Granger causality Wald Test results: pre-GFC period.

Table 5.

VEC Granger causality Wald Test results: post-GFC period.

As discussed earlier, the aim of this study is to examine whether adjustments from CIP deviation to CIP equilibrium, i.e., the arbitrage incentive, affect changes in domestic long-term interest rates or follow the path of exchange rate changes. Through the VEC Granger Causality analysis results, we can analyze whether the swap basis variable plays a leading role in changes in domestic long-term interest rates.

As shown in Table 3, the VEC Granger Causality test results for the entire sample period indicate that when domestic long-term interest rates (Rt) are the dependent variable, changes in the swap basis variable (SBt) show a significant Granger causality relationship with changes in domestic long-term interest rates. Additionally, changes in foreign long-term interest rates (Rf,t) and monetary policy variables (Callt) also exhibit significant Granger causality relationships with changes in domestic long-term interest rates. However, when the exchange rate (St) is the dependent variable, changes in the swap basis variable (SBt) do not show a significant Granger causality relationship with exchange rate changes. Instead, monetary policy variables (Callt) and economic growth rate (Yt) changes exhibit significant Granger causality relationships with exchange rate changes. These Granger causality results suggest that changes in the swap basis had a leading role in inducing changes in domestic long-term interest rates.

Table 4 and Table 5 present the results of the VEC Granger Causality analysis for the periods before and after the Global Financial Crisis (GFC). When domestic long-term interest rates (Rt) are the dependent variable, changes in the swap basis (SBt) show a Granger causality relationship with changes in domestic long-term interest rates at the 10% significance level before the GFC and at the 1% significance level after the GFC. Additionally, when domestic long-term interest rates (Rt) are the dependent variable, changes in foreign long-term interest rates (Rf,t) show a significant Granger causality relationship with changes in domestic long-term interest rates at the 1% significance level after the GFC. However, when the exchange rate (St) is the dependent variable, none of the explanatory variables show a significant Granger causality relationship with exchange rate changes, both before and after the GFC. These results suggest that the impact of arbitrage incentives on changes in domestic long-term interest rates was more pronounced after the GFC, particularly for periods characterized by relatively severe CIP deviations.

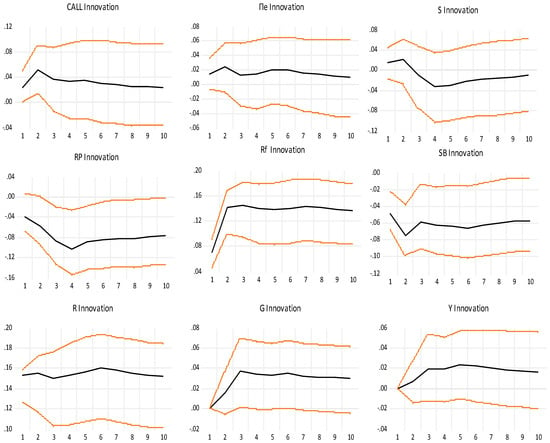

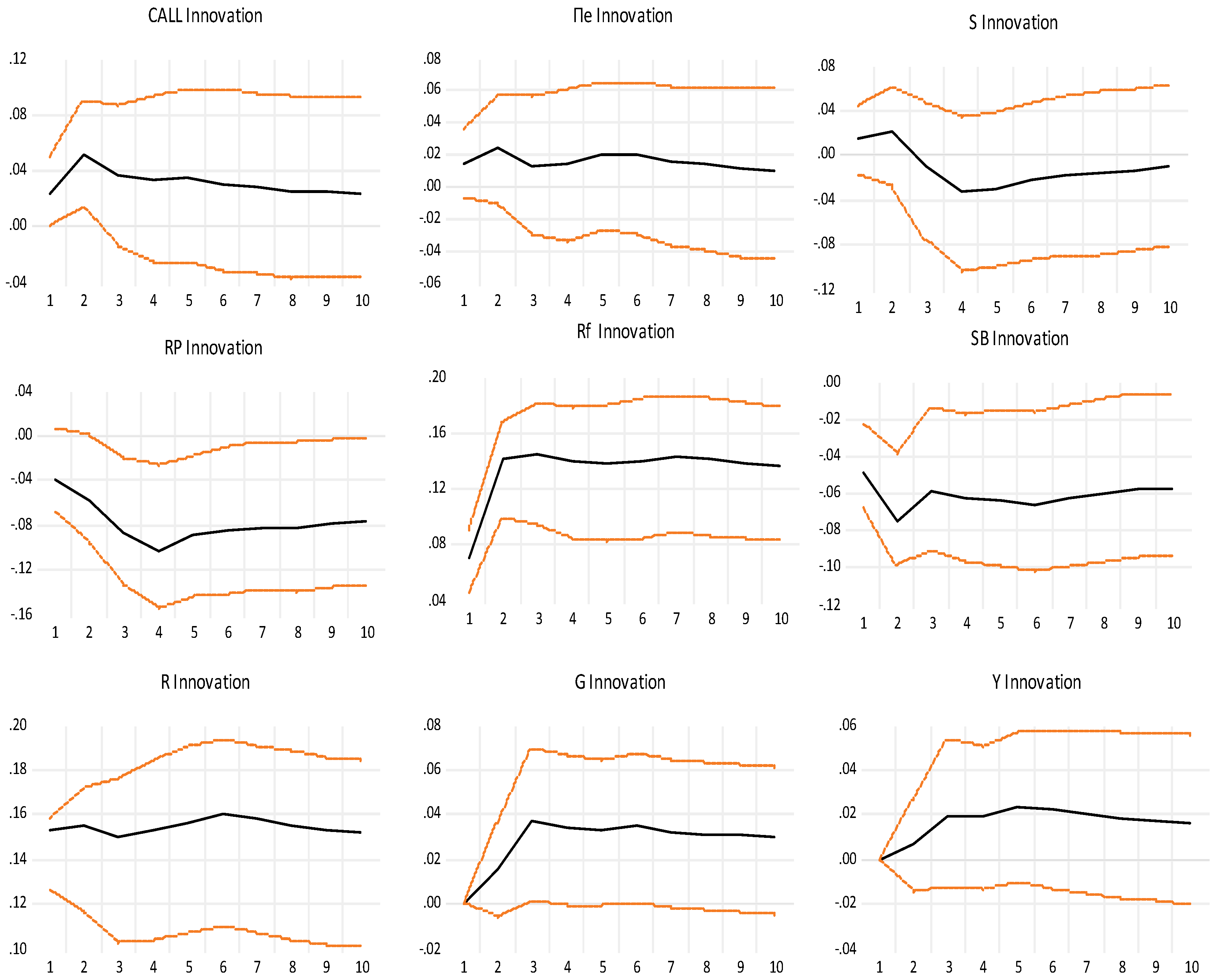

Figure 2 displays the results of the Impulse Response Function (IRF) analysis for the entire sample period. It illustrates how domestic long-term interest rates (Rt) directly respond to shocks in each variable. Domestic long-term interest rates (Rt) exhibit a statistically significant negative (−) response to an upward shock in the swap basis (SBt) over the entire sample period. This result supports the hypothesis that a shock-induced adjustment to CIP equilibrium through an increase in the swap basis leads to changes in domestic interest rates. Moreover, domestic long-term interest rates (Rt) show a significant positive (+) response to an upward shock in foreign long-term interest rates (Rf,t), confirming the phenomenon of the synchronization of Korean and U.S. long-term interest rates. Additionally, domestic long-term interest rates (Rt) display a significant positive (+) response to an upward shock in the monetary policy variable (Callt) over the short term (1–2 months). Furthermore, the domestic long-term government bond yield (Rt) shows a significant negative (−) response to an upward shock in the domestic risk variable (RPt), with a lag of 1–2 months. These results were interpreted as stemming from the increased preference for safe-haven investments in times of financial instability.

Figure 2.

The Impulse Response Function results: entire sample period. Note: The figures in all panels illustrate the response of Korean long-term interest rates (R) to a Cholesky one-standard-deviation shock in each endogenous variable. The red dashed lines represent the 95 percent confidence band, which was derived using standard percentile bootstrap with 999 bootstrap repetitions. The X-axes denote months, with t = 0 indicating the month of a shock.

The Impulse Response Function analysis results confirm that the swap basis (SBt), foreign long-term interest rates (Rf,t), and monetary policy variables (Callt) had statistically significant effects on domestic long-term interest rates (Rt), consistent with the earlier Granger Causality analysis results.

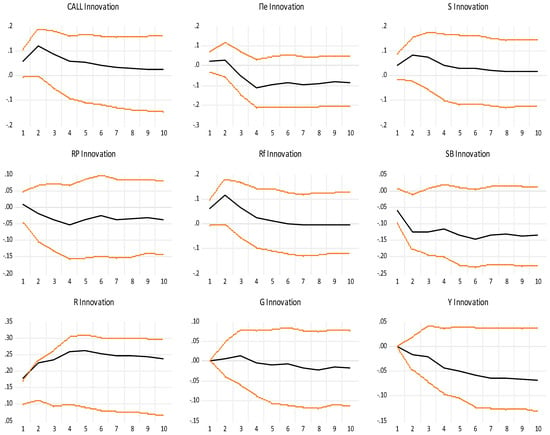

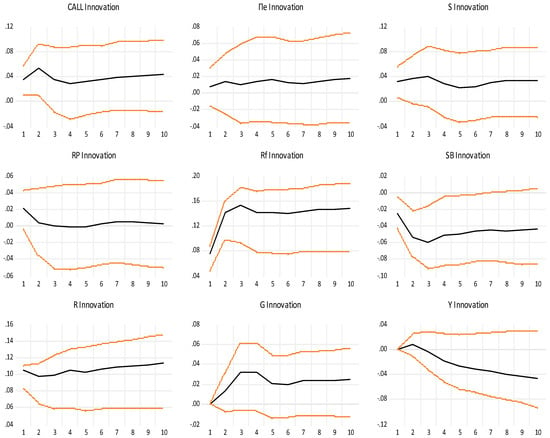

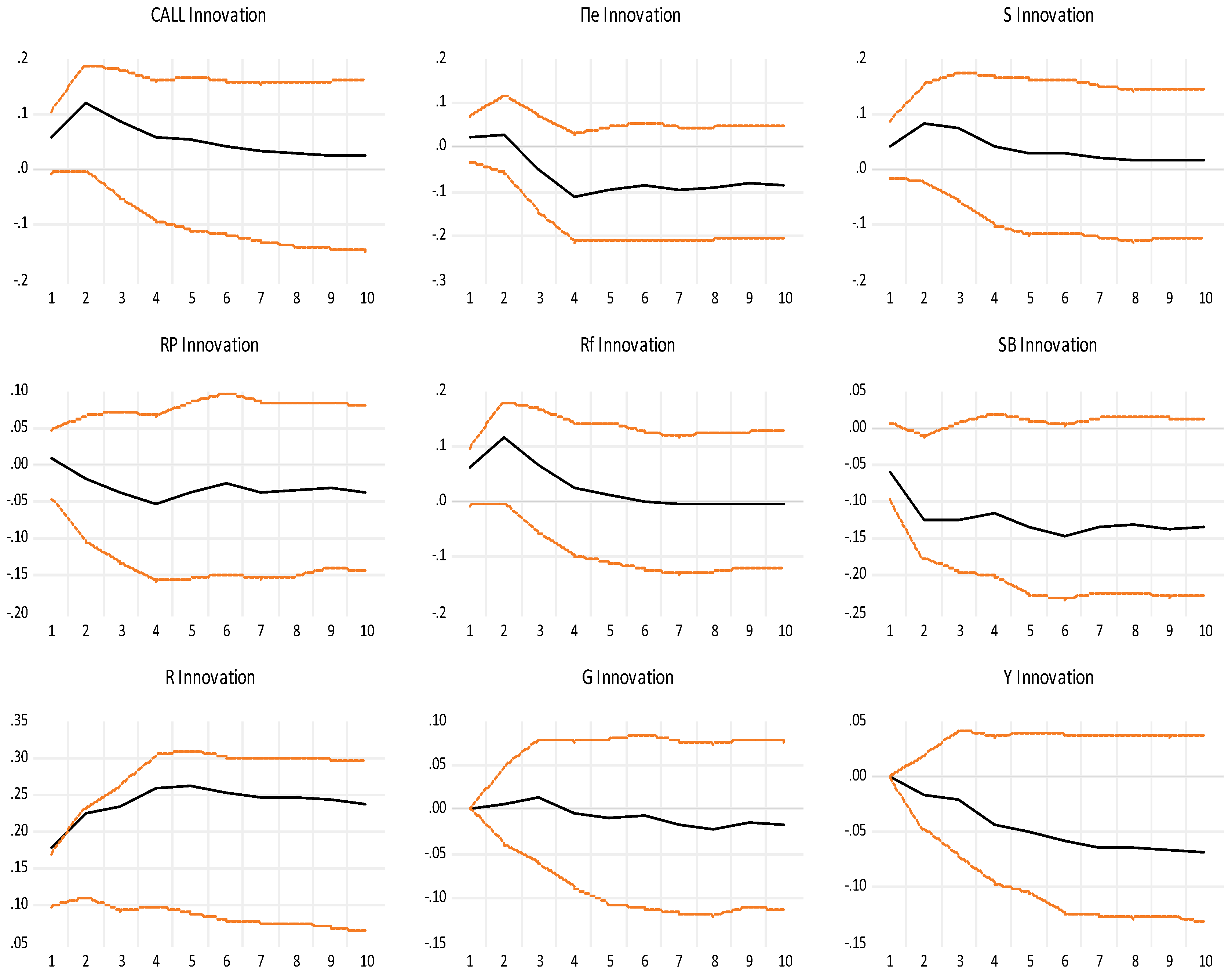

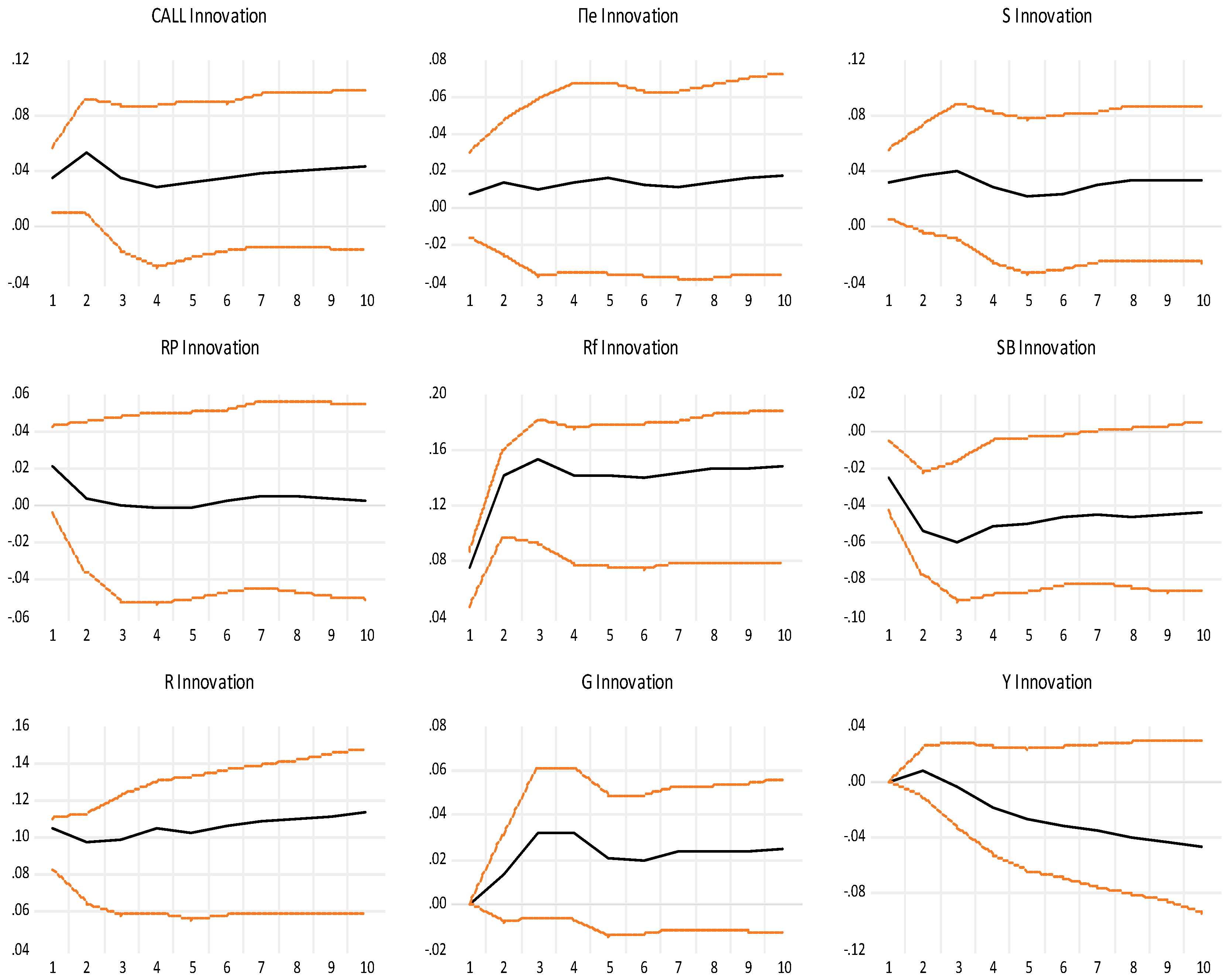

Figure 3 and Figure 4 present the results of the Impulse Response Function analysis for the periods before and after the Global Financial Crisis (GFC). When domestic long-term interest rates (Rt) are the dependent variable, they exhibit a significant short-term negative (−) response to an upward shock in the swap basis (SBt) before the GFC. After the GFC, domestic long-term interest rates (Rt) show an even stronger and more significant short-term negative (−) response to an upward shock in the swap basis (SBt). These results, consistent with the Granger causality results, suggest that the impact of arbitrage incentives on changes in domestic long-term interest rates was more pronounced after the GFC.

Figure 3.

The Impulse Response Function results: pre-GFC period. Note: The figures in all panels illustrate the response of Korean long-term interest rates (R) to a Cholesky one-standard-deviation shock in each endogenous variable. The red dashed lines represent the 95 percent confidence band, which was derived using standard percentile bootstrap with 999 bootstrap repetitions. The X-axes denote months, with t = 0 indicating the month of a shock.

Figure 4.

The Impulse Response Function results: post-GFC period. Note: The figures in all panels illustrate the response of Korean long-term interest rates (R) to a Cholesky one-standard-deviation shock in each endogenous variable. The red dashed lines represent the 95 percent confidence band, which was derived using Standard percentile bootstrap with 999 bootstrap repetitions. The X-axes denote months, with t = 0 indicating the month of a shock.

Additionally, when domestic long-term interest rates (Rt) are the dependent variable, they show a significant positive (+) response to an upward shock in foreign long-term interest rates (Rf,t) after the GFC, while no significant response can be observed before the GFC. Moreover, when domestic long-term interest rates (Rt) are the dependent variable, they exhibit a significant short-term positive (+) response to an upward shock in the monetary policy variable (Callt) only after the GFC.

The Impulse Response Function analysis results for the post-GFC period confirm that the swap basis (SBt), foreign long-term interest rates (Rf,t), and monetary policy variables (Callt) had statistically significant effects on domestic long-term interest rates (Rt), a result that is consistent with the findings for the entire sample period.

To explore whether arbitrage incentives following CIP deviation are adjusted along the path of exchange rate changes, the extent to which the exchange rate (St) directly responds to shocks in each variable was examined. The Impulse Response Function analysis results for the exchange rate show that it does not exhibit a significant response to an upward shock in the swap basis (SBt) over the entire sample period, before the GFC, and after the GFC.1

5. Conclusions

In this study, I analyzed the impact of arbitrage following CIP deviations on Korea’s long-term interest rates, considering concerns about the weakening control over long-term interest rates in emerging market countries due to CIP deviations after the Global Financial Crisis (GFC). This analysis was conducted using Vector Error Correction (VEC)-model-based Granger Causality and Impulse Response Function analyses. The study period spans from February 2002 to September 2023, and a comparative analysis was performed between the periods before and after the GFC.

The results of the Granger Causality analysis indicate that changes in the swap basis reflecting CIP deviations show a significant Granger causality relationship with changes in domestic long-term interest rates. Moreover, during the period after the GFC when CIP deviations were relatively severe, the arbitrage incentive exhibited a stronger leading role in inducing changes in domestic long-term interest rates.

The results of the Impulse Response Function analysis reveal that domestic long-term interest rates exhibit a significant negative (−) response to an upward shock in the swap basis. Furthermore, in the post-GFC period, domestic long-term interest rates showed an even stronger and more significant negative (−) response to an upward shock in the swap basis. Additionally, foreign long-term interest rates and monetary policy variables also have significant effects on domestic long-term interest rates. These findings imply that the adjustment path from CIP deviations through arbitrage is more strongly manifested in changes in domestic interest rates, especially after the GFC, rather than through exchange rate fluctuations.

The findings of this study suggest the importance of considering global factors’ influence on domestic long-term interest rates when making monetary policy decisions in small open economies. The results indicate an expansion of external influences such as international arbitrage and global interest rates on domestic long-term interest rates. These findings reveal concerns regarding the diminished transmission effects between long- and short-term interest rates in the monetary policy of small open economies’ central banks. However, this study’s analysis, focusing on the impact and associated risks of CIP deviation in the Korean context, limits the generalizability of implications for small open economies or emerging market economies. Therefore, future research utilizing data from various emerging market economies to develop more generalized models appears necessary.

Funding

This research received no external funding.

Data Availability Statement

The data used in the study are available on Bank of Korea Database, and Korea Center for International Finance statistics. Data are, however, available from the author upon request.

Conflicts of Interest

The author declares no conflict of interest.

Note

| 1 | Due to spatial constraint in the paper, the Impulse Response Function analysis results for the exchange rate were not shown. |

References

- Akram, Q. Farooq, Dagfinn Rime, and Lucio Sarno. 2008. Arbitrage in the foreign exchange market: Turning on the microscope. Journal of International Economics 6: 237–53. [Google Scholar] [CrossRef]

- Avdjiev, Stefan, Wenxin Du, Catherine Koch, and Hyun Song Shin. 2019. The dollar, bank leverage, and deviations from covered interest parity. American Economic Review: Insights 1: 193–208. [Google Scholar] [CrossRef]

- Baba, Naohiko, Frank Packer, and Teppei Nagano. 2008. The spillover of money market turbulence to FX swap and cross-currency swap markets. BIS Quarterly Review 2008: 73–86. [Google Scholar]

- Backus, David. K., and Jonathan. H. Wright. 2007. Cracking the conundrum. Brookings Papers on Economic Activity 2007: 293–316. [Google Scholar] [CrossRef]

- Beltran, Daniel. O., Maxwell Kretchmer, Jaime Marquez, and Charles. P. Thomas. 2013. Foreign holdings of U.S. treasuries and U.S. treasury yields. Journal of International Money and Finance 32: 1120–43. [Google Scholar] [CrossRef]

- Bernanke, Ben. S. 2017. Federal Reserve policy in an international context. IMF Economic Review 65: 1–32. [Google Scholar] [CrossRef]

- Bonser, Neal Catherine, and Timothy R. Morley. 1997. Does the yield spread predict real economic activity? A multicountry analysis. Economic Review 82: 37–53. [Google Scholar]

- Bräuning, Falk, and Kovid Puria. 2017. Uncovering Covered Interest Parity: The Role of Bank Regulation and Monetary Policy. Federal Reserve Bank of Boston Research Paper Series Current Policy Perspectives Paper No. 17-3. Boston: Federal Reserve Bank of Boston. [Google Scholar]

- Bruno, Valentina, and Hyun Song Shin. 2012. Capital Flows and the Risk-Taking Channel of Monetary Policy. BIS Working Paper No. 400. Basel: Bank for International Settlements. [Google Scholar]

- Cerutti, Eugenio, Maurice Obstfeld, and Haonan Zhou. 2020. Covered Interest Parity Deviations: Macro-financial Determinants. CEPR Discussion Papers. Paper No. 13886. Paris and London: CEPR Press. [Google Scholar]

- Clostermann, Jörg, and Franz Seitz. 2005. Are Bond Markets Really Overpriced: The Case of the US. Working Paper No. 11. Ingolstadt: University of Applied Sciences Ingolstadt. [Google Scholar]

- Cochrane, John H. 2007. Commentary on macroeconomic implications of changes in the term premium. Economic Review 89: 271–82. [Google Scholar]

- Du, Wenxin, Alexander Tepper, and Adrien Verdelhan. 2018. Deviations from covered interest rate parity. The Journal of Finance 73: 915–57. [Google Scholar] [CrossRef]

- Du, Wenxin, Benjamin Hebert, and Amy Wang Huber. 2019. Are Intermediary Constraints Priced? NBER Working Paper No. 26009. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Estrella, Arturo, Anthony P. Rodrigues, and Sebastian Schich. 2003. How stable is the predictive power of the yield curve? Evidence from Germany and the United States. Review of Economics and Statistics 85: 629–44. [Google Scholar] [CrossRef]

- Frenkel, Jacob A., and Richard Levich. 1975. Covered interest arbitrage: Unexploited profits? Journal of Political Economy 83: 325–38. [Google Scholar] [CrossRef]

- Frenkel, Jacob A., and Richard Levich. 1977. Transaction costs and interest arbitrage: Tranquil versus turbulent periods. Journal of Political Economy 85: 1209–26. [Google Scholar] [CrossRef]

- Graeve, Ferre De, Marina Emiris, and Raf Wouters. 2009. A Structural decomposition of US yield curve. Journal of Monetary Economics 56: 545–59. [Google Scholar] [CrossRef]

- Hong, Gee Hee, Anne Oeking, Kenneth H. Kang, and Changyong Rhee. 2021. What do deviations from covered interest parity and higher FX hedging costs mean for Asia? Open Economies Review 32: 361–94. [Google Scholar] [CrossRef]

- Hunt, Chris. 2008. Financial turmoil and global imbalances: The end of Bretton Woods II? Reserve Bank of New Zealand Bulletin 71: 45–55. [Google Scholar]

- Iida, Tomoyuki, Takeshi Kimura, and Nao Sudo. 2018. Deviations from covered interest rate parity. International Journal of Central Banking 14: 275–325. [Google Scholar]

- Korea Financial Supervisory Service. 2023. Foreign Investors’ Security Trading Trends. Available online: https://www.fss.or.kr/fss/bbs/B0000107/view.do?nttId=131858&menuNo=200135 (accessed on 30 December 2023). (In Korean).

- Kozicki, Sharon, and Gordon Sellon. 2005. Longer-term perspectives on the yield curve and monetary policy. Economic Review 99: 5–33. [Google Scholar]

- Liao, Gordon. 2019. Credit Migration and Covered Interest Rate Parity; Board of Governors of the Federal Reserve System International Finance Discussion Papers. Paper No. D2019-152. Washington: Federal Reserve Board.

- McCormick, Frank. 1979. Covered interest arbitrage: Unexploited profits? Comment. Journal of Political Economy 87: 411–17. [Google Scholar] [CrossRef]

- Obstfeld, Maurice. 2015. Trilemmas and Tradeoffs: Living with Financial Globalization. BIS Working Paper No. 480. Basel: Bank for International Settlements. [Google Scholar]

- Rey, Hélène. 2016. International channels of transmission of monetary policy and the Mundellian trilemma. IMF Economic Review 64: 6–35. [Google Scholar] [CrossRef]

- Sushko, Vladyslav, Claudio E.V. Borio, Robert N. McCauley, Robert N. McCauley, and Patrick M. McGuire. 2016. The Failure of Covered Interest Parity: FX Hedging Demand and Costly Balance Sheets. BIS Working Paper No. 590. Basel: Bank for International Settlements. [Google Scholar]

- Turner, Philip. 2014. The Global Long-Term Interest Rate, Financial Risks and Policy Options in EMEs. BIS Working Paper No. 441. Basel: Bank for International Settlements. [Google Scholar]

- Warnock, Francis E., and Veronica Cacdac Warnock. 2009. International capital flows and U.S. interest rates. Journal of International Money and Finance 28: 903–19. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).