Impacts of the Transition to the Expected Loss Model on the Portuguese Banking Sector

Abstract

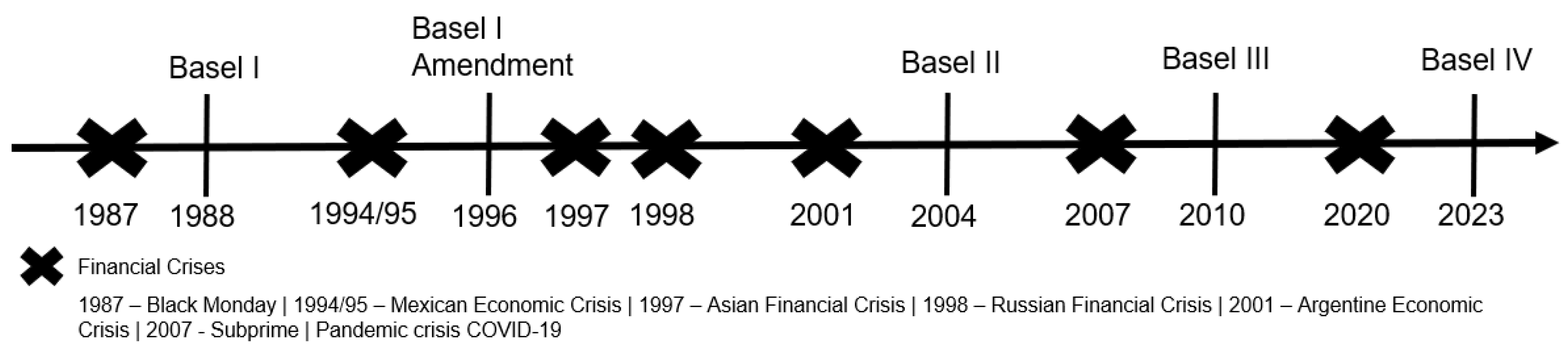

1. Introduction

2. Literature Review

2.1. Normative and Regulatory Frameworks

2.2. Studies on the Impact of Adopting the IFRS 9 ECL Model in Financial Institutions

3. Methodology

3.1. Analysis Model and Variables

3.2. Sample and Data

4. Results and Discussion

4.1. Descriptive Statistics and Normality Tests

4.2. Analysis and Discussion of Results

5. Conclusions, Limitations, and Future Studies

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

| 1 | In the specialized literature on the subject, it is common to encounter the terms Loan Loss Provisions (LLPs) and Loan Loss Allowances (LLAs) to designate credit impairment losses. For the sake of uniformity in the terminology used in studies, this research will use the abbreviation LLP to express credit impairment losses recognized in the period, and LLA for the accumulated credit impairment losses, following the approach of Salazar et al. (2023). |

References

- Arias, José, Maquieira Carlos, and Jara Mauricio. 2020. Do legal and institutional environments matter for banking system performance? Economic Research 33: 2203–28. [Google Scholar] [CrossRef]

- Augusto, Francisco, and Sónia Félix. 2014. O Impacto da Recapitalização Bancária no Acesso ao Crédito por Empresas não Financeiras. Lisbon: Banco de Portugal. Available online: https://www.bportugal.pt/paper/o-impacto-da-recapitalizacao-bancaria-no-acesso-ao-credito-por-empresas-nao-financeiras (accessed on 13 March 2023).

- Banco de Portugal. 2011. Exercício de Stress Test Europeu: Principais Resultados dos Bancos Portugueses. Lisbon: Banco de Portugal. [Google Scholar]

- Basel Committee on Banking Supervision. 2017. Regulatory Treatment of Accounting Provisions—Interim Approach and Transitional Arrangements. Basel: Basel Committee on Banking Supervision. Available online: https://www.bis.org/bcbs/publ/d401.htm (accessed on 20 March 2021).

- Bikker, Jacob A., and Paul A. J. Metzemakers. 2005. Bank provisioning behaviour and procyclicality. Journal of International Financial Markets, Institutions and Money 15: 141–57. [Google Scholar] [CrossRef]

- BIS. 2011. Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems (Revised). Basel: Bank for International Settlements. Available online: https://www.bis.org/publ/bcbs189.htm (accessed on 9 October 2020).

- Bischof, Jannis, and Holger Daske. 2016. Interpreting the European Union’s IFRS endorsement criteria: The case of IFRS 9. Accounting in Europe 13: 129–68. [Google Scholar] [CrossRef]

- Bushman, Robert M., and Christopher D. Williams. 2015. Delayed expected loss recognition and the risk profile of banks. Journal of Accounting Research 53: 511–53. [Google Scholar] [CrossRef]

- Costa, Carlos Silva. 2016. Desafios Para o Sistema Financeiro e Competitividade da Economia. Lisbon: Banco de Portugal. [Google Scholar]

- Dantas, Jose Alves, Matheus Assis Micheletto, Fernando Augusto Cardoso, and Antonio Augusto Pinho Franca de Sa Freire. 2017. Credit losses in Brazilian banks: Expected losses and incurred models and impact of IFRS 9. Revista de Gestão, Finanças e Contabilidade 1: 5–24. Available online: https://www.revistas.uneb.br/index.php/financ/article/view/3110 (accessed on 20 March 2021).

- EBA. 2016. Report on Results from the EBA Impact Assessment of IFRS 9. Paris: European Banking Authority. Available online: https://eba.europa.eu/documents/10180/1360107/EBA+Report+on+impact+assessment+of+IFRS9 (accessed on 20 March 2021).

- EBA. 2018. First Observations on the Impact and Implementation of IFRS 9 by EU Institutions. Paris: European Banking Authority. [Google Scholar]

- ESRB. 2017. Financial Stability Implications of IFRS. Germany: European Systemic Risk Board. Available online: https://www.esrb.europa.eu/pub/pdf/reports/20170717_fin_stab_imp_IFRS_9.en.pdf (accessed on 20 March 2021).

- European Commission. 2021. Report on the Proposal for a Regulation of the European Parliament and of the Council Amending Regulation (EU) No 575/2013 as Regards Requirements for Credit Risk, Credit Valuation Adjustment Risk, Operational Risk, Market Risk and the Output Floor. Belgium: European Commission. Available online: https://www.europarl.europa.eu/doceo/document/A-9-2023-0030_EN.html (accessed on 20 March 2021).

- European Union. 2017. Regulation (EU) 2017/2395 of the European Parliament and of the Council of 12 December 2017. Belgium: European Union. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32017R2395 (accessed on 20 March 2021).

- EY. 2018. IFRS 9 Expected Credit Loss. London: Ernst & Young. Available online: https://www.ey.com/Publication/vwLUAssets/ey-ifrs-9-expected-credit-loss/$File/ey-ifrs-9-expected-credit-loss.pdf (accessed on 1 February 2021).

- Ferreira, Domingos. 2011. Instrumentos Financeiros. Lisbon: Rei dos Livros. [Google Scholar]

- Gebhardt, Günther. 2016. Impairments of Greek government bonds under IAS 39 and IFRS 9: A case study. Accounting in Europe 13: 169–96. [Google Scholar] [CrossRef]

- Gebhardt, Günther, and Zoltan Novotny-Farkas. 2011. Mandatory IFRS adoption and accounting quality of European banks. Journal of Business Finance and Accounting 38: 289–333. [Google Scholar] [CrossRef]

- Giner, Begonã, and Araceli Mora. 2019. Bank loan loss accounting and its contracting effects: The new expected loss models. Accounting and Business Research 49: 726–52. [Google Scholar] [CrossRef]

- Gomaa, Mohamed, Kiridaran Kanagaretnam, Stuart Mestelman, and Mohamed Shehata. 2019. Testing the efficacy of replacing the incurred credit loss model with the expected credit loss model. European Accounting Review 28: 309–34. [Google Scholar] [CrossRef]

- Groff, Maja Zaman, and Barbara Mörec. 2021. IFRS 9 transition effect on equity in a post bank recovery environment: The case of Slovenia. Economic Research-Ekonomska Istrazivanja 34: 670–86. [Google Scholar] [CrossRef]

- IASB. 2020. IFRS 9 and COVID-19. Available online: https://cdn.ifrs.org/-/media/feature/supporting-implementation/ifrs-9/ifrs-9-ecl-and-coronavirus.pdf?la=en (accessed on 24 September 2021).

- Khan, Eazaz, and Vanya Damyanova. 2018. European Bank’s Capital Survives New IFRS 9 Accounting Impact, but Concerns Remain. New York: S&P Global Market Intelligence. Available online: https://www.spglobal.com/marketintelligence/en/news-insights/research/european-banks-capital-survives-new-ifrs-9-accounting-impact-but-concerns-remain (accessed on 16 February 2021).

- KPMG. 2016. IFRS 9 Instrumentos Financeiros: Novas Regras Sobre a Classificação e Mensuração de Ativos Financeiros, Incluindo a redução No Valor recuperável. Available online: https://assets.kpmg/content/dam/kpmg/pdf/2016/04/ifrs-em-destaque-01-16.pdf (accessed on 14 May 2022).

- Laureano, Raul M. S. 2020. Testes de hipóteses e regressão: O meu manual de consulta rápida. Lisbon: Edições Sílabo. [Google Scholar]

- Löw, Edgar, Lisa Emma Schmidt, and Lars Franz Thiel. 2019. Accounting for Financial Instruments under IFRS 9: First-Time Application Effects on European Banks’ Balance Sheets. Working Paper Series 2019—N.º 48; Frankfurt am Main: European Banking Institute. Available online: https://ssrn.com/abstract=3622311 (accessed on 16 April 2021).

- Marton, Jan, and Emmeli Runesson. 2017. The predictive ability of loan loss provisions in banks: Effects of accounting standards, enforcement and incentives. British Accounting Review 49: 162–80. [Google Scholar] [CrossRef]

- Novotny-Farkas, Zoltán. 2016. The interaction of the IFRS 9 expected loss approach with supervisory rules and implications for financial stability. Accounting in Europe 13: 197–227. [Google Scholar] [CrossRef]

- Nuss, Jonathan, and Osman Sattar. 2014. Balloning loss reserves could deflate bank capital. Financial Reporting 20: 20–21. [Google Scholar]

- Pucci, Richard. 2017. Accounting for Financial Instruments in an Uncertain World: Controversies in IFRS in the Aftermath of the 2008 Financial Crisis. Doctoral thesis, Copenhagen Business School, Frederiksberg, Denmark. Available online: https://research.cbs.dk/en/publications/accounting-for-financial-instruments-in-an-uncertain-world-contro (accessed on 14 September 2023).

- Resende, Miguel, Carla Carvalho, and Cecília Carmo. 2024. Impacts of the Expected Credit Loss Model on Pro-Cyclicality, Earnings Management, and Equity Management in the Portuguese Banking Sector. Journal of Risk and Financial Management 17: 112. [Google Scholar] [CrossRef]

- Salazar, Yadira, Paloma Merello, and Ana Zorio-Grima. 2023. IFRS 9, banking risk and COVID-19: Evidence from Europe. Finance Research Letters 56: 104130. [Google Scholar] [CrossRef]

- Silva, Eduardo Sá. 2017. IFRS 9—Instrumentos Financeiros—Introdução às Regras de Reconhecimento e Mensuração. Porto: Vida Económica. [Google Scholar]

{kind=link}

| Objectives: To analyze the impact of adopting the ECL model as anticipated in IFRS 9 on the level of LLAs in loans, on own equity, and the CET1 ratio of Portuguese banks. | ||

| Hypothesis H1 | Hypothesis H2 | Hypothesis H3 |

| : LLA as of 31 December 2017 (data collected through the consolidated reports and accounts of the year 2017). : gross value of customer loans as of 31 December 2017 (data collected through the consolidated reports and accounts of the year 2017). : LLP derived from the adoption of the ECL model as anticipated in IFRS 9 (data collected through the consolidated reports and accounts of the year 2018). : own equity of Portuguese banks as of 31 December 2017 (data collected through the consolidated reports and accounts of the year 2017). : Total Own Funds (TOF) is a calculation performed in accordance with the rules defined in the Basel III agreement, considering capital elements such as shares, retained earnings, among other capital elements (data collected through the consolidated reports and accounts of the year 2017). : Risk-Weighted Assets (RWA), calculated according to the rules defined by the Basel III agreement, weighted by the credit, market, and operational risk of each bank (data collected through the consolidated reports and accounts of the year 2017). | ||

| Approach adapted from studies like Dantas et al. (2017) and Groff and Mörec (2021). | ||

| Testing the equality of two population distributions. For variables that have a normal distribution, the t-test is used; for variables that do not follow a normal distribution, the non-parametric option—the Wilcoxon test—is used (Laureano 2020). | ||

| Banks/ (in Thousands of Euros) | Total Assets 31 December 2017 | % * | % ** | % *** | ||||

|---|---|---|---|---|---|---|---|---|

| CGD | 93,247,914 | 26.78% | 8,274,316 | 25.84% | 59,810,942 | 4,555,961 | 101,606 | 1.23% |

| BCP | 71,939,450 | 20.66% | 7,179,736 | 22.42% | 50,955,423 | 3,321,931 | 241,414 | 3.36% |

| Santander | 53,168,990 | 15.27% | 4,032,232 | 12.59% | 41,387,044 | 1,740,865 | 28,142 | 0.70% |

| Novo Banco | 52,054,849 | 14.95% | 4,832,174 | 15.09% | 31,422,441 | 5,631,498 | 258,955 | 5.36% |

| BPI | 29,640,209 | 8.51% | 2,823,586 | 8.82% | 22,243,689 | 584,907 | 34,611 | 1.23% |

| Montepio | 20,200,024 | 5.80% | 1,762,921 | 5.50% | 14,063,139 | 1,033,821 | 145,403 | 8.25% |

| GCA | 17,988,440 | 5.17% | 1,449,365 | 4.53% | 9,373,039 | 652,085 | 19,393 | 1.34% |

| Haitong | 3,275,905 | 0.94% | 533,766 | 1.67% | 750,124 | 120,217 | 633 | 0.12% |

| Finantia | 1,988,472 | 0.57% | 454,951 | 1.42% | 238,118 | 8238 | 531 | 0.12% |

| BIG | 1,851,222 | 0.53% | 339,534 | 1.06% | 309,342 | 248 | −98 | −0.03% |

| Credibom | 1,566,169 | 0.45% | 160,275 | 0.50% | 1,467,910 | 35,656 | 10,610 | 6.62% |

| CTT | 720,792 | 0.21% | 76,389 | 0.24% | 79,393 | 118 | 869 | 1.14% |

| Alves Ribeiro | 618,643 | 0.18% | 106,392 | 0.33% | 357,632 | 28,783 | 154 | 0.14% |

| TOTAL | 348,261,079 | 100.00% | 32,025,637 | 100.00% | 232,458,236 | 17,714,328 | 842,223 | 29.57% |

| Type of Impact | Item with the Highest Impact | Bank |

|---|---|---|

| Negative Impact | Customer Loans | BCP |

| Negative Impact | Investments in Credit Institutions | CTT |

| Positive Impact | Customer Loans | BIG |

| Negative Impact | Debt Instruments | Finantia |

| Negative Impact | Customer Loans | Alves Ribeiro |

| Negative Impact | Customer Loans | GCA |

| Negative Impact | Customer Loans | Montepio |

| Negative Impact | Customer Loans | CGD |

| Negative Impact | Customer Loans | Novo Banco |

| Negative Impact | Customer Loans | BPI |

| Negative Impact | Customer Loans | Credibom |

| Negative Impact | Customer Loans | Santander |

| Negative Impact | Investments in Credit Institutions | Haitong |

| Banks/Variables | ||||||

|---|---|---|---|---|---|---|

| BCP | 0.065 | 0.070 | 0.463 | 0.514 | 0.119 | 0.114 |

| CTT | 0.001 | 0.012 | 0.002 | 0.013 | 0.265 | 0.262 |

| BIG | 0.001 | 0.000 | 0.001 | 0.000 | 0.451 | 0.451 |

| Finantia | 0.035 | 0.037 | 0.018 | 0.019 | 0.230 | 0.230 |

| Alves Bandeira | 0.080 | 0.081 | 0.271 | 0.272 | 0.213 | 0.213 |

| GCA | 0.070 | 0.072 | 0.450 | 0.470 | 0.148 | 0.146 |

| Montepio | 0.074 | 0.084 | 0.586 | 0.729 | 0.116 | 0.105 |

| CGD | 0.076 | 0.078 | 0.551 | 0.570 | 0.139 | 0.138 |

| Novo Banco | 0.179 | 0.187 | 1.165 | 1.288 | 0.128 | 0.120 |

| BPI | 0.026 | 0.028 | 0.207 | 0.222 | 0.123 | 0.121 |

| Credibom | 0.024 | 0.032 | 0.222 | 0.309 | 0.099 | 0.089 |

| Santander | 0.042 | 0.043 | 0.432 | 0.442 | 0.142 | 0.140 |

| Haitong | 0.160 | 0.161 | 0.225 | 0.227 | 0.203 | 0.202 |

| Descriptive Statistics | ||||||

| N | 13 | 13 | 13 | 13 | 13 | 13 |

| Minimum | 0.001 | 0.000 | 0.001 | 0.000 | 0.099 | 0.089 |

| Maximum | 0.179 | 0.187 | 1.165 | 1.288 | 0.451 | 0.451 |

| Mean | 0.064 | 0.068 | 0.353 | 0.390 | 0.183 | 0.179 |

| Median | 0.065 | 0.070 | 0.271 | 0.309 | 0.142 | 0.140 |

| Standard Deviation | 0.054 | 0.054 | 0.316 | 0.352 | 0.095 | 0.098 |

| Kolmogorov–Smirnova | Shapiro–Wilk | |||||

|---|---|---|---|---|---|---|

| Statistic | df | Sig. | Estatística | df | Sig. | |

| 0.231 | 13 | 0.057 | 0.879 | 13 | 0.069 | |

| 0.231 | 13 | 0.056 | 0.887 | 13 | 0.089 | |

| 0.154 | 13 | 0.200 * | 0.877 | 13 | 0.064 | |

| 0.151 | 13 | 0.200 * | 0.885 | 13 | 0.085 | |

| 0.258 | 13 | 0.018 | 0.765 | 13 | 0.003 | |

| 0.249 | 13 | 0.027 | 0.786 | 13 | 0.005 | |

| Hypothesis H1 | Hypothesis H2 | Hypothesis H3 | |

|---|---|---|---|

| t-Statistic (parametric) | −3.55 | −2.73 | |

| z-Statistic (non-parametric) | 1.00 | ||

| p-value | 0.002 | 0.009 | <0.001 |

| Student’s t | Ha μ Measure 1 − Measure 2 > 0 | Ha μ Measure 1 − Measure 2 > 0 | |

| Wilcoxon’s W | Ha μ Measure 1 − Measure 2 < 0 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Resende, M.; Carvalho, C.; Carmo, C. Impacts of the Transition to the Expected Loss Model on the Portuguese Banking Sector. J. Risk Financial Manag. 2024, 17, 163. https://doi.org/10.3390/jrfm17040163

Resende M, Carvalho C, Carmo C. Impacts of the Transition to the Expected Loss Model on the Portuguese Banking Sector. Journal of Risk and Financial Management. 2024; 17(4):163. https://doi.org/10.3390/jrfm17040163

Chicago/Turabian StyleResende, Miguel, Carla Carvalho, and Cecília Carmo. 2024. "Impacts of the Transition to the Expected Loss Model on the Portuguese Banking Sector" Journal of Risk and Financial Management 17, no. 4: 163. https://doi.org/10.3390/jrfm17040163

APA StyleResende, M., Carvalho, C., & Carmo, C. (2024). Impacts of the Transition to the Expected Loss Model on the Portuguese Banking Sector. Journal of Risk and Financial Management, 17(4), 163. https://doi.org/10.3390/jrfm17040163