Abstract

This paper reports a new global Mittag-Leffler synchronization criterion with regard to fractional-order hyper-chaotic financial systems by designing the suitable impulsive control and the state feedback controller. The significance of this impulsive synchronization lies in the fact that the backward economic system can synchronize asymptotically with the advanced economic system under effective impulse macroeconomic management means. Matlab’s LMI toolbox is utilized to deduce the feasible solution in a numerical example, which shows the effectiveness of the proposed methods. It is worth mentioning that the LMI-based criterion usually requires the activation function of the system to be Lipschitz, but the activation function in this paper is fixed and truly nonlinear, which cannot be assumed to be Lipschitz continuous. This is another mathematical difficulty overcome in this paper.

Keywords:

Mittag-Leffler stability; Caputo fractional-order derivative; non-Lipschitz continuity; hyper-chaotic financial system; Mittag-Leffler function; impulsive control; synchronization MSC:

34D06; 34A37

1. Introduction

Hyperchaotic financial mathematical models include the information of average profit margin, which simulates the actual complex and changeable financial market better, and has attracted much attention from researchers [1,2,3,4,5]. As has been pointed out in [1,6], an extension of fractality concepts in the investigation of economic systems has been used. In the field of mathematical applications to physics and engineering, numerous researchers have adopted fractional calculus as an effective method to model and simulate various nonlinear systems [1,7,8]. For example, in [1], a fractional-order hyperchaotic financial system was investigated, and the adaptive control scheme for synchronization and chaos suppression of the fractional-order economic systems was proposed. However, impulsive control is not considered in [1]. In fact, impulsive control is always one of the means of macroeconomic management [2,3]. In [2], a synchronization criterion of a chaotic financial system was derived by using an impulsive control method, and differential mean value theorem. The authors in [3] utilized impulse control to stabilize a globally hyperchaotic financial system. However, the results in [2,3] are only applicable to integer order differential equation models, and the effective methods used in [2,3] are not suitable for fractional-order hyperchaotic financial mathematical models. Indeed, fractional-order financial systems always involve Mittag-Leffler stability, which is different from those of [2,3]. Moreover, the Riemann–Liouville fractional-order derivative was studied in [1], and so, in this paper, we consider the Caputo fractional-order derivative. To overcome the above-mentioned mathematical difficulties, we design a suitable controller and utilize impulsive control to achieve drive-response synchronization. The significance of this impulsive synchronization lies in the fact that the backward economic system can synchronize asymptotically with the advanced economic system under the effective impulse macroeconomic management means. Particularly, unlike the first-order derivative of positive integer order, the derivative formula of fractional order to product is an inequality. In the case of one-dimensional variables, the inequality formula was derived by the authors of [9] in 2014. However, as far as we know, the formula of fractional quadratic inequality has not been derived, though this formula of fractional quadratic inequality has been cited by some studies [8]. Therefore, for the sake of mathematical rigor, this paper incidentally offers the proof of this quadratic inequality, by which the LMI-based criterion can be built. For decades, a large number of stability and synchronization theorems of fractional order neural network systems have been given in the literature on fractional order neural networks. However, because the activation functions of neural networks are usually assumed to be Lipschitz continuous and linear in nature, the activations function of chaotic financial systems in this paper are fixed, which cannot be assumed to be Lipschitz continuous, but, in fact, are truly nonlinear and non-Lipschitz continuous. This brings essential difficulties to the research on the synchronization of a fractional financial system in this paper. Indeed, because the activation function is fixed and non-Lipschitz continuous, many theorems and lemmas given in the literature involved in fractional neural networks cannot be directly cited in this paper. Considering that many important indicators and variables in the financial market, such as interest rates, options and stocks, have certain memory, many authors in the literature began to study the stability and synchronization of fractional chaotic financial systems [10,11]. Hence, the authors of this paper consider the synchronization research of fractional hyper-chaotic financial system. Different from the previous literature [10,11], this paper will offer an LMI-based synchronization criterion for the first time, which is convenient for computer MATLAB software to calculate and test quickly.

This article has the following novelties:

- ⋄

- This paper offers an original definition (see Definition 4) of chaotic financial systems’ synchronization, in which the boundedness of the interest rate and the investment demand conforms to financial reality.

- ⋄

- Because the activation function of a chaotic financial system in this paper is non-Lipschitz continuous, many lemmas given in the previous fractional-order neural network literature cannot be applied to this paper. The authors overcome the mathematical difficulties caused by true nonlinearity and obtain the LMI-based synchronization criterion for the first time in hyper-chaotic systems, where the so-called LMI criterion is the criterion with regard to linear matrix inequality [12,13,14].

- ⋄

- Because the LMI-based synchronization criterion of fractional-order chaotic financial system is obtained in this paper, the mathematical methods in this paper are different from those of the existing literature involved in the synchronization of fractional-order chaotic financial systems (see, e.g., [10]).

2. Preliminaries

Generally speaking, there are three common fractional derivatives, including the Grunwald–Letnikov fractional derivative, Riemann–Liouville fractional derivative, as well as the Caputo fractional derivative.

In this paper, the Caputo fractional derivative is considered.

Definition 1 ([15]).

The fractional integral of order χ for a function is defined by

where and

Definition 2 ([15]).

where stands for the Laplace transform of . In particular, when , one obtains that

The Caputo fractional derivative of order χ for a function (the set of all n-order continuous differentiable functions on ) is defined as

where , n is the first integer greater than χ; that is, , and the Laplace transform of is given as

Definition 3 ([15]).

where and denote the real parts of s.

The one-parameter and the two-parameter Mittag-Leffler functions are defined as

respectively, and the Laplace transform of the two-parameter Mittag-Leffler function is

As mentioned in the introduction, many important elements of the financial market have memory factors [10,11]; we may consider the following fractional-order hyper-chaotic financial system as the drive system:

which can be written in compact form

where ,

and the initial value is of

where a represents savings, b represents the unit investment cost, and c represents the elasticity of commodity demand. d and k are nonlinear and linear feedback coefficients, respectively. x represents the interest rate, y represents the investment demand, z represents the price index, and u represents the average profit margin.

Consider the corresponding response system as follows,

where and each is a controller to be designed. , and each represents a fixed impulsive instant, and , , for all . Here,

Design the following state feedback controller

where M is a real-time state feedback gain matrix.

In our study, the following assumption conditions are useful:

- (H1)

- , and , for all .

- (H2)

- , where , and L is a constant matrix.

Since the resources of human society and the economic market are limited, the interest rate and the investment demand are actually limited, too. Specifically, the authors of [16] proved the boundedness of the dynamics of a chaotic financial system by using a Laplacian semigroup. Thereby, the boundedness assumption (H1) is reasonable. In numerical examples, we can determine the values of and through numerical simulation and the trial and error method.

Definition 4.

System (5) is said to achieve global Mittag-Leffler synchronization with System (2) if there exist two positive constants such that for any initial values and with and , the null solution of System (6) is global Mittag-Leffler stable.

The following Lemma about Caputo fractional-order derivative with a one-dimensional variable is common in many studies [1,7,17,18,19].

Lemma 1.

Let be a continuous and derivable function. Then, for any

3. Main Results

In this section, we present the LMI-based synchronization criterion for chaotic financial systems:

Theorem 1.

Assume that conditions (H1)–(H2) hold. If there exists a positive definite symmetric matrix P and positive real number such that

then System (5) achieves global Mittag-Leffler synchronization with System (2), where I is the identity matrix, and

Proof.

where

First, it follows from (H1) and (3) that

Consider the Lyapunov function as follows,

where P is a positive definite symmetric matrix. Below, in order to derive a common result on Caputo fractional derive and quadratic forms, we might temporarily assume that P is a positive definite symmetric matrix with n-dimensions, and e is a vector with n-dimensions.

Then there is a congruent transformation such that

where Q is the n-dimensional matrix with and each is a positive real number for . Here, each is one of the eigenvalues of the matrix P because the n-dimensional symmetric matrix must have n real eigenvalues, and moreover, a n-dimensional positive definite symmetric matrix must have n positive eigenvalues. Therefore, there is the standard orthogonal matrix Q such that the matrix P contracts with .

Hence,

where B is a positive definite symmetric matrix with

Let , then

where

Lemma 1 and yield

then

Obviously, there exists a function , and so there is a function such that

where .

Denote by ∗ the convolution operator, then it follows by taking the Laplace transform and inverse Laplace transform of (12) that

which together with means

In consideration of , the above inequality means that the null solution of System (6) is globally Mittag-Leffler stable. This completes the proof. □

Remark 1.

The LMI-based synchronization criterion of Theorem 1 is different from those of [10], Theorem 1 and [11], Theorem 3.1, which illuminates that the mathematical methods used in this paper are different from those of [10,11]. In fact, the Matlab LMI toolbox can not be applied to [10], Theorem 1 and [11], Theorem 3.1, while our Theorem 1 is suitable for the solvability of the LMI toolbox. Specifically, in order to derive the LMI-based synchronization criterion, some original techniques are applied to derive the fractional-order quadratic inequality formula in the proof of Theorem 1, such as the comprehensive application of the congruent transformation of matrix, fractional-order derivative’s definition, and its properties.

4. Numerical Example

Below, we give a numerical example of the synchronization of fractional-order () financial systems:

Example 1.

Equip Systems (2) and (5) with the data with which System (2.2) is hyper-hyper-chaotic [10,11]. In addition, set

Let then

Using MATLAB LMI toolbox to solve LMI conditions (9) and (10) results in the following feasibility data:

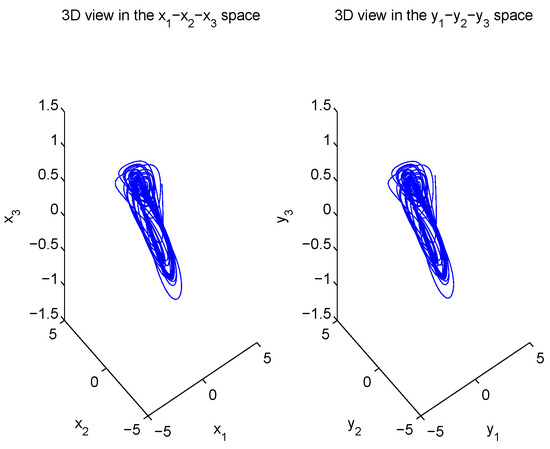

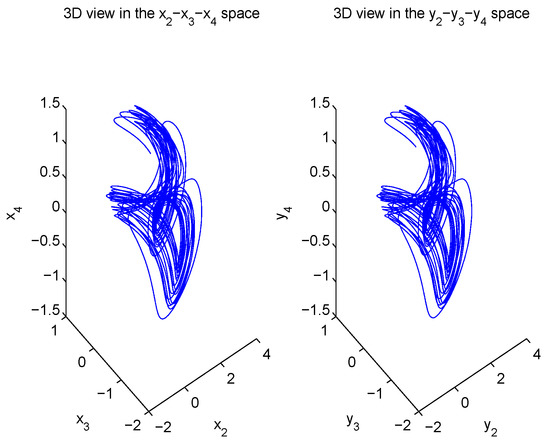

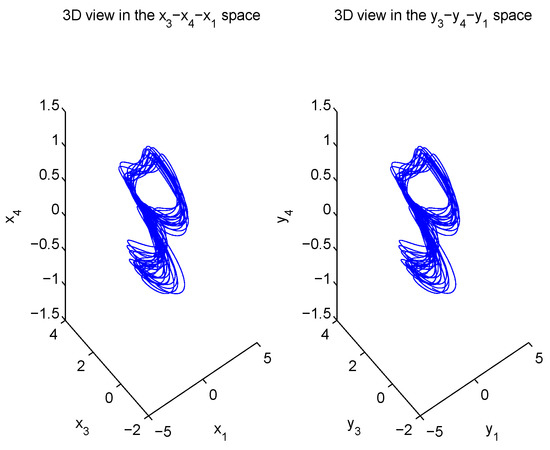

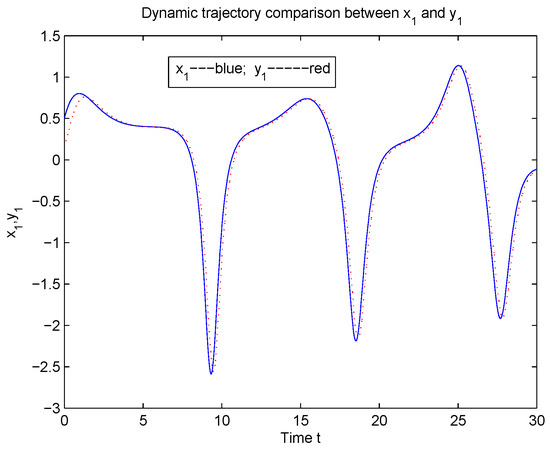

According to Theorem 1, System (5) is global Mittag-Leffler synchronization with System (2) (see Figure 1, Figure 2, Figure 3, Figure 4, Figure 5, Figure 6 and Figure 7).

Figure 1.

Three-dimensional view synchronization for fractional-order .

Figure 2.

Three-dimensional view synchronization for fractional-order .

Figure 3.

Three-dimensional view synchronization for fractional-order .

Figure 4.

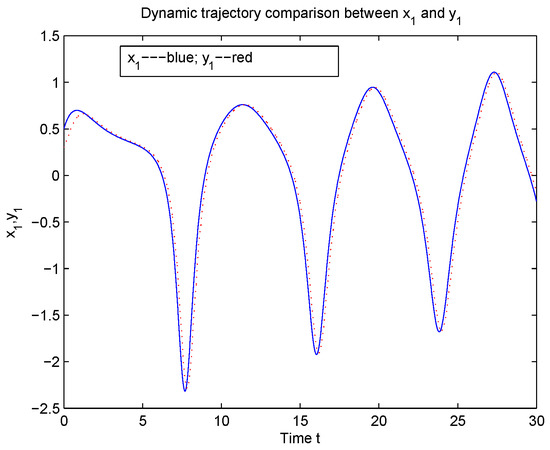

Computer simulations of synchronization between and for fractional-order .

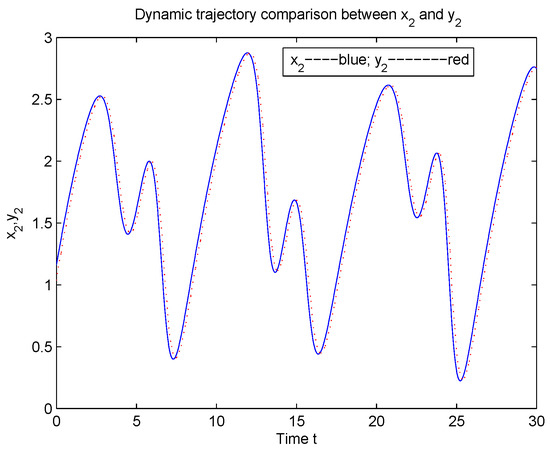

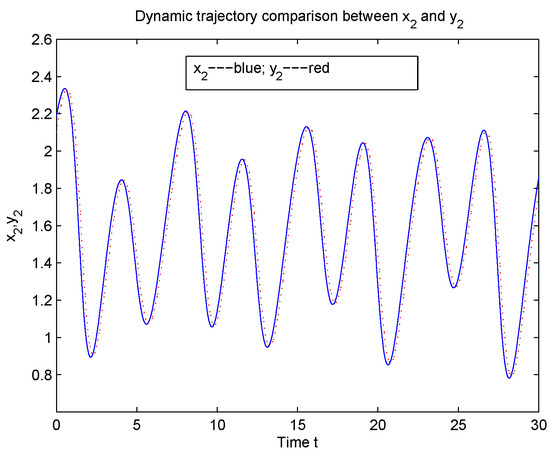

Figure 5.

Computer simulations of synchronization between and for fractional-order .

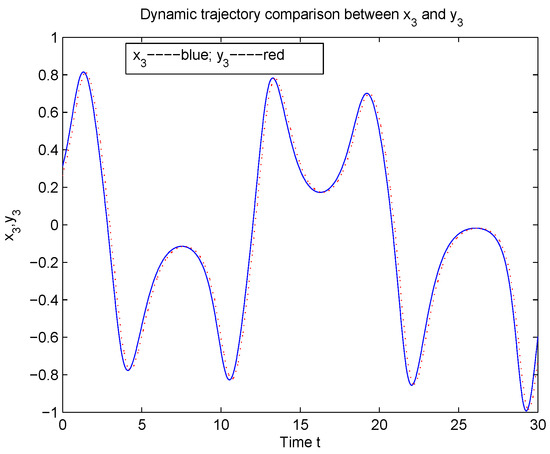

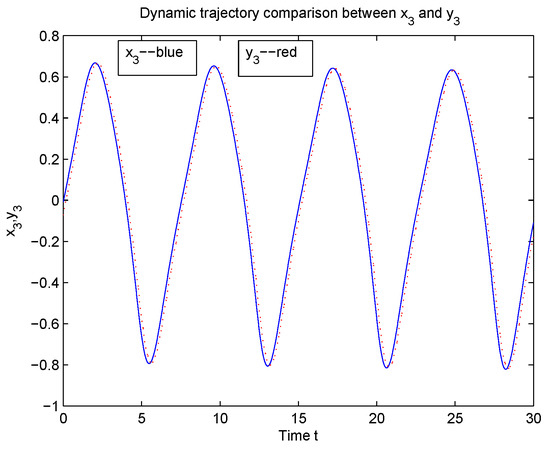

Figure 6.

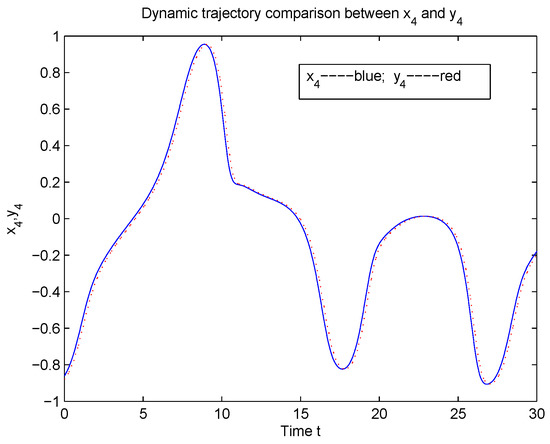

Computer simulations of synchronization between and for fractional-order .

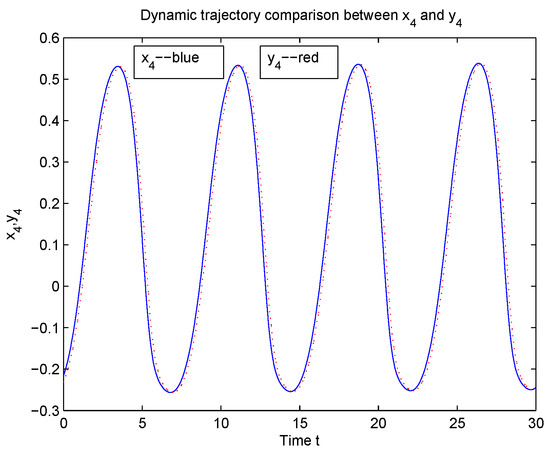

Figure 7.

Computer simulations of synchronization between and for fractional-order .

Remark 2.

Numerical simulation shows the effectiveness of Theorem 1. Indeed, we can see from Figure 1, Figure 2 and Figure 3 that System (5) is in global Mittag-Leffler synchronization with System (2). Moreover, we can also see it from Figure 4, Figure 5, Figure 6 and Figure 7 that and , and . Hence, condition (H1) holds.

Remark 3.

It follows from Figure 4, Figure 5, Figure 6 and Figure 7 that the dual control of input control and pulse control in Theorem 1 makes the synchronization effect better than that of unilateral input control [10].

Finally, we point out that Theorem 1 is also suitable to the case of integer order, for example, integer order

Example 2.

Let then

Using the MATLAB LMI toolbox to solve LMI conditions (9) and (10) results in the following feasibility data:

According to Theorem 1, System (5) is in global Mittag-Leffler synchronization with System (2) (see Figure 8, Figure 9, Figure 10 and Figure 11).

Figure 8.

Computer simulations of synchronization between and for .

Figure 9.

Computer simulations of synchronization between and for .

Figure 10.

Computer simulations of synchronization between and for .

Figure 11.

Computer simulations of synchronization between and for .

Remark 4.

Figure 8, Figure 9, Figure 10 and Figure 11 illustrate that the synchronization speeds of the financial systems in Example 2 are faster than those in Example 1, for the data are different from those of Example 1. In fact, the corresponding data in Example 1 made financial systems chaotic (see [1,3,4,5,10]).

5. Conclusions

Inspired by recent literature related to fractional-order models or chaotic systems [17,18,19,20,21,22], the authors design the suitable impulsive control and the state feedback controller to make fractional-order hyper-chaotic financial systems global Mittag-Leffler synchronized and use the computer Matlab LMI toolbox to verify the effectiveness of the newly-obtained criterion. Both theoretical and numerical examples show that as long as the impulsive macroeconomic management measures are appropriate, the backward economic system can gradually synchronize with the advanced economic system. Theoretical and numerical simulations show that under the dual effects of input control and impulse control; that is, the government’s real-time economic subsidies and support and periodic impulse poverty alleviation, it helps the backward economic system to keep up with the advanced economic system. What is important is that Theorem 1 quantifies the range of economic subsidies and the intensity of impulse poverty alleviation to ensure that the synchronization effect is significant.

Finally, the impulsive control involving time delay and the impulsive control under trigger event mechanisms still need to be studied for the mathematical model of macroeconomics [23,24,25,26]. It is an interesting problem of how to establish a reasonable model in line with the principles of macroeconomics. The interaction of accelerators and multipliers intensifies the cumulative process of production shrinkage. Once the capital equipment of the enterprise is gradually adjusted to the level corresponding to the minimum income, the role of the acceleration principle will stop the negative investment, and a slight improvement in the investment situation will also lead to the re-growth of income, so a new cycle will start again. The re-growth of income leads to a new “induced investment” through the role of acceleration; the latter promotes the further sharp growth of income through the role of multipliers, which launches the cumulative process of economic expansion. This cumulative process will push the national economy to the peak of “full employment” and bounce back from there into recession. Hence, according to the relevant principles of macroeconomics, the existence and stability analysis of periodic solutions of hyperchaotic financial systems is also an interesting problem we will consider in the next step.

Author Contributions

Writing—original draft and revising, X.L.; Participating in discussion of the literature and polishing English, R.R., S.Z., X.Y., H.L. and Y.Z. All authors have read and agreed to the published version of the manuscript.

Funding

This work was jointly supported by the National Natural Science Foundation of China (NSFC) under Grant No. 61673078, Central guiding local science and technology development special project of Sichuan (No. 2021ZYD0015), the Sichuan Province Natural Science Foundation of China (NSFSC) (Nos. 2022NSFSC0541, 2022NSFSC0875).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare that they have no conflict of interest.

References

- Yousefpour, A.; Jahanshahi, H.; Munoz-Pacheco, J.M.; Bekiros, S.; Wei, Z. A fractional-order hyper-chaotic economic system with transient chaos. Chaos Solit. Fractals 2020, 130, 109400. [Google Scholar] [CrossRef]

- Pecora, L.M.; Carroll, T.L. Synchronization in chaotic system. Phys. Rev. Lett. 1990, 64, 821–824. [Google Scholar] [CrossRef] [PubMed]

- Zheng, S. Impulsive stabilization and synchronization of uncertain financial hyperchaotic systems. Kybernetika 2016, 52, 241–257. [Google Scholar] [CrossRef][Green Version]

- Yu, H.; Cai, G.; Li, Y. Dynamic analysis and control of a new hyperchaotic finance system. Nonlinear Dyn. 2012, 67, 2171–2182. [Google Scholar] [CrossRef]

- Stelios, B.; Hadi, J.; Frank, B.; Aly Ayman, A. A novel fuzzy mixed H2/H∞ optimal controller for hyperchaotic financial systems. Chaos Solit. Fractals 2021, 146, 110878. [Google Scholar]

- Laskin, N. Fractional market dynamics. Phys. A 2000, 287, 482–492. [Google Scholar] [CrossRef]

- Li, Y.; Chen, Y.; Podlubny, I. Mittag-Leffler stability of fractional order nonlinear dynamic systems. Automatica 2009, 45, 1965–1969. [Google Scholar] [CrossRef]

- Xu, B.; Li, B. Event-triggered state estimation for fractional-order neural networks. Mathematics 2022, 10, 325. [Google Scholar] [CrossRef]

- Norelys, A.C.; Manuel, A.D.; Javier, A.G. Lyapunov functions for fractional order systems. Comm. Nonlinear Sci. Numer. Simul. 2014, 19, 2951–2957. [Google Scholar]

- Huang, C.; Cai, L.; Cao, J. Linear control for synchronization of a fractional-order time-delayed chaotic financial system. Chaos Solit. Fractals 2018, 113, 326–332. [Google Scholar] [CrossRef]

- Zhang, Z.; Zhang, J.; Cheng, F.; Liu, F.; Ding, C. Stability control of a novel multidimensional fractional-order financial system with time-delay via impulse control. Inter. J. Nonlinear Sci. Numer. Simul. 2021, 22, 1–11. [Google Scholar] [CrossRef]

- Yao, X.; Zhong, S. EID-based robust stabilization for delayed fractional-order nonlinear uncertain system with application in memristive neural networks. Chaos Solit. Fractals 2021, 144, 110705. [Google Scholar] [CrossRef]

- Li, X.D.; Yang, X.; Song, S. Lyapunov conditions for finite-time stability of time-varying time-delay systems. Automatica 2019, 103, 135–140. [Google Scholar] [CrossRef]

- Li, X.D.; Ho, D.W.C.; Cao, J. Finite-time stability and settling-time estimation of nonlinear impulsive systems. Automatica 2019, 99, 361–368. [Google Scholar] [CrossRef]

- Podlubny, I. Fractional Differential Equations; Academic Press: San Diego, CA, USA, 1999. [Google Scholar]

- Rao, R.; Li, X.D. Input-to-state stability in the meaning of switching for delayed feedback switched stochastic financial system. AIMS Math. 2021, 6, 1040–1064. [Google Scholar] [CrossRef]

- Song, Q.; Chen, Y.; Zhao, Z.; Liu, Y.; Alsaadif, F.E. Robust stability of fractional-order quaternion-valued neural networks with neutral delays and parameter uncertainties. Neurocomputing 2021, 420, 70–81. [Google Scholar] [CrossRef]

- Song, Q.; Chen, S.; Zhao, Z.; Liu, Y.; Alsaadif, F.E. Passive filter design for fractional-order quaternion-valued neural networks with neutral delays and external disturbance. Neural Net. 2021, 137, 18–30. [Google Scholar] [CrossRef] [PubMed]

- Li, Y.; Wang, Y.; Li, B. Existence and finite-time stability of a unique almost periodic positive solution for fractional-order Lasota-Wazewska red blood cell models. Int. J. Biomath. 2020, 13, 2050013. [Google Scholar] [CrossRef]

- Liu, X.; Li, K.; Song, Q.; Yang, X. Quasi-projective synchronization of distributed-order recurrent neural networks. Fractal Fract. 2021, 5, 260. [Google Scholar] [CrossRef]

- Yang, X.; Lu, J.; Ho, D.W.C.; Song, Q. Synchronization of uncertain hybrid switching and impulsive complex networks. Appl. Math. Model. 2018, 59, 379–392. [Google Scholar] [CrossRef]

- Fang, Y.; Yan, K.; Li, K. Impulsive synchronization of a class of chaotic systems. Syst. Sci. Control Eng. 2014, 2, 55–60. [Google Scholar] [CrossRef]

- Hu, W.; Zhu, Q. Moment exponential stability of stochastic delay systems with delayed impulse effects at random times and applications in the stabilisation of stochastic neural networks. Inter. J. Control 2020, 93, 2505–2515. [Google Scholar] [CrossRef]

- Li, X.D.; Li, P. Stability of time-delay systems with impulsive control involving stabilizing delays. Automatica 2021, 124, 109336. [Google Scholar] [CrossRef]

- Li, X.D.; Zhang, T.; Wu, J. Input-to-state stability of impulsive systems via event-triggered impulsive control. IEEE Trans. Cybern. 2022, 52, 7187–7195. [Google Scholar] [CrossRef] [PubMed]

- Li, X.D.; Peng, D.; Cao, J. Lyapunov stability for impulsive systems via event-triggered impulsive control. IEEE Trans. Auto. Control 2020, 65, 4908–4913. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).