Hybrid DE-Optimized GPR and NARX/SVR Models for Forecasting Gold Spot Prices: A Case Study of the Global Commodities Market

, , ,

, , ,  and

and

Abstract

:1. Introduction

2. Materials and Methods

2.1. Experimental Dataset

2.2. Time-Series Analysis: Computational Procedures

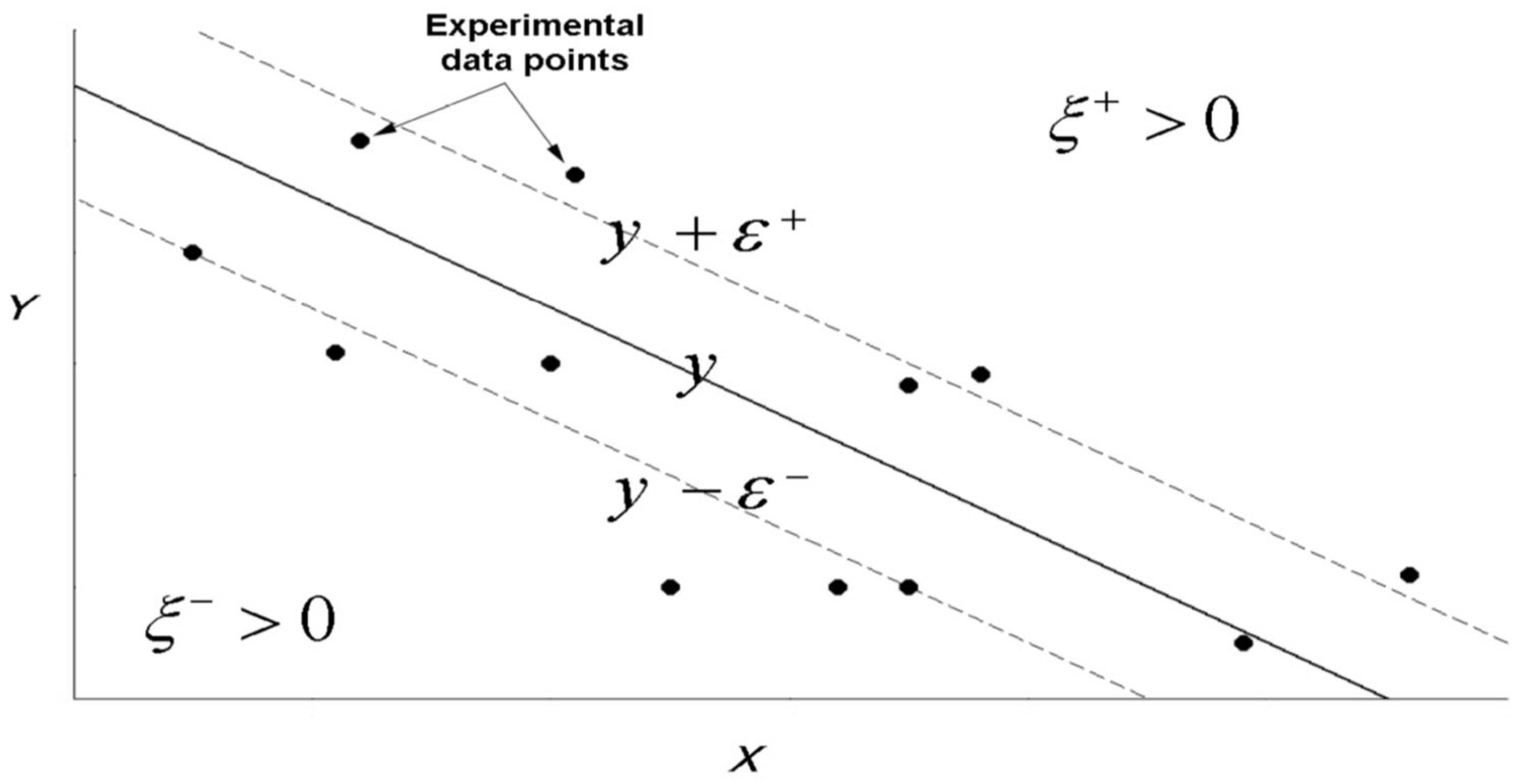

2.2.1. Support Vector Machines Regression (SVR)

2.2.2. Gaussian Process Regression (GPR)

- is the training dataset covariance matrix and is the test dataset covariance.

- is the training and test dataset covariance matrix and .

2.2.3. Differential Evolution (DE) Optimizer

- Initialization;

- Mutation;

- Recombination;

- Selection.

- Initialization

- Mutation

- Recombination

- Selection

2.3. Accuracy of This Approach

2.4. Numerical Schemes

- Direct multi-step;

- Recursive multi-step;

- Direct–recursive hybrid.

- Direct multi-step (DM)

- Recursive multi-step (RM)

- Direct–recursive hybrid (DH)

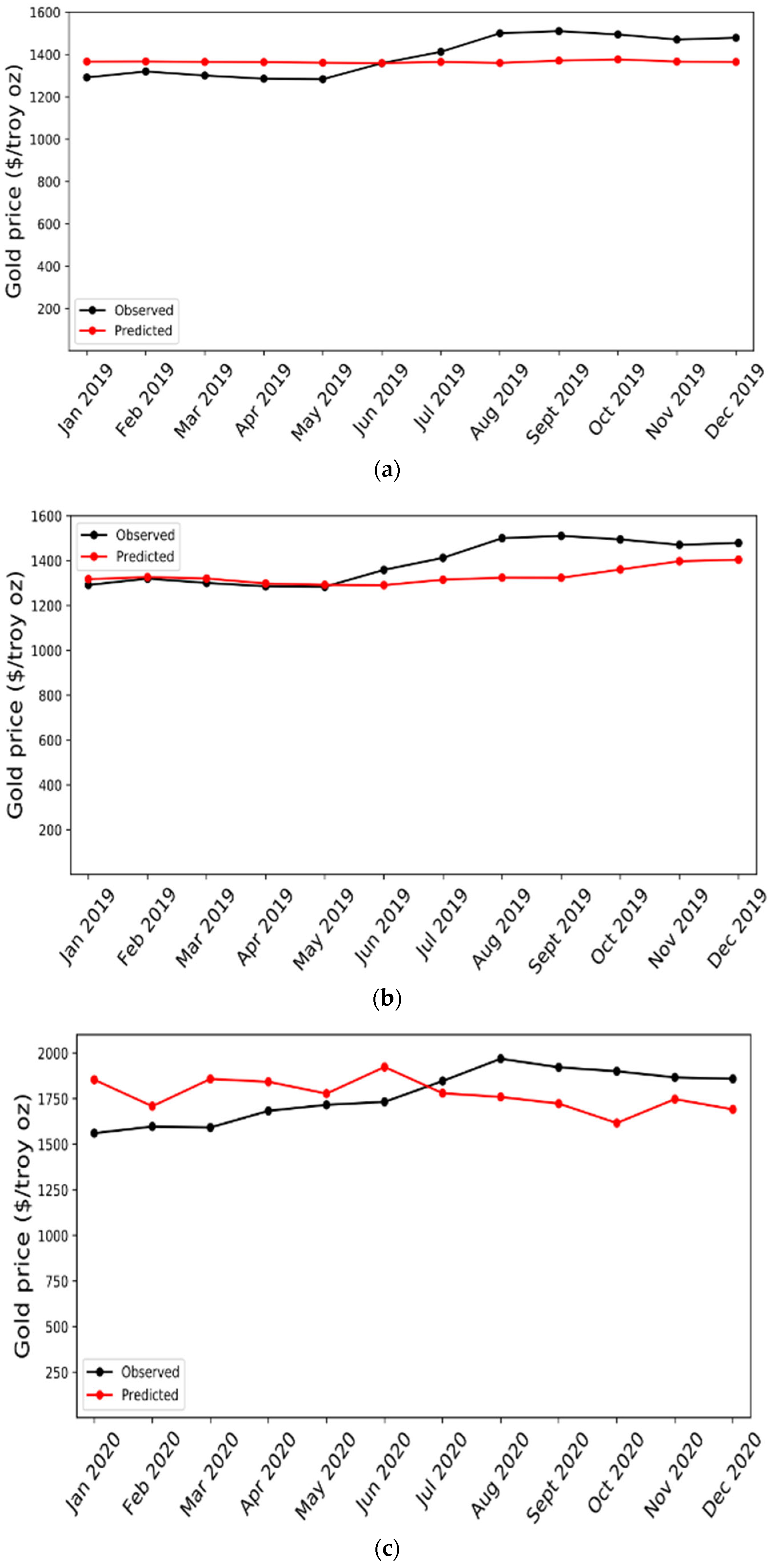

3. Results and Discussion

- For 2020, the year of the pandemic, the MAPEs are the worst. It seems reasonable to attribute this to the atmosphere of unpredictability brought on by the pandemic’s numerous, unprecedented, and unexpected changes.

- The results obtained with only one variable are generally improved by the NARX models, though this is not always the case.

- The best models were obtained by using strategy 1.

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Goodell, J.W.; Huynh, T.L.D. Did Congress trade ahead? Considering the reaction of US industries to COVID-19. Financ. Res. Lett. 2020, 36, 101578. [Google Scholar] [CrossRef]

- Bampinas, G.; Panagiotidis, T. On the relationship between oil and gold before and after financial crisis: Linear, nonlinear and time-varying causality testing. Stud. Nonlinear Dyn. Econom. 2015, 19, 657–668. [Google Scholar] [CrossRef]

- Chaya, J.; Azar, S.A.; Khakhar, P. Financial non-neutrality; A link between income inequality and aggregated debt characteristics in the United-States. Int. J. Soc. Sci. Humanit. Stud. 2021, 13, 29–54. [Google Scholar]

- Haaskjold, H.; Aarseth, W.K.; Røkke, T.A.; Ivarson, M. Spinning the IPD Wheels- Moving towards frictionless project delivery. J. Mod. Proj. Manag. 2021, 9, 70–87. [Google Scholar]

- Rodríguez, A.C.; Aguilar, J.L.; Arbiol, I.A. Relationship between physical physiological and psychological responses in amateur soccer referees. Rev. Psicol. Deporte 2021, 30, 26–37. [Google Scholar]

- Iglesias García, C.; Saiz Matinez, P.; García-Portilla González, M.P.; Bousoño García, M.; Jiménez Treviño, L.; Sánchez Lasheras, F.; Bobes, J. Effects of the economic crisis on demand due to mental disorders in Asturias: Data from the Asturias Cumulative Psychiatric Case Register (2000–2010). Actas Españolas Psiquiatr. 2014, 42, 108–115. [Google Scholar]

- Iglesias-García, C.; Sáiz, P.A.; Burón, P.; Sánchez-Lasheras, F.; Jiménez-Treviño, L.; Fernández-Artamendi, S.; Bobes, J. Suicidio, desempleo y recesión económica en España. Rev. De Psiquiatr. Y Salud Ment. 2017, 10, 70–77. [Google Scholar] [CrossRef]

- Tuan, B.A.; Pho, K.H.; Pan, S.H.; Wong, W.K. Applications in sciences in the prevention of COVID-19. Adv. Decis. Sci. 2022, 26, 1–16. [Google Scholar]

- Hoang, V.T.H.; Wong, W.K.; Zhu, Z.Z. Is gold different for risk-averse and risk seeking investors? An empirical analysis of the Shanghai Gold Exchange. Econ. Model. 2015, 50, 200–211. [Google Scholar] [CrossRef]

- Hoang, V.T.H.; Zhu, Z.Z.; Xiao, B.; Wong, W.K. The seasonality of gold prices in China: Does the risk-aversion level matter? Account. Financ. 2018, 60, 2617–2664. [Google Scholar] [CrossRef]

- Hoang, V.T.H.; Zhu, Z.Z.; Khamlichi, A.E.; Wong, W.K. Does the Shari’ah screening impact the gold-stock nexus? A sectorial analysis. Resour. Policy 2019, 61, 617–626. [Google Scholar] [CrossRef]

- Eryigit, M. Short-term and long-term relationships between gold prices and precious metal (palladium, silver and platinum) and energy (crude oil and gasoline) prices. Econ. Res. Ekon. Istraživanja 2017, 30, 499–510. [Google Scholar] [CrossRef]

- Yaya, O.S.; Vo, X.V.; Olayinka, H.A. Gold and silver prices, their stocks and market fear gauges: Testing fractional cointegration using a robust approach. Resour. Policy 2021, 72, 102045. [Google Scholar] [CrossRef]

- Atri, H.; Kouki, S.; imen Gallali, M. The impact of COVID-19 news, panic and media coverage on the oil and gold prices: An ARDL approach. Resour. Policy 2021, 72, 102061. [Google Scholar] [CrossRef] [PubMed]

- Tanin, T.I.; Sarker, A.; Hammoudeh, S.; Shahbaz, M. Do volatility indices diminish gold’s appeal as a safe haven to investors before and during the COVID-19 pandemic? J. Econ. Behav. Organ. 2021, 191, 214–235. [Google Scholar] [CrossRef] [PubMed]

- Alawi, A.H. Media and intercultural communication shifts: A semiotic analysis of the cultural identity in two international films. Croat. Int. Relat. Rev. 2021, 27, 1–13. [Google Scholar]

- Agyei-Ampomah, S.; Gounopoulos, D.; Mazouz, K. Does gold offer a better protection against losses in sovereign debt bonds than other metals? J. Bank. Financ. 2014, 40, 507–521. [Google Scholar] [CrossRef]

- Balcilar, M.; Gupta, R.; Pierdzioch, C. Does uncertainty move the gold price? New evidence from a nonparametric causality-in-quantiles test. Resour. Policy 2016, 49, 74–80. [Google Scholar] [CrossRef]

- Baur, D.G.; McDermott, T.K. Is gold a safe haven? International evidence. J. Bank. Financ. 2010, 34, 1886–1898. [Google Scholar] [CrossRef]

- Bilgin, M.H.; Gozgor, G.; Lau, C.K.M.; Sheng, X. The effects of uncertainty measures on the price of gold. Int. Rev. Financ. Anal. 2018, 58, 1–7. [Google Scholar] [CrossRef]

- Bouoiyour, J.; Selmi, R.; Wohar, M.E. Measuring the response of gold prices to muncertainty: An analysis beyond the mean. Econ. Model. 2018, 75, 105–116. [Google Scholar] [CrossRef]

- Beckmann, J.; Berger, T.; Czudaj, R. Gold price dynamics and the role of uncertainty. Quant. Financ. 2019, 19, 663–681. [Google Scholar] [CrossRef]

- Maghyereh, A.I.; Abdoh, H. Connectedness between crude oil and US equities: The impact of COVID-19 pandemic. Annu. Rev. Econ. 2022, 17, 2250029. [Google Scholar] [CrossRef]

- Arfaoui, M.; Rejeb, A.B. Oil, gold, US dollar and stock market interdependencies: A global analytical insight. Eur. J. Manag. Bus. Econ. 2017, 26, 278–293. [Google Scholar] [CrossRef]

- Macdonald, E. Handbook of Gold Exploration and Evaluation; Woodhead Publishing: New York, NY, USA, 2007. [Google Scholar]

- Stevens, R. Mineral Exploration and Mining Essentials; Robert Stevens Publishing: London, UK, 2011. [Google Scholar]

- Skonieczny, M. Gold Production from Beginning to End: What Gold Companies Do to Get the Shiny Metal into Our Hands; Investment Publishing: New York, NY, USA, 2015. [Google Scholar]

- U.S. Geological Survey. Gold, Mineral Commodity Summaries. 2018. Available online: https://www.usgs.gov/centers/nmic/gold-statistics-and-information (accessed on 10 March 2024).

- Streifel, S. Impact of China and India on Global Commodity Markets Focus on Metals & Minerals and Petroleum, Report. 2006. Available online: http://www.tos.camcom.it/Portals/_UTC/Studi/ScenariEconomici/39746563551035393/ChinaIndiaCommodityImpact.pdf (accessed on 10 March 2024).

- Cuddington, J.T.; Jerrett, D. Super Cycles in Real Metals Prices? IMF Econ. Rev. 2008, 55, 541–565. [Google Scholar] [CrossRef]

- Roache, S.K. China’s Impact on World Commodity Markets. IMF Working Paper No. 12/115. 2012. Available online: https://ssrn.com/abstract=2127010 (accessed on 10 March 2024).

- Gordon, R.B.; Bertram, M.; Graedel, T.E. Metal stocks and sustainability. Proc. Natl. Acad. Sci. USA 2006, 103, 1209–1214. [Google Scholar] [CrossRef] [PubMed]

- Tilton, J.E.; Lagos, G. Assessing the long-run availability of copper. Resour. Policy 2007, 32, 19–23. [Google Scholar] [CrossRef]

- Li, J.; Wang, R.; Aizhan, D.; Karimzade, M. Assessing the impacts of COVID-19 on stock exchange, gold prices, and financial markets: Fresh evidences from econometric analysis. Resour. Policy 2023, 83, 103617. [Google Scholar] [CrossRef]

- Baur, D.G.; Lucey, B.M. Is Gold a Hedge or a Safe Haven? An Analysis of Stocks, Bonds and Gold. Financ. Rev. 2010, 45, 217–229. [Google Scholar] [CrossRef]

- Corbet, S.; Larkin, C.; Lucey, B. The contagion effects of the COVID-19 pandemic: Evidence from gold and cryptocurrencies. Financ. Res. Lett. 2020, 35, 101554. [Google Scholar] [CrossRef]

- Ji, Q.; Zhang, D.; Zhao, Y. Searching for safe-haven assets during the COVID-19 pandemic. Int. Rev. Financ. Anal. 2020, 71, 101526. [Google Scholar] [CrossRef]

- Dooley, G.; Lenihan, H. An assessment of time series methods in metal price forecasting. Resour. Policy 2005, 30, 208–217. [Google Scholar] [CrossRef]

- Cortazar, G.; Eterovic, F. Can oil prices help estimate commodity futures prices? The cases of copper and silver. Resour. Policy 2010, 35, 283–291. [Google Scholar] [CrossRef]

- Khashei, M.; Bijari, M. An artificial neural network (p,d,q) model for time series forecasting. Expert. Syst. Appl. 2010, 37, 479–489. [Google Scholar] [CrossRef]

- Ma, W.; Zhu, X.; Wang, M. Forecasting iron ore import and consumption of China using grey model optimized by particle swarm optimization algorithm. Resour. Policy 2013, 38, 613–620. [Google Scholar] [CrossRef]

- Kriechbaumer, T.; Angus, A.; Parsons, D.; Rivas Casado, M. An improved wavelet–ARIMA approach for forecasting metal prices. Resour. Policy 2014, 39, 32–41. [Google Scholar] [CrossRef]

- Sánchez Lasheras, F.; de Cos Juez, F.J.; Suárez Sánchez, A.; Krzemień, A.; Riesgo Fernández, P. Forecasting the COMEX copper spot price by means of neural networks and ARIMA models. Resour. Policy 2015, 45, 37–43. [Google Scholar] [CrossRef]

- Storn, R.M.; Price, K. Differential evolution—A simple and efficient heuristic for global optimization over continuous spaces. J. Glob. Optim. 1997, 11, 341–359. [Google Scholar] [CrossRef]

- Brockwell, P.J.; Davis, R.A. Introduction to Time Series and Forecasting; Springer: New York, NY, USA, 2016. [Google Scholar]

- Shumway, R.H.; Stoffer, D.S. Time Series Analysis and Its Applications: With R Examples; Springer: New York, NY, USA, 2017. [Google Scholar]

- Rasmussen, C.E. Gaussian Processes in Machine Learning: Summer School on Machine Learning; Springer: Berlin/Heidelberg, Germany, 2003. [Google Scholar]

- Hastie, T.; Tibshirani, R.; Friedman, J. The Elements of Statistical Learning: Data Mining, Inference, and Prediction; Springer: New York, NY, USA, 2016. [Google Scholar]

- Kuhn, M.; Johnson, K. Applied Predictive Modeling; Springer: New York, NY, USA, 2018. [Google Scholar]

- World Bank Commodity Price Data (The Pink Sheet). Bloomberg, Engineering and Mining Journal; Platts Metals Week; and Thomson Reuters Datastream; World Bank. 2021. Available online: http://pubdocs.worldbank.org/en/561011486076393416/CMO-Historical-Data-Monthly.xlsx (accessed on 10 March 2024).

- Vapnik, V. Statistical Learning Theory; Wiley–Interscience: New York, NY, USA, 1998. [Google Scholar]

- Cristianini, N.; Shawe–Taylor, J. An Introduction to Support Vector Machines and Other Kernel–Based Learning Methods; Cambridge University Press: New York, NY, USA, 2000. [Google Scholar]

- Schölkopf, B.; Smola, A.J.; Williamson, R.C.; Bartlett, P.L. New support vector algorithms. Neural Comput. 2000, 12, 1207–1245. [Google Scholar] [CrossRef]

- Hansen, T.; Wang, C.J. Support vector based battery state of charge estimator. J. Power Sources 2005, 141, 351–358. [Google Scholar] [CrossRef]

- Li, X.; Lord, D.; Zhang, Y.; Xie, Y. Predicting motor vehicle crashes using Support Vector Machine models. Accid. Anal. Prev. 2008, 40, 1611–1618. [Google Scholar] [CrossRef] [PubMed]

- Steinwart, I.; Christmann, A. Support Vector Machines; Springer: New York, NY, USA, 2008. [Google Scholar]

- Hamel, L.H. Knowledge Discovery with Support Vector Machines; Wiley-Interscience: New York, NY, USA, 2011. [Google Scholar]

- Chang, C.-C.; Lin, C.-J. LIBSVM: A library for support vector machines. ACM Trans. Intell. Syst. Technol. 2011, 2, 1–27. [Google Scholar] [CrossRef]

- Price, K.; Storn, R.M.; Lampinen, J.A. Differential Evolution: A Practical Approach to Global Optimization; Springer: Berlin/Heidelberg, Germany, 2005. [Google Scholar]

- Feoktistov, V. Differential Evolution: In Search of Solutions; Springer: New York, NY, USA, 2006. [Google Scholar]

- Rocca, P.; Oliveri, G.; Massa, A. Differential evolution as applied to electromagnetics. IEEE Trans. Antennas Propag. 2011, 53, 38–49. [Google Scholar] [CrossRef]

- Rasmussen, C.E.; Williams, C.K.I. Gaussian Processes for Machine Learning; MIT Press: Cambridge, MA, USA, 2006. [Google Scholar]

- Marsland, S. Machine Learning: An Algorithmic Perspective; Chapman and Hall/CRC Press: Boca Raton, FL, USA, 2014. [Google Scholar]

- Schneider, M.; Ertel, W. Robot learning by demonstration with local Gaussian process regression. In Proceedings of the IEEE/RSJ International Conference on Intelligent Robots and Systems, Taipei, Taiwan, 18–22 October 2010; pp. 255–260. [Google Scholar]

- Shi, J.Q.; Choi, T. Gaussian Process Regression Analysis for Functional Data; Chapman and Hall/CRC Press: Boca Raton, FL, USA, 2011. [Google Scholar]

- GPy: A Gaussian process framework in Python. Available online: http://sheffieldml.github.io/GPy/ (accessed on 23 June 2023).

- Chakraborty, U.K. Advances in Differential Evolution; Springer: Berlin/Heidelberg, Germany, 2008. [Google Scholar]

- Artime Ríos, E.M.; Sánchez Lasheras, F.; Suarez Sánchez, A.; Iglesias-Rodríguez, F.J.; Seguí Crespo, M.M. Prediction of Computer Vision Syndrome in Health Personnel by Means of Genetic Algorithms and Binary Regression Trees. Sensors 2019, 19, 2800. [Google Scholar] [CrossRef] [PubMed]

- Wasserman, L. All of Statistics: A Concise Course in Statistical Inference; Springer: New York, NY, USA, 2003. [Google Scholar]

- Freedman, D.; Pisani, R.; Purves, R. Statistics; WW Norton & Company: New York, NY, USA, 2007. [Google Scholar]

- Casteleiro-Roca, J.L.; Jove, E.; Sánchez-Lasheras, F.; Méndez-Pérez, J.A.; Calvo-Rolle, J.L.; de Cos Juez, F.J. Power Cell SOC Modelling for Intelligent Virtual Sensor Implementation. J. Sens. 2017, 2017, 9640546. [Google Scholar] [CrossRef]

- Krzemień, A.; Riesgo Fernández, P.; Suárez Sánchez, A.; Sánchez Lasheras, F. Forecasting European thermal coal spot prices. J. Sustain. Min. 2015, 14, 203–210. [Google Scholar] [CrossRef]

- Sánchez, A.B.; Ordóñez, C.; Sánchez Lasheras, F.; de Cos Juez, F.J.; Roca-Pardiñas, J. Forecasting SO2Pollution Incidents by means of Elman Artificial Neural Networks and ARIMA Models. Abstr. Appl. Anal. 2013, 2013, 238259. [Google Scholar] [CrossRef]

- Liu, K.; Cheng, J.; Yi, J. Copper price forecasted by hybrid neural network with Bayesian Optimization and wavelet transform. Resour. Policy 2022, 75, 102520. [Google Scholar] [CrossRef]

- Ghosh, I.; Jana, R.K. Clean energy stock price forecasting and response to macroeconomic variables: A novel framework using Facebook’s Prophet, NeuralProphet and explainable AI. Technol. Forecast. Soc. 2024, 200, 123148. [Google Scholar] [CrossRef]

- Suárez Gómez, S.L.; García Riesgo, F.; Pérez Fernández, S.; Iglesias Rodríguez, F.J.; Díez Alonso, E.; Santos Rodríguez, J.D.; De Cos Juez, F.J. Wavefront Recovery for Multiple Sun Regions in Solar SCAO Scenarios with Deep Learning Techniques. Mathematics 2023, 11, 1561. [Google Scholar] [CrossRef]

- Sanchez Lasheras, F.; Ordóñez, C.; Roca-Pardiñas, J.; de Cos Juez, F.J. Real-time tomographic reconstructor based on convolutional neural networks for solar observation. Math. Methods Appl. Sci. 2019, 43, 8032–8041. [Google Scholar] [CrossRef]

- Liu, Z.; Qian, S.; Xia, C.; Wang, C. Are transformer-based models more robust than CNN-based models? Neural Netw. 2024, 172, 106091. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

| Method | DH | RM | DM |

|---|---|---|---|

| DE/SVR | 7.80 | 7.63 | 7.80 |

| DE/GPR | 8.06 | 8.69 | 5.06 |

| NARX DE/SVR | 7.61 | 6.72 | 5.92 |

| NARX DE/GPR | 7.51 | 6.72 | 7.48 |

| Method | DH | RM | DM |

|---|---|---|---|

| DE/SVR | 22.60 | 20.61 | 19.80 |

| DE/GPR | 22.82 | 21.82 | 10.12 |

| NARX DE/SVR | 20.77 | 20.86 | 22.94 |

| NARX DE/GPR | 20.23 | 20.44 | 16.16 |

| Type | Year | Optimal Parameters | |

|---|---|---|---|

| Model 1 | NARX DE/SVR | 2019 | |

| Model 2 | DE/GPR | 2019 | |

| Model 3 | DE/GPR | 2020 |

| Model | MAE | MAPE (%) | RMSE | R2 |

|---|---|---|---|---|

| Model 1 | 83.841 | 5.92 | 92.700 | 0.152 |

| Model 2 | 73.654 | 5.06 | 95.873 | 0.389 |

| Model 3 | 177.32 | 10.12 | 192.68 | 0.301 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

García-Gonzalo, E.; García-Nieto, P.J.; Fidalgo Valverde, G.; Riesgo Fernández, P.; Sánchez Lasheras, F.; Suárez Gómez, S.L. Hybrid DE-Optimized GPR and NARX/SVR Models for Forecasting Gold Spot Prices: A Case Study of the Global Commodities Market. Mathematics 2024, 12, 1039. https://doi.org/10.3390/math12071039

García-Gonzalo E, García-Nieto PJ, Fidalgo Valverde G, Riesgo Fernández P, Sánchez Lasheras F, Suárez Gómez SL. Hybrid DE-Optimized GPR and NARX/SVR Models for Forecasting Gold Spot Prices: A Case Study of the Global Commodities Market. Mathematics. 2024; 12(7):1039. https://doi.org/10.3390/math12071039

Chicago/Turabian StyleGarcía-Gonzalo, Esperanza, Paulino José García-Nieto, Gregorio Fidalgo Valverde, Pedro Riesgo Fernández, Fernando Sánchez Lasheras, and Sergio Luis Suárez Gómez. 2024. "Hybrid DE-Optimized GPR and NARX/SVR Models for Forecasting Gold Spot Prices: A Case Study of the Global Commodities Market" Mathematics 12, no. 7: 1039. https://doi.org/10.3390/math12071039

APA StyleGarcía-Gonzalo, E., García-Nieto, P. J., Fidalgo Valverde, G., Riesgo Fernández, P., Sánchez Lasheras, F., & Suárez Gómez, S. L. (2024). Hybrid DE-Optimized GPR and NARX/SVR Models for Forecasting Gold Spot Prices: A Case Study of the Global Commodities Market. Mathematics, 12(7), 1039. https://doi.org/10.3390/math12071039