Abstract

Mobile payment, replacing traditional methods like cash and cards, offers users convenience and accessibility, benefiting individuals, businesses, and governments. However, most research on mobile payment adoption has primarily focused on developed countries, leaving a gap in understanding the adoption factors in developing nations. This study addresses this gap by investigating the determinants of mobile payment adoption in Thailand, an emerging economy experiencing significant smartphone adoption and e-commerce growth. Through a quantitative approach and a survey of 475 Thai consumers, this research applies an extended Unified Theory of Acceptance and Use of Technology (UTAUT) model as a theoretical foundation to examine Thai consumers’ mobile payment adoption. Data analysis using SPSS 28.0 and AMOS 28.0 identifies key factors influencing Thai consumers to adopt mobile payment. By offering a comprehensive research model and considering evolving smartphone technology, this study aims to guide policymakers and stakeholders in promoting mobile payment adoption, ultimately enhancing Thailand’s economic development and tourism industry.

1. Introduction

In the era of the 4.0 Industrial Revolution, advancements in information and communications technology, along with wireless Internet, have integrated functionalities into smartphones, making them indispensable in daily life worldwide (Arniati 2023; Nguyen et al. 2023). This evolution has significantly influenced the growth of e-commerce and mobile commerce (Changchit et al. 2023b; Loh et al. 2023). Mobile commerce, encompassing various services like mobile advertising, mobile games, and mobile payment, has become a cornerstone of modern transactions (Changchit et al. 2023b).

Mobile payment, particularly, serves as a crucial platform supporting other mobile commerce applications (Tew et al. 2022). Defined as the use of wireless Internet-connected devices to conduct financial transactions, mobile payment enables convenient, anytime, and anywhere purchases and services (Bailey et al. 2022). The concept of a cashless society has garnered growing interest due to the widespread adoption of cashless transactions and the increasing circulation of digital currency (Chang et al. 2024). It is gradually replacing traditional forms of payment, offering benefits such as expanded consumer reach for businesses and improved convenience for consumers (Belanche et al. 2022).

The growth of mobile payment extends beyond developed countries, with significant adoption in developing and newly emerging economies (Chang et al. 2023). Southeast Asia, for instance, has seen a rapid increase in mobile payment transactions, driven by modernizing telecommunications infrastructure and increasing smartphone penetration (Arniati 2023).

Despite the growing importance of mobile payments, research has predominantly focused on developed countries, leaving a gap in the understanding of the adoption factors in developing or newly emerging countries (Bui et al. 2022). The emphasis on developed countries in previous studies may be attributed to their advanced telecommunications infrastructure and higher income levels. This study aims to fill this gap by examining the factors influencing mobile payment intention in Thailand, a newly emerging economy with a high smartphone adoption rate and a booming tourism industry (Chinnapakjarusiri et al. 2024).

This research aims to propose a comprehensive model to understand mobile payment adoption factors, considering the evolving landscape of mobile payment and its implications for developing economies like Thailand. The findings are expected to inform policymakers and businesses on strategies to promote mobile payment, potentially attracting more international business and tourism to Thailand.

Overall, this paper contributes to the understanding of mobile payment adoption in emerging economies and provides insights that can drive its further growth and development. The subsequent sections of this paper detail the characteristics of mobile payment, the adoption landscape in Thailand, the research methodology, results, and implications for theory and practice, followed by conclusions, limitations, and future research directions.

2. Literature Review

2.1. Previous Studies on Mobile Payment

Mobile payment is considered as an evolutionary form of online payment (Hanafiah et al. 2024). Mobile payment is conducted via a mobile network (Ghosh 2024). In other words, mobile payment is regarded as a process in which at least one stage of a financial transaction is performed through a handheld mobile device connected to the wireless Internet, for example, a smartphone, tablet, or personal digital assistant, capable of processing a financial transaction through a mobile network (Chang et al. 2024).

Revolutionary advances in information and communications technology, along with wireless Internet, are fundamentally transforming the mobile payment sector (Mollick et al. 2023). Mobile payment is predicted to become the most popular payment method in the future, superseding traditional forms such as cash, checks, debit cards, and credit cards (Changchit et al. 2023b).

Numerous studies have been conducted to identify the factors influencing the intention to use mobile payment (Ling et al. 2024; Wen et al. 2023). These studies draw on theories/models of behaviors, attitudes, and technology acceptance (Momani 2020). The theory of reasoned action (TRA) by Fishbien and Ajzen (1975) explains individual behaviors, focusing on attitudes toward the behavioral and subjective norms. The theory of planned behavior (TPB) by Ajzen (1991) suggests that beliefs can determine intended and actual behaviors.

The technology acceptance model (TAM) by Davis et al. (1989) examines information technology acceptance, with perceived ease of use and usefulness as key variables. Some studies augment these with factors like perceived trust, transaction convenience, speed, security, privacy, and perceived compatibility, influencing mobile commerce intentions (Mollick et al. 2023).

A study by Sun et al. (2020) emphasizes perceived compatibility, portability, and subjective norms, while Handarkho (2021) focuses on behavioral beliefs, social influences, and personal characteristics. Phan et al. (2020) and Belanche et al. (2022) highlight similar factors, with Singh (2020) adding social influences and performance expectancy. Chen and Lai (2023) note that perceived risk and cost hinder mobile payment intention.

Most research on mobile payment has been on developed countries, with limited studies in Southeast Asia and even fewer in Thailand despite its high smartphone adoption rate. Prior studies often consider factors in isolation. Therefore, a comprehensive and systematic research model that integrates various factors is needed to enhance the explanatory power of mobile payment intention, especially given the evolving technological landscape in newly emerging countries like Thailand. This study addresses these gaps.

2.2. Current Situation on Mobile Payment in Thailand

Thailand is a newly emerging country with a population of 71 million people (Worldometers 2023). The country boasts enormous potential for economic growth and development, situated in a strategic position in Southeast Asia that attracts significant foreign direct investment. As a result, more multinational companies and their supply chains are establishing business operations in Thailand.

The success of the Thai economy can be attributed to economic reform and transformation policies, which aim to attract foreign companies to establish manufacturing and processing plants in the country. Additionally, Thailand’s tourism industry is flourishing, supported by its beautiful landscapes and the hospitality of its people (Chinnapakjarusiri et al. 2024). The country’s Internet infrastructure and information and telecommunications technology are also increasingly modernized, with over 90% of the population using smartphones (Boonsiritomachai and Sud-On 2023) and approximately 49% participating in e-commerce.

Thailand’s e-commerce sales hit $31 billion in 2023, accounting for about 10% of the country’s total retail sales of consumer goods (Vu and Nguyen 2024). Thailand is seen as having significant potential to further develop mobile payment. Popular forms of mobile payment in the world are present in Thailand. Statistics show that within the next 5 years, the growth rate of mobile payment in Thailand will reach an average of 7.51% a year (Ponsree 2024).

Despite the benefits of mobile payment, it is surprising that not all Thai citizens use mobile payment. This could be due to approximately 48 percent of the Thai population living in rural areas in Thailand that have limited telecommunications infrastructure (Telecom Review 2024; Worldometers 2024). Previous studies have identified factors that influence mobile payment usage. However, these studies are mostly conducted in developed countries. A notable feature of these studies is that they examine factors in isolation and discretely, not as constituent components of an integrated research model. Furthermore, the evolution of mobile payment requires adding new factors to the research model to increase its explanatory power for intention to use mobile payment. These factors include perceived security, perceived privacy, perceived compatibility, and technology competency.

Given the fact that Thailand can be a representative of developing or newly emerging countries, it is necessary to choose a comprehensive research model to examine intention to use mobile payment. The model chosen in this study is the Unified Theory of Acceptance and Use of Technology (UTAUT). The reason for choosing this model is that it is built on the outstanding features of other technology acceptance theories and models. To increase its explanatory power for the intention to use mobile payment, variables added to the UTAUT include technology competency, perceived compatibility, perceived privacy, perceived security, and attitude toward mobile payment.

Thailand is increasingly attracting foreign direct investment, multinational companies and their supply chains are moving to Thailand, and Thailand’s tourism industry has potential for further growth. In addition, the Thai government is working to improve the telecommunications infrastructure in the rural parts of Thailand (Telecom Review 2024), opening even more opportunities to expand mobile payment in Thailand. Therefore, identifying factors that influence intention to use mobile payment in Thailand will help Thailand develop strategies and policies to promote the acceptance and use of mobile payment, which, in turn, further support economic growth and development in Thailand.

3. Theoretical Background, Research Model, and Hypotheses

Based on the review of outstanding features of technology acceptance models and theories, Venkatesh (2022) developed the Unified Theory of Acceptance and Use of Technology (UTAUT). Four basic factors make up the UTAUT, including performance expectancy, effort expectancy, social influence, and facilitating conditions. The UTAUT has been used in many studies on the acceptance of a new technology in different contexts.

Consistent with studies using the UTAUT, this study also focuses on four basic factors: performance expectancy, effort expectancy, social influence, and facilitating conditions to examine the intention to use mobile payment in Thailand. It is worth noting that mobile payment is an evolutionary form of online payment. In the mobile payment environment, transactions and exchanges are conducted anytime and anywhere. As a form of technology use in payment, an individual’s technology competence plays an important role in influencing the intention to use mobile payment.

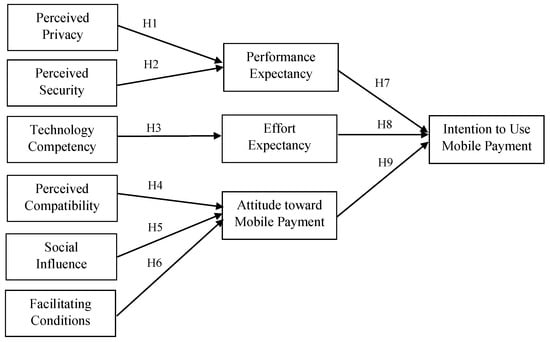

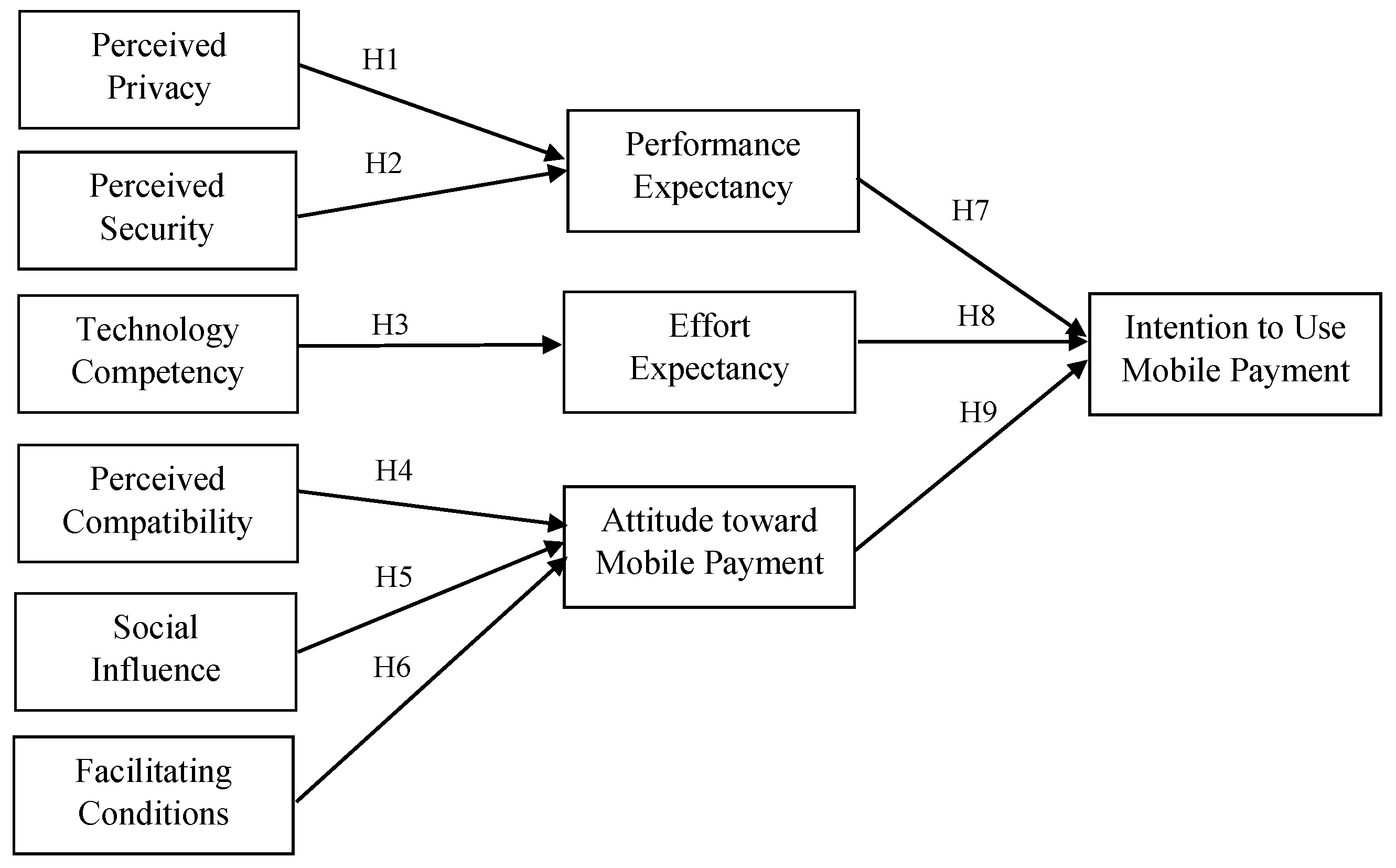

Perceived compatibility is also an important factor, because individuals will be willing to participate in activities that are compatible with their lifestyle and social image. In the mobile payment environment, transactions and exchanges take place without limitations of space and time, so risks related to privacy and security are considered higher than in other payment contexts. Therefore, perceived privacy, perceived security, perceived compatibility, technology competency, and attitude toward mobile payment, from a study by Changchit et al. (2023a), were integrated into the UTAUT. These factors are expected to influence the intention to use mobile payment. This is consistent with the studies of Changchit et al. (2023a). Figure 1 shows the integrated research model utilized to examine consumers’ intentions to use mobile payment in Thailand.

Figure 1.

Research models and hypotheses.

3.1. Perceived Privacy and Security

Accepting and using a new technology involves risks (Bland et al. 2024; Katini et al. 2023). Since mobile payment can be conducted anywhere and anytime, consumers face difficulties in evaluating its reliability (Abrahim Sleiman et al. 2023). In other words, consumers are concerned about security and privacy issues. If consumers are assured that their personal and financial information is respected, not used for illegal purposes, and not transferred to third parties without their consent, their expectations about the outcomes of using mobile payment will be enhanced. Empirical studies also show that perceived privacy and perceived security are positively related to performance expectancy (Changchit et al. 2023b). Consistent with these studies, the following hypotheses are proposed:

H1.

A positive relationship exists between perceived privacy and performance expectancy.

H2.

A positive relationship exists between perceived security and performance expectancy.

3.2. Technology Competency

Technology competency is seen as the degree to which consumers can use technologies in different contexts (Alzeaideen et al. 2024). Consumers with high technology competency seem to be motivated and encouraged to use technologies to complete tasks at work, at home, or in social interactions and communications (Ling et al. 2024). Consumers with high levels of technology competency will feel it is easy to learn how to use mobile payment (Changchit et al. 2024). Furthermore, in the context of mobile payment, consumers with good technology competency tend to be confident that using mobile payment does not require significant efforts in terms of time and cost (Al-Okaily et al. 2024). Consistent with previous studies, the following hypothesis is proposed:

H3.

A positive relationship exists between technology competency and effort expectancy.

3.3. Perceived Compatibility

Perceived compatibility in the mobile payment environment can be understood as the extent to which the characteristics of mobile payment align with the intrinsic characteristics of mobile payment consumers (Ayoungman et al. 2021). These intrinsic characteristics may include lifestyles, values, social images, or experiences (Changchit et al. 2024). The intrinsic characteristics of consumers are considered crucial in determining their preference for mobile payment over other forms of payment. Empirical studies in the contexts of online banking, online payment, e-commerce, and m-commerce have demonstrated that perceived compatibility significantly influences attitudes toward the use of technology or innovation (Pushpa et al. 2022). Thus, the following hypothesis is proposed:

H4.

A positive relationship exists between perceived compatibility and attitude toward mobile payment.

3.4. Social Influence

Social influence is understood as the extent to which consumers perceive that individuals significant to them, such as friends, co-workers, or family members, believe they should or should not adopt a technology or innovation (Venkatesh et al. 2012). It is worth noting that in many situations, the attitudes and behaviors of these individuals influence consumers’ attitudes toward technology adoption (Geng et al. 2023). In the context of mobile payment, if social influence is substantial, consumers’ attitudes toward mobile payment adoption will be positively influenced. Consistent with previous studies, the following hypothesis is proposed:

H5.

A positive relationship exists between social influence and attitudes toward mobile payment.

3.5. Facilitating Conditions

Facilitating conditions are the degree to which a consumer believes that the technological, organizational, and human infrastructures exist to support the adoption or use of a technology or innovation (Chawla and Joshi 2023). These enabling conditions include technological, organizational, and human factors or attributes that act to remove the barriers related to the acceptance or use of a technology or innovation (Man et al. 2022). Consistent with previous studies (e.g., Man et al. 2022; Roh et al. 2023), the following hypothesis is proposed:

H6.

A positive relationship exists between facilitating conditions and attitudes towards mobile payment.

3.6. Performance Expectancy

Performance expectancy demonstrates the usefulness of a technology or innovation (Purohit et al. 2022). The expected benefits generated by using a technology can influence the intention to use that technology. Consumers’ perception that using mobile payment can bring convenience and benefits will lead to the intention to use or accept mobile payment (Widyanto et al. 2020). Consistent with previous studies, the following hypothesis is proposed:

H7.

A positive relationship exists between performance expectancy and the intention to use mobile payment.

3.7. Effort Expectancy

Effort expectancy is understood as the degree to which using a technology is difficult or easy (Wei et al. 2021). Effort expectancy serves as an important factor influencing technology acceptance (Saprikis et al. 2022). In the mobile payment environment, if consumers perceive that it is simple to use mobile payment or that using mobile payment does not require significant efforts, they will tend to use mobile payment. Consistent with previous studies, the following hypothesis is proposed:

H8.

A positive relationship exists between effort expectancy and the intention to use mobile payment.

3.8. Attitude toward Mobile Payment

In the e-commerce or mobile commerce environment, a technology is considered successful if consumers are able and willing to accept and use that technology (Upadhyay et al. 2022). Consumers with positive attitudes are more likely to accept technology than other consumers (Lu and Ahn 2023). In the context of mobile payment, consumers will have a positive attitude towards mobile payment if they can achieve their goals or expected benefits from using mobile payment (Changchit et al. 2023b). Positive attitudes will boost the intention to use mobile payment. Consistent with previous studies, the following hypothesis is proposed:

H9.

A positive relationship exists between attitude toward mobile payment and the intention to use mobile payment.

4. Research Methodology

4.1. Measurement Instrument

The survey instrument for this study was developed based on an adaptation of the UTAUT scales developed by Venkatesh (2022) and a study by Changchit et al. (2023). The questionnaire includes scales, namely the intention to use mobile payment, performance expectancy, effort expectancy, attitude towards mobile payment, perceived privacy, perceived security, technology competency, perceived compatibility, social influence, and facilitating conditions.

A mobile payment expert, fluent in both English and Thai, translated the questionnaire into Thai. Another mobile payment expert, proficient in both English and Thai, back-translated the Thai version into English to evaluate the level of consistency between the Thai and English versions. Two mobile payment researchers fluent in both Thai and English independently reviewed the Thai and English versions of the survey. The results indicated that both the Thai and English versions were consistent and accurate. Evaluations to validate the appropriateness and reliability of the items constituting the scales in the measurement model were performed.

The survey questionnaire consists of two parts: The first part aimed to collect data on consumers’ perceptions about mobile payment and their intention to use mobile payment. The second part aimed to collect demographic information. To enhance the reliability and validity of the questionnaire, three professors and ten mobile payment consumers filled out the questionnaire and provided feedback. Some adjustments were made based on the feedback to improve the questionnaire.

Appendix A summarizes the constructs and measurement items designed to assess consumer perception levels about mobile payment and their intention to use mobile payment. All items use a 5-level Likert scale (1 = strongly disagree and 5 = strongly agree).

4.2. Data Collection and Subjects’ Demographics

Questionnaires were developed using Google Forms and distributed online via Facebook pages, using a snowball method for data collection. The survey began with a qualifying question asking if the potential participant was a Thai citizen currently living in Thailand and at least 18 years old. If the potential participant did not meet these criteria, they were thanked for their willingness to participate but informed that they did not qualify, as only participants with Thai citizenship living in Thailand were being studied. Four hundred and seventy-five (475) subjects qualified and participated in this study. Each question was set with validation to require a response, ensuring that all surveys were fully completed. According to Hair et al. (2009), the sample size should be at least ten times the number of variables; thus, the sample size for this study is considered sufficient and appropriate. The demographics of the respondents are shown in Table 1.

Table 1.

Subjects’ demographics (n = 475).

5. Data Analysis

SPSS 28.0 and AMOS 28.0 were used to analyze the data. This section describes the data analysis.

5.1. Reliability Test

A reliability test was conducted to assess the internal consistency of the survey instrument’s constructs. The reliability of each construct in the research model was calculated, and the results are presented in Table 2. All reliability test results exceed the recommended value of 0.70 (Nunnally 1978), indicating that the internal consistency of the constructs is satisfactory.

Table 2.

Reliability test *.

5.2. KMO and Bartlett’s Test

The Kaiser–Meyer–Olkin (KMO) and Bartlett’s tests were conducted to assess the unidimensionality of the scales (refer to Table 3). The sphericity test yielded a significant p-value of 0.000. Additionally, the sampling adequacy was confirmed by a value of 0.959.

Table 3.

KMO and Bartlett’s Test.

5.3. Common Method Bias

Harman’s single-factor test was employed to verify the absence of common method bias in the model. The analysis was performed using SPSS, conducting an unrotated, single-factor constraint factor analysis. As depicted in Table 4, the highest variance explained by one factor was 41.896%, suggesting that there are no significant concerns regarding common method bias.

Table 4.

Total variance explained.

5.4. Analysis of Factor Loadings

To assess the convergent validity of the factors, factor loadings were examined to ensure that each survey item loaded appropriately onto its corresponding factor (refer to Table 5). The findings indicate that the thirty-nine survey items loaded onto ten factors, explaining 74.621% of the total variance. Items with factor loadings below the recommended threshold of 0.6 (Hair et al. 2009) were eliminated during the data analysis process.

Table 5.

Factor analysis *.

5.5. Multicollinearity Test

To address the potential adverse effects of multicollinearity, an assessment was conducted within the research model (Cenfetelli and Bassellier 2009). As shown in Table 6 below, the Variance Inflation Factor (VIF) ranged from 1.799 to 2.828, all below the threshold of 10. This indicates that multicollinearity is not a significant concern in this dataset.

Table 6.

Multicollinearity test.

5.6. Structural Equation Model (SEM)

SPSS AMOS 28.0 was utilized to analyze the research model. Seven structural equation modeling (SEM) fit measures were evaluated to determine the overall goodness of fit of the model. All goodness of fit indices were found to be within acceptable ranges (refer to Table 7), suggesting that the model exhibited a strong fit with the data (Bentler and Bonett 1980; Hu and Bentler 1999; Tucker and Lewis 1973).

Table 7.

Fit indices for the models.

5.7. Hypothesis Testing

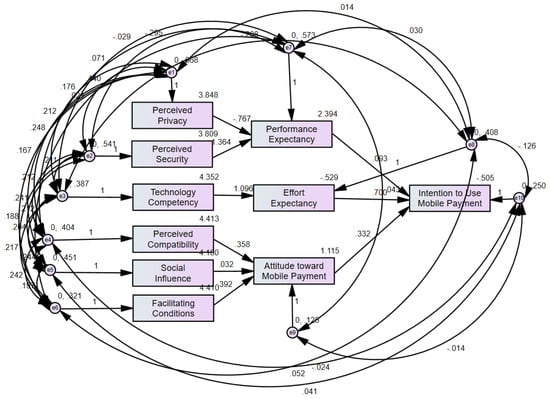

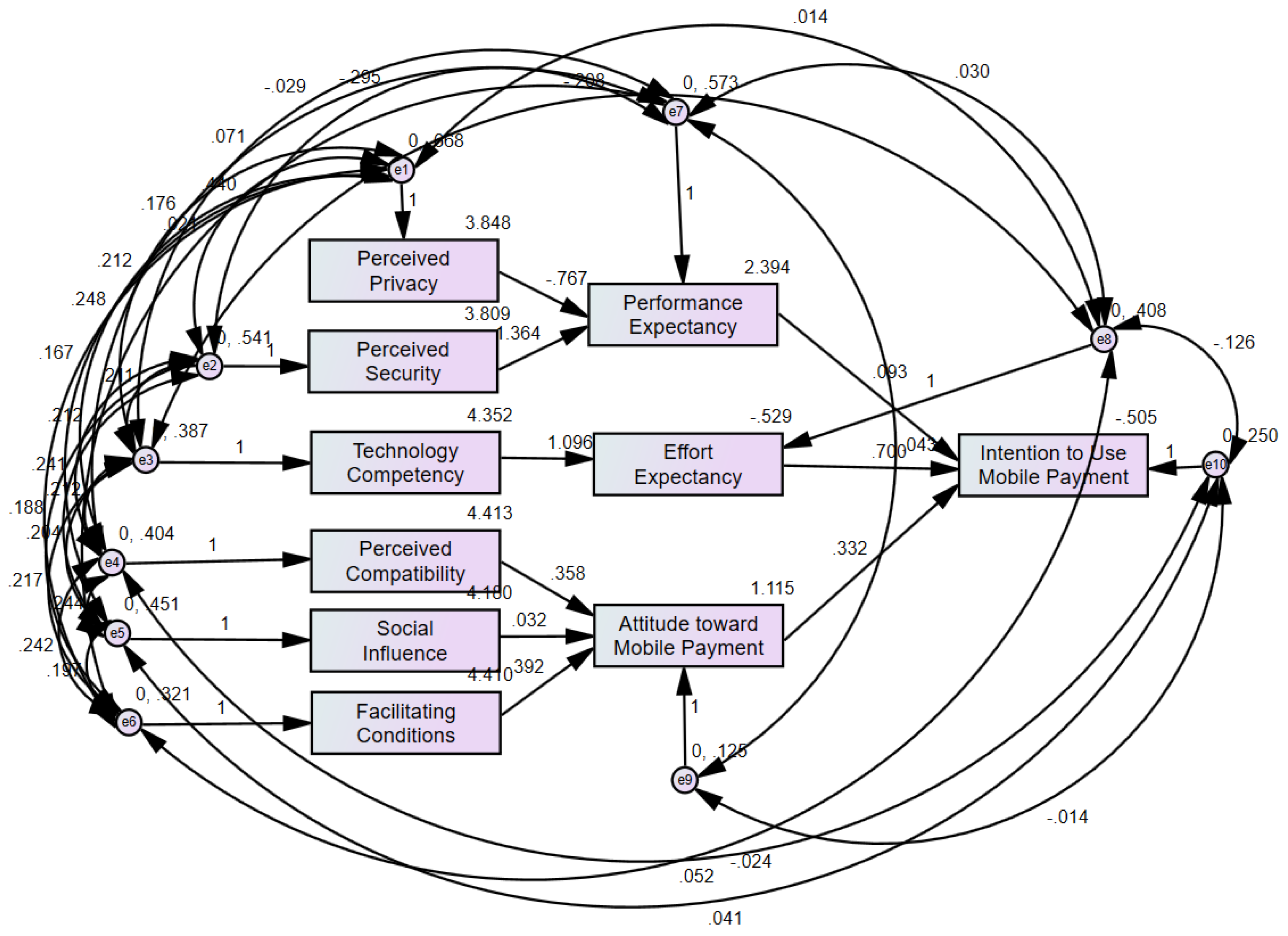

Table 8 provides the results of the hypothesis testing. Figure 2 illustrates the properties of the causal paths, including standardized path coefficients.

Table 8.

Hypothesis testing.

Figure 2.

Path analysis of structure equation model.

6. Results and Discussion

The research model proposed in this study received partial support, with the data validating six out of nine hypotheses. Specifically, H1, which posited a significant relationship between perceived privacy and performance expectancy, was supported (β = −0.767, p-value < 0.001). Contrary to the expected positive relationship, a negative correlation was found, consistent with Alanzi et al. (2023). While this aligns with the significance noted by Abd-Alrazaq et al. (2020), it contrasts with their positive correlations, possibly due to Thai consumers perceiving that enhanced privacy protections in mobile payment systems may detract from system performance.

The findings corroborate H2, providing evidence for a positive relationship between perceived security and performance expectancy (β = 1.364, p < 0.001). Given the direct linkage of mobile payments to consumers’ banking or credit card accounts, the security of these transactions emerges as a crucial part of the anticipated performance from mobile payment technologies. The likelihood of consumers attributing a higher performance to mobile payment technology increases when they perceive their financial information as safeguarded. The significant finding for H2 agree with the results reported in mobile payment studies by Katini et al. (2023) and Abrahim Sleiman et al. (2023).

The current study supports hypothesis H3, indicating a significant positive relationship between technology competency and effort expectancy (β = 1.096, p-value < 0.001). The rationale posited that higher technology competency reduces the effort required to use mobile payment technology. This finding aligns with Nguyen (2023) but contradicts Bailey et al. (2022), who found no significant relationship. The discrepancy may be attributed to the generally simplistic design of mobile payment technology, which minimizes the effort needed across all levels of technology competency.

The data analysis revealed support (β = 0.358, p-value < 0.001) for the proposed positive relationship between perceived compatibility and attitude toward mobile payment (H4). This relationship essentially looks at how mobile payment fits into the lifestyles of consumers. The better the fit that mobile payment provides with the consumer’s lifestyle, the more likely the consumer is to have a positive attitude towards mobile payment. This finding agrees with the findings reported in studies by Nguyen (2023) and Alzaidi (2022). This could be explained by the ubiquity of mobile devices in Thailand. Those who possess a smart mobile device are likely to have that device with them for most of their waking hours. Thus, it is perceived as compatible with their lifestyles, resulting in a more favorable attitude toward mobile payment.

The data analysis results did not support H5, which proposed a positive relationship between social influence and attitude toward mobile payment (β = 0.032, p-value = 0.283). This finding is consistent with studies by Lu and Lu (2020) on Chinese Millennials’ mobile payment adoption and Sharma et al. (2020). However, it contradicts Geng et al. (2023), who reported a significant relationship. The discrepancy may be attributed to Thailand’s collectivist culture, where individuals have large social networks with diverse opinions on mobile payment. Consequently, Thai consumers may prioritize perceived benefits over social influence when deciding to adopt mobile payment.

Support was found for H6, which proposed a positive relationship between facilitating conditions and attitude toward mobile payment (β = 0.392, p-value < 0.001). Facilitating conditions, such as having a compatible device, the ability to use it, and a wireless Internet connection, are essential for utilizing mobile payment (Chawla and Joshi 2023). This finding aligns with studies by Chawla and Joshi (2023) and Roh et al. (2023) but contrasts with Abd-Alrazaq et al. (2020). Since the introduction of the Thailand 4.0 Strategy in 2016, the Thai government has promoted digital economy initiatives, enhancing mobile device usage and broadband connectivity. Collaborative efforts with the Central Bank of Thailand have further supported mobile payment adoption, fostering a positive attitude toward mobile payment among Thai consumers (Mastercard 2024).

The data analysis results did not support H7, which proposed a positive relationship between performance expectancy and the intention to use mobile payment (β = 0.093, p-value = 0.293). This finding aligns with the results of de Blanes Sebastián et al. (2023) and Purohit et al. (2022) but diverges from studies by Bailey et al. (2022), Linge et al. (2023), and Widyanto et al. (2022). The absence of a significant link between performance expectancy and intention may be due to Thailand’s longstanding preference for cash transactions, which diminishes the perceived advantages of mobile payments. Additionally, the maturity of mobile payment technology in Thailand may lead consumers to base their decision on other factors.

The analysis confirmed the hypothesized positive relationship between effort expectancy and the intention to use mobile payment (H8), with significant support (β = 0.700, p < 0.001). This aligns with findings from Linge et al. (2023) and Purohit et al. (2022) while contrasting with studies by Bailey et al. (2022) and de Blanes Sebastián et al. (2023), which found no significant correlation. The current study’s findings may be attributed to the simplicity of mobile payment systems, which require minimal effort to use, and the technological competence of consumers who find these systems easy to adopt, thereby increasing their intention to use mobile payment.

The data analysis results did not support H9, which proposed a positive relationship between attitude toward mobile payment and the intention to use mobile payment (β = 0.332, p-value = 0.110). This finding is quite interesting and contradicts reports found in many prior studies (e.g., Lu and Ahn 2023; Yang et al. 2023). Several factors may contribute to this unexpected result.

First, it is possible that external factors, such as social influence and facilitating conditions, play a more dominant role in shaping the intention to use mobile payments in Thailand. In a collectivist society like Thailand, the opinions and behaviors of peers, family, and social networks can have a stronger impact on individual decisions compared to personal attitudes.

Second, the widespread adoption of mobile payments in Thailand may have reached a point where the intention to use is driven more by practical considerations and convenience than by personal attitudes. With the Thai government’s strong push for digital economy initiatives and the collaboration with the Central Bank of Thailand, mobile payment infrastructure and support have become robust, possibly reducing the influence of personal attitudes on usage intention.

Third, the novelty effect of mobile payment technology might have worn off, making attitudes less predictive of usage intentions. As mobile payments become a standard and routine part of everyday transactions, users’ intentions might be influenced more by habitual behaviors and established routines than by their attitudes toward the technology.

7. Study Implications

7.1. Theoretical Implications

The current study significantly expands upon the Unified Theory of Acceptance and Use of Technology (UTAUT) by incorporating several crucial variables specific to the mobile payment context within Thailand’s dynamic market landscape. By integrating perceived privacy, perceived security, technological competency, perceived compatibility, and attitude toward mobile payment, this research enriches our understanding of the intricate factors influencing mobile payment adoption in developing regions.

This advancement is particularly noteworthy, as it sheds light on the unique considerations and challenges faced by consumers in emerging economies like Thailand. Unlike findings from more advanced economies, the factors driving technology adoption in developing contexts can vary significantly due to cultural, economic, and infrastructural differences. Therefore, this study provides valuable insights that cannot be simply extrapolated from research conducted in developed nations.

Moreover, this research endeavor addresses a notable gap in the existing literature, as identified by Bui et al. (2022), by offering a comprehensive examination of mobile payment adoption within developing economies. By delving deeply into this relatively underexplored area, the study contributes not only to academic knowledge but also to practical understanding and application in real-world settings.

Furthermore, the dynamic nature of technological advancements, particularly in the realm of mobile payment, necessitates continuous investigation and adaptation. As new technologies emerge and consumer preferences evolve, previously significant factors may become obsolete or require re-evaluation. Thus, ongoing research efforts are crucial for staying abreast of these developments and ensuring the relevance and applicability of findings over time.

Lastly, the proposed research model serves as a robust framework that can guide future studies on mobile payment adoption in developing economies. By providing a comprehensive structure and incorporating the key variables relevant to these contexts, this model lays the groundwork for further exploration and refinement in this field. It not only facilitates a deeper understanding of mobile payment dynamics but also offers practical implications for policymakers, businesses, and other stakeholders striving to promote technological innovation and economic development in developing nations.

7.2. Practical Implications

The findings of this study provide actionable insights for mobile payment service providers, offering guidance on how to develop systems that better align with user preferences. For instance, the research highlights the paramount importance of privacy and security for Thai consumers, indicating that providers should prioritize implementing robust measures in their systems to ensure the safety and confidentiality of users’ information. Additionally, the study emphasizes the significance of aligning mobile payment systems with the needs and lifestyles of Thai consumers. This is exemplified by the observed relationship between perceived compatibility and attitudes toward mobile payment, suggesting that systems tailored to fit seamlessly into users’ lives are more likely to be embraced.

Moreover, the study’s focus on facilitating conditions resonates with the Thai government’s Thailand 4.0 Strategy, which seeks to enhance Internet connectivity and advance the digital economy. Enhancing the telecommunications infrastructure to better serve the rural areas of Thailand (see Telecom Review 2024) is only part of the solution; the Thai government should also consider implementing educational programs to boost the digital literacy of residents in the rural areas. This could be accomplished through public–private partnerships to improve the financial inclusion among the Thai population. By emphasizing the importance of user experience, the research suggests that providers should concentrate on creating intuitive user interfaces, simplifying registration and authentication processes, and refining transaction pathways. These efforts are essential for enhancing the overall user experience and fostering a greater adoption of mobile payment solutions in Thailand.

8. Conclusions, Limitations, and Future Research Directions

This study applied an extended UTAUT model as a theoretical foundation to examine Thai consumers’ mobile payment adoption. The proposed research model accounted for approximately 74 percent of the variance on Thai consumers’ behavioral intentions towards mobile payment adoption. This study takes a step towards filling a gap in the literature by addressing the adoption of mobile payment in the developing economy of Thailand.

By expanding the Unified Theory of Acceptance and Use of Technology (UTAUT) framework to include constructs such as perceived privacy, perceived security, technological competency, perceived compatibility, and attitude toward mobile payment, this investigation explains the impact of certain factors on the willingness of individuals to adopt mobile payments. Highlighting the pivotal role of privacy and security, this study underscores consumer apprehensions regarding the safeguarding of their financial dealings within mobile payment frameworks. Furthermore, it provides evidence of the significance of technology competency and the perceived compatibility with individual consumer lifestyles and their attitude towards mobile payments, subsequently influencing their intent to adopt.

This study provides practical insights for businesses offering mobile payment services, advocating for a concerted emphasis on bolstering privacy, security, and overall user experience. Through the alignment of mobile payment frameworks with consumer preferences and the assurance of stringent security protocols, service providers are positioned to stimulate broader acceptance among Thai consumers. Moreover, the findings furnish critical implications for policy architects, highlighting the instrumental role of enabling conditions, such as expansive broadband wireless Internet access and conducive digital economic policies, in the enablement of mobile payment adoption.

Overall, this study addresses a gap within the existing literature by delivering an exhaustive dissection of the determinants influencing mobile payment adoption in the context of developing economies. It not only corroborates the expanded UTAUT model within the Thai milieu but also offers actionable items for stakeholders endeavoring to bolster financial inclusivity and economic advancement via mobile payment technologies. Future inquiries may delve into the enduring effects of these determinants on mobile payment acceptance and investigate the transformative potential of emerging technologies in refining consumer dispositions and behaviors towards mobile payment.

Empirical research inherently has its limitations, and this study is no exception. The focus was on Thai consumers, with data collected via an online survey from self-selected participants, introducing self-selection bias as a limitation. Participants who chose to participate may hold different perspectives compared to those who did not, potentially limiting the representativeness of the sample for the Thai population. However, given the constraints of empirical research, the researchers consider the sample sufficient.

Furthermore, this study solely concentrated on participants from Thailand, despite the availability of mobile payment in numerous other developing economies. Future research could explore a more diverse sample across multiple developing countries and compare mobile payment perspectives between developed and developing economies, offering insights into cultural and economic influences. A comparative study across developing economies with diverse cultures could also be an intriguing area for future research. Additionally, exploring the impact of financial risk on mobile payment adoption in Thailand is another promising avenue for future investigation.

The investigation into mobile payment system acceptance in Thailand represents an advancement in understanding technology acceptance within developing economies. This research offers insights that can be instrumental in similar economies grappling with comparable technological adoption challenges and opportunities. Understanding the dynamics of technology adoption among consumers in these contexts is vital for businesses and policymakers aiming to drive innovation and economic progress. This study contributes to the scholarly dialogue on technology acceptance, laying the groundwork for future research endeavors in this domain and offering valuable implications for academia and industry alike.

Author Contributions

Conceptualization, C.C., methodology, C.C. and R.C.; writing—original draft preparation, L.P. and R.C.; writing—review and editing, C.C., L.P. and R.C.; supervision, C.C. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

The raw data supporting the conclusions of this article will be made available by the authors on request.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A. Research Questionnaire

| Performance Expectancy (PE) | |

| Mobile payment is useful to purchase products or services | |

| Mobile payment makes it easier to conduct transactions | |

| Mobile payment enables me to buy products or services faster | |

| Mobile payment saves me time | |

| Mobile payment makes my life easier | |

| Effort Expectancy (EE) | |

| Learning to use mobile payment is easy | |

| It does not require much effort to learn how to use mobile payment | |

| It is easy to perform the steps required to use mobile payment | |

| It is easy to become skillful at using mobile payment | |

| Conducting transactions via mobile payment is easier than using other payment methods | |

| Technology Competency (TC) | |

| My skills with technology are good | |

| I am not afraid of using technology | |

| My ability to learn new technology is good | |

| I am always interested in new technology | |

| I enjoy working with technology | |

| Perceived Privacy (PP) | |

| I believe that mobile payment providers will protect the privacy of my personal data | |

| I believe that mobile payment systems will not disclose my personal data | |

| I believe that mobile payment systems will keep transactions confidential | |

| I believe that mobile payment systems will keep my information confidential | |

| I believe that mobile payment systems will prevent others from looking at my data | |

| Perceived Security (PS) | |

| Using mobile payment enable me to conduct transaction securely | |

| I feel confident about the security of mobile payment system | |

| I am not worried about the security of mobile payment | |

| I believe that mobile payment systems protect me from unauthorized transactions | |

| I believe that the transactions conducted via mobile payment are secured | |

| Perceived Compatibility (PC) | |

| Mobile payment fits my lifestyle | |

| Mobile payment is compatible with my shopping behavior | |

| Mobile payment is compatible with my busy schedules | |

| Mobile payment is suitable for me | |

| Mobile payment is compatible with my lifestyle | |

| Social Influence (SI) | |

| People who are important to me find using mobile payment beneficial | |

| People who are important to me use mobile payment | |

| People who are important to me think I should use mobile payment | |

| People who are important to me encourage me to use mobile payment | |

| People who are important to me enjoy using mobile payment | |

| Facilitating Conditions (FC) | |

| I have the resources necessary to use mobile payment | |

| I have the knowledge necessary to use mobile payment | |

| Mobile banking is compatible with other systems I use | |

| A person (or group) is available for assistance with system difficulties | |

| I have the devices necessary to use mobile payment | |

| Attitude toward using mobile payment (ATT) | |

| Using mobile payment is a good idea | |

| Using mobile payment is beneficial | |

| Using mobile payment is favorable | |

| Using mobile payment is a wise thing to do | |

| I am positive toward mobile payment | |

| Intention to Use Mobile Payment (INT) | |

| I like to use mobile payment to purchase products and services | |

| I feel comfortable using mobile payment | |

| I intend to use/continue using mobile payment | |

| I like paying via mobile payment | |

| I will choose mobile payment if it is available | |

References

- Abd-Alrazaq, Alaa, Ali Abdallah Alalwan, Brian McMillan, Bridgette M. Bewick, Mowafa Househ, and Alaa T. Al-Zyadat. 2020. Patients’ adoption of electronic personal health records in England: Secondary data analysis. Journal of Medical Internet Research 22: e17499. [Google Scholar] [CrossRef]

- Ajzen, Icek. 1991. The theory of planned behavior. Organizational Behavior and Human Decision Processes 50: 179–211. [Google Scholar] [CrossRef]

- Alanzi, Turki, Raghad Alotaibi, Rahaf Alajmi, Zainab Bukhamsin, Khadija Fadaq, Nouf AlGhamdi, and Norah Bu Khamsin. 2023. Barriers and facilitators of artificial intelligence in family medicine: An empirical study with physicians in Saudi Arabia. Cureus 15: e49419. [Google Scholar] [CrossRef] [PubMed]

- Al-Okaily, Manaf, Ali Abdallah Alalwan, Dimah Al-Fraihat, Abeer F. Alkhwaldi, Shafique Ur Rehman, and Aws Al-Okaily. 2024. Investigating antecedents of mobile payment systems’ decision-making: A mediated model. Global Knowledge, Memory and Communication 73: 45–66. [Google Scholar] [CrossRef]

- Alzaidi, Maram Saeed. 2022. Exploring the Determinants of Mobile Banking Adoption in the Context of Saudi Arabia. International Journal of Customer Relationship Marketing and Management 13: 1–16. [Google Scholar] [CrossRef]

- Alzeaideen, Khaled, Nidal Al-Ramahi, Mahmoud Odeh, Mohammad Sabri, Nadia Qoazmar, Allam Hamdan, and Huda Atassi. 2024. The Influence that Covid-19 Has Had on the Electronic Payment System, Including Perspectives on Its Usage, Trust, and Competency. In Intelligent Systems, Business, and Innovation Research. Cham: Springer Nature Switzerland, pp. 87–97. [Google Scholar]

- Arniati, Lulu’ul Musytarsyidah. 2023. Factors Influencing Behavioural Intention to Use Mobile Payments in Southeast Asia in 2012–2022. Paper presented at the 5th International Conference on Applied Economics and Social Science, ICAESS 2023, Batam, Riau Islands, Indonesia, 7 November 2023; Bratislava: European Alliance for Innovation, p. 12. [Google Scholar]

- Ayoungman, Fairtown Zhou, Nazmul Hasan Chowdhury, Nida Hussain, and Papel Tanchangya. 2021. User attitude and intentions towards fintech in Bangladesh. International Journal of Asian Business and Information Management (IJABIM) 12: 1–19. [Google Scholar] [CrossRef]

- Bailey, Ainsworth Anthony, Carolyn M. Bonifield, Alejandro Arias, and Juliana Villegas. 2022. Mobile payment adoption in Latin America. Journal of Services Marketing 36: 1058–75. [Google Scholar] [CrossRef]

- Belanche, Daniel, Miguel Guinalíu, and Pablo Albás. 2022. Customer adoption of p2p mobile payment systems: The role of perceived risk. Telematics and Informatics 72: 101851. [Google Scholar] [CrossRef]

- Bentler, Peter M., and Douglas G. Bonett. 1980. Significance tests and goodness of fit in the analysis of covariance structures. Psychological Bulletin 88: 588. [Google Scholar] [CrossRef]

- Bland, Eugene, Chuleeporn Changchit, Charles Changchit, Robert Cutshall, and Long Pham. 2024. Investigating the components of perceived risk factors affecting mobile payment adoption. Journal of Risk and Financial Management 17: 216. [Google Scholar] [CrossRef]

- Boonsiritomachai, Waranpong, and Ploy Sud-On. 2023. Promoting habitual mobile payment usage via the Thai government’s 50: 50 co-payment scheme. Asia Pacific Management Review 28: 163–73. [Google Scholar] [CrossRef]

- Bui, Nhuong, Zachary Moore, Hayden Wimmer, and Long Pham. 2022. Predicting customer loyalty in the mobile banking setting: An integrated approach. International Journal of E-Services and Mobile Applications 14: 1–22. [Google Scholar] [CrossRef]

- Cenfetelli, Ronald T., and Geneviève Bassellier. 2009. Interpretation of formative measurement in information systems research. MIS Quarterly 33: 689–707. [Google Scholar] [CrossRef]

- Chang, Andreas, Theresia Gunawan, and Ujang Sumarwan. 2023. A conceptual framework of mobile payment system adoption and use in Southeast Asia. Journal of ASEAN Studies 11: 15–31. [Google Scholar] [CrossRef]

- Chang, Wei-Lun, Yen-Hao Hsieh, and I-Ting Lu. 2024. Switching to cashless? Exploring costs of switching intention in mobile payment. Journal of Organizational Computing and Electronic Commerce 34: 134–57. [Google Scholar] [CrossRef]

- Changchit, Chuleeporn, Charles Changchit, Robert Cutshall, Long Pham, and Mohan Rao. 2023a. Understanding the determinants of customer intention to use mobile payment: The Vietnamese perspective. Journal of Global Information Management 31: 1–27. [Google Scholar] [CrossRef]

- Changchit, Chuleeporn, Robert Cutshall, and Joseph S. Mollick. 2023b. A three country comparative study of social commerce adoption. Journal of Computer Information Systems 64: 1–16. [Google Scholar] [CrossRef]

- Changchit, Chuleeporn, Robert Cutshall, Ginger DeLatte, Alimursal Ibrahimov, and Charles Changchit. 2024. Exploring personality traits’ impact on risk perception in mobile payments. Journal of Computer Information Systems, 1–16. [Google Scholar] [CrossRef]

- Chawla, Deepak, and Himanshu Joshi. 2023. Role of mediator in examining the influence of antecedents of mobile wallet adoption on attitude and intention. Global Business Review 24: 609–25. [Google Scholar] [CrossRef]

- Chen, Chun-Lung, and Wen-Hsiang Lai. 2023. Exploring the impact of perceived risk on user’s mobile payment adoption. Review of Integrative Business and Economics Research 12: 1–20. [Google Scholar]

- Chinnapakjarusiri, Natworadee, Aishath Rafiyya, and Arnon Kasrisom. 2024. Enhancing International Tourist Brand Awareness in the Digital Economy: A Case Study of Bangkok in Thailand. Advance Knowledge for Executives 3: 1–10. [Google Scholar]

- Davis, Fred D., Richard P. Bagozzi, and Paul R. Warshaw. 1989. User acceptance of computer technology: A comparison of two theoretical models. Management Science 35: 982–1003. [Google Scholar] [CrossRef]

- de Blanes Sebastián, María García, Arta Antonovica, and José Ramón Sarmiento Guede. 2023. What are the leading factors for using Spanish peer-to-peer mobile payment platform Bizum? The applied analysis of the UTAUT2 model. Technological Forecasting and Social Change 187: 122235. [Google Scholar] [CrossRef]

- Fishbein, Martin, and Icek Ajzen. 1975. Belief, Attitude, Intention, and Behavior: An Introduction to Theory and Research. Reading: Addison-Wesley. [Google Scholar]

- Geng, Lili, Huixian Hui, Xiaomeng Liang, Shaocong Yan, and Yongji Xue. 2023. Factors affecting intention toward ICT adoption in rural entrepreneurship: Understanding the differences between business types of organizations and previous experience of entrepreneurs. Sage Open 13: 21582440231197112. [Google Scholar] [CrossRef]

- Ghosh, Manimay. 2024. Empirical study on consumers’ reluctance to mobile payments in a developing economy. Journal of Science and Technology Policy Management 15: 67–92. [Google Scholar] [CrossRef]

- Hair, Joseph F., William C. Black, Barry J. Babin, and Rolph E. Anderson. 2009. Multivariate Data Analysis: A Global Perspective, 7th ed. Upper Saddle River: Prentice Hall. [Google Scholar]

- Hanafiah, Mohd Hafiz, Muhammad Aliff Asyraff, Mohd Noor Ismawi Ismail, and Juke Sjukriana. 2024. Understanding the key drivers in using mobile payment (M-Payment) among Generation Z travellers. Young Consumers, February 21. [Google Scholar]

- Handarkho, Yonathan Dri. 2021. Understanding mobile payment continuance usage in physical store through social impact theory and trust transfer. Asia Pacific Journal of Marketing and Logistics 33: 1071–87. [Google Scholar] [CrossRef]

- Hu, Li-tze, and Peter M. Bentler. 1999. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal 6: 1–55. [Google Scholar] [CrossRef]

- Katini, K., S. Amalanathan, and Kaikho Hriizhiinio. 2023. Can mobile wallet usage contribute towards environmental sustainability? Evidence from a moderated mediation approach. Universal Access in the Information Society 8: 1–17. [Google Scholar] [CrossRef]

- Ling, Pick-Soon, Kelvin Yong Ming Lee, Liing-Sing Ling, and Mohd Kamarul Anwar Mohd Suhaimi. 2024. Investors’ intention to use mobile investment: An extended mobile technology acceptance model with personal factors and perceived reputation. Cogent Business & Management 11: 2295603. [Google Scholar]

- Linge, Ashish A., Tushar Chaudhari, Baldeo B. Kakde, and Mahesh Singh. 2023. Analysis of factors affecting use behavior towards mobile payment apps: A SEM approach. Human Behavior and Emerging Technologies 2023: 3327994. [Google Scholar] [CrossRef]

- Loh, Xiu-Ming, Voon-Hsien Lee, and Lai-Ying Leong. 2023. A multi-dimensional nomological network of mobile payment continuance. Journal of Computer Information Systems 63: 1070–92. [Google Scholar] [CrossRef]

- Lu, Shiwen, and Jiseon Ahn. 2023. An empirical examination of push-pull-mooring factors influencing restaurant customers’ intention to use mobile payment: A comparison of mobile payment service types. Technology Analysis & Strategic Management 9: 1–13. [Google Scholar]

- Lu, Xuechun, and Hui Lu. 2020. Understanding Chinese millennials’ adoption intention towards third-party mobile payment. Information Resources Management Journal 33: 40–63. [Google Scholar] [CrossRef]

- Man, Siu Shing, Yingqian Guo, Alan Hoi Shou Chan, and Huiping Zhuang. 2022. Acceptance of online mapping technology among older adults: Technology acceptance model with facilitating condition, compatibility, and self-satisfaction. ISPRS International Journal of Geo-Information 11: 558. [Google Scholar] [CrossRef]

- Mastercard. 2024. Transforming Thailand to a Digital Economy. Payment and Cybersecurity Solutions. Available online: https://b2b.mastercard.com/news-and-insights/success-story/thailand-promptpay/ (accessed on 4 April 2024).

- Mollick, Joseph, Robert Cutshall, Chuleeporn Changchit, and Long Pham. 2023. Contemporary mobile commerce: Determinants of its adoption. Journal of Theoretical and Applied Electronic Commerce Research 18: 501–23. [Google Scholar] [CrossRef]

- Momani, Alaa M. 2020. The unified theory of acceptance and use of technology: A new approach in technology acceptance. International Journal of Sociotechnology and Knowledge Development 12: 79–98. [Google Scholar] [CrossRef]

- Nguyen, Luan-Thanh, Yogesh K. Dwivedi, Garry Wei-Han Tan, Eugene Cheng-Xi Aw, Pei-San Lo, and Keng-Boon Ooi. 2023. Unlocking pathways to mobile payment satisfaction and commitment. Journal of Computer Information Systems 63: 998–1015. [Google Scholar] [CrossRef]

- Nguyen, Minh Sang. 2023. Factors affecting Gen Z’s intention to use QR Pay in Vietnam after Covid-19. Innovative Marketing 19: 100. [Google Scholar]

- Nunnally, J. C. 1978. Psychometric Theory. New York: McGraw Hill. [Google Scholar]

- Phan, H., M. Tran, V. Hoang, and T. Dang. 2020. Determinants influencing customers’ decision to use mobile payment services: The case of Vietnam. Management Science Letters 10: 2635–46. [Google Scholar] [CrossRef]

- Ponsree, Khwanjira. 2024. QR code payment in Thailand 4.0 era: Expand the understanding of perceived susceptibility to COVID-19 in the TAM theory. Current Psychology 4: 1–19. [Google Scholar] [CrossRef]

- Purohit, Sonal, Rakhi Arora, and Justin Paul. 2022. The bright side of online consumer behavior: Continuance intention for mobile payments. Journal of Consumer Behaviour 21: 523–42. [Google Scholar] [CrossRef]

- Pushpa, A., C. Nagadeepa, KP Jaheer Mukthar, Hober Huaranga-Toledo, Laura Nivin-Vargas, and Matha Guerra-Muñoz. 2022. User’s Continuance Intention Towards Digital Payments: An Integrated Tripod Model DOI, TAM, TCT. In International Conference on Business and Technology. Cham: Springer International Publishing, pp. 708–17. [Google Scholar]

- Roh, Taewoo, Byung Il Park, and Shufeng Simon Xiao. 2023. Adoption of AI-enabled robo-advisors in Fintech: Simultaneous employment of UTAUT and the theory of reasoned action. Journal of Electronic Commerce Research 24: 29–47. [Google Scholar]

- Saprikis, V., G. Avlogiaris, and A. Katarachia. 2022. A comparative study of users versus non-users’ behavioral intention towards m-banking apps’ adoption. Information 13: 30. [Google Scholar] [CrossRef]

- Sharma, Shavneet, Gurmeet Singh, and Stephen Pratt. 2020. Does consumers’ intention to purchase travel online differ across generations?: Empirical evidence from Australia. Australasian Journal of Information Systems 24: 5–24. [Google Scholar] [CrossRef]

- Singh, Sindhu. 2020. An integrated model combining ECM and UTAUT to explain users’ post-adoption behaviour towards mobile payment systems. Australasian Journal of Information Systems 24: 1–27. [Google Scholar] [CrossRef]

- Abrahim Sleiman, Kamal Abubker, Lan Juanli, Hong Zhen Lei, Wenge Rong, Wang Yubo, Shunhang Li, Jingyi Cheng, and Fouzia Amin. 2023. Factors that impacted mobile-payment adoption in China during the COVID-19 pandemic. Heliyon 9: 1–12. [Google Scholar] [CrossRef]

- Sun, Sunny, Rob Law, and Markus Schuckert. 2020. Mediating effects of attitude, subjective norms and perceived behavioural control for mobile payment-based hotel reservations. International Journal of Hospitality Management 84: 102331. [Google Scholar] [CrossRef]

- Telecom Review. 2024. Progress of Thailand’s Village Broadband Internet Initiative—Telecom Review Asia Pacific. Available online: https://www.telecomreviewasia.com/news/featured-articles/4053-progress-of-thailand-s-village-broadband-internet-initiative (accessed on 5 July 2024).

- Tew, Hui-Ting, Garry Wei-Han Tan, Xiu-Ming Loh, Voon-Hsien Lee, Wei-Lee Lim, and Keng-Boon Ooi. 2022. Tapping the next purchase: Embracing the wave of mobile payment. Journal of Computer Information Systems 62: 527–35. [Google Scholar] [CrossRef]

- Tucker, Ledyard R., and Charles Lewis. 1973. A reliability coefficient for maximum likelihood factor analysis. Psychometrika 38: 1–10. [Google Scholar] [CrossRef]

- Upadhyay, Nitin, Shalini Upadhyay, Salma S. Abed, and Yogesh K. Dwivedi. 2022. Consumer adoption of mobile payment services during COVID-19: Extending meta-UTAUT with perceived severity and self-efficacy. International Journal of Bank Marketing 40: 960–91. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath. 2022. Adoption and use of AI tools: A research agenda grounded in UTAUT. Annals of Operations Research 308: 641–52. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, James Y.L. Thong, and Xin Xu. 2012. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Quarterly 36: 157–178. [Google Scholar] [CrossRef]

- Vu, Khuong, and Trung Nguyen. 2024. Exploring the contributors to the digital economy: Insights from Vietnam with comparisons to Thailand. Telecommunications Policy 48: 102664. [Google Scholar] [CrossRef]

- Wei, Min-Fang, Yir-Hueih Luh, Yu-Hsin Huang, and Yun-Cih Chang. 2021. Young generation’s mobile payment adoption behavior: Analysis based on an extended UTAUT model. Journal of Theoretical and Applied Electronic Commerce Research 16: 618–37. [Google Scholar] [CrossRef]

- Wen, Chao, Nan Wang, Jiaming Fang, and Meng Huang. 2023. An integrated model of continued m-commerce applications usage. Journal of Computer Information Systems 63: 632–47. [Google Scholar] [CrossRef]

- Widyanto, Hanif Adinugroho, Kunthi Afrilinda Kusumawardani, and Amreyzal Septyawanda. 2020. Encouraging behavioral intention to use mobile payment: An extension of Utaut2. Jurnal Muara Ilmu Ekonomi Dan Bisnis 4: 87–97. [Google Scholar] [CrossRef]

- Widyanto, Hanif Adinugroho, Kunthi Afrilinda Kusumawardani, and Helmy Yohanes. 2022. Safety first: Extending UTAUT to better predict mobile payment adoption by incorporating perceived security, perceived risk and trust. Journal of Science and Technology Policy Management 13: 952–73. [Google Scholar] [CrossRef]

- Worldometers. 2023. Available online: https://www.worldometers.info/population/ (accessed on 4 April 2024).

- Worldometers. 2024. Thailand Demographics. Worldometer. Available online: https://www.worldometers.info/demographics/thailand-demographics/ (accessed on 5 July 2024).

- Yang, Cheng-Chia, Shang-Yu Yang, and Yu-Chia Chang. 2023. Predicting older adults’ mobile payment adoption: An extended TAM model. International Journal of Environmental Research and Public Health 20: 1391. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).