Hedging Strategies in Carbon Emission Price Dynamics: Implications for Shipping Markets

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. CO2 Emission Cost

3.2. Optimal Hedge Ratio (OHR) Estimation

3.2.1. Single Instrument Optimal Hedge Ratio

3.2.2. Composite Instrument Optimal Hedge Ratio

3.3. Hedging Models

3.3.1. Ordinary Least Square (OLS) Model

3.3.2. Error Correction Model (ECM)

3.3.3. Asymmetric Dynamic Conditional Correlation (ADCC) Model

3.3.4. Student’s t-Copula (t-Copula) Model

3.4. Hedging Performance

3.4.1. Variance Reduction Hedging Effectiveness (HE)

3.4.2. Diebold–Mariano (DM) Test

4. A Case Study: CO2 Emissions and Bunker Risk Management in Shipping

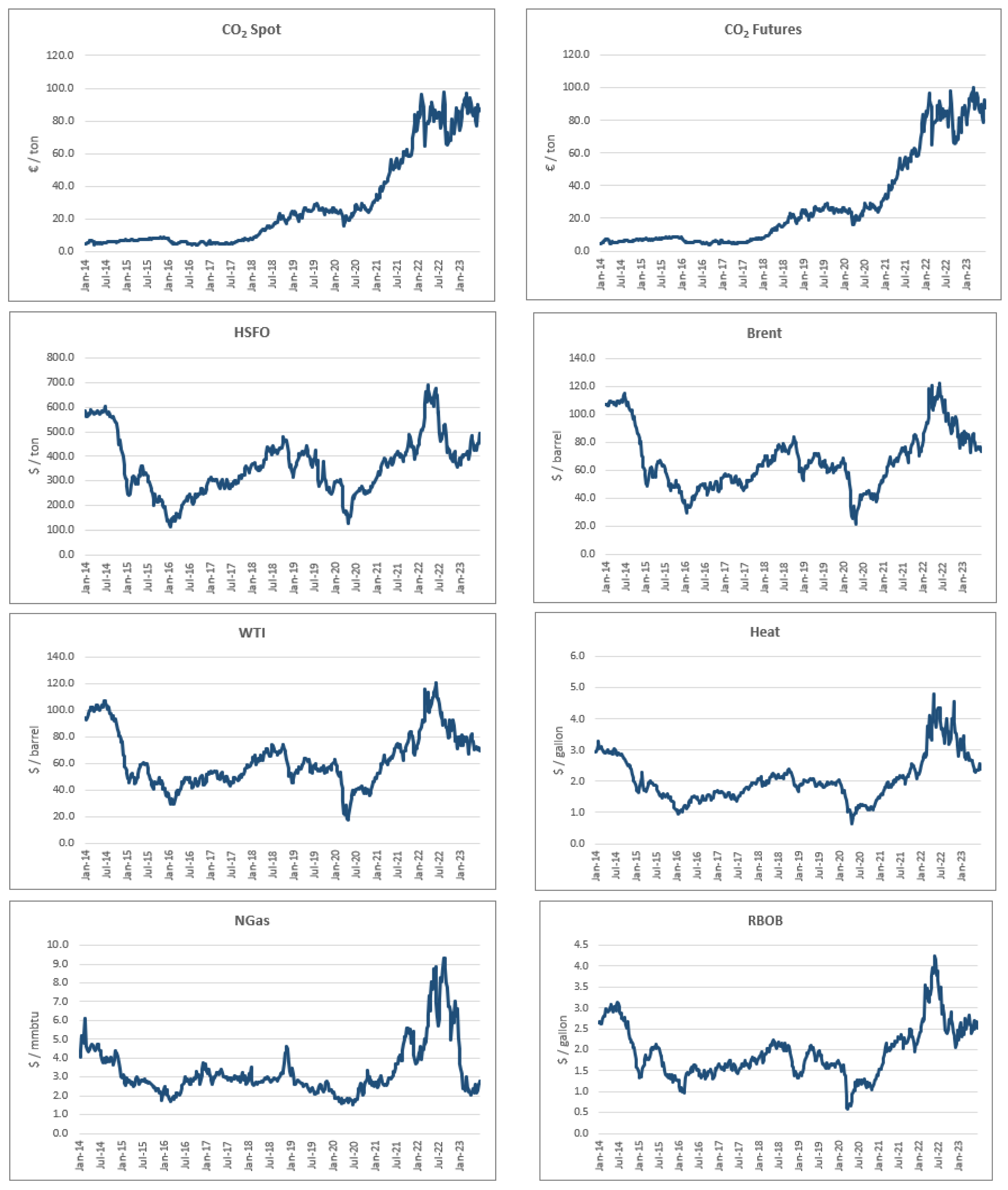

5. Data

6. Estimation Results

6.1. Single Hedging Strategy Performance

6.2. Composite Hedging Strategy Performance

6.3. Case Study on Carbon and Bunker Risk Hedging in Shipping

7. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| ADCC | Asymmetric Dynamic Conditional Correlation |

| CCER | China-certified emissions reduction |

| CCX | Chicago climate exchange |

| CER | Certified emissions reduction |

| CET | Carbon emissions trading |

| CH4 | Methane |

| CII | Carbon intensity indicator |

| CO2 | Carbon dioxide |

| DM | Diebold–Mariano test |

| DWT | Deadweight tonnage |

| EC | European Commission |

| ECM | Error correction model |

| EEA | European economic area |

| EEDI | Energy efficiency design index |

| EEXI | Energy efficiency existing ship index |

| EU | European Union |

| EU ETS | EU emissions trading scheme |

| EUA | European Union Allowances |

| GDP | Gross domestic product |

| GHG | Global greenhouse gas |

| GT | Gross tonnage |

| HE | Hedging effectiveness |

| HFLSO | Heavy-sulfur fuel oil |

| HFO | Heavy fuel oil |

| IMO | International Maritime Organization |

| JVETS | Japan voluntary emissions trading system |

| LNG | Liquified natural gas |

| MBM | Market-based measure |

| MDO | Marine diesel oil |

| MRV | Monitoring, reporting and verification |

| N2O | Nitrous oxides |

| OHR | Optimal hedging ratios |

| OLS | Ordinary least square |

| RoPax | Roll-On/Roll-Off/Passenger |

| RoRo | Roll-on/Roll-off |

| t-copula | Student’s t-copula |

| VLCC | Very large crude carrier |

References

- International Maritime Organization (IMO). Fourth IMO Greenhouse Gas Study 2020; Safe, Secure and Efficient Shipping on Clean Oceans; IMO: London, UK, 2021. [Google Scholar]

- International Maritime Organization (IMO). Study of Greenhouse Gas Emissions from Ships; IMO: London, UK, 2000. [Google Scholar]

- Sikora, A. European Green Deal—Legal and financial challenges of the climate change. ERA Forum 2021, 21, 681–697. [Google Scholar] [CrossRef]

- Ellerman, D.; Marcantonini, C.; Zaklan, A. The European Union emissions trading system: Ten years and counting. Rev. Environ. Econ. Policy 2020, 10, 89–107. [Google Scholar] [CrossRef]

- Bruninx, K.; Ovaere, M.; Delarue, E. The long-term impact of the market stability reserve on the EU Emission Trading System. Energy Econ. 2020, 89, 104746. [Google Scholar] [CrossRef]

- Ibikunle, G.; Gregoriou, A. Emissions trading in Europe: Background and policy. In Carbon Markets. Microstructure, Pricing and Policy; Ibikunle, G., Gregoriou, A., Eds.; Palgrave Macmillan: Cham, Switzerland, 2018. [Google Scholar]

- Kopsch, F. Aviation and the EU Emissions Trading Scheme—Lessons learned from previous emissions trading schemes. Energy Policy 2012, 49, 770–773. [Google Scholar] [CrossRef]

- Schinas, O.; Bergmann, N. Emissions trading in the aviation and maritime sector: Findings from a revised taxonomy. Clean. Logist. Supply Chain 2021, 1, 100003. [Google Scholar] [CrossRef]

- Regulation (EU) 2015/757 of the European Parliament and of the Council of 29 April 2015 on the Monitoring, Reporting and Verification of Carbon Dioxide Emissions from Maritime Transport, and Amending Directive 2009/16/EC (Text with EEA Relevance), Pub. L. No. 32015R0757. 2015. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32015R0757&from=EL (accessed on 30 June 2023).

- Lagouvardou, S.; Psaraftis, H.; Zis, T. A literature survey on market-based measures for the decarbonization of shipping. Sustainability 2020, 12, 3953. [Google Scholar] [CrossRef]

- Schinas, O. Financing of low-carbon technology projects. In Sustainable Energy Systems on Ships: Novel Technologies for Low Carbon Shipping; Baldi, F., Coraddu, A., Mondejar, M., Eds.; Elsevier: Amsterdam, The Netherlands, 2022. [Google Scholar]

- Eide, M.; Endresen, Ø.; Skjong, R.; Longva, T.; Alvik, S. Cost-effectiveness assessment of CO2 reducing measures in shipping. Marit. Policy Manag. 2009, 36, 367–384. [Google Scholar] [CrossRef]

- Xing, H.; Spence, S.; Chen, H. A comprehensive review on countermeasures for CO2 emissions from ships. Renew. Sustain. Energy Rev. 2020, 134, 110222. [Google Scholar] [CrossRef]

- Degiuli, N.; Martić, I.; Farkas, A.; Gospić, I. The impact of slow steaming on reducing CO2 emissions in the Mediterranean Sea. Energy Rep. 2021, 7, 8131–8141. [Google Scholar] [CrossRef]

- Lindstad, E.; Polić, D.; Rialland, A.; Sandaas, I.; Stokke, T. Decarbonizing bulk shipping combining ship design and alternative power. Ocean Eng. 2022, 266, 112798. [Google Scholar] [CrossRef]

- Gu, Y.; Wallace, S.; Wang, X. Can an Emission Trading Scheme really reduce CO2 emissions in the short term? Evidence from a maritime fleet composition and deployment model. Transp. Res. Part D 2019, 74, 318–338. [Google Scholar] [CrossRef]

- Zhu, M.; Shen, S.; Shi, W. Carbon emission allowance allocation based on a bi-level multi-objective model in maritime shipping. Ocean Coast. Manag. 2023, 241, 106665. [Google Scholar] [CrossRef]

- Christodoulou, A.; Dalaklis, D.; Ölçer, A.I.; Masodzadeh, P.G. Inclusion of shipping in the EU-ETS: Assessing the direct costs for the maritime sector using the MRV data. Energies 2021, 14, 3915. [Google Scholar] [CrossRef]

- Enderle, B. A European emissions trading scheme for the maritime sector. Aust. J. Marit. Ocean Aff. 2013, 5, 51–53. [Google Scholar] [CrossRef]

- Benz, E.; Trück, S. Modeling the price dynamics of CO2 emission allowances. Energy Econ. 2009, 31, 4–15. [Google Scholar] [CrossRef]

- Fan, Y.; Wang, X. Which sectors should be included in the ETS in the context of a unified carbon market in China? Energy Environ. 2014, 25, 613–634. [Google Scholar] [CrossRef]

- Blyth, W.; Bunn, D.; Kettunen, J.; Wilson, T. Policy interactions, risk and price formation in carbon markets. Energy Policy 2009, 37, 5192–5207. [Google Scholar] [CrossRef]

- Zeeshan, M.; Han, J.; Rehman, A.; Ullah, I.; Afridi, F.E.A.; Fareed, Z. Comparative Analysis of Trade Liberalization, CO2 Emissions, Energy Consumption and Economic Growth in Southeast Asian and Latin American Regions: A Structural Equation Modeling Approach. Front. Environ. Sci. 2022, 10, 917468. [Google Scholar] [CrossRef]

- Chen, H.; Liu, Z.; Zhang, Y.; Wu, Y. The linkages of carbon spot-futures: Evidence from EU-ETS in the third phase. Sustainability 2020, 12, 2517. [Google Scholar] [CrossRef]

- Fan, J.H.; Roca, E.; Akimov, A. Estimation and performance evaluation of optimal hedge ratios in the carbon market of the European Union Emissions Trading Scheme. Aust. J. Manag. 2014, 39, 73–91. [Google Scholar] [CrossRef]

- Philip, D.; Shi, Y. Optimal hedging in carbon emission markets using Markov switching models. J. Int. Financ. Mark. Inst. Money 2016, 43, 1–15. [Google Scholar] [CrossRef]

- Kavussanos, M.; Nomikos, N. Futures hedging when the structure of the underlying asset changes: The case of the BIFFEX contract. J. Futures Mark. 2000, 20, 775–801. [Google Scholar] [CrossRef]

- Alizadeh, A.; Huang, C.-Y.; van Dellen, S. A regime switching approach for hedging tanker shipping freight rates. Energy Econ. 2015, 49, 44–59. [Google Scholar] [CrossRef]

- Papailias, F.; Thomakos, D.; Liu, J. The Baltic Dry Index: Cyclicalities, forecasting and hedging strategies. Empir. Econ. 2017, 52, 255–282. [Google Scholar] [CrossRef]

- Alizadeh, A.; Kavussanos, M.; Menachof, D. Hedging against price fluctuation using petroleum futures contracts: Constant versus time-varying hedge ratios. Appl. Econ. 2006, 36, 1337–1353. [Google Scholar] [CrossRef]

- Alizadeh, A.; Nomikos, N. Cost of carry, causality and arbitrage between oil futures and tanker freight markets. Transp. Res. Part E Logist. Transp. Rev. 2004, 40, 297–316. [Google Scholar] [CrossRef]

- Zeng, S.H.; Jia, J.M.; Su, B.; Jiang, C.X.; Zeng, G.W. The volatility spillover effect of the European Union (EU) carbon financial market. J. Clean. Prod. 2021, 282, 124394. [Google Scholar] [CrossRef]

- Zhu, B.; Huang, L.; Yuan, L.; Ye, S.; Wang, P. Exploring the risk spillover effects between carbon market and electricity market: A bidimensional empirical mode decomposition based conditional value at risk approach. Int. Rev. Econ. Financ. 2020, 67, 163–175. [Google Scholar] [CrossRef]

- Zhang, Y.J.; Sun, Y.F. The dynamic volatility spillover between European carbon trading market and fossil energy market. J. Clean. Prod. 2019, 112, 2654–2663. [Google Scholar] [CrossRef]

- Chevallier, J. The European carbon market (2005–2007): Banking, pricing and risk-hedging strategies. In Handbook of Sustainable Energy; Galarraga, I., González-Eguino, M., Markandya, A., Eds.; Edward Elgar Publishing: Cheltenham, UK, 2011. [Google Scholar]

- Chevallier, J. Anticipating correlations between EUAs and CERs: A Dynamic Conditional Correlation GARCH model. Econ. Bull. 2011, 31, 255–272. [Google Scholar]

- Pinho, C.; Madaleno, M. Hedging with CO2 Allowances: The ECX Market; Working Paper No. 55; Departamento de Economia, Gestão e Engenharia Industrial, Universidade de Aveiro: Aveiro, Portugal, 2010. [Google Scholar]

- Psaraftis, H. Green maritime logistics: The quest for win-win solutions. Transp. Res. Procedia 2016, 14, 133–142. [Google Scholar] [CrossRef]

- Wang, K.; Fu, X.; Luo, M. Modeling the impacts of alternative emission trading schemes on international shipping. Transp. Res. Part A Policy Pract. 2015, 77, 35–49. [Google Scholar] [CrossRef]

- Miola, A.; Marra, M.; Ciuffo, B. Designing a climate change policy for the international maritime transport sector: Market-based measures and technological options for global and regional policy actions. Energy Policy 2011, 39, 5490–5498. [Google Scholar] [CrossRef]

- Franc, P.; Sutto, L. Impact analysis on shipping lines and European ports of a cap-and-trade system on CO2 emissions in maritime transport. Marit. Policy Manag. 2014, 41, 61–78. [Google Scholar] [CrossRef]

- Koesler, S.; Achtnicht, M.; Köhler, J. Course set for a cap? A case study among ship operators on a maritime ETS. Transp. Policy 2015, 37, 20–30. [Google Scholar] [CrossRef]

- Hermeling, C.; Klement, J.H.; Koesler, S.; Köhler, J.; Klement, D. Sailing into a dilemma: An economic and legal analysis of an EU trading scheme for maritime emissions. Transp. Res. Part A Policy Pract. 2015, 78, 34–53. [Google Scholar] [CrossRef]

- Gritsenko, D. Regulating GHG Emissions from shipping: Local, global, or polycentric approach? Mar. Policy 2017, 84, 130–133. [Google Scholar] [CrossRef]

- Meng, B.; Chen, S.; Haralambides, H.; Kuang, H.; Fan, L. Information spillovers between carbon emissions trading prices and shipping markets: A time-frequency analysis. Energy Econ. 2023, 120, 106604. [Google Scholar] [CrossRef]

- Balcılar, M.; Demirer, R.; Hammoudeh, S.; Nguyen, D.K. Risk spillovers across the energy and carbon markets and hedging strategies for carbon risk. Energy Econ. 2016, 54, 159–172. [Google Scholar] [CrossRef]

- Lin, B.; Chen, Y. Dynamic linkages and spillover effects between CET market, coal market and stock market of new energy companies: A case of Beijing CET market in China. Energy 2019, 172, 1198–1210. [Google Scholar] [CrossRef]

- Zhao, Y.; Zhou, Z.; Zhang, K.; Huo, Y.; Sun, D.; Zhao, H.; Sun, J.; Guo, S. Research on spillover effect between carbon market and electricity market: Evidence from Northen Europe. Energy 2023, 263, 126107. [Google Scholar] [CrossRef]

- Tan, X.; Sirichand, K.; Vivian, A.; Wang, X. How connected is the carbon market to energy and financial markets? A systematic analysis of spillovers and dynamics. Energy Econ. 2020, 90, 104870. [Google Scholar] [CrossRef]

- Jiang, C.; Wu, Y.-F.; Li, X.-L.; Li, X. Time-frequency connectedness between coal market prices, new energy stock prices and CO2 emissions trading prices in China. Sustainability 2020, 12, 2823. [Google Scholar] [CrossRef]

- Yu, L.; Li, J.; Tang, L.; Wang, S. Linear and nonlinear Granger causality investigation between carbon market and crude oil market: A multi-scale approach. Energy Econ. 2015, 51, 300–311. [Google Scholar] [CrossRef]

- Ji, Q.; Zhang, D.Y.; Geng, J.B. Information linkage, dynamic spillovers in prices and volatility between the carbon and energy markets. J. Clean. Prod. 2018, 198, 972–978. [Google Scholar] [CrossRef]

- Su, X.; Deng, C. The heterogeneous effects of exchange rate and stock market on CO2 emission allowance price in China: A panel quantile regression approach. PLoS ONE 2019, 14, 1–11. [Google Scholar] [CrossRef]

- Oestreich, M.; Tsiakas, I. Carbon missions and stock returns: Evidence from the EU Emissions Trading Scheme. J. Bank. Financ. 2015, 58, 294–308. [Google Scholar] [CrossRef]

- Graham, M.; Hasselgren, A.; Peltomäki, J. Using CO2 emission allowances in equity portfolios. In Handbook of Environmental and Sustainable Finance; Ramiah, V., Gregoriou, G.N., Eds.; Elsevier: Amsterdam, The Netherlands, 2016. [Google Scholar]

- Rannou, Y.; Boutabba, M.A.; Barneto, P. Are green bond and Carbon Markets in Europe complements or substitutes? Insights from the activity of power firms. Energy Econ. 2021, 104, 105651. [Google Scholar] [CrossRef]

- Seifert, J.; Uhrig-Homburg, M.; Wagner, M. Dynamic behavior of CO2 spot prices. J. Environ. Econ. Manag. 2008, 56, 180–194. [Google Scholar] [CrossRef]

- Alberola, E.; Chevallier, J.; Chèze, B. Price drivers and structural breaks in European carbon prices 2005–2007. Energy Policy 2008, 36, 787–797. [Google Scholar] [CrossRef]

- Rickels, W.; Proelß, A.; Geden, O.; Burhenne, J.; Fridahl, M. Integrating carbon dioxide removal into European emissions trading. Front. Clim. 2021, 3, 690023. [Google Scholar] [CrossRef]

- Bonacina, M.; Cozialpi, S. Carbon Allowances as Inputs or Financial Assets: Lesson Learned from the Pilot Phase of the EU-ETS. Available at SSRN 139217. 2009. Available online: https://www.zbw.eu/econis-archiv/handle/11159/58493 (accessed on 30 June 2023).

- Hintermann, B.; Peterson, S.; Rickels, W. Price and Market Behavior in Phase II of the EU ETS: A Review of the Literature. Rev. Environ. Econ. Policy 2016, 10, 108–128. [Google Scholar] [CrossRef]

- Mansanet-Bataller, M.; Pardo, A.; Valor, H. CO2 prices, energy and weather. Energy J. 2007, 28, 73–92. [Google Scholar] [CrossRef]

- Keppler, J.H.; Mansanet-Bataller, M. Causalities between CO2, electricity, and other energy variables during Phase I and Phase II of the EU ETS. Energy Policy 2010, 38, 3329–3341. [Google Scholar] [CrossRef]

- Bredin, D.; Muckley, C. An emerging equilibrium in the EU emissions trading scheme. Energy Econ. 2011, 33, 353–362. [Google Scholar] [CrossRef]

- Chevallier, J. Carbon futures and macroeconomic risk factors: A view from the EU ETS. Energy Econ. 2009, 31, 614–625. [Google Scholar] [CrossRef]

- Shah, M.-H.; Ullah, I.; Salem, S.; Ashfaq, S.; Rehman, A.; Zeeshan, M.; Fareed, Z. Exchange rate dynamics, energy consumption, and sustainable environment in Pakistan: New evidence from nonlinear ARDL cointegration. Front. Environ. Sci. 2022, 9, 814666. [Google Scholar] [CrossRef]

- Essandoh, O.K.; Islam, M.; Kakinaka, M. Linking international trade and foreign direct investment to CO2 emissions: Any differences between developed and developing countries? Sci. Total Environ. 2020, 712, 136437. [Google Scholar] [CrossRef]

- Zeeshan, M.; Han, J.; Rehman, A.; Ullah, I.; Afridi, F.E.A. Exploring determinants of financial system and environmental quality in high-income developed countries of the world: The demonstration of robust penal data estimation techniques. Environ. Sci. Pollut. Res. 2021, 28, 61665–61680. [Google Scholar] [CrossRef]

- Zeeshan, M.; Han, J.; Rehman, A.; Bilal, H.; Farooq, N.; Waseem, M.; Hussain, A.; Khan, M.; Ahmad, I. Nexus between foreign direct investment, energy consumption, natural resource, and economic growth in Latin American countries. Int. J. Energy Econ. Policy 2021, 11, 407–416. [Google Scholar] [CrossRef]

- Wang, Y.; Wu, C.; Yang, L. Hedging with futures: Does anything beat the naïve hedging strategy? Manag. Sci. 2015, 61, 2870–2889. [Google Scholar] [CrossRef]

- Shi, Y. Reducing greenhouse gas emissions from international shipping: Is it time to consider market-based measures? Mar. Policy 2016, 64, 123–134. [Google Scholar] [CrossRef]

- Sharma, U.; Karmakar, M. Measuring minimum variance hedging effectiveness: Traditional vs. sophisticated models. Int. Rev. Financ. Anal. 2023, 87, 102621. [Google Scholar] [CrossRef]

- Cappiello, L.; Engle, R.; Sheppard, K. Asymmetric dynamics in the correlations of global equity and bond returns. J. Financ. Econ. 2006, 4, 537–572. [Google Scholar] [CrossRef]

- Patton, A. On the out-of-sample importance of skewness and asymmetric dependence for asset allocation. J. Financ. Econ. 2004, 2, 130–168. [Google Scholar] [CrossRef]

- Patton, A. Modelling asymmetric exchange rate dependence. Int. Econ. Rev. 2006, 47, 527–556. [Google Scholar] [CrossRef]

- Kroner, K.F.; Sultan, J. Time-varying distributions and dynamic hedging with foreign currency futures. J. Financ. Quant. Anal. 1993, 28, 535–551. [Google Scholar] [CrossRef]

- Psaraftis, H.; Kontovas, C. Speed models for energy-efficient maritime transportation: A taxonomy and survey. Transp. Res. Part C Emerg. Technol. 2013, 26, 331–351. [Google Scholar] [CrossRef]

- Psaraftis, H. Market-based measures for greenhouse gas emissions from ships: A review. WMU J. Marit. Aff. 2012, 11, 211–232. [Google Scholar] [CrossRef]

- Wang, S.; Notteboom, T. The adoption of liquefied natural gas as a ship fuel: A systemic review of perspectives and challenges. Transp. Rev. 2014, 34, 749–774. [Google Scholar] [CrossRef]

- Johnson, L. The theory of hedging and speculation in commodity futures. Rev. Econ. Stud. 1960, 27, 139–151. [Google Scholar] [CrossRef]

- Lien, D.; Tse, Y.K.; Tsui, A.K. Evaluating the hedging performance of constant-correlation GARCH model. Appl. Financ. Econ. 2002, 12, 791–798. [Google Scholar] [CrossRef]

- Ghosh, A.; Clayton, R. Hedging with international stock index futures: An intertemporal error correction model. J. Financ. Res. 1996, 19, 477–491. [Google Scholar] [CrossRef]

- Sklar, A. Fonctions de répartition á n dimensions et leurs marges. Publ. L’institut Stat. L’université Paris 1959, 8, 229–231. [Google Scholar]

- Frees, E.; Valdez, E. Understanding relationship using copulas. N. Am. Actuar. J. 1998, 2, 1–25. [Google Scholar] [CrossRef]

- Embrechts, P.; Lidskog, F.; McNeal, A. Modelling dependence with copulas and applications to risk management. In Handbook of Heavy Tailed Distributions in Finance; Rachev, S., Ed.; Elsevier: Amsterdam, The Netherlands, 2003. [Google Scholar]

- Ederington, L.H. The hedging performance of the new futures markets. J. Financ. 1979, 34, 157–170. [Google Scholar] [CrossRef]

- Diebold, F.X.; Mariano, R. Comparing predictive accuracy. J. Bus. Econ. Stat. 1995, 13, 253–263. [Google Scholar]

- Cummins, M. EU ETS market interactions: The case for multiple hypothesis testing approaches. Appl. Energy 2013, 111, 701–709. [Google Scholar] [CrossRef]

- Batten, J.A.; Kinateder, H.; Szilagyi, P.G.; Wagner, N.F. Hedging stocks with oil. Energy Econ. 2021, 93, 104422. [Google Scholar] [CrossRef]

- Jarque, C.M.; Bera, A.K. Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Econ. Lett. 1980, 6, 255–259. [Google Scholar] [CrossRef]

- Phillips, P.C.; Perron, P. Testing for a unit root in time series regression. Biometrika 1988, 75, 335–346. [Google Scholar] [CrossRef]

- Lien, D. A not on the superiority of the OLS hedge ratio. J. Futures Mark. 2005, 25, 1121–1126. [Google Scholar] [CrossRef]

- Čech, F.; Zítek, M. Marine fuel hedging under the sulfur cap regulations. Energy Econ. 2022, 112, 106204. [Google Scholar] [CrossRef]

- Regulation (EU) 2023 of the European Parliament and of the Council of 13 July 2023 on the Use of Renewable and Low-Carbon Fuels in Maritime Transport and Amending Directive 2009/16/EC (Text with EEA Relevance), Under Publication. 2023. Available online: https://www.europarl.europa.eu/doceo/document/A-9-2022-0233_EN.html (accessed on 30 June 2023).

{kind=link}

| Fuel Type | Emission Factor (MT CO2/MT Fuel Consumption) |

|---|---|

| Heavy fuel oil (HFO) | 3.114 |

| Marine diesel oil (MDO) | 3.206 |

| Liquified Natural Gas (LNG) | 2.750 |

| Voyage 1 | Voyage 2 | Voyage 3 | ||

|---|---|---|---|---|

| Vessel specifications | ||||

| Vessel type | VLCC | Suezmax | Capesize | |

| Dwt | 318,000 | 157,000 | 180,000 | |

| Speed (knots) | Laden | 12.5 | 12.5 | 12 |

| Ballast | 12 | 12 | 13 | |

| Consumption at sea (tons/day) | Laden | 67 | 45 | 43 |

| Ballast | 51 | 35 | 43 | |

| Voyage assumptions (at sea) | ||||

| Trading route | Ras Tanura– Rotterdam | Houston– Rotterdam | Tubarao– Rotterdam | |

| Voyage distance (miles) | Laden | 11,289 | 5041 | 11,289 |

| Ballast | 4475 | 5041 | 4475 | |

| Sea time (days) | 55.9 | 36.0 | 38.1 | |

| Voyage assumptions (in ports) | ||||

| Port time (days) | 4 | 4 | 6.5 | |

| Consumption in port (tons/day) | 5 | 5 | 5 | |

| Algorithm | Description |

|---|---|

| Hedging instruments data input (at time t): CO2 future price, petroleum futures prices | At time t, the shipowner fixes a voyage charter contract for a shipment at time t + n. To hedge his exposure to the CO2 and bunker cost, he decides to buy the forward CO2 and petroleum hedging instruments contracts in order to lock his CO2 allowance and bunker prices. |

| Hedge ratios (at time t): Econometric model estimations for the hedge ratios | The number of future contracts for hedging CO2 and bunker cost for both the fronthaul and backhaul voyages are determined using the results of the hedge ratios that the econometric models have estimated using the market return data over the period from t − 361 to t (estimation window). |

| Hedging effectiveness assessment (at time t + n): Estimation of the variance reduction hedging effectiveness and Diebold–Mariano tests | The out-of-sample hedging effectiveness is assessed at time t + n, comparing the variance of hedged portfolio across the different econometric models, as well as the reduction in the variance of the hedged portfolio relative to the unhedged portfolio. |

| Voyage completion and idle time before a new voyage will be fixed | The vessel has returned to the loading ports and is waiting a period of 7 days before a new voyage will be fixed for a shipment that will take place 1 month later. |

| CO2 Spot | CO2 Futures | HSFO | Brent | WTI | Heating | NGas | RBOB | |

|---|---|---|---|---|---|---|---|---|

| Panel A. Price level | ||||||||

| Mean | 28.209 | 28.434 | 361.23 | 67.662 | 62.924 | 2.0763 | 3.3316 | 1.9470 |

| S.D. | 28.139 | 28.518 | 120.37 | 21.334 | 20.486 | 0.7356 | 1.4260 | 0.6293 |

| Max | 97.580 | 99.800 | 688.75 | 122.01 | 120.67 | 4.7817 | 9.3360 | 4.2522 |

| Min | 4.0800 | 4.0800 | 112.00 | 21.440 | 16.940 | 0.6467 | 1.4950 | 0.5737 |

| Skewness | 1.1423 | 1.1589 | 0.4339 | 0.5608 | 0.6427 | 0.9967 | 1.8929 | 0.8355 |

| Kurtosis | 2.8638 | 2.9123 | 2.7912 | 2.6660 | 2.8307 | 3.8228 | 6.8166 | 3.7266 |

| J-B | 108.24 * | 111.18 * | 16.466 * | 28.305 * | 34.735 * | 96.111 * | 597.25 * | 68.617 * |

| PP test | 0.8219 | 0.8629 | −0.9284 | −1.0760 | −0.9488 | −0.9001 | −1.1540 | −0.6248 |

| Panel B: Logarithmic returns | ||||||||

| Mean | 0.0059 | 0.0059 | −4.413 × 10−4 | −7.184 × 10−4 | −5.763 × 10−4 | −3.694 × 10−4 | −8.699 × 10−4 | −1.131 × 10−5 |

| S.D. | 0.0653 | 0.0654 | 0.0580 | 0.0546 | 0.0578 | 0.0557 | 0.0742 | 0.0611 |

| Max | 0.2427 | 0.2356 | 0.2513 | 0.3135 | 0.2758 | 0.2816 | 0.2184 | 0.2703 |

| Min | −0.3495 | −0.3510 | −0.3473 | −0.2907 | −0.3469 | −0.3912 | −0.2860 | −0.4348 |

| Skewness | −0.7165 | −0.7236 | −0.5316 | −0.2276 | −0.4483 | −0.5424 | −0.4760 | −0.9383 |

| Kurtosis | 6.9247 | 6.8112 | 8.8219 | 8.6431 | 8.3365 | 10.4583 | 4.3414 | 12.5385 |

| J-B | 360.04 * | 342.77 * | 722.38 * | 661.07 * | 603.95 * | 1.171 × 103 * | 55.801 * | 1.949 × 103 * |

| PP test | −22.491 * | −22.541 * | −20.263 * | −20.603 * | −19.035 * | −22.693 * | −22.529 * | −20.404 * |

| Variance | HE | DM | |||

|---|---|---|---|---|---|

| ECM | ADCC | t-Copula | |||

| Unhedged | 0.4453 | ||||

| OLS | 0.0024 | 99.471 | −0.1598 | −2.6402 *** | −4.3980 *** |

| EC | 0.0024 | 99.470 | −2.6392 *** | −4.4023 *** | |

| ADCC | 0.0079 | 98.233 | 2.0795 ** | ||

| t-copula | 0.0035 | 99.212 | |||

| Panel A. Carbon and Brent | ||||||||

| OLS | ECM | ADCC | t-copula | |||||

| Carbon | Brent | Carbon | Brent | Carbon | Brent | Carbon | Brent | |

| Mean | 1.0444 | 0.5667 | 1.0218 | 0.5400 | 1.2152 | 0.1503 | 1.0037 | 0.1616 |

| Variance | 0.0021 | 0.0037 | 0.0006 | 0.0021 | 0.1294 | 0.0054 | 0.0023 | 0.0158 |

| Max | 1.1274 | 0.7044 | 1.0794 | 0.6523 | 2.4910 | 0.3695 | 1.1817 | 0.6858 |

| Min | 0.9588 | 0.4883 | 0.9684 | 0.4767 | 0.4519 | 0.0008 | 0.8076 | 0.0009 |

| Panel B. Carbon and WTI | ||||||||

| OLS | ECM | ADCC | t-copula | |||||

| Carbon | WTI | Carbon | WTI | Carbon | WTI | Carbon | WTI | |

| Mean | 1.0625 | 0.4579 | 1.0432 | 0.4105 | 1.2355 | 0.1399 | 1.0309 | 0.1324 |

| Variance | 0.0024 | 0.0069 | 0.0012 | 0.0058 | 0.1303 | 0.0046 | 0.0021 | 0.0078 |

| Max | 1.1428 | 0.6347 | 1.0966 | 0.5721 | 2.5015 | 0.3998 | 1.2110 | 0.5320 |

| Min | 0.9687 | 0.3720 | 0.9675 | 0.3439 | 0.4709 | 0.0108 | 0.8201 | 0.0023 |

| Panel C. Carbon and Heat | ||||||||

| OLS | ECM | ADCC | t-copula | |||||

| Carbon | Heat | Carbon | Heat | Carbon | Heat | Carbon | Heat | |

| Mean | 1.0677 | 0.6272 | 1.0466 | 0.6340 | 1.2370 | 0.1469 | 1.0271 | 0.1394 |

| Variance | 0.0035 | 0.0139 | 0.0021 | 0.0086 | 0.1274 | 0.0067 | 0.0023 | 0.0188 |

| Max | 1.1709 | 0.7976 | 1.1325 | 0.7632 | 2.4789 | 0.5692 | 1.1998 | 1.1705 |

| Min | 0.9635 | 0.3878 | 0.9599 | 0.4433 | 0.4675 | 0.0000 | 0.8174 | 0.0003 |

| Panel D. Carbon and NGas | ||||||||

| OLS | ECM | ADCC | t-copula | |||||

| Carbon | NGas | Carbon | NGas | Carbon | NGas | Carbon | NGas | |

| Mean | 1.1125 | 0.1081 | 1.1120 | 0.1234 | 1.2816 | 0.1349 | 1.0911 | 0.0832 |

| Variance | 0.0034 | 0.0008 | 0.0023 | 0.0008 | 0.1387 | 0.0068 | 0.0032 | 0.0091 |

| Max | 1.1956 | 0.1676 | 1.1786 | 0.1839 | 2.6309 | 0.7448 | 1.3121 | 0.7164 |

| Min | 0.9932 | 0.0570 | 1.0082 | 0.0662 | 0.5130 | 0.0000 | 0.8452 | 0.0002 |

| Panel D. Carbon and RBOB | ||||||||

| OLS | ECM | ADCC | t-copula | |||||

| Carbon | RBOB | Carbon | RBOB | Carbon | RBOB | Carbon | RBOB | |

| Mean | 1.0338 | 0.4318 | 1.0126 | 0.4193 | 1.2230 | 0.1235 | 1.0143 | 0.1009 |

| Variance | 0.0012 | 0.0006 | 0.0006 | 0.0005 | 0.1306 | 0.0049 | 0.0013 | 0.0054 |

| Max | 1.1007 | 0.4954 | 1.0560 | 0.4918 | 2.4758 | 0.4515 | 1.1520 | 0.3363 |

| Min | 0.9690 | 0.3924 | 0.9578 | 0.3765 | 0.4649 | 0.000 | 0.8174 | 0.0002 |

| Panel A. Variance | |||||

| Unhedged | OLS | EC | ADCC | t-Copula | |

| Carbon + Brent | 1.0148 | 0.2996 | 0.2926 | 0.4465 | 0.3659 |

| Carbon + WTI | 0.3348 | 0.3286 | 0.4568 | 0.3640 | |

| Carbon + Heating | 0.3254 | 0.3355 | 0.4523 | 0.3615 | |

| Carbon + NGas | 0.3869 | 0.3857 | 0.5127 | 0.3814 | |

| Carbon + RBOB | 0.3127 | 0.3135 | 0.4665 | 0.3693 | |

| Panel B. Hedge effectiveness (HE) | |||||

| OLS | EC | ADCC | t-copula | ||

| Carbon + Brent | 70.4736 | 71.1625 | 55.9997 | 63.9394 | |

| Carbon + WTI | 67.0082 | 67.6192 | 54.9862 | 64.1319 | |

| Carbon + Heating | 67.9312 | 66.9398 | 55.4290 | 64.3771 | |

| Carbon + NGas | 61.8748 | 61.9937 | 49.4722 | 62.4104 | |

| Carbon + RBOB | 69.1805 | 69.1105 | 54.0301 | 63.6047 | |

| Panel C. DM test | |||||

| EC | ADCC | t-copula | |||

| Carbon + Brent | OLS | 0.6671 | −2.3418 *** | −1.1966 | |

| EC | −2.7273 *** | −1.5238 * | |||

| ADCC | 1.9243 ** | ||||

| Carbon + WTI | OLS | 0.8218 | −2.3587 *** | −0.6912 | |

| EC | −2.7029 *** | −0.9839 | |||

| ADCC | 2.3083 ** | ||||

| Carbon + Heating | OLS | −3.0267 *** | −2.2895 ** | −0.9196 | |

| EC | −2.1343 ** | −0.6753 | |||

| ADCC | 2.3150 ** | ||||

| Carbon + NGas | OLS | 0.6592 | −3.2964 *** | 0.8039 | |

| EC | −3.2308 *** | 0.6533 | |||

| ADCC | 3.2325 *** | ||||

| Carbon + RBOB | OLS | −0.2938 | −3.0501 *** | −1.4213 | |

| EC | −3.0709 *** | −1.4392 | |||

| ADCC | 2.2526 ** | ||||

| Panel A. VLCC—Voyage: Ras Tanura–Rotterdam | |||||||

| Carbon | Bunker | Total | |||||

| Unhedged voyages | Variance | 2.2175 | 2.43314 | 2.1542 | |||

| Mean | 271,208 | 1,179,158 | 1,450,367 | ||||

| Max | 496,913 | 2,067,189 | 2,532,195 | ||||

| Min | 110,551 | 710,369 | 851,310 | ||||

| Total | 4,339,333 | 18,866,532 | 23,205,866 | ||||

| OLS | t-copula | ||||||

| Carbon | Bunker | Total | Carbon | Bunker | Total | ||

| Hedged voyages (Carbon + Brent) | Variance | 0.2603 | 1.3513 | 0.9999 | 0.3939 | 2.2920 | 1.5813 |

| HE | 88.260 | 44.462 | 53.580 | 82.236 | 5.7976 | 26.592 | |

| Mean | 265,797 | 1,162,924 | 1,428,721 | 255,484 | 1,173,514 | 1,428,998 | |

| Min | 508,345 | 2,200,648 | 2,666,039 | 499,873 | 2,087,008 | 2,537,307 | |

| Max | 110,837 | 630,828 | 741,665 | 102,207 | 706,124 | 808,330 | |

| Total | 4,252,751 | 18,606,786 | 22,859,537 | 4,087,739 | 18,776,223 | 22,863,962 | |

| Hedged voyages (Carbon + Heat) | Variance | 0.4308 | 1.2293 | 0.9381 | 0.4176 | 2.2305 | 1.5637 |

| HE | 80.572 | 49.476 | 56.452 | 81.164 | 8.3268 | 27.409 | |

| Mean | 272,977 | 1,169,663 | 1,442,640 | 261,770 | 1,174,997 | 1,436,767 | |

| Min | 533,848 | 2,104,226 | 2,591,232 | 515,962 | 2,069,378 | 2,535,162 | |

| Max | 113,449 | 626,033 | 739,482 | 108,031 | 705,680 | 813,711 | |

| Total | 4,367,633 | 18,714,604 | 23,082,237 | 4,188,314 | 18,799,950 | 22,988,265 | |

| Panel B. Suezmax—Voyage: Houston–Rotterdam | |||||||

| Carbon | Bunker | Total | |||||

| Unhedged voyages | Variance | 1.7432 | 0.8898 | 0.6700 | |||

| Mean | 115,967 | 513,349 | 629,317 | ||||

| Max | 209,397 | 902,939 | 1,090,775 | ||||

| Min | 47,495 | 210,995 | 260,340 | ||||

| Total | 2,435,313 | 10,780,337 | 13,215,650 | ||||

| OLS | t-copula | ||||||

| Carbon | Bunker | Carbon | Bunker | Carbon | Bunker | ||

| Hedged voyages (Carbon+ Brent) | Variance | 0.2579 | 0.6244 | 0.4785 | 0.3248 | 0.8442 | 0.5790 |

| HE | 85.200 | 29.829 | 28.588 | 81.364 | 5.1347 | 13.5785 | |

| Mean | 114,507 | 507,677 | 622,184 | 109,786 | 512,509 | 622,295 | |

| Min | 220,527 | 935,925 | 1,097,048 | 209,484 | 914,616 | 1,080,941 | |

| Max | 45,908 | 237,436 | 286,932 | 45,609 | 212,027 | 261,164 | |

| Total | 2,404,649 | 10,661,211 | 13,065,860 | 2,305,499 | 10,762,691 | 13,068,190 | |

| Hedged voyages (Carbon + Heat) | Variance | 0.4235 | 0.9722 | 0.7206 | 0.3224 | 0.7758 | 0.5279 |

| HE | 75.7020 | 0.000 | 0.000 | 81.5032 | 12.8159 | 21.215 | |

| Mean | 117,565 | 504,046 | 621,610 | 112,096 | 513,183 | 625,279 | |

| Min | 229,205 | 947,781 | 1,111,963 | 212,113 | 917,521 | 1,095,771 | |

| Max | 46,094 | 223,326 | 273,580 | 46,259 | 226,961 | 277,405 | |

| Total | 2,468,857 | 10,584,962 | 13,053,819 | 2,354,016 | 10,776,838 | 13,130,854 | |

| Panel C. Capesize—Voyage: Tubarao–Rotterdam | |||||||

| Carbon | Bunker | Total | |||||

| Unhedged voyages | Variance | 1.7432 | 0.8898 | 0.6700 | |||

| Mean | 115,967 | 513,349 | 629,317 | ||||

| Max | 209,397 | 902,939 | 1,090,775 | ||||

| Min | 47,495 | 210,995 | 260,340 | ||||

| Total | 2,435,313 | 10,780,337 | 13,215,650 | ||||

| OLS | t-copula | ||||||

| Carbon | Bunker | Carbon | Bunker | Carbon | Bunker | ||

| Hedged voyages (Carbon+ Brent) | Variance | 0.2579 | 0.6244 | 0.4785 | 0.3248 | 0.8442 | 0.5790 |

| HE | 85.200 | 29.829 | 28.588 | 81.364 | 5.1347 | 13.5785 | |

| Mean | 114,507 | 507,677 | 622,184 | 109,786 | 512,509 | 622,295 | |

| Min | 220,527 | 935,925 | 1,097,048 | 209,484 | 914,616 | 1,080,941 | |

| Max | 45,908 | 237,436 | 286,932 | 45,609 | 212,027 | 261,164 | |

| Total | 2,404,649 | 10,661,211 | 13,065,860 | 2,305,499 | 10,762,691 | 13,068,190 | |

| Hedged voyages (Carbon + Heat) | Variance | 0.4235 | 0.9722 | 0.7206 | 0.3224 | 0.7758 | 0.5279 |

| HE | 75.7020 | 0.000 | 0.000 | 81.5032 | 12.8159 | 21.215 | |

| Mean | 117,565 | 504,046 | 621,610 | 112,096 | 513,183 | 625,279 | |

| Min | 229,205 | 947,781 | 1,111,963 | 212,113 | 917,521 | 1,095,771 | |

| Max | 46,094 | 223,326 | 273,580 | 46,259 | 226,961 | 277,405 | |

| Total | 2,468,857 | 10,584,962 | 13,053,819 | 2,354,016 | 10,776,838 | 13,130,854 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Syriopoulos, T.; Roumpis, E.; Tsatsaronis, M. Hedging Strategies in Carbon Emission Price Dynamics: Implications for Shipping Markets. Energies 2023, 16, 6396. https://doi.org/10.3390/en16176396

Syriopoulos T, Roumpis E, Tsatsaronis M. Hedging Strategies in Carbon Emission Price Dynamics: Implications for Shipping Markets. Energies. 2023; 16(17):6396. https://doi.org/10.3390/en16176396

Chicago/Turabian StyleSyriopoulos, Theodoros, Efthymios Roumpis, and Michael Tsatsaronis. 2023. "Hedging Strategies in Carbon Emission Price Dynamics: Implications for Shipping Markets" Energies 16, no. 17: 6396. https://doi.org/10.3390/en16176396

APA StyleSyriopoulos, T., Roumpis, E., & Tsatsaronis, M. (2023). Hedging Strategies in Carbon Emission Price Dynamics: Implications for Shipping Markets. Energies, 16(17), 6396. https://doi.org/10.3390/en16176396