Abstract

Recent decades have witnessed an unprecedented demand for corporate sustainability. Driven by a desire to remain competitive amidst economic turmoil and climate change, organisations are embedding sustainable measures into their long-term goals and strategies. Despite such progress, corporate sustainability is taking longer than anticipated, and to understand the reasons behind the delay, this research employs a systematic literature review to identify and categorise the key barriers to the adoption of corporate sustainability. A collection of barriers from 56 articles is established, totalling 90 unique barriers grouped into six main categories. The findings reveal that corporate sustainability is highly complex, emphasising the need for a transdisciplinary approach that incorporates various theoretical frameworks. The findings will be a general guide for any organisation to prepare itself for tackling sustainability barriers while equipping policymakers in developing policies aimed at reducing their magnitude. Equally, it will provide insights to institutions of higher learning on the significance of cross-industry cooperation to ensure skill gaps are addressed at earlier stages and aligned with organisational needs.

1. Introduction

The 21st century has been characterised by a continuous shift in focus to corporations in the sustainability debate, especially larger ones, as the public perceives them to be responsible for the negative environmental and societal impacts facing them (Lozano, 2014, 2015; Lozano & Barreiro-Gen, 2023; Lozano et al., 2015). To counter the trend, many organisations are recognising the interdependencies between the environmental, economic, and social dimensions of their activities (Lozano et al., 2015; Rosati & Faria, 2019; Kücükgül et al., 2022). Organisations are increasingly embedding sustainability as a strategic priority for products and service innovations to align their vision with the UN sustainable development goals (SDGs) promoting corporate sustainability (CS) (Kücükgül et al., 2022; Ceschin, 2013; Lozano, 2012). Dyllick and Hockerts define CS as meeting the needs of a firm’s (company or business) direct and indirect stakeholders without compromising its ability to meet the needs of future stakeholders (Rosati & Faria, 2019; Dyllick & Hockerts, 2002). This can be translated as value creation across economic, social, and environmental fronts by organisations both for present and for future generations (Moursellas et al., 2024). Creating a balance between the organisation’s main goal (profit) and the environment and its stakeholders’ needs (Ashrafi et al., 2018, 2019). Research posits that the level of willingness of stakeholders is more likely to influence how organisations implement their sustainability vision (Lopes de Sousa Jabbour et al., 2020).

To ensure these organisations are competitive and sustainable, a vast majority are embarking on a journey characterised by radical changes, which in most instances involves challenges of coping with the already established operational tactics (Ceschin, 2013; Tukker & Tischner, 2006). This is a multifaceted journey, as organisations view the associated changes as complex in comparison to their traditional ways of operation, while their consumers are tied to their cultural inertia, making them consider these changes as valueless (O. K. Mont, 2002). However, adopting holism with regard to organisational contextual factors is significant in overcoming the associated challenges (Lozano, 2012, 2014, 2015; Steger et al., 2007; Linnenluecke & Griffiths, 2010).

As sustainability continues to dominate the public debate, an increased desire for environmentally and socially ethical products and services by stakeholders is leading the demand side, whereas investors are pushing for sustainable organisations to establish business models that are resilient and adaptive to risks as a cushion against future financial shocks (Lozano & Barreiro-Gen, 2023; Pajunen et al., 2016). This trend has attracted considerable interest from scholars, policymakers, and the public, trying to understand the complexity of the interactions (Battaglia et al., 2016). However, achieving a balance between organisational demands and constrained resources remains a pertinent challenge on the path to sustainability (Lopes de Sousa Jabbour et al., 2020; Pajunen et al., 2016; Montiel & Delgado-Ceballos, 2014; Ebrahimi & Koh, 2021). Understanding the associated challenges is critical for advancing both theoretical and practical knowledge in corporate sustainability.

Due to the variety of sustainability initiatives, managers are realising that integrating sustainability is a tactical opportunity that can leverage their performance (Battaglia et al., 2016; Bux et al., 2020). A strategic move characterised by exponential growth in environmental consciousness, accompanied by a widespread adoption of terminologies such as “net zero”, “eco-efficiency”, “environmentally friendly”, “socially responsible”, “green washing”, and “circular economy”, clearly indicates how sustainability is taking a centre role in organisational decision making (Moursellas et al., 2024; Free et al., 2024; Ikram et al., 2020; Heras-Saizarbitoria et al., 2022). Unfortunately, the proliferation of frameworks, reporting standards, regulations, and metrics for quantifying sustainability has created confusion for organisations about how best to proceed and which methods to implement rendering sustainability as a barrier (Lozano, 2015; Bebic et al., 2024). Organisational pressures to meet set targets have led to circumvention of sustainability reporting requirements, rendering the process deceptive, with reduced urgency and rigour given to sustainability commitments compared to other business objectives (Broccardo et al., 2023; Nikula, 2022).

Whilst trends such as embedding sustainability in vision statements, promoting eco-efficiency measures, and the enactment of the triple bottom line, reporting standards are increasingly visible in public materials (Filho et al., 2022; Basit et al., 2024) and with public pressure and demand for sustainable products forcing sustainability higher on the agenda, numerous barriers and competing priorities continue to hinder progress (Moursellas et al., 2024; Filho et al., 2022; Basit et al., 2024; Bocken & Geradts, 2020; George et al., 2016; Khatter et al., 2021; de Paiva Duarte, 2015; Macintyre et al., 2020; Jarrah et al., 2024). Unlocking the potential for CS calls for a clear understanding of these barriers and balancing environmental, social, and economic goals while closing the gap between intentions (targets) and achievements (impacts) (de Paiva Duarte, 2015). Failure to identify barriers can lead to a cycle that cannot identify the corrective actions in achieving positive sustainable outcomes (Filho et al., 2022; Basit et al., 2024).

Previous studies have provided a detailed series of theoretical constructs to analyse CS from a broader lens. The existing literature has been linked to agency theory (S. Li et al., 2021), theory of resource dependency (Lopes de Sousa Jabbour et al., 2020; Liu et al., 2023), institutional theory (Rosati & Faria, 2019; Ebrahimi & Koh, 2021; Filho et al., 2022; Kelling et al., 2021), triple-bottom-line theory (Hubbard, 2009), theory of political costs (Milne, 2002), strategic foresight theory (Demneh et al., 2023), theory of legitimacy (Benvenuto et al., 2023), signal, and the upper echelons theory (Benvenuto et al., 2023; Abatecola & Cristofaro, 2020; Friske et al., 2023) to explain the complexity of organisational sustainability. However, much of this work focuses on the drivers for sustainability, with barriers discussed shallowly (Lozano, 2015; Broccardo et al., 2023; Nikula, 2022; Bocken & Geradts, 2020; Khatter et al., 2021; Benvenuto et al., 2023; Carmo et al., 2023; Mattia et al., 2021; Zhao et al., 2022). Fewer studies have explicitly discussed the barriers as either internal or external. However, there exists no clear delineation to define these barriers, since the desire to address the transitional phase arises, imposing a barrier. Moreover, the complex nature of institutions and stakeholders cannot be separated and must be addressed as a system to ensure a unified approach to these barriers. Some of the widely discussed barriers, though not limited to these, include the managerial approaches, as well as financial, technical, regulatory, and cognitive barriers (Moursellas et al., 2024; S. Li et al., 2021; Kong, 2013; Tsang et al., 2023; Rodriguez-Fernandez, 2016; Kuppig et al., 2016).

There is an increased concern from academia, policymakers, and decisionmakers on how to make organisations more sustainable. Several studies have pointed out the need to adjust the existing university curriculum to align it with the business needs and integrate sustainability into this coursework (Lozano et al., 2015; Bux et al., 2020; Barber et al., 2014). By doing so, this has the potential to address the existing skill gap, especially with the new dynamics of sustainability. Different dimensions of corporate sustainability have been identified across the literature, with compliance, transparency, trust, an inadequate skill set, the value of sustainability and methodological issues on reporting, and the quantification of sustainability highlighted as issues of concern (Lozano & Barreiro-Gen, 2023; Lozano et al., 2015; Ceschin, 2013; Moursellas et al., 2024; Benvenuto et al., 2023; Blanco-Portela et al., 2017; Ceschin & Vezzoli, 2010). From this literature review, we draw a list of barriers and group them into main barriers that can be addressed from a policy perspective, as further presented in Table 1. Building on the study objective, this research aims to identify the primary barriers to CS and how to strategically transform and align them with organisational sustainability objectives. By addressing this question, this study seeks to bridge the gap between sustainability intentions and outcomes, providing a detailed analysis of the structural, cultural, and economic challenges organisations face in their sustainability journey. This will act as a general guide for any organisation to prepare itself for tackling sustainability barriers. Equally, it will also equip policymakers in developing policies aimed at reducing the magnitude of these barriers. Additionally, it will provide insights to the institutions of higher learning on the significance of cross-industry cooperation to ensure skill gaps are addressed at earlier stages and aligned with organisational needs.

Table 1.

A list of corporate sustainability barriers gathered from the literature.

To answer the research question, a systematic literature review was conducted with the aim of developing an in-depth (unitary and compact) understanding of CS in a multi-theory context and presenting the barriers to organisational sustainability. The study considers CS studies from 2010 to 2024 to ensure it captures the most up-to-date developments in academia.

Finally, it is observed that corporate sustainability barriers are highly complex and strongly interdependent, which in turn requires a holistic approach to ensure a multi-actor approach is in place when addressing these barriers. In this sense, due to the broadness of CS, this research was delimited from interviewing corporate organisations to get a glimpse of the actual challenges. More details on this delimitation can be found in Section 4 (Discussion). Besides this introduction, the present research is organised into four sections. The next section contemplates on the research methodology. Section 3 addresses the broad thematic areas derived from the SLR; Section 4 addresses the discussions and directions for future research. Finally, Section 5 describes the conclusions of the study followed by bibliographic references.

2. Methods

The research adopted a systematic literature review (SLR) which is a tool for identifying key trends or findings to complex and highly fragmented theoretical backgrounds (Broccardo et al., 2023; Benvenuto et al., 2023). To conduct a replicable SLR, Tranfield et al. (2003) recommends that accurate planning execution and planning is a prerequisite (Tranfield et al., 2003). Equally, SLR was chosen based on the basic principles of being systematic, transparent, replicable, and synthesisable (Broccardo et al., 2023; Benvenuto et al., 2023; Tranfield et al., 2003; Engert et al., 2016). SLR has the capacity to provide a framework for a rigorous and well-planned analysis responding to the specific research questions through the identification, selection, and critical evaluation of study results shortlisted from the identified extant literature (Tranfield et al., 2003).

In line with SLR, the steps highlighted in (Broccardo et al., 2023; Benvenuto et al., 2023) followed the following approach:

- Identification of the research question—What are the main barriers to corporate sustainability implementation?

- Database selection—Scopus and Web of Science database were selected for data extraction.

- Identification of search words—Relevant key words were defined following the Benvenuto et al. (2023) prescriptions in reviewing the determinants for sustainability reporting systems to examine the barriers to CS implementation. The search criteria applied was ((organisation* OR firm* OR entity* OR business*) AND (sustainability* OR sustainable* OR Corporate sustainability*) AND (Barriers* OR obstacles* OR Drivers*) AND (Green economy* OR supply AND chain* OR value AND chain*).

- Database search, inclusion, and exclusion—After the database search, all articles that were not published in business, management, and environmental journals were excluded. A total of 2709 articles were recorded. Similarly, any article not published in English language was excluded from the list. Further exclusion criteria were applied to articles under processing and only published articles in reviewed journals were incorporated in the list. Book chapters, conference proceedings, and online publications were also excluded. Studies published between 2010 and 2024 were selected to ensure the most up-to-date barriers across corporate sustainability implementation were identified.

- Duplicates removal—Duplicates from both databases were manually removed. There was a wide range of similarity of the articles found from both databases because of journal indexing and the inclusion criteria of only published articles.

- Analysis—A total of 307 articles passed the exclusion and inclusion criteria. To ensure the articles were relevant to the context, a thorough abstract and title overview was carried out over the 308 articles and to ensure the content of those articles that were vaguely loose were further excluded. A total number of 56 articles were reviewed for this study and all the barriers highlighted in each are presented in Table 1.

- The analyses of the reviewed articles were scrutinised and all the barriers listed in the articles were listed in Table 1. The collected list of barriers was further scrutinised to remove duplicates and the same barriers. A total of 90 unique barriers were identified and were grouped into six clusters, as summarised in Table 2 and discussed in the Results section.

Table 2. List of unique barriers derived from the literature collection and their main grouping.

- Thematic analysis—Synthesising the individual barriers identified in Table 1 and the literature reviewed resulted in a wide range of propositions (list of barriers). Discussing the 90 individual elements would be challenging. Therefore, this research adopted thematic analysis to group the related propositions based on the theoretical background and the close similarity in addressing sustainability complexity, as summarised in Table 2. Although strong cross-thematic elements were unavoidable, the grounded theories aided in the clustering of the propositions into their respective themes. The clusters were based on the reviewed literature and the most repetitive elements across the reviewed literature.

3. Results

The research findings indicate that CS is a complex undertaking that cannot be explained by a single method and involves a transdisciplinary approach exhibiting strong interdependencies across stakeholders. Pedersen and Andersen (2015) conducted a global-expert study for the fashion industry sustainability and reported that the strong interdependencies across the value chain forms the basis for barriers to its sustainability (Pedersen & Andersen, 2015; Pedersen et al., 2019). Therefore, the totality of CS cannot be viewed from a single perspective but rather a holistic approach (Lozano, 2012, 2014, 2015; Lozano & Barreiro-Gen, 2023; Lozano et al., 2015, 2016; Moursellas et al., 2024; Blanco-Portela et al., 2017). To solve this complexity, a transformative approach that embraces holism to include all actors is imperative, as CS is diverse and dynamic.

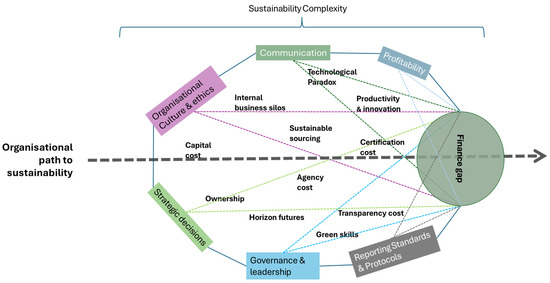

Singh and Rahman (2021) in their work on how CS can be integrated into the SDGs shows that there exists no single business that is untouched by the challenges raised by SDGs (Singh & Rahman, 2021). Since SDGs are highly connected, and no single pillar can address SDGs, CS must be viewed as diverse and dynamic, meaning they can only be understood from a holistic perspective (Moursellas et al., 2024; Mahajan et al., 2023). This complexity explains the inconsistent translation of sustainable strategies into tangible actions across different organisations. This has been blurred further by sustainability cynical tactics in a fast-growing business environment (Porter et al., 2016; Carmichael, 2022). Vardari et al. (2020) explains the intricacies of CS cutting across an adaptation of economic, environmental, and social factors to the activities and mechanisms of corporate decision making coupled with the principles of governance and risk management (Vardari et al., 2020). A broad and complex undertaking which cannot be solved by a one-size-fits-all approach, as elaborated in Figure 1. Depending on the size, nature, and specificity of each organisation, a strategic approach to address CS to promote its success is critical. Moursellas et al. (2024) explains how SMEs experience different barriers that cannot be compared to large organisations and must be viewed differently from larger organisations (Moursellas et al., 2024).

Figure 1.

The complexities of an organisation’s journey towards sustainability and the barriers which may hinder progression. Source: Authors’ elaboration based on the literature.

The organisational capacity includes a broader social and environmental aspects, whilst advancing the triple-bottom-line approach to ensure a balance between people, planet, and profit (Aragón & Macedo, 2010; Aguilera et al., 2021; Bowen & Aragon-Correa, 2014). Dorado et al. (2022) evaluated 85 Spanish manufacturing companies’ environmental and corporate policies and found out those companies that had environmental management systems in place had a positive effect on sustainability. Similar barriers are reported by Chowdhury et al. (2023) in evaluating options for mitigating barriers to supply-chain sustainability. However, they recommended the need for managers to show new leadership approaches by exploring advancing stakeholder engagement on the new front.

Koster et al. (2019) evaluates how NGOs are changing their advocacy role to lead in sustainability implementation and reported that cognitive and institutional norms are main barriers. To understand how such engagements can be undertaken, Barber et al. (2014) evaluated how sustainability can be integrated into the business curricula and emphasised that institutional organisations and business must come together and rethink their roles in sustainability, as sustainability can be firmly entrenched within the existing structures without incurring further costs. However, this must be approached with caution to ensure individual interests do not override the organisational goals.

Conflicting and proliferating regulations further amplify this issue, presenting sustainability as a barrier to organisational performance (Filho et al., 2022; Setyaningsih et al., 2024; Lozano et al., 2016; Siew, 2015). Moreover, the legal environment within which organisations operate necessitates a broader perspective than profit making, requiring active participation in society. However, the lack of coherent policy in integrating organisations into the society elaborates on the complexity of sustainability. Altomonte et al. (2014) evaluated the sustainability of the built-up environment highlights knowledge and regulatory standards as the main barriers to the future of the sector. Historically, there are new developments cutting across from corporate social responsibility (CSR) to the environmental social governance (ESG) (George et al., 2016; Tsang et al., 2023; Kuppig et al., 2016; Pedersen et al., 2019; Bogers et al., 2022; Haas, 2017) to ensure the organisations gain legitimacy and prevent legal sanctions. Bebic et al. (2024) reported legal complexities, standardisation gaps, and rapid implementation pressures as the main barriers to ESG implantation across mechanical and plant engineering companies in German.

Profit making is a major driver for corporate organisations (Pajunen et al., 2016; Milne, 2002). From a broader perspective, sustainability is viewed as a factor that affects the financial position of organisations, thus either increasing or decreasing the financial gap (Chowdhury et al., 2023; Setyaningsih et al., 2024; Apolloni et al., 2024; Christie, 2021), as presented in Figure 1. If not balanced, organisations are blurred by profit maximisation trying to reduce associated costs, resulting in a scenario that can be viewed as a “profit vision tunnel” which is depicted by the finance gap in Figure 1. Any sustainability measure introduces an extra cost to the organisation, triggering managers to only focus on how to ensure that profit is not affected “profit vision tunnel”, limiting its ability to maximise sustainability success factors in both short-term and long-term plans (Apolloni et al., 2024; Christie, 2021). This problem can be solved by broadening the scope of evaluation from the triple-bottom-line model and integrating SDGs to ensure organisational sustainability is anchored on a framework that all incorporates all elements of CS into business operations (Singh & Rahman, 2021). Pajunen et al. (2016) evaluated the value of sustainability from the industry perspective and reported that well-integrated and responsible environmental measures tend to improve financial performance.

From a methodological point of view, CS performance evaluation is a complex undertaking, attributed to the convergence of social, environmental, and economic matters (Montiel & Delgado-Ceballos, 2014). Although these aspects could be evaluated separately, the complexity of the convergence has led to divergent views from researchers, academicians, and policymakers in delivering standalone methodologies and approaches to quantify corporate governance (Setyaningsih et al., 2024; Y. Li et al., 2024; Lozano et al., 2016; de Villiers et al., 2022). The complexity of methodologies to quantify corporate sustainability corelates to the lack of ability, stemming from an inability of human resources to adequately develop and implement a shared green vision for the company (Moursellas et al., 2024; Khatter et al., 2021; Apolloni et al., 2024). This is further aggravated by a lack of green skills that could advance corporate sustainability (Fuchs, 2024).

Technological advancement coupled with wider adoption and application is gaining momentum across CS (Battaglia et al., 2016; Karaszewski et al., 2021). However, a lack of green skills and methodological frameworks has led to the development of “Blackbox AI tools” to define the meaning of sustainability for organisations (Kücükgül et al., 2022; Pedersen & Andersen, 2015; Siew, 2015). Embracing the use and application of blockchain technology has the potential to answer these needs (Luzzani et al., 2021; Karaszewski et al., 2021). Pedersen and Andersen (2015) emphasise the significance of rethinking existing skills and knowledge across the fashion industry to do away with sustainability draggers for the sector. They recommend a partnership between the academia and the industry to design a skillset aimed at advancing sustainability while addressing the knowledge gaps. A lack of partnership is more likely to widen the gap, leading to marginalisation of the academia (Barber et al., 2014; Pedersen & Andersen, 2015). The impact of marginalisation can be associated with delayed market entry for early careers, as the market bias leads to a focus only on experienced workers where, in most instances, the new green skills might not be available to them (Wierenga et al., 2024). Similar findings are reported by Khatter et al. (2021) in the case of Australian hotels, where lack of knowledge and skills in sustainability are a major barrier.

Technological threats are reducing sustainability performance due to the complexity of the reported data and information (Basit et al., 2024; Apolloni et al., 2024; Oguntegbe et al., 2022). Although there is no clear evidence, there exists a mixed relationship between technology and sustainability creating a wider disparity with only economic gains being advanced at the expense of sustainability (Liu et al., 2023; Luzzani et al., 2021). Considering this, the research identified six clusters of barriers which are further discussed in Figure 1 above.

3.1. Finance Gap

A complex relationship exists between profitability and corporate sustainability as there is no clear evidence as to whether its positive or negative (Moursellas et al., 2024; Benvenuto et al., 2023). Managers of profitable organisations tend to use sustainability objectives for personal gains such as ensuring their positions and increasing their level of renumerations (Khatter et al., 2021; Frias-Aceituno et al., 2014). In contrast, when organisations are incurring losses, and the managers are required by law to report sustainability progress, profitability becomes a barrier to sustainability (Moursellas et al., 2024; Larrinaga-González, 2010). In such instances, profitability is viewed as an indicator of investment quality, rather than its impact on the environment (Oyedijo et al., 2024; Y. Li et al., 2024). This necessitates striking a balance between profitability and sustainability, as most organisations will only publish their progress whenever they have positive returns, as opposed to when they are making losses (de Villiers et al., 2022).

Contrary to the political cost theory, where organisations ought to voluntarily declare sustainability progress, managers tend to lean towards resource availability to respond to market forces, depending on whether they operate in a bank or market-based economy (Rosati & Faria, 2019; Rodriguez-Fernandez, 2016; Y. Li et al., 2024). From a growth perspective, organisations with greater growth opportunities will invest more resources into sustainability. Moursellas et al. (2024) highlighted the lack of research and development as a major barrier to SMEs, which can be associated with their small capital, which limits them from investing in R&D. However, this approach is majorly driven by the desire to reduce costs while limiting information asymmetry (Christie, 2021). If not well balanced, sustainability can adversely influence shareholder wealth and thus the company value or profitability, widening or narrowing the finance gap (Khatter et al., 2021; Brown et al., 2006).

Other accrued costs which negatively impact profitability include, but are not limited to, the ability to pay highly skilled sustainability experts and consequently punitive government fines due to a lack of compliance (Moursellas et al., 2024; Nikula, 2022; S. Li et al., 2021; Y. Li et al., 2024; Christie, 2021). Similarly, this can be viewed from the lens of managerial opportunism, which has an adverse effect on the financial performance when advancing social and environmental activities (Y. Li et al., 2024). A challenge further aggravated when shareholders decide to engage in individual benefits at the expense of an organisation (Jian et al., 2024). Y. Li et al. (2024) evaluated the effect of environmental policy on corporate sustainability and found that stringent regional assessments coupled with high investment costs coupled with low-quality environmental disclosure information were main barriers to listed companies’ sustainability (Y. Li et al., 2024). This necessitated the need for transparency to ensure companies do not consider sustainability as a hidden cost, thus increasing their willingness to invest in sustainability.

Unfortunately, there exist mixed relationships between sustainability and organisational profitability (Pajunen et al., 2016; Hubbard, 2009). Capital costs associated with membership, compliance, and associated efforts are seen as an impediment to sustainability implementation (Gregory et al., 2014). To mitigate the risks associated with these costs, entities tend to deviate towards low-risk profiles to attract investors. This mostly common involves “sin”, i.e., industries with a high carbon risk, where an extra cost must be incurred to ensure such industries remain competitive. The justification process for all the sustainability activities in a firm attracts an auditing process which increases the operational costs. The additional cost coupled with resistance to change within the organisation is more likely to result in hidden costs, negatively impacting the organisation portfolio (Gregory et al., 2014; Ng & Rezaee, 2015).

To overcome associated costs, most organisations are exploring transparency for sustainability. To legitimise their actions and commitment towards sustainability, organisations are investing considerable resources in producing reports to increase organisations’ trust levels (Xia et al., 2023). However, transparency reports face criticism regarding their legitimacy, the methodologies used, and the uncertainty as to whether such organisations are genuine or if it is a tactic against greenwashing claims (Xia et al., 2023; Khosroshahi et al., 2021). Therefore, reducing any undertaking that would broaden the finance gap while narrowing the profit margin has a higher chance of limiting organisational performance within the profit-tunnel scope.

3.2. Sustainability Reporting Standards and Protocols

Organisational sustainability reporting is a lengthy process involving a great deal of information (Benvenuto et al., 2023; Paridhi & Ritika, 2024). In line with the voluntary disclosure theory, organisations may share information voluntarily with the aim of reducing information asymmetries (Benvenuto et al., 2023). However, in instances where the cost outweighs the benefits, this process increases the capital cost, becoming a barrier to sustainability. Paridhi and Ritika (2024) highlight the resource constraints coupled with the intricate nature of reporting metrics measurements across sustainability as major barriers. Similar findings are reported by Ceschin (2013) in an evaluation of the critical factors for implementing and diffusing innovations for six companies as part of sustainability, where he highlights regulatory barriers. He reported that most companies do not internally reward sustainability, which further creates a barrier when the government introduces policies aimed at attracting corporate sustainability. In exploring the role of public policy in overcoming barriers to systems innovation, O. Mont and Lindhqvist (2003) highlighted how a well-structured regulatory framework can reduce high upfront costs, increasing awareness across the organisation and thus reducing regulatory uncertainties which are barriers to organisational sustainability.

The cost associated with reporting limits those companies with less resources, but since they are legally bound depending on their jurisdiction, these organisations tend to provide ambiguous and unverifiable reports to demonstrate environmental compliance (Milne, 2002). Tilt et al. (2021), in assessing the state of business sustainability reporting in sub-Saharan Africa, highlights how the voluntary reporting frameworks can significantly create a barrier in embedding social norms coupled to the changes in the regulatory requirements. This is a practice that goes against signal theory, which emphasises the importance of robust information in reducing asymmetries while creating value for all, as grounded in stakeholder theory (Mahajan et al., 2023). This practice infringes assurance and transparency principles in sustainability (Tang & Higgins, 2022; Xia et al., 2023; Khosroshahi et al., 2021; Datt et al., 2022). In view of the political-cost-theory paradigm, organisations will only provide information to reduce associated political costs and benefits from state subsidies (de Villiers et al., 2022; Roe, 1991; Gray, 2010). This creates unfair ground for sustainability to be implemented by organisations.

The voluntary nature of the reporting process comes at increased cost to the organisation (Larrinaga-González, 2010). The resource-dependence theory suggests that organisations often opt for the cheapest option on the market, resulting in inconsistencies in reporting procedures (Dickins & Urtel, 2023). This can be related to why regulators are opting for quality-assurance services from third parties to promote transparency, albeit at an increased cost to verify and validate sustainability reports, creating an impartial ground and thus illegitimatising the trust levels (de Villiers et al., 2022; Datt et al., 2022). Similarly, the wide variety of standards makes it difficult for experts and companies to work together to come up with interoperable standards. A situation further compounded by the financial need and human workforce required to achieve interoperability of standards from the existing regulations (de Villiers et al., 2022).

The complexity associated with reporting standards is compounded by auditing and reporting parties trying their best to increase assurance (Gray, 2010). This is a disruptive process and is driving a change from technological and strategic operations to ethically guided processes. However, creating the balance between practical and ethical issues of reporting amidst fast-changing technology makes it harder for organisations and managers to create an illusion when reporting on sustainability. Similarly, baseline data are also hard to obtain for many, when we are baselining, if it presently does not consider action already engaged in.

The adoption of “one size-fits all” for different companies is a barrier (Moursellas et al., 2024; Setyaningsih et al., 2024). Diversity in data and reporting systems increases the cost streams from the initial investment, leading to uncertainty on a return on investment. This uncertainty gap is more likely to overwhelm investors and stakeholders across organisations. Therefore, future reporting standards are likely to emerge because of corporate and performance deviation from the financial auditing based on an ethically driven holistic approach with the potential to capture sustainability reporting (Dickins & Urtel, 2023).

Similarly, there has been increased adoption of rating systems by companies to justify their commitment to sustainability reporting in the market (Aristizábal-Monsalve et al., 2022; Bernardi et al., 2017). However, there exists a gap in transparency in these rating systems (Basit et al., 2024). Investors require detailed information on these ratings, and the time spent on responding to these requests and delivering reports is most likely to limit the implementation of organisational strategies and goals (Geysi, 2024; Tang & Higgins, 2022; Xia et al., 2023; Khosroshahi et al., 2021). Despite a high demand for transparency, data breaches, a lack of trust, and poor network security are key barriers identified across SMEs’ sustainable business practices (Basit et al., 2024).

3.3. Organisational Governance and Leadership

Companies operating within a fragile and dynamic business environment, are forced to rethink leadership in response to change. The fast-evolving pace within CS can be attributed to the replacement of corporate social responsibility (CSR) with environmental social governance (ESG) (Tsang et al., 2023; Ng & Rezaee, 2015). Similarly, it explains the “G” in ESG and its fundamental role in embedding, monitoring, and evaluating an organisation’s progress. Despite the continued emphasis on the importance of corporate governance in sustainability, many organisations have been reluctant due to the complexity of sustainability and the dynamics involved in implementation, reporting, monitoring, and progressing improvement (Freund & Hernandez-Maskivker, 2021; Ng & Rezaee, 2015). Cognitive barriers such as the culture of company leadership may significantly influence how they view internal and external problems and thus decision making (Abatecola & Cristofaro, 2020; Fraser et al., 2022; Matoh et al., 2024). The situation worsens when organisational leadership does not guard stakeholders’ interests from opportunistic behaviours (Lopes de Sousa Jabbour et al., 2020). Fraser et al. (2022), while evaluating how local procurement was a proxy for shared value and sustainable development in the mining sector in Mongolia, reported that the community viewed the lack of support by the international company (poor CSR) as a barrier to sustainable development (Fraser et al., 2022). This case can be applied to any organisation to ensure that stronger CSR and community engagement play a significant role in its sustainability vision (Jian et al., 2024).

To ensure co-existence with the society, organisations are advocating for strategic and sustainable corporate governance to overcome opportunistic behaviours and leadership challenges (Kong, 2013; Matoh et al., 2024; Jian et al., 2024). Zhao et al. (2022) reported support from the top management as the main driver for decarbonisation across the UK plastics supply chain and, therefore, a lack of support is a major barrier to sustainability (Zhao et al., 2022). Kong (2013) argues that if not well balanced, sustainability in the context of corporate governance is more likely to replace the role of minority shareholders (Ikram et al., 2020). This is more likely to disrupt the operations of an organisation, thus hindering value creation, and may create a major challenge to corporate governance on how to minimise conflicts (Kücükgül et al., 2022; Gregory et al., 2014).

Corporate governance actors tend to raise conflicting goals, with the majority focusing on the risk-averse options, ensuring they can avoid pursuing environmentally sustainable outcomes (Jian et al., 2024; Gregory et al., 2014; Ng & Rezaee, 2015). Such arguments are related to high investment costs in upgrading the existing infrastructure and training the existing workforce. Ng and Rezaee (2015) evaluated the impact of CSR on capital cost and reported that social sustainability is negatively associated with the cost of capital. Additionally, power conflicts on how to monitor large shareholders and the board of directors can negatively affect sustainability goals (de Villiers et al., 2011).

Delving further into the nature of ownership, research indicates that the nature of ownership determines sustainability inclination level (Matoh et al., 2024; Jian et al., 2024). Ownership types influence organisational environmental outcomes in varying degrees, from family-owned firms to state and institutional investors (Jian et al., 2024; Richards et al., 2017). Family firms are more likely to invest in initiatives—taking on an environmental strategy only if there is family commitment and long-term orientation (Calza et al., 2016). On the other hand, state-owned companies have a greater capacity to absorb externalities and can implement sustainability in line with the state commitment (Calza et al., 2016). The only challenge arises when the state must fulfil the polluter-pays principle, where these organisations do not commit to the levies charged (Khan, 2015). This becomes a barrier on how to increase commitment and disclose enforcement commitment, unless it is driven solely by the state. It also raises the question as to how the organisations with boards manage this complexity.

Companies with boards of directors have the tendency to strategically set environmental sustainability to mitigate any issue that could lead the organisation into physical, regulatory, and reputational risk (Matoh et al., 2024; Aguilera et al., 2021). Amran et al. (2014) explained how larger boards tend to have a stronger environmental commitment, such as stronger networking and legitimacy (Amran et al., 2014). However, this can be limited by Chief Executive Officer (CEO) duality, which further puts the board into a dilemma on how to stick to the organisational goals and financial gains in the short term at the expense of environmental initiatives (Jian et al., 2024). Such controversies have led to the questioning of the credibility of the directors’ background in terms of environmental credentials. Research has shown that boards with a larger composition of women demonstrate a better performance than their counterparts. This has been argued from the perspective that women in the upper echelons and agency-based theory perspectives exhibit greater traits due to their passion for environmental and social issues and monitoring capabilities (Abatecola & Cristofaro, 2020; Christie, 2021).

To overcome the drawbacks of CEO duality, some organisations are opting for the recruitment of Chief Sustainability Officers (CSOs) (Jian et al., 2024; Aguilera et al., 2021). Research into the influence of Chief Financial Officers (CFOs) has been mixed, with some scholars arguing that the recruitment of CSOs lead to better sustainability performance, while others have criticised the step as only a way of greenwashing and symbolism rather than substantive environmental protection, especially in instances where earning management is dominant (Jian et al., 2024). Instances where CSOs do not meet the public expectations are more likely to be a risk to environmental sustainability and thus a barrier from a governance perspective (Jian et al., 2024; Peters et al., 2019; Fu et al., 2020). However, these challenges can be overcome by ensuring that employees play a critical role when choosing and voting for their board. Involving employees in organisational decision making has the potential to ensure sustainability involves a bottom-up approach rather than top-down model, where it is seen as an obligation (Thomas & Doerflinger, 2020). Thus, labour environmentalism could play a substantial role in shaping future organisational sustainability, where employees drive the agenda within their organisation. However, to realise this, a shift in the skills for green human-resource management within a company can help ensure that employees are equipped with green skills (De Stefano et al., 2018).

3.4. Strategic Decisions Between Short-Term Profit and Sustainability

Corporate governance effects on sustainability cannot be measured from a financial standpoint alone (Pajunen et al., 2016; Friske et al., 2023; Gregory et al., 2014; Jensen, 2001). This is a fundamental theory in corporate sustainability identification and the quantification of the key initiatives that can champion organisational sustainability. A plethora of guidelines, standards, protocols, and methodologies exist in the market, making it difficult for any organisation to choose the right initiative (Bebic et al., 2024; Lozano et al., 2016; de Villiers et al., 2022).

In instances where performance measurements are not clear, they are more likely to mislead organisational practices and thus bias the choice of sustainability indicators. This further complicates the accuracy of what is reported (Geysi, 2024). The use of proxy data in reporting compounds the problem (Siew, 2015; de Villiers et al., 2022). Therefore, desired and selected indicators to measure corporate sustainability should be flexible and change with environment and time, deterring the use of proxy data and information (Moursellas et al., 2024). To achieve data accuracy, there is a need for an iterative and ongoing process involving all the actors across the entire organisation (Lopes de Sousa Jabbour et al., 2020). This includes a fact-based procedure that relies on a robust methodology and not a plethora of guidelines in the current context of organisational sustainability (Belal et al., 2024; Aboramadan et al., 2020). This can also include anchoring future methodologies on the principle of simplicity to address the complexity surrounding sustainability (Siew, 2015). Although this must not transcend beyond the comprehensive approach of the entire undertaking.

The complexity of this approach has resulted in managers finding themselves in a difficult position as to whether to pursue short-term goals or profitability, especially those in charge of SMEs (Moursellas et al., 2024; Basit et al., 2024; Bocken & Geradts, 2020). Mostly, managers tend to forego long-term goals for profitability, presenting a dilemma on how to balance sustainability in favour of short-term goals (Siew, 2015). However, whether an SME or a large corporation, sustainability is imperative as a competitive advantage in a fast-changing business environment (Bebic et al., 2024; Basit et al., 2024). Therefore, it must be considered from a strategic decision management perspective to ensure future growth is aligned with sustainability to increase its willingness to take risks (Y. Li et al., 2024).

3.5. Communication

The narrative “information is power” is contextual in corporate sustainability. Ikram et al. (2020), in evaluating the social dimensions of corporate sustainability, highlights how communication is key in organisational sustainability (Ikram et al., 2020). They highlight how clear communication coupled with transparency acts as a robust tool in promoting shared organisation vision. However, the lack of it can be an impediment to the implementation of sustainability and winning the trust of the public (Geysi, 2024; De Vries et al., 2015). Communication as a cultural practice for any organisation must be viewed as a strong tool to advance organisational goals (Filho et al., 2022). The concept of shareholder value maximisation has been held for a longer period in an organisational setting, which is in contrast with modern-day societal needs and expectations (Gregory et al., 2014; Fraser et al., 2022; Ludolf et al., 2017). When organisations fail to transition from this traditional approach to communication, they are more likely to face self-inflicted ruin and damage due to public alienation because of distrust in corporate governance and sustainability systems (Xia et al., 2023; Khosroshahi et al., 2021; Sun et al., 2023).

Poor communication leads to increased views by the public that organisations are increasing shareholder value maximisation (Bocken & Geradts, 2020; Geysi, 2024). This has been destructive to organisations and associated with executives discounting the importance of non-shareholders’ concerns and costs (Khatter et al., 2021; Kong, 2013). A decision that, when ignored, leads to organisational management abandoning the broader mix of participants’ needs within the organisation, claiming that their opinions can only be counted when they are commensurate to contributions (Abatecola & Cristofaro, 2020). This mode of communication has widened the public distrust due to shareholder capitalism derailing sustainability concerns (Carmichael, 2022; Khosroshahi et al., 2021).

Communication around sustainability can be challenging, and navigating successfully is important for an organisation’s profile, reputation, and brand value (Gregory et al., 2014; Friske et al., 2023; Ludolf et al., 2017). Greenwashing has resulted in a lack of public trust due to high-profile cases like Volkswagen (VW) emissions falsification, making society aware of deception (Siano et al., 2017). Greenwashing aims at making false, exaggerated, or misleading claims about a product or service’s environmental benefits, usually to appeal to environmentally conscious consumers or meet regulations. However, this backlash can lead to some organisations hiding their successes due to fear of backlash, especially if they do not have the data/evidence or have not addressed their entire supply chain (Basit et al., 2024). This includes high-profile cases such as H&M, which serve to warn organisations against claiming success too confidently (Y. Li et al., 2024). If an organisation addresses their entire supply chain to achieve societal ‘kudos’ for sustainability, it can prove difficult to discuss and develop an evolving, step-by-step sustainability programme, without a safe space for open conversation and reward for the steps one has taken (Basit et al., 2024). This means the action and reward benefits of sustainability are not aligned, and this becomes a barrier if action is taken and the ‘kudos’ not given to the corporation unless they are performing perfectly in all areas. Understanding and compassion within society towards corporations and their communications is key (Kaner, 2021).

These moral disengagements have further been accelerated by increased public activism against corporate organisations lacking active involvement in environmental sustainability (Bux et al., 2020). Increased attention from the public and reduced engagement from corporate organisations has been considered a form of moral disengagement which widens public distrust (Geysi, 2024). This has led to the perception of cronyism by the public, that organisations are colluding with the regulators to support greenwashing in different forms (Lozano, 2015; Khatter et al., 2021; Shahnazi et al., 2024). Research has shown that there is a negative relationship between capital cronyism and green innovation investment, which is an index for sustainability (Marie et al., 2024).

3.6. Organisational Culture and Ethics

Organisational ideas, customs, regulations, habits, traditions, and social behaviour define culture (Ceschin, 2013; Ceschin & Vezzoli, 2010). Organisational culture transcends beyond an organisation’s boundaries (Bux et al., 2020; Ikram et al., 2020; Aboramadan et al., 2020). Therefore, understanding organisational culture and how it can be an impediment towards sustainability is paramount.

A high level of cooperation is required for accepting short-term loss for long-term societal gain (Matoh et al., 2024; Murray et al., 2010). A micro-level culture of cooperation is required within an organisation to understand group behaviours. The larger the corporation, the more difficult it becomes for group gain to benefit the individual, and the individual may select selfish opportunistic behaviours (Cordes et al., 2010).

From a meso-lens and institutional economics perspective, culture determines humans’ perceptions and forms behaviours (Matoh et al., 2024; Aboramadan et al., 2020; Linnenluecke & Griffiths, 2010). The rate of acceptance for sustainable practices within any country is subject to values and norms. Research has shown that national culture directly influences and indirectly affects investor protection (Luo et al., 2013). In the examination of a country’s impact on corporate carbon-disclosure propensity reported a significant association between masculinity, power, and uncertainty avoidance (Sun et al., 2023). Naeem and Neal (2012), in evaluating the Asian Pacific education-sector integration of sustainability reported that there was significant delay in integrating sustainability across the curriculum due to complex social cultural factors. Similar findings are reported by Lozano (2014) in an evaluation of how to design university courses to align with future sustainability.

At the organisational level, resistance to change business-as-usual approaches is the main barrier to implementing corporate sustainability (Pedersen & Andersen, 2015; Gardas et al., 2019; Pedersen et al., 2019; Gardas et al., 2018). This resistance cuts across the board from both employers and employees and leadership, significantly influencing the implementation of corporate sustainability (Wijethilake et al., 2023). Increased and progressive resistance has the potential to undermine corporate sustainability, as it shapes the leadership style and employees’ norms, which can cause a misalignment of the organisational objectives. Employee reluctance coupled with a lack of managerial support can be detrimental if embedded in organisational culture, where it presents a barrier to fostering a shared commitment to sustainability (Linnenluecke & Griffiths, 2010; Tsai, 2011).

The dilemma to align organisational values and actual behaviours is a major challenge to leaders especially when embedding sustainability into an organisational framework. Corporate leadership in this instance finds it challenging to front an entry point for sustainable practices in the day-to-day business practices, especially in cases where resistance to change is strongly embedded (Porter et al., 2016). Organisations where cultures are entrenched in short-term profit-making can find difficulties in embedding sustainability practices which are long term in terms of value creation. The resistance can be amplified further by employee scepticism based on experience where the organisation had portrayed divergent scenarios between rhetoric and actions in relation to implementing sustainability (Ludolf et al., 2017; Wijethilake et al., 2023).

The nature of leadership in any organisation plays a significant role in influencing and shaping culture. Ineffective leadership portrayed by a lack of environmental and sustainability commitments coupled with the exclusion of employees in organisational sustainability strategy development presents itself as an impediment. Thus, future leadership must embrace a culture that prioritises a holistic contribution from employees to ensure commitment by employees is key to sustainability (Siew, 2015; Linnenluecke & Griffiths, 2010; Bogale & Debela, 2024; Aggarwal & Agarwala, 2021). Transcending beyond communication is the hierarchy of leadership within an organisation. A closed hierarchy presents itself as a barrier to employee innovative culture. Leadership styles such as centralised decision making limits the adoptability of diverse perspectives which are essential in the implementation of corporate sustainability (Ludolf et al., 2017).

4. Discussion

Despite the fast-growing trend for CS, its implementation and adoption remain limited. This research contributes to the existing literature on challenges that face corporate organisations when implementing sustainability and how such barriers have resulted in the slow adoption and implementation of corporate sustainability. Combining both a systematic literature review and thematic analysis revealed several barriers which were further grouped into six main themes. These findings are in line with the findings by Ashrafi et al. (2019), who evaluated CS across the US and Canadian maritime sector and reported that despite the consideration of CS as essential for the sectors, the prevalent lack of sustainability competencies, high cost of implementing sustainability, and limited customer interests are major barriers to CS (Ashrafi et al., 2019).

A case study on CSR as one of the practices organisations have been implementing in their journey to sustainability has been reported by Bux et al. (2020). They evaluated the main barriers to CSR across the manufacturing industry and identified 15 barriers. They classified the barriers as a derivative of a lack of the will to know and the will to implement within the companies, further aggravated by inadequate policy and coupled with a lack of stakeholder awareness on their role in promoting CS (Ashrafi et al., 2019; Bux et al., 2020). Similar barriers were reported by Pedersen and Andersen across the Indian fashion industry, where rigidity to management change and complex regulatory frameworks were the main barriers (Ceschin, 2013).

From Figure 1, it is evident that organisational sustainability is a complex undertaking characterised by strong interdependencies across the reviewed themes. This is further supported by a wide number of theories with the same theme. Therefore, to realise increased corporate sustainability, all actors must be involved jointly. A practice that must transcend beyond an individual approach towards an integrated one in establishing linkages geared towards attaining a multiplier effect of value creation. Lozano (2014), in his vast research, highlights how innovativeness and creativity are enablers of corporate sustainability; however, these must be fronted by all actors to promote a win–win scenario (Lozano, 2014, 2015; Lozano & Barreiro-Gen, 2023).

Ceschin proposes the adoption and implementation of transitional management approach. He defines the approach as a combination of systemic instruments to create an environment for the transitioning arena (Ceschin, 2013). Such a system has a potential for establishing a protected environment for sustainability to thrive (George et al., 2016; Eccles et al., 2014). However, ensuring all management levels are well informed about the set decisions and visions is of significance. If not well implemented, management-control strategies can be agent of conflict across the management, with the cognitive barriers of middle and low-tier management considering initiatives as way of micromanaging their work and thus sabotaging sustainability (Battaglia et al., 2016).

CS is an iterative process as the needs of the stakeholders are constantly changing. Thus, it is imperative for organisations implementing a multifaceted approach to ensure whenever an aspect changes in relation to its sustainability journey, it swiftly changes with the contextual factors. Avinash and Rahman, in their work on how to integrate SC in SDGs, acknowledges that there exists a strong interconnectedness of the perceived goals and practices, and organisations ought to approach CS in a holistic manner to avoid bias (Singh & Rahman, 2021).

However, Battaglia et al. (2016), in assessing how management control influences sustainability, outlines the existence of nine barriers, which they categorise as either technical, organisational, or cognitive. They caution that management-control systems if not well implemented can supress sustainability (Battaglia et al., 2016). This is more likely to happen when the top management prioritises economic directions of organisation over its overall development.

Achieving a win–win scenario across a complex environment due to the interconnectedness nature calls for organisations to adopt adaptive and systemic approaches (Ceschin, 2013; Ceschin & Vezzoli, 2010). The vast majority of the reviewed literature has been on the specific aspect of barriers, but this research points out that system scanning for barrier identification is fundamental, as the inherent interdependencies across elements of success are strong. Although a wide number of studies have highlighted the significance of stakeholders, this research advocates for diversity to ensure complex issues are addressed from all perspectives (Singh & Rahman, 2021; Mahajan et al., 2023; Jensen, 2001; Wolf, 2014). Most importantly, in instances where adaptive policies and choices need to be implemented, a holistic approach to the changes must be embraced. This research emphasises the importance of systems thinking when implementing adaptative measures to address complexity in regard to organisational sustainability.

Secondly, the major limiting factor of the identified barriers has been highly associated with the organisation’s goal of profit making. De Stefano et al. (2018); De Vries et al. (2015); Haessler (2020) and Wang et al. (2024) discuss in broad depth how striking a balance between sustainability and profitability is a major challenge for organisations. Khatter et al. (2021) in evaluating barriers and drivers for the Australian hotel industry highlights financial challenges as a main barrier. They explain how attracting customers with hoteliers has the potential to create a bubble of sustainability, yet in reality it is a greenwashing mechanism (Khatter et al., 2021). This research advances their work by showing how sustainability is viewed as a factor that affects the financial position of organisations, thus either increasing or decreasing the financial gap, as presented in Figure 1. In many instances, organisations are blinded by profit maximisation and trying to reduce the associated costs, resulting in a scenario that can be viewed as a “profit vision tunnel”, as depicted by the finance gap in Figure 1. If an organisation is not locked into its sustainability journey, it is more likely to be trapped in the “profit vision tunnel”, limiting the ability to integrate other sustainability success factors in both short-term and long-term plans. Although De Vries et al. (2015), in their work on profit or sustainability, expounds on how to create a balance between the two, this research posits that most organisations are lured by profit maximisation, which further hinders diversity in terms of the factors to be considered when implementing corporate sustainability.

Equally, effectively promoting organisational sustainability begins with simplifying the ambiguity of the term to ensure all actors and stakeholders have the same understanding (Kafa et al., 2020). They explain how the use of multiple methodologies is a potential solution. Their work provides a framework of methodologies that could help organisations navigate organisational complexity in sustainability. This research advances their work by advocating for integrating systems thinking, shareholder engagement, and adaptive management after system scanning to implement holistic and flexible models and approaches to sustainability.

Fourthly, diversity across organisations accounts for the wide range of tools, methodologies, approaches and standards to quantify progress towards sustainability, a scenario that presents itself as a barrier to organisational sustainability. Lozano (2014), Rosati and Faria (2019), Free et al. (2024), Setyaningsih et al. (2024), Siew (2015), Larrinaga-González (2010) and Datt et al. (2022) present how the wide array of tools and methodologies are creating confusion. This research further shows how such diversity across methodological approaches and reporting standards, as well as data-collection and reporting systems, can be leveraged through the integration of technology in reporting frameworks to promote transparency, trust, and investor confidence. Assurance to organisations has been watered down by the widespread existence of tools and methodologies which, in most instances, are profit driven (Larrinaga-González, 2010). To solve such confusion and increase organisational assurance, this research underscores the importance of adopting lean communication strategies to promote trust, transparency, and investor confidence.

This research further underscores how the use of digital technologies such as blockchain to track and verify product and process information has the potential to combat greenwashing claims which have negatively impacted corporate sustainability. Existing studies point to technology, in general, as useful in closing the barrier gap (Filho et al., 2022; Bocken & Geradts, 2020; George et al., 2016; de Paiva Duarte, 2015; Wang et al., 2024). This research adds to this work by pointing out the future of blockchain technology, which holds the potential for data analytics in real time, providing policymakers and corporate leaders with the place-based projections and insights most sought after (Luzzani et al., 2021). However, realising the full potential of technology in CS must be addressed from a basic viewpoint. This is especially true at institutions of learning, where skill sets must be reconfigured to squarely incorporate sustainability skills. Lozano et al. (2015) evaluates how university courses should be redesigned and concludes that the existing skills have been geared towards hard technocentric skills, which are a barrier in the market. Therefore, industrial and academic actors must work together to ensure the required skills to advance CS are incorporated in the education system. Equally, at the organisational level, discrepancies exist, with very few companies that have institutionalised sustainability across all its cadres. In most of those institutionalised and incorporated organisations, it only exists at the managerial level (Lozano, 2012; Linnenluecke & Griffiths, 2010). Therefore, it is imperative for organisations to break the “black-box” approach to sustainability knowledge and skills, both within the organisation and across its external stakeholders.

However, the research further acknowledges that the world of technology is versatile and dynamic. To promote adaptability in such an environment, this research underscores the fundamentals of future-proofing sustainability, as envisioned in corporate governance as a result of well-orchestrated strategic decisions and foresight. Amran et al. (2014); Fu et al. (2020) and D’Amato and Korhonen (2021) elaborated on how organisations can leverage corporate foresight to promote sustainability. This research highlights how future tactics must adopt adaptive management systems and leadership techniques that transcend beyond profit orientation to strike a balance between profit maximisation and sustainability. Equally, such measures ensure that unforeseen risks, which can arise when implementing sustainability, are factored in to ensure organisations build better decision-making frameworks, while fostering innovation and building long-term resilience. This research further improves the existing literature by highlighting how blending strategic foresight with lean communication and technological advancement has the potential to close the finance gap, which is the main barrier to organisational sustainability.

This also involves appreciating the fact that any systematic review is an iterative process and has its own limitations, in the sense that there is lack of clarity in determining alternatives to the selected reviewed literature. From a methodological perspective, only articles published in English were reviewed, and the authors acknowledge that there could be more work published in other languages. Equally, the lack of real-time interviews with organisations and observations over a certain period on how the said barriers are impacting organisations remains another grey area for future research. Additionally, the applied search protocol was biased, as it was based on the authors’ areas of expertise. Future research can include testing each of the identified barriers independently on organisational performance over a given period under different policy discourse. Another area to explore in the future research is how corporate sustainability addresses the SDGs. This was an area that was not explored in this article.

Whereas the findings present an elaborate picture of barriers to corporate sustainability, an empirical analysis is needed to understand the perceived value of each group (theme) of the identified barriers. Such an analysis could be conducted across organisations of different clusters in terms of size and geographical location to determine how each barrier affects the organisational sustainability path. Equally, from a policy perspective, other research can examine how emerging policies in addressing sustainability are addressing these barriers.

5. Conclusions

Corporate sustainability enables organisations to address the challenges of today without compromising the ability of future organisations to meet their goals. However, despite increased efforts to align organisations with sustainable development goals to implement sustainability, successful implementation has been slower than expected. For this reason, this study aimed to identify barriers from the literature that are hindering CS. This study identified barriers from previous studies and contextualised them to the organisational setup. To achieve this, we conducted a systematic literature review and thematic analysis to group the identified list of barriers to common clusters. The results identified a total number of 90 unique barriers and grouped them into six clusters. This research is subject to limitations, as it relied on previous studies. The majority of the previous studies either reviewed the literature or involved a case study for a specific sector. Future research can go the extra mile to combine case studies from several sectors with interviews from both the consumer and supplier side to ensure that all aspects of the stakeholders’ concerns are addressed. Barrier identification alone is not enough if the full potential of CS is to be realised. Since the main goal of the study was the identification of barriers, future research could explore the mechanisms through which these barriers can be addressed, as they have been shallowly discussed in this research. Equally, as today’s world is highly dynamic, evaluating the impacts of policy changes and developments on these barriers and how policymakers can effectively address these barriers to promote CS is necessary to establish sustainable future entities.

Author Contributions

Conceptualization, J.P.-T. and K.M.; methodology, K.M. and M.S.; validation J.P.-T., K.M. and J.C.; formal analysis, J.P.-T., K.M., M.S. and J.C.; writing—original draft preparation, K.M.; writing—review and editing, J.P.-T., K.M., M.S. and J.C.; visualisation, J.C.; supervision, J.P.-T.; funding acquisition, J.P.-T. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

No new data were created and all materials mentioned have been referenced to the respective sources where necessary.

Acknowledgments

We sincerely acknowledge Barbara Carbon and the reviewers for their effort in critiquing and going through our work.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Abatecola, G., & Cristofaro, M. (2020). Hambrick and mason’s ‘upper echelons theory’: Evolution and open avenues. Journal of Management History, 26, 116–136. [Google Scholar] [CrossRef]

- Aboramadan, M., Albashiti, B., Alharazin, H., & Zaidoune, S. (2020). Organizational culture, innovation and performance: A study from a non-western context. Journal of Management Development, 39, 437–451. [Google Scholar] [CrossRef]

- Aggarwal, P., & Agarwala, T. (2021). Green organizational culture: An exploration of dimensions. Global Business Review. [Google Scholar] [CrossRef]

- Aguilera, R. V., Aragón-Correa, J. A., Marano, V., & Tashman, P. A. (2021). The corporate governance of environmental sustainability: A review and proposal for more integrated research. Journal of Management, 47, 1468–1497. [Google Scholar] [CrossRef]

- Altomonte, S., Rutherford, P., & Wilson, R. (2014). Mapping the way forward: Education for sustainability in architecture and urban design. Corporate Social Responsibility and Environmental Management, 21, 143–154. [Google Scholar] [CrossRef]

- Amran, A., Lee, S. P., & Devi, S. S. (2014). The influence of governance structure and strategic corporate social responsibility toward sustainability reporting quality. Business Strategy and the Environment, 23, 217–235. [Google Scholar] [CrossRef]

- Apolloni, M., Volgger, M., & Pforr, C. (2024). Analysis of accommodation providers’ carbon footprint in Australia: Motivations and challenges. International Journal of Contemporary Hospitality Management, 36, 1490–1511. [Google Scholar] [CrossRef]

- Aragón, A. O., & Macedo, J. C. G. (2010). A system ic theories of change’ approach for purposeful capacity development. IDS Bulletin, 41, 87–99. [Google Scholar] [CrossRef]

- Aristizábal-Monsalve, P., Vásquez-Hernández, A., & Botero, L. F. B. (2022). Perceptions on the processes of sustainable rating systems and their combined application with Lean construction. Journal of Building Engineering, 46, 103627. [Google Scholar] [CrossRef]

- Ashrafi, M., Acciaro, M., Walker, T. R., Magnan, G. M., & Adams, M. (2019). Corporate sustainability in Canadian and US maritime ports. Journal of Cleaner Production, 220, 386–397. [Google Scholar] [CrossRef]

- Ashrafi, M., Adams, M., Walker, T. R., & Magnan, G. (2018). How corporate social responsibility can be integrated into corporate sustainability: A theoretical review of their relationships. International Journal of Sustainable Development and World Ecology, 25, 671–681. [Google Scholar] [CrossRef]

- Barber, N. A., Wilson, F., Venkatachalam, V., Cleaves, S. M., & Garnham, J. (2014). Integrating sustainability into business curricula: University of New Hampshire case study. International Journal of Sustainability in Higher Education, 15, 473–493. [Google Scholar] [CrossRef]

- Basit, S. A., Gharleghi, B., Batool, K., Hassan, S. S., Jahanshahi, A. A., & Kliem, M. E. (2024). Review of enablers and barriers of sustainable business practices in SMEs. Journal of Economy and Technology, 2, 79–94. [Google Scholar] [CrossRef]

- Battaglia, M., Passetti, E., Bianchi, L., & Frey, M. (2016). Managing for integration: A longitudinal analysis of management control for sustainability. Journal of Cleaner Production, 136, 213–225. [Google Scholar] [CrossRef]

- Bebic, M., Badie, N. B., Tyll, L., & Srivastava, M. (2024). Exploring the barriers and drivers of ESG in the German Mittelstand: A qualitative analysis of mechanical and plant engineering companies. Corporate Social Responsibility and Environmental Management, 32, 2147–2170. [Google Scholar] [CrossRef]

- Belal, M. M., Shukla, V., & Balasubramanian, S. (2024). Greening the pharmaceutical supply chain. Business Strategy and the Environment, 34, 1917–1948. [Google Scholar] [CrossRef]

- Benvenuto, M., Aufiero, C., & Viola, C. (2023). A systematic literature review on the determinants of sustainability reporting systems. Heliyon, 9, e14893. [Google Scholar] [CrossRef]

- Bernardi, E., Carlucci, S., Cornaro, C., & Bohne, R. A. (2017). An analysis of the most adopted rating systems for assessing the environmental impact of buildings. Sustainability, 9(7), 1226. [Google Scholar] [CrossRef]

- Blanco-Portela, N., Benayas, J., Pertierra, L. R., & Lozano, R. (2017). Towards the integration of sustainability in Higher Eeducation Institutions: A review of drivers of and barriers to organisational change and their comparison against those found of companies. Journal of Cleaner Production, 166, 563–578. [Google Scholar] [CrossRef]

- Bocken, N. M. P., & Geradts, T. H. (2020). Barriers and drivers to sustainable business model innovation: Organization design and dynamic capabilities. Long Range Planning, 53, 101950. [Google Scholar] [CrossRef]

- Bogale, A. T., & Debela, K. L. (2024). Organizational culture: A systematic review. Cogent Business & Management, 11. [Google Scholar] [CrossRef]

- Bogers, M., Biermann, F., Kalfagianni, A., Kim, R. E., Treep, J., & de Vos, M. G. (2022). The impact of the Sustainable Development Goals on a network of 276 international organizations. Global Environmental Change, 76, 102567. [Google Scholar] [CrossRef]

- Bowen, F., & Aragon-Correa, J. A. (2014). Greenwashing in corporate environmentalism research and practice: The importance of what we say and do. Organization & Environment, 27, 107–112. [Google Scholar] [CrossRef]

- Broccardo, L., Vola, P., Zicari, A., & Alshibani, S. M. (2023). Contingency-based analysis of the drivers and obstacles to a successful sustainable business model: Seeking the uncaptured value. Technological Forecasting and Social Change, 191, 122513. [Google Scholar] [CrossRef]

- Brown, W. O., Helland, E., & Smith, J. K. (2006). Corporate philanthropic practices. Journal of Corporate Finance, 12, 855–877. [Google Scholar] [CrossRef]

- Bux, H., Zhang, Z., & Ahmad, N. (2020). Promoting sustainability through corporate social responsibility implementation in the manufacturing industry: An empirical analysis of barriers using the ISM-MICMAC approach. Corporate Social Responsibility and Environmental Management, 27(4), 1729–1748. [Google Scholar] [CrossRef]

- Calza, F., Profumo, G., & Tutore, I. (2016). Corporate ownership and environmental proactivity. Business Strategy and the Environment, 25, 369–389. [Google Scholar] [CrossRef]

- Carmichael, D. (2022). Sustainability assurance as greenwashing. [Online]. Available online: www.ssir.org (accessed on 22 October 2024).

- Carmo, C., Correia, I., Leite, J., & Carvalho, A. (2023). Towards the voluntary adoption of integrated reporting: Drivers, barriers, and practices. Administrative Sciences, 13, 148. [Google Scholar] [CrossRef]

- Ceschin, F. (2013). Critical factors for implementing and diffusing sustainable product-Service systems: Insights from innovation studies and companies’ experiences. Journal of Cleaner Production, 45, 74–88. [Google Scholar] [CrossRef]

- Ceschin, F., & Vezzoli, C. (2010). The role of public policy in stimulating radical environmental impact reduction in the automotive sector: The need to focus on product-service system innovation. International Journal of Automotive Technology and Management, 10, 321–341. [Google Scholar] [CrossRef]

- Chowdhury, M. M. H., Rahman, S., Quaddus, M. A., & Shi, Y. (2023). Strategies to mitigate barriers to supply chain sustainability: An apparel manufacturing case study. Journal of Business and Industrial Marketing, 38, 869–885. [Google Scholar] [CrossRef]

- Christie, A. (2021). The agency costs of sustainable capitalism. [Online]. Available online: https://perma.cc/G7V9-XC9N (accessed on 6 August 2024).

- Cordes, C., Richerson, P. J., & Schwesinger, G. (2010). How corporate cultures coevolve with the business environment: The case of firm growth crises and industry evolution. Journal of Economic Behavior & Organization, 76, 465–480. [Google Scholar] [CrossRef]

- D’Amato, D., & Korhonen, J. (2021). Integrating the green economy, circular economy and bioeconomy in a strategic sustainability framework. Ecological Economics, 188, 107143. [Google Scholar] [CrossRef]

- D’Amico, E., Coluccia, D., Fontana, S., & Solimene, S. (2016). Factors influencing corporate environmental disclosure. Business Strategy and the Environment, 25, 178–192. [Google Scholar] [CrossRef]